5 minute read

rallying

resulting from deforestation.

Overall, import demand, especially in price-sensitive countries, is likely to continue to fluctuate depending on how successfully palm oil can maintain its traditional discount to competing soft oils.

Weather boosts soya

Weather risk lifted soyabean prices off lows reached in May when they briefly touched the US$12.70/bushel level, with soyabean oil falling towards US$0.45/lb. Recently, soyabeans exceeded US$16/ bushel and oil US$0.67/lb, although both have lost some ground since.

Attention has been riveted on Argentina’s crop estimates, continuing to shrink amid severe drought. The USDA recently cut its forecast for Argentine soyabean production to 25M tonnes, with some private analysts estimating levels as low as 20M tonnes. This compares with last season’s 44M tonnes and the previous two years’ range of 46-48M tonnes. Fortunately for consumers, the shortfall still does not quite match the 25.5M tonne increase estimated for Brazil’s record 2022/23 harvest, now seen around 156M tonnes and already making in-roads into the export market share of its largest competitor, the USA.

The USA, meanwhile, has been having its own weather issues, with the USDA recently estimating that 70% of the Corn Belt, where most soya is grown, to be under some form of drought.

The weather outlook is improving with some recent rains and a wetter forecast for much of July, keeping the USDA’s 52 bushel/acre yield forecast for this year on track, up 5% from 2022. However, the harvest area is now expected to decline by over 4%, lopping 5.7M tonnes off earlier crop forecasts which, at around 117M tonnes, show only marginal gain from last year’s low 116.4M tonnes.

The USDA is bullish on next year’s Latin American soyabean crop prospects, seeing a further 7M tonne increase in Brazil and a massive 23M tonne revival in Argentina. However, these estimates are speculative at this early stage of the year, with planting still several months away.

Growth in global soyabean crushing – which stalled in the past season amid US and Argentine crop shortfalls – is expected to jump in the coming season from 312M tonnes to 330 tonnes, with gains in China (+4M tonnes), the USA (+2.1M tonnes), Brazil (+2.75M tonnes) and Argentina (+6.25M tonnes). Prospective larger supply gains would land the global soya market with a massive 19M tonne stock rise to a new record of 121M tonnes.

Forward futures markets reflect this looser supply outlook, with soyabean prices dropping back to a low US$13/ bushel for the first half 2024, and soyabean oil to the upper US$0.50/lb.

Rapeseed/canola outlooks

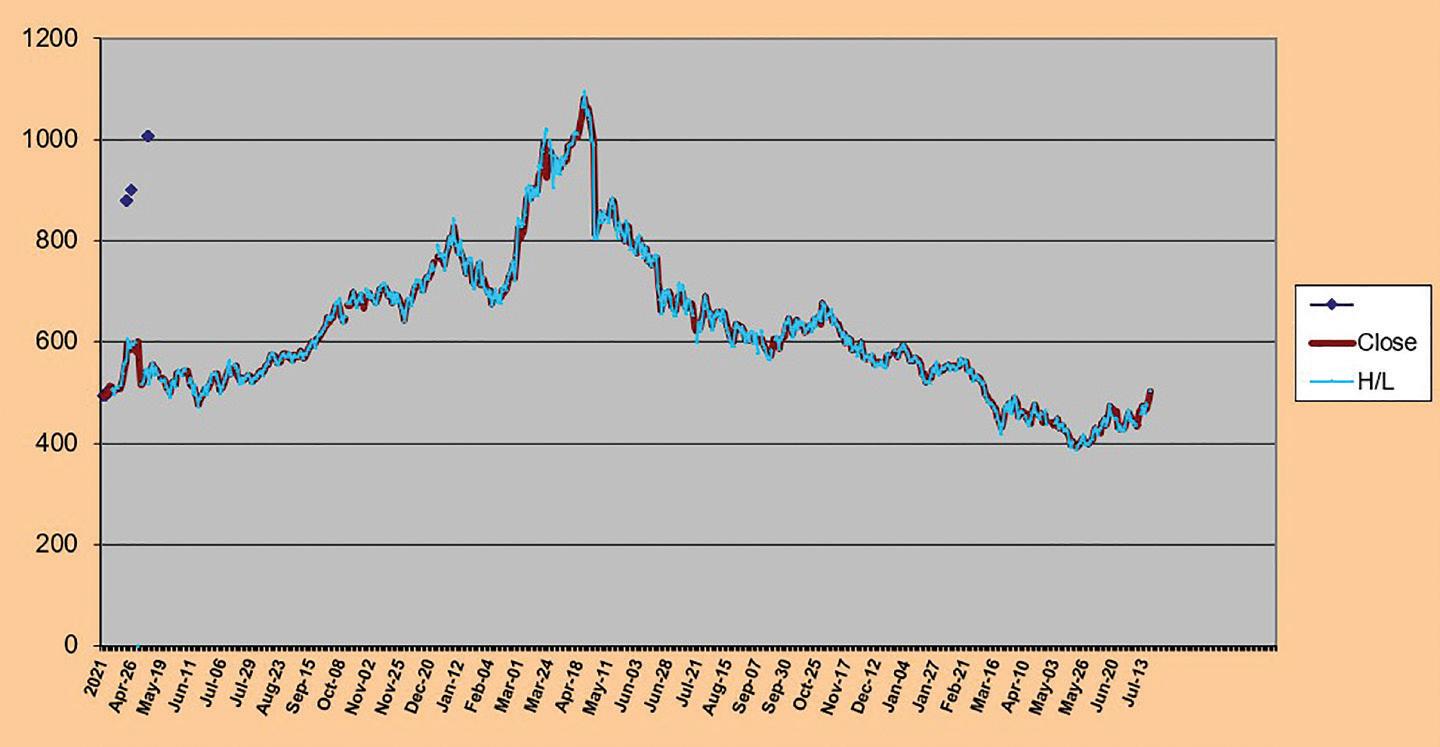

Rapeseed/canola futures prices hit 2.5 year lows in June as the market continued to reflect the past season’s much larger supply and trade/official expectations of a repeat in 2023/24. Expectations that other oils would remain in adequate supply also contributed to physical crude canola oil in May trading at its lowest monthly average since July 2020 (see Figure 3, following page).

A more recent firmer trend has been partly due to the rally in soyabean oil prices. Some crop issues have also emerged for rapeseed itself. Based on a larger sown area and expected better yields, the markets were initially looking at a rise in European output to perhaps 21M tonnes from last year’s 19.54M tonnes (which was itself more than 2M tonnes more than in 2021).

More recently, observers have been trimming yield assumption after a long hot, dry spell in Western Europe’s key canola states. In early July, French analyst Strategie Grains cut its total EU crop estimate from 20.4M tonnes to 19.8M tonnes, with USDA projections of around 20.2M tonnes.

Global production is already expected to decline from its record 2023 peak as Australia’s crop shrank back from last year’s record of 8.3M tonnes. That remarkably high figure was achieved due to a combination of a larger sown area and high yields which, in an El Niño year, analysts think is unlikely to be matched. The current USDA forecast for Australian canola production is 4.9M tonnes.

Canada’s canola crop forecast has been fluctuating amid the onset of very dry weather, first in the subsidiary province of Alberta and latterly in top-producing Saskatchewan state.

Statistics Canada recently estimated that the country’s canola planted area had risen 3.2% year-on-year to 8.9M ha (22.08M acres) and the USDA is still projecting a 20.3M tonne crop against last year’s 19M tonnes. Canadian crush has also risen by a steep 16.3% with the past season’s crop recovery and strong demand for the oil from expanding biodiesel production, both trends expected to continue in 2023/24.

Black Sea canola suppliers had been forecast to produce less rapeseed in 2023 based mainly on slightly lower sown areas. However, Ukraine recently rebutted forecasts of a crop fall from 3.5M tonnes to 3.2M tonnes, actually forecasting an increase to 3.7M tonnes based on better than expected yield prospects. That emboldened the USDA to raise its own forecast to 4M tonnes.

Russian production, meanwhile, is seen contracting from 4M tonnes to 3.7M tonnes. However accurate these forecasts prove, the main issue may remain how much oilseed/oil gets crushed/exported from a still war-torn region. With the United Nations-brokered Black Sea ‘safepassage’ export corridor closed at least for the time being, the trade will likely remain cautious about assuming supply as normal, especially amid the recent signs of political instability within Russia.

Amid the outlook for minimal/negative canola supply growth in 2023/24, the EU (Paris) and Canadian (Winnipeg) futures markets are suggesting that rapeseed prices will be fairly similar to those offered now, possibly a shade firmer through the coming year.

Larger EU sunflowerseed crop?

Sunflower oil prices have declined significantly with larger-than-expected supplies and the overall weaker trend in other soft oil and palm oil prices.

Yet even amid the uncertainty generated by the Black Sea conflict, regional farmers seem to be sowing larger areas. Russian planting is seen up by 400,000ha to 9.5M ha and Ukraine sowing higher by more than 500,000ha total 5.7M ha. Western European farmers are again expected to have sown a larger than usual area of around 5.2M ha as well.

The EU is also hoping for a rebound in yields that dropped by almost a quarter to a low average of 1.79 tonnes/ ha during last year’s hot dry summer in some key member states. The current USDA forecast is for a jump back to 2.21 tonnes/ha, which could land the bloc with a bumper 11.5M tonne crop, compared with last year’s crop of 9.29M tonnes and 2021’s total of 10.29M tonnes.

Assuming the war in Ukraine does not impact recent forecasts for a 16.5M tonne Russian crop and a 11.8M tonne Ukrainian crop, sunflower oil crushers could enjoy a needed jump in new crop seed input, albeit against a backdrop of smaller carry-in stocks from the 2022/23 marketing year.

In Ukraine, where stocks have been used to keep exports going amid recent smaller harvests, carryover is expected to have fallen from 4.7M tonnes in 2021/22 to 1.37M tonnes last year and just 480,000 tonnes in 2023. This has been the major component in world sunflowerseed stocks falling from 8M tonnes to under 4M tonnes over the same period. Russian and European stocks have also tightened over the past two years.

Ukrainian exports of sunflowerseed are expected to plummet in the coming season from 2.03M tonnes to just 800,000 tonnes to maintain domestic crush at around 12.7M and oil exports at around ‘normal’ levels of about 4.75M tonnes, according to the USDA.

Much depends on how long the Black Sea grain export corridor deal holds up. With Russia pulling out of the Black Sea Grain Initiative as we went to press, traders were hoping sunflowerseed would not be drawn into the broader military conflict, with some of Ukraine’s alternative export outlets developed enough to soften the risk.

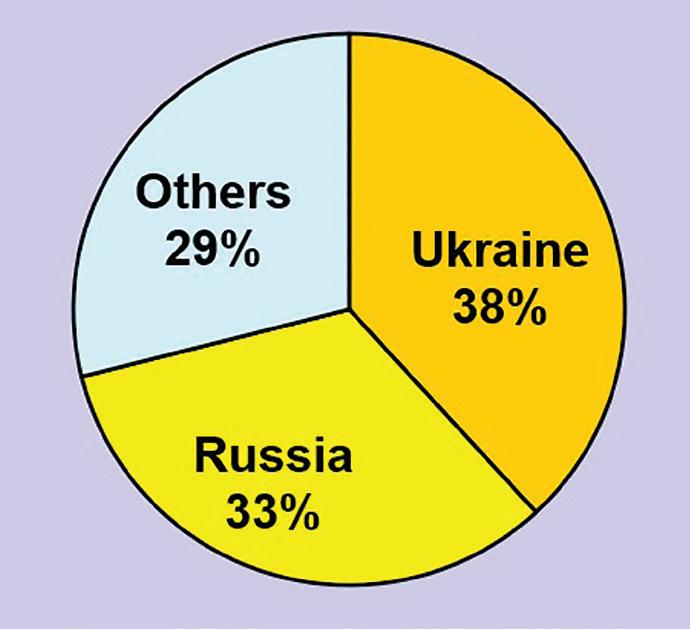

If all goes well with crop and geopolitics, Ukraine is projected to supply about 38% of global sunflower oil exports in the new 2023/24 season – similar to the past two years (see Figure 4, above left).

Russia is forecast to account for just over one-third of world supply. Preferred by many in some of the food sector, sunflower oil consumption has been edging up since prices have declined. After reaching a record US$2,570/tonne in March 2022, the Rotterdam benchmark price averaged just US$923/tonne in June this year. Along with cheaper soyabean oil, that has been encouraging big importers like India to switch back to this favoured oil from previously cheaper substitutes like palm oil. ●

John Buckley is OFI’s market correspondent