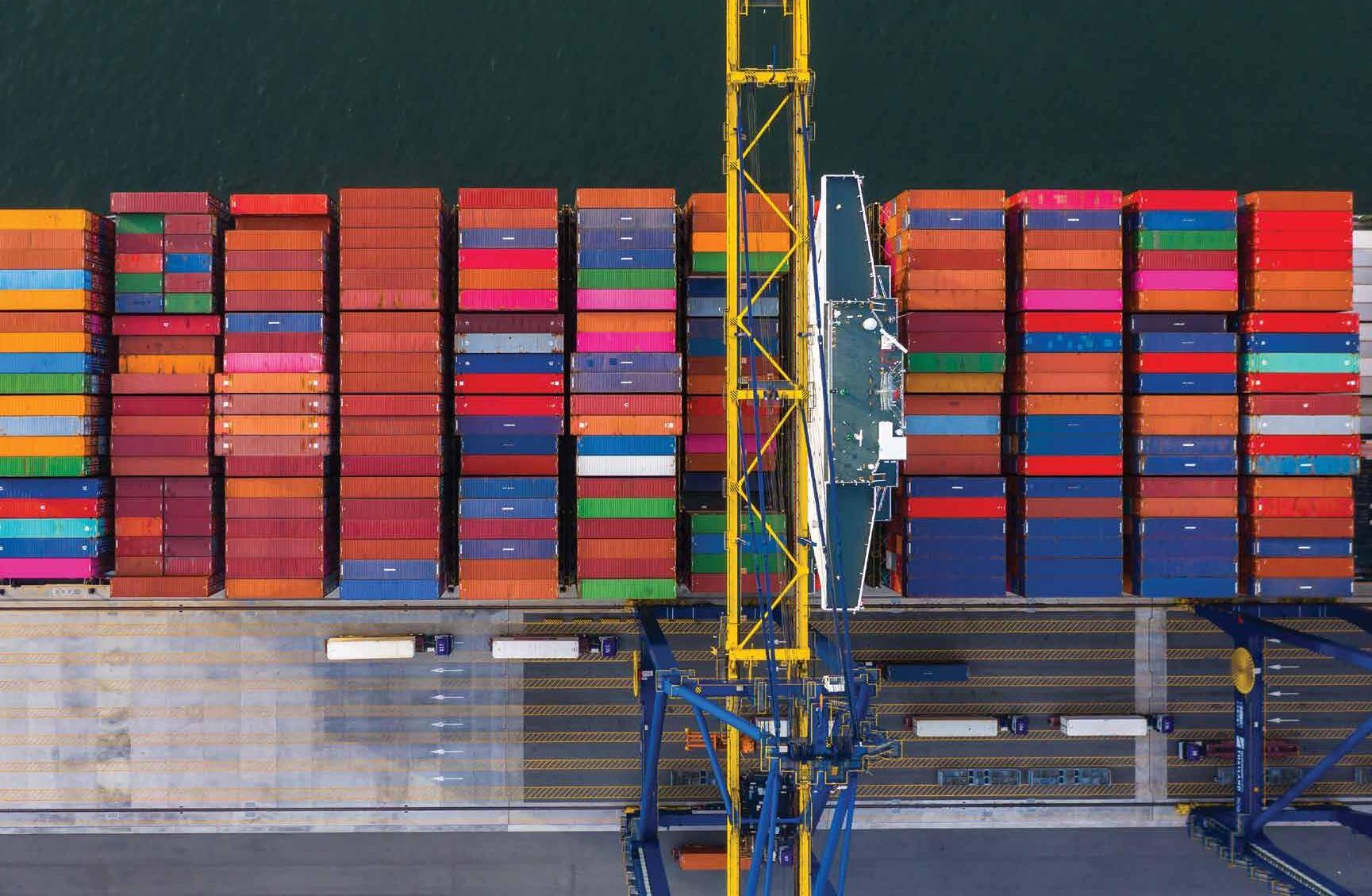

Lloyd’s continues its evolution From its maritime origins to the pandemic, and beyond PAGE 18 May 2023 • New Hampshire IN THIS ISSUE 5 An umbrella, E&S market update 9 Excess lines of power 25 Flood insurance coverage

Find out more at ConcordGroupInsurance.com We offer bundled coverages for Contractors with optional enhancements. From quotes to claims, The Concord Group has the tools to meet your customers’ needs. Build better insurance with bundled coverages for your small business customers.

COVER STORY

18 Lloyd’s continues its evolution From its maritime origins to the pandemic, and beyond

FEATURE 25 Flood insurance coverage

The E&S industry is ready to respond to the increasing need

Statements of fact and opinion in PIA Magazine are the responsibility of the authors alone and do not imply an opinion on the part of the officers or the members of the Professional Insurance Agents. Participation in PIA events, activities, and/or publications is available on a nondiscriminatory basis and does not reflect PIA endorsement of the products and/or services.

President and CEO Jeff Parmenter, CPCU, ARM; Executive Director Kelly K. Norris, CAE; Communications Director Katherine Morra; Editor-In-Chief Jaye Czupryna; Advertising Sales Representative Kordelia Hutans; Senior Magazine Designer Sue Jacobsen; Communications Department contributors: Athena Cancio, David Cayole, Patricia Corlett, Darel Cramer, Anne Dolfi, Kordelia Hutans and Lily Scoville.

Postmaster: Send address changes to: Professional Insurance Agents Magazine, 25 Chamberlain St., Glenmont, NY 12077-0997.

“Professional Insurance Agents” (USPS 913-400) is published monthly by PIA Management Services Inc., except for a combined July/August issue. Professional Insurance Agents, 25 Chamberlain St., P.O. Box 997, Glenmont, NY 12077-0997; (518) 434-3111 or toll-free (800) 424-4244; email pia@pia. org; World Wide Web address: pia.org. Periodical postage paid at Glenmont, N.Y., and additional mailing offices.

©2023 Professional Insurance Agents. All rights reserved. No material within this publication may be reproduced—in whole or in part—without the express written consent of the publisher.

May 2023 • New Hampshire

DEPARTMENTS 4 In brief 9 Tech 13 Sales 31 E&O 35 Ask PIA 38 Readers’ service and advertising index 39 Officers and directors directory

COVER DESIGN David Cayole Vol. 67, No.

May 2023

5

‘MARKET OF LAST RESORT’

Yesterday … Today … and tomorrow

E&S: The size of the market

The U.S. surplus-lines insurance market size was valued at $52.1 billion in 2019 and is projected to reach $125.9 billion by 2027, growing at a compound annual growth rate of 15.2% from 2020 to 2027.

Challenges facing E&S

New emerging risks and challenges for the E&S market, include the soaring cost of nuclear verdicts, social inflation, consumer inflation, cyberrisks, third-party litigation funding, human trafficking risks for hotels and motels, and climate change.

Coining terms and writing policies since the 17 th century

1. Appetite alignment. Is the carrier’s E&S offering a natural extension of its standard-line appetites?

2. Diversified offering. Does it offer a broad appetite across a variety of risk exposures supported by a diverse portfolio of products?

3. Service capabilities. Does the carrier offer a customer service center that manages small E&S policies as part of its standard- and specialty-lines capabilities?

4. Value-added solutions. Does it offer the option to access its products via a dedicated E&S underwriting team that can leverage in-house brokerage capabilities to provide added benefits to retail agents?

Laugh-related insurance?

Abbott and Costello took out an insurance policy for $250,000 to cover them if an argument split their team. Too bad the policy didn’t protect them from their break-up in 1957—when the IRS got them for back taxes.

Also, there is an insurance policy designed for comedians. It’s called Death by Laughter Insurance

Insuring

NESSIE?

In 1971, Cutty Sark, a whisky manufacturer, offered $1 million pounds ($2.4 million) to anyone who captured the Loch Ness Monster Then, asked Lloyd’s of London to underwrite the contest. The insurance company agreed, with one condition … it would get to keep Nessie.

The contract between Lloyd’s and Cutty Sark stated:

As far as this insurance is concerned, the Loch Ness Monster shall be deemed to be: In excess of 20 feet in length.

Acceptable as the Loch Ness Monster to the curators of the Natural History Museum, London

In the event of loss hereunder, the monster shall become the property of the underwriters hereon.

So, if you are in Scotland, and you manage to catch Nessie, give Cutty Sark a call. We hope the company kept its insurance policy.

4 PROFESSIONAL INSURANCE AGENTS MAGAZINE IN

BRIEF

Lloyd’s of London was established at a London coffee house in 1662

has insured everything from

to

and it coined the term underwriting

a reminder that everything is new and high-risk until it isn’t, the company: 2013 designed a policy to cover the dangers of crossing Antarctica 1965 created satellite insurance established aircraft insurance 1911 1904 underwrote the first auto policy

It

ocean cargo

celebrities’ body parts,

As

Four questions insurance agents should ask before partnering with an E&S carrier.

4

An umbrella, E&S market update: Inconsistency is consistent

Steve Levin, area president, Risk Placement Services

As 2022 ended, one thing remained consistent in the umbrella and excess & surplus casualty insurance marketplace: inconsistency. Very simply, the casualty market is being driven by a supply-and-demand shift in the excess casualty capacity.

The continuing lack of supply in the lead layer and the hazardous businesses has pushed up rates in this sector. However, there’s more supply than demand in the excess of $10 million, which has driven competition that’s led to program restructuring and rate stabilization—or in some cases, reductions.

On a macro level, the E&S market appears relatively consistent. However, on a micro level, it can be challenging to predetermine accounts that will be oversubscribed versus undersubscribed on capacity.

Before getting into some of the aspects driving the above, let’s do a quick recap of 2022—and discuss some initial thoughts from carriers regarding the year 2023.

2022 excess casualty insurance recap

• Average rate increases for the first 11 months of the year were in the 5-7.5% range, with a slight uptick in December.

• There is an abundance of capacity excess of $10 million, as we probably have close to double the carriers trying to deploy less capacity than the market had in 2019, which has led to competition and yearover-year rate reductions in some cases.

• Losses continue to come in, with carriers and reinsurers being vigilant on reserve amounts of prior years.

• Auto insurance loss costs have increased.

• Settlements on catastrophic claims continue to increase.

Initial excess casualty expectations for 2023

• Carriers are targeting rate increases of approximately 8% on their books, with most of the increase needing to come in the lead layer.

• There is slight uncertainty of treaty renewals (most excess casualty renewals happen between March and July).

• Claim inflation, medical inflation and legal inflation will continue.

• A significant amount of competition in excess of $10 million will continue.

Reinsurance impacts on the market

Since September 2022, there was a lot of talk about the challenges that property reinsurance renewals will have, but there hasn’t been nearly as much conversation on the casualty reinsurance side. While the casualty side isn’t expected to be nearly as difficult as the property side, a few different carriers have told us that they expect their treaty costs to go up in 2023.

There’s likely to be more scrutiny on underwriting diligence, and less support for those who are still trying to enter the umbrella and E&S marketplace. We’ve seen a few of the new market entrants pull back on writing new business or regrouping on their business plans. While this trend isn’t entirely tied to reinsurance, reinsurance is most likely a component, as reinsurers deploy their finite amount of capacity and look to balance underperforming sectors of their overall book.

Carrier creativity to offer additional capacity

During the third and fourth quarters of 2022, we witnessed a handful of carriers increase their participation in lead layers. This increase happened on lead $5 million placements that stretched to $10 million, lead $10 million placements that went to $15 million and most surprising was seeing lead $2 million placements on auto-driven exposure go to $5 million.

In doing some investigative work on these increases, we found that a few of these carriers were securing facultative reinsurance for the additional capacity they were offering. They undercut the market by eliminating their ceding commission and taking the capacity net/net. While this approach could be a good short-term business decision, we question if it’s sustainable for the long haul, and if the insureds that benefitted from these changes in 2022 will see higher-than-average increases in 2023.

On a similar note, carriers that were mitigating overall increases across their book had used the strategy of sometimes buying less treaty reinsurance and deploying more net capacity, therefore not passing as much of a cost increase onto customers. However, as losses continue to roll in, more reinsurance is being purchased with premiums likely to continue to rise—albeit not at the pace seen in recent years.

(continued on page 6.)

5 PIA.ORG NEWS TO USE

NEWS TO USE (continued from page 5.)

Large settlements are driving up costs for everyone

One of the biggest challenges the brokering community has had over the last three years is conveying to buyers why their pricing is going up, and why they are being penalized when they have never had a large claim. In 2022, we had a handful of insureds who incurred high settlements. In each instance, the insured never had a significant excess loss, and the settlement was higher than the previous high settlement for a similar claim in a similar jurisdiction.

The increase in claim settlements will continue to have an impact on market pricing, as it drives up loss costs, requiring carriers to increase rates to remain in business.

A look ahead

There are a lot of positives in the current umbrella and E&S marketplace, which we think will lead to more stable excess liability renewals for 2023 on a macro level. It’s important to keep the nuances of the market in mind when setting expectations with clients. Results probably will remain somewhat inconsistent on an individual account basis, and a small percentage of buyers won’t benefit from the same results as their peers. This abnormality can be driven by a small factor that has little to do with the individual insureds or a change in their risk profile, so ability to explain the macro-view of the market to relate to their individual account will be key to smoother renewals.

The most important things agents and brokers can do for their client is to secure accurate and comprehensive

renewal specifications and exposures to present to carriers; to communicate effectively; to involve all incumbent underwriters to get a better understanding of what they anticipate; and to leave plenty of time before the effective date, as the majority of the underwriting community doesn’t have the full authority they had in years past to make difficult decisions.

As always, the right specialty partner can make it easier for agents to come through for their clients in these market conditions.

Since 2015, Levin has served as vice president of the northeast region where he oversees five profit centers and 15 locations. Most recently, he was the branch manager of RPS Uniondale where he worked with the team to help triple the overall premium and revenue in a four-year time span. He helped recruit new producers and he was involved in getting a scratch office off the ground in Staten Island. Prior to his position at RPS, Levin was senior vice president at AON, where he managed the sales and marketing of the Travel Agents/Tour Operators Professional Liability program, and was involved in its overall growth. He has been recognized as Man of the Year by UJA Long Island Chapter and a recipient of RPS’s David E. McGurn Founder’s Award for significant contributions to the growth of the firm. He is an active supporter of the Juvenile Diabetes Research Foundation. Levin holds a BA in Economics from the State University of New York at Albany.

PROFESSIONAL INSURANCE AGENTS MAGAZINE 6

WE PICTURE THE WORST FOR YOU. WHOLESALE BROKERAGE | BINDING AUTHORITY | EXCLUSIVE PROGRAMS JencapGroup.com

Proudly serving quick service restaurants Workers Compensation Insurance • No volume requirements • Competitive rates • Multiple options for premium payments • Open to Shock Loss/High Mods Send in your submissions today. For more information contact a marketing rep at 844-761-8400 or email us at Sales@Omahanational.com. [ Coverage in: AZ • CA • CT • GA • IL • NC • NE • NJ • NY • PA • SC Smart. Different. Better. Omaha National Underwriters, LLC is an MGA licensed to do business in the state of California. License No. 078229. “A” (Excellent) rated coverage through Omaha National Insurance Company, Preferred Professional Insurance Company, and/or Palomar Specialty Insurance Company.

BRADFORD J. LACHUT, ESQ. Director of government & industry affairs, PIA Northeast

Excess lines of power

As a card-carrying nerd (see headshot above) I like to draw analogies between insurance and the nerdy stuff I love. As a huge Lord of The Rings fan—I have spent enough hours watching the Lord of the Rings movies that I’m now partially fluent in Entish—whenever I think about excessand-surplus lines of insurance, I think about Mordor. More specifically I think about Boromir’s iconic line about going to Mordor to destroy the One Ring, the Ruling Ring. For the non-nerdy, Boromir (played by the great Sean Bean), says this about trying to get into Mordor, the land of Sauron, the big bad of the Lord of the Rings trilogy: “One does not simply walk into Mordor. Its Black Gates are guarded by more than just Orcs. There is evil there that does not sleep, and the Great Eye is ever watchful.”

Much like Mordor, you do not simply place an insurance risk in the E&S marketplace. No. The admitted marketplace is guarded by laws and regulations. There are insurance departments in each state that never sleep and keep an ever-watchful eye to make sure risks are not being placed in the E&S marketplace illegally.

PIA.ORG 9

TECH

Declinations

How does one get to the E&S marketplace? As Boromir said we cannot simply walk. Instead, retail producers need to clear some legal hurdles—called the diligent-effort requirement. First, agents are required to put forth a diligent effort to place a risk in the standard marketplace before they can move to the E&S market. To satisfy this, most states require an agent to obtain a certain number of declinations—usually three—from authorized insurers. However, agents are not free to get three declinations from any three carriers. The declinations must pass the reason-to-believe standard that is used to measure the acceptability of the declinations. Under this standard, a retail

producer must show that there has been an objective basis for a producer’s belief that the authorized insurers declining the risk are in the business of writing the type or class of coverage. Producers may evidence this by a recent acceptance of a similar risk; advertising by the carrier; media or industry communications; or another valid basis. Many states require the retail producer— often in conjunction with the wholesale producer—to record and attest to the declinations, and then file it with the entity charged with monitoring the E&S marketplace.

There is a trick to avoiding this process—and it doesn’t involve riding on the back of a giant eagle. Before going over these hurdles, retail agents should first see if they even need to jump at all. Before going through the diligent-effort process, retail agents should look at their state’s export list, sometimes referred to as the white list. The export list identifies specific risks for which the state’s insurance department has waived the requirement for brokers to go through the diligenteffort requirement. Generally, the export list is used for risks that have been predetermined to be generally unavailable from authorized insurers.

E&O exposures

Once past the regulatory hurdles, producers are not in the clear. They must face an opponent more fearsome than an Uruk-hai: errorsand-omissions exposures! The E&S marketplace is difficult to get into because it is less regulated than the admitted marketplace. It is important to remember that many of the E&O exposures are because the companies and policies in the E&S market are regulated differently than

PROFESSIONAL INSURANCE AGENTS MAGAZINE 10

Please refer to actual policy for details. Policies are underwritten by Great American Insurance Company, Great American Insurance Company of New York, Great American Alliance Insurance Company, and Great American Assurance Company, authorized insurers in 50 states and the DC. Products not available in all states. © 2023 Great American Insurance Company, 301 E. Fourth St., Cincinnati, OH 45202 5637-AGB (05/23) Bow, NH 877.552.2467 aimscentral.co m TM FROM THE FARM AND RANCH PROFESSIONALS AT STOP STALLINGLET US QUOTE YOUR COVERAGE!

producers are used to in the standard market. That starts with the companies themselves.

Most producers have a stable of insurance companies they are familiar with and work with on a routine basis. That is not the case in the E&S market where retail producers most likely are not dealing directly with an insurance carrier at all. Instead, they are working through a wholesale producer, who is working with an E&S carrier that the retail producer may never heard of before. This lack of familiarity creates two issues for retail agents. The first is one of timing. Because a retail producer will likely utilize a wholesale producer to bind or make changes to a policy, there is an extra step in the process that could make it longer than in the standard world. Retail producers should make it a point to explain to clients that policy changes, including initial binding, may not happen immediately.

The second concerns the financial strength of the E&S carrier. Because these carriers are not regulated to the same level as admitted carriers, they may not be required to carry the same monetary reserves as admitted carriers. In addition, E&S carriers generally are not covered by state guaranty funds. This means that policyholders may have no safety net in the case of an E&S carrier falling into financial distress. This makes it essential that retail producers verify the financial strength of the E&S carriers that are insuring the risks.

Nonstandard forms

Retail producers also need to make themselves aware of the types of policies offered in the E&S market. Generally, nonadmitted carriers are not required to file or get approval of their policy forms from state insur-

ance departments. As such, the insurance products offered in the E&S market can be radically different than their admitted counterparts. Admittedly, that is part of the allure of the marketplace. It is a place where unique and different coverages can be found. In the quest for the unique and different though, retail producers should make sure they still are providing the base protections that would be provided in admitted policies.

The E&S policy not only serves as the best place to understand coverage, it also is the best place to find out what protections are in place for policyholders in the event of a policy termination. Many E&S policies—especially commercial policies—are not governed by the same rules regarding policy terminations as standard policies.

The amount of advance notice an E&S carrier is required to give in the event of an adverse action like a termination, as well as the form of the notice, often are different than those in the admitted world. While most states require at least 60-days notice of the cancellation of a standard-lines policy, an E&S carrier only may be required to provide written notice of 10 or 15 days.

Just as those who journey through Middle Earth can be faced with unexpected twists and turns, those retail producers who turn to the E&S marketplace to find coverage for their clients need to stay on their toes. However, as with any adventure, one is sure to find friends and allies to make the going easier. Make sure you have open conversations with your E&S carrier representatives, and allow for plenty of time for the binding process. Oh! And don’t forget your pocket-handkerchief.

Lachut is PIA Northeast’s director of government & industry affairs.

PIA.ORG 11

www.tagcobrand.com/pia Visit us at: New Member Benefit for Your Agency A 401(k) Program Done for You— Cost Effectively

Brooks Insurance Agency is proud to support Professional Insurance Agents (PIA)

Since its founding in 1991, Brooks Insurance Agency has successfully serviced the standard markets and brokered distressed and complex lines of business. We are here to help agents find the coverage their clients need.

We represent 80+ quality carriers, including several new and exciting markets, across the country. Plus, a broad array of products and services in admitted and non-admitted markets.

MARKET STRENGTHS AND EXPERTISE

• Broad market reach

• High-touch broker specialists

• Easy, online quoting process

• Collective approach to complex insurance needs

Visit our website at www.brooks-ins.com.

Brooks Group Insurance Agency, LLC NJ License 1575143

BROOKS IS YOUR FULL-SERVICE WHOLESALER How can we help you? Call us at 732.972.0600 or email us at info@brooks-ins.com © 2023 Brooks Insurance Agency, LLC is a wholly-owned subsidiary of Venbrook Group, LLC. All rights reserved.

JOHN CHAPIN President, Complete Selling

A frustrating problem costing you time and sales

Recently, I met with a new sales rep who’s been in sales for a little over six months. He’s made two sales—he should be closer to 30. I started by asking how many sales calls he’s been making, how many proposals he’s presented, what he’s been saying, and what his overall process has been. It didn’t take long to identify his problem.

Keep in mind that most prospects are trying to get rid of you. The average executives have 52 hours of work on their desks, and they get 200-300 emails a day along with 25-40 voicemails. Add that to their to-do list of 73 items (okay, I guessed on that one), but you get the point. Even if you aren’t calling on business owners or other executives, the average person still has more than ever on his or her plate along with a ton of distractions. Now imagine you enter the equation, looking for some of the prospect’s time. If the prospect is part of the 3-5% of people who needs you right now, you

Has your cluster lost its luster?

Alpha Northeast can bring it back.

Partnering with us means that you can grow your business and continue doing what you do best.

And, we’re an affiliate of the nation’s second largest insurance agency network, ISU Insurance Agency Network—so you’ll get to work with some of the best regional and national carriers around.

When you combine forces with us:

You’ll be eligible for a 100% commission payout from noncontracted carriers and profit share from first dollar.

You’ll have greater opportunity to maximize the benefit of networking with other agencies—which means more underwriting clout and increased profit share.

You’ll have access to the top national and regional carriers.

If you choose to leave the network, you’ll face zero penalty—but we bet you’ll stay.

might be okay—but that’s not usually the case. As a result, the prospect’s goal is to get rid of you as quickly as possible. Couple all this with the fact that the average person does not like to say no to other people, and you have a real conundrum.

The problem

So, let’s look at how this scenario plays out and where it may be causing you problems. You reach someone who is super-busy, who isn’t really

PIA.ORG 13

SALES

With Alpha Northeast, your agency will shine brighter than ever. And let’s be honest—you deserve it.

www.isu-alphane.com

interested in what you have, and he or she doesn’t like to say no to people. You hand the person a card and some literature as you introduce yourself and your agency.

The prospect peruses the information briefly and then says, “Looks great, give me a call next Tuesday.” You think you have a hot lead—and not wanting to lose the lead by irritating him or her with a bunch of questions—you agree to the next meeting and you’re on your way. You call next Tuesday, and you can’t reach the person. You leave a message and send an email. Both sound something like, “Hi, this is (your name with your agency). I stopped in last Thursday and gave you my card and some literature and you told me to call you back on Tuesday, so that’s why I’m calling you. Please call me back.” Ouch! Of course, the prospect didn’t call back. A few days later, you repeat the process. Nothing happens. You try several more times and still no response, the prospect is ghosting you. Now multiply this by the number of prospecting calls you’re making and the number of people who are busy, not really interested, and don’t want to tell you no, and add the fact that you keep chasing them anyway. The result: On a scale of one to 10, your frustration level is a 10.

What you should do

Obviously, when you talk to people you want to spark some interest by letting them know what’s in it for them to talk to you. Even the people who did have initial interest during your first interaction probably have forgotten about you by the time you follow up. When you do follow up, remind them why they might be interested, don’t just drop your name, and ask them to call you back.

To end the frustration, you must ask the questions necessary to determine interest, or lack thereof. Most salespeople have an aversion to asking direct questions. They are afraid they’re going to tick off the prospect and lose them. Please trust me on this one. You’re only going to tick off people who are lying to you about their interest because their goal is to simply get rid of you and it’s not working. If you come across as a professional who’s worthy of respect, and you make a proper connection, the truly interested people will be happy to answer your questions so that you can best help them.

Ask the right questions

What does it look like to ask the necessary questions to determine interest?

When someone says to call back next Tuesday, let the person know you’d be happy to do so, and find out why he or she wants you to call next Tuesday. When people ask for quotes or proposals, tell them you’ll be happy to get that to them and ask if they’re ready to move ahead if they like what they see. If they say yes, ask what they need to see. If they say no, ask what factors are preventing them from moving ahead, and refuse to do quotes for people who aren’t ready, willing, able to move forward now.

Ultimately, your questions are going to revolve around the when, what, why and how. When are the prospects looking to decide? What are they looking for specifically? Why are they looking for that, and why are they looking to buy when they are? And finally, how are they going to buy?

By how, I’m referring to their buying process along with how they will pay for the product. Regarding the buying process: Will they be looking at competitive products? What are the criteria to decide? Who is involved in the decision? And, how will they execute on their decision? The how behind the actual purchase may involve cash, financing, etc. Finally, close on every call—whether that’s closing the sale, or simply taking the next step in the sales process. Speaking of sales process, always make sure you are in control of it. Never be in a position in which it’s up to the prospect to get back to you. The ball always needs to be in your court.

When someone does say no

Some people will tell you no and they usually will do it with some attitude. These are the analytic personality types who would rather be right than happy and who like to fight with people. They are the exception, not the rule, and while we still want to question these people to see if their no is a smoke screen, we can thank them for not stringing us along.

Chapin is a motivational sales speaker, coach, and trainer. For his free eBook: 30 Ideas to Double Sales and monthly article, or to have him speak at your next event, go to www.completeselling.com. He has over 35 years of sales experience as a No. 1 sales rep, and he is the author of the 2010 sales book of the year: Sales Encyclopedia (Axiom Book Awards). Reach him at johnchapin@completeselling.com.

PROFESSIONAL INSURANCE AGENTS MAGAZINE 14

CP The Premins Company The Premins Company 132 32nd St., Ste. 408 | Brooklyn, NY 11232 • (718) 375-8300 (800)599-3279 • info@premins.com • www.premins.com 117742 1021 ✔ Credit cards for a flat $8.75 fee ✔ Debit cards for a flat $3.85 fee ✔ Free e-check ✔ Free check by fax ✔ Free auto bill pay ✔ Cash payments at CVS, Walmart and most 7-Eleven stores ✔ 24-hour online account access/management ✔ If you finance NYAIP apps, it’s time to go paperless with Premins Insurance Premium Financing with Unparalleled Payment Options Providing exceptional personalized service to the premium finance industry since 1965. OF INSURANCE PREMIUM FINANCING • OVER •

x x x x x Get your quote today! (800) 424-4244 | memberservices@pia.org Employee Benefits for Insurance Agencies Let the PIA Members’ Choice group benefits program take care of your agency. Medical Dental/vision LTD with Reliance Standard Term life with Reliance Standard PIA’s curated programs for member agencies and brokerages feature carrier selection, flexible coverage, top-notch customer service, and claims assistance when you need it.

The security you need . The name you trust . OUR PRODUCTS Businessowner’s Commercial Auto Commercial Package Commercial Property Commercial Umbrella General Liability Homeowners Personal Umbrella Professional Liability/E&O Workers’ Compensation Pay-As-You-Go options with hundreds of payroll partners! Not all Berkshire Hathaway GUARD Insurance Companies provide the products described herein nor are they available in all states. Visit www.guard.com/states/ to see our current product suite and operating area. APPLY TO BE AN AGENT: WWW.GUARD.COM/APPLY/

PROFESSIONAL INSURANCE AGENTS MAGAZINE 18

HANK WATKINS

R Regional director & president, Americas, Lloyd’s

ounded in 1688 at Edward Lloyd’s coffee shop in London, Lloyd’s is among the world’s longest continuously running commercial enterprises. Until the mid-1800s, the Lloyd’s market’s main business was the insurance of ships and cargos to and from ports around the globe. With developing economies came the need for innovative risk transfer solutions and the capital and distribution required to provide insurance and reinsurance capacity in a growing number of countries. For much of our history, the risks and the risk takers have been based in London. The risk-taking brokers have traveled the world—physically and virtually—in search of business opportunities for the market.

PIA.ORG 19

This access to the Lloyd’s market, which as recently as the 1980s was home to more than 400 syndicates writing most classes of business, still is facilitated by the more than 350 brokers registered by the Corporation of Lloyd’s to transact business on our platform. Based in London, they have for much of Lloyd’s history been the source of new and renewal business opportunities and remain key members of the Lloyd’s global ecosystem.

An overview

While most readers of this article access the Lloyd’s market via local wholesale brokers and managing general agents with binding authority from one or more syndicates (aka coverholders), these local distribution partners rely on

the expertise and experience of the Lloyd’s-registered broker to match policyholder needs with syndicate risk appetites. Depending on how the retail agent accesses the Lloyd’s market, policies are issued by the wholesale broker or coverholder and claims are administered according to the class of business. For example, property and some types of liability claims typically are handled by thirdparty adjusters, with cyber, management and professional liability and aviation claims assigned to specialist law firms.

You Joined

Market Leading RBT Program?

EverGuard, The Best Long-Term Partner For Your RBT Business.

EverGuard, is a superior Restaurant, Bar & Tavern market with 40+ years’ experience. Our continued longevity offering an uninterrupted market assures you will receive the best product underwritten by an AM Best “A” rated carrier without program interruptions.

EverGuard’s respected reputation in the RBT market speaks to our stability and reliability to provide industry-leading response time and customer service to our partner agencies.

• Exceptional service is an EverGuard priority

• Uncompromised program loyalty

• Great coverages at competitive pricing with available A&B, Enhancement Endorsement & more

• No limit on alcohol sales

• Package Policy: Property, GL & Liquor Liability

• Entertainment considered

• Experienced & Professional Staff

Determining how your client’s claim will be administered is an important step in placing coverage with Lloyd’s, particularly when multiple syndicates are supporting a delegated authority or open-market placement. The specialist nature of Lloyd’s, which in the U.S., is the largest surplus-lines market and a top-five reinsurer, often requires class of business expertise to ensure our promise to pay all valid claims—more than £25 billion (nearly $31 billion) worldwide last year—is met for you and your customers.

Going into 2023, the number of syndicates operating at Lloyd’s is less than a quarter of the roster occupying “boxes” in the Underwriting Room when the Titanic became the market’s largest loss to date or when, during the early to mid-1990s a combination of major losses including Hurricane Andrew, Piper Alpha and litigation in the U.S., related to asbestos and environmental exposures resulted in significant challenges to Lloyd’s solvency. Through a multiyear initiative known as “Reconstruction and Renewal,” the market recovered and it has transitioned since then from capital provided by individual names pledging unlimited responsibility for

PROFESSIONAL INSURANCE AGENTS MAGAZINE 20

Isn’t

Time

Bars, Taverns, Brewpubs, Comedy Clubs, Diners, Restaurants, Tasting Rooms… Michael Maher EverGuard

Michael@everguardins.com 1900 W. Nickerson St. Seattle, WA 98119 206.957.6576 | everguardins.com

It

the

Insurance Services VP, Business Development

EverGuard does not offer or solicit the program in the states of New Hampshire, Connecticut or Vermont.

losses generated by the syndicate(s) they supported to capital provided primarily by the insurance industry, pension funds and private equity. While the number of syndicates underwriting risk has significantly reduced, the capital backing them currently exceeds £100 billion (nearly $123 billion), providing the Lloyd’s market with the financial strength needed to withstand the increasingly damaging manufactured and natural catastrophes the world is experiencing.

A look at today

As the world’s largest specialist insurance and reinsurance market, the subscription approach to risktaking—particularly for large and complex risks—remains a pillar of the market’s success. While today there are fewer than 100 syndicates operating at Lloyd’s, they transacted insurance and reinsurance premium of £46.7 billion ($57.3 billion), roughly half of the premium written in the overall London market last year. More importantly, after several years of unprofitable experience related to the increasing volatility of natural catastrophes, the pandemic, geopolitical conflict and a misalignment between pricing and claims in some lines of business, the Lloyd’s market delivered a combined ratio in 2022 of 91.9% and underwriting profit of £2.6 billion ($3.2 billion). With profitability restored and a commitment by the corporation and market to maintain underwriting discipline in the years ahead, Lloyd’s is well-positioned to continue innovating and responding to the growing variety of risk scenarios facing the industry.

Supporting the market is the Lloyd’s Corporation, not in itself an insurer, but an independent organization

and regulator that provides oversight and standards aimed to protect and to maintain the market’s reputation around the world. We provide the premises from which the market operates, situated at One Lime Street in the City of London; approve syndicate business plans and capital requirements; evaluate their performance against business plans; hold the licenses they use to access business in more than 70 countries; manage rating agency relationships and the Central Fund—a £4 billion ($4.9 billion) backstop designed to protect policyholders, should a syndicate providing coverage be unable to pay a valid claim.

The U.S. and the U.K.

Given the complexity and size of the U.S. economy and longstanding relationship with the United Kingdom, it may not be surprising that the U.S. is Lloyd’s largest market. More than 45% of the market’s global premium was generated in the U.S. last year, with roughly two-thirds attributed to surplus lines and the balance to reinsurance. Property remains the largest class of business for Lloyd’s in the U.S., with significant capacity also dedicated to general liability, cyber, management and professional liability, aviation, marine, energy and transportation.

In the U.S., we provide several services to the syndicates including regulatory affairs, market development, claims advocacy, and media and public relations support. Working with leading business, academic and insurance experts, the corporation also contributes original research, reports and analysis to strengthen the market’s collective understanding of new and emerging risks.1 These reports are intended to provide insights to help agents and brokers respond to the challenges to which our industry actively seeks solutions.

The pandemic and other catastrophes

As the global economy emerges from the pandemic, inflationary pressures caused by supply-chain challenges and geopolitical tensions have led to stagnant economic growth in many parts of the world, with many economies facing possible recessions in 2023. From an insurance standpoint, the resulting pressure on price and the affordability issues for customers must be balanced with the risk of near-term price adequacy and long-term reserve resilience. This is a global challenge for the industry, one requiring constant attention to ensure we’re able to support policyholders through economic hardship and uncertainty.

Systemic risks are high impact, catastrophic events that could have detrimental impacts across multiple economies and territories. These risks are the most difficult to quantify, understand and mitigate as they often affect multiple industries, countries and sectors simultaneously. Examples of systemic risks include pandemics, climate change, large-scale cyberattacks and geopolitical conflict. In 2022, major economic losses continued to stem from events that were systemic in nature, including the conflict in Ukraine and extreme weather events including Hurricane Ian, record rainfall in California and the devastating tornado in Mississippi.

The potential scale of these events makes cross-societal collaboration essential. The insurance industry is preparing for their occurrence through exposure

PIA.ORG 21

management, capital modeling and scenario planning for a range of eventualities. We also are working closely with governments, regulators and other industries to share expertise, resources and networks to help protect society against future systemic events. At the same time, Lloyd’s is working to help the industry understand and assess the impact of systemic risks by generating innovative insights and insurance solutions2 and delivering products and services to the market.3

Flooding

In a world where catastrophic flooding is increasing in frequency, flood insurance premiums have become unaffordable for people and businesses in many high-risk locations. Some companies cannot secure cover at all. Lloyd’s has access to a program, developed by a recent graduate of the Lloyd’s Lab, that helps businesses thrive in a world of increased urbanization and climate change.

The program has built a new type of parametric insurance coverage for at-risk locations. One of the benefits of this type of insurance includes rapid payment of claims following a triggering event, in this case the level rising waters reach at an insured property. The fastest claim paid, to date, took just five hours and 36 minutes. This is game-changing for the catastrophic flood insurance market, which is rapidly growing because of climate change, and where traditional claims adjustment often can take weeks or months to settle.

A data-driven industry

The increased availability of data and analytics has had a profound impact on the insurance industry, facilitating the development of parametric solutions, many of which are available from surplus-lines carriers. The ability to collect, process and analyze quality data will continue to drive insurance industry competitiveness, as the benefits of having the right data capabilities are realized in better risk assessments and efficiency gains through automa-

Hiring made easy

tion. Ultimately, policyholders gain via more affordable protection and faster payment of claims. Lloyd’s is committed to creating a better, faster and cheaper market.4

Hopefully, this whistlestop tour of Lloyd’s has affirmed the commitment of the market and Corporation of Lloyd’s to delivering relevant, sustainable risk-transfer solutions via our distribution partners throughout the United States.

Watkins is responsible for the delivery of Lloyd’s strategy in the U.S., Canada and Latin America. From offices in Atlanta, Boston, Chicago, Dallas, Frankfort, Ky., New York, Montreal, Toronto, Bogota, Mexico City, Miami and Rio de Janeiro, Lloyd’s actively is engaged in educational and marketing outreach to retail, wholesale and reinsurance intermediaries, risk managers, MGAs and MGUs/coverholders and risk management programs at colleges & universities. It also provide claims, media relations and regulatory support to the Lloyd’s market throughout the region. Watkins has more than 35 years of experience in the insurance industry and has held a range of underwriting, client management and leadership positions in the U.S., and Europe at Chubb, Johnson & Higgins, Marsh and HRH. With more than 62% of Lloyd’s global premium in 2021, the Americas region is Lloyd’s largest market for insurance (E&S in the US) and reinsurance. For additional information, visit www.lloyds.com/en-us/ lloyds-around-the-world/us.

1 Lloyd’s Risk Reports (bit.ly/3TKbxUF)

2 Lloyd’s Futureset (bit.ly/3ZifJw8)

3 Lloyd’s Lab (bit.ly/3njK1kF)

4 Lloyd’s Blueprint Two (bit.ly/3LUWDt0)

PROFESSIONAL INSURANCE AGENTS MAGAZINE 22

To access, visit “Tools and Resources” at pia.org

Let

your

116225 919

PIA help with

staffing needs! We’ve created the Agency Staffing Assistance Program—an online member service that helps you find and keep good employees.

These are the Workers’ Comp Markets You’re Looking for! 2270-D-2022 Market Access Only With Your PIA Membership (800) 424-4244, ext. 318 | memberservices@pia.org | https://bit.ly/3Rpe5oc Provided in partnership with Agency Resources Scan to Get Started Hundreds of class codes A low-minimum premium Quick turnaround Simplified submission process Trusted carriers Competitive commissions Exclusive Features for PIA Members Painting Plumbing Restaurants Retail And, more … Auto Body Cabinet/Floor Installation Electrical Grocery/Deli/Supermarkets Landscapers Masonry Program Appetite Guide

PIA is here to help you navigate through uncertain times, so let’s make sure you have great errors-and-omissions coverage at a competitive price. We’ll Navigate Your E&O Coverage You Focus on Business Scan to learn more and get a quote. Call (800) 424-4244, ext. 408 | Web www.pia.org

PIA is the Best Choice for E&O • Our professional liability and cyber liability programs are designed for your agency’s needs and risk exposures • Critical coverage options—especially important when many agents are working remotely • Top-rated, stable E&O carriers • Experience & expertise from our team

Why

Flood insurance coverage

Congress is asking what can be done to increase the number of Americans who are purchasing flood insurance coverage, and the insurance industry is ready to respond.

In March 2023, the Housing & Insurance Subcommittee of the House Financial Services Committee hosted a hearing entitled, “How Do We Encourage Greater Flood Insurance Coverage in America?” To help answer that question, the subcommittee invited experts in the private flood insurance industry to talk about the issue. The Wholesale & Specialty Insurance Association was one of four witnesses invited to testify and provide the wholesale, specialty and E&S insurance industry perspective to answer the question. WSIA member, Patrick Small, president of DUAL Specialty Flood, testified at WSIA’s request.

The March 10 hearing was intended to help inform the subcommittee’s work on this issue over the next two years of the congressional session. Throughout the hearing there was one issue that the members of Congress and the witness panel continued to agree on: the National Flood Insurance Program needs a long-term extension

and must be financially stable. The subcommittee asked the industry witnesses questions about how to accomplish those goals for the NFIP, and it provided an opportunity to educate lawmakers about the industry’s perspective on how a stable NFIP helps bolster take-up of coverage for flood insurance in both the private market and the NFIP. The industry witnesses and subcommittee members also agreed on the need to bolster consumer education and about the risks of flood—not just in flood zones— and why more Americans should seek and/or accept the coverage. Wholesale, specialty and E&S insurance professionals work with their retail-agent trading partners to deliver a variety of flood coverages across the U.S., and they are eager to help provide educational tools to consumers.

History of private flood insurance and Congress

Congress established the NFIP in 1968 to make up for a lack of available flood insurance from the private insurance market. The program has enabled property owners in

PIA.ORG 25

BRADY KELLEY Executive director, WSIA

The E&S industry is ready to respond to the increasing need

participating communities to purchase insurance protection from the federal government. However, with the Biggert-Waters Flood Insurance Reform Act of 2012, Congress recognized the need and opportunity to encourage more active participation by the private insurance market and to encourage more Americans to purchase appropriate levels of flood coverage. WSIA, PIA and other industry experts continue to advocate for the role of private flood insurance as an option for consumers.

While WSIA and other industry trades were supportive of the Biggert-Waters Flood Insurance Reform Act, it took time for its reforms to facilitate growth in the private market. Those in the insurance industry believed a primary reason for that delay was a flawed and potentially confusing definition of private flood insurance that was adopted as part of the law. It lacked clarity for lenders issuing federally backed mortgages and introduced questions regarding if or when lenders could accept a private insurance policy to fulfill the mandatory purchase requirement for certain properties in specific flood zones.

To address that concern, stakeholders supported the Flood Insurance Modernization and Market Parity Act, first introduced in the 114th Congress as H.R.2901 and in the 115th Congress as H.R.1422. These bills would have revised the definition of private flood insurance to make clear that lending institutions could accept private flood insurance policies, including E&S policies to fulfill a property owner’s mandatory purchase requirement. Both bills unanimously passed the U.S. House, but never became law. However, clarification came in the form of The Final Rule for Loans in Areas Having Special Flood Hazards, issued in 2019 by five federal agencies overseeing lenders (i.e., the Federal Deposit Insurance Corp., the Office of the Comptroller of the Currency, the U.S. Federal Reserve, the National Credit Union Administration, and the Financial Conduct Authority). The Rule offered specific guidance and instructions to lenders that allowed them to accept private policies. The Federal Housing Administration issued a similar rule in 2022 that clearly states private insurance, including E&S policies, can be accepted in lieu of NFIP policies. These rules have opened significantly more options for property owners to choose from beyond only the NFIP. The agency rules have provided clarification that private flood policies are acceptable, but there were additional provisions in the legislation that would further improve the E&S market’s ability to provide coverage. Although the current definition of private flood insurance was adopted in 2012, it used outdated language and is inconsistent with the changes Congress made two years prior in the Nonadmitted and Reinsurance Reform Act. Updating it to include terms consistent with the NRRA, such as “eligible insurer” and “home state” are technical changes that are noncontroversial. WSIA continues to encourage Congress to consider this technical change and ensure consistent terminology in federal law.

Consumers need access to private flood insurance

With changing weather patterns, increasing frequency in catastrophic weather events and ongoing development in areas that are prone to flood events, the

need for adequate flood insurance coverage also continues to grow. Consumers can purchase flood insurance through the NFIP, but it is limited to $250,000 for residential and $500,000 for commercial property and is further limited to specific perils. These coverage limits often are insufficient for consumers. Often, insureds’ agents need access to the E&S market to offer solutions to consumers who need coverage beyond what the standard market or the NFIP can offer. These situations are where the E&S market can offer flexible solutions.

The good news for retailers is that leveraging a wholesale expert doesn’t increase the cost of the transaction to the insured. WSIA partnered with Conning Inc. to conduct an updated analysis of 2016-20 data investigating the non-loss cost of the wholesale transaction vs. retail transaction.

That analysis confirmed that wholesale distribution not only doesn’t increase the cost of the transaction to the insured, but that the cost of wholesale distribution was actually lower than retail distribution by 1.8 percentage points. There’s never a cost to obtain a wholesale quote, which makes it a logical step for retailers to investigate on behalf of insureds, and it can deliver tremendous added value.

The impact of the last 10 years

The 15 state E&S stamping and services offices (e.g., the Excess Line Association of New York) maintain policy data, including flood coverages. In an analysis of E&S flood insurance data, there is a positive correlation between E&S premium and the improved regulatory environment since the passage of the

PROFESSIONAL INSURANCE AGENTS MAGAZINE 26

Biggert-Waters Flood Insurance Reform Act. When looking at California, Florida, New York and Texas, which collectively account for nearly 50% of the U.S. E&S insurance market, E&S flood insurance premium has grown from $119 million in 2011 to $437 million in 2022, an average of 14% per year (see Chart 1).

The number of policies written in these states during that time has increased even faster. In 2011, there were only 11,653 E&S flood policies written in the four states mentioned in the previous paragraph; in 2022, more than 204,000 policies were written, an average increase of 33% per year. Most of those new policies were written on residential risks, giving more options to consumers, just as the Biggert-Waters Flood Insurance Reform Act intended (see Chart 2). Several states have taken specific actions related to E&S coverage that have allowed consumers’ agents to assess options more freely for their customers, including providing exemptions for diligent searches in a variety of manners, including:

Louisiana, Mississippi, Virginia, and Wisconsin—generally eliminated diligent searches for all risks.

Florida—generally eliminated diligent searches for commercial risks, except commercial residential. However, in compliment to its commercial flood exemption, Florida also eliminated diligent search for any residential flood risk.

Alaska, Arizona, Connecticut, Idaho, Iowa, New Jersey, Oklahoma, Pennsylvania, and Rhode Island—exempt all flood risks from diligent-search requirements, either by legislative or regulatory actions.

Six states provide diligent-search exemptions with certain stipulations, including:

California–excess coverage only

Maryland–excess coverage, only unless the NFIP is unavailable

Michigan–excess coverage only

Nevada–forced place coverage only

New Mexico–excess coverage only

New York–excess coverage only unless the NFIP is unavailable

Additionally, Oklahoma exempted flood insurance from premium tax, and Mississippi from state filing fees—allowing consumers some relief from additional expenditures related to these coverages. All these measures combine to provide more options to the consumer.

Opportunities for trading partners

The Housing & Insurance Subcommittee is comprised of members of Congress from across the country, each of whom have unique economic and geographical concerns to represent from their diverse constituencies; however, there is one thing that they all have in common—flooding.

The subcommittee will continue its work to implement NFIP reforms, create incentives to bolster take-up rates in both the program and private market, and implement modernizations to an outdated system.

PIA.ORG 27

2022 Stamping Office Flood Premium by Type Commercial Residential Uncharacterized 12.3% 41% 46.8% Chart 1 Commercial Residential Uncharacterized 8.4% 77.8% 13.8% 2022 Stamping Office Flood Policies by Type Chart 2

We have the solutions YOU

Now is the perfect time for PIA and WSIA members to partner to help increase this much needed coverage across their client bases. If you are looking for help with your privatemarket flood program—especially for your unique and difficult to place risks—contact your wholesale trading partner for options.

Kelley has served as WSIA’s executive director since August 2017, and he was previously National Association of Professional Surplus Lines Offices’ executive director since September 2011. As executive director, Kelley is responsible for the overall management of the association’s staff support activities, services to members and business operations. Prior to joining WSIA, he was the chief financial and business strategy officer for the National Association of Insurance Commissioners with oversight of the NAIC Finance Division, Products and Services Division, Technical Services Division and the NAIC Financial Regulation Standards and Accreditation Program. In this role, Kelley was responsible for all financial management and reporting, business strategy, risk management and compliance activities.

PROFESSIONAL INSURANCE AGENTS MAGAZINE 28 Industry Resource Center www.pia.org (800) 424-4244 resourcecenter@pia.org member inquiries QuickSource requests contracts reviewed tool kit hitsAsk PIA hits MarketBase™ requests

2405-D-2023 “I am so proud of being a PIA member!” —Robert Charles Robert Charles Brokerage Inc. “There is no way I could get by without PIA.” —Richard A. Mayo, CPCU Romay Insurance Services

1,724 4,955 3,8141,673 1,216 28

NEED PIA membership brings with it a wealth of benefits for the professional, independent insurance agent or broker—but the personal assistance of PIA’s Industry Resource Center alone is worth the investment.

Elevate Your Ethical Standards and Cyber Expertise

E&O Loss Prevention and Ethics^UN^FF

May 9, 2023 | 9 a.m. - 12 p.m.

Cathy Trischan, CPCU, CIC, CRM, AU, AAI, CRIS, ARM, MLIS, TRIP

This comprehensive course will guide you through the complex world of ethical responsibilities and decisionmaking in the insurance industry, while providing invaluable insights from an E&O perspective. With expert guidance and real-life examples, you’ll gain the knowledge and skills you need to make informed decisions and protect yourself and your clients from potential liabilities.

Cyber Coverage—Why the Need?

May 16, 2023 | 10 a.m. - 1 p.m.

Robin Federici, CPCU, AAI, ARM, AINS, AIS, CPIW

Cyber insurance coverage is a must when it comes to protecting digital assets. This session will provide you with the knowledge and tools you need to stay ahead of the curve and protect your organization— and your clients—from first- and third-party cyber security risks. From understanding the latest laws and regulations related to cyberliability, to exploring recent cyber insurance claims and insurance policies and endorsements, you’ll gain a deep understanding of this critical area of risk management.

Experience the Very Best Live, Online Programs with Our Expert Instructors—Reserve Your Spot Today ^UN^FF —E&O Loss Prevention credit approved by Fireman’s Fund and Utica National. Call the PIA E&O Department at (800) 424-4244 for details. PIA Members Save 50% Reserve Your Spot: pia.org/edu Call: (800) 424-4244

Stay on the cutting edge of HR laws and regulations

PIA HR Info Central offers:

• Points to consider when developing your agency’s personnel policy

• An administrator’s guide to assist your HR manager in job responsibilities

• Comprehensive job descriptions to tailor to your agency’s needs

• HR forms to customize

• Federal and state Labor Law information

• And more pia.org/IRC/hrinfocentral

Take our HR audit

The agency HR audit tool helps identify HR issues that may need special attention.

116316 1019

M. PEARSALL, CPCU, CPIA President, Pearsall Associates Inc.

What and when am I supposed to document?

Every errors-and-omissions claim that has ever been made has been impacted by the level of agency documentation in some way. Take the opportunity to educate staff members on what the expectations are for documentation. Document agency standards in writing for all employees to know, understand and follow to help avoid any confusion about those expectations. Be sure to include answers to the following concerns.

The when issue

What is the expected time period for when telephone conversations should be documented in the agency system? Avoid statements like “as soon as practicable” because this could vary by agency staff member.

Address the timeline for documenting meetings with customers, too. Ideally, document and take care of the task at hand by documenting immediately

following a conversation with the agency customer or prospect, as details become less clear as other tasks and conversations take place during the day.

The what issue

Issues include how coverage deletions should be handled, how and when to document when the customer declines a specific coverage, etc. The days of simply entering the discussion in the agency system are gone.

PIA.ORG 31 E&O

CURTIS

Steer Your Contractor and Used Car Dealer Risks to the Pros Turn to the folks that understand your clients’ businesses, deliver A- (Excellent) rated commercial auto and garage liability coverages, and provide the resources and support you need to achieve profitable growth. Business Auto Liability and Physical Damage • Contractors – Commercial Building, Electrical, HVAC, Painting, Plumbing, Roofing, Janitorial Services and more Garage Liability — Used Car Dealers • Dealer and Transporter Plates Writing in NY, NJ, PA, CT & OH* • Convenient Online Quoting • 24/7/365 Claims Reporting • Flexible Payment Options Contact us today: 516-431-4441 x3507 producer@lancerinsurance.com www.lancerinsurance.com * Please contact us for a list of available products and coverages by state

General pia@pia.org

Conference conferences@pia.org

Design + Print design.print@pia.org

Education education@pia.org

Government & Industry Affairs govaffairs@pia.org

Industry Resource Center resourcecenter@pia.org

Member Services memberservices@pia.org

Publications publications@pia.org

Young Insurance Professionals yip@pia.org

Those discussions must be memorialized in an email back to the customer and include the key information. There have been situations in which the customer—after suffering a loss—contradicts the information in the agency system. He or she may state “I told you I wanted the coverage” when you heard the opposite.

The how-much-detail-is-needed issue

What is the expected level of documentation of a phone conversation? Include the actual name of the customer, as opposed to “insured,” as well as sufficient detail of the exact essence of the conversation.

The documentation should be such that another agency staff member could read the documentation, know exactly what was discussed, and any next steps or open items.

The abbreviation issue

What abbreviations are acceptable and which words need to be spelled out? Note the list of acceptable abbreviations. If there is no abbreviation for a specific issue, then fully spell the issue.

The watch-what-you-say issue

A good rule for documentation: Don’t put anything in the system that a jury

The audit process

For agents who have an audit process in place, adherence to documentation expectations should be carefully reviewed.

For agents who don’t have an audit process, at a minimum, someone in a management position should review file documentation to determine if the staff is meeting expectations.

Auditing often (e.g., weekly, monthly) is a great way to reinforce positive behavior or conversely coach staff who are falling short of expectations. Strong file documentation will reduce errors and, if an E&O claim is made, favorable documentation will help in the defense of your agency. This is too important to leave to chance. As the saying goes: If it is not in the

Pearsall is president of Pearsall Associates Inc., and special consultant to the Utica

Utica National Insurance Group and Utica National are trade names for Utica Mutual Insurance Company, its affiliates and subsidiaries. Home Office: New Hartford, NY 13413. This information is provided solely as an insurance risk management tool. Utica Mutual Insurance Company and the other member insurance companies of the Utica National Insurance Group (“Utica National”) are not providing legal advice, or any other professional services. Utica National shall have no liability to any person or entity with respect to any loss or damages alleged to have been caused, directly or indirectly, by the use of the information provided. You are encouraged to consult an attorney or other professional for advice on these issues. © 2023 Utica Mutual Insurance Company

PROFESSIONAL INSURANCE AGENTS MAGAZINE

Email> Keep these addresses handy to reach PIA electronically

116889

Call Design + Print at (800) 424-4244, or email design.print@pia.org. The perks of working with Design + Print this spring: Rainy season brings flooding (and lots of it) Your insureds need to be prepared. When you work with us, you get the best, from the best, and all at a competitive price. Educate your insureds about flood insurance Inform your insureds about how you can help them maximize their coverage Collaborate with design experts to reach—and engage—your insureds effectively Send flood postcards that are attuned to your brand—and we’ll even mail them for you Choose us. 555 visit us a 123 Main Ave, Any own, USA 1 Rumqui qui ulpa po nus Tis in conse por millu secustrum consequos ma nos sequam quaepel ist itatiore vel mint quun volent doluptureped Title: Your logo here 555 Main St. Anytown, USA 12345 Visit youragency.com Or call (555) 555-5555 We’re here to help. Make an informed flood insurance policy decision with <Your Agency>. Get answers to your flood‑related insurance questions. Flooding is the most common (and costly) natural disaster in the U.S. An inch of water in your home can cost over $25,000 in damage. Homeowners policies exclude flood damage. Relying on just your homeowners insurance to cover hurricane or windstorm damage can be costly. Consider Flood Insurance Put your mind at rest with a hassle-free quote! Your logo here

Grow your book of business— offer the protection of Hartford Flood Exclusive online access for PIA members—Personal & Commercial Flood policies • Competitive commissions for PIA members • Multi-rater quoting system • Certified & accurate flood zone determinations • Dedicated sales director assigned to your agency The program is available to PIA members and their policyholders in all 50 states, the District of Columbia and Puerto Rico, and offers special PIA member commissions starting with the first sale (no minimums to qualify). Get started—contact The Hartford today. CT/NY—Art Brickley | (860) 547-2190 | a.brickley@thehartford.com NJ—Cheryl A. Maginley | (860) 547-5007 | Cheryl.Maginley@thehartford.com VT/NH—Michele Battis | (704) 972-5918 | Michele.Battis@thehartford.com

PIA TECHNICAL STAFF

Have a question? Ask PIA at resourcecenter@pia.org

Time-element exposures, joint ownership and more

Waiver of subrogation

Q. Can a commercial general liability policy insured waive subrogation in a separate contract without impacting coverage under the policy?

A. The policy’s “Transfer of Rights of Recovery Against Others to Us” provision implies that an insured—prior to loss—may waive rights against another party by separate agreement. This provision states that insureds must do nothing after loss to impair their rights to recover from others, to preserve them for the insurer to assume in a subrogation action.

If there is any doubt about the enforceability of the separate agreement, you may be certain of the outcome by using the Waiver of Transfer of Rights of Recovery Against Others to Us (CG 24 04) endorsement. The insurer agrees not to seek subrogation recovery from persons or organizations scheduled on this endorsement, regardless of the rights the insured may have.—Dan Corbin, CPCU, CIC, LUTC

Damage in transit–time-element exposure

Q. We insure a publisher who sends out copy of documents for layout offpremises. If the copy is damaged as it is being transferred via auto, the publisher could suffer a major loss of income. How do we cover him for his resulting time-element exposure?

A. Although the publisher’s work has insurable value and is subject to loss, the significant loss potential is with the missed deadline, resulting in thousands of dollars of lost revenue. The Insurance Services Office Inc.’s business income policy restricts its application to physical damage to property by a covered peril “at the premises described in the declarations, including personal property in the open (or in a vehicle) within 100 feet.” There is no in-transit coverage. Possibly, time-element coverage could be added by manuscript wording in the inland marine market. Shipments of new computer systems or production machinery to the insured’s business are other examples of similar income loss exposures. Loss of such items in transit could result in a time-element loss, just as surely as if the property were installed and operating at the time of loss.—Dan Corbin, CPCU, CIC, LUTC

Joint ownership coverage endorsement

Q. Could you clarify what the Joint Ownership Coverage (PP 03 34) endorsement to the ISO personal auto policy is designed to do?

A. A vehicle owned jointly by husband and wife is eligible for the personal auto policy without this endorsement and the policy includes both under its standard definition of “you” (i.e., the most privileged category of insured). The PP 03 34 endorsement changes the definition of “you” to mean two or more individuals (other than husband and wife) residing in the same household, or two or more nonresident relatives, who jointly own the insured vehicle. The endorsement is designed to provide coverage for persons who jointly own a vehicle and who are:

1. related (other than by marriage) and living in the same household (e.g., parents and children);

2. unrelated and living in the same household (e.g., roommates); or

3. related, but living in separate households (e.g., siblings sharing a pickup truck).

Worth noting is an exclusion to Part A–Liability Coverage that states:

PIA.ORG 35 ASK PIA

By phone …

We do not provide Liability Coverage for the ownership, maintenance or use of any vehicle, other than ‘your covered auto’ by any: 1) ‘nonresident relative’; or 2) ‘family member’ of a ‘nonresident relative.’

For example, if two brothers share a pickup truck together, their individually owned vehicles are not covered and would need to be insured under their own policies. These brothers also have no coverage for non-owned autos (i.e., rented or borrowed autos), which means a gap in protection if they do not have individually owned vehicles insured separately.

If the nonresident relative jointly owning the vehicle does not have an individually owned vehicle to insure separately, a named non-owner policy could be purchased to cover their use of non-owned vehicles. As an alternative, ISO introduced an option in the 2005 edition of the PP 03 34 endorsement to delete the exclusion and cover nonresident relatives and their families when using non-owned autos. If insurers are not reluctant to offer this option, it will be very effective in filling the coverage gap.

The Joint Ownership Coverage (PP 03 34 09/18) endorsement is used to alter the ISO personal auto policy in New Hampshire and Connecticut. A statespecific form (PP 13 36 04/19) is used by New Jersey; PP 03 78 01/20 is used in New York state; and PP 03 80 09/18 is used in Vermont.— Helen K. Horn, CIC, CPIA, CISR

Trigger for personal and advertising injury

Q. I’m confused by the various triggers for coverage used on an ISO Claims-Made Commercial General Liability form. Is Coverage B–Personal and Advertising Injury Liability subject to an occurrence or a claims-made trigger?

A. The trigger depends on which edition of the claims-made CGL policy form you are dealing with. In editions dated prior to 1988, Coverage B–Personal and Advertising Injury Liability had an occurrence trigger applying to “personal injury” caused by an offense committed during the policy period.

In forms dated 1988 or later, the offense must be committed after the retroactive date (if any) but before the expiration date of the policy. Coverage is triggered when a claim (arising from such offense) is first made during the policy period (or during any extended reporting period applicable to the policy).

—Dan Corbin, CPCU, CIC, LUTC

Health club professional liability

Q. From a coverage standpoint is it better to rely on the silence of a commercial general liability policy for professional coverage if it is not excluded? Or is it better to purchase a miscellaneous professional liability policy? The exposure is a health/athletic club. No exclusions apply.

A. For health clubs classified under general liability codes 44311 or 44315, the ISO rules instruct the insurer to exclude professional liability by attaching endorsement CG 22 76.

However, if the insurer does not add this endorsement, there will be coverage for the professional liability exposure.—Dan Corbin, CPCU, CIC, LUTC

PROFESSIONAL INSURANCE AGENTS MAGAZINE 36

(800) 424-4244 pia@pia.org pia.org

Online … PIA serves members.

PIANH Company Partners

Supporting Premier

As of publication date. For more information go to pia.org.

Sponsoring

DIGITAL

DIRECTORY Readers’ service and advertising index PROFESSIONAL INSURANCE AGENTS MAGAZINE Name Agency Address City/town State ZIP Phone Check advertisers of interest, complete form and mail to: PIANH • 25 Chamberlain St. P.O. Box 997 • Glenmont, NY 12077-0997. Or, fax (888) 225-6935. 38

10 Agricultural Insurance Management Services

11 Alpha Northeast

BC Applied Underwriters

17 Berkshire Hathaway Guard Insurance Companies

9 BioSurance

12 Brooks Insurance Agency

2 Concord Group Insurance

20 EverGuard

34 The Hartford

7 JENCAP

31 Lancer Insurance

8 Omaha National

11 PIA 401(k)

28 PIA Ad Solutions

22 PIA ASAP

33 PIA Design & Print

24 PIA E&O Insurance

29 PIA Education

32 PIA Email

30 PIA Industry Resource Center

16 PIA Members’ Choice Options

36 PIA Member Services

38 PIA Northeast Advertising

23 PIA NumberONE Comp Program

15 Premins Company

PIA.org • 10‑15,000 visits each month. PIA digital news • Distributed as a member-exclusive benefit. • Drive traffic to your website. Advertise with PIA Northeast PRINT PIA Magazine • Gives readers power to grow their business in a competitive marketplace. • Single- and multi-state options available. (800)424‑4244, ext. 231 Reach the insurance industry’s property/casualty segment

DIRECTORY

PIANH 2022-2023 Board of Directors

OFFICERS

President

Keith T. Maglia Insurance Solutions Corp.

60 Westville Road Plaistow, NH 03865-2947 (603) 382-4600

kmaglia@isc-insurance.com

Vice President

Jeffrey Foy, AAI Foy Insurance-Manchester

1889 Elm St. Manchester, NH 03104-2500 (603) 641-8111

jeff.foy@foyinsurance.com

Secretary/Treasurer

Casey Hadlock Hadlock Agency Inc. 150 Old County Road Littleton, NH 03561-3628 (603) 444-5500

casey@bestinsurance.net

Immediate Past President and National Director

Lyle W. Fulkerson, Esq.

HPM Insurance

101 Ponemah Road #1 Amherst, NH 03031-2816 (603) 673-1201

lyle@hpminsurance.com

ACTIVE PAST PRESIDENTS

Lisa Nolan, CPCU Cross Insurance 1100 Elm St. Manchester, NH 03101-1500 (603) 669-3218

lnolan@crossagency.com

John Obrey Obrey Insurance Agency Inc. 1B Commons Drive, Unit 13a PO Box 1018 Londonderry, NH 03053-1018 (603) 432-3883

john@obreyinsurance.com

(800) 424-4244 pia@pia.org pia.org By phone … Online … PIA serves members.

Workers’ Compensation • Transportation – Liability & Physical Damage • Construction Liability • Fine Art & Collections Homeowners – Including California Wildfire & Gulf Region Hurricane • Structured Insurance • Financial Lines • Surety Aviation & Space • Environmental & Pollution Liability • Real Estate • Reinsurance • Warranty & Contractual Liability Infrastructure • Entertainment & Sports ...And More To Come. MORE TO LOVE FROM APPLIED.® MORE IMAGINATION. ©2023 Applied Underwriters, Inc. Rated A- (Excellent) by AM Best. Insurance plans protected U.S. Patent No. 7,908,157. It Pays To Get A Quote From Applied.® Learn more at auw.com/MoreToLove or call sales (877) 234-4450