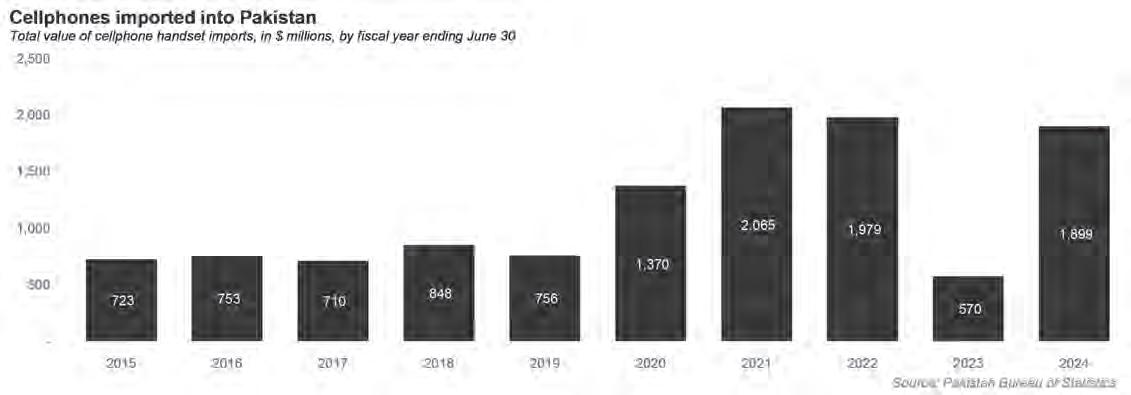

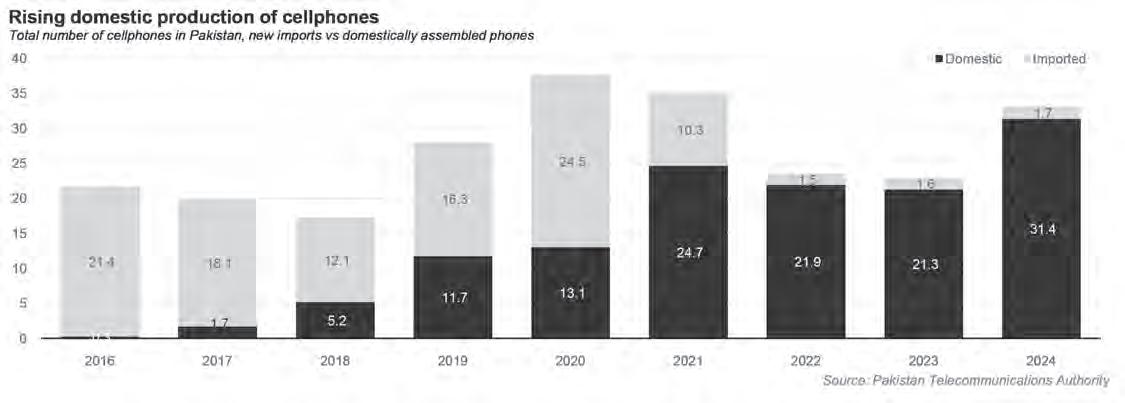

09 Pakistan’s locally assembled mobile phone production rose 47% in 2024

11 Meskay & Femtee to acquire Mandviwalla Mauser Plastic Industries for Rs207 million

12 Obituary: Tycoon, philanthropist, Imam — Aga Khan IV

18 Battle for KE’s ownership heats up

22 Kia’s new Sportage: When a small price gap tells a bigger story

24 A 5% rise in petrol consumption indicates stability in consumer spending

26 Fertilizer sales down 6% as weakness in farm sector continues 28 Pakistan’s steel industry is in crisis

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Pakistan’s locally assembled mobile phone production rose 47% in 2024

A combination of economic recovery, import curbs, and increased taxation on imported phones helped the domestic industry increase production

Profit Report

Pakistan’s domestic mobile phone assembly industry has surged to unprecedented levels, with local manufacturers producing 31.4 million units in 2024 — a 47% year-over-year increase — ac-

cording to a new report by Topline Securities analyst Sunny Kumar.

The findings, based on data from the Pakistan Telecommunication Authority (PTA), reveal how government import restrictions and tax policies have reshaped the market, reducing reliance on foreign devices and creating a booming homegrown manufacturing sector.

December 2024 marked a milestone, with local assembly hitting 2.95 million units — a 28% month-over-month jump. The fourth quarter saw 8.8 million units produced, up 67% from the previous quarter’s 5.3 million. This growth builds on a broader upward trend: compared to 2022, production has climbed 43% annually, driven by economic recovery,

tax advantages for locally assembled phones, and population growth.

Key drivers of this recovery include import restrictions. Imposed in 2023 to curb dollar outflow, these policies forced consumers and retailers to turn to locally assembled devices.

Then there was the tax policy meant to incentivize domestic phones. Imported phones face significantly higher tariffs (up to 30%) compared to locally assembled ones (10–15%), creating a pricing advantage for domestic products.

But perhaps most important is the economic recovery. Improved macroeconomic stability boosted consumer spending, particularly in urban centers.

Of the 31.4 million units assembled in 2024, 59% (18.64 million) were smartphones, while 41% (12.74 million) were 2G devices. This split reflects Pakistan’s evolving digital landscape, with increased smartphone adoption. Rising internet penetration (45% as of 2024) and affordable 4G devices from brands like Infinix and Tecno have expanded access.

Having said that, the persistent market share of 2G phones indicates that low-income users and rural areas still rely on basic phones due to cost and network coverage gaps.

Infinix led 2024 production with 3.98 million units, followed by Itel (3.64 million) and VGO Tel (3.37 million). Notably, Air Link Communication — the sole publicly listed assembler — manufactured Tecno (2.85 million units, +97% YoY) and Xiaomi (2.35 million units, +79% YoY), ranking fourth and sixth, respectively.

Air Link’s success underscores its strategic partnerships and economies of scale. The company’s shares trade at an FY25 price-toearnings ratio of 11.6x, with Topline Securities recommending a “buy” amid expectations of rising smartphone demand.

In 2024, locally assembled devices met 95% of Pakistan’s mobile demand—a dramatic shift from the 67% average between 2019 and

2023. This transformation stems from deliberate policy moves:

The government imposed escalating tariffs on imported phones while slashing taxes on locally manufactured devices. By 2023, imported smartphones faced a 30% regulatory duty, whereas locally produced units incurred only 10–15% taxes.

Then there are the industrial incentives. Manufacturers importing assembly components (e.g., screens, batteries) received duty waivers. Companies like Air Link secured rebates for exporting surplus units to Afghanistan and Central Asia. And the PTA mandated device registration in 2021, blocking non-compliant imports and funneling demand toward registered local assemblers.

Despite progress, the industry faces hurdles, not least of which is the fact that it is still dependent on component imports: 75% of parts (e.g., semiconductors, cameras) are still imported, exposing manufacturers to exchange rate risks. These came to the fore over the past two years when the rupee lost over half its value.

Some budget brands compromise on materials to keep prices low, harming consumer trust. And the industry still largely serves as assemblers for foreign brands, with Pakistani brands holding low market shares. Chinese giants like Transsion Holdings (Infinix, Tecno) dominate, leaving little room for Pakistani-owned brands.

However, analysts remain optimistic. Topline’s report projects smartphone sales to grow at a 22% CAGR through 2026, driven by youthful demographics and 5G rollout plans. Air Link’s expansion into high-margin accessories (e.g., chargers, wearables) could further bolster profitability.

Pakistan’s mobile assembly boom offers lessons for other sectors. By aligning tariffs, incentives, and regulations, the government nurtured a $1.5 billion industry that employs over 30,000 workers.

As Pakistan moves towards near-autarky in cellphone manufacturing, the handful of local players have engaged in behaviour that is already different from the automakers in one key way: they have begun asking for policies to incentivise exports, instead of merely being satisfied with creating an oligopoly to serve the tariff-protected domestic market.

The government appears to already be in discussions with industry representatives to offer as much as an 8% tax rebate on mobile phone exports to local manufacturers if they can achieve exports equal to their imports of parts and fully assembled phones within three years. It is unclear whether or not this policy will go into effect, though the aggressive export-oriented nature of the lobbying suggests a desire to be globally competitive, which is what an industry needs to do in order to have an impact on the domestic market.

Yet industry executives caution about getting too optimistic too quickly about exports. Air Link’s management, for instance, point out that only about 20% of the value of a cellphone can even be manufactured locally, since about 80% of the value of a smartphone consists of the LCD screen, the chips, and the motherboards, which are highly specialised products that only a handful of companies produce for every single user in the world. None of them are likely to locate production facilities in Pakistan any time in the foreseeable future.

But just because a significant portion of the value of a smartphone will continue to consist of imported components does not mean that they cannot become a meaningful generator of export earnings for the country. As the Air Link management pointed out in a briefing to analysts, that is precisely the model being followed by assemblers in Vietnam, who only assemble phones with the more complex parts continuing to be manufactured mainly in Taiwan, and yet phone assembly contributes meaningfully to Vietnam’s export totals.

And as complicated as the most valuable parts of cellphones are, laptops are even more complex, with much the same narrow supply chains involved in its highest value parts: semiconductors, LCD screens, motherboards, all precision manufactured in facilities that are so critical and so difficult to get right that the United States and China are effectively preparing for war over who gets to control those technologies.

Laptop assembly has not yet begun in Pakistan in a significant way just yet, and even cellphone assembly is quite new. It is way too early to say whether or not this is the beginnings of a large scale industrialisation of Pakistan that would include electronics manufacturing, but we do know what variables to watch out for in order to know whether or not we are headed in that direction.

If the domestic assemblers are able to be-

gin exporting a substantial proportion of their production capacity within the next five years or so, it is likely that that the tariff protections will prove to be a truly temporary measure that helped an infant industry get on its feet and eventually become globally competitive on the strength of its own product quality.

If that does not happen, expect to live with terrible cellphone sets – or very expensive imported ones – for the next 60 years. n

Meskay & Femtee to acquire Mandviwalla Mauser Plastic Industries for Rs207 million

One of Pakistan’s largest rice exporters set to buy a struggling publicly listed plastics manufacturing plant

Profit Report

For less than the price of a house in DHA Karachi, one of Pakistan’s largest rice and agricultural commodity trading companies is about to acquire a publicly listed plastic manufacturing company.

Meskay & Femtee Trading Company (Pvt) Ltd has announced a public offer to acquire up to 74.41% of Mandviwalla Mauser Plastic Industries Limited for approximately Rs207 million. The acquisition is set to take place through a combination of a share purchase agreement and a public tender offer.

According to the public announcement, Meskay & Femtee intends to purchase 21,391,485 ordinary shares, representing 74.41% of the issued share capital of Mandviwalla Mauser, at a price of Rs5.0534 per share. This initial acquisition will be executed through a share purchase agreement with Mr. Azeem H. Mandviwalla, the current majority shareholder.

In addition to the share purchase agreement, Meskay & Femtee is extending a public offer to acquire the remaining 25.59% of shares from minority shareholders at a price of Rs13.47 per share. This offer will remain open for acceptance from March 26, 2025, to April 1, 2025.

The acquisition is being managed by Intermarket Securities Limited, which has confirmed the acquirer's capability to implement the public offer in accordance with regulatory requirements. Meskay & Femtee has provided a bank guarantee from Habib Metropolitan Bank Limited to ensure adequate financial resources for fulfilling its obligations under the public offer. Meskay & Femtee, primar-

ily engaged in agricultural processing and trading, views this acquisition as a strategic move to diversify its business portfolio. The company stated that acquiring Mandviwalla Mauser is deemed more feasible than developing a similar business from scratch, providing an immediate and established platform for growth.

Following the acquisition, Meskay & Femtee plans to continue operating Mandviwalla Mauser as a listed entity. The acquirer has expressed intentions to expand the target company's operations to enhance its growth and market presence.

The acquisition is being conducted in compliance with the Securities Act, 2015, and the Listed Companies (Substantial Acquisition of Voting Shares and Takeovers) Regulations, 2017. The Securities and Exchange Commission of Pakistan will oversee the process to ensure adherence to all relevant regulations.

Mandviwalla Mauser Plastic Industries Ltd has a long history in Pakistan's plastic industry. It was incorporated as a public limited company on June 13, 1988 and began operations on February 13, 1989. It was established to bring an organized, corporate structure to a previously disorganized industry.

The company changed its name to Mandviwalla Mauser Plastic Industries Ltd after signing a know-how agreement with Mauser Werke of Germany. The company’s manufacturing facilities are located at Port Qasim, Karachi, with excellent infrastructure for industrial operations.

The company operates two main units: an injection molded plastic products unit, and a blow molding unit. It produces a wide range of products including automobile parts, textile bobbins, plastic chairs, and household

items. It also manufactures 210-liter plastic drums, and is the only manufacturer of plastic barrels up to 210 liters capacity in Pakistan. It uses technology provided by Mauser WERKE GmbH, Germany

Mandviwalla Mauser has gained considerable market share and credibility among multinational companies through innovations and improved products.

Meskay & Femtee (Pvt) Ltd is a prominent rice exporting company based in Pakistan, with a rich history dating back to 1993. The company has its roots in a family business started by Mr. Roopan Mal Manghwani in the 1960s, who established a Rice Husking Plant in Khorwah, Badin, Sindh.

Mr. Teka Mal, the second eldest son of Mr. Manghwani, founded Meskay & Femtee and has been instrumental in its growth.

The company operates a modern rice processing plant that can parboil rice with a daily capacity of 400 metric tons. It has a total rice production capacity of approximately 1,450 tons per hour. It operates out of a 40acre facility in Dhabeji, 15 km from Port Qasim

Meskay & Femtee has grown from a traditional rice processing operation to become one of Pakistan's largest and most technologically advanced rice millers and exporters.

This acquisition could potentially lead to synergies between Meskay & Femtee's agricultural business and Mandviwalla Mauser's plastic manufacturing capabilities, possibly opening up new opportunities in packaging and storage solutions for agricultural products.

Following the acquisition, Meskay & Femtee plans to continue operating Mandviwalla Mauser as a listed entity and expand its operations to enhance growth and market presence. n

Spiritual guidance and business genius: The life and times of the

Aga Khan

Prince

Karim

Al-Husseini controlled a massive fortune matched only by the huge impact he had on the world and Pakistan

By Abdullah Niazi

There are and have been people in our world who lead extraordinary lives. Prince Karim Al-Husseini, known to the world for the past seven decades as the Aga Khan, lived many such lives.

He was different things to different people. To the international community, he was a globe-trotting senior statesman with British, Portuguese, and Canadian citizenship. In development circles, he was a billionaire with a vision for a world who became known for his philanthropy, vast resources, patronage of the arts, and connections. To the social elite of Europe and beyond, he was an exotic but noble gentleman of means; he lived in a Chateau in France, had a palace in Lisbon, remained a close personal friend of the King of England, and was a famed horsebreeder.

But to the 1.5 crore Nizari Ismailis spread across 25 countries, he was the Hazar Imam of his age — the ultimate religious authority in this world with the sole authority to interpret the hidden meaning of religious scripture. A direct claimant to the legacy of the Fatimid Caliphate, the most powerful Muslim Empire of the 10th and 11th centuries, he will be laid to rest in Egypt next to his grandfather in Aswan.

His legacy spans across a vast expanse comprising religion, philanthropy, medicine, media, hospitality, education, banking, architecture, heritage, to name only a few things. In Pakistan as well, the name Aga Khan carries weight with it. Prince Karim’s grandfather, Aga Khan III, was born in Karachi and was the founding President of the All India Muslim League. The Aga Khan Fund for Economic Development (AKFED), a for-profit organisation founded in 1984, owns HBL, Pakistan’s largest and oldest bank. It also owns Jubilee Insurance, the largest private-sector insurance company in the country. The work of his charitable organisation, The Aga Khan Foundation, goes far beyond these two entities. In fact, Prince Karim Aga Khan had a significant personal impact on the development of Gilgit Baltistan, where a large number of

his spiritual followers reside.

By lineage, Prince Karim was the 49th Imam of the Nizari Ismailis. The last in an unbroken chain of leaders. Many of his ancestors were emperors. Others were ascetics and exiles. He was only the fourth to bear that title Aga Khan, but within the modern history of Pakistan and the Islamic World, he was a singularly unique individual.

As the world remembers Prince Karim Aga Khan IV, it is important to remember the multiplicity that governed his seven decades as the leader of the Nizari Ismailis. As a businessman, he has amassed personal wealth from real estate, hospitality, horsebreeding and other enterprises with a distinct business philosophy. As the Hazir Imam, the Aga Khan used tithes paid by his followers to turn the Ismailis into a unified, cooperative, community unlike any other in the world. It is a multiplicity that began when he was young. When he superseded his own father to become the Imam of his people, whilst still a 20-year old undergraduate at Harvard University.

An evolving community

When Prince Karim Al Husseini became the leader of the Nizari Ismaili community, he was still a Sophomore. At the age of 20, he was a generation removed from the title of Aga Khan, but his grandfather’s will saw him ascend to the head of the community ahead of his father Prince Aly.

As Aga Khan IV, Prince Karim inherited a delicately balanced community. The Ismailis were in the midst of a period of prosperity in the middle of a fraught history. In the 10th and 11th Century, Prince Karim’s ancestors had ruled the Fatimid Empire, but exile and the fall of their Caliphate eventually followed. By the 19th century, the Nizari Imam was based in Iran where followers from all over the world would come to pay homage.

In 1840 the first Aga Khan and forty-sixth Ismaili Imam fled from Persia after an unsuccessful rebellion against the Qajar Throne. The Imam settled in Sind and helped the British in the annexation of the country in the Second Afghan War. By way of

reward the Imam was given a pension by the Governor and the rank of hereditary prince. This title is of great significance for the Ismailis and the community; not only does it give the Imam status in the eyes of his followers, but it also enables the community to regard itself vis-a-vis other organizations as a distinct, autonomous social group whose leader can negotiate on equal terms with other leaders

This was the beginning of the modern-day Nizari community as we see it today. By 1844, the first Aga Khan, Hassan Ali Shah, moved to Bombay in British India supported by a large number of his Khoja followers in the region. During his time in Sindh and Bombay, Hassan Ali Shah developed close ties with the British, in particular with Charles Napier who conquered Sindh.

The first Nizari Imam to use the title Aga Khan, Hassan Ali Shah was a trailblazer. In India, he aligned himself deftly with the support of the Khojas even winning a landmark case to establish his identity as the Imam of the Nizaris. He was succeeded by his son, Aqa Ali Shah, who became known as Aga Khan II. His was a short tenure and he died four years after ascending, being succeeded by his seven year old son as Aga Khan III.

Born in Bombay, Aga Khan III went to school in Europe, travelled the world, and used his position as head of Nizaris all over the world to pursue development projects across the world. He was Imam in the age of the end of empires, but he established an apolitical ascendence among world leaders. He received commendations from the German Emperor, the Ottoman Sultanate, and was eventually Knighted by Queen Victoria as Sir Sultan Mohamed Shah. He began a modernisation campaign amongst his community, promoting ideas of Islamic Rationalism and encouraging his community to gain Western education.

To fund these activities, Aga Khan III stressed upon an important tenet of the Nizaris: Dasond. This is a tithe that Nizaris pay directly to their Imam in a means to purify their wealth. The amount of the tithe depends on who you are, but generally it is between 1012%. As he expanded the Nizari community and pursued different projects, Aga Khan III stressed the importance of these tithes. Using them, the community organised itself, turning their Jammat Khanas into, as described in a study by the London School of Economics, as not just a mosque but also “administrative head- quarters, the social centre, the accommodation centre, the library, the employment bureau, the Ismailia Association and the relief centre.”

One aspect of the Ismaili community’s economic prosperity lies in an ethos of mutual support and help existing within the commu-

nity and devotion to the Imam. This can result in commercial cooperation and marriages within the community.

The economic philosophy of the Nizaris is described in some detail by Peter B Clarke, a professor of sociology at LSE. “The Ismailis are in the words of their Imam ‘business people’ and are encouraged to be adventurous and successful. An injunction of the Imam exhorts them: ‘Don’t live in a lump, spread out, leave home and town for the bush if you can be successful there.’ Money, moreover, is sanctified, sacra- mentalized, made symbolic: ‘The money that I give you’, another of the firmans reads, ‘is holy money and it must be spent with great care. There are commands to economize, ‘Economy in daily life as part of religion is necessary,” he writes.

“Alongside this advice there is maximum emphasis put on health, welfare, hygiene and education, insurance, investment and economic uplift. Innumerable firmans stress the maximization of material prosperity, acquisitive rationality, financial rationality and rationality of work. Indeed the pursuit of economic gain by means of the aforementioned rationalities is almost an ‘article of faith’; as one firman puts it: ‘According to our faith, one of the greatest services you can render the cause of religion is to make your worldly affairs a success.”

This was the direction Aga Khan III took the Nizaris towards. He encouraged them to do business with each other, to become educated and join the civil services around the world. For a long time, Nizaris in Syria dominated the bureaucracy. The community produced doctors, lawyers, and researchers of international note. Wherever there was a gap that needed to be filled, under the direction of the Aga Khan, individual members of the community would be helped. It was the case of a minority group banding together economically and socially under the wing of a spiritual leader.

A new man for a new job

The impact of Aga Khan III on the Nizaris is immeasurable. He was their Imam since he was a child, being the community’s guiding light for 72 years. In his time as the Aga Khan, he modernised his community, established himself as an international leader of repute, represented India in the League of Nations, played a vital part in the creation of Pakistan. But by the 1950s, things were changing quickly. The age of empire was coming to a close. Colonies were gaining independence, and in the post World War era, borders were being drawn up. This was the atomic age, and the Aga Khan was growing old.

When he died in 1957, he was succeeded by his grandson, Prince Karim. As Aga Khan IV, it was up to him to decide the identity the community would take. This was a strange era to be taking up this mantle. For starters, what nationality did the Aga Khan have? He was born in Geneva, and over time he would gain passports from different countries including the United Kingdom, Portugal, and Canada. But largely the Aga Khan occupied a position of esteem in the global world order, being treated almost as a head of state without a state. He participated in the Summer Olympics on the Iranian skiing team and maintained close working relationships in most of the countries he had followers in.

In his initial years as the head of the Nizaris, the Aga Khan largely dealt with existential issues that arose as a result of growing nationalist sentiment all over the world, and the tensions of the Cold War.

In 1972, under the regime of President Idi Amin of Uganda, people of South Asian origin, including Nizari Ismailis, were expelled. The South Asians, some of whose families had lived in Uganda for over 100 years, were given 90 days to leave the country. The Aga Khan phoned his long-time friend Canadian Prime Minister Pierre Trudeau. Trudeau’s government agreed to allow thousands of Nizari Ismailis to immigrate to Canada.

The Aga Khan also undertook urgent steps to facilitate the resettlement of Nizari Ismailis displaced from Uganda, Tanzania, Kenya, and Burma, to other countries. Most of these Nizari Ismailis found new homes in Asia, Europe, and North America.The initial resettlement problems were overcome rapidly by Nizari Ismailis due to their educational backgrounds and high rates of literacy, as well as the efforts of the Aga Khan and the host countries, and with support from Nizari Ismaili community programmes.

This would quickly become a feature of the Nizari community. The Aga Khan IV encouraged Ismā’ālā Muslims settled in the industrialized world to contribute towards the progress of communities in the developing world through various development programs. The Economist noted that Isma’ili immigrant communities integrated seamlessly as immigrant communities and did better at attaining graduate and post-graduate degrees, “far surpassing their native, Hindu, Sikh, fellow Muslims, and Chinese communities”.

The business of being Imam

By the 1980s, Prince Karim had established himself as Aga Khan IV. To his Nizari followers, he was much the same as any leader the community had seen over centuries. To the world, he had

become a figure of immense wealth and fame with important social and political connections. Unlike his grandfather and predecessor, Aga Khan IV remained largely politically untethered.

He was, however, a businessman of some note. The Ismaili community in its cohesion pays monetary tribute to the Aga Khan as well. Up until Aga Khan IV, what happened with these funds was largely informal. Theologically, the funds from the community were used at the discretion of the Imam. Aga Khan I, for example, used them to fund his campaigns against the Qajars. Over time, the family of the Aga Khan has also developed vast personal wealth. The family has been famous for their horsebreeding for many generations now, and they have investments in real estate, hospitality and other areas as well.

According to the official communication of Aga Khan IV, the Aga Khan’s personal wealth is kept entirely separate from the tithes (religious dues and contributions) given by the Ismailis. The tithes or religious dues of the Ismailis and all Ismaili Imamat assets are used exclusively for the needs, investments, and expenses of the Ismaili community - such as the construction and maintenance of Jamatkhanas, Ismaili community banks, cooperatives, loans, and social programs.

In the case of Prince Karim, his personal wealth came from four sources. The first was the family’s horsebreeding business. Aga Khan IV had some of the most famous horses in the world, one of which was even kidnapped by the Irish Republican Army for ransom. He also inherited real estate investments from his grandmother, Lady Aly Shah, as well as businesses and assets from his father. His father Prince Aly Khan pledged allegiance to his own son, and when he died, Aga Khan IV received his personal wealth including his horsebreeding business. He was also the heir to Aga Khan III’s personal fortune. Since then, Aga Khan IV has used this personal wealth to make more investments in tourism and real estate development such as in the Costa Smeralda in Sardinia, the Meridiana Airline, and the Ciga Hotel chain.

This is the personal wealth which he holds as Prince Karim Al-Husseini, not as the Aga Khan. Conservative estimates have put his net worth somewhere between $3-10 billion. The other wealth he controls is the wealth coming from the Nizari community, which he manages as the Imam. In its structure this bifurcation is almost tribal. On becoming Imam, the Aga Khan personally inherited what was left to him as a legal heir of his grandfather and father, while the Imamat continued to own its own assets.

The idea is that the assets of the Imamat will be used for community work. Up until Aga Khan IV, this work was largely done

informally and in a discretionary manner. The big change made by Aga Khan IV was to institutionalise this. In the 1960s, most of the Nizari community existed in developing regions, ranging from East Africa to Soviet Central Asia and the subcontinent. The beginnings of this institutionalisation began when the Aga Khan set up a group of companies under the corporate name Industrial Promotion Services (IPS) in 1963. Each company was created to provide venture capital, technical assistance and management support to encourage and expand private enterprise in Sub-Saharan Africa and South Asia. In its own words, at the time, IPS’s investments focused on providing goods and services that these regions lacked, as they began to emerge from a colonial and conflict-stricken past. The aim was to improve livelihoods through the creation of jobs and the inflow of investment.

In 1967, these companies started to be known as being under the umbrella of the Aga Khan Development Network (AKDN). By the 1980s, these companies had grown and so had the needs of the organisation. It is a universal reality of charity that at some points organisations need to find funding beyond donors. For this purpose, charitable organisations often engage in for-profit business, the proceeds of which are pumped back into the charitable works.

This is why the Swiss organisation Aga Khan Fund for Economic Development (AKFED). This is one of many such organisations that fall under the AKDN umbrella. Among them are Aga Khan agencies for academics, habitat, microfinance, education services, health services, a trust for culture preservation, the Aga Khan University, and the University of Central Asia.

These agencies and organisations in some cases are profitable, and are involved in a number of businesses all over the world.

The Aga Khan and Pakistan

The impact of Aga Khan IV on Pakistan has been enormous. Among the Pakistani political elite, he seems almost to be a Pakistani. One reason for this, of course, is the connection his father had to Pakistan. Aga Khan III was born in Bombay and led the Muslims at the Simla Delegation, becoming the founding President of the All India Muslim League. He remained honourary President of the League after partition and all the way up to his death in 1957.

Perhaps the sentimentality of this, along with his many followers in Pakistan, have been a reason for the Aga Khan to invest in Pakistan. For example, Pakistan has one of the larger networks of Aga Khan Schools

which are spread all over the world. Many of these schools opened up in the wake of the war on terror.

In areas of Pakistan where militant madrassas turned out the likes of the Taliban, Aga Khan schools give both boys and girls a broad and liberal education. They take pride in their Muslim heritage, learning that Muslims made significant advances in mathematics, optics, urban development, geography and navigation; that Islam inspired the poetry of Rumi and the science of Avicenna and the philosophy of al-Hallaj. They learn that Muslim states in the past such as the Fatimid Empire protected minorities such as Christians and Jews, and that pluralism is one of the creations of God.

The Aga Khan University (AKU) is the most ambitious Ismaili educational project since the creation of Al-Azhar University in Fatimid Cairo in the tenth century. AKU started with a medical school that focused on training nurses. Not only did this greatly improve the medical capacity in Pakistan, but it opened unprecedented professional opportunities for Pakistani. Over time, the Aga Khan Teaching Hospital has become the best medical university in Pakistan, and the go to choice for most medical procedures.

It was founded in 1983 as Pakistan’s first private university, initially taking the form of a nursing school. Over the years, it has expanded to six campuses across three continents, facilitating learning in a wide variety of disciplines.

On top of this, as we have mentioned before, the AKFED owns HBL which is Pakistan’s largest bank. It is also a major investor in Serena Hotels, owning 49% of the company.

HBL Microfinance Bank (HBL MfB), formerly FMFB-Pakistan, was one of the earliest AKAM affiliates to be established in 2002. Since then, it has provided over $712 million in loans to more than 2.9 million customers, becoming a strong player in the country’s microfinance industry and ranking amongst the top five providers. Currently, over one-third of the Bank’s clients are female and two-thirds of the borrowers reside in rural areas. The foundations are involved in other areas such as building habitats, supporting civil society organisation, cultural development, heritage preservation, and so much more.

The role of the Aga Khan in Pakistan, in particular in education and healthcare, is often understated. But perhaps what is most significant about the Aga Khan’s life are the institutions he created. In the course of his life, he wore many different hats and wore them with distinction. It remains to be seen how the institutions he created fare under the stewardship of a new generation. n

Kia’s new Sportage: When a small price gap tells a bigger story

As dealers command premiums, Kia’s hybrid pricing strategy reveals a calculated gamble

Profit Report

In the cutthroat world of automotive innovation, few concepts are as tantalizing—or treacherous—as the first-mover advantage. For years, Kia’s Sportage has dominated Pakistan’s SUV landscape, having sold over 40,000 units since its 2019

launch to become the country’s highest-selling locally produced C-SUV.

The vehicle carved its niche by masterfully blending affordability with aspirational design, setting a new benchmark for the modern crossover segment.

Yet despite this success, Kia faced mounting pressure to reinvent its flagship SUV. The urgency stemmed from two critical challenges:

an increasingly crowded market where new competitors threatened its dominance, and restless dealers whose profitability hinged heavily on the Sportage—the only model in Kia’s Pakistani lineup to resonate strongly with consumers.

The answer to these challenges has arrived in the form of the Sportage L, a fifth-generation reinvention whose calculated pricing strategy reveals Kia’s ambitious plans

to defend its crown.

The evolving landscape

The Pakistani SUV market has transformed dramatically since the Sportage first arrived. What was once a playing field dominated by a handful

of established players has evolved into a battlefield of new entrants, each vying for market share with increasingly competitive offerings. It’s in this charged environment that Kia has launched its counter-offensive: the Sportage L.

Lucky Motors, Kia’s local partner, introduced three variants of the new Sportage L last week. The lineup starts with the Alpha at Rs. 9.49 million, moves up to the FWD at Rs. 11.82 million, and tops out with the HEV Hybrid at Rs. 12.85 million. Each variant targets a specific market segment, but it’s the pricing structure that reveals Kia’s broader strategy.

The company hasn’t just relied on pricing to make its case. The new Sportage L comes with an array of customization options previously unseen in this segment. Buyers can choose from three interior themes—from the understated All Black cloth to the bold Carmine Red artificial leather—and five exterior colors ranging from the subtle Gravity Grey to the striking Fusion Black. Kia has also backed the launch with an aggressive warranty package: 4 years or 100,000 kilometers for the standard variants, and an industry-leading 8-year (160,000 km) warranty for the hybrid’s battery system.

However, the true intrigue of the Sportage L lies in its sophisticated pricing calculus. At first glance, the HEV hybrid’s Rs. 12.85 million price tag seems modest—a mere 9% premium over the FWD petrol variant. This pricing strategy becomes particularly fascinating when compared to competitors like Haval H6 HEV and Toyota Corolla Cross Hybrid, which command 12% and 15% premiums respectively over their petrol versions.

The Haval H6 Hybrid, priced at Rs. 11.749 million compared to its petrol variant at Rs. 10.449 million, represents a Rs. 1.3 million difference. Similarly, Toyota’s Corolla Cross hybrid at Rs. 9.012 million stands Rs. 1.15 million above its petrol counterpart at Rs. 7.862 million.

Industry experts suggest this pricing model reflects a deeper understanding of behavioral economics, specifically the concept of decoy pricing—a psychological tactic making alternatives seem less appealing to nudge consumers toward a target product.

This strategy mirrors what marketing theorists call the Starbucks Effect: When a medium latte costs Rs.1000, and a large is priced at Rs.1100, the marginal difference naturally incentivizes customers to “upsize.” Similarly, Kia’s HEV hybrid, loaded with Advanced Driver Assistance Systems (ADAS) and other premium features, is positioned as the “logical upgrade” from the FWD.

The compressed price gap cleverly obscures the HEV’s true premium, which industry analysts argue should be 19–20% (Rs. 2 million) when factoring in the comprehensive suite of added features. The FWD variant thus

serves as a sophisticated decoy—a psychological anchor making the HEV appear irresistibly value-packed. This pricing strategy is reminiscent of McDonald’s “Extra Value Meals,” where the bundled price makes individual item purchases seem illogical.

When factoring in taxes and freight charges, the price gap shrinks even further at the consumer level, making the hybrid variant an increasingly compelling choice for prospective buyers.

Beyond pricing

Yet Kia’s pricing strategy is running headfirst into Pakistan’s notorious ‘ON’ market. Despite the company’s official stance against premiums, the new Sportage L is already commanding an extra Rs. 1 million above its sticker price—money split between dealers and investors who’ve spotted an opportunity.

This isn’t surprising. Kia dealers, starved of a major launch for years, see the Sportage L as their chance to cash in. The company’s “firstcome, first-served” policy and requirement for full upfront payment have only added fuel to the fire. What’s meant to ensure fair distribution has instead created an artificial shortage, with dealers and investors swooping in to capitalize on buyers’ eagerness to skip the queue.

The ON pricing phenomenon reveals a deeper truth about Pakistan’s automotive market: unofficial premiums often serve as indicators of a vehicle’s perceived value and social status. While manufacturers officially discourage such practices, the resulting exclusivity often enhances brand desirability. This dynamic creates a complex ecosystem where official prices serve merely as starting points for market-driven valuations. For Kia, while officially maintaining a stance against ON pricing, the practice inadvertently benefits its brand positioning by creating an aura of exclusivity and high demand.

Beyond pricing tactics, Kia’s hybrid gambit shows both defensive instinct and forward thinking. As rivals like Haval and MG make inroads with their hybrid SUVs, Kia couldn’t afford to sit back. The HEV Sportage isn’t just about keeping up—it’s about staying ahead in Pakistan’s gradual shift toward electrification.

Yet for all its clever pricing and market positioning, Kia faces a fundamental challenge. The Sportage’s success story is being tested by competitors who’ve had years to study its playbook. They’re offering similar technology, often at sharper prices. While Kia has written Pakistan’s SUV playbook so far, the next chapter might not be entirely in its hands. The real test will be whether the market rewards its first-mover legacy or embraces the alternatives that followed in its wake. n

Battle for KE’s ownership heats up

A flurry of letters from January have surfaced, indicating a growing battle for control of Pakistan’s first vertically integrated electric company

Profit Report

The battle for the ownership and ultimate control of K-Electric (KE) is heating up. The latest increase in temperature comes nearly two years after a fateful transaction in the Cayman Islands changed the ownership structure of Pakistan’s oldest vertically integrated electric company forever.

The transaction in question took place in early 2023. The company, once an Abraaj asset, was sold to AsiaPak Investments in a deal that took place in the Cayman Islands far away from Pakistani regulators and stakeholders. AsiaPak is run by Sheheryar Chishty, a former highflying banker who now owns Daewoo in Pakistan and has deep interests in Thar Energy.

Despite two years passing, Mr Chishty and his company have not been allowed to take the reins of the KE management. Behind this delay is a tussle between the new regime and some of the company’s minority shareholders, in particular influential Saudi investors that have been involved in KE and have had a claim in the company since long before Mr Chishty arrived on the scene. In a recent letter these Saudi investors, under the banner of Al-Jomaih, have claimed that Mr Chishty and his investment firm are in breach of securities regulations for not properly disclosing information. The letter was written to KE to express concerns that KE has not made necessary disclosures about changing ownership patterns. They also question the extent of Mr Chishty’s shareholding and his posturing as the company’s real owner.

The letter was written in a bid to keep Mr Chishty away from management control of KE, and goes so far as to call his actions “unlawful” and “in breach of fiduciary duties owed to limited partners”. However, KE has since made disclosures based on the letter by Al-Jomaih, which was sent on the 25th of January 2025. In this disclosure, they have also attached older correspondence from Mr Chishty which clears up his declaration of a change in Ultimate Beneficial Owner (UBO) of KE — which is an important legal term. How does all of this work? As a company, KE is governed by a complex ownership structure that has only gotten more convoluted over time. As things stand, the battle between Mr Chishty and Al-Jomaih is reaching crescendo. Even as court cases continue to be fought abroad, the question remains: what will eventually happen to KE?

The KE problem and a proposed solution

To really understand the current scenario, it is important to figure out what is going on with KE’s sale. A great deal can be seen

through the company’s corporate history. Let’s start at the beginning.

Thirty-two years after Thomas Edison created the world’s first utility company in Lower Manhattan, the Karachi Electric Supply Company (KESC) was founded in 1913 (rebranded in 2013 as K-Electric). It is the country’s only vertically integrated utility, with its own power generation, transmission, and distribution assets. Until the late 1960s, KESC was largely a financially self-sustaining entity. In the 1980s, the company briefly became a subsidiary of the Water and Power Development Authority (WAPDA) and was at one point placed under the management of the Pakistan Army.

The modern history of K-Electric that is relevant to us now begins after all of this. In 2005, the Musharraf Administration sold off a 66.4% stake of the company to a consortium of the Al-Jomaih Holding Company, a diversified Saudi Conglomerate, and the National Industries Group, a publicly listed Kuwaiti financial conglomerate (which also owns a large stake in Meezan Bank). For three years, the Saudi-Kuwaiti conglomerate failed to make any headway in turning around the company, finally turning in 2008 to Arif Naqvi, the former Karachiite who had gone on to create Abraaj Capital in Dubai.

Abraaj was already the largest private equity firm in the Middle East by then, and had previously made forays into the Pakistani market before. In October 2008, Abraaj bought out half of the Jomaih-NIG stake in KESC, injecting $391 million into the company. It then began a turnaround effort the likes of which have never been seen in Pakistan before. Abraaj spared no expense in trying to turn around KESC, investing upwards of $1 billion in the company’s power generation and transmission infrastructure, which brought the utility’s power generation efficiency rate from 30% in 2008 to 37%. As per KE’s own numbers, from 2009 when Abraaj took over KE’s transmission and distribution (T&D) losses were 35.9%. By 2019 this number had fallen to just under 20%.

This was a bonafide come-from-behind recovery.

During this journey, Abraaj was ready to reap their rewards. They had taken KE on at a time when the company was a loss making entity (they made losses up until 2011-12) and turned it into a profitable power company. In 2016, they sold 66.4% of K-Electric to Shanghai Electric, the Chinese power company, for a whopping $1.7 billion making it the biggest acquisition of a Pakistani company in a decade.

This was always the plan for Abraaj. It is the very reason private equity firms came into existence in the first place. Abraaj came in, took control of a storied company with a unique economic purpose that had been sullied by bad management and turned it

around through a combination of strategic capital investments and modern management techniques. Now they were ready to sell it off in a healthy, relatively unleveraged state to a strategic buyer.

Except what seemed like a deal made in the stars was cursed. To cut a very long story short, consistent delays on the part of the government meant the Shanghai deal could not go through. Despite a lot of political lobbying on the part of Abraaj’s Arif Naqvi, the deal was dead in its tracks. And then came the crash. In 2019, Arif Naqvi and Abraaj were involved in an international scandal that ended with the company utterly bankrupt. And along with it the Shanghai Electric deal went kaput. For six years Abraaj’s baggage weighed the Shanghai deal down and KE remained unsold.

As tough a year as it was for Arif Naqvi and Abraaj, 2019 was no bed of roses for K-Electric. Place the company in its context. For decades the company was a self-sustaining profitable entity. It met an unfortunate fate in the form of nationalisation and bounced around different government departments before finally being bought by a private equity company which set it straight and back to making money and providing its services efficiently. But when time came for a permanent new owner to take over, disaster struck.

At this time KE was under steady leadership. Moonis Alvi has been the CEO of the company since June 2018, a year before Abraaj came crashing down. Mr Alvi is an old hand at KE, and was one of the architects of its revival under Abraaj having been part of the team since 2008. He was the company’s CFO before his elevation to the top job.

So when it became clear Abraaj was done for, there was still a steady, stabilising hand available to keep the ship afloat. Mr Alvi continued in the same way that things had been going. Transmission and distribution losses continued to fall and have come down to as low as 15.27% compared to the 35.9% that existed when Abraaj first took over in 2008.

But keeping things afloat can only go on for so long. From 2019 onwards KE was in a bit of a fix. It didn’t know exactly what to do with itself, so the focus became fixing losses and increasing efficiencies in other areas such as health, safety, and environmental (HSE) standards. None of this ends up helping the bottom line significantly, and to have any sort of long-term vision you need a long-term owner. For a while many thought Shanghai Electric would still be involved and interested, and the company did keep renewing their interest in keeping the deal alive every six months.

The baggage of Abraaj proved too much and kept weighing down the deal. and KE remained unsold. That is of course until a quiet, seemingly normal day two years ago.

Enter Chishty

Shaheryar Chishty had been interested in K-Electric for a while. The former highflying international banker was born in Lahore, raised in Karachi in a navy family, and came back to Pakistan in 2011 where he acquired ownership of Daewoo as well as interests in CPEC backed projects regarding Thar Coal. A self-described investor in orphan assets, Mr Chishty had been impressed by the Abraaj led turn around of KE and had tried to acquire the company. At that point, CPEC was at its peak and Chinese investors were deeply interested in putting money into Pakistan. Because of his involvement in CPEC projects in the past, particularly in Thar Coal, Chishty was well connected in China and put together a consortium that would bid for control of KE. But Shanghai beat him to it.

“There were Chinese investors, other Asian investors, and a couple others with interests in KE as well but in the end Abraaj ended up receiving a very good offer from Shanghai Electric,” Mr Chishty told Profit last year.

So when the opportunity presented itself again, Mr Chishty started making moves to acquire KE, which he did in the Cayman Islands.

The assumption was that the KE management and shareholders would be happy at the acquisition because it would mean direction. The Shanghai deal was clearly not happening, and KE was not doing too well either. Just look at their financials from 2023 where the company reported its first loss in 12 years. And it wasn’t some small dip in fortunes. K-Electric bled over Rs 31 billion last year in the wake of rising electricity prices and increasing line losses.

This was a dark moment in the history of the storied company. Its problems had caught up with it. These losses were ten times greater than the Rs 3 billion loss they incurred in 2020 because of the pandemic. Even though KE had been on a mission to cut line losses and make themselves more efficient, the company was always going to be a victim of the times. In the past couple of years, power prices have been raised by the government, the rupee has depreciated, inflation has soared, and the cost of borrowing from banks has risen sharply because of the very high interest rate that has been maintained for some time now.

Because of inflation, people are either using less electricity or they are not paying their bills or they are stealing. This has reduced KE’s recovery ratio from 96.7% in 2022 to 92.8% in 2023. The company also supplied 7.3% less power during the year “due to reduced economic activity”.

Despite all of this Mr Chishty and his other investors have not been allowed to take management control of KE. This does not mean they haven’t been trying, and the majority sharehold-

K-Electric is being treated as an orphan child by the shareholders, by the federal government, by the management and for whatever reason they are doing so is not my job to figure out

Shaheryar Chishty, AsiaPak Investments

ers actually have a detailed plan with regards to how they want to go about best utilising KE. So why don’t they get a seat at the table?

The ownership structure

What we have here is a legacy company that was in trouble, it was revived via private equity before falling victim to the very private equity firm that gave it a second life. Now, the company has new owners that have plans for it but somehow they are unable to get their foot in the door. Why is this so?

To understand this we must get to the bottom of how KE was acquired by these new owners. Profit covered this last year when the change in ownership first happened.

But to cut a long story short:

Since KE was owned by Abraaj, which as a company has gone bankrupt, its assets are a little all over the place. Just take a look at the ownership structure of KE. When the Al Jomaih group entered the picture in 2005, they created KES Power Limited (KESP) which was a Cayman Islands company. This company paid the government of Pakistan directly and acquired a 66.4% stake in K-Electric in Pakistan.

So when Abraaj wanted to buy KE from Al Jomaih in 2009, they funnelled over $370 million in foreign direct investment into KE through the KESP company in Cayman. This money was channelled through the Infrastructure & Growth Capital Fund L.P. (“IGCF”), a $2 billion Cayman Islands private equity fund with investment contributed by over 100 different international investors, managed then by Abraaj Investment Management.

This means KE is owned by the KESP in the Caymans, which after Abraaj’s entry is now owned by the IGCF. So when Chishty wanted to acquire Abraaj’s stake in KE, it could not acquire KE in Pakistan. It had to go to the

KESP in Cayman. Chishty’s company, AsiaPak Investments, created a special purpose company called Sage Venture Group Limited (Sage) and registered it in Cayman. Sage then bought out the Infrastructure Growth and Capital Fund LP (IGCF or the Fund), which holds an indirect material stake in K-Electric Limited. These transactions were authorised in proceedings at a court in the Cayman Islands, according to court documents.

This essentially meant that Mr Chishty and his AsiaPak Investments now owned the majority of the shares in K-Electric. This did not translate to them having control of the board of KE in Pakistan, but they could easily translate this into management control in Pakistan. Well, at least in theory they could. What they did not quite expect was that some of the minority shareholders would give them a real run for their money.

The fights kick off

This is where we get to the events of the last couple of years. Remember, what Mr Chishty has bought is a 53.8% stake in KESP, which is the company which owns 66.4% in KE. The remaining 46.2% of KESP is owned by Al-Jomaih Power, and Denham Investments. This is the same Al Jomaih that first bought KE through the KESP in 2005 before they sold it to Abraaj in 2008.

The acquisition by AsiaPak seems to have not gone down well with Al Jomaih. This is where we get into the recent set of documents released by KE in its disclosures. And we will work our way backwards. On the 30th of January, KE sent a letter to the PSX announcing they were sending over a disclosure form for price sensitive information. The company explained that they received a letter from Al Jomahi on the 25th of January and were making the disclosure as a result. They were also attaching letters from Mr Chishty from July 2024, and more informa-

tion and documents with the disclosures.

Al Jomaih’s letter claims that IGCF, the fund that bought KESP from Al Jomaih, was not allowed to distribute shares to a limited partner such as Sage, which is owned by AsiaPak and eventually Chishty. It also raises the question of whether or not Sage has provided evidence as to its acquisition. “I understand that IGCF was not, as a matter of law, permitted to distribute the shares in kind to thehgnited partners in the fund and I have seen no evidence to support Sage’s assertion that it holds 46.11% of KPH. It is also not clear to me whether such evidence has been provided by Sage or anyone else to KIE.” Sage claims the acquisition was explained by them in July 2024. Back then, an article had appeared in Business Recorder, quoting the SECP as not being happy with KE’s acquisition since they had not been provided details of Ultimate Beneficiary Owner (UBO). This was challenged in a letter sent by Mr Chishty to the SECP, in which he points out he had communicated a change in UBO to the SECP on multiple occasions, and as far back as February 2023. In the letter, he claims to be the UBO.

“I have repeatedly through the SC Response Letters sought to answer any questions raised by the SECP and to inform my interpretation of the applicable regulatory and/or legal requirements. I intend to reiterate certain key facts and update the SECP on recent developments to the offshore holding structure of which I am the Ultimate Beneficial Owner (“UBO”). I welcome advice and assistance from the SECP (as also requested in the SC Response Letters) in the interpretation and application of any legal requirements that may become applicable to me as the UBO of Sage Venture Group Limited (“Sage) - a company incorporated and existing under the laws of the British Virgin Islands (“BVI”),” read the letter seen by Profit. Another document to go with this is Draft Form 44 from KESP to KE, which is from February 2023 and was presented by Mark Skelton, the Chairman of the Board of Directors of the KESP, and a representative of the original SPV 21 Fund involved in the acquisition. In the document, there is a breakdown of the ownership, details of which are given below:

• KES Power Limited (*KESP”) holds 66.4% of the issued share capital of K-Electric Limited (“KE”)

• IGCF SPV 21 Limited (*IGCF SPV 21”) holds 53.8% of the issued share capital of KES Power Limited.

• K Power Holdings Limited (‘KPH”) (Formerly IGCF SPV 26 Limited) holds 70.6% of the non-voting issued share capital of IGCF SPV 21.

• Sage Venture Group Limited holds 100% of the Shares of KPH and 46.1% of the B share capital of KPH

“AJH has had a long history with its indirect investment in KE, so one would have thought it knew how its investment was made, via KES Power Limited (KESP). KESP is the owner of 66.4% of shares in KE – not any of the KESP shareholders. KESP stakeholders are only indirect economic shareholders of KE”

• AsiaPak Investments Limited (“AsiaPak Investments”) holds 100% of the issued share capital of Sage.

KPH Management

• KPH is managed by its board of directors comprising Mr. Shaheryar Arshad Chishty : Faisal Siddiqui; Darin Baur; Sameer Chishty, Casey MeDonald

• Mr. Shaheryar Arshad Chishty is the UBO of KPH.

• The Managing Partner (Senior Managing Official) of KPH is Shaheryar Chishty

A more detailed letter by Mark Skelton gives a strongly worded reply to the Al Jomaih letter. Three days after Al Jomaih wrote to KE, and two days before the disclosures were made, Mr Skelton wrote a letter to the SECP which started by saying “It is disappointing that Al Jomaih Holding Co (AJH) decided to send such a misleading letter to KE”.

“AJH has had a long history with its indirect investment in KE, so one would have thought it knew how its investment was made, via KES Power Limited (KESP). KESP is the owner of 66.4% of shares in KE – not any of the KESP shareholders. KESP stakeholders are only indirect economic shareholders of KE.”

Where things stand

The situation, however, is that AsiaPak essentially owns the same position in KE that Abraaj did up until it went bankrupt. And up until the Abraaj scandal blew up, the private equity fund had complete control over the KE board and could appoint its representatives onto it. This is something that through repeated legislation and stay order Mr Chishty’s AsiaPak has not been allowed to do.

Part of the reason could be the fact that the minority shareholders in question that form Al Jomaih have some serious influence within circles that matter in Pakistan. The Saudi and Kuwaiti investors that make up the consortium are people that the government does not necessarily want to get onto the bad

Mark Skelton, KESP

side of. Perhaps nothing is more telling of this than reports of the Special Investment Facilitation Council getting involved in this kerfuffle, with the Executive Committee of SIFC setting up a three-member committee to resolve issues related to the power utility.

“K-Electric is being treated as an orphan child by the shareholders, by the federal government, by the management and for whatever reason they are doing so is not my job to figure out,” explains Mr Chishty in a conversation with Profit last year. During the interview, it was clear the process is frustrating. And why would it not be? When you buy something, you expect you’ll be able to apply it as you see fit. As a man with a plan, he feels very little is being done to set KE on the straight path.

This is what it boils down to for Mr Chishty and his AsiaPak Investments. In 2022, they bought an investment that they expected to have control of and run as they saw fit as majority shareholders. Instead, they have been denied this consistently. By the time they get control (if they do any time soon that is), what state will KE be in and will their plans be viable?

As Mr Chishty explains to us, his entire approach to the problem was to focus on high cost imported fuel that KE used to produce electricity. His plan was to use his influence and experience in Thar Coal to shift Karachi onto a cheaper fuel source for its electricity. KE is plagued by many problems. The company is plagued by problems and is far from an investor’s dream. The only thing it has going for it is the monopoly it holds over electric supply in one of the world’s largest cities. Yet even this is under threat with people slowly coming to rely more and more on home based solar solutions. As things stand, Karachi is caught in a vicious cycle of energy being insufficient, unaffordable, uncompetitive, unreliable. Unaffordable energy reduces consumer purchasing power and lowers quality of life, leads to reduced tax base, as well as growing dissatisfaction with provincial and municipal leaders. The last thing the company needs is a protracted ownership battle. n

A 5% rise in petrol consumption indicates stability in consumer spending

The rise in diesel consumption may indicate an increase in commercial transportation and agricultural production

Profit Report

Pakistan’s oil marketing sector has emerged as an unlikely barometer of economic resilience, with January 2025 petroleum consumption data revealing dual narratives: sustained consumer spending power driving petrol demand and a diesel-led industrial revival defying macroeconomic headwinds. The latest reports from Topline Securities and Arif Habib Ltd. paint a picture of an economy navigating challenges through shifting fuel consumption patterns, offering cautious optimism for fiscal year 2025.

Pakistan’s oil marketing companies (OMCs) reported flat year-over-year total petroleum sales of 1.38 million tons in January 2025, masking significant sectoral shifts beneath the surface. The stability comes despite a 1% month-over-month increase in petrol and diesel prices, suggesting demand inelasticity in

key economic segments.

Let us take a look at the key figures from January, released by the Oil Companies Advisory Council, an industry group. They indicate that petrol consumption was up 1% year-on-year and 10% month-on-month during January 2025. Petrol is mostly consumed by urban commuters and is seen as among the most sensitive to inflationary pressures. When prices get beyond the purchasing power of most consumers, they tend to cut back on discretionary driving, which reduces petrol consumption in the country.

Diesel consumption, meanwhile, was up 17% year-on-year and about 5% month-onmonth during January 2025. Diesel is mostly used in commercial transportation and agriculture, which may indicate a pickup in commercial and agricultural activity in the country.

The 7-month cumulative figures for the fiscal year ending June 30, 2025 show clearer growth trajectories, with total petroleum sales

up 4% year-on-year to 9.41 million tons, led by diesel’s 11% year-on-year surge.

The 5% year-on-year growth in petrol sales through 7MFY25 to 4.37 million tons reveals surprising consumer resilience. This sustained demand comes despite average petrol prices remaining 20-25% higher than pre-2023 levels. Meanwhile, persistent inflationary pressures (CPI averaging 28% in fiscal year 2024), and disposable income erosion from currency depreciation cannot have helped matters.

So what is driving this resilience? Three factors.

1. Urban mobility demand: The 10% MoM January surge coincides with school reopenings and winter tourism, reflecting restored education and service sector activity.

2. The Bykea phenomenon: Increased use of motorbikes for goods delivery – through online platforms such as Bykea, among others – (up 15% per PBS data) as SMEs optimize logistics costs.

3. Hybrid work models: Corporate shifts to partial office attendance sustaining commuter demand without pre-pandemic peak traffic.

"Petrol has transitioned from luxury to essential commodity status," notes Topline’s energy analyst. "Even at Rs 275/liter, demand demonstrates remarkable price inelasticity in urban centers".

The 17% year-on-year diesel sales jump to 600,000 tons in January – the highest monthly volume since FY22 – signals awakening commercial and industrial activity. This aligns with activity in several sectors that are primary consumers of diesel as their fuel.

In agriculture, there has been a higher allocation of government funds for subsidies for tubewells for irrigation, which use diesel as fuel to pump groundwater to the surface. This has cause the Rabi (winter) crop sowing to increase acreage by 8% year-over-year.

In transportation, cross-border trade with Afghanistan is being revived and is up 40% year-on-year as the effects of the US withdrawal of troops from that country continue to fade into the background. Freight volumes at the military-owned National Logistics Cell – the nation’s largest commercial trucking operator – are up 22% this year.

In manufacturing, diesel is often a fuel in captive power plants and is used as a substitute for when there are shortages of natural gas. Captive power plants are the power plants that large scale manufacturers establish within their own factories so that they do not have to rely on the grid’s electricity, which is often the subject of rolling outages. Given the fact that large scale manufacturing is up 3.6% year-onyear, the increased diesel consumption could be an indicator of industrial activity levels picking up.

In construction, infrastructure projects have resumed after the government has sought to revive the infrastructure projects associated with the China Pakistan Economic Corridor (CPEC). Cement sales are up 5% compared to the same period last year.

Arif Habib Ltd also attributes diesel’s resurgence to successful anti-smuggling operations, recovering 15-20% of the informal market previously served by Iranian imports. The resulting formal sector sales growth comes despite diesel prices averaging Rs290 per liter – 18% higher than fiscal year 2024 lows.

The fuel consumption trends intersect with macro developments. On the positive side, the government collected Rs651 billion in the form of the petroleum development levy – a form of sales tax on petrol and other oil products – during the first seven months of the fiscal year ending June 30, 2025. This number represents 51% of full year target, and is likely to result in easing fiscal pressures.

Meanwhile, the 46% year-on-year decline in furnace oil consumption illustrates the successful and continued shift in thermal power generation away from expensive fuels like furnace oil and most cost-effective options like imported reliquefied natural gas (RLNG) as well as other renewables.

It may also help the market that – after decades of the dominance of state-owned oil companies – the private sector market is taking market share, which may be helping boost overall industry volumes. Hascol’s 31% year-on-year sales growth and GO’s 196% surge indicate competitive dynamics spurring service improvements

Meanwhile, the state-owned Pakistan State Oil (PSO) saw its sales drop by 5% yearon-year during the same period, highlighting its continued decline in the market.

All, however, is not well in the oil market. The energy sector’s intercorporate circular debt problem – caused by the government failing to honour the full level of subsidies it owes power companies, who in turn cannot pay their fuel suppliers in time – continues to be a massive problem. As of December 2024, the oil market companies have Rs700 in circular debt receivables, according to a regulatory filing by PSO.

There may also be some trouble on the horizon. Pakistan still imports most of its oil, and global prices have been rising. Brent crude prices – the global benchmark for oil – were up 12% last quarter compared to the previous quarter.

Analysts project fiscal year 2025 petro-

leum sales growth between 4-6%, contingent on a handful of demand catalysts. Among these are the operationalization of ML-1 railway and special economic zones as part of the CPEC revival. Implementation of the Kissan Package 2.0 subsidies would also help increase demand in agriculture. And the renewal of the European Union’s GSP+ preferential trade status for Pakistan would drive textile sector diesel demand.

The risks to this thesis are many as well, foremost of which is the increase in energy prices likely to be mandated by the International Monetary Fund (IMF) as a condition of its continued bailouts of the government of Pakistan. A global recession, meanwhile, would reduce consumption in the economy that is fueled in part by remittances from Pakistanis living abroad. And LNG supplies may not remain stable, which may impact fuel choices among industrial consumers.

Pakistan’s oil consumption narrative reveals an economy adapting to constraints – consumers prioritizing mobility essentials, industries optimizing fuel mixes, and policymakers balancing fiscal needs with growth imperatives. While diesel’s revival sparks hope for manufacturing and export recovery, sustained growth requires addressing structural issues.

The coming months will test whether Pakistan’s oil consumption trends reflect temporary adaptation or the foundation of durable recovery. With global oil markets and domestic reforms at inflection points, OMC sales sheets may well write the next chapter of the country’s economic story. n

Fertilizer sales down 6% as weakness in farm sector continues

Farmers struggle as a combination of crop failures and rising prices squeeze their pocket books, and agricultural credit fails to fill in the gap

Profit Report

Pakistan’s fertilizer industry is navigating turbulent waters, with January 2025 data revealing deepening divergences between urea and diammonium phosphate (DAP) consumption trends. Provisional figures from Arif Habib Ltd (AHL) and Topline

Securities highlight a 27% year-over-year collapse in urea offtake to 446,000 metric tons and a 6% year-on-year decline in DAP sales to 63,000 metric tons during the first month of 2025.

These trends underscore systemic challenges plaguing smallholder farmers and shifting industrial dynamics, even as the Punjab government’s Kissan Card program sparks localized DAP demand surges.

Key factors driving the overall reduction in volumes include the stunning collapse in sales of urea, the most commonly used fertilizer in the country. Every company in the sector that sells urea took a hit to its sales.

Engro Fertilizers’ urea sales plunged 49% year-on-year to 107,000 metric tons, while Fauji Fertilizer Company (FFC) and its recently amalgamated subsidiary Fauji Fertilizer Bin Qasim (FFBL) saw a 27% year-onyear decline to 194,000 metric tons. Seasonal factors (post-Rabi slowdown) and temporary plant shutdowns exacerbated the slide.

The picture in diammonium phosphate (DAP) was a bit more complex. Despite the overall 6% decline, FFC/FFBL’s DAP sales surged 31% year-on-year to 37,000 metric tons, while Fatima Fertlizer reported a 225x yearon-year increase (albeit from a very low base).

Urea consumption has now fallen for three consecutive quarters, with offtake in the third quarter of 2024 down 17% year-on-year (1.5 million metric tons). Analysts attribute this to several factors.

The first of these is input cost inflation. Urea prices averaged Rs4,046 per 50-kilogram bag in January 2025, up 28% compared to average prices during fiscal year 2023. This now means that combined fertilizer costs consume 34% of wheat farmers’ production budgets

Then there are the declines in crop yields, accompanied by a credit crunch pushed by rising interest rates that have only recently started coming down. Cotton yields crashed 50% in 2024 due to pink bollworm outbreaks, slashing farmer incomes. And while overall farm credit did increase, it is highly skewed towards larger farmers and not the smaller farmers that form the bulk of farming in the country. Smallholders (<5 acres) received just 18% of fiscal year 2025’s Rs1.27 trillion agricultural credit volumes.

Meanwhile, it now appears that Engro Fertilizers may have been too hasty in withdrawing its Rs100 per bag dealer incentive earlier in January 2025. And gas price hikes – up 23% for feedstocks since July 2024 – may have been a contributing factor in plant shutdowns.

In the DAP markets, however, it is a more nuanced story.

In October 2024, Punjab’s Kissan Card initiative triggered a substantial 44% year-onyear surge in demand for fertilizers, equating to 309,000 metric tons. This demand continued to accelerate into November, as wheat sowing ramped up, pushing national offtake up by 95% year-on-year. However, by January 2025, a seasonal pullback in sales of 54% month-on-month masked an underlying structural demand that remained strong despite the temporary drop.

The agricultural sector is now facing serious concerns about an inventory glut. As of

January, stocks of DAP (Diammonium Phosphate) reached 141,000 metric tons, reflecting a 38% increase from the previous month and sparking fears of oversupply. The FATIMA Group’s DAP inventory surged threefold to 33,000 metric tons, signaling possible distribution bottlenecks within the sector.

One of the key policy interventions in recent months has been the Punjab government’s Kissan Card program, which has received mixed reviews. The Rs75 billion initiative, aimed at providing Rs 30,000 per acre interest-free loans for seeds and fertilizers, had disbursed Rs18 billion by January 2025, benefiting over 600,000 smallholders. Among these cardholders, DAP usage increased by 62% compared to non-beneficiaries.

However, critics argue that the scheme is flawed in its design, favoring Punjab’s wheat belt at the expense of other regions. Farmers in Sindh and Balochistan received less than 10% of the total credit, and the loan caps fell short of covering the full fertilizer needs of cotton and rice growers.

On the corporate front, the performance of major fertilizer companies has shown sharp divergence. The January 2025 urea sales data reveals that FFC/FFBL sold 194,000 metric tons, reflecting a 27% decline year-on-year, while EFERT's sales dropped 49%, totaling 107,000 metric tons. In contrast, FATIMA Group saw a 10% increase, with 108,000 metric tons sold.

EFERT's struggles have been particularly severe, with the company losing 8 percentage points in market share since FY2023. January 2025 inventory levels surged to 213,000 metric tons, marking a 74% increase month-on-month, and plant shutdowns in Q3 2024 resulted in 22 lost production days. Meanwhile, FFC has shown resilience by

capturing 38% of the DAP market, benefiting from Afghan transit trade deals, and reducing its reliance on urea from 62% to 51% of its revenue.

Looking ahead to the Rabi 2025 wheat season, which saw 8.9 million hectares of land being sown—up 4% from the previous year— market participants are grappling with a range of possible outcomes. In the best-case scenario, urea demand could recover to 650,000 metric tons per month by March 2025, with DAP offtake stabilizing at 85,000 metric tons per month, driven by import parity pricing.

However, a more pessimistic scenario sees smallholders cutting urea applications by 15-20%, potentially leading to a wheat deficit of 4.2 million metric tons. Additionally, the growing DAP inventory could prompt a 1015% reduction in prices, further complicating the outlook.

In response to these challenges, several policy measures are being proposed. First, the government could redirect Rs45 billion from fuel subsidies to offer targeted urea vouchers to farmers. A revamped Kissan Card 2.0 is suggested, expanding eligibility to 1.2 million farmers and offering crop-specific support packages.

To support the fertilizer sector, there is also a call for gas price rationalization, capping feedstock costs at $6 per MMBtu for fertilizer plants. Furthermore, aligning local DAP prices with global import parity pricing of $610620 per ton could help stabilize the market. With global urea prices rising 12% quarter-on-quarter and DAP affordability slipping, policymakers face a rapidly closing window to implement these interventions. Despite the challenges, there are still seeds of recovery in the sector, though urgent action is needed to nurture them. n

Pakistan’s steel industry is in crisis

The issue of quality standards is a question of very fundamental safety

By Ghulam Abbas

How can you be sure the house you live in is safe? Who guarantees that the apartments, homes, and office buildings you inhabit are constructed with durable, high-quality materials? Despite the significant sums spent on construction, many Pakistanis remain uncertain about the quality of the most fundamental building material: steel.

Shouldn’t this uncertainty concern us all?

These are the questions this article seeks to explore. What you may find startling is that a substantial portion of the 3.8 million tonnes of steel produced annually in Pakistan is of substandard quality. This revelation is not just a matter of economic concern but a pressing public safety issue.