Did you know that regulatory authorities flagged over 30% of reviewed companies for non-compliance with Ind AS 2 last year? These errors not only distort financial statements but can lead to hefty penalties and loss of investor trust.

Indian Accounting Standard Ind AS 2 (Inventories) establishes the principles for measuring and disclosing inventory in financial statements. Compliance with Ind AS 2 is essential to ensure transparency, comparability, and accuracy in financial reporting. However, several companies fail to adhere to these requirements, leading to misstatements and non-compliance issues.

This article highlights key observations made by the Financial Reporting Review Board (FRRB) on Ind AS 2 compliance, using real-world financial statement examples. It also explores the consequences of non-compliance and its impact on financial reporting.

To help finance professionals quickly identify key issues, here’s a summary of frequent compliance errors and their potential impact:

Compliance Issue

Incorrect Inventory Valuation

Wrong Cost Formula Application

Misclassified NonInventory Costs

Lack of Disclosure on Cost Formulas

Raw Material Valuation Errors

Key Mistake Impact

Ignoring Net Realizable Value (NRV)

Not distinguishing FIFO from the weighted average

Capitalizing legal & ad expenses as inventory

Not specifying FIFO or weighted average method

Valuing at cost without NRV assessment

Overstated profits, misleading financials

Confused financial reporting

Artificially inflated asset values

Reduced transparency for investors

Regulatory scrutiny, misreported financials

2.1

Ind AS 2, Para 9 – “Inventories shall be measured at the lower of cost and net realizable value.”

Ind AS 2, Para 6 – “Net realizable value is the estimated selling price in the ordinary course of business, less the estimated costs of completion and the estimated costs necessary to make the sale.”

Several companies valued inventories solely at cost without comparing them to the net realizable value (NRV). For instance, a company reported its raw materials, workin-progress, and finished goods at the weighted average cost but did not verify if the market value was lower. This approach violates Ind AS 2 since inventories should always be recorded at the lower of cost or NRV.

Failure to consider NRV can lead to an overstatement of inventory values, resulting in incorrect profit calculations. This misrepresentation may mislead investors and stakeholders about the company’s financial health, affecting decision-making and potentially leading to regulatory scrutiny.

Quick Fix – Always cross-check inventory values against the Net Realizable Value (NRV) before finalizing financial statements.

One company valued finished goods under forward contracts at NRV without considering the cost. Further, it was noted that other finished goods were valued at lower costs or market prices instead of NRV. The estimated costs of completion and the estimated costs necessary to make the sale have not been reduced from the estimated selling price for the purpose of valuation of inventories. The company did not follow the proper valuation formula.

Valuing inventories incorrectly affects the cost of goods sold (COGS) and gross profit margins. It can also distort financial performance metrics and lead to regulatory non-compliance, increasing audit risks and penalties.

Quick Fix – Ensure that NRV is properly calculated by deducting estimated costs of completion and sale. Follow a consistent inventory valuation approach across all finished goods, aligning with Ind AS 2 guidelines.

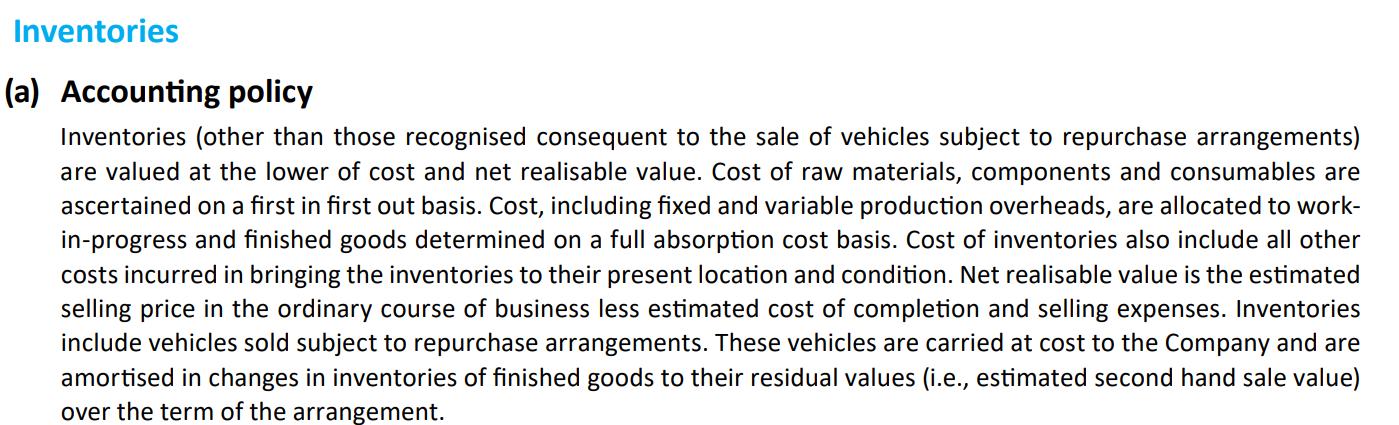

A relevant extract of notes forming part of the consolidated financial statements of Tata Motors Limited for the year ended March 2024 reflecting appropriate disclosure of accounting policy is enclosed herewith:

Ind AS 2, Para 15 – “Other costs are included in the cost of inventories only to the extent that they are incurred for bringing inventories to their present location and condition.”

Ind AS 2, Para 16 –”Examples of costs excluded from the cost of inventories and recognized as expenses in the period in which they are incurred include:

(a) abnormal amounts of wasted materials, labour, or other production costs;

(b) storage costs, unless those costs are necessary for the production process before a further production stage;

(c) administrative overheads that do not contribute to bringing inventories to their present location and condition; and

(d) selling costs.”

Certain companies incorrectly capitalized legal and professional charges, listing expenses, and advertisement costs to Work-In-Progress (WIP). These expenses were not directly related to inventory production and should have been expensed in the period they were incurred.

Capitalizing unrelated costs artificially inflates inventory values and defers expenses, misstating profitability and asset values. This practice can mislead investors and auditors, potentially leading to financial restatements and loss of stakeholder confidence.

Quick Fix – Only capitalize costs directly related to bringing inventories to their present location and condition. Expense unrelated costs (e.g., legal, advertising, listing fees) in the period incurred to avoid inflating inventory values.

Ind AS 2, Para36 – “The financial statements shall disclose:

(a) The accounting policies adopted in measuring inventories, including the cost formula used.”

Several companies disclosed the cost formula they used (e.g., weighted average or FIFO) but failed to specify the accounting policy adopted. On the other hand, one company’s policy stated that inventories were valued at cost or NRV but did not clarify whether FIFO or weighted average method was applied.

Lack of disclosure on cost formula creates ambiguity in financial statements, making it difficult for stakeholders to assess inventory valuation consistency. Investors rely on such disclosures for analyzing profitability trends, and incomplete information can reduce financial statement credibility.

Quick Fix – Clearly disclose both the cost formula (FIFO or weighted average) and the accounting policy adopted in financial statements to ensure transparency and avoid investor confusion.

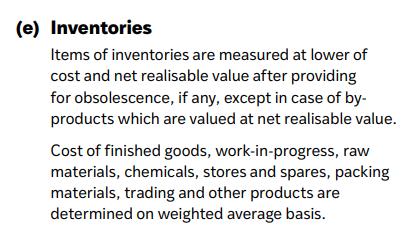

An extract of notes to the Standalone Financial Statements of Reliance Industries Limited for the year ended 31st March 2024 reflecting disclosure of the cost formula used is as below:

Ind AS 2, Para 9 – “Inventories should be valued at the lower of cost and net realizable value.”

Ind AS 2, Para 36 – “The financial statements shall disclose the cost formula used.”

One company stated that raw materials were valued at the weighted average cost but did not assess NRV. Additionally, it misclassified the weighted average method as an accounting policy instead of a cost formula.

Confusing cost formulas with accounting policies create misinterpretation risks for auditors and investors. This can lead to regulatory scrutiny, questioning whether inventory valuation is appropriately aligned with Ind AS 2.

Quick Fix – Properly differentiate between cost formulas (e.g., FIFO, weighted average) and accounting policies Ensure that NRV assessments are conducted for raw materials and not just finished goods.

Compliance with Ind AS 2 is essential for maintaining transparency, reliability, and consistency in financial reporting. The observations discussed in this article highlight frequent errors in inventory valuation, disclosure, and classification, which can result in material misstatements and regulatory non-compliance. To uphold financial integrity, companies must ensure that inventories are measured at the lower of cost and net realizable value (NRV), non-inventory costs are not improperly capitalized, and cost formulas—such as FIFO or weighted average—are clearly disclosed. Failure to adhere to these principles not only contravenes Ind AS 2 but also erodes investor confidence, distorts financial performance and may attract regulatory scrutiny or penalties. To mitigate these risks, organizations should proactively review and refine their inventory accounting policies and financial disclosures, ensuring they align with Ind AS 2 requirements and best practices.

Founded 1972

Evolution From a small family business to a leading technology-oriented Publishing/Product company

Expansion

Launch of Taxmann Advisory for personalized consulting solutions

Aim

Achieve perfection, skill, and accuracy in all endeavour

Growth

Evolution into a company with strong independent divisions: Research & Editorial, Production, Sales & Marketing, and Technology

Future

Continuously providing practical solutions through Taxmann Advisory

Editorial and Research Division

Over 200 motivated legal professionals (Lawyers, Chartered Accountants, Company Secretaries)

Monitoring and processing developments in judicial, administrative, and legislative fields with unparalleled skill and accuracy

Helping businesses navigate complex tax and regulatory requirements with ease

Over 60 years of domain knowledge and trust

Technology-driven solutions for modern challenges

Ensuring perfection, skill, and accuracy in every solution provided

Income Tax

Corporate Tax Advisory

Trusts & NGO Consultancy

TDS Advisory

Global Mobility Services

Personal Taxation

Training

Due Diligence

Due Dilligence

Advisory Services

Assistance in compounding of offences

Transactions Services

Investment outside India

Goods

Transaction Advisory

Business Restructuring

Classification

Due Diligence

Training

Advisory

Trade Facilitation Measures

Corporate

Corporate Structuring

VAT Advisory

Residential Status

Naveen Wadhwa

Research and Advisory [Corporate and Personal Tax]

Chartered Accountant (All India 24th Rank)

14+ years of experience in Income tax and International Tax

Expertise across real estate, technology, publication, education, hospitality, and manufacturing sectors

Contributor to renowned media outlets on tax issues

Vinod K. Singhania Expert on Panel | Research and Advisory (Direct Tax)

Over 35 years of experience in tax laws

PhD in Corporate Economics and Legislation

Author and resource person in 800+ seminars

V.S. Datey Expert on Panel | Research and Advisory [Indirect Tax]

Holds 30+ years of experience

Engaged in consulting and training professionals on Indirect Taxation

A regular speaker at various industry forums, associations and industry workshops

Author of various books on Indirect Taxation used by professionals and Department officials

Manoj Fogla Expert on Panel | Research and Advisory [Charitable Trusts and NGOs]

Over three decades of practising experience on tax, legal and regulatory aspects of NPOs and Charitable Institutions

Law practitioner, a fellow member of the Institute of Chartered Accountants of India and also holds a Master's degree in Philosophy

PhD from Utkal University, Doctoral Research on Social Accountability Standards for NPOs

Author of several best-selling books for professionals, including the recent one titled 'Trust and NGO's Ready Reckoner' by Taxmann

Drafted publications for The Institute of Chartered Accountants of India, New Delhi, such as FAQs on GST for NPOs & FAQs on FCRA for NPOs.

Has been a faculty and resource person at various national and international forums

the UAE

Chartered Accountant (All India 36th Rank)

Has previously worked with the KPMG

S.S. Gupta Expert on Panel | Research and Advisory [Indirect Tax]

Chartered Accountant and Cost & Works Accountant

34+ Years of Experience in Indirect Taxation

Bestowed with numerous prestigious scholarships and prizes

Author of the book GST – How to Meet Your Obligations', which is widely referred to by Trade and Industry

Sudha G. Bhushan Expert on Panel | Research and Advisory [FEMA]

20+ Years of experience

Advisor to many Banks and MNCs

Experience in FDI and FEMA Advisory

Authored more than seven best-selling books

Provides training on FEMA to professionals

Experience in many sectors, including banking, fertilisers, and chemical

Has previously worked with Deloitte

Taxmann Delhi

59/32, New Rohtak Road

New Delhi – 110005 | India

Phone | 011 45562222

Email | sales@taxmann.com

Taxmann Mumbai

35, Bodke Building, Ground Floor, M.G. Road, Mulund (West), Opp. Mulund Railway Station Mumbai – 400080 | Maharashtra | India

Phone | +91 93222 47686

Email | sales.mumbai@taxmann.com

Taxmann Pune

Office No. 14, First Floor, Prestige Point, 283 Shukrwar Peth, Bajirao Road, Opp. Chinchechi Talim, Pune – 411002 | Maharashtra | India

Phone | +91 98224 11811

Email | sales.pune@taxmann.com

Taxmann Ahmedabad

7, Abhinav Arcade, Ground Floor, Pritam Nagar Paldi

Ahmedabad – 380007 | Gujarat | India

Phone: +91 99099 84900

Email: sales.ahmedabad@taxmann.com

Taxmann Hyderabad

4-1-369 Indralok Commercial Complex Shop No. 15/1 – Ground Floor, Reddy Hostel Lane Abids Hyderabad – 500001 | Telangana | India

Phone | +91 93910 41461

Email | sales.hyderabad@taxmann.com

Taxmann Chennai No. 26, 2, Rajan St, Rama Kamath Puram, T. Nagar

Chennai – 600017 | Tamil Nadu | India

Phone | +91 89390 09948

Email | sales.chennai@taxmann.com

Taxmann Bengaluru

12/1, Nirmal Nivas, Ground Floor, 4th Cross, Gandhi Nagar

Bengaluru – 560009 | Karnataka | India

Phone | +91 99869 50066

Email | sales.bengaluru@taxmann.com

Taxmann Kolkata Nigam Centre, 155-Lenin Sarani, Wellington, 2nd Floor, Room No. 213

Kolkata – 700013 | West Bengal | India

Phone | +91 98300 71313

Email | sales.kolkata@taxmann.com

Taxmann Lucknow

House No. LIG – 4/40, Sector – H, Jankipuram Lucknow – 226021 | Uttar Pradesh | India

Phone | +91 97924 23987

Email | sales.lucknow@taxmann.com

Taxmann Bhubaneswar

Plot No. 591, Nayapalli, Near Damayanti Apartments

Bhubaneswar – 751012 | Odisha | India

Phone | +91 99370 71353

Email | sales.bhubaneswar@taxmann.com

Taxmann Guwahati

House No. 2, Samnaay Path, Sawauchi Dakshin Gaon Road

Guwahati – 781040 | Assam | India

Phone | +91 70866 24504

Email | sales.guwahati@taxmann.com