5 minute read

Resource Markets Since Pandemic

RESouRCE mARkEtS SinCE pAndEmiC outbREAk

whAt’S hAppEnEd, why And whERE wE ARE Right now

The resources sector has performed strongly for the past two years, recovering strongly from the pandemic lows of early 2020, and this momentum culminated in a very strong Q4 2021 performance, which in turn has generated positive momentum into 2022. This scenario is reflected in the robust performance of the Bloomberg Commodity Index over the past couple of years.

In the immediate pandemic environment of 2020, we initially saw China doing most of the heavy lifting as far as commodity demand was concerned, boosted by government stimulus measures. This led to record prices of iron ore, in particular. The bulk commodity has been a key ingredient in China’s economic growth policy for decades, used in residential construction and steel production on a mammoth scale.

Iron ore prices have eased significantly from their

peak however, as China cleaned up its environmental act ahead of the Beijing Winter Olympics, and simultaneously sought to jawbone prices in a downward direction. But iron ore ominously seems to be regaining some of its lost momentum, as markets anticipate a rebound in China demand post the Olympics.

During 2020, we also saw gold outperforming the rest of the commodity space, as investors sought the security of gold bullion at a turbulent time, with the spot price reaching an all-time high around US$2,030 per ounce. 2021 by contrast, however, was a somewhat disappointing year for the precious metal, but this was not entirely surprising as financial markets adopted a ‘risk-on’ mentality into 2021.

We began to see rest-of-the-world commodity demand begin to play catch-up towards the latter stages of 2020 and into 2021, driven by government stimulus measures to reboot economies, especially in terms of future-facing industries like renewable energy.

A dramatic increase in industrial production led to a spectacular increase in energy demand, which has since translated into multi-year highs for all types

A dramatic increase in industrial production led to a spectacular increase in energy demand, which has since translated into multi-year highs for all types of energy during Q4 2021 and into 2022 – including crude oil, natural gas, thermal coal and uranium, as well as electricity costs throughout Asia, Europe and North America.

of energy during Q4 2021 and into 2022 – including crude oil, natural gas, thermal coal and uranium, as well as electricity costs throughout Asia, Europe and North America.

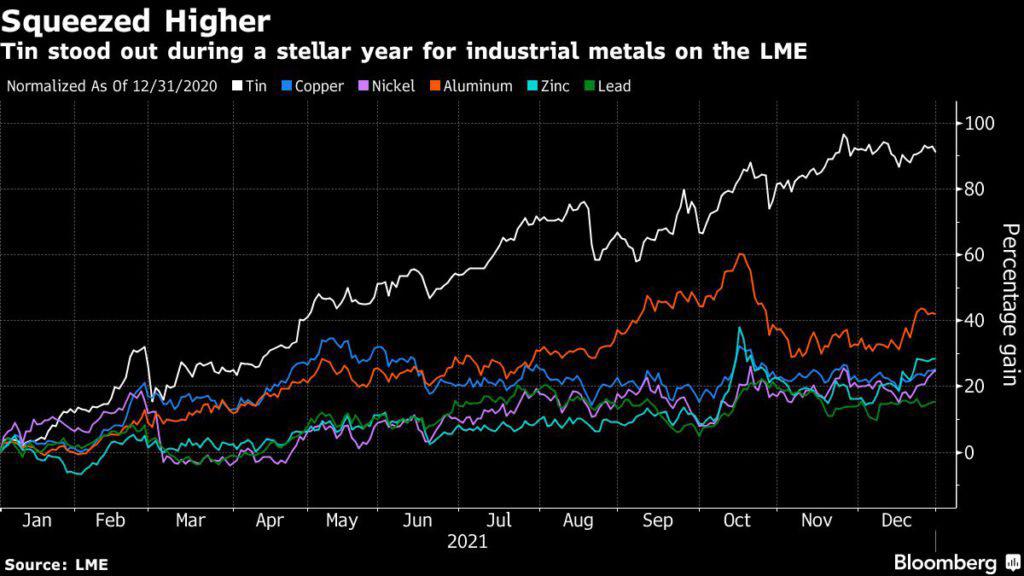

Simultaneously, a whole host of industrial metals also soared to record highs during Q4 2021, with some maintaining their momentum into 2022. Their performance has been driven by traditional near-term demand factors, as well as an understanding that end-users want to get their hands on supply now

due to the medium and longer-term prospects for metals-intensive green energy.

We’ve also seen the emergence of inflation as a major influence in the global economic recovery, which is not surprising given the rising cost of production inputs such as energy, raw materials, and also transportation costs. And the consequences of this are clear. The cost of production is escalating rapidly, and these additional charges are being

passed on to consumers. It is also clear that many central bankers have underestimated (and continue to underestimate) the prospect of inflation.

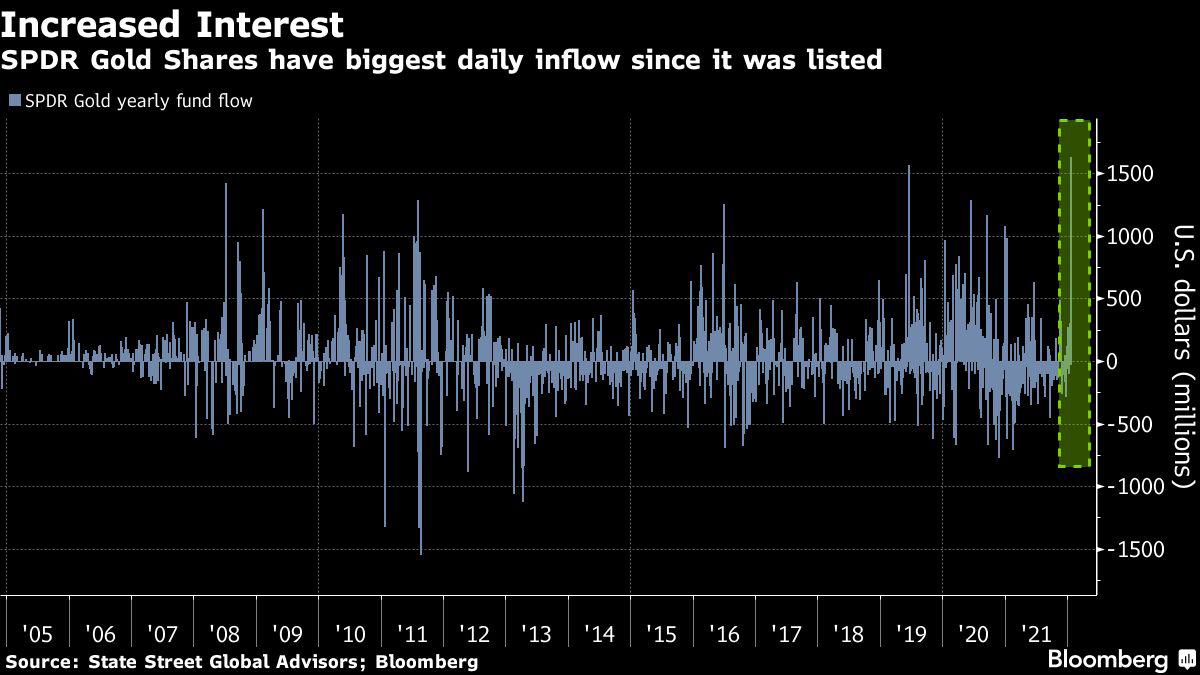

In terms of where we sit presently in early 2022, the outlook for the commodity sector remains robust, driven by positive fundamentals in terms of strong demand and supply shortages. If we look for example at the six major industrial metals traded on the London Metal Exchange, we see that they are all in a state of backwardation (a situation where buyers are prepared to pay a premium for immediate delivery). traded fund, recently recorded its biggest net inflow in dollar terms since its listing in 2004 — worth $1.63 billion.

And despite expectations for multiple US interestrate hikes this year, markets are betting that ‘real’ interest rates will stay negative. There is a feeling that real yields will remain negative as the Fed struggles to tighten policy enough to push interest rates above inflation.

The year ahead will not be without its challenges for resources markets – with inflation, covid and volatility casting a shadow – but supply tightness with respect to most commodities is likely to continue, generating a supportive environment for commodity prices.

Gavin is based in Sydney, Australia and has followed the fortunes of international resource markets for the past 25 years, covering both equities and commodities, as a research analyst. He believes that the most interesting resource opportunities are typically found at the smaller end of the market, which these days is his exclusive area of focus.

The resource sector is on an inexorable growth path, driven by an ever-increasing world population and modernization of living standards in emerging economies, as well as a significant shift in how we generate energy. This will provide enormous growth in the demand for commodities of all types.

Gavin is the Head of Mining & Metals with research group Independent Investment Research (IIR) and he is the Founding Director and Senior Resource Analyst with MineLife.

For more information about MineLife, please visit: www.minelife.com.au

This situation of backwardation also applies to other commodities at present, like crude oil. Brent crude futures, which soared 50% during 2021, are up a further 15% already in 2022 at seven-year highs of $90 a barrel. Crude oil recently managed to register its biggest January gain in at least 30 years, and also its best monthly gain since February 2021, as robust demand outpaced fresh supply. We are likely to see more OPEC+ supply restraint, with many members unable to meet their currently allowable production quotas. With production capacity tight, inventories low and geopolitics racking several producing regions, oil is hurtling towards $100 a barrel.

After being outshone during 2021 by the energy and industrial metals sectors, it looks as though it’s time for gold to make up the ground it lost. Gold has just received a very bullish sign from investors who are returning to the precious metal in a big way. SPDR Gold Shares, the largest bullion-backed exchange-