Market Update

January 2025

Poultry

Cooked Meats

Seafood Dairy

Bakery

Canned + Dried

Beverage + Impulse

Fresh Produce

Catering Supplies

•

•

•

•

•

•

•

January 2025

Poultry

Cooked Meats

Seafood Dairy

Bakery

Canned + Dried

Beverage + Impulse

Fresh Produce

Catering Supplies

•

•

•

•

•

•

•

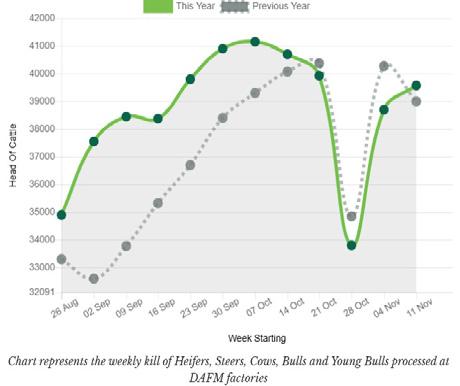

Beef pricing continues to rise:

• Imports of South African beef into Europe have declined, driving increased demand and boosting exports by 4%

• European production is down 1% year-on-year

• Irish cattle price inflation is projected at 6% year-on-year (2024-25)

• Kill numbers are down 4% year-on-year

• Prime cattle weights have decreased by approximately 6% year-on-year

• UK cattle prices are around €1.10/kg higher than Irish prices

• Irish cattle supplies are expected to tighten in the short to medium term

• Strong demand continues from key export markets

• Non-meat inflation, particularly in energy and labour, is contributing to market price increases.

Sysco provides a wide range of beef options and alternative cuts to help you navigate rising prices. Contact your ASM for more information.

The pork market remains stable, though commodities can be volatile:

• Supply is expected to remain steady in the coming weeks

• Slaughter numbers and weights are anticipated to remain stable

*Source: Bord Bia

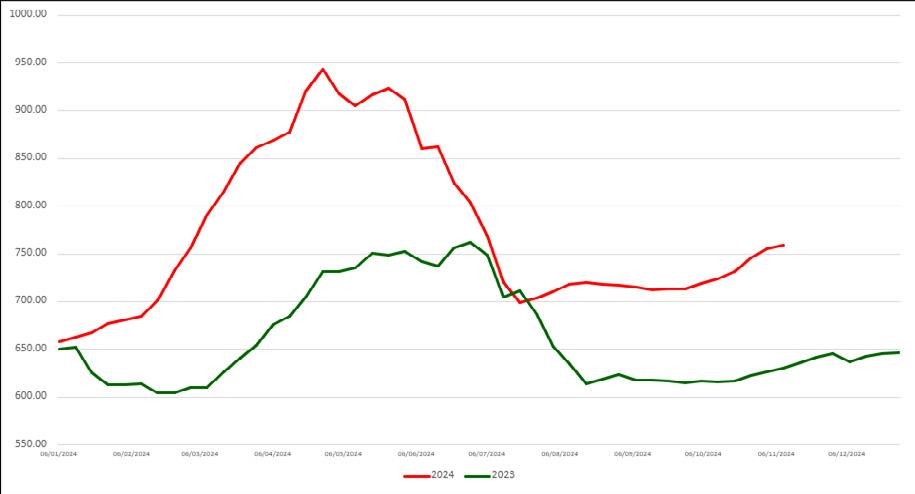

Irish lamb prices are averaging 20.4% higher year to date compared to last year, with the trend expected to continue into 2025 due to:

• Rising livestock prices

• Higher input costs for farm suppliers

• Poor grass growth, leading to lambs finishing later and lighter, reducing overall supply

• Australian and New Zealand lamb being redirected to other markets, increasing demand in Europe

• A significant decrease in forecasted available livestock numbers

*Source: Bord Bia

Sysco can offer frozen alternatives for leg of lamb. Speak to your ASM for more information.

The fresh poultry market witnessed price increases of approximately 4% in Q4 2024. In Q1 2025, fresh poultry prices are expected to experience a slight downward movement before rising again as the barbecue season approaches. Frozen products, including fillets and processed chicken, will see increases of approximately 7% in January 2025.

Throughout Q4 2024, the European market experienced exceptionally high demand for several cuts, such as breast fillets, inner fillets, and leg meat, particularly in the Netherlands, Germany, Denmark, and France. Polish chicken breast prices have increased by 20% year-on-year.

Countries outside Europe, such as the Middle East, China, and Mexico, are offering elevated prices for EU and globally produced poultry, making it challenging for EU countries to secure stock at reasonable costs. Flooding and a Newcastle disease outbreak in Brazil have put increased pressure on the EU market exports.

Rising feed costs month-over-month could lead to an increase in chicken production costs in 2025.

EU chicken meat consumption is expected to increase by 2.2% year-over-year, reaching 12.6 million tonnes (carcass weight equivalent) in 2024, driven by both retail sales and consumption in the foodservice sector.

According to the European Commission, EU chicken exports are forecast to decline by 1% year-over-year in 2024.There have been increasing numbers of Highly Pathogenic Avian Influenza (HPAI) outbreaks across several European countries, reducing the quotas of birds available for export from affected countries.

No frozen turkey stock has been available throughout the EU market since the start of Q4, as suppliers have not frozen any stock due to strong demand and pricing for fresh turkey.

• Polish and German fresh male lobe and butterfly prices have increased by roughly 52% since September 2024. A salmonella outbreak on Polish farms is preventing exports, coupled with huge demand from France.

• One Polish producer lost over 200 metric tonnes of turkey in September due to salmonella issues, lowering export volumes, as volume recovery is slow due to bird placements month-over-month.

Pricing is expected to remain strong into the first quarter of 2025 but will see some deflation of around 5% coming into the New Year and will continue to stabilise.

Duck continues to see stabilisation in the market coming into Q1 of 2025.

Effective January 2025, we will experience price increases for the first time since early 2022 from our primary Spanish charcuterie vendor, Noel. These increases average 25% across their product range. Although these price changes taking effect in January may seem significant, they are in line with movements in the Spanish pork market over 2022 and 2023, during which our prices remained unchanged.

Over the past two years, the Spanish market has faced inflationary pressures on various aspects impacting production costs. These factors include, but are not limited to:

1 Pork price inflation

2 Approximately 20% increase in packaging costs

3 Approximately 8% rise in labor costs since our last price change

4 Escalating energy prices

To help support our customers throughout the month of January, we have worked with Noel to provide promotions across some of the product lines impacted by these increases.

Pork price inflation in 2023 has surpassed any historical data for pork. The 52wk average pork price is +49.5% above 2021.

• Spanish pork prices are published weekly and can be tracked on various portals

• Pork inflation 2022 is driven by cost of production as energy as well as feed have seen unprecendented cost increases

• The driving force behind 2023 price increases has been reported as an uplift in demand alongside the continued tightening of supply. Production of pig meat in the EU was the lowest volume recorded in over a decade in 2023, at 20.6 million tonnes €1.90

Salmon prices increased throughout November and December as European smokers prepared for the festive season. Prices are expected to remain elevated into the New Year, with no significant reductions anticipated until approximately February.

High demand across Europe persists, while limited harvests from farms will require several weeks to replenish stock levels.

The cod market has been highly volatile, with minimal catches reported in Irish waters. Most purchases have come from Scottish auctions, where prices can fluctuate by up to €1/kg.

A 31% reduction in the Barents Sea cod quota has been recommended for 2025, likely adding further pressure to prices.

Hake is being landed primarily by Spanish vessels fishing in Irish waters, with limited landings from Scottish or Irish vessels. Strong demand in Spain is driving up prices, adding pressure to this already constrained market.

Prices remain elevated due to stagnant catch levels, with no significant increases reported.

Prices and availability of all seafood species remain influenced by various factors, including demand, quotas, and catch levels.

The combination of weakened supply and increased demand has caused the markets to further strengthen to levels not seen since 2022. The market remains volatile and will continue into the early part of 2025.

Irish milk supply for the first six months was down 7%, representing a significant drop year on year. It is estimated the total reduction for 2024 to finish at -3%. These reductions are on the back of a weakened base in comparison to the milk supply in 2023.

• The global dairy markets remain uncertain, and we have seen price volatility

• Irish supply has been down due to 12 months of extremely poor weather

• The CSO has also confirmed that milk intake from January to September 2024 has declined by -4.1% when compared with the same period in 2023

The milk prices in the table below are those quoted by co-ops for the month of September (2024).

Source: Agriland

Butter prices remain at record highs, with a significant increase since January 2024. Prices have risen from €5,500/ tonne to €8,375/tonne, representing a staggering 52% increase and a year-on-year change of over 45%.

Graphs below illustrate the impact of butter price increases over the past 18 months.

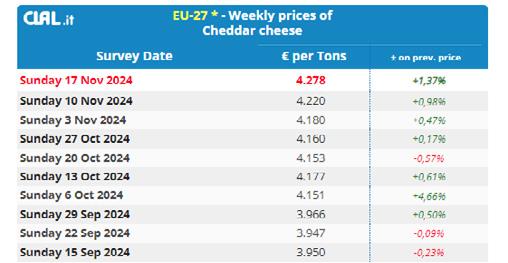

Cheddar

Shifts in demand have influenced valorization, driving changes in pricing for individual commodities. This has led to reduced production of Irish Cheddar in 2024, as butter yields higher milk prices and commands greater volumes.

Prices are expected to remain firm into Q3 2025. Over the past 10 weeks, Cheddar prices have risen by 8% due to limited availability.

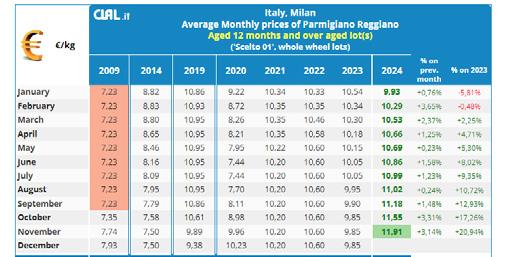

Italian Cheese

Italian cheese prices are under pressure due to raw material shortages, which have reduced production and limited availability of finished products.

Prices have consistently increased month-on-month since January 2024.

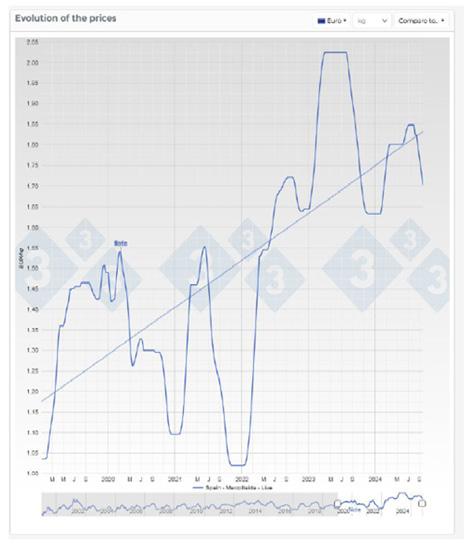

In November, the average price of wheat increased by 7.1% month-on-month and increased by 4.2% year-on-year.

The recent price increase is due to heavy rainfall in parts of southern Russia, but overall, the US Plains helped winter wheat planting and eased concerns over dryness for the 2025 harvest. As the graph illustrates, wheat prices are trending downward after a significant spike.

However, the factor keeping the cost high is gluten. The new season crop had low gluten levels. As a result, additional raw material had to be purchased at an additional cost to increase the gluten content of the flour for bakery lines.

In December, sugar contract prices increased by 8.4% month-onmonth but were 16.9% lower year-on-year. This decline has been reflected in reduced sugar commodity prices in the market.

However, unseasonal rain may cut Brazil’s sugar season short, tightening supply and raising concerns about potential deficits in early 2025.

*Mintec Source

Cocoa prices reached record highs over the summer but have since begun to decline slightly.

Despite this, suppliers remain locked into longer contracts to secure supply, preventing any noticeable reduction in market prices for the time being.

*Mintec Source

• Walnuts: A smaller Californian crop this season, coupled with a poor Chilean harvest, has reduced walnut availability.

• Sultanas: Lower-than-expected yields and quality issues caused by rainfall during drying periods make it challenging to secure long-term contracts.

• Almonds: Production is at its lowest since 2020. Prices are expected to remain firm in the fourth quarter, pending next season’s crop.

• Cashews: Vietnam’s crop is down 20% due to El Niño, resulting in supply shortages.

• Coconuts: Prices have steadily risen over recent months as climate conditions have reduced yields.

• Cherries: Another poor crop year in Italy, Spain, and Eastern Europe has limited availability.

• Blueberries: Rising prices are driven by labour shortages, higher wages, and the warmer El Niñoinfluenced weather.

• Strawberries: A brief and intense flowering period led to a short harvest.

• Raspberries: Rain showers lowered fruit quality, with more defects and fewer whole berries, causing an early harvest end and worsening anticipated shortages.

• Blackberries: Heatwaves following rain showers led to sunburned fruit and reduced quality overall.

• Pineapple: Costa Rica is experiencing low availability due to El Niño. Natural flowering that typically boosts supply has failed to improve volumes.

• Rhubarb: Poland’s rhubarb harvest was hit by persistent cold nights and low precipitation, cutting yields by over 60%.

• Mango: Increased fruit drop during the setting stage has significantly lowered yields, leading to price hikes.

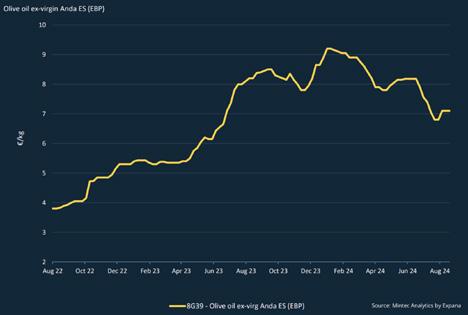

After a period of volatility in the market, inflationary pressures have eased on some key commodity areas, namely Oils, Pasta and Rice.

Prices are expected to decrease ahead of a bumper crop in Spain this harvest. However, caution must be exercised when selecting supply partners to ensure crop quality.

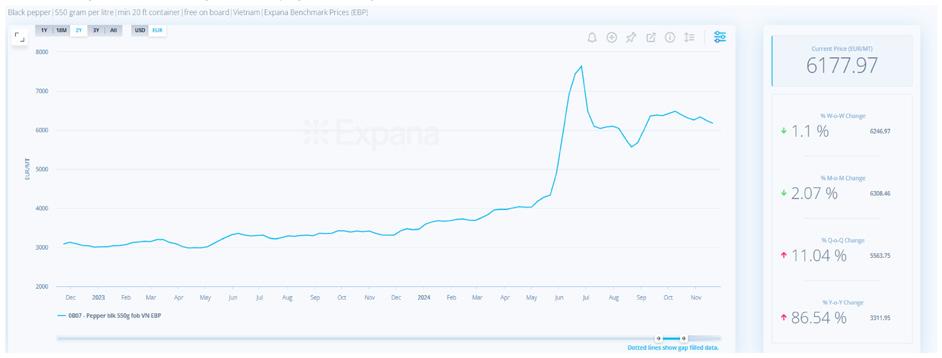

Significant price increases have occurred due to climate activity (super typhoons and tropical storms resulting in flooding) in key growing areas.

Source: Mintec December 2024

After a period of volatility in the market, inflationary pressures have eased on teas. While pressures on soft drink prices resulting from the Government’s Deposit Return Scheme (DRS) have stabilised, other challenges persist in core juice-based products. Coffee and confectionery products should be highlighted, as manufacturers face higher costs for key ingredients.

Global coffee prices remain at an all-time high, primarily driven by unfavourable weather conditions and poor crop yields. Arabica and Robusta prices have increased throughout November and December.

Tight supply has made it increasingly difficult to source apple concentrate, causing a 48% increase in pricing.

Source: Mintec December 2024

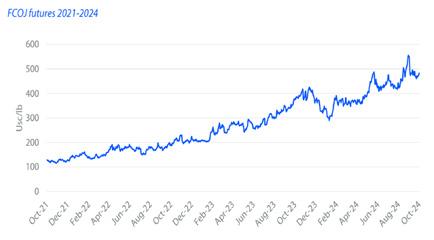

Concentrated orange juice prices remain very strong, further pushing up pricing. Manufacturers are seeking blended alternatives to counterbalance these increases; however, market movements are still evident. Weather conditions, rainfall, temperatures, and crop yields have all contributed to these increases.

Adverse weather conditions have significantly impacted the availability of key fruit and vegetable products in recent weeks, a trend expected to continue due to ongoing cold weather.

As winter progresses, reduced availability and increased demand for Dutch and Spanish onions are driving upward pressure on prices.

Heavy rains and storms in Valencia during late October and early November, followed by unseasonably mild weather in late November, have severely affected the quality of oranges and clementines. Growers are actively addressing these issues by adjusting post-harvest treatment methods to maintain quality.

Retail demand and consumption have rebounded with the arrival of colder weather. The foodservice sector is ramping up in preparation for the Christmas season, driving increased demand for peeling produce. Some pressure has come on price as harvest was timely this year, however, yields are reported to be average, especially on later planted crops.

In Northern Europe, efforts to clear problem lots in storage are softening market trends, although prices remain stable. However, issues with late-planted and late-lifted crops are becoming more prevalent. Dry samples are showing firmness, with some higher values reported this week.

The seed market remains exceptionally tight this year. Where stocks are available, priority is being given to repeat buyers. Export demand from the Canary Islands is described as steady by some buyers and very strong by others.

The average price of Kraftliner remained flat monthon-month in October, rising 13.5% year-on-year to €924/mt. Contrary to expectations, demand did not increase, and paper pulp prices fell by 2% during October. Similarly, Testliner, Fluting, and Cartonboard prices have remained stable since April 2024.

This stability is reflected in disposables and packaging, with most prices holding steady. While some packaging lines experienced slight price increases over the summer, primarily due to freight costs, these have now stabilised. A reduction in prices is anticipated in early 2025 as container shipping costs return to more manageable levels.

In October, the average price of EU HDPE and LDPE rose slightly by approximately 0.5% month-on-month and remains slightly elevated compared to last year. PET and PP prices have stayed relatively stable both month-on-month and year-on-year.

Pricing across plastic products, including refuse sacks and disposable packaging, has remained steady. With decreasing container shipping costs, some price reductions are expected as we move into 2025.

Source: Mintec

Aluminium prices remain significantly elevated, up 18% year-on-year and rising 6.2% over the past three months. However, we have successfully mitigated these increases, keeping prices for foil and foil containers stable.