OFFICIAL PARTNERS THE ANNUAL GUIDE TO THE MOST INFLUENTIAL, INNOVATIVE COMPANIES AND POWERFUL FIGURES WITHIN THE FINTECH INDUSTRY

The worlds leading fintech newspaper thefintechtimes.com /fintech-times/ /thefintechtimes /thefintechtimes Scan me to read the latest edition

WELCOME TO THE FOURTH EDITION OF THE FINTECH POWER 50

This year’s Fintech Power 50 cohort of companies is more diverse than ever – both in terms of which sectors they’re disrupting and where in the world they are disrupting them.

Our talented tech stars are pushing the boundaries in Asia, Canada, Europe, the Middle East, Nigeria, the UK and the USA. They are having an impact in regtech, paytech, wealthtech, banking-as-a-service, insurtech, lendtech, core banking and open banking.

What that demonstrates to me is that the events of the last couple of years in terms of COVID – which forced digital transformation on folk who would have taken their own sweet time about it – has created a flywheel of innovation that is truly touching everyone and changing

every aspect of our financial lives for the better. That includes those who’ve not had access to a full range of financial services until now, limiting their own and even their country’s economic potential.

This sudden acceleration in innovation has, inevitably, crashed us into some fundamental walls – policy and regulation; exposed weaknesses in infrastructure; and shone a spotlight on attitudes and cultures that still persist within legacy institutions and which are holding back progress. We need a fresh perspective on all those as much as we do on products and their delivery.

While our lively cohort are busy at the coalface, spinning up ideas and technology to solve painpoints for customers and the industry, you’ll find writing in this issue of The Fintech Power 50, 10 finfluencers – people with years of experience and broad strategic awareness – who are taking a thoughtful approach to some of those structural issues.

»The events of the past couple of years have created a flywheel of innovation

Although many of them hold positions of real influence beyond the industry, we can’t leave it all to them. As Natasha De Terán writes on page 85, ‘it’s in the confluence of imagination, innovation and investment with policy, regulation and infrastructure that real transformation can really happen’. And she urges founders to take time to get involved with what fintechs perhaps see as dull, but are nevertheless deeply important, discussions that fundamentally affect fintechs' own operation and growth.

Dr Leda Glyptis, on page 70, believes that ‘we are at a moment of time in our industry where we get the opportunity to do more and make more of an impact on the societies we live in than ever before’. That feeling of urgency – not to let this opportunity pass – and fintechs’ responsibility to seize it, is reflected by many of her fellow finfluencers. We hope that this year’s The Fintech Power 50 accelerator programme will inspire and help its members to take that opportunity: to deliver on fintech’s promise – for everyone.

Mark Walker Co-founder, The Fintech Power 50

JASON WILLIAMS

MARK WALKER

JASON WILLIAMS

MARK WALKER

www.thepower50.com THEFINTECHPOWER50 3

Our team of dedicated fintech accountants and business advisers understand the complex demands of the sector. The team provide a full service to clients of all sizes, from start-ups to substantial international groups, to ensure businesses meet their compliance obligations whilst helping to maximise their potential. Our core services to the fintech sector include: Tom Moore Head of Financial Services www.mks.co.uk • Strategic advice • Data proctection • Cybersecurity • Staff engagement • Regulatory reporting and advice • Audit and accounts • Tax • HR and payroll • Fundraising and M&A • Legal services UNLOCKING YOUR FINTECH BUSINESS’ POTENTIAL

FINTECH WALES WE’RE ON A MISSION!

FinTech Wales is a not-for-profit organisation that champions the country’s fintech community on the global stage.

Wales was named as one of the top 10 fintech clusters in the Kalifa Review Of UK Fintech, and is, in the opinion of FinTech Wales’ CEO Sarah Williams-Gardener, the place to start up, scale up and accelerate innovative fintech businesses.

We spoke to her about the Welsh fintech ecosystem and what FinTech Wales is doing to empower the country as a force in the fintech community worldwide.

TFP50: Can you tell us more about the FinTech Wales mission?

Sarah Williams-Gardener: Our strategy is to support innovation, create jobs and economic growth by developing an ecosystem that enables fintechs to flourish and succeed, thanks to the availability of talent, skills and investment.

We have the most incredible fintech businesses and professionals here, with so much to be proud of. We want to do our thriving community justice and empower individuals and fintech organisations to be successful on the world stage while being a major driver in the UK economy.

TFP50: What are your biggest challengers?

SWG: It’s no secret that the world

is seeing huge shortages in certain skills, which has a significant impact on organisations’ ability to develop and thrive. FinTech Wales has a highly-valued skills strategy, which comes in three parts:

■ Raise awareness of the fantastic career opportunities we have in fintech

■ Develop skills required now and in the future to support the rapid growth of our ecosystem

■ Retain and upskill the talent we have available in Wales

Through partnerships with our members, education providers, governments and other organisations, we have introduced a number of programmes to tackle all three objectives, all of which have a strong focus to encourage people of all ages and backgrounds into fintech.

TFP50: What are you most excited about in the Welsh world of fintech? SWG: Every day we’re seeing established organisations embracing innovation, scaling businesses raising funds to support their rapid growth, and all sorts of new ventures being launched. Our accelerator programme, The Foundry, alone has taken 16 startups through a 12-week, no-equity, mentoring programme and their success to date is extraordinary. They have collectively raised more than £20million in investment, and whilst some of these companies originated from outside of Wales, they all now have a presence here,

bringing jobs, innovation and even more talent to our economy.

Our ecosystem energises new ventures to thrive and encourages corporate partnerships to be established. I’m confident we’ll have another FTSE 100 in our community before too long.

TFP50: What would you say to encourage a fintech to start or scale here?

SWG: Wales has so much on offer for any business looking to grow. Whether you’re a startup, scaleup or enterprise business, you’ll enjoy a complete sense of belonging. Our ecosystem is inclusive, and boasts a community of leaders who sincerely believe that we are stronger together. This ecosystem benefits from established brilliant fintechs, truly inspirational leaders, and great universities and higher education providers, who are growing the talents and skills of the future. We work closely with the government, too, which has prioritised fintech for growth.

With enchanting beaches and mountains, Wales is also a beautiful place to live and work. The ability to take time out and reflect is essential for any business owner and their employees. Once you get a taste of Wales, it’s very hard to leave.

One thing that Wales doesn’t do well, however, is shout enough about what it has achieved, which is why promoting its successes is a key part of our strategy. We’re shouting from the rooftops how innovative and successful the Welsh fintech ecosystem is – and there’s still so much more to come from our Welsh fintech hub of excellence.

Enjoy the benefits of being a FinTech Wales member and join our community today

www.thepower50.com THEFINTECHPOWER50 5

CEO Sarah Williams-Gardener on what makes Wales great for starting and scaling a business – and why it needs to be less modest

–www.fintechwales.org

Presenting Rise Connect

Rise Connect is a global, virtual network of fintech leaders shaping the future of financial services, with support from the Barclays network and key industry partners.

Access exclusive content, peer-to-peer networking, events and opportunities to help you succeed.

Apply Now

HOW TO RAISETHE STAKES

Angela Yore and Kimberley Waldron, Co-founders of SkyParlour, discuss how PR is helping fintechs attract considerable venture capital, even in the midst of a funding ‘downturn’

At SkyParlour, we remember a time when fintech was only really understood by those working alongside traditional financial institutions and banks.

When we launched in 2009, the sector was still finding its feet, with some commentators doubting how much staying power the industry would have.

Fast forward more than a decade and things are now very different. The sector has reached a new stage of maturation.

In 2021, the UK fintech sector received more than $37.3billion in investment, according to KPMG. Despite some recent concerns about a funding slowdown, fintech industry body Innovate Finance believes the sector will see similar figures again this year.

Adoption rates of fintech solutions are also skyrocketing. In 2021, open banking platform Plaid found the use and adoption of fintech had reached mass scale in the UK, with up to 86 per cent of consumers using it.

A SEA OF OPPORTUNITY

This impressive growth has had a positive effect across the industry, including for smaller businesses. Thriving market conditions have created opportunities for exciting new businesses to get a start in the sector. Now that a path has been forged for them, innovators clearly feel

more confident about bringing forward-thinking fintech solutions to market. It’s a case of a rising tide lifting all ships. However, challenges remain. In particular, businesses, be they a stalwart of the fintech sector or a bootstrapped startup fighting for its first big break, still don’t know how to get the most out of funding, especially in moments of broader economic uncertainty.

THE RIGHT PATH WITH PR

Over our history, SkyParlour has partnered with numerous fintech companies through different stages of their investment journey. Despite reports of a slowdown, we have helped our clients to secure nearly $1billion in funding in the past two years alone. It might sound too good to be true, but it’s not; it’s just testament to the benefits of the well-organised, expertly planned PR campaigns we deliver.

If you’re unfamiliar with PR, you might ask why that is. Well, with the right PR approach, businesses in fintech can really showcase what sets them apart from their competition.

PR provides businesses with an opportunity to highlight areas of true strength and enables them to be amplified in the minds of angel investors and venture capital businesses who may be looking to invest. Our services help

fintechs to truly stand out from the crowd, which is more important than ever if investors are becoming more risk averse.

A TRACK RECORD OF SUCCESS

You only need to look at some of our recent results to see this in action. Whether its relative new starters, such as SEON (with whom we worked closely as it first secured a record-breaking Series A investment, and then a record-breaking Series B investment), or Finaro, which announced its acquisition by the American leader in commerce-enabling technology, Shift4, in a deal valued at US $575million.

What’s more, once investment is secured, a good PR company will generate even further value from it. Funding rounds come with huge PR potential and must be approached accordingly. For example, we recently helped our client, Weavr have its Series A investment round covered by leading sites, including Bloomberg and Business Insider. Gaining such notable coverage has helped to further grow the company’s profile and put it in an even better position ahead of its next round of investment.

Learn more at www.skyparlour.com

www.thepower50.com THE FINTECHPOWER50 7

Identity verification through informed AI. Learn how Jumio is using informed AI to deliver identity verification as it should be. Visit jumio.com Loved by users. Loathed by fraudsters.

REGUL ATING INNOVATION

Pierre Berger, Partner and Head of Financial Services and the Insurance Sector for DLA Piper Belgium, considers the challenges involved

The financial services sector, in constant search of speed, efficiency and optimisation, is fertile ground for the emergence and development of automative and innovative solutions.

Often based on AI – in particular, machine learning – these solutions already have many applications in the markets and are experiencing a rapid and growing evolution.

Financial institutions are encouraged to use AI and machine learning to deliver a number of benefits: cost reduction, process automation, risk management optimisation, productivity improvement and an uplift in profitability. Meanwhile, new and innovative firms – fintechs – are developing technologies to not only optimise but also to entirely rethink the provision of financial services.

Many applications of AI are already a reality in financial markets, notably in relation to investment services (algorithmic and high-frequency trading, robo-advisors), banking services (neo-banks, credit scoring) and in financial crime management (anti-money laundering/combating the financing of terrorism, fraud detection).

But, beyond the emergence of new business models, financial technology innovation also offers opportunities for regulated institutions in terms of compliance with regulatory and prudential requirements (regtech) and to financial authorities for regulatory, supervisory and control purposes (suptech). The rise of regtech and suptech has been driven by the substantial increase in the availability

and granularity of data, and by the development of technologies, as well as infrastructures such as Cloud computing and application programming interfaces (APIs), which make it possible to collect, store, and analyse large data sets more quickly and efficiently.

The application of these new technologies, however, affects the risks inherent in the financial system and itself introduces new risks; for example, in terms of data protection, market integrity, or in terms of cyber risks.

From a legal perspective, it poses a challenge to traditional regulatory methods. The fintech ecosystem, which brings new players alongside regulated financial institutions, is changing the dynamics of the financial system and challenging the application of existing regulations to new fintech activities.

Most European financial regulation is technology-neutral – it applies equally to regulated financial services, regardless of the type of underlying technology used. This approach should ensure that the emergence of new technologies that are developed to provide a regulated service won’t affect the need to comply with the regulatory framework applicable to the provision of that service. However, this approach may itself be a source of legal uncertainty because of the difficulty of applying traditional regulatory requirements to disruptive businesses.

Meanwhile, a particular challenge for regulators is to identify and monitor emerging new dynamics within markets, which also requires them to have a deep understanding of the technologies used to deliver innovative services or products.

Against this backdrop, regulators are trying to develop strategies to respond to developments and to improve their understanding of new fintech activities.

Various European member states have set up innovation facilitators, including regulatory sandboxes and innovation hubs. This approach allows regulators to develop their knowledge of technology at an early stage in order to confront it with regulation and their supervision methods. For innovative firms, it allows them to gain quicker access to market and to better understand the prudential rules and requirements applicable to their activities.

AT A GLANCE

DLA Piper is a global law firm with a presence in more than 40 countries. It is a leader in the financial services and fintech sector, advising clients on the full lifecycle of financial regulatory matters. This includes authorisation and compliance, transactional and products advice, investigations and enforcement and litigation. It regularly assists clients with the development of AI-driven products and tools from a legal perspective. Clients range from multinational, Global 1000 and Fortune 500 enterprises, to emerging companies developing industry-leading technologies. DLA Piper also advises governments and public sector bodies.

CONTACT: Pierre.Berger@dlapiper.com

WEBSITE: www.dlapiper.com

www.thepower50.com THEFINTECHPOWER50 9

Why do 5 of the top 10 global banks trust the Appian Low-Code Platform for building and running their most complex, mission-critical applications? Because Appian makes it easy to create powerful workflows with a unified platform for change. We discover, design, and automate your processes so you can punch above your weight class.

Why do 5 of the top 10 global banks trust the Appian Low-Code Platform for building and running their most complex, mission-critical applications? Because Appian makes it easy to create powerful workflows with a unified platform for change. We discover, design, and automate your processes so you can punch above your weight class.

Why do 5 of the top 10 global banks trust the Appian Low-Code Platform for building and running their most complex, mission-critical applications? Because Appian makes it easy to create powerful workflows with a unified platform for change. We discover, design, and automate your processes so you can punch above your weight class.

To learn more, visit appian.com/finserv

Modernize and deliver exceptional client experiences, fast.

To learn more, visit appian.com/finserv

Modernize and deliver exceptional client experiences, fast.

To learn more, visit appian.com/finserv

Modernize and deliver exceptional client experiences, fast.

THE LOW-CODE CHECKLIST

When you’re in the market for a technology to help your business run better, you’re likely to hear solution and platform vendors make pitches that focus on their current features and functionality, as well as future capabilities on their innovation road maps. But will they really deliver the

outcomes you want?

When evaluating your options, it’s best to first define your needs, discover where opportunities exist, be brutally honest about where the challenges lie, and then gauge the available technologies against these requirements. This is the best approach to ensure the technology you invest in meets all your needs once your developers and users get their hands on it.

A low-code application development platform may not be the first thing you think of when you’re in the early stages of researching technology options. But, if the priorities and concerns listed below appear on your list of issues to address, then low-code may be exactly what you need.

■ My speed to market is critical

You operate in a highly competitive environment, so the faster you can stand up new applications to meet the business’ needs, the better.

■ My organisation/market requires rapid change and agility This is true for just about everyone now. It may prove to be the new normal.

■ I have complex business processes

By automating these processes, you will allow your staff to focus their energies on activities that will add value to your business.

■ Our routing and approval paths are cumbersome The path to the necessary approvals and input must be clearly defined and seamlessly executed.

■ We need to minimise coding errors, reduce security vulnerabilities, and/or increase data quality Whether you feel that your current, more manual efforts to achieve these outcomes are holding you back, or you’re lagging in these areas and putting the business at risk,

automation could be the solution.

■ We need to increase our developers’ productivity Rapidly changing business needs are putting pressure on your development team. You need a way to deliver applications faster to alleviate this pressure.

■ There are bottlenecks that mean we can’t make rapid and informed decisions If your stakeholders don’t have the data necessary to make the most informed decisions, there could be negative impact on the business.

■ We have multiple data sources but we don’t want to mess about with migrating data You have data stored in a variety of systems and formats, but it is all essential and should all be accessible from a single interface.

■ We operate in a regulated environment – we can’t afford to compromise compliance You need compliance and governance built into your technology. There's no room for surprises or workarounds when strict adherence to guidelines is a must.

■ We’re sitting on a large amount of tech debt Tech debt tends to create more backlog the longer it’s left unchecked. But there are technologies available that reduce it, not add to it.

■ IT spends a lot of time on maintenance, which detracts from innovation Your tech needs to be fast, agile, and easy to maintain, while still delivering the power to run processes.

A low-code platform satisfies all of these and many other requirements. By creating code in the background, according to the highest security and standards, it takes care of the (coding) details and automatically stays up to date with the latest technology. Low-code is:

■ Fast Development can be 10 times faster than traditional approaches.

■ Powerful Complete automation enables applications to easily integrate into core business systems.

■ Easy to maintain Because the vendor keeps the platform up to date with the latest security and device standards, those updates are automatically passed on to the application.

To help decide if a low-code platform is right for you, Appian has produced The Ultimate Low-Code Automation Buyer’s Guide, which provides an evaluation framework that helps business and IT leaders find the best platform for their needs. It can be accessed by visiting the Appian website at appian.com.

AT A GLANCE

Appian is the unified platform for change. We accelerate customers’ businesses by discovering, designing, and automating their most important processes. The Appian Low-Code Platform combines the key capabilities needed to get work done faster – Process Mining + Workflow + Automation – in a unified low-code platform. Appian is open, enterprise-grade, and trusted by industry leaders.

WEBSITE: appian.com

www.thepower50.com THEFINTECHPOWER50 11

Faced with an increasingly crowded marketplace of technology solutions, Appian's Marianne Elie says a low-code platform could be your best option

OCR LABS

No matter what role you play in a user onboarding process – user, product owner, compliance, risk, fraud, sales, or marketing officer… the list goes on – it’s becoming increasingly demanding to meet exceptionally high standards.

Customers expect the best, most risk-appropriate onboarding experience; product owners, sales and marketing departments want the highest conversion rates; risk, fraud and compliance officers want the lowest fraud rates and losses – and all while complying with a myriad of local and international regulatory requirements. How can all these priorities be met?

FULL AUTOMATION

The use of deep learning, neural networks and computer vision isn’t new. Every time, you make choices on Amazon or Google, that decision is fed into an engine to improve your experience. So, why shouldn’t identity verification be the same?

Many legacy solutions have relied on ‘hybrid’ solutions that combine some level of automation (mainly templating, but more on that later) with a human ‘super-spotter’ or call centre. This

approach has been the mainstay of the industry for some time due to technology limitations. But we have developed and rolled out the capability to leverage riches of deep learning in order to provide an identity-proofing experience that can satisfy all onboarding roles.

Can a human spot a change in watermark on a driving licence or a person’s heartbeat between video frames (photoplethysmography – try saying that three times, fast!) to give a 100 per cent liveness video fraud assessment?1

The role of people shouldn’t be limited to comparing a document with a photo or video. This is the kind of work that machines and technology were made for. Higher priority tasks, such as case investigations or strategic initiatives, provide so much more value to both staff and organisations.

Automation leads to predictable onboarding times for product owners, sales and marketing executives, while their colleagues in risk, fraud and compliance know that the exact checks and balances are being applied to every application with repeatable and reliable consistency.

TALKING YOUR LANGUAGE

At OCR Labs, we are incredibly proud that our technology can recognise more than 16,000 document types from virtually every location in the world, along with 142 languages and typesets. We do this through the power of neural networks and contextual analysis, not the traditional templating approach.

Templating identity documents takes great time and resources and is prone to user frustration, whereas using a contextual approach to detecting documents is more seamless and scalable.

We can’t expect humans to remember the intricate formats and security elements of thousands of official documents. Deep learning can detect these in seconds – and not just all of the visible factors, but the invisible changes, too.

Being able to rely on a system to automatically accept and reject documents does wonders for both catching fraud and the overall user experience. Knowing that each user, no matter the market you are serving, is

THE END OF HYBRID IDENTITY VERIFICATION

OCR Labs is putting a new way of developing and executing on identity proofing at the forefront of KYC – one that relies on machine learning and neural networks over human super-spotters

THEFINTECHPOWER50 www.thepower50.com12

receiving an equal experience helps you to present a consistent brand experience.

ADDRESSING RACIAL BIAS

Humans and algorithms don’t always see all faces equally, whether due to the data sets used for training or a cross-race effect (the tendency to more easily recognise faces in one’s own racial group).

Studies conducted by the National Institute of Standards and Technology have found that most algorithms have a harder time recognising people with darker skin tones. Facial recognition technology has been around for decades, but it is primarily focussed on whether an image contains a face and whether that face matches the face in another image.

To do this, most facial recognition systems measure the distances between certain facial features, like the space between the eyes for example. Skin tone has traditionally not been considered at all. As a result, facial recognition can be less accurate for different ethnicities and can cause a racial bias.

We’ve built our facial recognition technology ourselves and skin tone is one of the primary factors we consider when matching a selfie with a user’s identity document. Combined with a live photo, which considers three dimensions of a face rather than just two, we are able to take skin tone into consideration, with 99.9997 per cent laboratory-measured efficacy.2

PROPRIETARY TECHNOLOGY

Exactingly made, precision-engineered and meticulously tested, our end-to-end ID verification system has been built

WHO WE ARE

OCR Labs makes user verification effortless through technology.

We build intelligent tools that protect users from identity fraud while enabling a seamless user experience. It removes the burden of identity verification for our customers, too, so they can focus on scaling their business without the compliance and operational overheads.

with an unerring focus, underpinned by cutting-edge research and rigorous continual testing against fraud. Building technology this precise allows us to create onboarding and verification products that are powerfully intuitive and natural – truly built around, and for, people. This ensures our products welcome your customers in, while powerful but invisible anti-fraud technology keeps fraudsters out. Deep learning, neural networks and big data have become part of our lives in the search for competitive advantage and societal gain. This applies to identity, too, as it becomes vital for access to goods and services globally.

1 iBeta/2BixeLab, both are NVLAP accredited biometrics testing labs, providing NIST accredited biometric testing services in accordance with ISO/IEC 17025:2017.

identity trust frameworks. These include Australian TDIF accreditation as an Identity Service Provider, SOC Type 1 & 2 and ISO 27001, 27017, 27018, 27701, 29100, 22301, 30107-3 (covering both PAD levels 1 and 2), 19795 and 9001.

OCR Labs is ranked #1 globally for detection of real and fraudulent ID.

AT A GLANCE

COMPANY: OCR Labs

FOUNDED: 2018 CATEGORY: ID verification

»

Can a human spot a change in watermark on a driving licence or a person’s heartbeat between video frames?

Using advanced image analysis and deep learning technology we securely verify users in seconds with just their ID and a smartphone, from anywhere in the world. In fact, we verify more than 16,000 documents in more than 230 countries and principalities – more than any other identity verification provider.

Our verification solution is used by startups through to global enterprises, including Westpac and ANZ banks, the Australian government, Vodafone, ZIP and BMW.

OCR Labs meets the most stringent privacy, data protection, security, resilience standards and global digital

KEY PERSONNEL: Russ Cohn, General Manager International (right)

HEAD OFFICE: UK

OFFICES IN: Australia, Turkey and USA

EMAIL: hello@ocrlabs.com

WEBSITE: ocrlabs.com/

LINKEDIN: linkedin.com/ company/ocrlabs

TWITTER: @ocrlabs

WHAT WE DO Automated identity verification

www.thepower50.com THEFINTECHPOWER50 13

Fighting financial crime in real-time has never mattered more for fintechs. From deep fake fraudsters to crypto cons, ComplyAdvantage spells out the risks

Fintechs are continuing to change the way consumers interact with their banks. Onerous trips to branches have been replaced by rapid transactions from mobile devices.

From the comfort of their homes, consumers can send money across borders, trade virtual assets and apply for a mortgage. This transformation has delivered tremendous benefits – a faster, more convenient customer experience and a more personalised service being just two. However, money launderers and fraudsters have also adapted.

Detecting and preventing financial crime means harnessing the vast amount of data that fintechs generate to act in real-time. Here are three key areas any fintech needs to consider as part of a risk-based, real-time response to risks.

THE EVOLVING USE OF SANCTIONS

Western governments have become increasingly reliant on sanctions as a tool of statecraft. As their populations have turned against the idea of military intervention abroad, sanctions have assumed a greater role. One example of this is in the field of human rights, where the so-called Global Magnitsky (GloMag) sanctions targeting human rights abuses – and corruption specifically – have become commonplace.

Since the Global Magnitsky Act was authorised in the United States in 2016, other similar programmes have become law in the European Union, United

Kingdom, Canada and Australia. As a result, sanctions are being applied more frequently than ever before.

Western sanction regimes accelerated still further with the Russian invasion of Ukraine. Countries have sanctioned thousands of entities across a wide range of sanctions lists, with new measures being announced daily in the early weeks of the war.

The potential impact of sanctions breaches on individuals and organisations underlines the point that governments take compliance with their laws and regulations extremely seriously, and, therefore, so should fintechs. Although sanctions laws can seem arcane in places, it pays for firms to understand their significance, and act accordingly. In evolving situations, such as the Russian invasion of Ukraine, this means acting fast, too.

THE SHIFTING DYNAMICS OF FRAUD

Fraud is another area where the risks and typologies that fintechs must screen for are changing. One example is deepfake technology. In 2021, bank robbers stole $35milion from a bank in the United Arab Emirates using a deepfake to mimic a legitimate business transaction.

Currently, money muling is a key typology concern for fintech compliance professionals. But deepfake technology could one day supersede this. Why would a money launderer go to the effort of recruiting and managing a money muling network if they could simply overlay

someone’s face onto their own and use it to open accounts? The FBI recently issued a statement, saying deepfake technology is set to be utilised more by malicious actors in the near future.

Fintechs must ensure their anti-money laundering programmes – and wider risk-based approach – are calibrated to just such emerging threats, as well as existing challenges.

THE RISING ADOPTION OF CRYPTO

With 98 per cent of firms interviewed for our The State Of Financial Crime 2022 report, saying they’re either crypto-native, accept/work with crypto, or plan to offer crypto-based services in the future, cryptocurrencies are continuing to become mainstream. This means the regulatory and financial crime risks posed by cryptocurrencies should be a concern to all fintechs. While many of these concerns are similar for fiat-based services, some are unique to crypto.

Regulatory frameworks around cryptocurrencies are developing rapidly, and will continue to do so for the foreseeable future. Firms should be agile to changing requirements related to licensing, taxation, reporting, customer onboarding, and much more. As a result, fintechs should conduct horizon-scanning exercises to ensure they’re monitoring events and incoming legislation.

They need to understand new requirements and their potential implications. Crucially, they should also

THEFINTECHPOWER50 www.thepower50.com14 COMPLYADVANTAGE

contribute to regulatory consultations whenever possible, to help shape the future of the industry.

Fintechs operating in the crypto space risk facing a simultaneous growth in their customer base, alongside a swathe of new regulatory requirements. This could lead to customers being onboarded who present a financial crime risk. Conversely, it could lead to significant delays in legitimate customers gaining access to the service, leading them to look elsewhere. Automated onboarding, screening and monitoring tools that help firms meet their regulatory requirements are critical to a proactive approach to this challenge.

THE BEST TIME FOR REAL-TIME

Sanctions, fraud and crypto are just three of the many areas where fintechs are being required to think – and act – in real time to tackle financial crime risks and deliver a great customer experience.

By investing in smart, flexible, automated risk-detection platforms

– and hiring the right talent – fintechs can develop a proactive approach. As competition intensifies for new customers and business, such firms will surely reap the rewards.

WHO WE ARE

ComplyAdvantage is the financial industry’s leading source of AI-driven financial crime counter risk intelligence.

Its mission is to neutralise the risk of money laundering, terrorist financing, corruption and other financial crime.

More than 500 enterprises in 75 countries rely on ComplyAdvantage to understand the risk of who they’re doing business with through the world’s only global, real-time database of people and companies. The company actively identifies tens of thousands of risk events from millions of structured and unstructured data points, every single day.

ComplyAdvantage has four hubs located in New York, London, Singapore and Romania and is backed by Goldman Sachs, Ontario Teachers’, Index Ventures and Balderton Capital.

AT A GLANCE

COMPANY: Comply Advantage

FOUNDED: 2014

CATEGORY: Real-time risk detection

KEY PERSONNEL: Charles Delingpole, Founder and CEO (above)

HEAD OFFICE: UK OFFICES IN: New York, Singapore and Romania

TEL: +44 (0) 207 834 0252

EMAIL: contact.uk@ complyadvantage.com

WEBSITE: complyadvantage.com

LINKEDIN: linkedin.com/company/ complyadvantage

TWITTER: @complyadvantage

»Fintechs must ensure their anti-money laundering programmes – and wider risk-based approach – are calibrated to emerging threats, as well as existing challenges

WHAT WE DO The leading source of AI-driven counter risk intelligence

15www.thepower50.com THEFINTECHPOWER50

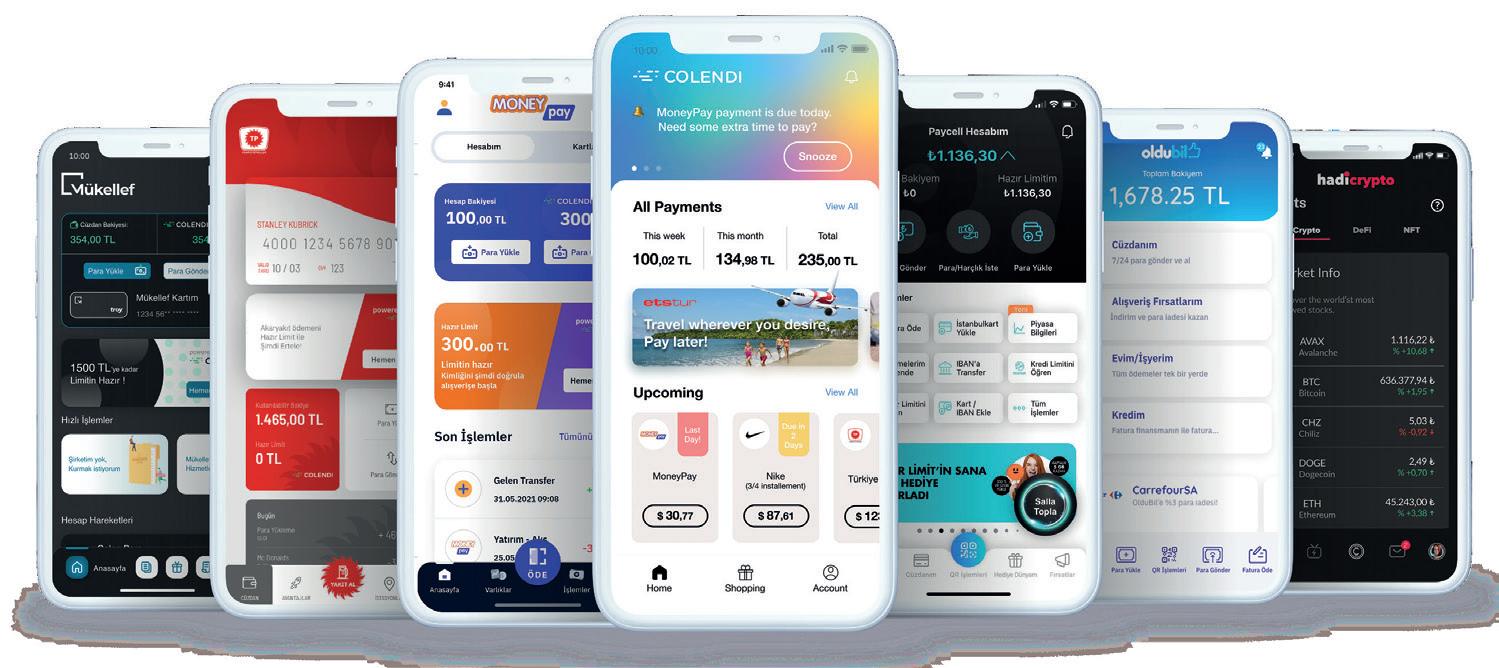

COLENDI IS THE FUTURE OF FINANCE

Using a decentralised scoring engine and real-life data, Colendi is unlocking credit for millions and giving its partners access to a whole new customer base

Colendi is a multifunctional banking-as-a-service platform that democratises banking services for consumers, merchants, and financial institutions.

Its goal is two-fold: to overcome the limitations associated with legacy banking and to solve a chronic financial problem that directly affects more than three billion people who do not have bank accounts and

more than five billion people who cannot get loans.

Colendi enjoyed the highest Series A round investment in the Turkish fintech sector, raising US$38million in a round that valued the startup at US$158million. In only 12 months, its platform has been able to reach seven million unique customers, handling more than five million transactions.

Colendi develops services based on scoring algorithms, combining new-generation financial technology

16

solutions, artificial intelligence and big data. Together with its platform partners and strategic business allies, it provides fast and easy access to loans with a buy now, pay later (BNPL) model as well as other distinct financial services to millions of users.

Its decentralised scoring engine unlocks significant potential by using AI and big data to identify low-risk customers who were previously underserved by financial institutions. Its credit analysis system considers social data, mobile phone data, demographic data, bill payment data, merchant transactions, and other data points to make smart credit decisions, based on risk in real time. The Colendi agile credit scoring algorithm uses more than 3,500 data points to provide the most democratic credit scoring for individuals who cannot get loans through banks. Thus, Colendi creates equitable and unbiased financial passports for the underbanked, unbanked, and underserved population.

A PARTNERSHIP MENTALITY

Colendi has already formed partnerships with the largest companies in the telecommunication, retail, energy and petroleum sectors in Turkey. Leveraging the joint venture mentality, instead of a single revenue stream, Colendi creates win-win mechanisms with its partners to optimise its presence in the financial ecosystem and expand its influence in the financial world.

Using the Colendi scoring engine, its partners can assess risk and provide funding to customers via their own resources. It allows them to make accurate lending decisions, track the status of lending and payments, and gain access to customers that were previously excluded from financial products. The BNPL feature, meanwhile, enables merchants to capture potential lost sales by allowing customers to gain instant credit at the checkout. This way, instead of downsizing their baskets, customers can use their credit to finalise their shopping and pay at a future date.

Partners can plug their existing financial

products directly into the Colendi platform and reach a large audience at a fraction of the typical acquisition cost and at a lower risk of default. Its embedded finance model matches consumers with financial products at the point of need in a less competitive environment, eliminating the need for search and evaluation.

In six quarters, Colendi has achieved a customer acquisition cost of $1.00, compared to a traditional retail banking acquisition cost of $350-1,500 – even better than the leading global fintech companies.

In a comparatively short period, Colendi has not only substantially built its user base and transaction flow, but it has also become a member of ACCIS (the global responsible data management organisation) and commissioned an active investor programme. An intense rollout of five new products and two new commissioned platforms, brought Colendi’s potential database to 111 million addressable customers in 2021. It continues to use

Turkey as the base from which to grow towards two billion end users, but it is also looking to expand to new countries and increase the size of its presence in the UK. Moreover, it aims to widen its already well-established joint venture partnership ecosystem, which grows exponentially.

Looking to the future, Colendi believes that settlement between customers, banks, and institutions will be part of decentralised finance (DeFi) and regenerative finance (ReFi) .

Colendi Co-Founder and Global CEO Bülent Tekmen says: “In today’s world, most companies, even those that have nothing to do with financial services, have changed the way they service their customers: they have begun to use alternative financial services as a means of staying competitive. In the recent past, the options for these services were limited and costly. We are aware of the need for alternative financial services and products along with privacy and security of data. So, Colendi offers a unique and frictionless integration of financial tools and services to any platform.”

He adds: “We believe that every company will be a fintech company in the not-too-distant future.”

WHO WE ARE AT A GLANCE

Colendi’s goal is to solve a chronic financial problem that directly affects more than three billion people who do not have bank accounts and more than five billion people who cannot get loans, using its multifunctional banking-as-a-service platform to overcome the limitations associated with legacy banking. Colendi develops unique services based on the Colendi Decentralised Scoring Engine and Colendi Protocol, using artificial intelligence and big data to provide bank-free risk assessments. Its scoring engine unlocks significant potential by identifying low-risk customers previously underserved by financial institutions. Together with its platform partners and strategic business allies, Colendi then provides millions of users with fast and easy access to loans, including buy now, pay later, as well as other distinct financial services.

COMPANY:

WHAT WE DO

The gateway to financial freedom

www.thepower50.com THEFINTECHPOWER50 17 COLENDI

Colendi FOUNDED: 2018 CATEGORY: Risk scoring KEY PERSONNEL: Co-founders Bülent Tekmen and Mihriban Ersin Tekmen HEAD OFFICE: UK OFFICES IN: Turkey EMAIL: info@colendi.com WEBSITE: colendi.com LINKEDIN: linkedin.com/ company/colendi/ TWITTER: @ColendiApp

Colendi creates equitable and unbiased financial passports for the underbanked, unbanked, and underserved

SALT EDGE

What’s the difference between the present world and the one from a quarter of a century ago? It’s the way things function.

Most processes are digitised and data is produced in quantities bigger than ever. With open banking regulations, the access to this data became the free pass to an infinite number of success stories. These stories will keep on growing, as long as data is properly handled.

And here comes the big challenge: it is literally impossible for humans to process so much information, so we turn to artificial intelligence (AI) with its machine learning (ML) capabilities to build up the era where almost everything becomes possible.

AI and ML are witnessing growing popularity among visionary businesses. According to a Dentons survey, published at the beginning of 2022, AI is already implemented by 12 per cent of big and medium enterprises, with another 48 per cent testing it.

But there’s still a big gap to be filled by the businesses that haven’t yet experienced the beauty of operations being improved with the help of AI and ML, so here are some ideas of potential use cases to explore in this direction:

1 Estimating life-time value (LTV)

A customer’s life-time value is a popular indicator of the profitability a business might get out of its interaction with customers. This is an important metric, since it allows creating and maintaining beneficial relationships with clients, thus increasing the profitability and growth of the company. Using the

available data on current profitable clients, a company can create several lookalike profiles and target the people falling under the criteria through various means. A clear picture on each client segment helps it focus its resources in a targeted, well-calculated manner, and this is where data science steps in.

There is a huge amount of available information, like a detailed overview of existing and lost clients, the products they use and the extent to which they use them, alongside other demographic and market indicators. Translating all that into straightforward insights, retrieved through secure APIs and analysed by AI and ML-based solutions like Salt Edge’s Financial Insights tool, comes in handy for institutions to understand what their customers want, and how they can fulfil their needs, thus successfully increasing their LTV.

2 Identifying fraud Machine-learning algorithms play an important role in identifying and preventing fraud in various areas, especially in the banking sector, including credit card usage, accounting, insurance, and others. Security is one of the most important aspects of financial services that banks pay attention to and the sooner they identify a fraud, the sooner they can limit the access to a bank account and minimise losses.

One of the most frequent applications of data science in fraud detection is the case when there are more transactions performed than usual and the bank’s system suspends them until the account owner confirms that it is them who

THE WIND IN YOUR SAILS

Automated data processing, and AI in particular, can propel a business across the commercial seas. Salt Edge is ready to help get them on board

initiated the transactions. The phases implemented by banks in fraud prevention with ML’s help are:

2 Evaluating the behavioural models

2 Testing the identified models

2 Preparing and adjusting the data sets by unifying, clustering predicting, and classifying them

Performing these steps with the help of AI and ML has managed to increase fraud prevention by 59 per cent in the banks implementing these systems.

»There’s still a big gap to be filled by the businesses that haven’t yet experienced the beauty of operations being improved with the help of AI and ML

THEFINTECHPOWER50 www.thepower50.com18

3 Risk modelling for investment banks

Using AI in this context is a top priority, as it helps regulate financial activities and determine the rates for bank’s financial instruments.

With investment banking estimating a companies’ value in order to create the corporate finance capital, facilitate mergers and acquisitions, and investment scopes, banks and data experts found themselves in a state of uncertainty due to the dispersed huge amounts of data. To level-up their internal decision-making process, banks needed more automation, more forward-looking predictions, and faster conclusions. According to financial executives who have already begun solving these problems with AI and ML, their credit risk profiling accuracy has improved by 45 per cent.

EMBRACE AND ADAPT

We are writing history and the ship will soon set sail. It’s best to make the most out of this moment and start leveraging the technological progress in your business, whether it is a

bank or other financial institution. The data already exists internally, in your customer relationship management (CRM), for example, and externally, in data management platforms (DMPs). Here is how you can make it workharder for you:

2 First make sure you are collecting it 2 Segment your audience and data, based on criteria relevant to your business. It’s better to automate this process as it will shorten the time necessary for analysing and understanding the data. There are great services available for that, including Salt Edge Data Enrichment services. This phase is usually based on analytical showcases, built on various techniques, like neural networks or linear regression

WHO WE ARE

We are a financial API platform providing PSD2 (revised Payment Services Directive) and open banking solutions for lenders, accounting companies, banks, and other institutions across the globe. There are two main vectors of activity: enabling third parties to get access to thousands of bank APIs via a unified gateway; and developing the technology necessary for banks to become compliant with PSD2 requirements. ISO 27001-certified and an account information service provider (AISP), licensed under PSD2, the company employs the highest international security measures to ensure stable and reliable connections between financial institutions and their customers. It is integrated with more than 5,000 financial institutions in more than 50 countries.

2 Once the models are built, it is necessary to integrate them in a regulated process, to automate it.

Considering ever-changing internal and external factors, these models’ quality should constantly be tested and updated as necessary

Efficiency is the key factor to reaching success: the sooner a business masters the new technologies, the more benefits it will see and the better-positioned it will be, compared to the competition.

We are transitioning from open banking to open finance, with the final target being open data. Data is essential for all sectors. So, the best time to start working with it is now.

AT A GLANCE

COMPANY: Salt Edge

FOUNDED: 2013

CATEGORY: Open banking

KEY PERSONNEL: Vasile Valcov, CCO (right)

HEAD OFFICE: Ontario, Canada

OFFICES IN: UK, Italy, Romania and Moldova

TEL: +1 437 886 3969

WEBSITE: saltedge.com/

LINKEDIN: linkedin.com/ company/salt-edge/ TWITTER: @saltedge

WHAT WE DO Open banking for every business

THEFINTECHPOWER50www.thepower50.com 19

EVERYONE IS SOMEONE

How global identity verification puts financial services on a fast track to success

In a world where customers seek competitive digital solutions, the pillars of success are rapidly changing for financial institutions and fintech operators.

Between frictionless onboarding, evolving compliance regulations, and ambitious growth plans, they feel the pressure to provide services with the ease and convenience customers expect.

A study by Deloitte has already shown that 38 per cent of new customers will abandon the account creation process if they find that onboarding takes too long or is overly involved. Meanwhile, in that same study, 26 per cent of customers reported that ‘easy enrolment and login’ are essential criteria for deciding who to do business with.

As competition grows fierce, financial service operators must look for ways to keep up with – or, better yet, outperform – the rest of the market. Those prioritising innovative and competitive consumer technology will have the upper hand. Partnering with a global identity verification solution can easily achieve this.

GAIN A COMPETITIVE EDGE

As business operations in nearly every industry shift to grow their digital solutions, this increase in demand reinforces the need for a trusted, secure

and agile digital identity ecosystem. By leveraging a global identity verification solution, financial service operators will be better positioned to delight customers through ease of onboarding, remain compliant with regulatory requirements and expand into new markets. Let’s take a closer look at how this is done.

1

Deliver a quick and seamless customer onboarding experience

Did you know Gartner predicts that, by 2023, 75 per cent of organisations will be using a single vendor with strong identity orchestration capabilities and connections to many other third parties for identity proofing and affirmation? This is up from less than 15 per cent in 2021.

Why does this matter when it comes to attracting new customers? Given that businesses need seamless and secure onboarding with minimal friction, your identity verification process is often the difference between success and failure.

Financial service operators can benefit from a customer onboarding experience that balances security and speed with a global identity verification solution. Fast and automated identity verification processes allow for quicker onboarding with risk-based workflows that let organisations apply the right amount of friction, based on business needs and customer profiles.

By delivering a quick and seamless onboarding process, financial service operators can provide customers with a frictionless experience that increases customer confidence and trust while also building their organisation’s reputation.

2 Effortlessly maintain regulatory and compliance requirements

Financial service operators need to create a smooth account opening process that satisfies anti-money laundering (AML), know your customer (KYC) and know your business (KYB) regulations – and this is where a global identity verification solution can shine.

Backed by the flexibility to adapt to changing regulatory requirements quickly and easily, financial service operators can ensure they are first to market with new products and services while simultaneously minimising risk.

Meanwhile, having good compliance processes can make it far easier to enter new markets in a fast and seamless way, rather than being held up by regulatory bodies and red tape.

3 Overcome global challenges and transcend borders

Unfortunately, many businesses fail to realise the additional verification challenges when venturing into unfamiliar markets. From region-specific data-handling best practices to finding reliable localised data sources that meet ISO security standards and more, organisations can easily find themselves scrambling to find appropriate solutions to address overlooked barriers.

However, a solution like Trulioo GlobalGateway is equipped to address these variances, more effectively helping financial service operators scale their compliance programmes when expanding into new markets. By working with a company that scales alongside you, financial service

THEFINTECHPOWER50 www.thepower50.com20 TRULIOO

operators can avoid the growing pains of international expansion.

Backed by more than 400 data sources and the ability to provide verification in countries with traditionally hard-to-match fields, Trulioo has the experience in multiple markets and multiple countries to get businesses where they need to go.

ARE YOU READY TO ACCELERATE YOUR SUCCESS?

Achieving frictionless onboarding while maintaining compliance regulations and advancing ambitious growth plans was something many financial institutions and fintech operators have, historically, agonised over achieving.

But, by embracing change through innovative customer-centric and agile technology, they no longer need to be held back by antiquated or legacy technology. Rather than being bogged down by slow, manual processes, global identity verification holds the key to accelerated success.

No matter the size of your business, where you’re located or where you’re looking to go, Trulioo has the customisability to get you there.

To find out how your business can begin leveraging an identity verification platform that’s built for change, visit the Trulioo website today.

WHO WE ARE

Trulioo is a leading global identity verification company, building trust online so that businesses and consumers can transact safely and securely.

Trulioo provides real-time verification of five billion consumers and 330 million business entities worldwide – all through a single API integration. Organisations rely on its identity verification platform, GlobalGateway, to help meet their business and compliance requirements and automate due diligence and fraud prevention workflows.

The Trulioo mission is to help provide every person on the planet with a digital identity to enable access to basic financial services and support.

AT A GLANCE

COMPANY: Trulioo

FOUNDED: 2011

CATEGORY: IDV

KEY PERSONNEL: Steve Munford, CEO (right)

HEAD OFFICE: Canada

OFFICES IN: United States, Ireland, Denmark and Romania

TEL: (+1) 888 773 0179

EMAIL: sales@trulioo.com

WEBSITE: trulioo.com

LINKEDIN: linkedin.com/ company/trulioo

TWITTER: @trulioo

THEFINTECHPOWER50www.thepower50.com 21

WHAT WE DO Global identity verification

THE PLUG-IN FOR SWITCHED-ON BUSINESSES

The opening up of banking has placed embedded finance on the front pages, due to its potential to transform how people and businesses alike consume financial services.

But making embedded finance a reality is often far from straightforward for businesses that want to use it.

It’s the reason why, at Weavr, we launched our embedded finance solution, called Plug-and-Play Finance. Our mission is to make it simple, easy and cost-effective for any business to offer any financial service, wherever their customers need it.

Our ultimate aim is to create economic opportunities for the majority of digital businesses that have struggled with the complexity, and corresponding heavy lifting, associated with using current banking-as-a-service (BaaS) offerings.

In doing so, we have been lucky enough to partner with innovative businesses such as Ben, an employee benefits programme, and Troc Circle, an invoice-netting platform, to enrich their offerings with financial services that

their customers value and move their own businesses forward.

Many companies are reassessing their relationship with financial services and the opportunities they unlock for growth. They come to us with the key question ‘how can embedded finance directly benefit my business?’. Our answer is that, ultimately, any digital business stands to benefit from embedded finance, which is why it’s important they understand it.

WHAT IS EMBEDDED FINANCE?

In looking to explore the concept, it’s important to start by establishing the

possibilities. At its core, embedded finance enables businesses to integrate financial services into their digital applications without needing to become a fintech to do so.

Embedded finance reduces the build effort and, in some cases, removes the significant compliance burden associated with offering financial services through BaaS. Once embedded, digital applications can offer richer solutions and experiences for customers that add to the bottom line. Importantly, it strengthens innovative businesses’ chances of becoming vital everyday services that customers love and rely on.

WHY IS IT IMPORTANT?

Giants like Uber and Deliveroo would not be able to offer their seamless customer experiences without the financial services embedded within them. Hail an Uber or order a takeaway and the payment takes place seamlessly in the background. These kinds of businesses have introduced new

THEFINTECHPOWER50 www.thepower50.com22 WEAVR

BaaS isn’t always the most convenient or cost-efficient way for a business to access embedded finance. So, Weavr offers them something different...

concepts to society such as ‘on-demand’ services that make our lives easier, save people time and money, and offer companies higher lifetime value from their customers. Likewise, they offer innovative businesses new sectors to disrupt with fresh technology offerings that are powered by embedded finance.

WHAT ARE THE BENEFITS?

Bringing financial services into an experience makes it richer for the customer, leads to greater engagement and stickiness, and opens up new revenue opportunities. Embedded finance providers like Weavr typically reduce the need for build work, which shortens the launch timeline and resource required to achieve it.

Businesses have enough to worry about without financial compliance, regulation and data security. So, some providers, including Weavr, do that for them.

More than anything, embedded finance positions businesses to gain a competitive advantage within their respective fields. It is more than a strategic opportunity – it is an imperative for any digital business wishing to keep its edge sharp.

IS IT TIME TO MOVE PAST BaaS?

BaaS providers still don’t make it easy enough for businesses to incorporate financial services into their digital applications.

Banks have tried to make inroads into offering embedded finance solutions. However, progress has been hindered by legacy infrastructure and layers of technology that still underpin most banking operations. The result can be seen in solutions that are inflexible and place a huge burden on the businesses that look to embed a bank’s services.

While embedded finance offers the solutions of BaaS, it does so without the time investment required when working with banks, the compliance burden that a business might have to take on, and the cost of implementing banks’ solutions.

WHY WORK WITH WEAVR?

We are the next generation of embedded finance. We have built Financial Plug-ins

that are pre-designed sets of financial services, tailored to common use cases that require payments infrastructure.

These include B2B supplier payments, expense management systems, freelancer platforms and more.

Our solution is highly flexible – we have ready-made Financial Plug-ins or we can build new ones to bespoke requirements in under an hour.

experience by turning usage insights around spending patterns into new product enhancements.

Through what we call Plug-and-Play Finance, Weavr radically increases speed to market for the mainstream of digital businesses by reducing the heavy-lifting experienced with other traditional BaaS offerings.

THE TIME FOR CHANGE IS NOW!

By working with Weavr, companies can not only efficiently embed financial solutions to improve customer experience and build revenue, but they can also keep the entire transactional process within their brand experience, rather than sending customers outside, e.g. to log in to a bank account at a vital point in the journey. That opens up the possibility to further improve customer

Weavr exists to democratise access to financial services by bringing together the worlds of finance and digital. By disrupting the current BaaS model and offering a simpler and more cost-effective way to embed finance, we empower entrepreneurs to deliver relevant financial services as an integral part of their digital applications.

While the power of embedded finance technologies and their ability to connect people with financial services in the digital world is limitless, the solutions must be simple to gain mainstream adoption. Weavr’s ambition is to deliver that simplicity through Plug-and-Play Finance.

WHO WE ARE AT A GLANCE

Weavr is the next generation of embedded finance for the digital economy.

We’re on a mission to enable any business to offer any financial service, anywhere their customers need it. We do that by providing everything to integrate those services seamlessly into a business’s mobile app or software-as-a-service (SaaS) application, safely, smoothly, and without the usual compliance burden.

Innovative businesses of all sizes and across diverse industries use Weavr to access a suite of ready-made Financial Plug-ins with in-built compliance.

With Weavr, businesses’ customers are empowered to collect, store and spend money, all in the context of their digital application. These applications, and the financial services integrated within them, are shaping the future of work, healthcare, education, real estate, and many other sectors.

COMPANY: Weavr

FOUNDED: 2018

CATEGORY: Embedded finance

KEY PERSONNEL: Alex Mifsud, Co-founder & CEO (right)

HEAD OFFICE: UK OFFICES IN: Malta

EMAIL: sales@weavr.io

WEBSITE: weavr.io

LINKEDIN: linkedin.com/company/ weavrpayments/

TWITTER: @WeavrPayments

WHAT WE DO

Frictionless Financial Plug-ins for innovators

www.thepower50.com THEFINTECHPOWER50 23

Embedded finance is more than a strategic opportunity – it’s an imperative for any digital business wishing to keep its edge sharp

REBUNDLING COMES OF AGE IN B2B FINANCIAL SERVICES

Anders la Cour, CEO of Banking Circle Group, on the benefits that this collaborative trend is likely to deliver in the banking and payments space

With the advent of the revised Payment Services Directive (PSD2) and open banking, fintech businesses were empowered to tackle individual elements of the value chain in financial services.

They focussed on where they could do things differently from the incumbents in order to fix a specific problem or fill a gap. This led to an unbundling of banking services, as businesses and consumers accessed them from a wide range of providers rather than the one or two big banks with which they had always previously had a relationship.

Today, significantly boosted by COVID-inspired digital acceleration, financial institutions (FIs) are recognising the value of delivering not just one, but multiple solutions from a single online platform. By expanding their proposition and rebundling banking solutions, fintechs can solve more than one problem for their clients, enabling them to better serve their end customers. And, in collaboration with fintechs, banks can add value and expand their offering quickly and without investing in building new solutions in house.

ADDING VALUE

For B2B fintechs, a multi-solution platform is great for giving their clients customer ‘stickiness’, by addressing the complete lifecycle of financial services that an individual or business might

require. To achieve that, FIs need to offer a range of financial services that their clients’ customers want and need – as well as those they may not yet realise they need – without those providers dissipating their brand values or service mission. Rebundling of financial services achieves this, not only delivering competitive advantage but also elevating FIs’ value as a whole.

Recent research from McKinsey (Global Banking Annual Review 2021: The Great Divergence) found that capital markets are anticipating the gap between valuations of banking industry leaders and followers will widen significantly in the next two to three years. According to McKinsey, fintechs are pivoting their value propositions and staying on the right side of this divergence by either doubling down on key value propositions and core markets or diversifying and collaborating to

» The culture of collaboration born in 2020 is inspiring a new ecosystem approach to deliver financial services for a marketplace that can’t afford for slow or high-cost processes to hold it back

build a platform of curated, rebundled services. Generally, they are working with a licensed partner who can deliver the regulated financial services needed.

Players of all sizes are rebundling financial services, creating platform businesses for growth through curated services rather than products, enabling them to expand into emerging and untapped industries. According to Hogan Lovells, this consolidation of financial services is predicted to increase still further in the coming months as businesses seek to deliver a wider range of solutions to an ever-growing customer base.

A number of high-profile acquisitions underline the value that rebundling is expected to deliver. For example, Visa has made several acquisitions in the last 12 months, including Tink, the open banking platform that enables financial institutions, fintechs and merchants to build financial products and services and move money; Earthport to expand its real-time payments network; and CurrencyCloud to provide foreign exchange solutions for cross-border payments. Buy now, pay later giant, Klarna, bought German payments

THEFINTECHPOWER50 www.thepower50.com24 BANKING CIRCLE GROUP

fintech, Stocard, enabling it to add the app for bundling multiple bank cards as well as deliver discount deals from a network of merchants. Rapyd acquired Icelandic payments solution company Valitor to extend its in-store and online payments acceptance solutions as well as card issuing for merchants.

And in November 2021 UK-based Paysafe, the leading specialised payments platform, acquired German fintech,

viafintech, to add digital banking apps that enable consumers to make deposits or withdraw cash from their digital bank accounts at a nearby retail store, using a barcode.

PAYMENTS OF THE FUTURE

The culture of collaboration born in 2020 and maturing in 2022 is inspiring a new ecosystem approach to deliver financial services that are fit for purpose for a marketplace that can’t afford for slow or high-cost processes to hold it back. The financial ecosystem is coming of age. And that’s where Banking Circle comes in. As a next-generation financial technology platform for global commerce, we enable payment companies, banks, global marketplaces and online merchants to accelerate the digitisation of their customer and supply chain interactions with a suite of modern financial solutions. By accessing multiple solutions from a single ecosystem, FIs will not only be able to respond more rapidly to market opportunities, gaining a ‘first-to-market’ position, but they will also see significant cost savings as well as that all-crucial customer ‘stickiness’.

WHO WE ARE AT A GLANCE

Banking Circle Group is a next-generation financial technology platform for global commerce.

It enables payment companies, banks, marketplaces and online merchants to accelerate the digitisation of their customer and supply-chain interactions with modern financial solutions.

At the centre of the Banking Circle ecosystem sits licensed bank, Banking Circle S.A., offering global cross-border payments, accounts and liquidity management through a global hub for real-time clearing and settlement with direct API access.

Banking Circle was launched to help banks, payments businesses and fintechs deliver a service to their business customers so they can transact globally

and more efficiently, without having to build their own infrastructure. It does this by connecting to the payment rails across all key geographies and jurisdictions, supported by a Cloudbased infrastructure, to provide direct access to clearing in multiple countries. Unconstrained by the legacy issues of correspondent banks, Banking Circle is providing a modern payment solution, enabling financial institutions to get as close to the clearing as possible. And that means the transaction will be faster and more cost-effective.

Based on McKinsey analysis of the size of the global B2C e-commerce space, it is estimated that Banking Circle now settles six per cent of the world’s B2C e-commerce flow and €100billion of the point-of-sale B2B e-commerce flow.

COMPANY: Banking Circle Group

CATEGORY: Technology platform for commerce

KEY PERSONNEL: Anders la Cour, Chief Executive Officer (right)

HEAD OFFICE: Luxembourg OFFICES IN: UK, Denmark, Germany and The Netherlands

EMAIL: info@bankingcircle.com

WEBSITE: bankingcircle.com

LINKEDIN: linkedin.com/ company/bankingcircle

TWITTER: @bankingcircle

www.thepower50.com THEFINTECHPOWER50 25

WHAT

WE DO Financial infrastructure you can bank on

HARD TIMES MASSIVE OPPORTUNITIES

2022 is shaping up to be the year of the Big Fintech Sale. So, go buy yourself a piece of the future, says Chris Skinner

2022 is proving to be a challenging year – harder than anything we have seen since the pandemic began.

Markets are tightening, funding is harder to find and, for the first time, many fintech startups are experiencing a recession. If you’ve never been through one, what does this mean for your business and the future of our industry?

First things first, a recession means that everything becomes hard… unless you are cash rich. There are some who are still feeling flush and, if you’re one of them, then I expect you are prospecting. Many fintech startups – bear in mind there are more than 26,000 of them – have great ideas, strong vision, passionate leadership. But, if they don’t have funding, then their runway is leading to a cliff-top. That’s a great moment for a cash-rich competitor to step in and buy cheap. As they always say, when everyone is buying, sell; if everyone is selling, buy.

Second, we are seeing fintechs struggling, laying off staff, cutting back on excess. It’s a good time for management and leadership to learn new lessons. These are not new lessons for those of us who have been around the block, though. They are lessons that we learn every few years. When asked what’s a recession?

Jamie Dimon, chair and CEO of J.P. Morgan, said ‘something that happens around every seven years’. Nevertheless, this is a big one and, for all the newbies

out there, my only advice is to make sure you have liquidity and funding. Without that, the predators will circle.

Third, there are, actually, some fintechs who have seen a recession before. Remember 2008? Several fintechs were around for the Great Financial Crisis and are still here now. Ask them how they coped and learn from their experiences.

Finally, the fact is that there is still a bubbling and explosive market here, that is vibrant and cool. We are going to get through this, because we can.

I was struck by a comment that Cristina Junqueira, cofounder of NuBank – now the biggest challenger bank success in the world with almost 50 million customers – made when it started out. She said: “If banks are Darth Vader, credit cards are the Death Star.” Back in 2015, Nubank could not get a bank licence from regulators. So, it launched a credit card that charged a quarter of the fees that banks charged, in what was then a barricaded marketplace. Its approach blew that market open and now Nubank is worth more than most banks in South America.

This experience generally holds true for most successful fintech unicorns, due to the networked world we live in today. This does not mean that old banks die and new banks take over, but it does mean massive change. For old banks, the challenge is to create a

business that exists as though it was born digital; for new banks, the challenge is to have a business born digital that has traction.

My guess is the outcome of all this will be that new banks and old banks will acquire and merge over the next decade – as markets tighten, predators bite. Don’t be surprised if, before 2030, one of the new banks acquires an old bank. In fact, some already have (Lending Club/Radius Bank, FNZ/ Fondsdepot Bank, etc). Equally, don’t be surprised if fintechs merge or banks buy fintechs, as some already have (Tink/FinTecSystems, Truist/Long Game, Goldman Sachs/ NextCapital, J.P. Morgan/Global Shares).

Although we may be living through hard times, there are still huge opportunities out there. So, for those who can buy, buy now, as there are lots of firms that are being forced to sell. And, whether buying or selling, remember that tomorrow is the only thing we can change. You cannot change yesterday. So, look upwards, stride onwards and be the change you want to see. Did someone ever say that?

AT A GLANCE

Chris Skinner is an independent commentaror on the financial markets and fintech, author and the voice behind the Finanser.com blog. His most recent book, Digital For Good, looks at how technology and finance can work together to address the big environmental and social issues of our time and make a better world. Chris is chair of Nordic Future Innovation, a non-executive director of the challenger consultancy firm 11:FS and on the advisory boards of many fintech and financial firms.

WEBSITE: chrisskinner.global

TWITTER: @Chris_Skinner

THEFINTECHPOWER50 www.thepower50.com26 CHRIS SKINNNER

A Cornerstone Advisors’ survey of financial institutions found that 11 per cent of banks already have a banking as a service (BaaS) strategy, eight per cent are in the process of developing one, and 20 per cent are considering it.

Why the interest? Growth opportunities. On average, banks that currently offer BaaS have six partners and support nearly 1.3 million account holders. Overall, a sponsor bank supporting one million consumer accounts and 300,000 commercial accounts could generate more than $40million in revenue annually – roughly $15 per consumer account and $71 per commercial account.

Industry-wide, Cornerstone estimates that the BaaS market could grow to more than $25billion in annual revenue in 2026. This would go a long way to replacing the inevitable loss of overdraft fees that the banking industry will face over the next five years.

EMBEDDED FINTECH JUMP-STARTS NPD

Banks can protect and grow their core products – e.g. payments and loans – by finding new distribution opportunities through embedded finance, which is the integration of financial services by non-financial actors, principally e-commerce. That might prove a difficult road, however, for mid-size financial institutions that find themselves shut out of those deals by retail platforms that partner exclusively with large banks. Instead, they can create new revenue streams from new products and services already created by fintech startups – a strategy called embedded fintech. There is often confusion between