Legal and Practical Scenarios for taxing

Real-Estate Industry

21st May 2024

Khandhar Mehta & Shah

CA. Rashmin Vaja

Khandhar Mehta & Shah

CA. Rashmin Vaja

Taxability Pre & Post 31-03-2019

Applicability of GST on various charges collected by Developers

Condition to be fulfilled for a New Residential Project (RREP & REP)

Taxability of Transferable Development Rights and Transfer of Development Rights

Taxability of Long-term Lease of 99 Years

Re-development models – Taxability & Valuation

ITC Reversal as per Rule 42 (Pre & Post 31-03-2019)

Plotting of Land and its intricacies

Recent Litigation matters for Builders/Promoters

Agenda

Indirect

Taxable Event Manufacture Provision of Service Import & Export Sale of goods within State Inter-State Sales On Entry of Goods in a state Supply

Authority for levy of Tax

Entry No. 84, List I, Schedule VII

Residuary

Entry No. 97, List I, Schedule VII

Entry No. 83, List I, Schedule VII

Entry No. 54 of List II (VAT) and 92A of List I (CST)

Entry No. 92A of List I of Schedule VII

Entry No. 52 of List II, Schedule VII Article 246A Part XI

Tax Excise Duty Service Tax Customs Duty Sales Tax / VAT Central Sales Tax (CST) Entry Tax (Octroi) Goods and Services Tax

Taxation under statue Nature of

Ideal Taxation & Constitutional Background

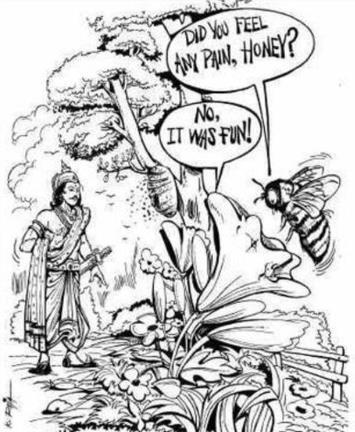

“Ved Vyas in his famous epic ‘Mahabharat’, about tax in ‘Ramarajya’, said that ‘the state tax be such which should not prove to be a burden on the subject; the King should behave like those bees which collect honey without causing harm to the tree.

-Justice Vineet Kothari while citing the Mahabharata in Karnataka Karsamadhan Judgement

Entry 49 of List II of Seventh Schedule - Article 246 -Taxes on lands and buildings is a State subject.

However, Article 246A of the Constitution grants concurrent powers to both the Center and the States to make laws regarding taxes on goods and services, which are overriding powers.

Article 366(26A) of Constitution defines Services means anything other than ‘goods’ –Whether “services” can cover immovable property ??

As per para 6(a) of Schedule II of CGST Act, works contract shall be treated as supply of service

As per Article 366(29A) of Constitution of India, tax on transfer of property in goods involved in execution of works contract is deemed to be sale of goods

Basic understanding of Construction Sector under GST

Coverage under definition of Goods and Services

“goods” means –

• every kind of movable property

• other than money and securities

• but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply.

“services” means –

Anything other than goods, money and securities but includes activities relating to the use of money or its conversion by cash or by any other mode, from one form, currency or denomination for which a separate consideration is charged;

[Explanation : For the removal of doubts, it is hereby clarified that the expression “services” includes facilitating or arranging transactions in securities;]

“works contract” means –

a contract for building, construction, fabrication, completion, erection, installation, fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any immovable property wherein transfer of property in goods (whether as goods or in some other form) is involved in the execution of such contract;

Section 7 prescribes Scope of Supply. It is very wide term which also includes sale, transfer, barter, exchange, license, rental, lease or disposal of goods or services for a consideration in course of furtherance of business.

Meaning of term “Services” is limited ?

What to consider – Goods or Services ?

Schedule II provides the list of activities to be treated as supply of goods or supply of services

Clause

5. Supply of services

The following shall be treated as supply of services, namely:-

(a) renting of immovable property;

(b) construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or after its first occupation, whichever is earlier.

Hence, where consideration (part or other) for a unit/flat received before Completion Certificate, it will be considered as supply of services and GST will be applicable. Where entire consideration for a unit/flat received after Completion Certificate, it will be treated as neither supply of goods nor supply of service and GST will not be applicable

Schedule III provides the list of transaction which should be treated neither supply of goods nor supply of service, which includes:

a) Sale of Land [in service tax “immovable property” was excluded, which means land and its rights]

b) Sale of Building, i.e., residential or commercial units where completion certificate is received

Hence, where completion certificate is not received in case of residential or commercial units, GST will be applicable.

‘Immovable Property’ ‘Land’

STATUTE DETAILS

Section 2(26) of General Clauses Act, 1897:

Section 2(z) of Real Estate (Regulation and Development) Act, 2016:

“Immovable Property” shall include land, benefits to arise out of land, and things attached to the earth, or permanently fastened to anything attached to the earth

“Immovable Property” includes land, buildings, rights of ways, lights or any other benefit arising out of land and things attached to the earth or permanently fastened to anything which is attached to the earth, but not standing timber, standing crops or grass.

Section 3 of Transfer of Property Act, 1882: “Immovable property" does not include standing timber, growing crops or grass.

Section 2(6) of Registration Act, 1908:

Section 3 (p) of The Right To Fair Compensation And Transparency In Land Acquisition, Rehabilitation And Resettlement Act, 2013

“Immovable property” includes land, buildings, hereditary allowances, rights to ways, lights, ferries, fisheries or any other benefit to arise out of land, and things attached to the earth or permanently fastened to anything which is attached to the earth, but not standing timber, growing crops nor grass.

“land” includes benefits to arise out of land, and things attached to the earth or permanently fastened to anything attached to the earth;

Section 3(4) of Bombay Land Revenue Code, 1879: ‘land’ includes benefits to arise out of land and things attached to the earth or permanently fastened to anything attached to the earth and also shares in or charges on the revenue or rent of village or other defined portions of territory”

Transaction Whether GST is payable ?

Sale of Land

Sale of Building

Sold either as it is or after some development such as levelling, laying down of drainage lines, water lines, electricity lines, etc. No

Where entire consideration is received after issuance of Completion Certificate (CC or BU)

Where full or part consideration is received before issuance of Completion Certificate (CC or BU)

After BU Booking No

Before BU Booking Yes

Contd…

Works Contract Services Yes Unit Payment Received Before CC Payment Received After CC GST will be levied on Taxability A - Rs. 50,00,000/- - Exempt B Rs. 30,00,000/- Rs. 20,00,000/- Rs. 50,00,000/- Taxable C Rs. 50,00,000/- - Rs. 50,00,000/- Taxable

Example:

Construction Sector under GST

GST Rate Upto 31-03-2019

Residential Complex

Commercial Complex

Affordable Units

GST @ 8% with ITC

Non-affordable Units :

GST @ 12% with ITC

GST @ 12% with ITC

GST Rate from 01-04-2019

Residential Complex

Commercial Complex

Affordable Units

GST @ 1% without ITC

Non-affordable Units :

GST @ 5% without ITC

GST @ 12% with ITC

Rate of Tax – Construction Services

Rate of Tax- Works Contract Services Works Contract under GST GST @18% with ITC On Service Portion in execution of Works Contract Service Tax @ 15% Works Contract Service under Service Tax On Total Amount - In case of Original Works On Total Amount - In case of Maintenance and repairs Service Tax @ 6% after considering abatement Service Tax @ 10.50% after considering abatement

Residential Real Estate Project (RREP)

Real Estate Project (REP)

Carpet Area (as per RERA) of Commercial apartment is not more than 15% of the Total Carpet Area

Carpet Area (as per RERA) of Commercial apartment more than 15% of the Total Carpet Area

Types of Project – 01-04-2019 onwards

1. Entirely

2. Commercial

Affordable Housing 3. Commercial + Non-affordable Housing 4. Affordable Housing + Non-affordable Housing + Commercial

Commercial Project

+

1. Affordable Housing 2. Non-Affordable Housing 3. Affordable Housing + Non-Affordable Housing 4. Affordable Housing + Commercial 5. Non-affordable Housing + Commercial 6. Affordable Housing + Non-affordable Housing + Commercial

GST Rates w.e.f. 01-04-2019 – New Projects Sr. Type of Project Referred as Effective Rate of Tax* 1 Affordable Housing Project RREP 1% 2 Non-Affordable Housing Project (Normal Residential Project) 5% 3 Carpet Area of Commercial Apartments is upto 15% of total carpet area a) Affordable RREP 1% b) Non-Affordable 5% c) Commercial Part 5% 4 Carpet Area of Commercial Apartments is more than 15% of total carpet area a) Affordable REP 1% b) Non-Affordable 5% c) Commercial Part 12% *The Value of transfer of land or undivided share of land, as the case may be shall be deemed to be one third of the total amount charged for such supply

GST Rates w.e.f. 01-04-2019 – Ongoing Projects Sr. Type of Project Referred as If Old rate Option is Exercised* If Old rate Option is not Exercised* 1 Affordable Housing Project RREP 8% 1% 2 Non-Affordable Housing Project (Normal Residential Project) 12% 5% 3 Carpet Area of Commercial Apartments is upto 15% of total carpet area a) Affordable Housing RREP 8% 1% b) Non-Affordable Housing 12% 5% c) Commercial Units 12% 5% 4 Carpet Area of Commercial Apartments is more than 15% of total carpet area a) Affordable Housing REP 8% 1% b) Non-Affordable Housing 12% 5% c) Commercial Units 12% 12% *The Value of transfer of land or undivided share of land, as the case may be shall be deemed to be one third of the total amount charged for such supply

Disclosure of Correct Value & Rate in GST Returns

Taxpayer must disclose full GST Rate on 2/3rd Taxable value for

# Type of Project Full Rate of Tax Effective Rate of Tax 1 Affordable Housing Project 1.5% 1% 2 Non-Affordable Housing Project 7.5% 5% 3 Commercial Units 18% 12%

Works Contract 18% 18%

4

Disclosure in GST Return Affordable Non-Affordable Commercial Affordable Non-Affordable Commercial Basic Receipt 1,00,000 1,00,000 1,00,000 1,00,000 1,00,000 1,00,000 Taxable Value 1,00,000 1,00,000 1,00,000 66,000 66,000 66,000 GST Rate 1% 5% 12% 1.5% 7.5% 18% Tax 1,000 5,000 12,000 1,000 5,000 12,000

disclosure purpose in GST Returns.

Recent Gujarat High Court Judgement

MUNJAAL MANISHBHAI BHATT V/S. UNION OF INDIA

The division bench of the Gujarat High Court comprising of Justice J. B. Pardiwala and Justice Nisha M. Thakore has read down Para 2 of Notification No. 11/2017 mandating 1/3rd deduction of Land as ultra-virus.

In recent judgement of Munjaal Manishbhai Bhatt v/s. Union of India, it is held that mandatory adopting 1/3rd of total amount charged towards value of land in construction contracts in cases where land cost is ascertainable “is ultra-vires the provisions as well as the scheme of the GST Law.”

Hon’ble Gujarat High Court opined that application of such mandatory uniform rate of deduction is discriminatory, arbitrary and violative of Article 14 of Constitution of India.

Hon’ble Gujarat High Court held that mandatory deduction of 1/3rd value of land in construction contracts is not sustainable in cases where the value of land is ascertainable or where the value of construction service can be derived with the aid of valuation rules.

Hon’ble Gujarat High Court held that such deduction can be permitted at the option of the taxable person particularly in cases where the value of land or undivided share of land is not ascertainable.

Scenario

Value of Construction Service Value of Land As per contract Land Value as per para 2 of Notification Land Value as held by Hon’ble Gujarat HC

A 1,20,00,000/- 60,00,000/- 40,00,000/- 60,00,000/B 1,20,00,000/- 50,00,000/- 40,00,000/- 50,00,000/C 1,20,00,000/- 30,00,000/- 40,00,000/- 30,00,000/D 1,20,00,000/- Not ascertainable 40,00,000/- 40,00,000/-

Total

Advances, Adjustment & Exempted Supply in Returns

Disclosure of 1/3rd Deemed Value of Land in GST Returns

As per the Valuation provision notified in NN 11/2017, value of construction services is equal to total value charged less 1/3rd value of land. Therefore only 2/3rd value is to be disclosed in GST Returns. Further full rate i.e 1.5% , 7.5% or 18% is to charged & disclosed in GST Returns. In our view, it is recommended not to disclose the 1/3rd portion in GST Returns as exempted.

Said receipt is to be disclosed as exempt supply in GST Returns and ITC reversal wherever applicable in case of ongoing project & commercial project needs to paid.

# Documents Event For whom GSTR-01 Table GSTR-3B Table 1 Value of Invoices On Sale Deed of Unit & Development & other

or Milestone as per agreement For units booked before Completion Certificate or Other Income Table 4 , 5 Table 3.1 (a) 2 Value of Debit Note Table 7 3 Value of Credit note Table 7 4 Value of Advances for

invoice not issued On Receipt of Advances Table 11

Value of Refund Voucher On refund of Advances 6 Value of Advances adjusted against Invoices Adjustment when Invoices issued 7 Bill of Supply for Exempt Supply for Unit booked after BU For units booked after Completion Certificate Table 8 Table 3.1 (c), (e)

Charges

which

5

Disclosure of Receipt of Units booked after BU / Completion Certificate and Pure Sale of Land

Rate of Tax & ITC eligibility in GST Regime

Period Project Type Sale of under Construction Effective GST Rate % ITC Eligibility Payment Mode 01-July-2017 to 31-Mar-2019 Residential Affordable units 8% Allowed Cash / Credit Non-Affordable units 12% Commercial Commercial units 12% 01-April-2019 onwards Residential (RREP) Affordable units 1% Not allowed Cash only Non-Affordable units 5% Commercial units 5% Commercial (REP) or exclusive Commercial units 12% Allowed Cash / Credit

GST on other charges collected by Builder & Society

Composite or Independent Supply

Section 2(30) of CGST Act "composite supply" means a supply made by a taxable person to a recipient consisting of two or more taxable supplies of goods or services or both, or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply;

Section 2(74) of CGST Act "mixed supply" means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply.

Section 2(90) of CGST Act "principal supply" means the supply of goods or services which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary;

Explanation to Notification no. 03/2019 dtd 29-03-2019 :

Gross amount shall be the sum total of; -

B. Amount charged for the transfer of land or undivided share of land, as the case may be including by way of lease or sub lease;

C. Any other amount charged by the promoter from the buyer of the apartment including preferential location charges, development charges, parking charges, common facility charges etc

Section 15. Value of Taxable Supply.-

(2) The value of supply shall include-

(a) any taxes, duties, cesses, fees and charges levied under any law for the time being in force other than this Act, the State GST Act, the UT GST Act and the GST (Compensation to States) Act, if charged separately by the supplier;

(c) incidental expenses, including commission and packing, charged by the supplier to the recipient of a supply and any amount charged for anything done by the supplier in respect of the supply of goods or services or both at the time of, or before delivery of goods or supply of services;

(d) interest or late fee or penalty for delayed payment of any consideration for any supply.

A. ……..

Puranik Builders Limited – Maharashtra AAAR

Question before AAAR:

a. Whether other charges received by the applicant will be treated as consideration for construction services of the company and classified under HSN 9954 along with the main residential construction services of the company or whether the same will be treated as consideration for independent services of the respective head?

b. Consequently, what will be the applicable effective rate of GST on services underlying the other charges?

Ruling delivered by AAAR:

Perception of consumer is an important factor in determining whether the services provided are bundled or not.

AAR refers the Supreme Courts observation “dominant intention test”, intention of contracting parties is of paramount importance.

Test that different elements are integral to one overall supply, if one or more is removed, nature of supply would be affected, has to be satisfied.

Nature of other charges in respect of independent services/ activities which are not inextricably linked and do not fulfill test of composite supply.

• Water Connection Charges

• Electricity meter and deposit for meter

• Development charges • Legal Fees

and

Share municipal Taxes. (after occupancy period)

Formation and registration of org. and legal charges

Share money, application & entrance fees of org.

Infrastructure charges

Inextricably linked and Naturally bundled

Taxable @ the rate of Construction service 1% , 5%, 12%

i. Club House maintenance ii. Advance maintenance iii.

iv.

v.

vi.

Taxable as an Independent Services i.e @ 18%

Not Inextricably linked

Independent Service

Applicability on other charges collected by Builder

Electricity, Sewerage and Water Connection Charges

Common Infrastructure Development Charges

(Road, Fire Safety, Street Light, Playground, Garden etc.)

Customer Advances for Flat / Office

PLC/Floor Rise/ Parking Charges/Legal Charges

Subscription Charges, Booking Fees, Administration Fees

Other Miscellaneous Charges

Club Development Charges / Internal Development Charges / External Development Charges

Interest on Late Payment (Only if actually collected )

Maintenance Deposit

Stamp Duty and Registration Charges

of Club

for Cancellation of Booking

Extra Civil Work Charges

Component GST Applicable GST rate for 1. Res. Unit before 01-04-19 2. Res. Units opted for old rate 3. Commercial Units GST rate for New Project after 01-04-2019 1. Affordable Units 2. Non-Affordable Units

Yes 8% for Affordable Units or 12% for Other Units 1% for Affordable Units or 5% for Other Units

No - -

Yes 18% 18% Charges

Membership

Applicability

on other Charges collected by Society

Various Charges (RWA) Residential Society Commercial Society Maintenance Charges less than Rs. 7500 per unit per month Not Taxable Taxable @ 18% Maintenance Charges more than Rs. 7500 per unit per month Taxable @ 18% Taxable @ 18% Maintenance Deposit Not Taxable Not Taxable Transfer Fees Taxable @ 18% Taxable @ 18% Other Miscellaneous Charges Taxable @ 18% Taxable @ 18% Aggregate Turnover Monthly maintenance Charge (per member) Supply considered as Should RWA register under GST ? GST Applicable or not ? More than Rs. 20 Lakhs Rs. 7500 or less Exempt No No More than Rs. 7500 Taxable Yes Yes Rs. 20 Lakhs or less Rs. 7500 or less Exempt No No More than Rs. 7500 Below Taxable Limit No No Note: (1) Basic Exemption limit of Rs. 20 Lacs shall be applicable to both, Residential as well as Commercial Society (2) In case of Residential Society, exemption of Rs. 7,500 per month per unit is available over and above the basic exemption limit of Rs. 20 Lacs

Affordable Housing Scheme

Affordable Residential Apartment means

Project description

New project commences on or after 01.04.2019

Ongoing project where builder has not exercised option to pay Tax @ 8%

Conditions

a) For Metropolitan cities (Bengaluru, Chennai, Delhi NCR, Hyderabad, Kolkata and Mumbai), area of residential unit must be less than or equal to 60 Square Meters;

b) For Non-Metropolitan cities area of residential unit must be less than or equal to 90 Square Meters; AND

c) Total Value of residential unit (whether in metro or non-metro must be less than or equal to Rs. 45 Lacs)

Ongoing projects covered under any affordable scheme as per earlier Notification

Old Schemes also covered under Affordable Housing:

Jawaharlal Nehru National Urban Renewal Mission or Rajiv Awaas Yojana

Works pertaining to “ln-situ redevelopment of existing slums using land as a resource, under the Housing for All (Urban) Mission/ Pradhan Mantri Awas Yojana (Urban)

works pertaining to the “Beneficiary led individual house construction / enhancement” under the Housing for All (Urban) Mission/Pradhan Mantri Awas Yojana

works pertaining to the “Economically Weaker Section (EWS) houses” constructed under the Affordable Housing in partnership

works pertaining to the “houses constructed or acquired under the CLSS for EWS/LIG/MIG-1/MIG-2

a single residential unit otherwise than as a part of a residential complex

low-cost houses up to a carpet area of 60 square meters per house in an affordable housing project which has been given infrastructure status

a residential complex predominantly meant for self-use or the use of their employees

Example related to Affordable Housing Project:

Total value includes:

Consideration charged for residential apartment:

- Charges towards share of land

- Any other charges by builder such as preferential location charges, development charges, parking charges, common facility charges etc.

Area (sqm) Value (In Lacs) City Affordable Housing or not Rate of GST ITC availability 60 45 Ahmedabad Yes 1% No 50 50 Surat No 5% 100 40 Nagpur No 5% 90 45 Mumbai No 5% 55 35 Noida Yes 1% 50 50 Hyderabad No 5%

Cont….

Conditions for Concessional Rates for New Project & Ongoing Project opted for New Rate

Conditions to be fulfilled for New Rate 1% / 5%

CASH only

GST to be paid by CASH only .

ITC

Maintain project wise inwards (ITC) from registered & unregistered dealer.

Disclosure

ITC not to be availed & shall be disclosed in GSTR-3B every month

Utilization of ITC not allowed. 80% from RD Mandatory to purchase 80% input goods & input services from registered dealer *

RCM on shortfall Tax @ 18% to be paid in shortfall of 80% from RD dealer # Mandatory RD purchase Cement & Capital goods shall be purchase from RD dealer only 20% relaxation Not allowed

* 80% of value of input and input services (excluding TDR, Long term lease, Electricity, HSD, Motor spirit, natural gas)

# Shortfall from mandatory purchase from registered dealer – Taxpayer needs to pay tax @ 18% under RCM and require to submit details in a prescribed form on GSTN by end of the quarter following the financial year i.e. 30th June after end of the financial year

Total six Conditions to be fulfilled on Yearly basis & Project wise for concessional rate of 1% / 5% . 1 2 3 4 5 6

Exclusion & Issues in mandatory 80% threshold :

Exclusion

Notified in notification no. 03/2019 dtd, 29-03-2019

1. Services by way of grant of development rights

2. Long term lease of land (against upfront payment in the form of premium, salami, development charges etc.)

3. FSI (including additional FSI)

4. Electricity

5. High speed diesel, motor spirit, natural gas]

Clarified in Real Estate FAQs issued by CBIC:

1. Purchase of land

2. Salary Cost

Certain other exclusions as per our view

1. Provisions of expenses / write off entries

2. Stamp duty / Franking cost

3. Interest cost (from bank / unsecured loans)

4. Fees paid to government

Issues

Mandatory purchase of 80% to be computed only for Input Goods & Input Services (not applicable on Capital Goods)

Capital Goods are mandatorily purchase from registered dealer.

Tax on new residential units is to be paid @ 1% / 5% in cash mode only and without availing & utilizing ITC (Even if other conditions are not fulfilled)

As per FAQ-II, Inward supplies of exempted goods/services shall be included in the value of supplies from unregistered persons while calculating 80% threshold.

Interest is exempted under GST law, whether interest paid to banks which are registered under GST is to be calculated as supplies from registered or unregistered persons.

Inward from the composition suppliers- whether to include or exclude.

Excess / shortfall from mandatory threshold – not to set off in next year

Review of Mandatory Conditions

Total procurement by a promoter for a project

Non-GST expenditures

TDR, FSI, Lease premium, Salary, Electricity , Depreciation, Provisional items, petrol ,diesel etc.

Exclude it from calculation

Procurement of Capital Goods from unregistered person

Promoter needs to pay GST on Capital Goods under RCM at applicable rates

RCM not applicable

Procurement of goods and services by promoter from registered person ≥ 80% Yes

No

Whether Cement is procured from an unregistered supplier?

Yes

Promoter needs to pay GST on Cement under RCM at applicable rates No RCM not applicable

Promoter is liable to pay GST under RCM for shortfall in criteria of 80% *

Yes

No

A promoter has procured following goods and services for construction of a residential real estate project during the financial year Sr. Name of Input Goods and Services Illustration 1 Illustration 2 Illustration 3 % of Input Goods/services received during the Financial Year Whether inputs received from registered supplier? % of Input Goods/servic es received during the Financial Year Whether inputs received from registered supplier? % of Input Goods/services received during the Financial Year Whether inputs received from registered supplier? 1 Sand 10 Yes 10 Yes 10 No 2 Cement 15 No 15 Yes 15 No 3 Steel 20 Yes 20 Yes 15 Yes 4 Bricks 15 Yes 15 Yes 10 Yes 5 Flooring Tiles 10 Yes 10 Yes 10 Yes 6 Paints 5 Yes 5 No 5 Yes 7 Architect Designing/ CAD drawing etc. 10 Yes 10 Yes 10 Yes 8 Aluminum windows, Ply, Commercial wood 15 Yes 15 No 25 No

Illustrations

RCM in case of supplies from unregistered person

Category of supply of goods and services

Supply of such Goods and Services or both (other than services by way of TDR, Long term lease of land or FSI) which constitute the shortfall from the minimum value of goods or services or both required to be purchased by a promoter for construction of project from the registered person.

Supplier Recipient Rate of tax Time of Supply

Tax is to be calculated for the full financial year or part thereof (up to date of BU) and to be paid till June of next FY.

Supply of Cement which constitute the shortfall from the minimum value of goods or services or both required to be purchased by a promoter for construction of project from the registered person.

Unregistered

Person Promoter

Tax is to be paid on monthly basis in which it is Procured Capital Goods supplied to a promoter for construction of a project.

Applicable Rates

18%

28%

Taxability of TDR & ToDR

“TDR” means – Transferable Development Rights’ (TDR) means certificates issued in respect of category of land acquired for public purposes either by the Central or State Government in consideration of surrender of land by the owner without monetary compensation, which are transferable in part or whole. The TDR Certificate inter-alia should mention the area surrendered and the cost of that area as per the circle rate.

TDR Guideline issued by NITI Aayog read with Para 2.1.46 of Consolidated FDI Policy Circular dated 28-8-2017

“ToDR” means – Transfer of ‘Development Rights’ means supply of ‘Development Rights’, by Owner of the land to a Developer / Builder / Construction Company, for constructing a complex, building or civil structure. Here, the said owner avails the ‘Construction Service’ from such Developer / Builder against a consideration, wholly or partly, in form of the said constructed complex, building or civil structure by getting possession thereof from such Developer / Builder. (In the case of Prahitha Construction Pvt Ltd- High court held that GST is applicable on ToDR. Further, Supreme Court Rejects Stay of demand and direct the petitioner to pay tax on TDR. Further SPL has been accepted for further hearing.)

Abr.

Type

TDR

Transferable Development Rights

ToDR

Transfer of Development Rights

Issuer Public Authority Landowner

Form TDRc Certificate Development Agreement

Purpose In form of Consideration for surrender of rights of land, Slum redevelopment Landowner transfer development rights to promoter/developer for area sharing or revenue sharing

Taxability

Neither Supply of Goods Nor supply of Services as notified 243W/243G

Supply of service taxable under entry at SI. No. 16 (iii) (Heading 9972) @ 18%

TDR or ToDR ?

Journey of Development Rights under GST

(01-07-17 to 31-03-2019)

Initial reference to the word "development rights" appears in Notification No. 04/2018 dated 25-Jan-2018.

It operates under the assumption that a "supply" exists between the landowner and developer & vice versa. Meaning transfer of Development Rights is a “Supply”.

As per Section 13 of CGST Act

Date of transfer of possession or right in the constructed area by entering into a conveyance deed or similar instrument (for example allotment letter)

As per Section 15 of CGST Act & Rules

Supply of Supplier Recipient Consideration Taxable Who is liable Time of Supply Valuation Up to 25-01-2018 25-01-2018 onwards Development Rights Landowner registered under GST Developer Construction Services Yes Supplier under FCM

Construction Services Promoter registered under GST Landowner Development Rights Yes Promoter under FCM NN 04/2018 dtd. 25-01-2018

Journey of Development Rights under GST (01-04-2019 onwards)

NN 05/2019 dtd. 29-03-2019

W.e.f 01-04-2019, the liability to pay GST on development rights shifted from the supplier (forward charge) to the recipient (reverse charge). There will be no liability on part of landowner for transfer of development rights.

Now, Promoter is liable to pay tax on both development rights under reverse charge and construction services provided to landowner under forward charge.

Further, promoters are not allowed to avail or utilize Input Tax credit for payment of tax for Residential Projects.

Supply Supplier Recipient Consideration Taxable Who is liable Time of Supply Development Rights Any Person registered under GST Promoter Construction Services Yes Promoter under RCM Refer next slides Construction Services Promoter Landowner Development Rights Yes Promoter under FCM

Taxability of development rights in different regime

•Immovable Property excluded from the definition of ‘Service’ Service Tax upto 30-06-2017

GST 01-07-2017 to 31-03-2019

•Not Taxable

• Taxable under FCM

• Notification 04/2018 CT (R) 25.01.2018 under Forward Charge Mechanism (FCM)

GST 01-04-2019 onwards

• Taxable under RCM

•Notification 05/2019 CT (R) 29-03-2019 under Reverse Charge Mechanism (RCM)

Transfer of Long-Term Lease of 99 years

Issues covered under Long term lease

Long term lease of Industrial Plots

Long term lease in case of JDA

Long term lease land by Local Authority

Long term lease as a part composite supply of construction of Flat

Transfer of Long-Term Lease of 99 years

In case of Industrial Plots

Granting of Long-term lease

(Plot to Industrial Units)

State Industrial Development Corporation (such as GIDC, MIDC etc.) across the country gives land on long term lease basis (more than 30 years) to industrial units.

Lease deed also permits the lessee to assign his interest in the given plot (for the remaining part of lease) to any other person subject to the approval of State Industrial Development Corporation.

Let's discuss whether GST is applicable on (a) when the industrial plot is initially allotted, and (b) when the original allottee transfers their leasehold rights to another industrial unit.

State Industrial Development Corporation Another Industrial Unit (Sub-lessee) Grant of Long-Term Lease Industrial Unit (Lessee) Assignment / Sub-Lease

Granting of Long-term lease (Original Lease)

State Industrial Development Corporation Industrial Units (Lessee)

Granting of Long-Term Lease of Industrial Plot

Exemption

(Entry 41 of NN 12/2017)

On upfront amount (called as premium, salami, cost, price, development charges or by any other name) payable in respect of service by way of granting of long-term lease of thirty years, or more)

Condition for exemption (Entry 41 of NN 12/2017)

Any violation or change in land use will hold the original lessor, original lessee (industrial units), and any subsequent lessee or buyer jointly liable for the central tax amount that would have been payable on the upfront lease amount, along with interest and penalty. Lease or sale agreements must explicitly state the exemption of central tax on long-term leases and ensure compliance by all parties involved.

Exemption Entry 41 of NN 12/2017- CTR

Upfront amount (called as premium, salami, cost, price, development charges or by any other name) payable in respect of service by way of granting of long term lease of thirty years, or more of industrial plots or plots for development of infrastructure for financial business, provided by the State Government Industrial Development Corporations or Undertakings or by any other entity having 20 per cent. or more ownership of Central Government, State Government, Union territory to the industrial units or the developers in any industrial or financial business area]

Explanation.- For the purpose of this exemption, the Central Government, State Government or Union territory shall have 20 per cent. or more ownership in the entity directly or through an entity which is wholly owned by the Central Government, State Government or Union territory.

NIL

Provided that the leased plots shall be used for the purpose for which they are allotted, that is, for industrial or financial activity in an industrial or financial business area:

Provided further that the State Government concerned shall monitor and enforce the above condition as per the order issued by the State Government in this regard:

Provided also that in case of any violation or subsequent change of land use, due to any reason whatsoever, the original lessor, original lessee as well as any subsequent lessee or buyer or owner shall be jointly and severally liable to pay such amount of central tax, as would have been payable on the upfront amount charged for the long term lease of the plots but for the exemption contained herein, along with the applicable interest and penalty

Sn Chapter Heading Description of Service Rate Condition 41 Heading

9972

Assigning of lease hold right (Sub-Lease)

Industrial Units (Original Lessee)

Assigning of lease hold rights in Industrial Plot

Another Industrial Units (Sub-Lessee)

Taxability

Department View:

• Across the country, tax authorities are issuing notices to industrial units (sub-lessees) for not eligible for exemption for this transaction of assignment of lease. Hence, tax authorities have started demanding GST @ 18% on the lease arrangement between original lessee and sub-lessee.

GCCI (Gujarat Chamber of Commerce & Industry) has filed writ petition challenging the applicability of GST on transfer of leasehold land in GIDCs.

Transfer of Long-Term Lease of land to promoter in case of construction of project

Granting of Long-term lease (To Builder/Promoter)

Local Authority (Lessor)

Exemption

(Entry 41B of NN 12/2017)

Granting of Long-Term Lease for project

Promoter (Lessee)

Limitation of Exemption

(Entry 41B of NN 12/2017)

The said transaction is exempted subject to the condition that the constructed residential units sold before issuance of completion certificate and GST is paid on them.

RCM

(Entry 5C of NN 13/2017)

In case of flats sold after issue of completion certificate (CC), exemption of TDR, FSI, long term lease shall be withdrawn. However, such withdrawal shall be limited to 1% of value in case of affordable houses and 5% of value in case of other than affordable houses.

In case of units sold after CC, Promoter is liable to pay GST under Reverse Charge (RCM) on amount paid to landowner (Lessor) @ 18% on units sold after issuance of completion certificate on the proportionate amount.

Such amount of 18% of GST cannot exceed 1% / 5% of GST on units sold after CC.

Granting of Long-term lease (To Builder/Promoter)

# Queries Residential Project Commercial Project 1 Who is liable to pay GST on long term Lease of land ? Promoter under RCM Promoter under RCM 2 Exemption (if any) Units booked upto BU - No Tax Units unbooked as on BU - Tax applicable No exemption 3 Time of Supply (Tax under RCM by Promoter) In any month before BU or in the month of BU Immediately on date of payment (or date after 60 days from date of invoice) 4 Valuation Lease premium paid Lease premium paid 5 GST Rate on Long term lease of land 18% 18% 6 Manner of Calculation of Tax Lower of: 1. Lease premium x 18% x unbooked Carpet Area / Total Carpet Area; or 2. 1% / 5% of value of unbooked units Lease premium x 18% 7 Valuation of unbooked units for 1% / 5% portion Equal to value of similar apartments nearest to the date of BU NA 8 Eligibility of ITC - for Promoter ITC not allowed ITC Allowed

Exemption Entry 41B of NN 12/2017- CTR

Description of Service Rate

Upfront amount (called as premium, salami, cost, price, development charges or by any other name) payable in respect of service by way of granting of long term lease of thirty years, or more, on or after 01.04.2019,for construction of residential apartments by a promoter in a project, intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or after its first occupation, whichever is earlier.

Heading 9972

The amount of GST exemption available for construction of residential apartments in the project under this notification shall be calculated as under:

[GST payable on upfront amount (called as premium, salami, cost, price, development charges or by any other name) payable for long term lease of land for construction of the project] x (carpet area of the residential apartments in the project ÷ Total carpet area of the residential and commercial apartments in the project).

Condition

Provided that the promoter shall be liable to pay tax at the applicable rate, on reverse charge basis, on such proportion of upfront amount(called as premium, salami, cost, price, development charges or by any other name) paid for long term lease of land, as is attributable to the residential apartments, which remain unbooked on the date of issuance of completion certificate, or first occupation of the project, as the case may be, in the following manner –

[GST payable on upfront amount(called as premium, salami, cost, price, development charges or by any other name) payable for long term lease of land for construction of the residential apartments in the project but for the exemption contained herein] x (carpet area of the residential apartments in the project which remain un- booked on the date of issuance of completion certificate or first occupation ÷ Total carpet area of the residential apartments in the project);

NIL

Provided further that the tax payable in terms of the first proviso shall not exceed 0.5 per cent. of the value in case of affordable residential apartments and 2.5 percent. of the value in case of residential apartments other than affordable residential apartments remaining un- booked on the date of issuance of completion certificate or first occupation.

The liability to pay central tax on the said proportion of upfront amount (called as premium, salami, cost, price, development charges orby any other name) paid for long term lease of land, calculated as above, shall arise on the date of issue of completion certificate or first occupation of the project, as the case may be.]

Sn

Chapter Heading

41B

Sn Category of Supply of Services

Long term lease of land (30 years or more) by any person against consideration in the form of upfront amount (called as premium, salami, cost, price, development charges or by any other name) and/or periodic rent for construction of a project by a promoter.

Any person Promoter.

(j) the term “promoter” shall have the same meaning as assigned to it in clause (zk) under section 2 of the Real Estate (Regulation and Development) Act, 2016 (16 of 2017).

Supplier of Service Recipient of Service 5C

RCM Entry 5C of NN 13/2017- CTR

Chapter 99

Supply of services other than services by way of grant of development rights, long term lease of land (against upfront payment in the form of premium, salami, development charges etc.) or FSI (including additional FSI) by an unregistered person to a promoter for construction of a project on which tax is payable by the recipient of the services under sub- section 4 of section 9 of the Central Goods and Services Tax Act, 2017 (12 of 2017), as prescribed in notification No. 07 / 2019- Central Tax (Rate), dated 29th March, 2019, published in Gazette of India vide G.S.R. No.254(E), dated 29th March, 2019.

Explanation. - This entry is to be taken to apply to all services which satisfy the conditions prescribed herein, even though they may be covered by a more specific chapter, section or heading elsewhere in this notification

Sn Chapter Heading Description of Service Rate Condition 39.

9Rate entry - NN 11/2017 – CTR

GST on long term lease of land as a part of composite supply of construction of flat by promoter to customer.

land

flats

Freehold

Leasehold

Sub lease Land

GST Rate 1% / 5% / 12% 1% / 5% / 12% 1/3rd land deduction Allowed Allowed

Construction Services on Freehold or Lease hold

Construction Services of

on

land

/

Applicable GST provision Entry 3 of 11/2017 Entry 16 of 11/2017

Rate entry - NN 11/2017 – CTR (NIL rate on lease)

16. Heading 9972

(i) Services by the Central Government, State Government, Union territory or local authority to governmental authority or government entity, by way of lease of land.

(ii) Supply of land or undivided share of land by way of lease or sub lease where such supply is a part of composite supply of construction of flats, etc. specified in the entry in column (3), against serial number 3, at item [(i), (ia), (ib), (ic), (id), (ie) and (if)].

Provided that nothing contained in this entry shall apply to an amount charged for such lease and sub-lease in excess of one third of the total amount charged for the said composite supply.

Total amount shall have the same meaning for the purpose of this proviso as given in paragraph 2 of this notification.

(iii) Real estate services other than (i) and (ii) above.

Paragraph 2 of NN 11/2017

-

-

-

Para 2. In case of supply of service specified in column (3), in item (i) ,(ia), (ib), (ic), (id), (ie) and (if) against serial number 3 of the Table above, involving transfer of land or undivided share of land, as the case may be, the value of such supply shall be equivalent to the total amount charged for such supply less the value of transfer of land or undivided share of land, as the case may be, and the value of such transfer of land or undivided share of land, as the case may be, in such supply shall be deemed to be one third of the total amount charged for such supply.

Explanation. –For the purposes of this paragraph and paragraph 2A below, “total amount” means the sum total of,(a) consideration charged for aforesaid service; and (b) amount charged for transfer of land or undivided share of land, as the case may be including by way of lease or sublease.]

Sn Chapter Heading Description of Service Rate Condition

Nil

Nil

9

PLC as a part of Lease Premium

Circular No. 177/09/2022-TRU dtd 03-Aug-2022

Issue 10 of Circular: Whether location charges or preferential location charges (PLC) collected in addition to the lease premium for long term lease of land constitute part of the lease premium or upfront amount charged for long term lease of land and are eligible for the same tax treatment.

10.2 As per entry 41 of the notification No. 12/2017- Central Tax (Rate) dated 28.06.2017 upfront amount, which is defined as “upfront amount (called as premium, salami, cost, price, development charges or by any other name) payable in respect of service by way of granting of long term lease (of thirty years, or more) of industrial plots or plots for development of infrastructure for financial business, provided by the State Government Industrial Development Corporations or Undertakings or by any other entity having 20 per cent or more ownership of Central Government, State Government, Union territory to the industrial units or the developers in any industrial or financial business area”, is exempt from GST

10.3 Allowing choice of location of plot is integral part of supply of long-term lease of plot and therefore, location charge is nothing but part of consideration charged for long term lease of plot. Being charged upfront along with the upfront amount for the lease, the same is exempt.

10.4 Accordingly, as per recommendation of the GST Council, it is clarified that location charges or preferential location charges (PLC) paid upfront in addition to the lease premium for long term lease of land constitute part of upfront amount charged for long term lease of land and are eligible for the same tax treatment, and thus eligible for exemption under Sl. No. 41 of notification no. 12/2017- Central Tax (Rate) dated 28.06.2017.

Joint Development Agreements

Taxable events under Joint Development Agreement

Landowner Developer Transfer of Development Rights (ToDR) Customer Sn Supplier Recipient Transaction/Supply 1 Landowner Promoter Transfer of Development Rights (ToDR) 2 Promoter Landowner Construction Services of Units (Resi / Comm) against consideration for TDR (in area sharing) or cash (in revenue sharing) 3 Promoter Customer Sale of under construction flats/ Ready to move Flats 4 Landowner Customer Sale of under construction flats/ Ready to move Flats (only in area sharing) Construction Services

Area Sharing in Joint Development Agreement

Landowner 60%

Carpet

Project Construction Services Developer Development Rights

of

Area of

Customer Customer

Construction

Sale of remaining 40% of Carpet Area

Services Sale of 60% of Carpet Area Construction Services

Landowner 60% of Project Revenue Construction Services Developer Development Rights

Customer Project Revenue Construction Services

Revenue Sharing in Joint Development Agreement

GST Implication on Transfer of Development Rights

Landowner Developer Transfer of Development Rights Issues

PROMOTER

Person liable to Tax

GST Rate

Exemption

Time of Supply

Valuation

/

From 01-04-2019, Liability of GST on transfer of development rights shifted from landowner to promoter under RCM 13/2017 CT(R) dtd. 28-06-2017 as amended by NN 05/2019 CT(R) dtd. 2903-2019

18% GST GST on transfer of Development Rights is payable @ 18% under RCM

Sr. No 16. item (iii) of NN 11/2017 CT(R) dtd. 28-06-2017 – Heading 9972

TDR for GST on residential units booked before completion certificate is exempted from GST 04/2019-CT(R) 29-03-2019

On or before issuance of Completion certificate / First Occupation

For Residential Units – for monetary or non-monetary consideration

For Commercial Units – for non-monetary consideration NN 06/2019 dtd 29-03-2019 as amended by 03/2021 dtd 02-06-2021

Commercial Units – For Monetary Consideration

Deemed to be equal to the value of similar apartments charged by the promoter from the independent buyers nearest to the date on which such development rights or FSI is transferred to the promoter.

Section 13 of CGST Act

Para 1A of NN 12/2017 inserted by NN 04/2019 CT(R) dtd 29-03-2019

Details Notification

Section

GST Implication on Construction Services to Landowner

Landowner

Construction Services

Person liable to Tax PROMOTER is liable to pay GST on construction services provided to landowner by promoter under forward charge.

GST Rate

Exemption

Time of Supply

1 % or 5% or 12% as applicable to type of area allocated to landowner–residential –affordable , non-affordable or commercial

NA

Valuation

NN 11/2017 as amended , also refer condition in entry 3 (i)(a) to (d)

After 1/3rd land deduction

NA

On or before issuance of Completion certificate / First Occupation for nonmonetary consideration NN 06/2019 dtd 29-03-2019 as amended by 03/2021 dtd 02-06-2021 for Monetary Consideration

Section 13 of CGST Act

deemed to be equal to the total amount charged for similar apartments in the project from the independent buyers, other than the person transferring the development right or FSI (including additional FSI), nearest to the date on which such development right or FSI (including additional FSI) is transferred to the promoter, less the value of transfer of land, if any, as prescribed in paragraph 2 above.

Para 2A of NN 11/2017 inserted by NN 03/2019 CT(R) dtd 29-03-2019

Developer

Details Notification

Section

Issues

/

Under Construction flats to Customers

Promoter to Customer Landowner to Customer Services Construction Services Construction Services Taxability Taxable @ 1% , 5% or 12% Taxable @ 1% , 5% or 12% 1/3rd Land Deduction Available Available ITC Availability For Residential Units – ITC not Available For Commercial Units – ITC Available For Residential Units – ITC Available For Commercial Units – ITC Available Landowner Developer Customer

GST Applicability – Area Sharing in JDA

# Issues Residential Project Commercial Project 1 Who is liable to pay GST on TDR? Developer under RCM Developer under RCM 2 Exemption (if any) Units booked upto BU - No Tax on TDR Units unbooked as on BU - Tax on TDR NA 3 Who is liable to pay GST on Construction Services Developer under FCM Developer under FCM 4 Time of Supply / Point of Taxation 1. Tax on TDR under RCM by developer 2. Tax on Construction Services under FCM by Developer In any month before BU or in the month of BU In any month before BU or in the month of BU 5 Valuation of TDR Equal to value of similar apartment nearest to date of TDR agreement Equal to value of similar apartment nearest to date of TDR agreement 6 Valuation of Construction Services Equal to value of similar apartment nearest to date of TDR agreement Less: 1/3 - Deemed value of land Equal to value of similar apartment nearest to date of TDR agreement Less: 1/3 - Deemed value of land 7 GST Rate on TDR 18% 18% 8 GST Rate on Construction Services 1% / 5% (Effective Rate) 12% (Effective Rate) 9 Manner of Calculation of Tax on TDR Lower of: 1. TDR x 18% x unbooked Carpet Area / Total Carpet Area 2. 1% / 5% of value of unbooked units TDR x 18% 10 Valuation of unbooked units Equal to value of similar apartments nearest to date of BU NA 12 Eligibility of ITC ITC allowed only for landowner ITC allowed to both landowner / Promoter

GST Applicability – Revenue Sharing in JDA

# Issues Residential Project Commercial Project 1 Who is liable to pay GST on TDR? Developer under RCM Developer under RCM 2 Exemption (if any) Units booked upto BU - No Tax on TDR Units unbooked as on BU - Tax on TDR NA 3 Time of Supply / Point of Taxation (Tax on TDR under RCM by developer) In any month before BU or in the month of BU Immediately on date of agreement or payment 4 Valuation of TDR Equal to monetary consideration paid by developer to landowner Equal to monetary consideration paid by developer to landowner 5 GST Rate on TDR 18% 18% 6 Manner of Calculation of Tax on TDR Lower of: 1. TDR x 18% x unbooked Carpet Area / Total Carpet Area 2. 1% / 5% of value of unbooked units TDR x 18% 7 Valuation of unbooked units Equal to value of similar apartments nearest to the date of BU NA 8 Eligibility of ITC - for Developer ITC not allowed ITC Allowed 9 Eligibility of ITC - for Landowner NA NA

Input Tax Credit (ITC) Reversal

Reversal as per Rule 42 in case flats sold after BU

Ongoing Project opted for old rate

Commercial Project (REP)

New Residential Project (RREP/REP)

ITC available (Turnover based ITC reversal as per Rule 42 exist upto 31-032019)

ITC available (Carpet Area based ITC reversal as per amended Rule 42)

ITC not available (Availed it and Reversed in same month)

Ongoing Residential Project opted for new rate

ITC not available (Availed it and Reversed in same month)

booked after BU Mandatory 6 Conditions applicable like Mandatory Cash Payment , 80% RD Purchase & 100% CG

ITC Reversal applicable on units

Purchase etc.

Reversal- in case of Units sold after BU (Rule 42)

Till 31.03.2019

• Input Tax Credit was required to reverse ITC based on taxable and Exempt supplies achieved in a particular Financial Year. Accordingly Input Tax Credit in the year when the builder receives Completion Certificate / BU permission were only considered for ITC reversal calculations and not the entire project ITC.

• With effect from 01.04.2019, criteria for ITC reversal for Builders is shifted from Turnover basis to Area based. ITC availed starting from 01.07.2017 or project started whichever is later during the entire project would have to be considered while calculating ITC reversal On or after 01.04.2019

Gujarat High Court in Alembic Ltd (TAX APPEAL NO. 140 of 2019)

Applicability of ITC Reversal as per Rule 42

CC / BU Received in Pre 01-04-2019 Post 01-04-2019

Rule 42 Applicability

Pre-amended Rule 42(1) & Rule 42(2) exist before 01-04-2019

Post Amended Rule 42 w.e.f 01-04-2019

ITC Reversal Turnover based Carpet Area based

Calculation on Month wise ITC (then Yearly Re-calculation) Project wise ITC

ITC pertains to

ITC availed after BU Date will be considered as common ITC ITC availed from 01-07-17 till date for the project will be considered as common ITC

Manner Tax period wise Project wise

Formula

CC- Completion Certificate

BU – Building Use Permission

ITC for tax period x Exempt Turnover / Total Turnover

Total ITC for project x Exempt Carpet Area / Total Carpet Area

Reversal as per Rule 42 - Example

Carpet Area of the Project (in Sq.Mtrs.) 40,000

Unsold Carpet Area on the Date of Receipt of BU (in Sq. Mtrs.) 12,000 (Amt in Cr.)

Year Total ITC Availed (a) Taxable Supplies (b) Exempt Supplies (c) Total Supplies (d) Carpet Area Sold (e) ITC Reversal

Rule 42 Prior 01.04.2019

Post 01.04.2019

2017-18 3.50 20.00 - 20.00 13,000 -2018-19 4.50 20.00 - 20.00 15,000 -2019-20 2.00 10.00 15.00 25.00 12,000 1.2Total 10.00 50.00 15.00 65.00 40,000 1.2 (2*15/25) 3.00 (10*12000/40000) Basic Project Details Project Started 01.10.2017 Project Completion 01.12.2019

as per

(Turnover Basis)

(Carpet Area Basis)

Total

Manner of Rule 42 Reversal - Part 1

Clause Details Total T Total ITC for the tax period 1,00,00,000 T1 ITC Exclusively for non-Business supplyT2 ITC Exclusively for exempt supplyT3 Block CreditC1 C1=T-(T1-T2-T3) 1,00,00,000 T4 ITC Exclusively for Taxable supply (T4 will be Zero for projects after 01-04-2019)C2 C2=C1-T4 Common Credit 1,00,00,000 D1 D1=C2 * (E / F) ITC to be Reversed 40,00,000 E Total Exempt Carpet Area for the tax period 40,000 Sq Ft F Total Carpet Area for the tax period 1,00,000 Sq Ft % of Exempt Supplies to Total Supplies 40 % D2 5% of C2 (attributable to non-business purpose)C3 C3=C2-(D1+D2) Credit Allowed from Common ITC 60,00,000

Manner of Rule 42 Reversal – Part 2

Step 1 Monthly

Reversal as per Rule 42(1)

Step 2 Yearly re-calculation as per Rule 42(3)

Step 3 Payment of short reversal Upto 30-Sep of Next FY

Step 4

Reclaim of excess reversal Upto 30-Sep of Next FY

Step 5

Pay interest on short reversal from 1st April till payment.

Applicability of amended Rule 42 upto 31-03-2019

• A Writ petition has been filed to declare Rule 42(3) of CGST Rules, 2017 as ultra vires the constitution of India.

• The main contention is whether Input Tax Credit (ITC) availed prior to 01-04-2019 must be reversed as per amended Rule 42 or Rule 42 exist upto 31-032019, in case completion certificate received before 31-03-2019 Said writ petition has been admitted in Calcutta High Court, hearing & order is awaited.

GEETA GANESH PROMOTERS PVT. LTD. – CALCUTTA HIGH COURT

Redevelopment of Residential Societies

1 Society to Developer (ToDR) Exempt* On such proportionate value of TDR/FSI/Upfront amount attributable to residential apartments sold to New Members after BU Issuance of Completion Certificate

2 Developer to Society/Old Members Taxable

Equal to the value of similar apartments sold nearest to the date of issuance of completion certificate [Less] 1/3rd Value of Land

3 Developer to New Members Taxable Transaction Value

ToDR means Transfer of Development Rights

Amount received or milestone achieved; Whichever is earlier

* Purely residential project will get full exemption at the initial stage, but builder will have to pay tax under RCM on proportionate basis if some units remain unsold after receipt of BU

01.04.2019

Transaction Whether taxable or not Value Time of Supply

GST Applicability w.e.f.

Sn

GST implication on free units

9. In case of redevelopment or slum rehabilitation project, (new or an existing project) whether the constructed units supplied to existing occupiers by the developer free of monetary consideration are taxable?....

Yes, units supplied free of cost also attract GST as their consideration is not money but TDR/ FSI or rights relatable to land on which construction takes place…

Valuation of Construction Services for free units to existing occupiers in redevelopment society

Para 2A. Where a registered person transfers development right or FSI (including additional FSI) to a promoter against consideration, wholly or partly, in the form of construction of apartments, the value of construction service in respect of such apartments shall be deemed to be equal to the Total Amount charged for similar apartments in the project from the independent buyers, other than the person transferring the development right or FSI (including additional FSI), nearest to the date on which such development right or FSI (including additional FSI) is transferred to the promoter, less the value of transfer of land, if any, as prescribed in paragraph 2 above.

#

Question Answer

CBIC FAQ 354/32/2019

dtd 14.05.2019 Notification no. 3/2019-CTR dated 29.03.2019

TRU

Redevelopment Practical Example

Particulars Old Units New Units Units 12 9 Sale Price/ unit - 50,00,000 Construction Cost + 10% Margin / Unit 30,00,000 30,00,000 Total Cost 3,60,00,000 2,70,00,000 ITC on Purchase Cost @ 15% (Estimated) 45,00,000 40,50,000 Option 1 – Value of Old Units Similar to New Units Option 1 Old Unit New Units Total Units 12 9 21 Sale Price – Similar to new units 50,00,000 50,00,000Total Value 6,00,00,000 4,50,0000 10,50,0000 GST Rate 5% 5%Tax 30,00,000 22,50,000 52,50,000 ITC Not available Not available Not available Net Payable in CASH 30,00,000 22,50,000 52,50,000 Option 2 – Value of Old Units as Construction Cost +10% margin Option 2 Old Unit New Units Total Units 12 9 21 Construction Cost + Margin 30,00,000Sale Price / Unit 50,00,000Total Value 3,60,00,000 4,50,00,000 8,10,00,000 GST Rate 18% 5%Tax 64,80,000 22,50,000 87,30,000 ITC 45,00,000 Not available 45,00,000 Net Payable in CASH 19,80,000 22,50,000 42,30,000

GST on Developed Plots

Definition of Project – GST & RERA

GST Act 2017 define the term “Project” in Notification 12/2017 CTR as amended by 04/2019 dtd 29-03-2019:

Clause (viii) The term “project” shall mean a Real Estate Project or a Residential Real Estate Project

Clause (ix) the term “Real Estate Project (REP)” shall have the same meaning as assigned to it in clause (zn) under section 2 of the Real Estate (Regulation and Development) Act, 2016 (16 of 2017).

Clause (x) The term “Residential Real Estate Project (RREP)” shall mean a REP in which the carpet area of the commercial apartments is not more than 15 per cent. of the total carpet area of all the apartments in the REP;

Rera Act 2016 define “Real Estate Project” under clause (zn) of section :

(zn) "real estate project" means :

• the development of a building or a building consisting of apartments, or

• converting an existing building or a part thereof into apartments, or

• the development of land into plots or apartment, as the case may be, for the purpose of selling all or some of the said apartments or plots or building, as the case may be, and includes the common areas, the development works, all improvements and structures thereon, and all easement, rights and appurtenances belonging thereto;

GST on developed Plot

Section 7 of the CGST Act defines the Scope of Supply, provides for those activities which shall neither be treated as a supply of goods nor as a supply of services covered under Schedule-III.

Sale of Land is neither covered under supply of goods nor supply of services as per Schedule – III of CGST Act. Therefore, transactions involving the sale of land are not subject to GST.

However, when transfer of land is combined with the construction services, there could be GST implications that require attention.

Vacant Plot + Basic Development

levelling, laying down of drainage lines, water lines, electricity lines Boundary wall etc.

= Developed Plot

Recent circular on Sale of land with basic development

Circular No. 177/09/2022-TRU dtd 03-Aug-2022

Issue 14 of Circular: Whether sale of land after levelling, laying down of drainage lines etc., is taxable under GST ?

14.1 Representation has been received requesting for clarification regarding applicability of GST on sale of land after levelling, laying down of drainage lines etc.

14.2 As per Sl no. (5) of Schedule III of the Central Goods and Services Tax Act, 2017, ‘sale of land’ is neither a supply of goods nor a supply of services, therefore, sale of land does not attract GST.

14.3 Land may be sold either as it is or after some development such as levelling, laying down of drainage lines, water lines, electricity lines, etc. It is clarified that sale of such developed land is also sale of land and is covered by Sr. No. 5 of Schedule III of the Central Goods and Services Tax Act, 2017 and accordingly does not attract GST.

14.4 However, it may be noted that any service provided for development of land, like levelling, laying of drainage lines (as may be received by developers) shall attract GST at applicable rate for such services.

Advance Rulings and Circular on Developed Plots

# Name of the applicant Authority Date Ruling Given by Authority GST Applicable? 1 Dipesh Anil kumar Naik Gujarat AAR 19-08-2020 Sale of Developed Plots i.e., sale of plots with common basic amenities will be considered as ‘construction service’. Yes, GST @ 5% Gujarat AAAR 22-12-2021 Yes, GST @ 18% 2 3 Shantilal Real Estate Services Goa AAR 18-05-2021 Sale of Developed Plot is not a supply. No 4 Circular 177 CBIC 03-08-2022 Sale of Developed Plot is not a supply. No 5 M/s Rabia Khanum KAR AAR 08-09-2022 Sale of Developed Plot does not attract GST referring to above circular No 6 KAR AAAR 14-02-2023 7 Godrej Properties KAR AAR 26-04-2023 Sale of Developed Plot does not attract GST No

GST on developed Plot with Additional Amenities

Section 7 of the CGST Act defines the Scope of Supply, provides for those activities which shall neither be treated as a supply of goods nor as a supply of services covered under Schedule-III.

Sale of Land is neither covered under supply of goods nor supply of services as per Schedule – III of CGST Act. Therefore, transactions involving the sale of land are not subject to GST.

However, when transfer of land is combined with the construction services, there could be GST implications that require attention.

Vacant Plot

Development

levelling, laying down of drainage lines, water lines, electricity lines Boundary wall etc.

Extra Development Landscaping, Club House, Luxurious Villa etc.

+

= Farm House Scheme

+

Basic

Taxability of Components of Developed Plots

Although such receipts are towards no supply, for the purpose of ITC reversal, it is advisable to disclose such receipts as Exempt supply in GSTR-1 as well as

Sn Consideration for Type Output Supply Input Supply Remarks Disclosure in GSTR-1 and GSTR-3B 1 Sale of Land with boundary wall, drainage, road, levelling etc. Immovable Property GST Not Applicable ITC directly related to Land development will not be available For common ITC, amount attributable

Land

will have to

proportion considering SALE OF LAND AS EXEMPT SUPPLY

GSTR-3B 2 Other construction Other Construction Services GST Applicable @ 18% ITC directly related to such construction income will be available in full. To

Taxable supply in GSTR-1 as well as GSTR-3B 3 Development Charges (Club House etc.) 4 Bunglow on Land

to

consideration

be reversed in that

be disclosed as

M/s Godrej Properties Limited – Karnataka AAR

1. Whether applicant is liable to charge GST, if booking of plot, receipt of consideration and agreement for sale is entered as well as sale deed is executed after the release certificate, on the following components:

a. Sale of Plot b. Basic Infrastructure Development charges c. Other Common amenities & facilities charges.

2. Whether applicant is liable to charge GST, if booking of plot and / or receipt of consideration and / or agreement for sale is entered prior to the release certificate and sale deed is executed after the release certificate, on the following components:

a. Sale of Plot b. Basic Infrastructure Development charges

Other Common amenities & facilities charges.

3. What is the applicability of GST if the sale price is a consolidated price in agreement for sale towards land cost, basic infrastructure development charges and other common amenities and facilities charges?

c.

Ruling delivered by AAR: Question before AAR: Particulars Booking, receipt & ATS after release certificate Booking & receipt before certificate and ATS after certificate Sale of Plot Not liable to GST Not liable to GST Basic Infrastructure Development charges Not liable to GST Not liable to GST Other common amenities and facilities charges GST applicable GST applicable Sale Price is consolidated price in ATS towards Land, basic Infrastructure & common amenities and facilities GST is applicable on charges proportionate to common amenities and facilities GST

common amenities

is applicable on charges proportionate to

and facilities

Anti-Profiteering for Real Estate Project

Anti-Profiteering under GST

Section 171 of CGST Act mandates that “any reduction in rate of tax on any supply of goods or services or the benefit of input tax credit shall be passed on to the recipient by way of commensurate reduction in prices.”

Thus, a person is considered to be profiteering if the prices of goods or services are not reduced despite:

1. A reduction in the tax rate on the supply of goods or services

2. The benefit of input tax credit being available

In pre-GST era, Central Excise duty was payable on most construction material at 12.5%. In addition, VAT was payable on construction material at 12.5% to14.5% in most of the States & the construction material also suffered entry tax. The input tax credit of the above taxes was inadmissible for meeting Service Tax liability of the builder, thus leading to cascading of input taxes on constructed flats & a higher effective , tax incidence. But GST regime allows full input tax credit for offsetting the headline rate of12%, thereby reducing the effective tax incidence.

If the Anti-Profiteering Authority comes to the conclusion that any registered person has profiteered, such person shall be liable to pay penalty equivalent to ten per cent. of the amount so profiteered:

National Antiprofiteering Authority (NAA) Director General of Anti Profiteering (DGAP) Standing Committee State Screening Committee Consumer Compliant / Application

Timeline of Anti Profiteering Measures & Litigation

28 Nov 2017 Establishment of NAA (National Anti-Profiteering Authority)

23 Nov 2022 Shifting the Authority from NAA to CCI- Competition Commission of India w.e.f Dec 2022

01 Dec 2022 NAA is set to wind up

No provision for an appeal against the NAA & CCI under GST law. The only recourse is to file a writ petition in the High Court.

2023 More than 100 companies filed writ petition challenging the constitution validity of Anti Profiteering Provision

29 Jan 2024 Delhi High Court upheld the constitutional validity of the Anti-profiteering provisions under GST law

19 Apr 2024 Supreme Court issue notice to Central Govt, CBIC, GST Council, NAA & CCI on a petition challenging Delhi High Court verdict, upholding the constitutional validity of anti-profiteering provisions filed by a real estate company.

Constitution Validity of Anti-Profiteering Provisions are currently pending before Supreme Court

Flawed Methodology adopted by NAA

Illustration of two identical real estate projects being developed by Developers A & B with the only difference being the advance payment received by them prior to the Goods and Services Tax Regime.

If the methodology adopted by NAA /DGAP is to be accepted, Developer A would be required to pass on 15% benefit to the flat buyers and Developer B who received 80% of the payment/amount post-Goods and Services Tax receive would be required to pass no benefit to the flat-buyers.

Turnover Pre GST Credit Pre GST Turnover GST Credit GST Credit to Turnover Pre GST Credit to Turnover GST Difference in ratio Developer A 60 6 40 10 10 25 15 Developer B 20 6 80 10 30 12.5 -17.5 60 6 40 10 10 25 15 20 6 80 10 30 12.5 -17.5 -40 -20 0 20 40 60 80 100 Developer A Developer B % % % % % %

Issues in Anti-Profiteering Provision for Real Estate

Explanation to Section 171 of CGST - “the expression "profiteered" shall mean the amount determined on account of not passing the benefit of reduction in rate of tax on supply of goods or services or both or the benefit of input tax credit to the recipient by way of commensurate reduction in the price of the goods or services or both”

Meaning of word commensurate not defined in GST law

There is no clear methodology for passing on benefits from tax rate reductions or increased ITC availability.

NAA/DGAP has followed same methodology for different type of industries

Appeal mechanism against NAA order is not available in GST law, taxpayer has to approach high court by filing writ petition.

For Real Estate Industry , NAA/DGAP has followed the methodology of difference of ratio of ITC to Turnover under PRE & POST GST.

Factors like seasonal demand, festivals, Home loan interest rate changes in GST period, location must be considered in pricing of flats.

RCM on payment to Government / Local Authority

As a Public Authorities

As per definition of ‘Business’ under Section 2 (17) (i) of CGST Act, 2017, it includes any activity or transaction undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities.

In view of the above definition of business, any activity or transaction carried out/provided by the Govts. in which they are engaged as public authorities shall constitute a supply leviable to GST, if it is made against a consideration except those transactions which are specifically notified as non-supplies under Section 7(2)(b) of CGST Act

Definition as per RTI Act (h) "public authority" means any authority or body or institution of self- government established or constituted(a) by or under the Constitution; (b) by any other law made by Parliament; (c) by any other law made by State Legislature; (d) by notification issued or order made by the appropriate Government, and includes any- (i) body owned, controlled or substantially financed; (ii) non-Government organisation substantially financed, directly or indirectly by funds provided by the appropriate Government;

1

Definitions Part

Section 2 (53) of Central GST Act -"Government" means the Central Government;

Section 2 (53) of State GST Act " Government " means the Government of State.

Section 2 (69) of CGST Act "local authority" means-

(a) a "Panchayat" as defined in clause (d) of article 243 of the Constitution;

(b) a "Municipality" as defined in clause (e) of article 243P of the Constitution;

(c) a Municipal Committee, a Zilla Parishad, a District Board, and any other authority legally entitled to, or entrusted by the Central Government or any State Government with the control or management of a municipal or local fund;

(d) a Cantonment Board as defined in section 3 of the Cantonments Act, 2006 (41 of 2006);

(e) a Regional Council or a District Council constituted under the Sixth Schedule to the Constitution;

(f) a Development Board constituted under article 371 8[and article 371J] of the Constitution; or

(g) a Regional Council constituted under article 371A of the Constitution;

“Governmental Authority” means an authority or a board or any other body, -

(i) set up by an Act of Parliament or a State Legislature; or

(ii) established by any Government, with 90per cent. or more participation by way of equity or control, to carry out any function entrusted to a Municipality under article 243W of the Constitution or to a Panchayat under article 243G of the Constitution.

“Government Entity” means an authority or a board or any other body including a society, trust, corporation,

(i) set up by an Act of Parliament or State Legislature; or

(ii) established by any Government, with 90per cent. or more participation by way of equity or control, to carry out a function entrusted by the Central Government, State Government, Union Territory or a local authority.]

Definitions Part 2

Neither supply of goods nor supply of services

Notified activities not treated as Supply under GST

As per Section 7 of CGST Act, it is mentioned that any activity covered under schedule III and any activity notified by government shall be neither treated as goods nor services.

Extract of provision contained in Section 7(2) of CGST Act is as below: Notwithstanding anything contained in sub-section (1),-

• (a) activities or transactions specified in Schedule III; or

• (b) such activities or transactions undertaken by the Central Government, a State Government, or any local authority in which they are engaged as public authorities, as may be notified by the Government on the recommendations of the Council, shall be treated neither as a supply of goods nor a supply of services.

Relevant Notification & Activities

In relation to the above provisions, the government has issued notifications specifying list of activities or transactions undertaken by Central Government, State Government or any local authority. As per Section 7(2)(b), all the activities are neither treated as supply of goods nor supply of services.

As per Notification No. 16/2018-Central Tax (Rate) read with Notification No. 14/2017-Central Tax (Rate), “Services by way of any activity in relation to a function entrusted to a Panchayat under article 243G of the Constitution or to a Municipality under article 243W of the Constitution” undertaken by the Central Government or State Government or Union Territory or any local authority in which they are engaged as public authority, shall be treated neither as a supply of goods nor a supply of service w.e.f. 27-07-2018.

Before 27-07-2018, same services mentioned above (Services provided by local authority under article 243W & 243G of constitution) is covered under S.no. 4 and 5 of exemption notification 12/2017-CT(R) dated 28-06-2017.

RCM on Payment to Government

Services supplied by the Central Government, State Government, Union territory or local authority to a business entity excluding, -