Presented by

CA. Niki Darshak Shah

Statistics

2. Background & Overview 3. Key Concepts

4. Overseas Investment & Illustrations

5. Key Restrictions

6. Reporting Requirements

7. Disinvestment

8. Case Studies

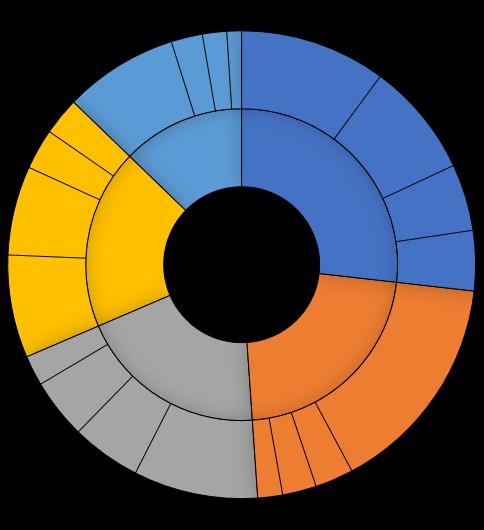

ODI Destinations (April 2023 - December 2023)

ODI Destinations (April 2020 - July 2022)

• Increase in Overseas Investment in the Netherlands & UAE

• Decrease in Overseas Investment in Mauritius

Wholesale,

Manufacturing

Transport,

In keeping with the spirit of liberalization and promoting ease of doing business in India, the Central Government and the Reserve Bank of India (RBI) have notified the new overseas investment framework on 22 August 2022.

RBI/FED/2024-25/121 FED Master Direction No.15/2024-25 on Overseas Investment dated July 24, 2024

Foreign Exchange Management (Overseas Investment) Rules, 2022 (OI Rules) notified by the Central Government vide Notification No. G.S.R. 646(E) dated August 22, 2022

Foreign Exchange Management (Overseas Investment) Regulations, 2022 (OI Regulations) notified by the Reserve Bank vide Notification No. FEMA 400/2022-RB dated August 22, 2022.

AND Companies incorporated in India

Bodies created under an Act of Parliament

Partnership firms registered under the Indian Partnership Act, 1932

Limited Liability Partnerships (LLPs)

Registered Trusts and Societies (under restricted conditions and with RBI approval)

Financial Commitment: It comprises of:-

• FC made by an Indian Entity in FE shall not exceed 400% of its Net Worth as on the date of last audited balance sheet.

• FC by Indian Entity can be made by way of equity capital, debt, non-fund based financial commitment (guarantee, pledge or charge)

• Guarantee

100% jointly or severally by two or more Indian Entity

No fresh guarantee treated for Roll-over guarantee 50% of Performance Guarantee

Note: : A person resident in India who has made a financial commitment in a foreign entity in accordance with the Act or rules or regulations made thereunder, shall not make any further financial commitment, whether fund-based or non-fund-based, directly or indirectly, towards such foreign entity or transfer such investment till any delay in reporting is regularised..

Overseas Investment

Overseas Direct Investment

• Acquisition of Unlisted equity capital of a Foreign Entity (FE), or

• Subscription to the MoA of a FE, or

• Investment > 10 % of the equity capital or control in a listed FE where investment < 10%

Debt/Non-fund based facilities Overseas Portfolio Investment

• Debt other than OPI - subject to control and arms-length interest on debt/loans

• Debt/non-fund based facilities such as guarantees/pledgesubject to control

• Lend or Invest in debt instrument issued by FE, including SDSs of IE

Aggregate amount is considered as Financial Commitment (FC)

• Investment other than ODI, in foreign securities

• Not in any Unlisted debt instruments

• Not in any securities issued by a person resident in India who is not in an IFSC

• Deemed OPI even after delisting

Restrictions and prohibitions

• Restricted sectors/activities for ODI are as under

- Real estate activity

'Real estate activity' means buying and selling of real estate or trading in transferable development rights but does not include the development of townships, construction of residential or commercial premises, roads or bridges for selling or leasing.

- Gambling in any form

- Dealing in financial products linked to INR (without prior RBI approval).

• Approval Route - Investment/FC in Pakistan (permissible under approval route) or any jurisdictions as may be advised/notified by the Central Government

• Financial Commitment by a PRII in a foreign entity that has invested or invests into India at the time of making such FC or at any time thereafter, either directly or indirectly, resulting in a structure with more than two layers of subsidiaries is not permitted.

• Two Routes for Outbound Investments by Resident Individuals – LRS (Liberalised Remittance Scheme) and ODI

• Investment is limited to USD 2,50,000 per Financial Year

• The Scheme is available to all resident individuals including minors

• Permissible capital a/c transactions by an individual under LRS are:

1. opening of foreign currency account abroad with a bank;

2. Acquisition of immovable property abroad, (ODI) & (OPI)

3. extending loans including loans in Indian Rs. to (NRIs) who are relatives as defined in Co. Act, 2013

• A limit of USD 2,50,000 per FY under the Scheme also includes/subsumes remittances for current account transactions: viz.

1. Private visit;

2. gift/donation;

3. going abroad on employment;

4. emigration;

5. maintenance of relatives abroad;

6. business trip;

7. medical treatment abroad;

8. studies abroad) available to resident individuals

Overseas Direct Investment

Overseas Portfolio Investment

General Permission

FC in all foreign entities < 400% of net worth as per the latest audited balance sheet

OPI in all foreign entity < 50% of

net worth as per the latest audited balance sheet

Net Worth

Net Worth definition linked with the Companies Act

• Paid-up share capital + All reserves created out of profits

• LLP/Partnership Firm: Capital + Undistributed profitaccumulated loss - deferred/ miscellaneous expenses not written off

Net Worth definition common for ODI & OPI

Overseas Direct Investment

Overseas Portfolio Investment

Approval

Prior Approval: FC > USD 1 Bn in FY,

even if within 400% limit (same as previous regime)

Listed IE may invest or reinvest

Manner for making investment

• Subscription to MoA or market purchase

• Capitalisation within the specified time period

• Swap of securities

• Bidding or tender procedure

• Rights issue or bonus issue

• Merger, demerger, amalgamation, etc.

• Rights issue or bonus issue

• Swap of securities

• Capitalisation with specified time

• Merger, demerger, amalgamation, etc.

Overseas Direct Investment

Overseas Portfolio Investment

Investment Limit

ODI + OPI to be within LRS ceiling of $ 250,000

ODI + OPI to be within LRS ceiling of $ 250,000

General Permission

Allowed only in Operating FE

• Not engaged in FS activity

• RI to not have control in FE, if such FE has subsidiary/SDS

• RI may make OPI by way of investment or reinvestment

• Transition of existing LRSPortfolio into ODI under current regulations - Reporting and filing requirements not clear

Manner of making investment

Overseas Direct Investment

1. Capitalization, within specified time period 2. Rights issue or Bonus shares

Overseas Portfolio Investment

Merger, demerger, amalgamation, etc.

ODI + OPI to be within LRS ceiling of $ 250,000

4. Gift as per conditions 5. Inheritance

Minimum qualification shares

Exceptions

ODI by way of 5, 6, 7, and 8 may be made even if

• FE engaged in FS activity

• has subsidiary/ SDS where RI has control

Sweat equity shares

8. ESOP/ employee benefit scheme

OI by way of 6, 7, and 8 to be deemed OPI, if acquisition of <10% in listed or unlisted without control

Outside India India • 1% Holding

>10% holding

Control/ No Control

Control/ No Control

<10% holding

Control

<10% holding

• Issue or transfer of equity capital of a foreign entity from PROI or PRI to PRI who is eligible to make such investment or from PRI to PROI shall be subject to a price arrived on an arm’s length basis.

• AD bank before facilitating a transaction to ensure compliance with ALP taking into consideration the valuation as per any internationally accepted pricing methodology for valuation.

• Form FC to be submitted for undertaking FC/ disinvestment/restructuring.

• First ODI not permitted before filing Form FC and obtaining UIN from RBI.

• Scope of statutory auditor's certificate for ODI significantly widened.

• APR filing now exempted in below scenarios

• Form OPI introduced for reporting of OPI for PRII (other than Individuals) making/ transferring any OPI.

- Where PRI is holding < 10% of equity without control in the FE and no other FC other than equity; or

- FE is under liquidation

• APR shall certified by CA/ CPA where the statutory audit is not applicable and is based on audited financial statements and where laws of the host country/jurisdiction, do not provide for mandatory auditing of accounts.

- Except PRII does not have control in the FE

• To be reported on half yearly basis.

• Share certificate to be submitted in 6 months, else funds to be repatriated.

• Dues receivable from the FE with respect to investment in such FE to be repatriated within 90 days from date of becoming due.

Unique Identification Number (UIN)

Submission of evidence of investment to AD Bank

Repatriation of dividend, royalty, technical fees, etc from FE

Repatriation of dividend/ other entitlements from subsidiary credited to foreign currency account

Repatriation of proceeds of transfer/ Disinvestment

Reporting Financial Commitment

To be applied through Form FC before initial FC

Within 6 months. If not, amount remitted to be repatriated to India within said 6 months

All receivables with respect to investment to be repatriated within 90 days

All receivables with respect to investment to be repatriated within 90 days

Within 90 days of it falling due

In Form FC – At the time of making FC or sending outward remittance, whichever is earlier

Reporting restructuring of balance sheet In Form FC – Within 30 days of restructuring

Reporting Disinvestment In Form FC – Within 30 days of receipt of proceeds

Reporting OPI by IE or transfer of OPI In Form OPI – Half yearly reporting within 60 days of September or March-end, including ESOP issued to employees

Annual Performance Report

IE/ RI to report on or before December 31 of every year

In case of multiple IE/RI, person with higher stake

Foreign Assets and Liabilities Report

Person excluded form reporting:

• Resident holding <10% equity capital in FE without control and No FC other than equity capital

• FE under liquidation

• APR shall certified by CA/ CPA where the statutory audit is not applicable and is based on audited financial statements and where laws of the host country/jurisdiction, do not provide for mandatory auditing of accounts

Resident Individual to file APR in case of ESOP (if considered ODI)

IE to submit by July 15 of every year

• Delay post date of publication of these rules:

• Submission can be made subject to payment of Late Submission Fees (LSF). However, the facility of payment of LSF can be availed within a period of 3 years from the due date of such submission.

• Delay - Pre-date of publication of these rules:

• Submission can be made subject to payment of Late Submission Fees (LSF). However, the facility of payment of LSF can be availed within a period of 3 years from the date of publication of these regulations in the Official Gazette i.e. 22nd August 2022.

• LSF mechanism/ calculation provided by RBI vide the directions issued in this regard.

• PRI who has made a financial commitment in a foreign entity shall not be permitted to make any further financial commitment, whether fund-based or non-fund-based, directly or indirectly till any delay in reporting is regularized.

• In case of delay in filing/submitting the requisite form/return/document - Pay the Late Submission Fee (LSF)

• The LSF for delay in reporting overseas investment-related transactions shall be calculated (per return) as per the following matrix:

1. Form ODI Part-II/ APR, FCGPR (B), FLA Returns, Form OPI, evidence of investment or any other return which does not capture flows or any other periodical reporting

2. Form ODI-Part I, Form ODI-Part III, Form FC, or any other return which captures flows or returns which capture reporting of non-fund based transactions or any other transactional reporting [7500 + (0.025% × A × n)]

“n” is the number of years of delay in submission rounded upwards to the nearest month and expressed up to 2 decimal points.

“A” is the amount involved in the delayed reporting.

• Maximum LSF: 100% of amount involved

• LSF Payment within 30 days

Where the disinvestment by a person resident in India pertains to ODI -

• the transferor, in case of full disinvestment other than by way of liquidation, shall not have any dues outstanding for receipt, which such transferor is entitled to receive from the foreign entity as an investor in equity capital and debt;

• the transferor, in case of any disinvestment, must have stayed invested for at least 1 year from the date of making the ODI.

Disinvestment by the Indian party from its JV / WOS abroad may be by way of:

• transfer / sale of equity shares

• liquidation of the JV / WOS abroad.

• merger / amalgamation of the JV / WOS abroad.

Modes of Disinvestment: An Indian Party may disinvest from JV/WOS either

• without write off or

• with write off subject to the compliance of some conditions.

Conditions for automatic route for disinvestment

• No write off of investment

• No outstanding dues such as dividend, royalty, technical know-how from JV/ WOS

• Sale after 1 full year of operations and APR for said year has been submitted

• Indian party is not under investigation in India

• Shares sold on a Stock Exchange or if unlisted, share price not less than value certified by CA/CPA based on the latest audited balance sheet

Party to report disinvestment through AD bank within 30 days