1 minute read

PARK CITY YEAR END REPORT | 2022

Park City real estate experienced an interesting and somewhat insulated journey during 2022. The first half of the year was marked by a continuation of the surging demand experienced over the last several years that has defined this and other elite resort communities. The second half experienced a return of rationality to the consumer but not an erosion of values beyond a very few.

Ultimately, 1170 residential transaction represents the fewest for the region in over a decade. While saturated demand underlies this slow down, limited supply remains the greatest constraining factor.

They year began with historically tight supply only to loosen just enough midyear for consumers reclaim just enough leverage to make informed purchasing decisions. The spring influx of supply, typical for this and all resort markets, did not backfill as well priced listings were absorbed by opportunistic buyers throughout spring and fall. Heading into the new year, the count of residential listings stands at just 344, or just under 3 months supply. While this is a dramatic increase relative to the beginning of 2022, it still represents market conditions that favor the seller.

As is typical of a changing market, asking prices lagged the changing market dynamics giving rise to extended days on market and a greater span between ask and selling prices. Days on market grew from 36 to 53 between H1 and H2 while discount rate grew from 2% to 6.5%.

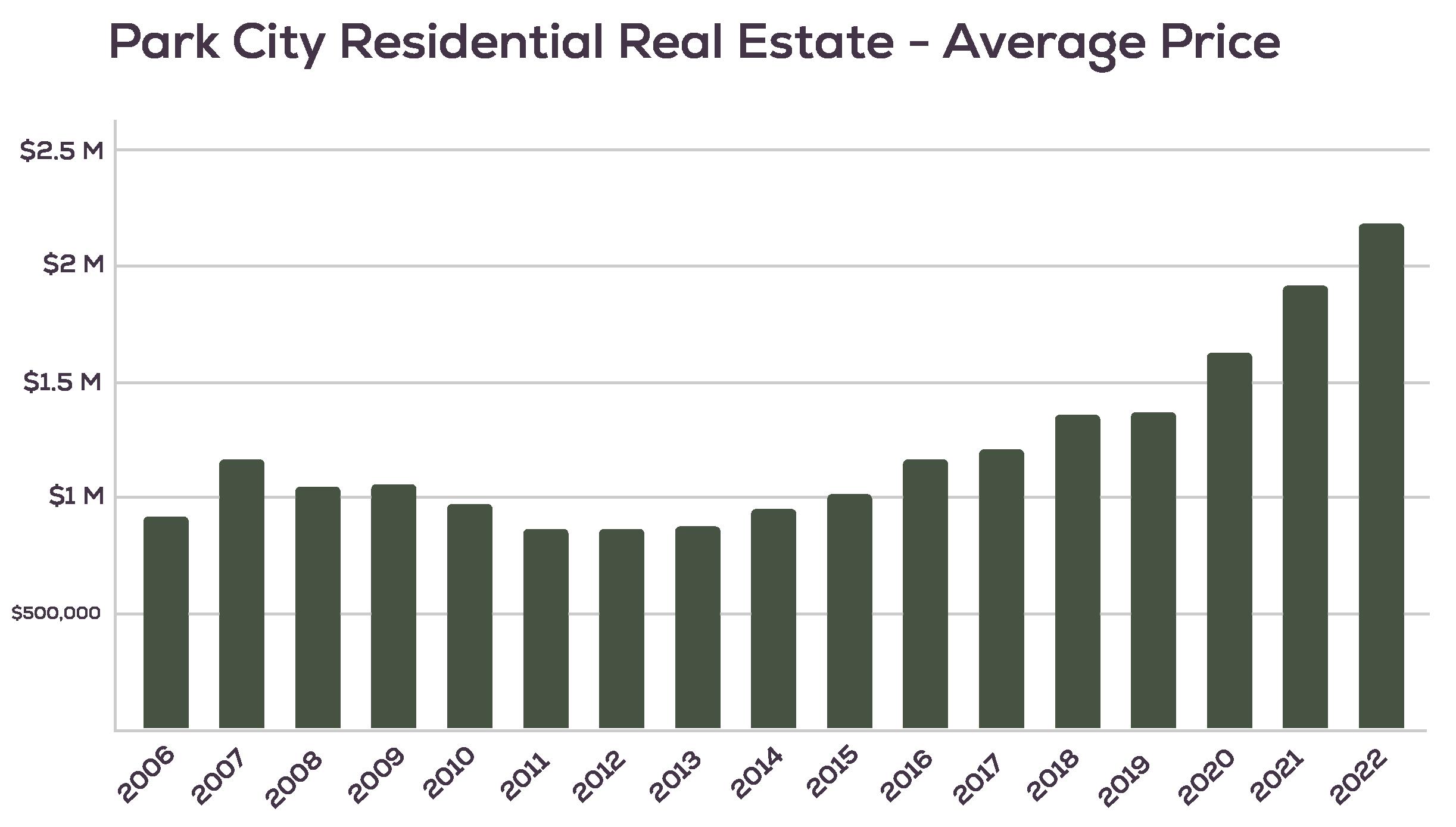

Nevertheless, property values have largely held in the absence of any perceptible distress and exceptionally high utility among property owners. Year over year, median price increased by 22% to $1,525,000 while average price grew by 14%. Notably, elite real estate captured an ever-growing portion of all sales. While total residential transactions dropped by nearly 50% from 2021, properties trading above $1,000,000 were down only half that amount. In fact, sales greater than $1,000,000 accounted for 71% of all residential transactions. In 2021, this amount was 71%.

Market leading transactions were distributed throughout the community including $39,600,000 in Colony, $16,850,000 in Deer Crest and $16,000,000 in Old Town. In total, 10 transactions eclipsed $10,000,000 the most ever in a year excluding 2021.

The outlook for 2023 is decidedly mixed. Despite headwinds in the housing sector, there remains steady demand and capacity to purchase. Very high usage and exceptionally little distress, whether mortgage carry burden or other forms of liquidity, equate to mostly stable pricing. Look for the typical surge in new listings at the end of ski season which could lead to prices drifting slightly lower as longer sales cycles equate to increased days on market.