19 minute read

Protecting IRAs in the Face of Long-Term Care

Protecting IRAs in the Face of LongTerm Care

By: Dale Krause, J.D., LL.M.

In most states, IRAs are countable toward Medicaid eligibility. This article provides practical advice for dealing with IRAs and other retirement assets in long-term care planning.

It is no secret that the U.S. population is aging. The oldest members of the Baby Boomer generation began turning 75 in the year 2021, with about 70 million peers to follow. The senior population is growing and, due to advances in medical science, living longer than ever before. Therefore, it is now more likely than ever that a senior will require skilled, long-term care in their lifetime. In fact, the Centers for Medicare & Medicaid Services (CMS) states that 70% of seniors will require long-term care at some point.

Long-term care is an inevitability for most people; however, many fail to understand the financial burden that follows placement in a nursing home. According to the 2021 Genworth Cost of Care Survey,1 the average cost of a semi-private room in a nursing home is $7,908 per month. With the average stay in a nursing home being 2.3 years, it is not surprising that longterm care can wipe out a person’s entire life savings, leaving nothing behind for their loved ones.

This is what makes long-term care an issue for estate planning and elder law attorneys. As attorneys, we take specific measures to ensure a client’s assets are protected and distributed in accordance with their wishes after death. But what about protecting their assets while they are alive? Entering the nursing home is arguably the biggest threat to your client’s estate plan. For those clients who do not have the proper mechanisms in place to minimize the financial impact of long-term care, they are truly at risk of losing everything. However, attorneys can provide a solution, even if the client is already in a nursing home.

Where Medicaid Comes In

Now that more seniors are entering nursing homes, conversations surrounding Medicaid have increased significantly. Medicaid is a joint state and federal program meant to provide financial assistance for medical care to those in need. Concerning longterm care, Medicaid will cover a person’s stay in a nursing home (or another Medicaid-approved facility) including room and board, pharmacy, and incidentals. This makes qualifying for Medicaid desirable to individuals who, whether through error or omission, did not plan in advance for a long-term care event.

However, to qualify for Medicaid, an individual must meet specific non-financial and financial requirements. Beginning with non-financial eligibility factors, the applicant must be over 65 years of age, blind, or disabled. The applicant must also be a United States citizen or a qualified alien. The individual must also be a resident of a Medicaid-approved facility, as previously noted. In short, Medicaid benefits are reserved for those in need of the medical care provided by nursing homes.2

Medicaid’s financial requirements are much more intricate than the non-financial requirements, and they differ depending on the marital status of the applicant. To add a layer of complexity, the financial requirements also vary from state to state. These financial requirements fall into two major categories: Income and Assets. Too much of either will prevent a person from qualifying for benefits.

To be eligible for Medicaid, the applicant’s income must be less than the private pay rate of the facility at which they are seeking residence and care. This means their monthly income from all sources—including Social Security, pension, etc.—must be less than the monthly nursing home bill. A few states apply a different restriction where the applicant’s income cannot exceed an amount other than the nursing home bill.

In the case of a married couple, the spouse in the nursing home (known as the institutionalized spouse) is subject to the rules for an individual previously noted. The income of the spouse living at home (known as the community spouse) is not considered when determining the eligibility of the institutionalized spouse. As such, the community spouse is not subject to income limitations or restrictions.

Although the community spouse is not subject to income limitations, there is a floor on the amount of income the community spouse should receive. This is known as the Monthly Maintenance Needs Allowance (MMNA)—a provision set forth by the Medicaid program that ensures the community spouse has enough income to support his or herself in the community once the institutionalized spouse begins receiving Medicaid benefits. This requirement is often referred to as an “anti-impoverishment provision” intended to protect the community spouse. If the community spouse’s income is less than the MMNA, they will receive a shift in income from the institutionalized spouse. As of July 1, 2022, this Monthly Maintenance Needs Allowance is between $2,288.75 and $3,435.3

In addition to being income eligible, the applicant must also be within certain asset limits. Assets are divided into two categories: Exempt and Countable. Exempt assets are not considered when determining an applicant’s Medicaid eligibility. Some of the most common exempt assets include the primary residence, one vehicle, prepaid funerals, personal effects, and household items. In short, these are items that may be retained by the institutionalized individual and/or the community spouse without jeopardizing benefits.

Exempt assets stand in contrast with countable assets, which include any resource or property not listed as an exempt asset that holds value and could become liquid. Common countable assets include checking or savings accounts, CDs, stocks, bonds, mutual funds, non-homestead real estate, second vehicles, and virtually any other investment that could be readily converted to cash.

Although the Medicaid rules regarding countable and exempt assets render an institutionalized individual effectively impoverished, there is a carve-out that allows the Medicaid applicant to retain assets with a limited value referred to as the “Individual Resource Allowance.” In most states, the Individual Resource Allowance is $2,000. This means a Medicaid applicant can retain no more than $2,000 in countable assets and remain eligible for benefits. If the applicant is single, this is all they may keep. If the applicant is married, the community spouse can retain a separate amount known as the “Community Spouse Resource Allowance” (CSRA). This allowance varies by state but is generally between $27,480 and $137,400 as of January 1, 2022.4

Unsurprisingly, most individuals do not automatically qualify for benefits. Countable assets exceeding the applicable limit must be eliminated, or “spent down” for the person to qualify for benefits. In many cases, this can be accomplished by paying off a mortgage or other debt, purchasing or improving exempt assets, or other assets preservation strategies. However, most families typically spend this money on the nursing home bill until they have depleted their life savings.

The Problem Asset

Readers of this article may have noticed a glaring omission from the list of common exempt and countable assets— retirement accounts. Retirement accounts come in many forms and permutations, including (but not limited to) the traditional IRA, 401(k) accounts, and Roth IRAs. In most cases, a pension plan is not grouped in with this category, assuming it is making regular payments to the owner and there is no accessible cash value. For purposes of this article, the term “IRA” will be applied to all appropriate retirement accounts.

Treatment of IRAs from a Medicaid countability perspective varies from state to state. In a select few states, IRAs are considered exempt assets for both the community spouse and institutionalized spouse. Some states only exempt IRAs for the community spouse. Still, other states will only treat it as exempt if the owner is taking their Required Minimum Distributions (RMDs). This means that the owner can have an IRA of any value, and it will not prevent them from qualifying for Medicaid benefits. One pitfall, however, is that RMDs count as income to the owner.

In most states, IRAs are considered countable assets, meaning the entire account value is considered when determining Medicaid eligibility. With most couples being subject to a countable asset limitation of $139,4005 or less, this causes significant hurdles in the path toward Medicaid eligibility, due mostly to the economic consequences associated with liquidating an IRA. Aside from the apparent tax hit the account would take, other side effects include income taxation at a higher rate, the possibility of taxation on the couple’s Social Security benefits, and increased Medicare Part B and D premiums.

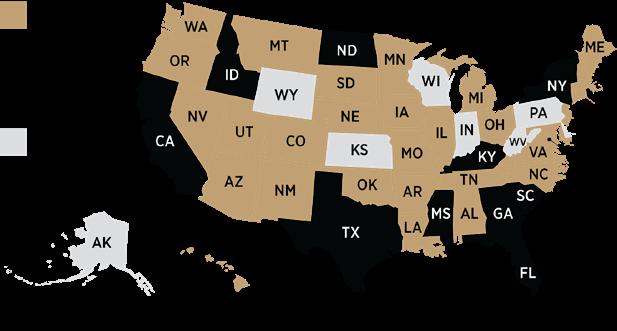

Table 1: Treatment of IRAs by State Medicaid Programs for LongTerm Care Purposes

Laying Out the Options

Thus far, we have established the problem surrounding long- term care, qualifying for Medicaid, and the additional concerns associated with IRAs. However, the goal of this article is to not only shed light on this common issue affecting estate planning and elder law clients, but also provide potential solutions attorneys can implement in their own practices.

As discussed, those attempting to qualify for Medicaid as a means of paying for long-term care can do so by “spending down” otherwise countable assets. Eliminating these assets is how one can accelerate eligibility without first exhausting their assets on the nursing home bill alone. The purpose of these socalled spend-down methods is asset protection—which should also be the goal of every estate planning and elder law attorney.

Common spend-down methods include paying off any outstanding debts, purchasing or improving exempt assets (for example, a new vehicle), and using tools to convert excess assets into income. These tools typically include promissory notes and Medicaid Compliant Annuities (MCAs). Both a promissory note and an MCA work by converting a lump sum of assets into an income stream.

In the case of a promissory note, the note is typically made between the institutionalized individual or the community spouse and a family member. The lender lends money to the maker who must then repay the money in accordance with the terms of the contract (typically monthly payments for a certain period of time). An MCA is a single premium immediate annuity (SPIA). In this case, the institutionalized individual or the community spouse establishes the contract with an insurance company that provides regular payments in exchange for a lump sum premium.

Both promissory notes and MCAs must comply with Deficit Reduction Act of 2005.6 In most cases, a promissory note must be non-transferable, may not cancel upon the lender’s death, and must require payments continue to the lender’s estate, which subjects the balance of the note to recovery by the state Medicaid agency for expenses paid on the institutionalized individual’s behalf. In regard to an MCA, the annuity contract must be irrevocable, non-assignable, provide equal monthly payments, have a term that is equal to or less than the owner’s Medicaid life expectancy7, and designate the state Medicaid agency as the primary or contingent death beneficiary.8

While it may seem the promissory note and the MCA stand on equal footing, it is important to recognize the promissory note is not a viable Medicaid planning strategy in every state. Several state Medicaid agencies specifically restrict the use of promissory notes as an allowable tool. Plus, promissory notes do not solve the problems associated with IRAs. Specifically, an IRA cannot be used to fund a promissory note, as it would first need to be liquidated. Therefore, the consequences of liquidation previously described would still come into effect. However, an MCA can be funded with an IRA.

The benefit of using an MCA in the case of an IRA is the avoidance of tax consequences associated with liquidating the account. Rather than creating a taxable event through liquidation, the funds may be transferred, tax-free, to the annuity. The funds are then taxed as payments are made over the term of the annuity. All payments received within a calendar year will be taxable to the owner. This allows the owner to eliminate the IRA as an asset for Medicaid purposes, spread the tax liability over several years, and accelerate their eligibility for benefits.

The DRA also provides preferential treatment to annuities funded with IRAs. In most states, a tax-qualified immediate annuity is not required to be irrevocable, non-assignable, offer equal monthly payments, or be actuarially sound. However, it does usually need to designate the state Medicaid agency as a beneficiary. Annuities funded with retirement accounts are generally non-assignable and irrevocable by nature. However, the client may be able to take advantage of using a term longer than their Medicaid life expectancy or structure the annuity with payments other than monthly (quarterly, annually, etc.).

How it Works in Practice

The basic concept surrounding MCA planning is simple: Fund the excess assets into the immediate annuity to qualify for Medicaid. However, there are always specific considerations that should be accounted for. The two most significant factors when dealing with IRAs and MCAs is ownership of the account, the health status of the applicant, and, in the case of a married couple, the health of the spouse living at home.

In the case of a community spouse owning the IRA, the strategy is straightforward. The IRA is transferred to an MCA, and the asset is eliminated. However, the owner has flexibility with respect to the term of the MCA. As previously noted, the annuity term must be equal to or less than the owner’s Medicaid life expectancy. In states with looser restrictions surrounding taxqualified annuities, the term could be even longer. However, in general, there is no benefit to using an extremely long term, as the state Medicaid agency is most likely the primary death beneficiary in these cases.

The goal is to choose an annuity term that is long enough for the community spouse to reap the economic benefits of the strategy, but short enough that he or she will likely outlive the annuity term to avoid the state Medicaid agency recovering the balance as primary beneficiary. There is no right or wrong answer when trying to determine the appropriate annuity term for a community spouse. Unexpected death or illness can derail any plan for Medicaid eligibility. Therefore, it is essential for attorneys to be diligent in explaining the possible effects of using a shorter term or a longer term and how those effects translate into economic consequences.

Beyond MCA planning for the community spouse, it is possible the institutionalized spouse owns the IRA in question. The biggest concern under these circumstances is the MCA income becoming part of their Medicaid co-pay to the nursing home. Ownership of the account cannot be changed without incurring immediate tax consequences, so the account cannot be transferred to the community spouse.

The benefit of the institutionalized spouse purchasing and MCA over the community spouse is the state Medicaid agency can be named contingent beneficiary instead of primary. The community spouse is the primary death beneficiary and has the right to take control of the funds, eliminating the state Medicaid agency’s claim on the annuity contract.

Whereas choosing the appropriate annuity term for the community spouse is subjective, choosing one for the institutionalized spouse is clear: Go long. Unless the community spouse is in very questionable health, the institutionalized spouse will likely predecease the community spouse. Therefore, the couple should take advantage of the favorable beneficiary rules and reduce the amount of income the MCA produces by choosing a longer annuity term.

In cases where the couple has monthly income below the MMNA, the institutionalized spouse can annuitize the IRA as usual with the intention of shifting the income to the community spouse under the MMNA regulations. To maximize the economic benefit of this option, the attorney or advisor should calculate the couple’s MMNA before implementing the plan.

In cases where the couple has monthly income above the MMNA, the MCA income would become part of the institutionalized spouse’s Medicaid co-pay.9 Though they would lose the income to the nursing home, there is still an economic benefit in securing the community spouse as primary death beneficiary and allowing them to receive the proceeds from the MCA after the institutionalized spouse’s death.

For those who want to avoid any of the MCA income going to the nursing home, the “Name on the Check Rule” may be a viable option. The “Name on the Check Rule” is based on a guideline used by Medicaid to determine to whom income belongs. If the income is payable individually, not jointly, it is considered available only to the respective spouse. In short, the income belongs to the person whose name is on the check. In the context of MCA planning, this guideline can be used to save the institutionalized spouse’s annuity income from going to the nursing home. They can annuitize the IRA and make the income payable to the community spouse only. The institutionalized spouse is the owner and annuitant of the contract, and the community spouse is designated as the payee.

The benefit of the “Name on the Check Rule” is that by naming the community spouse as payee, the institutionalized spouse avoids increasing their income, and the payments do not become part of the monthly Medicaid co-pay. Instead, all income is diverted to the community spouse, who, as previously mentioned, can have unlimited income. Although this strategy is often an excellent solution when an institutionalized spouse owns an IRA, its success can never be guaranteed. Precedence for this strategy exists in just under half of the United States, meaning it does have a high success rate.10 However, caution should always be exercised when attempting the “Name on the Check Rule.”

It is important to note that the “Name on the Check Rule” is not an IRS regulation. In the eyes of the Internal Revenue Service, the income and tax liability is still that of the institutionalized spouse as they are still the owner of the IRA; it is only for Medicaid purposes that the income is attributed to the community spouse.

Utilizing an individual’s full Medicaid life expectancy is typically the most conservative approach in MCA planning, and, as previously mentioned, there isn’t necessarily a benefit in using a term shorter than this (assuming the community spouse is not in failing health). The “Name on the Check Rule” is more likely to be questioned by a Medicaid caseworker if the annuity has a short term that diverts a significant amount of income to the community spouse each month. With the beneficiary rules on the client’s side, it is best to play it safe and use a longer term.

It is also important to maintain the paper trail when using this strategy. Most insurance carriers allow the owner to set up electronic payments for the annuity income. While convenient, it does not provide a caseworker clear evidence as to whose name is on the monthly check. It is best to receive a paper check that can be used to support your client’s case, should it become necessary.

When is an MCA not the Right Fit?

Although MCAs are useful vehicles to protect assets, their use may not always be appropriate. For example, when dealing with an IRA of small value, it may make more sense to liquidate the funds and transfer the net proceeds to the community spouse, as this is typically faster than transferring the funds to an MCA. In that situation, the consequences of liquidating the funds may be offset by medical expense deductions when filing that year’s taxes. If the tax consequences would be minimal, the timing factor may be more important than keeping the IRA intact, given the high average monthly cost of the nursing home.

Conclusion

With more seniors in need of nursing home care and the majority of those individuals being unprepared for the high cost of care, it is more likely than ever that estate planning and elder law attorneys, as well as attorneys of any practice area, will encounter a client that has entered a long-term care facility and is at risk of losing their life savings. The important thing to remember is that they do not have to deplete their money paying the nursing home. More specifically, they do not have to liquidate their IRA to pay for care. They do have options, though seeking advice from a properly trained professional is key to a positive outcome.

Note: Always consult a tax expert before making any decisions pertaining to IRAs.

Dale Krause, J.D., LL.M. is the President and CEO of Krause Financial Services—a firm that specializes in assets preservation solutions, education, and resources for long-term care, including Medicaid Compliant Annuities, Long-Term Care Insurance, and more.

Endnotes

1. Genworth Cost of Care Survey 2021, conducted by CareScout® , November 2021, available at: https://www.genworth.com/aging-andyou/finances/cost-of-care.html.

2. Some states employ “waiver” programs which extend long-term care Medicaid benefits beyond skilled nursing homes, including assisted living facilities and at-home medical care programs.

3. 2022 SSI and Spousal Impoverishment Standards, available at: https://www.medicaid.gov/federal-policy-guidance/downloads/ cib06022022.pdf

4. See n. 3.

5. This figure includes the maximum Community Spouse Resource Allowance of $137,400 and the average Individual Resource Allowance of $2,000.

6. Pub. L. 109-171 (S. 1932) available at: https://www.congress.gov/ bill/109th-congress/senate-bill/1932

7. Medicaid life expectancy is typically determined by the Actuarial Life Table published by the Social Security Administration, though some states use state-specific life expectancy tables.

8. Most cases require the state Medicaid agency be designated the primary death beneficiary on a Medicaid Compliant Annuity. Exceptions exist in cases where the owner has a minor or disabled child, or in situations where the person in the nursing home purchases the MCA and they have a community spouse at home.

9. The Medicaid co-pay (sometimes referred to as the Patient Liability) is the amount the Medicaid recipient is responsible for attributing to their cost of care. It is determined by deducting certain medical expenses, a shift in income under the MMNA rules (if applicable), and a small Personal Needs Allowance from their monthly income.

10. Per the experience of Krause Financial Services.

SUMMER 2022 eReport