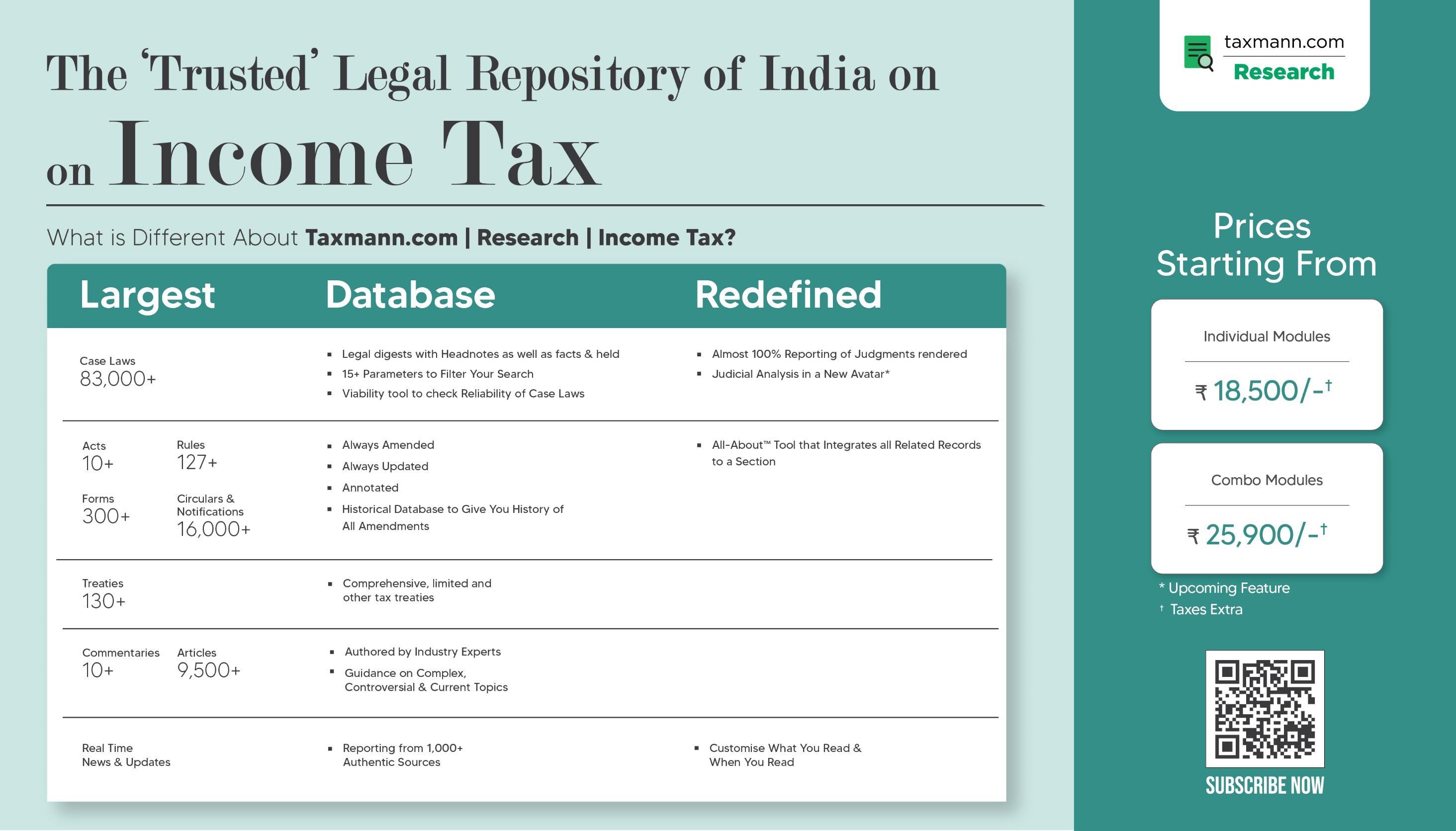

Taxation and Other Aspects of Private Trusts

Presentation Prepared by Nitin Satani Ayush Agarwal CA ROHAN SOGANI Speaker

DISCUSSION POINTS

Introduction to Private Trust Structure for Succession Planning

Overview of the Indian Trust Act, 1882

Tax Implications at the Time of Settlement of the Private Trust

Taxation of Income

earned by the Private Trust

Tax Implications on the Distribution of Assets on Termination of Trust or Otherwise

Effective Vehicle for Ring-fencing of assets

Implications under the Companies Act when a Private Trust holds Equity Shares

Applicability of FEMA on Private Trusts

CA Rohan Sogani 22nd December 2023

CA Rohan Sogani 22nd May, 2024

2

TRUSTSTRUCTURE

Beneficiaries

Fiduciary Capacity to manage the TrustAssetsfor the benefit ofBeneficiaries

Tr ust Trustees

Settles/ Contributes the Trust Property

Settlor/ Contributories

SShhaarreess// IInntteerreessttssiinn eennttiittiieess Shares/ Interests in entities Physical Assets

ADVISORY BOARD TO SUPERVISE THE TRUSTEES

CA Rohan Sogani 22nd December 2023 CA Rohan Sogani 14th March, 2024 nd May, 2024

3

INDIAN TRUST ACT, 1882

• Section 3 of the Indian Trust Act, 1882 defines ‘Trust’ as: “an obligation annexed to the ownership of the property, arising out of a confidence reposed in and accepted by the owner, or declared and accepted by him for the benefitoftheanother,orofanotherand theowner”

• Trust is not a separate legal entity. It is an obligation casted on the trustee by the settlor to employ the trust assets for the benefit of the beneficiaries

• Settlor / Author is the person who settles the trust. He can be a trustee or a beneficiaryaswell.

• Trustees are the persons who are bestowed with the responsibility of managing the assets of the trustandrightsand powersforwealthdistribution

• Beneficiaries are the persons for whom the trust has beensettled.

CA Rohan Sogani 22nd December 2023

CA Rohan Sogani 22nd May, 2024

4

STRATEGIC CONSIDERATIONS

CA Rohan Sogani 22nd December 2023

CA Rohan Sogani 14th March, 2024 nd May, 2024 5 Strategic Considerations Controlled Succession Planning Biz Managed Professionally Passing of wealth from generation to generation Asset protection Maintenance of the Family Creating single pool of investment

ROLES OF SETTLOR/TRUSTEE/BENEFICIARY

• ROLEOFTHESETTLOR

- Settlorhas no roletoplayintheoperations oftheTrust

- Settlortodecideon theOriginalTrustee,theTrustframeworkand initialbeneficiaries oftheTrust

• DUTIES&POWERSOFTHETRUSTEE

- TooperatetheTrustas pertheobjectsoftheTrust

- Tobuy/sellpropertyandinvesttheTrustmoneyandmonitor theinvestments

- Todistributeincome/assetsoftheTrust

- TogetreimbursementofexpensesincurredwhileexecutingobjectsoftheTrust

- Toaddorremovebeneficiary

- ToaddfurtherTrustees

• ENTITLEMENTSTOTHEBENEFICIARY

- EnjoyprofitsoftheTrustproperty

- ToexpecttheTrusteetoproperly protectand administerTrustproperty

- TocompeltheTrusteetoperformhis dutyproperly

CA Rohan Sogani 22nd December 2023

CA Rohan Sogani 14th March, 2024

nd May, 2024 6

TYPE OF TRUSTS

Type of Trusts

CA Rohan Sogani 22nd December 2023

CA Rohan Sogani 14th March, 2024 nd May, 2024 7

Revocable Trust v. Irrevocable Trust OralTrust v. WrittenTrust Testamentary Trust v. Non-testamentary Trust Specific Trust v. Discretionary Trust

CA Rohan Sogani 22nd December 2023 OVERVIEW OF THE INDIAN TRUST ACT, 1882 CA Rohan Sogani 22nd May, 2024 Sections Particulars 1 to 3 Preliminary & Title and Definitions 4 to 10 Creation of Trust – Conditions 11to 30 Duties and Liabilities of Trustees 31 to 45 Rights & Powers of Trustees 46 to 54 Disabilities of Trustees 55 to 69 Rights and Liabilities of Beneficiaries 70 to 76 Vacating the office of Trustees 77 to 79 Cessation of Trust 80 to 96 Certain Obligations-ATrust 8

PRIVATE TRUSTS Vs. WILL

Particulars Possibility of Succession Planning

Name beneficiaries for property

Leave property to young children

Revise your document

Avoid probate

Attracts stamp duty on transfer of Immovable Property

Comes into effect after death

Imperative to structureSuccession Planning to mitigate levy of Estate Duty

CA Rohan Sogani 22nd December 2023 CA Rohan Sogani 14th March, 2024 nd May, 2024

9 Private Trust

✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓

Wills

TAXATION OF PRIVATE TRUSTS [1/2]

Specific Trust

Where Trust’s income does not include business income

Section 161(1)

• Trustees are taxed in the like manner and to the same extent as the beneficiaries

• Assessment to be in same status as thatof each of beneficiaries

Where Trust’s income includes business income

Section 161(1A)

• Taxable at MMR –subject to certain exceptions

Discretionary Trust

Where Trust’s income does not include business income

Section 164(1)

• Taxableat MMR –subject to certain exceptions

Where Trust’s income includes business income

Proviso to Section 164(1)

• Taxableat MMR –subject to certain exceptions

Trustee may be taxed in representative capacity in both specific and discretionary trust

CA Rohan Sogani 22nd December 2023 CA Rohan Sogani 14th March, 2024 nd May, 2024

10

TAXATION OF PRIVATE TRUSTS [2/2]

RATES APPLICABLE TO INDIVIDUALS WILL BE CHARGED IF ALL THE FOLLOWINGCONDITIONSARESATISFIED:

• Trustisdeclaredbyasettlorbyway ofaWill;and

• Trustisdeclared exclusivelyforthebenefit ofanydependent relative;and

• SuchTrustistheonlytrustsodeclared byhim

RATESAPPLICABLE TOAOPWILLBECHARGED INACASE WHERE:

• Noneofthebeneficiaries:

– hastaxableincome exceeding theBasisExemption Limit;or

– isabeneficiary under anyotherprivateTrust or

• Where the relevant income or part of the relevant income is receivable under a trust declared byanyperson byWilland such trustistheonlytrustsodeclared byhim;

CA Rohan Sogani 22nd December 2023 CA Rohan Sogani 14th March, 2024 CA Rohan Sogani 22nd May, 2024

11

GIFT RECEIVED BY PRIVATE TRUST

• TAXABILITY IN THEHANDS OF DONOR –Section47(iii)-Transaction Not regarded as“Transfer”

• TAXABILITY IN THEHANDS OF TRUST/DONEE:

• “Relative” incaseofTrust

• Section 56(2)(x) :

Provided that this clause shall not apply to any sum of money or any property received— (I) from any relative; or… (X) from an individual by a trust created or established solely for the benefit of relative of the individual;

• clause (i) of proviso –Relationshipto betested from recipient’sperspective i.e.itneedstobetested whether thedonor qualifiesasa‘relative’from theperspective ofrecipient

• clause (x) of proviso –For trusts, relationshipneedsto betested from donor’s perspective andnot from recipient’sperspective i.e.itneedstobetested whether beneficiaries for whose benefit the trust issettledqualifyas‘relative’from the perspectiveof donor

CA Rohan Sogani 22nd December 2023 CA Rohan Sogani 14th March, 2024 CA Rohan Sogani 22nd May, 2024

12

CA Rohan Sogani 22nd December 2023 CA Rohan Sogani 14th March, 2024 nd May, 2024

[1/2] 13 Beneficiaries A Family Trust ABC Pvt. Ltd. Declaration of Beneficial ownership AB CD SECTION 89, 90 OF COMPANIES ACT, 2013

DECLARATION OF BENEFICIAL OWNERSHIP

Where the member of the reporting company is a trust (through trustee), and the individual,-

CA Rohan Sogani 22nd December 2023 CA Rohan Sogani 14th March, 2024 nd May, 2024

[2/2] 14

DECLARATION OF BENEFICIAL OWNERSHIP

S. No. Intimation to Company Type of Trust 1 Trustee Discretionary Trust or Charitable Trust 2 Beneficiary Specific Trust 3 Author or Settlor Revocable Trust

RING-FENCING OF ASSETS [1/2]

• Private Trust has emerged as an effective vehicle for succession planning for BUSINESS HOUSES.

• Transfer of Personal Assets to Trust, so that these assets can be insulated against possible future defaults of the businesses.

• Insolvency and Bankruptcy Code, 2016 has ushered new framework which provides easier mechanism for lenders to initiate recovery proceedings.

CA Rohan Sogani 22nd December 2023 CA Rohan Sogani 14th March, 2024 nd May, 2024

15

Transfer of Personal Assets

Private Family Trust

RING-FENCING OF ASSETS [2/2]

• Supreme Court in LALIT KUMAR JAIN VS. UNION OF INDIA [2021] 127 taxmann.com 368 (SC) held that “Guarantors obligation is not absolved for the balance amount dues due to involuntary process, i.e. by operation of law or due to liquidation or insolvency proceedings”

IBC - IMPACTING TRANSFER OF ASSETS TO TRUST:

• Section 164 states that any transaction entered by the bankrupt during the period of 2 years, ending the filing of application for bankruptcy, which causes bankruptcy process triggered, shall be considered as an undervalued transaction.

“In such scenario there would be heavy onus on such individual, to prove that transfer of assets/ property by him to private trust was out of a bonafide arrangement.”

CA Rohan Sogani 22nd December 2023 CA Rohan Sogani 14th March, 2024 nd May, 2024

16

FEMA ASPECTS OF TRUSTS – OVERVIEW

CA Rohan Sogani 22nd December 2023 CA Rohan Sogani 14th March, 2024 nd May, 2024

[1/2] 17 S. No. Particulars Gift to NR Gift to resident 1 Settlement of Assets a. From NRO b. From NRE a. Ntf. 13(R) - USD 1 million repatriation from NRO b. Freely permitted from NRE Permitted 2 Settlement of Currency (FCY) by way of remittance from abroad

not applicable as there is no change of assets in India for NR FEMA not applicable as there is no change of assets in India for NR 3 Settlement of Shares in Indian Companies FEM NDI Rules, 2019 - permitted FEM NDI Rules, 2019permitted 4 Settlement of Immovable Property in India FEM NDI Rules, 2019 - permitted FEM NDI Rules, 2019permitted NRI Settlor with Resident and Non - Resident beneficiaries - Trust in India S.No. Particulars Gift to NR Gift to Resident 1 Settlement of Currency (INR) LRS Scheme - permitted to NRI relatives FEMA not applicable 2 Settlement of shares in Indian companies FEM NDI Rules, 2019-Approval Route, subject to conditions FEMA not applicable 3 Settlement of Immovable Property in India FEM NDI Rules, 2019-permitted to NRI relatives FEMA not applicable Resident Settlor with Resident and Non- Resident beneficiaries- Trust in India

FEMA

FEMA ASPECTS OF TRUSTS –

CA Rohan Sogani 22nd December 2023 CA Rohan Sogani 14th March, 2024 nd May, 2024

OVERVIEW [2/2] 18 S.No. Particulars Gift to NR Gift to Resident 1 Settlement of Foreign Currency Permitted 2 Settlement of shares in Foreign companies 3 Settlement of Immovable Property outside India NRI Settlor with Resident and Non - Resident beneficiaries - Trust outside India FEMA not applicable FEM OI Rules, 2022 - Permitted S.No. Particulars Gift to NR Gift to Resident 1 Settlement of currency (INR) under LRS scheme LRS Scheme- permitted to any NRI LRS Scheme- not permitted 2 Settlement of shares in Foreign companies FEM OI Rules, 2022 Not permitted FEM OI Rules, 2022Permitted 3 Settlement of Immovable Property outside India FEM OI Rules, 2022- not permitted FEM OI Rules, 2022Permitted 4 Settlement of assets held outside India u/s. 6(4) of FEMA FEMA not applicable General permission under OI Rules Resident Settlor with Resident and Non- Resident beneficiaries- Trust outside India

Thank You! For More Information, Visit: https://taxmann.com/ Download Taxmann App Follow us on Social Media