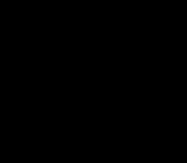

Help insureds mitigate the rise in private-security claims PAGE 16 IN THIS ISSUE 9 Best practices with claims 13 The talent shortage and claims 23 Claims process automation March 2024 • New York

NNt Discounts up to 35% Call us for a quote today at 800-556-8355 Get a quick estimate by visiting our website at www.LovellSafety.com Pricing Power, Dividend Prowess: Lovell Safety Management, Your Key to Financial Success Over $1.19 Billion in Dividends Issued to Date Lovell Safety Management Co., LLC 22 Cortlandt Street, 33rd Floor New York, NY 10007 212-709-8600 | 1-800-5-LOVELL www.lovellsafety.com Lovell Safety Management continues its track record of providing affordable workers’ compensation insurance coverage for the following industries: New Program Asbestos Abatement • Building Metal Trades • Cleaners • Construction • Electrical Manufacturers • Hospitals • Launderers and Cleaners • Municipalities • Painters and Decorators • Paper Products Manufacturers • Retail Lumber • Roofers and Sheet Metal Workers • Truckers, Movers, and Warehouse Workers

16

Help insureds mitigate the rise in private-security claims

FEATURE

23 AI: Claims process automation

What agents need to know

Statements of fact and opinion in PIA Magazine are the responsibility of the authors alone and do not imply an opinion on the part of the officers or the members of the Professional Insurance Agents. Participation in PIA events, activities, and/or publications is available on a nondiscriminatory basis and does not reflect PIA endorsement of the products and/or services.

President and CEO Jeff Parmenter, CPCU, ARM; Executive Director Kelly K. Norris, CAE; Communications Director Katherine Morra; Editor-In-Chief Jaye Czupryna; Advertising Sales Representative Kordelia Hutans; Senior Magazine Designer Sue Jacobsen; Communications Department

contributors: Athena Cancio, David Cayole, Jeana Coleman, Patricia Corlett, Darel Cramer, Matthew McDonough and Damon Whimple.

Postmaster: Send address changes to: Professional Insurance Agents Magazine, 25 Chamberlain St., Glenmont, NY 12077-0997.

“Professional Insurance Agents” (USPS 913-400) is published monthly by PIA Management Services Inc., except for a combined July/August issue. Professional Insurance Agents, 25 Chamberlain St., P.O. Box 997, Glenmont, NY 12077-0997; (518) 434-3111 or toll-free (800) 424-4244; email pia@pia. org; World Wide Web address: pia.org. Periodical postage paid at Glenmont, N.Y., and additional mailing offices.

©2024 Professional Insurance Agents. All rights reserved. No material within this publication may be reproduced—in whole or in part—without the express written consent of the publisher.

COVER DESIGN David Cayole Vol. 68, No. 3 March 2024 March 2024 • New York

COVER STORY

Prevent protects

DEPARTMENTS 4 In brief 9 Tech 13 Staffing 27 Connect 33 Ask PIA 37 Officers and directors directory 38 Readers’ service and advertising index

BRIEF

A LOOK AT LOSSES AND CLAIMS

FITCH RATINGS: SOME RELIEF FOR P/C INSURERS IN 2024

Fitch ratings released a report to indicate that the property/casualty insurers will see “some relief” in 2024 as “personal auto line recovery contributes to statutory profit improvement.” Ultimately, Fitch’s

outlook still is neutral, as 2023’s financial results

“reflect larger year-over-year underwriting losses and lower statutory earnings,” which in turn were due to poor performances from personal auto and

Fitch maintains that “following two years of large underwriting losses, auto results will show more material improvement as rate increases take hold and claims severity trends moderate, though a return, to segment underwriting profits is less likely. “Countering the auto rebound are continued challenges p/c insurers are facing in managing catastrophe exposures and loss-cost uncertainty in many segments amid higher inflation and growing claims

REFLECTING ON THE MAUI FIRE: LOSSES AND THE FUTURE

The Hawaii wildfires of 2023 are among the deadliest in United States history, predominately impacting the island of Maui and taking the lives of 100 people from the Town of Lahaina; four people still are missing. On top of the human cost and the damage to the environment, economic damages compound the suffering of the survivors. Data from the state Insurance Division indicates that 3,732 residential property claims were made; 1,683 were total loss claims. As of Sept. 30, 2023, $660.4 million of the total $1.29 billion in claims has been paid out to policyholders.

While the fires in West Maui and Upcountry were not as catastrophic, they were extremely costly. The former saw 1,400 total loss claims out of 1,985 personal motor vehicle claims; $21.6 million out of $25.3 million in claims has been paid out to policyholders. The latter saw 12 total losses against 299 residential property claims, and 25 total losses out of 63 personal motor vehicle claims: in total, this cost $32.6 million, with $16.3 million being paid out to policyholders (as of the time of this writing).

The cause of the Maui fires was due to drought conditions in the state—combined with unmanaged brush along the island’s power lines. Climate change, making the conditions in the state hotter and drier than average, set the stage for what could have been a more manageable wildfire into something devastating.

Independent agents should make sure that their insureds have adequate coverage in case they are victim to a wildfire, and it results in a total loss of property (home or auto). Drought conditions can turn even the unlikeliest of places into a tinderbox.

PROFESSIONAL INSURANCE AGENTS MAGAZINE 4

PROFESSIONAL INSURANCE AGENTS MAGAZINE 4

IN

.....................................................................................................................

.....................................................

THINKING ABOUT FLOOD CLAIMS

The National Ocean Atmospheric Administration has reported that in 2023, there were 25 natural disasters that exceed $1 billion dollars in losses. Two of these disasters were floods: The flooding in California from January to March, and the flooding in the Northeast in July, the total cost of all disasters in 2023 is at $81 billion-with floods costings $6.8 billion.

March marks the start of spring, and with spring comes increased rain and melting snowpack across the country. In the Northeast, we start to see an uptick in precipitation that lasts until about August. While every spring shower isn’t a flood, it does bring flooding damage: Some neighborhoods and towns are susceptible to rainfall, while the rest of the country and state tick along like business as usual.

It’s important to talk to clients about flood insurance, and how it’s seperate from their homeowners policy. Flood insurance is offered through private, state and government entities, notably through National Flood Insurance Program under the Federal Emergency Management Agency.

While floods weren’t the costliest disasters of 2023, they still made a significant impact on homes and communities. Make sure that your clients are protected adequately from spring showers that turn into torrential downpours.

HELPFUL TIP:

Be clear about the process of your client’s auto claim. This should help to keep them satisfied. After all, overpromising and underdelivering is sure to earn their ire. Especially when it is for as something as important as their vehicle.

• Overall satisfaction for claims was at 878 on a scale of 1,000 - a five-point increase from 2022.

• The average repair cycle from first notice of loss is at 23.1 days. This is a 6.2 day increase from 2022; prepandemic repair times were 12 days on average.

TRENDS IN AUTO CLAIMS

If you’ve spoken to your insureds about their automobile after an accident, you may have noticed that the length of the repair times have significantly gone up. However, as you talk shop with your fellow agents, you also may have noticed that insureds satisfaction has overall stayed the same (as satisfied as they can be waiting for their car to be fixed). These two factors don’t seem like they should correlate, so what gives?

J.D. Power and Associates investigated this phenom in its 2023 U.S. Auto Claims Satisfaction Study, and found that this wasn’t just some anecdotal trend, but a statistical fact. While one would think longer wait times would annoy insureds, its tempered by the fact that they’re given realistic expectations and transparency about what happens to their vehicle next. The only area for improvements that J.D. Power notes is that customers were dissatisifed with their rental car experience: Some had a rental car for so long that they started to incur out-of-pocket costs.

PIA.ORG 5 WWW.PIA.ORG 5

.............................. .............................. ..............................

* *Calculations are not yet finalized, and total costs have not been determined.*

Break down: Anatomy of a personal auto claim

By Theophilus Alexander, government & industry affairs specialist, PIA Northeast

Have you had to talk a client out of ignoring a claim? Sometimes examples are the best teaching tools. PIA Northeast’s Government & Industry Affairs Specialist Theophilus Alexander shares an experience he had with a claim (prior to joining PIA). Perhaps it’s a lesson your clients can learn too.

The story

I have been unfortunate enough to experience an insurance claim. A hit-and-run fender bender left my car with minor, front-end damage. Afterward, like most people, I filed a claim with my insurance company.

Once the claim was in motion, the insurance carrier suggested I take my car to a Guaranteed Repair Network shop. Its appeal lay in benefits like repairs performed by certified technicians and warranties on the repairs extending for as long as I owned the car. Enticing, right? Well, I was sold. So, I went to the collision repair shop. While there, the technician scanned my car’s VIN, assessed the collision damage and handed me a quote.

Where the story gets juicy

Picture me, a young adult facing a $500 deductible that at the time seemed like too much money to fork over. The car was drivable, and the damage was minor—which I thought wouldn’t affect anything—so I ignored the situation. I did not think about any possible consequences.

To my surprise, at my next insurance renewal, the premium increased. Without the proper guidance— because I did not have a professional insurance agent— not only did I file a personal auto claim unnecessarily, but I neglected to cash the claim check and repair the car, which resulted in a premium hike. It all happened because I assumed filing a claim was necessary without fully understanding the details of my policy.

What should have happened

No. 1: File a police report. In case of injury, call or text 9-1-1 or have someone else do it. If you are seriously injured, avoid moving and wait for emergency responders. If you can move, check on your passengers. For nonemergency fender-benders, use the police department’s nonemergency phone number.

No. 2: Document the scene of the accident. Immediately after an accident, capture crucial evidence by taking photos of the scene and vehicle damage. If you have a dash camera or cloud-based footage of the accident, maintain that documentation, which will serve as visual evidence, establish the sequence of events and determine which party is liable.

No. 3: Exchange contact information. After ensuring your safety and that of your occupants, and other parties involved (if possible), exchange contact and insurance information with all involved parties, be sure to collect the: 1. full names and contact information; 2. insurance company and the policy number; 3. the driver’s license and license plate number; 4. color, make and model of the vehicle(s) involved; and 5. the location of the accident.

No. 4: Review your insurance coverage. Before you file a claim, understand your coverages, limits, exclusions and deductibles. Reviewing your policy before contacting your insurance carrier will save you time and avoid filing a claim for a loss that isn’t covered, or where the cost of the repairs is less than your deductible or could be an outof-pocket expense. Your insurance agent can help.

No. 5: Contact your insurance company. After you’ve determined whether the damage to your car is covered, you need to file your claim with your company. Work with your independent agent. Make sure you have the information related to your claim, including the date of loss, police report, photographs or videos of the damage, medical bills for injuries, and other documentation.

No. 6: Prepare for insurance adjuster. Some insurance companies may send an adjuster to inspect your car and see what damage was sustained during the accident. Other insurance companies may require you to obtain an estimate for repair costs. The repair shop will assess the damage and send the report to the insurance company.

No. 7: Receive the claim payment and repair the vehicle. When it comes to receiving the claim payment and paying for the vehicle repairs, it may be dependent on the practice of your insurance company. Some insurance companies pay for the repair shop directly, and other companies pay and allow you to handle the bill.

The lesson

My personal auto claim journey underscores the importance of navigating the personal auto insurance claim process with vigilance and informed decision-making. The aftermath of an accident is an event we all hope to avoid, but when faced with the unexpected, understanding the intricacies of filing a claim become paramount.

This article is adapted from “Break down: Anatomy of a personal auto claim,” which can be read in its entirety on PIA Northeast News & Media (blog.pia.org).

PROFESSIONAL INSURANCE AGENTS MAGAZINE 6 NEWS TO USE

Serving the companies that build America and keep it running Workers Compensation Insurance • No volume requirements • Competitive rates • Multiple options for premium payments • Open to Shock Loss/High Mods Send in your submissions today. For more information contact a marketing rep at 844-761-8400 or email us at Sales@Omahanational.com. [ Coverage in: AZ • CA • CT • GA • IL • NC • NE • NJ • NY • PA • SC Smart. Different. Better. Omaha National Underwriters, LLC is an MGA licensed to do business in the state of California. License No. 078229. “A-” (Excellent) rated coverage through Omaha National Insurance Company, Preferred Professional Insurance Company, and/or Palomar Specialty Insurance Company.

BRADFORD

BRADFORD

Best practices to assist clients during the claims process

Rarely is the role of the insurance agent or broker ever more important to a client than when that client has experienced a claim. Guiding clients through the claims process is a critical component of the agent’s or broker’s job. It involves not just a deep understanding of the

but also a compassionate approach to client management.

However, navigating the claims process can be tricky. Between communicating with your client, carriers and third parties to managing client expectations, the claims process quickly can become a quagmire for agents. Let’s outline some best practices for assisting clients during claims, highlighting how to facilitate a smooth process while minimizing the possibility of an errors-and-omissions claim.

Can you hear me now?

Effective communication with your clients is perhaps the single most important aspect of successfully managing a claim. Always keep them informed about each step of the claims process. Remember typically clients will have little, if any, experience with insurance claims.

PIA.ORG 9 TECH

J. LACHUT,

&

PIA Northeast TRAVEL AGENTS AND TOUR OPERATORS PROFESSIONAL LIABILITY PROGRAM Partner with Aon Today! 45+ years serving the travel industry • Brokers - No minimum premium volume requirements to place business in this program • Recognized industry partner with top national travel associations • Custom policy specifically designed for the travel industry Professional Liability Insurance for: • Travel Agents and Travel Agencies • Standard Tour Operators • Student Tour Operators • Adventure Tour Operators • Receptive Tour Operators • Destination Management Companies • Meeting Planners (Corporate) Policy Includes: • Worldwide Territory • General Liability • Errors & Omissions • Non-owned & Hired Auto • Personal Injury • Industry specific endorsements Learn more at www.aontravpro.com/broker

ESQ. Director of government

industry affairs,

policies,

They will be relying on you, the insurance professional, for guidance and pertinent updates.

Explain the timelines, the paperwork involved, and what they can expect during each phase. Encourage questions and provide clear, concise answers. Remember, what seems obvious to you might be completely foreign to your client. Included in good communications, is being clear with your client about expectations both in how long the claim might take to be settled and the ultimate cost of the claim.

Flex your brain

Your clients are going to turn to you—the insurance professional— to answer their questions about their insurance policies. Because of this, you need to have an in-depth understanding of your clients’ policies. This knowledge allows you to set realistic expectations about what is covered and what is not. Be prepared to explain policy terms in simple language and how they apply to the current claim. Remember: While you may be the expert, it’s OK to not have all the answers. If you don’t know the answer to your clients’ questions, tell them that. Then call PIA Northeast, so we can help you find them.

Document, document … and document!

Documentation is your best defense against E&O claims. In your agency, you should have a firm documentation policy that incorporates claims coming from multiple sources. And, you need to make sure that all of your team members are familiar with, and follow each policy.

The documentation policy for a claim reported over the phone might be different than the procedure for a claim reported via email. It also is important to have a policy on submission of a claim through social media. Many agencies utilize social media to connect to their clients, however agents may not want clients to conduct official business—like submitting a claim—through social media. Keep detailed records of all communications, including emails, calls and meetings. Document advice given, decisions made and actions taken. This will be invaluable if there’s ever a dispute about the handling of the claim.

PROFESSIONAL INSURANCE AGENTS MAGAZINE 10

Please refer to actual policy for details. Policies are underwritten by Great American Insurance Company, Great American Insurance Company of New York, Great American Alliance Insurance Company, and Great American Assurance Company, authorized insurers in 50 states and the DC. Products not available in all states. © 2024 Great American Insurance Company, 301 E. Fourth St., Cincinnati, OH 45202 5647-3-AGB (03/24) Bow, NH 877.552.2467 aimscentral.co m TM FROM THE FARM AND RANCH PROFESSIONALS AT THIS ST. PATRICK’S DAY, GET COVERAGE THAT SHAMROCKS!

Be an advocate

There are few times more stressful for a client than in the immediate aftermath of a loss. While agents must adhere to the terms of the policy, as well any agency agreements with insurance carriers, advocating for your client’s best interests within those parameters is essential. This includes negotiating with adjusters and ensuring the claim is processed fairly and promptly. Demonstrating empathy and understanding for your clients can go a long way in building trust and easing client anxiety. Listen to their concerns and acknowledge their feelings.

Be a teacher

Use the claims process as an educational opportunity. The best claim is the one that never happens. In the aftermath of a loss, take the time to educate your clients about risk management and prevention strategies. Discuss common risks associated with their policy type and provide tips on how to mitigate them. For instance, if a client has just faced a burglary claim, offer advice on security improvements or alert systems.

This proactive approach in teaching clients about potential risks and how to avoid future claims not only helps them in the long run, but it also cements your role as more than just an insurance agent; you become a trusted adviser and a resource for preventive strategies.

Additionally, consider providing regular informational resources, such as newsletters or workshops. These help to keep your clients informed and engaged in managing their risks effectively while simultaneously keeping your agency at the front of the client’s mind. Did you

know that you can purchase personal-lines and commercial-lines newsletters through PIA, which can be sent to your clients to keep them informed of various exposures that they may have, and also serve as an E&O prevention tool for your agency? For more information, contact PIA Design & Print at (800) 424-4244 or design.print@pia.org.

Build your network

Building relationships with adjusters, appraisers and other insurance professionals is more than just a professional courtesy; it’s a strategic move that can enhance the claims process for your clients significantly.

By having a robust network, you can expedite claims, access expert opinions quickly, and find solutions to complex claim issues more efficiently. These relationships allow for smoother negotiations and better understanding among professionals, which ultimately leads to more favorable outcomes for your clients. Regularly engage with your network through PIA events, professional groups, and ongoing communication to keep these relationships strong and mutually beneficial.

Conclusion

Handling client claims effectively is a blend of technical skill, thorough documentation, empathetic client management and relationship building. By following these best practices, you can enhance client satisfaction, foster longterm relationships, and uphold a high standard of professional service.

Remember, your role in guiding clients through the complexities of the claims process not only helps them navigate a difficult time, but it also strengthens the trust and credibility of your agency.

Lachut is PIA Northeast’s director of government & industry affairs.

Hiring made easy

Let PIA help with your staffing needs! We’ve created the Agency Staffing Assistance Program—an online member service that helps you find and keep good employees.

PIA.ORG 11

To access, visit “Tools and Resources” at pia.org

116225 919

132 32nd St., Ste. 408 | Brook ly n, N Y 11232 • (718) 375-8300 (800) 599-3279 • info@premins.com • ww w.premins.com Licensed in NY-NJ-PA-FL-CT-OH PROVIDING EXCEPTIONAL PERSONALIZED SERVICE TO THE PREMIUM FINANCE INDUSTRY SINCE 1965 The Premins Company CP INSURANCE PREMIUM FINANCING WITH UNPARALLELED PAYMENT OPTIONS Credit Cards For a Flat Fee of $9.19 Up To $5,000 Debit Cards For a Flat Fee of $4.04 Free E-Check • Free Auto Bill Pay Cash Payments at CVS • ACE • Walmart • Walgreens • 7-Eleven 24 Hour Online Account Access/Management Specializing in Personal • Commercial • Excess • Assigned Risk All Trademarks and Logos are Property of Their Respective Owners

JULIE CIRILLO, ESQ. Chief risk officer, Engage PEO

JULIE CIRILLO, ESQ. Chief risk officer, Engage PEO

Is AI the answer to talent shortages in claims?

Talent shortages continue to rank in the top 10 concerns of insurance industry stakeholders.1 According to the U.S. Census Bureau 12,000 people per day will turn 65 in 2024, calling this milestone “Peak 65.” Peak 65 is expected to lead to talent shortages in the insurance industry. The U.S. Bureau of Labor Statistics suggests that the industry could lose around 400,000 workers through attrition by 2026. While technology and artificial intelligence can have great impact on the operational and underwriting activity of insurance companies, claims maybe the holdout area where people will continue to be inherently necessary, especially when it comes to workers’ compensation claims. AI is only part of the answer.

Why claims need humans

When employees get injured, it is an inherently personal experience. Injured employees may not know how they will get paid or put food on the table for

their family. They are struggling to coordinate medical care, and likely they are in pain and potentially heading down the path of depression. They want and need to talk to a person, a compassionate person—not a chatbot or frustrating electronic answering decision-tree system. When an injured employee does not get a compassionate person on the other end of the phone at the insurance carrier or third-party administrator, he or she could call

We have an appetite for small business.

The

The affordable price your clients deserve

We’ve been successfully protecting small businesses since 1983.

PIA.ORG 13

STAFFING

Browse

of our products at www.guard.com.

all

traditional coverage your clients need

The customized options your clients desire.

.

someone who does care—an attorney who could drive the cost of that claim significantly higher.

Getting a good outcome on a workers’ compensation claim is dependent on the knowledge, experience and tools that are available to the adjusters handling the claim. It takes all three components to manage the claim, and the pending shortage of highly knowledgeable and experienced adjusters is a concern for employers, agents and carriers, as it could lead to rising claim costs.

I had the opportunity to consult with a client on a potential work-related death claim, in which due to the circumstances, the claim was going to be denied. We surveyed multiple adjusters who were handling our claims to choose the right adjuster with the compassion and personality traits to be able to explain to the widow why the claim was being denied and what other avenues she could take to seek reimbursement. We did not choose the adjuster who was handling the claim initially. The conversation went well, and the widow never hired an attorney and she did not challenge the denial.

The wrong communication could have resulted in extensive litigation costs.

The sweet spot for AI

While AI can’t replace the knowledge and experience for how to approach and handle the personal aspects of a workers’ compensation claim, it can be built into the tools available to adjusters to use. Integrating AI algorithms into the claims system to scan the data and identify potential problem claimants, or complex injuries needing complex medical treatment—then leveraging AI assistance to guide and direct an adjuster to available medical resources or even implementing those resources proactively—will help the adjuster to manage the claim. It also will build efficiency on the adjusting team and ultimately curb costs.

How to de-risk carrier/TPA selection

In any request for proposal, it’s important to have a clear understanding of the tools available to the adjusters. The third-party administrator can wow an employer with all the bells and whistles of an employer-facing risk management information system, but then fail to invest in the system that the adjusters use. This makes the adjusters’ job even harder and longer. I recommend that part of the process include sitting at the desk of an adjuster to understand the tools and resources available that make their jobs easier.

In my view, it also is critical to review the use of AI and technology in claims management. A critical question is whether the adjuster has an integrated AI claims mitigation program. The key to look for is that the AI results and guidance requirements are built into the claims system and require action from the adjuster.

There are two types of AI in claims systems—one that is integrated and another that just sends an email to the adjuster, which the adjuster is not required to act on, and that he or she can ignore. In today’s claims world it is not enough for the AI system to flag a claim red, yellow or green. The AI tool should be interactive with the adjuster—producing real results that are actionable with process and workflow activities, which trigger based upon the result.

For example, AI could review data pertaining to a claim and issue or restrict payments automatically, or request medical records, or assign a nurse case manager or peer review, because the claim was flagged as red. Or AI could scrub the pharmaceutical data to identify medicine overuse or incompatible medicines prescribed in claims, and request peer-to-peer intervention between the pharmacy benefit manager and the treating physician. Using AI to assist and guide adjusters will bring efficiency to their work, and it has the potential to allow adjusters to carry a higher case load.

As the industry faces an impending shortage of claims adjusters, it would be foolish to think we can replace the personal aspect with chatbots and electronic decision trees. Some claims require a personal touch and the knowledge and experience of a seasoned adjuster. Then, we must supplement those skills with technology and AI to bring efficiency to the adjusting process, and improve the process so we can do more with fewer adjusters.

Cirillo is the chief risk officer for Engage. She is a seasoned veteran in the workers’ compensation industry, with more than 20 years of experience in workers’ compensation litigation, claims management and risk management. She is a former workers’ compensation defense attorney and has held multiple senior roles in management, claims, loss prevention, risk management and sales. Cirillo earned a Bachelor of Arts from the University of South Carolina-Columbia and a Juris Doctor from the University of Pittsburgh School of Law.

1 Risk & Insurance, 2023 (tinyurl.com/n2vwu9td)

PROFESSIONAL INSURANCE AGENTS MAGAZINE 14

These are the Workers’ Comp Markets You’re Looking for! 2270-D-2022 Market Access Only With Your PIA Membership (800) 424-4244, ext. 318 | memberservices@pia.org | https://bit.ly/3Rpe5oc Provided in partnership with Agency Resources Scan to Get Started Hundreds of class codes A low-minimum premium Quick turnaround Simplified submission process Trusted carriers Competitive commissions Exclusive Features for PIA Members Painting Plumbing Restaurants Retail And, more … Auto Body Cabinet/Floor Installation Electrical Grocery/Deli/Supermarkets Landscapers Masonry Program Appetite Guide

PROFESSIONAL INSURANCE AGENTS MAGAZINE 16

RICHARD G. RANDAZZO President, Brownyard Claims Management

Help insureds mitigate the rise in private-security claims

nsurance claims, specifically general liability claims, are on the rise in the private-security industry. This comes as no surprise to those familiar with private-security work. Several factors driving this phenomenon, include economic challenges, rising tensions across the country and the steep increase in gun violence over the past decade.

PIA.ORG 17

According to an article in Forbes, businesses are looking to cut costs to ease inflation burdens along with other financial issues.1 This sometimes-singular focus on bottom-line management in the security industry often results in situations in which accidents or even violence can become unavoidable— leading to costly claims. Similarly, rising tensions and gun violence place security guards in no-win circumstances while putting many private-security firms at risk of steep insurance rate increases or loss of coverage.

In an increasingly hard insurance market, agents and brokers can offer tools and resources to insureds to help prevent or minimize some of the most damaging claims.

Inadequate security budgets

While general liability claims are the most common in the security industry, claims of failure to provide adequate security are prominent among these general liability issues. Hired-guard firms alleged to have not provided satisfactory security per their contract often find themselves accused of improper training, distractions, not enough guards on-site and more.

There are countless circumstances that can lead to a failure to provide adequate security. In a University of Mississippi vs. Louisiana State University football game, a security guard was overtaken by fans storming the field, which resulted in multiple injuries. In the report of the incident, it was clear the guard attempted to stop the fans. However, one guard against countless, enthusiastic sports fans determined to rush the field is a losing proposition.

Too often these types of claims are the result of miscommunications during contract negotiations. Consequently, if the client ends up dictating the terms of the relationship, the security firm may have less protection in place than it should. In these negotiations, the client may ask for something specific that is not achievable—which puts the guards in a no-win scenario.

If security clients are unwilling to accept a firm’s recommendation on security staffing or they request fewer guards in a bid to save money while still fulfilling their requirement to provide security, the risks for the firms involved manifest at the outset. These situations position security firms to work in lessthan-ideal circumstances. If an incident occurs, security failures—and resulting insurance claims—likely will follow.

PROFESSIONAL INSURANCE AGENTS MAGAZINE 18

Grow Your Book, One Driving School at a Time When it comes to safeguarding driving school vehicles, Lancer stands head and shoulders above the rest. We write both private passenger and mixed fleet driving schools and offer A- “Excellent”-rated commercial auto coverages to keep your clients well protected. • Writing in CT, NJ, NY, OH, & PA • Agency Headquarters online quoting • No minimum premiums • No minimum/maximum units Submit your driving school risks to Lancer today and watch your portfolio thrive. 516-431-4441 x 3507 producer@lancerinsurance.com www.lancerinsurance.com

When faced with staffing shortages, regardless of the cause, securityguard companies should consider leaning into their expertise. Firms can offer safety training for clients in addition to security training protocols. They can provide a written plan for clients to consider in case of fires, theft, workplace violence and any other circumstances that could create safety issues. Security firms should review these plans with clients and ensure the clients understand what to do in case of an emergency. If clients are trained and aware of the plan, an incident is less likely to escalate or result in a claim.

Another tool to employ when staffing concerns exist includes the proper use of closed-circuit television security systems to monitor multiple areas simultaneously. With CCTV systems, guards can monitor most aspects of a property from a central location. If an issue occurs, a guard using a CCTV monitoring system is more likely to be both timely and responsive when incidents occur on a property.

Contract negotiation also plays an important role in minimizing risk in situations in which there are not enough guards for the level of threat. Often, security firms hope for big contracts with marquee clients or large venues that promise significant income and growth opportunities for their businesses. Agents and brokers should advise private-security owners to proceed with caution in such situations. Insurers are often best positioned to advise security firms of the potential fallout of a claim juxtaposed with any potential financial or reputational benefit a large or prestigious client might provide.

To avoid inadequate security claims, private-security firms will need to approach new clients with trans-

parency and clear communication. They should outline, in detail, what is and is not achievable. Additionally, private-security firms can share drafts of any contracts with their agent or broker before signing so they can receive thoughtful advice regarding potential risks that may be apparent in the contract terms. Once the agent or broker has shared thoughts and the contract has been negotiated, it is important that all parties sign the contract, or post orders, so the contract language is legally memorialized. Unsigned contracts are rarely enforceable in obligating the parties to the terms negotiated and can pose additional risk to guard firms.

Action-over claims

Action-over claims are another subset of failure-to-provide-adequate-security claims. Action-over claims are frequent in the private-security industry. In these instances, an insured’s security guard is injured on the job and he or she pursues legal action against the client where the injury occurred. An actionover claim is filed when the client has language in the contract that places indemnity obligations on the private-security firm and makes the firm the responsible party for any injuries the guard incurred.

Like most failure-to-provide-adequate-security claims, action-over claims result from contractual issues. When a private-security firm agrees to take on indemnification in a contract, unless otherwise stated, that includes injuries to its own guards—even if the client is at fault. In most cases, workers’ compensation coverage can help protect a firm. If the injury is minor, the guard will file a workers’ compensation claim that can be settled relatively quickly.

However, when the injury is more serious, the guard may decide to pursue legal action against the client. If the guard pursues legal action, the client likely will point back to the security firm for indemnification and the firm will be responsible for both the workers’ compensation claim, and the client’s payment to the injured guard. Action-over claims can be cyclical, causing defense, settlement and other costs to rise. Often the carrier will work to settle the case to avoid a nuclear verdict and ultimately it will pay more than necessary.

To help mitigate action-over claims, agents and brokers can confirm privatesecurity firms have workers’ compensation coverage to help settle any minor incidents with guards quickly. For major injuries in which the guard may pursue legal action against the client, the best form of protection an agent or broker can suggest is preventative action. Private-security firms should ensure it is stated clearly in all contracts that the security firm will not indemnify the client for the client’s own alleged negligence.

Slip, trip and fall claims that lead to injury for the insured guards are another frequent cause for general liability claims and can result in workers’ compensation and action-over claims. To avoid injury, agents and brokers can advise security clients to do a thorough walkthrough of any new space they are guarding to identify potential risks before the contract begins. Doing so will help firms mark curbs, speed bumps or other hazards to avoid during future patrols. Familiarization also can help guards map out the most accurate patrol route and identify shortcuts to best navigate the property—especially in cases of fast-moving security incidents.

PIA.ORG 19

Armed-guard failures

According to the Gun Violence Archive mass shootings in the U.S.—defined as incidents in which four or more people are killed or injured—are up from 272 in 2014, to 656 as of Dec. 7, 2023.2 In fact, in the past four years alone there have been more than 600 mass shootings per year.

With this increase in gun-related violence there has been an increase in security claims tied to armed guards, gun violence or both. For example, in my first 10 to 15 years at Brownyard, we saw three or four shooting claims total. In the following 15 years, that number jumped to approximately three or four shooting claims per year.

EverGuard, a long-term partner for your RBT business.

• Exceptional service is an EverGuard priority

• Uncompromised program loyalty

• Great coverages at competitive pricing with available A&B, Enhancement Endorsement & more

• No limit on alcohol sales

• Package Policy: Property, GL & Liquor Liability

• Entertainment considered

• Experienced & Professional Staff

EverGuard, is a superior Restaurant, Bar & Tavern market with 40+ years’ experience. Your RBT clients can depend upon EverGuard for their protection.

Our continued longevity offering an uninterrupted market assures you will receive the best product underwritten by an AM Best “A” rated carrier without program interruptions. EverGuard’s respected reputation in the RBT market speaks to our stability and reliability to provide industry leading response time and customer service to our partner agencies.

EverGuard Insurance Services

1900 W. Nickerson St., Seattle, WA 98119

Visit EverGuardins.com for a listing of the states the program is available

EverGuard does not offer or solicit the program in the states of Connecticut, New Hampshire, or Vermont

Michael Maher

EverGuard Insurance Services

VP, Business Development

Michael@everguardins.com

206.957.6576

EverGuardins com

Like the failure-to-provide-adequatesecurity claims mentioned earlier in this article, shooting claims often result from the client’s unwillingness to pay for an appropriate level of security. Generally, armed guards are required in areas with frequent high levels of crime or high-tension situations. Guns or exposure to violence can escalate quickly and create additional risk. Alternatively, having a well-supported security force can help better manage tense situations, as well as provide the experience and resources necessary to de-escalate and help avoid accidents and/or injuries appropriately.

Of course, not all firearms claims come from guards using a firearm. Many occur when a third party shoots another individual, or a group of people, such as in a massshooting situation. As a result, firms that are asked to guard areas with large groups of people congregated in a smaller space, such as concerts or schools, pose significant exposure to a guard firm in this era of exacerbated active-shooter claims.

Regardless of the cause, gun violence claims are costly and create unique challenges for both the insured and the insurer. When guns are involved in a claim the injuries often are catastrophic. As a result, the privatesecurity company incurs devastating costs that can lead to steep increases in rates or loss of coverages entirely. Fortunately, agents and brokers who support armed-security work can assist clients in mitigating both individual and third-party shooting claims by advising them to be selective in the clients they sign.

Should a firm choose to sign a client that requires an armed guard, it should conduct a thorough background and history check on both the organization and the loca-

PROFESSIONAL INSURANCE AGENTS MAGAZINE 20

Tavern

Leader

The Trusted Restaurant, Bar &

Market

With The Best-In-Class Service & Reliability

tion before any contract is finalized. Similarly, security agents and brokers should advise security firms that employ armed guards to ensure all officers are screened properly, are licensed, are trained and are supervised. Guard firms should conduct thorough background checks on both clients and guards, as well as providing regular, consistent training for all guards around safe firearm usage.

Obtaining a thorough understanding of the space or situation to be guarded can help security firms best prepare. While avoiding armed-guard work is the best way to avoid potential shooting claims, it is not always possible. Insureds working with firms that undertake armed-guard work should consider providing de-escalation training and other tools for guards as additional

layers of protection to ease potential tensions. As in all situations, negotiation can be an important risk mitigation tool for guard firms considering armed work. Professional insurance agents should advise their clients to avoid any indemnification contract language in these scenarios to ensure appropriate liability limitations and/or restrictions.

With private-security claims on the rise, agents and brokers are the best line of defense to help minimize potential claims. The preventative steps and insights agents and brokers can offer to their clients can sometimes circumvent some of the most common and frequent claims. When both parties communicate clearly, and they are aware of the responsibilities on all sides, confusion and unnecessary litigation often can be avoided.

Randazzo is president of Brownyard Claims Management Inc., a loss-prevention and full-service claims facility that has served all of those insured by the Brownyard Group for the last 30 years. Reach him at rrandazzo@brownyard.com or (800) 645-5820.

1 Forbes , 2023 (tinyurl.com/547zc5e7)

2 Gun Violence Archive (tinyurl.com/2f2au53v)

PIA.ORG 21

Grow your book of business—offer the protection of Hartford Flood Exclusive online program access for PIA members—Personal and Commercial Flood policies Why Hartford Flood • Competitive commissions • Multi-rater quoting system • Online quoting, endorsements and policy issuance • Free flood zone determinations, certified to be accurate • Dedicated flood sales director assigned to your agency The program is available to PIA members and their policyholders in all 50 states, the District of Columbia and Puerto Rico, and offers special PIA member commissions starting with the first sale (no minimums to qualify). Get started—contact The Hartford today. CT/NY—Art Brickley | (860) 547-2190 | a.brickley@thehartford.com NJ—Cheryl A. Maginley | (860) 547-5007 | Cheryl.Maginley@thehartford.com VT/NH—Michele Battis | (704) 972-5918 | Michele.Battis@thehartford.com

Call (800) 424-4244, ext. 408 | Web www.pia.org Why PIA is the Best Choice for E&O • Our professional liability and cyber liability programs are designed for your agency’s needs and risk exposures • Critical coverage options—especially important when many agents are working remotely • Top-rated, stable E&O carriers • Experience & expertise from our team PIA is here to help you navigate through uncertain times, so let’s make sure you have great errors-and-omissions coverage at a competitive price. We’ll Navigate Your E&O Coverage You Focus on Business Scan to learn more and get a quote.

MEREDITH BARNES-COOK Partner, ReSource Pro

AI: Claims process automation

What agents need to know

Claims process automation kicked into high gear about 20 years ago with the emergence of robotics process automation to augment core claims systems and streamline high-volume, predictable and repetitive tasks.

Meaningful improvements in the end-to-end claim process were realized using RPA, but there also were experiments that exposed its limitations. Flash forward to where we are today with the emergence of artificial intelligence technologies—most recently generative AI—and we see that the automation journey has not changed that much. There is no one-technology-fits-all solution. Each type of AI solves different problems, and none should be expected to wholly eliminate the need for people, to provide claims service and make claims decisions.

All of this is not to say that automation technology hasn’t been a boon to the claim process. RPA and AI continue to improve agent and customer experience, to enhance decision-making, and to enable better loss outcomes. GenAI is incredibly powerful, but it will have its limits and risks, too. So, as independent agents hear about a carrier’s

claims technology plans, it is helpful to understand how carriers have navigated an increasing array of automation solutions, to anticipate the benefits to the agency and its clients.

How claims tech has evolved

When RPA was first introduced, carriers jumped at the opportunity to address a growing list of automation opportunities that fell outside the intended function of their core claims systems. Early RPA successes included moving data between disconnected systems and eliminating a tedious, people-driven process. The value went well beyond more efficiency, speed and accuracy. It increased the capacity for claims adjusters to focus on the activities that could not be automated (e.g., coverage and liability decisions, and evaluating complex losses).

However, with these automation wins came the discoveries of the RPA’s limitations. As a technology designed to mimic a set of manual, rule-based and repetitive actions, it was not intended to interpret and understand new information. Carriers found RPA’s boundaries when a

PIA.ORG 23

software robot would fail because something changed in either the data source (i.e., a new ACORD form version) or the destination (e.g., screen changes in the claims system). The automation would fail until a new bot was created. While some might have deemed this a failure of RPA as a technology, the issue was learning RPA’s intended capabilities in real time.

New automation solutions quickly generate buzz across the insurance industry. Based on early and limited information, carriers will theorize about the scope of problems that can be solved. Theories can morph into assumptions that become expectations—even before any actual experience and results. When reality doesn’t live up to those expectations, disappointment is inevitable. Ideally, the story does not end there; carriers loop back with a better focus to maximize the automation solution’s use as intended. Many claims organizations did this with RPA, doubling down within the fenceposts of the technology’s intent.

A learning journey for claims automation

As AI has made its way into the claims journey over the past decade, there have been similar hype-cycle experiences. About five years ago, almost 80% of carriers were exploring—or at least receptive to—a path toward a touchless auto-claim process.1 The race was on for customers to submit photos of the damage to their car. The vision was for AI to generate the repair estimate, and the carrier would issue a check automatically.

The reality was that AI could not yet do all that the appraiser could—including decoding the VIN and discerning prior damage. Policyholders, carriers and even repair shops were surprised by an uptick in the need for supplemental appraisals to catch what the photos and AI missed.

But it was key not to treat this as a wasted effort and walk away. The learnings have guided vendors on how to use AI differently, and the earlier capability gaps are closing. In the interim, automation acts as a smart digital assistant for the appraiser. AI assesses the damage based on the photos, and then the appraisers apply their expertise and human discretion to finalize the estimate. This is still a streamlined customer experience, and it maximizes the use of the appraisers’ time.

A key takeaway from this type of experimentation is that we need to begin with the expectation that as we shift from assumption to understanding a new technology, we will discover its potential and boundaries—and both must be respected.

What could GenAI mean to claims

The emergence of generative AI in late 2022 introduced a powerful technology that also was widely accessible. GenAI takes a huge step beyond other AI technologies that can identify, extract and analyze data, execute tasks and create predictions. GenAI also leverages vast stores of training data to learn patterns and then create text, images, videos, computer code or content in other formats that resemble human-generated content.

Regarding the impact of GenAI on claims specifically, the insurance industry has much to be excited about, but a great deal to be mindful of when applying the technology. When GenAI gets it right, its capabilities can be astounding.

On the other hand, as anyone who has experimented with platforms like ChatGPT knows, when GenAI gets things wrong it can get them very wrong—hence the use of the term “hallucinates” to describe the technology’s mistakes.

Many of the early GenAI insurance solutions are a co-pilot approach that offers claims adjusters a powerful digital assistant. Instead of the early assumption that GenAI would eliminate the role of people, its power is in analyzing multiple data sources, creating summaries and offering recommendations—while keeping humans in the loop to make decisions. Carrier experiments with GenAI often have begun with internally facing processes, to measure and improve accuracy, avoiding any customer or agent impacts.

Challenges when applying tech to claims

All participants in the claims journey—from policyholders to claimants, agents, and providers— are consumers in their personal lives. The service experience offered by retailers, restaurants and entertainment providers has established the baseline expectation for insurance interactions. We expect the claim process to be easy, transparent and proactive, offering both digital selfservice and the option to interact with a person. Carriers must be mindful to match the technology solution with the capability they strive to build. This entails understanding both the capabilities and limitations of a given solution.

It is important for carriers to define both the end-target state and the incremental path to get there. And, carriers must watch carefully for the

PROFESSIONAL INSURANCE AGENTS MAGAZINE 24

magpie effect—in which the hype results in incorrectly using technologies. Careful matching prevents carriers from using a powerful tool like GenAI when RPA’s less complex automation capabilities would do the trick. This is one of the early lessons of RPA when carriers began with rules-based automation and later tried to introduce cognitive-use cases that RPA could not support.

Rethinking when automation can be empathetic

At first glance, the idea of embedding AI into the workers’ compensation claim process might feel uncaring because an injury is involved. However, carriers that are tapping into modern solutions that can understand language, recognize emotion and speed up workflow are removing the pauses that create friction. AI can recognize and extract information from an ACORD claim form, passing that data into the core claims system. Claims can be triaged automatically to assign to the appropriate claims adjuster. An automated and comprehensive new claim acknowledgment can reach the injured worker via email or text, answering his or her questions about what happens next and when.

Predictive tools can provide the claims adjuster with a summary of the loss and recommend the next best actions and even the initial reserves. Other critical and predictable tasks—like obtaining a wage statement or introducing a medical provider network—can become automated digital conversations. Each of these automated experiences increases the claims adjusters’ availability to use their expertise to manage each injury and make

important decisions quickly. It improves the experience for all involved, because the claims adjuster has more capacity for person-to-person conversations when that is what the claimant or policyholder prefers.

Summing it up

Agents will want to follow their carrier partners’ use of technology across the claims journey and not solely to understand how customer experience will change. Claims technology can create opportunities for agents to modify their own processes for greater speed and efficiency. For instances when the agents are not their customers’ first point of contact to submit a claim, they will want to know if a carrier partner is expanding their options to include a digital self-service experience. If a carrier is automating new claim acknowledgments and claim-status updates, the agents will appreciate knowing these additional customer touches are being added. Some agents may even want to receive a copy.

Overall, AI technologies are impacting the insurance industry profoundly— and the claims process is no exception to this shift.

While this may not be news to many of us, there are some key points agents should keep in mind regarding GenAI hype, the specialization of AI tools, and where each is best utilized in the claims process. Agents also should understand the best methods to employ to remain connected to carrier partners as new AI technologies are implemented into the claims process.

Barnes-Cook is a partner with ReSource Pro’s Consulting Practice with almost 40 years of insurance and claims experience. For more information visit www.resourcepro.com.

1 LexisNexis, 2019 (tinyurl.com/5b95ddkw)

PIA.ORG 25

General pia@pia.org Conference conferences@pia.org Design + Print design.print@pia.org Education education@pia.org Government & Industry Affairs govaffairs@pia.org Industry Resource Center resourcecenter@pia.org Member Services memberservices@pia.org Publications publications@pia.org Young Insurance Professionals yip@pia.org Email> Keep these addresses handy to reach PIA electronically 116889

Employee Benefits for Insurance Agencies

Let the PIA Members’ Choice group benefits program take care of your agency.

Medical Dental/vision

LTD with Reliance Standard

Term life with Reliance Standard

PIA’s

today! (800) 424-4244 | memberservices@pia.org

curated programs for member agencies and brokerages feature carrier selection, flexible coverage, top-notch customer service, and claims assistance when you need it. Get your quote

Streamline claims processes for enhanced efficiency

The insurance industry has long been plagued by inefficiencies that can slow down the claims process, leading to frustrated policyholders, increased costs, and ultimately, a poor policyholder experience. Many of these inefficiencies are rooted in antiquated systems and unnecessary human interactions, which hinder the seamless flow of information and communication.

In the modern era in which technology is at our fingertips, there is no excuse for such outdated practices. Let’s discuss the common challenges traditional claims processing causes, and how agents and insurance professionals can enhance claims triage through streamlined processes and increased efficiency.

The pitfalls of traditional claims processing

The traditional claims process is marred by numerous challenges, most notably the reliance on archaic systems and unnecessary human interventions. Agents and insurance professionals who resist the adoption of new technologies are contributing to a stagnant industry, and the consequences can be dire. Antiquated processes continue to devalue customer relationships, leading to delays in claims processing. In turn, these delays contribute to indemnity leakage and escalating expenses. Additionally, poor claims experiences drive policyholders to explore other options—leading to less acquisitions for carriers during renewal periods.

One of the critical issues is that these systems and processes don’t adapt to the preferred communication methods of policyholders. For example, policyholders who initially purchased their policies through email or text messaging without engaging in phone conversations. When these same policyholders need to file a claim electronically, their natural tendency is to communicate through the same channels. Unfortunately, some agents and insurance professionals fail to recognize this customer preference, leading to friction in the communication process. Recognizing and adapting to policyholder communication tendencies is essential to ensuring efficient and satisfactory interactions. Being armed with a clear understanding of policyholder communication preferences and with transparently specific data points—from the quote process through to the life cycle of the policy across numerous platforms—can help to avoid stagnation and friction for all involved. Each communication and touch point during an insured’s policy life cycle allows the producers, underwriters, claims professionals and product teams to understand habits and preferences of the insured. Using these data points and communication

preferences allows the carrier to better understand the needs of the insured no matter the situation that may arise. Storing and sharing data points across the landscape reduces friction during a claims process or renewal.

Understanding the insured’s claims history and communication preferences allows the carrier to better triage claims, as information that has been analyzed drives business logic and strategic decision making. Reviewing claims history and severity across reported damages, coupled with machine logic allows the carrier to understand potential severity of a reported claim by understanding more about the property and the insured. Accurate severity reserves pre-claim assignment leads to shorter cycle times by ensuring the proper adjuster is assigned to the claim and the claim follows the correct process for adjustment. A $150,000 fire claim is handled differently than a $15,000 fire claim, and understanding the difference during triage reduces friction for all parties.

Many states are implementing statutes that limit the number of adjusters who a claim can be assigned to throughout the claim process due to the immense amount of friction that reassignments have on the insured. Being able to triage properly with the use of pre-captured data and loss facts greatly reduces the need to

PIA.ORG 27

CLAY RISING Chief claims officer, Brush Claims

CONNECT

change adjusters due to changes in severity. The more the carrier knows when the claim is received, the quicker and cleaner the claims process becomes.

The crucial role of efficiency for agents

Efficiency is what drives success in the insurance industry, and it’s a fundamental aspect of maintaining a competitive edge. Insurance is unique in that there is no physical product; agents and carriers are selling a promise to policyholders to indemnify them for covered losses in exchange for a premium.

The claims process, which averages an 8% claims frequency rate, often is a source of confusion for policyholders. It falls on the industry to ensure that the

process is communicated efficiently and executed to minimize delays, leakage and escalating costs.

Lawyers Professional Liability Coverage

If you have law firms as clients, you know they have unique insurance requirements that can’t be covered by a standard general liability policy. We can help you help them.

Parsons & Associates has programs designed to help you cover your clients’ unique insurance needs.

(800)

www.4lawyersinsurance.com

Advanced InsurTech solutions drive efficiency and are key to transforming the claims process. Having a technology-forward claims management system offers complete policyholder control and transparency, from first notice of loss through to completion. Automation is a beneficial tool in the claims journey, enabling adjusters to make complex coverage decisions while efficiently communicating with policyholders. Policyholders should be able to access realtime updates on the status of their claims through a customer portal, staying informed and empowered throughout the process.

Efficiency is crucial for all individuals involved throughout an insured’s policy life cycle and that does not cease once a policy is bound. Understanding the insured and the property is a crucial piece for agents to grasp. Knowing underwriting guidelines and carrier preferences reduces friction during the initial sale of the product, but even further, it allows the carrier to make decisions based on information and data points established during the initial pre-policy issuance conversations and documentation. Having clean data and facts surrounding a property allows the carrier to institute workflows during a catastrophic event that may produce wide-scale claims volume. Patterns and behaviors of insureds hold steady based on past performance, and new decisions are made to efficiently guide an insured through the claims process to reduce friction. Ultimately, friction increases the carrier’s Loss Adjustment Expense as cycle times struggle and claims remain open. Friction also introduces more oppor-

4 40-9932

PROFESSIONAL INSURANCE AGENTS MAGAZINE 28

tunity for litigation and inflated estimates due to time being extended.

Integrate new technologies in the claims process

For agents and insurance professionals looking to integrate new technologies and modernize claims processes for policyholders, several key principles are essential:

No. 1: Understand your workflow. Start by analyzing and understanding each part of your existing workflow and processes that interact with claims. This comprehension should extend from the sales cycle through to claims completion.

No. 2: Identify roadblocks. Recognize speed bumps and roadblocks in your internal processes that impede efficiency. These challenges provide a roadmap for process improvements and digitization.

No. 3: Take a holistic approach. Look for holistic process improvements rather than attempting to plug in quick fixes. Comprehensive changes may be more effective in the long run.

No. 4: Allocate resources. Recognize the importance of allocating the necessary resources—both in terms of finances and workforce— to support and drive the adoption of new technologies for claims processing.

No. 5: Remain dedicated. Understand that any transition is reliant on agents and insurance professionals dedicating time, energy and resources to become successful in any digital transformation.

The insurance industry’s path to enhanced efficiency in claims processing lies in embracing InsurTech solutions. This transfor-

mation is a pivotal strategy for agents and insurance professionals, driving streamlined workflows to make things easier and more convenient while creating positive experiences for today’s policyholders.

Having a deep understanding of your claims workflow is essential to knowing where friction is introduced and how it can be reduced. Looking at the complete claim life cycle is an integral piece to finding the solution to the potential problems in a workflow. Often, trying to solve for one friction point creates additional friction points and it does not solve the entire problem—it increases complexities and adds failure points. Focusing on the entire process is the only fix to a broken workflow.

Rising is the chief claims officer at Brush Claims, an InsurTech claims solution firm. He grew up in the insurance industry working for his dad in an independently owned agency throughout high school. He utilized that experience to gain degrees in risk management and insurance and corporate finance. He also joined The Travelers as an adjuster, and quickly became a commercial general adjuster. After a few years of catastrophe duty and traveling throughout the southeast, he worked at ASI. Throughout his nearly nine years at ASI (later to become Progressive Home), he held numerous leadership roles. In his last role, Rising led its National Large Loss and Major Case groups for both catastrophe and noncatastrophe events in 44 states. Utilizing his experience gained from that role, he joined start-up Kin as its first vice president of claims.

L. Davey DD Agency

PIA.ORG 29

Industry Resource Center 1,724 member inquiries 4,955 QuickSource requests 3,814 tool kit hits 1,673 Ask PIA hits 1,216 MarketBase™ requests 28 contracts reviewed www.pia.org (800)424-4244 resourcecenter@pia.org 2405-D-2023 PIA membership brings with it a wealth of benefits for the professional, independent insurance agent or broker—but the personal assistance of PIA’s Industry Resource Center alone is worth the investment. “I can’t thank you and your team enough for your assistance. Your step-by-step assistance with reference to the cyber security regulations was incredibly helpful. You guys are amazing. ” —Deborah

Inc. We have the solutions YOU NEED

Own Your Risk Management Potential

James K. Ruble

Graduate Seminars

Taught by the nation’s top instructors and open to all dues-paid designees, these CE-approved seminars explore advanced topics and apply real-life scenarios.

May 15-16 Webinar

Aug. 21-22

HYBRID—Webinar/Turning Stone Casino, Verona, NY

Nov. 6-7 HYBRID—Webinar/Hard Rock Hotel Casino, Atlantic City, NJ

LIVE ONLINE AND IN-PERSON HYBRID SEMINARS:

April 3-4 HYBRID—Webinar/Caesar’s, Atlantic City, NJ

CE-approved in all 50 states. For details, contact the National Alliance at (800) 633-2165. REGISTER ONLINE https://bit.ly/3VfDBOW

Group 534: Almost all construction classes eligible

Group 533: Woodworkers, lumberyard, and building material dealers

Group 501: Plumbing, heating, cooling, and steamfitting contractors

New to NYSIF prospects may qualify for an enhanced discount

50% of the service fee paid to brokers for the first three policy terms!*

Unbroken string of dividends since group’s inception!

Hamond Safety Management included service checklist

Knowing your client’s business and exposure

Assisting with payroll audits

Assisting employers with claim filing

Working with the carrier to assure proper claim handling

Hearing and testimony support including prehearing interviews with witnesses

Support with underwriting and billing issues

Assisting with OSHA issues and training

Safety audits and risk management

Development of safety programs, both corporate and site-specific

2718-D-2023 *Service fee paid to brokers on subsequent renewals and on returning members at our usual 20%. Direct quote requests to: (800) 285-2258 • Fax: (516) 488-5940 info@hamondgroup.com • hamondgroup.com Members are not just policyholders! At Hamond, our staff averages over 40 years of workers’ compensation experience!

Underwritten by the New York State Insurance Fund. Excellence

REAL CLAIMS SOLUTIONS

REAL DIVIDENDS

$348 Million Paid

Our rich dividend history stands as a testament to the success of our claims process.

• Up to 45% savings upfront

• Advance discounts up to 35%

• NYS Assessment deferrals until dividends for the first two periods

Brokers receive 50% commissions for first three policy periods on all new Safety Group business.

Cosmo Preiato 800-394-7004, ext. 203 2500 Westchester Ave., Suite 400A Purchase, NY 10577 cosmop@friedlandergroup.com www.friedlandergroup.com

Safety and Workers’ Compensation Strategies To Unleash Productivity and Profits

Featuring insightful interviews with experts including Paul O’Neil, 72nd Secretary of the U.S. Treasury

By

Adam Friedlander - Now on Amazon.com

**10% increase in advance discount

*5% to increase advance discount

*Underwritten by the New York State Insurance Fund, 199 Church Street, New York, NY 10007. Dividend not guaranteed.

RETAILERS

Retail Group of NY Workers’ Comp. Safety Group #544*

2022-23 40%**

2021-22 40%**

2020-21 40%**

36% average dividend since inception in 1922

WHOLESALERS

Wholesale Group of NY Workers’ Comp. Safety Group #551*

2022-23 42.5%**

2021-22 40%**

2020-21 35%**

32% average dividend since inception in 1993

FINANCIAL SERVICES

Financial Services Group of NY Workers’ Comp. Safety Group #558*

2022-23 50%**

2021-22 40%

2020-21 40%

39% average dividend since inception in 1994

RESTAURANTS

Restaurant Group of NY Workers’ Comp. Safety Group #556*

2021-22 40%**

2020-21 40%**

2019-20 35%*

36% average dividend since inception in 1993

HOTELS

Hotel Group of NY Workers’ Comp. Safety Group #578*

2021-22 35%**

2020-21 35%**

2019-20 25%*

21% average dividend since inception in 2006

OIL DEALERS

Oil Dealer Group of NY Workers’ Comp. Safety Group #582*

2021-22 35%**

2020-21 35%**

2019-20 35%*

21% average dividend since inception in 2010

SOCIAL SERVICES

Social and Health Services Group of NY Workers’ Comp. Safety Group #585*

2021-22 40%**

2020-21 35%**

2019-20 25%*

20% average dividend since inception in 2011

RESIDENTIAL CARE

Residential Care Group of NY Workers’ Comp. Safety Group #586*

2022-23 35%**

2021-22 35%**

2020-21 30%**

18% average dividend since inception in 2012

Have a question? Ask PIA at resourcecenter@pia.org

Valet parking, trucker's general liability and more

NYAIP: Refunds for company rating errors

Q. My insured is in the New York Automobile Insurance Plan. The company incorrectly surcharged both the prior year’s policy and the current policy. We got that straightened out, but now the company wants to apply the refund as a credit on the insured’s unpaid installments. The insured wants a check. Who is right?

A. According to the NYAIP Manual Section 14.E.2.f, “Return premium resulting from changes to the policy may be used to reduce the outstanding balance [owed on the policy].”

However, Rule 29.D.3.e(3), states the insured has the option of receiving a dollar refund in lieu of a credit if an additional charge was levied through a company error. Therefore, the company should provide the insured with a check.—Helen K. Horn, CIC, CPIA, CISR

Defensive-driver courses must be DMVapproved to qualify for a discount

Q. My insured’s discount for taking the defensive-driving course expires next month. However, she resides out-of-state for part of the year and she won’t be home in time to take the course before the credit expires. Can she take a similar course out-of-state and receive credit?

A. Your insured would not be able to take a similar course out-of-state as the rules and requirements governing course content are set by New York’s Department of Motor Vehicles.

She would have to take a New York-approved course to receive the discount per New York Insurance Law Section 2336(a).—Helen K. Horn, CIC, CPIA, CISR

Damage coverage for valet parking

Q. I saw Ask PIA 900241—Coverage for valet parking in the Ask PIA library, which discussed liability coverage for a rented vehicle that is being parked by a valet. What about physical damage coverage in that scenario? Unless an insured has a New York policy, I would recommend that the insured not let a valet park a rental car because the coverage is too uncertain when physical damage is involved.

A. According to the renter’s personal auto policy, the PAP Part D–Coverage For Damage To Your Auto covers a “non-owned auto” as stated below:

INSURING AGREEMENT

A. We will pay for direct and accidental loss to “your covered auto” or any “non-owned auto,” including its equipment, minus any applicable deductible shown in the Declarations. If loss to more than one “your covered auto” or “non-owned auto” results from the same “collision” only the highest applicable deductible will apply. We will pay for loss to “your covered auto” caused by:

1. Other than “collision” only if the Declarations indicates that Other Than Collision Coverage is provided for that auto.

2. “Collision” only if the Declarations indicates that Collision Coverage is provided for that auto. If there is a loss to a “nonowned auto,” we will provide the broadest coverage applicable to any “your covered auto” shown in the Declarations.

However, the Part D exclusion applies to “non-owned autos” used by any person in the auto business. The valet driver’s personal auto policy would not cover it for the same reason.

PIA.ORG 33 ASK PIA PIA TECHNICAL STAFF

11. Loss to any “non-owned auto” being maintained or used by any person while employed or otherwise engaged in the “business” of:

a. Selling;

b. Repairing;

c. Servicing;

d. Storing; or

e. Parking vehicles designed for use on public highways. This includes road testing and delivery.

An exception occurs in New York state with the mandatory PP 03 46–Rental Vehicle Coverage endorsement. This endorsement covers all obligations of the renter without the inclusion of the garage business exclusion found in the PAP.

B. The rental car company

The rental car company contract likely voids coverage for an unauthorized driver, which means no coverage. The renter should request to be shown in the contract where valet drivers are covered.

C. The hotel or restaurant

The employer of the valet driver should take responsibility if it can be shown that the driver/employer is at fault. If another driver is at fault, recovery must be sought from that driver.

A good article on the subject can be found online at tinyurl.com/4k5e3rfz.

—Dan Corbin, CPCU, CIC, LUTC

Title with salvage brand

Q. My client’s auto was totaled in an accident. The insurer is discounting the value of the auto because its title has been “salvage branded.” Is the insurer permitted to do this?

A. Generally, an auto titled with a “salvage brand” will be worth less, but the amount is negotiable so the insured needs to do his or her homework to get the best deal.

This is what Kelley Blue Book states about it: “A salvaged, reconstructed or otherwise ‘clouded’ title has a permanent negative effect on the value of a vehicle. The industry rule of thumb is to deduct 20-40% of the Blue Book value, but salvage-title vehicles really should be privately appraised on a caseby-case basis in order to determine their market value.”—Dan Corbin, CPCU, CIC, LUTC

Trucker’s general liability

Q. What does a trucker’s general liability policy cover when not operating vehicles covered on the motor carrier policy?

A. Trucker’s general liability insurance provides various coverages; here are some of the major ones:

• non-vehicle accidents in parking lots and rest stops;

• loading or unloading using a mechanical device not attached to truck or trailer (e.g., forklift, front-end loader, crane);

• injuries to customers on the trucker’s premises;

• injuries to customers caused by the trucker on the customer’s premises;

• products and completed operations (e.g., products causing damage after delivery);

• libel, slander or invasion of privacy under personal and advertising injury coverage;

• repair of other trucker’s vehicles;

• guard dog liability;

• contractual liability;

• host liquor liability;

• legal liability for fire damage to leased premises or rented motel rooms; and