28 minute read

Australia - ASX

1

INTRODUCTION

Recently climate change has significantly affected the Australian economy. The floods have pushed up fruit and vegetable prices, which, according to Climate Council economist, Nicki Hutley, has cost Australia millions of dollars. The supply disruptions in Australia have evidently resulted in rampant price increases, with fruit and vegetable prices rising 6.7%.

Further, Australia is experiencing an economic crisis where we have seen significantly inflated prices. The Central Bank’s choice to increase the cash rate has been a reaction to mitigate the destructive consequences of inflation, with expectations to hit 2.6%. Hitting the 2.6% will be reflective of Australia’s economic contraction of 1.5%.

China’s imposition of tariffs on Australian agricultural products has significantly led to the economic loss of farmers. This has been demonstrated by the 80.5% tariff on Australian malt barley in 2020. Australian barley growers have consequently revealed their loss of $35 per tonne having to sell their quality malt barley to other markets as livestock feed. Since China is a major buyer of Australian mart barley, this demonstrates the reduced global buyers of Australian commodities.

Additionally, Australia’s dependence on China has strained their economic growth. China’s strict focus on fulfilling their COVID-zero strategy has been inefficient for their economy, as the continual lockdowns have impacted businesses and supply chains. Nicholas Burns (United States Ambassador to China) stated that the “zero-Covid policy…has had a major impact” on businesses, with reference to how the financial hub, Shanghai was also forced to lockdown. This had a huge effect upon Australia’s economy where supply chain disruptions have weakened demand for resources like iron ore.

EQUITIES

In the financial year 2022, high and rising inflation accompanied by the prospect of aggressive monetary tightening weakened the performance of Australian equities, with the All Ordinaries index and S&P/ASX 200 both falling by around 10%. Despite considerable volatility brought on by persistent supply chain disruptions and Russia’s invasion of Ukraine, the S&P/ASX 200 has recently recorded its fourth weekly rise as market expectations for rate hikes come off.

However, with inflation not expected to peak until later this year, market sentiment has largely been driven by questions about how much further the RBA will have to increase interest rates. One the one hand, Westpac are forecasting a peak cash rate of 3.35%, warning that inflation would get out of control if the Reserve Bank fails to keep hiking rates. On the other hand, CBA warns that if the cash rate exceeds 3% the risk of house prices crashing rises alongside the risk of a recession as households are put under increased financial strain.

It has long been said that when the United States sneezes, the world catches the cold. While CommSec predicts that the Australian share market will rebound by 79% over the financial year 2023, sharemarket volatility will likely continue alongside global recession fears as Australian shares track Wall Street.

COMMODITIES

With Australia’s iron ore export earnings worth $133 billion in 2021–22, Australia is the largest iron ore producer in the world. Despite a volatile 2021, iron ore prices remained relatively stable in the recent June quarter, averaging US$130 a tonne following a rebound from lows of US$80 a tonne in November 2021. Since then, prices have been more volatile, falling from over US$140 in early June to a little over US$100 in mid-July. Although prices have recently reversed course to the upside ($US111 a tonne), several headwinds impede a sustained iron ore recovery. Notably, given China accounts for 69% of the world’s iron ore imports, price recovery is dependent on Chinese steel demand, which may be weak amid lockdowns, an emerging property crisis and heightened geopolitical tensions. Additionally, significant downside risk for prices may be the prospect of new supply, with Australian export volumes alone expected to rise by 53 million tonnes to 929 million tonnes by 2023–24.

Australia’s metallurgical (steel-making) and thermal coal export earnings have risen strongly in the past six months as global supply disruptions intensify. Indeed, coal prices reached historic highs earlier in the year as the Russian invasion of Ukraine acted as a supply shock to an already tight market. Although metallurgical coal prices have been particularly volatile, ranging from US$198-$439 a tonne in the past financial year, prices are expected to fall by almost half to around US$240 a tonne by 2024 as supply conditions normalise. Similarly, as climate-related and pandemic disruptions ease, Goldman Sachs anticipate that thermal coal prices will fall from an average of US$212 per tonne in 2022 to US$110 a tonne in 2024. Given China plans for rapid decarbonisation and energy independence, Chinese demand for Australian coal is likely significantly lower in the medium-term even if Beijing reverses its current ban on Australian coal imports.

Throughout 2022, the Australian bond market has seen a large surge in bond yields, in response to the expectations of the RBA’s aggressive rate hikes to combat high inflation. This steep pace of OCR increases, amounting to a 175 basis point increase to 1.85% (September 2022) over 4 months, has not been experienced by the Australian debt market since 1994. However, the larger effect of this change on the Australian economy and specifically the bond market is still likely to result in the following months.

Since the start of 2022, yields for 10y Australian Government bonds have risen to 3.44% from about 1.74%. Treasuries continue to rise with expectations now being held that central banks around the world will take a more dovish approach to inflation, in fears of sparking a recession. However, there is still contention about cash rate expectations in Australia, with AMP’s Chief Economist Shane Oliver expecting the cash rate to peak at 2.6% within the next 12 months, whilst noting that a 3% forecast is too high. On the other hand, bond markets have been placing the benchmark rate at 3.2% by Christmas, reaching a peak of 3.6% by next Easter.

In Australia, as seen in the graph below, bond markets have experienced a tighter spread between short and long-dated ACGB yields, hence resulting in a flatter yield curve. This serves as an indication of the market’s expectation of rate hikes in the near term, as well as the loss in confidence of growth following these hikes, particularly with looming recession sentiment. With an inverted US yield curve, the deepest inversion since 2000, this has historically served as a reliable predictor for recessions.

Looking forward, buying opportunities for bonds have emerged for investors who expect increasing bond prices and contracting yields, as bonds have been oversold. Notably, the AOFM have recently issued and plan to continue to issue approximately $125bn of Treasury Bonds throughout 2022-23. Further, assuming the RBA is successful in effectively lowering and managing inflation in 2022-23, this shows strong promise for the Australian debt market, given the fact that bonds tend to outperform equities during recessionary periods, as they are viewed as ‘risk-free’ or safe haven assets. The corporate bond market has also been attracting attention given its elevated spreads, with NAB senior debt yielding 4.1% and BOQ AAA rated covered bonds yielding 5.1%.

As a result of the RBA’s lag to raise rates relative to the Fed, the AUD has subsequently weakened against the USD. This was most notable in April, when the AUD/USD fell 5.6% from its year-to-date peak of 75c, its biggest monthly loss in over 2 years. This was a result of the Fed’s 25bps rate hike in mid-March, whilst the RBA continued to maintain its near-zero cash rate of 0.1%. This continues to be the story for the Aussie, despite the RBA’s decision to make four consecutive rate hikes, due to the Fed having aggressively made 75bps increases as they now sit at 2.5%. The AUD has further been weighed down by the Chinese real estate sector crisis, and due to the Australia-China tariff wars. Nonetheless, since the start of 2022, the Aussie has strengthened against the Euro, GBP and Yen.

However, with the looming threat of recession and forecasts of diminishing commodity prices and demand for Australian exports, the AUD will no longer be able to be held up by trade surpluses, and thus it is likely to underperform against safe-haven currencies like USD and JPY. Notably, ANZ Research foresees that Australia’s biggest trading partner, China, seeks to limit their reliance on coal imports, and thus their steel output is expected to weaken this year.

As Australia is inextricably tied to the current geopolitical tensions of the world, there are many prominent risks associated with this market. The Russian Ukraine war set the stage for record inflationary numbers across the world, with Australia’s CPI of 6.2% at its highest since 1990. With these numbers showing no signs of slowing down, continued rate hikes pressure consumer confidence, risking a housing downturn. Despite lowered signs of consumer confidence, labor force participation and unemployment rates are at record levels. The combination of a 50-year low of 3.5% unemployment and job vacancies trending up, places great pressure on businesses that are already struggling to find workers. Should this declining trend continue, Australia faces the risk of a labor shortage in the next few months.

Our bilateral relationship with China risks taking a turn for the worse, with China’s zero COVID-19 policy constraining economic activity in the manufacturing and services sector. Whilst lockdowns have loosened in recent months, our strategic relationship risks further straining with China-US tension escalating due to Nancy Pelosi’s diplomatic visits to Taiwan. Should our relationship with China worsen, it will be detrimental to migration, service and commodity exports.

2

INTRODUCTION

The Japanese Economy is likely to face a number of economic issues in the coming year as a result of domestic and global forces.

In comparison to Europe and the US reaching inflation levels of 8%, Japan’s CPI is only up 2.5% year over year in April. However, inflationary pressures are likely to surge in the coming months due to pent-up demand as covid restrictions are eased which will create demand-pull inflation.

Additionally, weakness in the Yen is contributing to increased import prices which could present a potential challenge for the Japanese Economy in the near future. This inflation is outstripping gains in wage growth, which could catalyse the economic issue of subdued longer-term consumption.

Additionally, the Japanese economy has already experienced negative growth in the early part of the year with real GDP falling an annualised -0.5% in Q1. This has been influenced by the trade imbalance created by modest growth in Japan's nominal exports of 15.3% in Q1 compared to imports which were 32.3% higher than the year earlier. This has been caused by weakened Chinese demand for Japanese exports, Japan’s top export market, because of lockdowns and the struggling property sector.

Additionally, strong import growth was driven by successful vaccination campaigns, whereby medical product imports more than doubled on a year-ago basis in February in Japan. Although, it is worth noting that pent-up demand has already risen and is likely to propagate moderate GDP growth forecasted to be 1.7% in 2022, and 1.8% in 2023. However, economic growth in the US and Europe is slowing, with the risk of recession emerging, creating a risk for Japanese exporters as some of their major export markets reduce their demand.

FX

The Japanese Yen has been extremely volatile in the past months as it fell more than 6%, from 139.18 yen on July 14th to 130.40 yen on August the 2nd. This came after the surge in the currency by 21% between March and July.

This volatility came about after the uncertainties of the Russian invasion on Ukraine, which inflated oil and other energy sources. Japan, as a net importer of oil, saw devastating impacts as Brent crude futures rose to $US140 a barrel. Japan's trade deficit for the first half of this year totaled nearly 8 trillion yen. This caused higher uncertainty for Japan and its currency, leading to larger depreciation of Yen.

Furthermore, as a result of the Russian-Ukraine War, the disrupted supply chain led to greater levels of inflation worldwide. To combat this, global monetary policies saw a tightening trend, with a central focus and speculation on the U.S. monetary policy. So far, the U.S. Federal Reserve has raised short term rates from zero to 1.5% and expected to increase to 3.5% by the end of the year. However, Japan’s cash rate remains committed to monetary easing and keeps the interest rate at -0.1%. The widening gap of the cash rate has caused greater depreciation of the Japanese Yen.

EQUITIES

The Japanese Stock Market is heavily influenced by the movements of Wall Street. As large company earnings are prepared to be released, there are great speculations on how inflation is impacting these businesses. Major indexes like S&P 500 fell 1.15% while Nasdaq Composite lost 2.26% as a result of these speculations. This impact is carried onto JPX, where the Nikkei 225 Index declined 1.77% and major technology stocks like SoftBank Group and Fanuc lost 4.28% and 4.54% respectively.

However, upbeat corporate earnings reports have helped JPX to recover, with Nikkei share average closing up 0.87%. This is the highest it has been since June 9th, 2022. Sentiment on Friday was lifted by a rally in Taiwanese stocks, with the TAIEX index climbing 2.27%, and gains in U.S. stock futures, said a market participant at a domestic asset management firm.

FIXED INCOME

The BoJ has reiterated its short-term interest rate of -0.1%, and its 10-year bond yield target of 0%, a global outlier compared to the hawkish central bank environment which has seen record amounts of monetary tightening in the face of high economic uncertainty and soaring inflation. The BoJ has kept its forward guidance on both short and long-term interest rates in a bid to combat economic uncertainty and encourage economic activity, and has continued its quantitative easing program through the purchasing of 10-year JGB bonds at 0.25%. Following a global debt rally, foreign investors purchased a record amount of long-term Japanese bonds in July, net buyers of ¥5.06tn (US$37.4b), reversing a net sale of ¥4.1tn in June.

COMMODITIES

“Japan’s largest commodity exports include refined petroleum ($9.76b), hot-rolled iron ($8.35b), Gold ($7.29b), flat-rolled steel ($4.79b) and refined copper ($4.13b). Japan is the 2nd largest iron and steel exporter, following China who dominates the market, exporting to over 190 different countries.

Japan’s largest commodity imports include crude petroleum ($72.3b), coal briquettes ($21.9 b), petroleum gas ($19.3b), refined petroleum ($16.5b) and copper ore ($9.19b). Japan is the 5th largest importer of goods in the world, and is the 2nd largest copper importer globally. As such, the JPX offers a robust market with ample opportunities for international organisations.

RISKS

WHY IS JP VULNERABLE?

Following nearly a century of strong economic growth, the start of the 1990s marked the time when the asset bubble of Japan burst and the stock market, to this day, has not fully recovered. Prime Minister Shinzo Abe’s ‘Abenomics’ involved efforts to make exports more attractive and boost inflation by increasing government spending to stimulate demand and consumption, introducing structural reforms to make the country’s companies and labour force more competitive. However, Japan still maintains the highest national debt-to-GDP ratio in the world at 228% and a relatively stagnant GDP growth over the past decade, growing by an average of 1% a year since 2013.

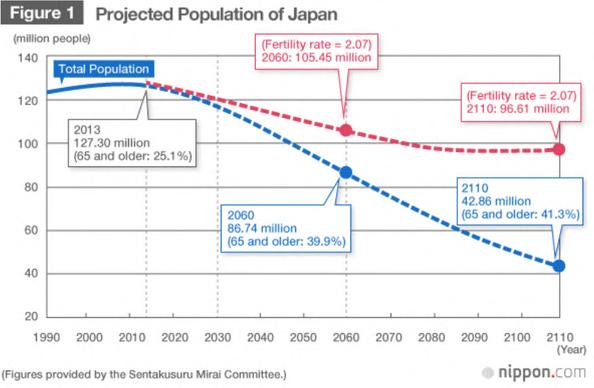

Meanwhile, its demographics faces the risk of an ageing population with a ⅓ of its residents over 60 years old, with plummeting birth rates, the population is estimated to reduce by 25% by 2050. Many risks as a result of this include increasing the need for government spending health care, products and services, and pensions. The rapidly reducing workforce leads to decreasing capacity in the labour power (total number of eligible workers aged 15 and older) of the country as well as lower income tax yields in a stagnating middle class bracket. The workforce, which measured 65.77 million in 2013, is projected to drop 42% by 2060 to 37.95 million. Despite efforts by governments to fight population decline, boost fertility rate through decreasing employment hours and maternity leave reforms, it is unable to avoid a hyper-aged society with low birth rates and 30% of Japanese consumers over the age of 65.

“This also explains the very gradual movement away from cash. In 2021, cashless payments only accounted for around 35% of private final consumption expenditure. Rather, businesses lost 1 trillion yen per year due to slower payment systems and less effective tax collection. This mentality is also largely prominent in corporations and their leaders who prefer to hoard cash and earn no return with interest, investing in employees, built upon the tenet of lifetime employment.

The Bank of Japan (BOJ) does not establish a ‘target inflation rate’, instead a ‘price stability target’ which aims to keep prices of domestic goods and services stable/consistent. Further, the lack of specific schedule of BOJ announcements heightens short-term exchange rate volatility, with yen valuations dramatically changing.

Japan faces the dilemma that a weak yen is bad for inflation but a strong one is undesirable for the stock market. The nation often welcomes a weaker currency as it makes exports more appealing, yet a hyper-inflation market in current economic climate, the cheaper currency makes imports more expensive. The BOJ has confronted the depreciation of its own currency with efforts to drive up stimulus aimed at keeping the 10-year JGB at its target.

Japanese stocks are often negatively viewed by investors due to concerns over trade tensions on the rise, especially with major powers US and China. Suffering from the USChina trade war, both countries take a total of 20% of Japan exports, Japanese companies have relied on China’s relatively cheap assembly lines, having moved away from being the intermediary of production pathways. BlackRock and UBS have both viewed the performance of Japanese equities as largely associated with updates in trade and geopolitical stability.

3

INTRODUCTION

In Q2 of CY22, the Chinese economy experienced negative GDP growth for the first time since 2019. This decline surprised market expectations as it predicted -1.5% instead of the materialised -2.6% growth. Without a doubt the 2 month lockdown across the economic powerstation (Shanghai) has severely influenced this quarterly decline. Partial lockdowns in other Chinese cities including the capital (Beijing) and the tech hub (ShenZhen), have also placed downward pressure on household consumption, declining -3.5% in March, with consumer confidence plunging and remaining below pre-Covid levels.

Despite this, labour market data still remains strong with a decline in the unemployment rate from 5.9% to 5.5% in June, in line with central bank targets. It must be noted that long term impacts of employment may destabilise as the consequence of heavy restrictions catch up coupled with the Evergrande’s property crisis.

Moreover, resurgent US-China tensions have been brought to light once again, increasing political uncertainty in the region, as Nancy Pelosi’s recent diplomatic visit to Taiwan was met with air combat exercises and missile displays from the Chinese military. Renewed pressure from the World Health Organisation for a probe into the initial Wuhan outbreak, combined with China’s refusal to condemn Russia’s invasion of Ukraine have increased international scrutiny on China.

ASSET CLASSES

EQUITIES

The Shanghai Stock Exchange has seen a 2.26% decrease in SSE Composite over the past week, indicating low performance within the stock market. However, on July 28th, the ChinaSwitzerland Stock Connect was launched. This allowed for SSE-listed companies to issue new shares on the SIX Swiss Exchange. The first 4 companies were able to successfully raise USD 1.6 billion from their investors through this corporation. The launch of this will catalyse sharing of market resources and potentially attract investors into the SSE market, assisting Chinese businesses to raise capital on the stock market. Further, due to the sustained lockdowns in Shanghai, it has prompted large uncertainty within the Shanghai Stock Market, causing large levels of capital flight from its foreign investors. China’s capital flows are seen to decrease significantly, amounting to a capital and financial account deficit of 892.4 USD in the first quarter of 2022, decreasing approximately 178.4% from the last quarter of 2021. Chinese stocks slumped 6% in April while the latest monthly flows data showed foreigners withdrew a net $17.5 billion from local shares and bonds in March. This caused further implications for currencies and government bonds, addressed later.

COMMODITIES

Demand for metals will rise in general following COVID in 2019 and 2020. Furthermore, the general outlook for the manufacturing industry looks positive. However, the recent collapse of Evergrande signifies a slowing property market in China, which can potentially cap overall metal demand. Regardless, metals are very dependent on the Chinese government’s implementation of zero-covid policy and measures to boost steel-intensive activities such as housing construction.

Secondly, China’s industrial sector accounted for two thirds of the country’s total consumption of energy, with manufacturing practices in particular utilising a large amount of coal. As of 2020, coal usage has reached 56.8% of China’s total energy use. Yet, China declared ahead of the 2021 UN Climate Change conference their intentions to bring non-fossil fuels in primary energy consumption to 25% and increase capacity of wind and solar power. This signifies growing attention towards renewable energy, thus reduction in demand for non-renewable sources such as coal.

It is also known that China is the biggest producer of rice (30% of global output). According to ITC Trademap, China’s exportation of rice reached approximately 1,196,781.0 metric ton in 2016, then subsequently increased to 2,304,487.0 metric ton in 2020. Due to the growing demand for fresh rice, the government is exporting its old stock at very low rates to Middle Eastern and African countries. Thus, the continuous high production of rice in the region is very likely to increase export quantity further.

FOREIGN EXCHANGE

In lieu of China’s Covid Zero policy, the lockdown in Shanghai caused the city’s foreign currency trades to drop by 30% since March. According to the State Administration of Foreign Exchange, Beijing had the most currency deals in April, placing Shanghai as second among 35 other Chinese provinces and municipalities (see graph). As such, for the first time, Shanghai has lost its title as the top currency trading hub, casting profound impacts on Shanghai’s economy.

The published data reflected the impact of lockdowns on the Chinese economy. It has been found that bank settlement and sales reduced by 30% from March to $61.8 million, forming 15% of the national tally in comparison to the share of approximately 20% prior to the lockdown in 2019.

he delays in corporate foreign exchange demand potentially limited liquidity and therefore reduced trade volumes. However, a senior Chinese Strategist at ANZ, Zhaopeng Xing, reassures that despite the slower process of making foreign exchange purchases, the total amount of dividend payout stays relatively constant.

FIXED INCOME

Further, the onshore yuan in April was seen as the greatest monthly loss since China unified its exchange market 28 years ago. This was due the accelerated outflows from the Chinese national markets and an increasing monetary policy gap with the United States as a result of concerns regarding the strike of Covid. Consequently, the volume of daily average dollar-yuan trading in the market declined by around $5 billion from January to March.

RISK

While the Covid lockdown in Shanghai has now ceased, the onset of the pandemic remains a prevalent issue that pressures financial markets. For example, there has been a significant decline in stock market prices, and this can potentially affect the entire Chinese market should there be further outbreaks in consideration of China’s covid zero policy. As of the outbreak of Covid-19, the risk of a stock market crash became much larger than usual as there were 6 days with a single-day crash of at least 2% in early 2020.

In addition, China as a highly populated country relies on imports from other countries. However, the reduced foreign exchange rates caused a drop in value of Chinese yuan, hence the increasing price of imports and consumer price index. As a result, Chinese consumers tend to make less purchases which poses the risk of hindered growth of China’s GDP.

4

INTRODUCTION

Hong Kong is known as an international financial hub, its economy is characterised by low tax rates, free trade and limited government interference. Its free-enterprise system, which is independent of the communistic structure of China, means that the region has its own policies related to money, finance, trade, customs and foreign exchange. Hong Kong’s stock market attracts more overseas investors, as it has multiple advantages such as a registration-based IPO system for faster and easier listing; greater international exposure for global expansion; stable financial infrastructure; effective regulatory framework.

However, as a special administrative region (SAR) of China, it is still ultimately influenced by the policies of the mainland. The impacts of these were clearly evident throughout the pandemic. Hong Kong employed its zero-covid strategy from the very beginning of the pandemic in 2020 and did well in taking preventative measures to prevent cases and deaths.

Further, strict coronavirus-prevention rules of Beijing’s sustained “zero-covid” policy have been a source of uncertainty for the international business community. It has heavily damaged its travel and service-based economy. Nearly half of European companies are considering leaving Hong Kong this year, according to the local European Chamber of Commerce. The city’s unemployment rate from February to April hit a 12-month high of 5.4%, with the pandemic and sustained lockdowns as the main cause. However, Hong Kong recently announced that it will ease Covid hotel quarantine requirements for people arriving from overseas to 3 days only, with additional 4 days of ‘medical surveillance’ at home or any hotel with limited movement allowed. As the rest of the world opens up, the city's insistence on maintaining strict travel restrictions, which have put the economy under severe strain, has been increasingly criticised. The Hong Kong handover turns 25 this year, reaching a critical halfway point, as Hong Kong will officially become a part of China in 2047. Following the mass unrest of Hong Kong’s protesters in July of 2019, 3 years on, the after-effects of the pro-democracy movement including a Beijing-imposed national security law and sweeping electoral changes have permanently reshaped the city. On June 30th 2022, President Xi Jinping took his first trip outside of mainland China since the pandemic to HK to participate in the ceremony to celebrate the anniversary. It is evident that Hong Kong and Beijing authorities no longer view democratic participation, fundamental freedoms, and independent media as part of this vision.

The Russian-Ukraine conflict has increased volatility - outlook 2022: high volumes Slowdowns in IPO activity HK$331.4B raised (2021), existing good environment and pipeline support the system to maintain these volumes however, the volatility of the overall market and a fragile geopolitical environment have decreased interest and investor confidence.

ASSET CLASSES

The Hong Kong exchange is host to the same typical array of asset classes as we find in Australia, with equities, fixed income and derivatives dominating the majority share of the market.

Hong Kong listed equities have had a rough year. Many of the similar trends of inflation, economic slowdown and general tough business conditions as we see in the USA and Australia have occured in Hong Kong, however this has been coupled with the rapid heighting of tensions between China and the Western world. This was amplified with the Russian invasion of Ukraine and the rapid and harsh reaction of the US, EU and ANZ regions, as China is an ally of Russia. Any connection between China and Russia in helping with the war would prompt a rapid withdrawal of funds, and a very sharp decrease in the market. In the three days following the Russian invasion of Ukraine, the Hang Seng fell approximately 20%. These significant withdrawals of Western funds have compounded economic issues alongside an economically restrictive covid-zero government policy in order to result in a -23% return for the Hang Seng index over the past 12 months. This compares to the ASX200, which returned -7% over this same time.

Derivatives followed a similarly volatile period, given that over 90% of derivatives on the Hong Kong market are either equity index options or stock options. Although equity turnover volume has been significantly lower through 2022 as a result of the withdrawal of funds, derivate volumes have remained robust, with a relatively unchanged profile as compared to the start of 2021.

After the collapse of major property developer Evergrande, the weakened property sector has led to a significant increase in the volatility and yield of most property-based Hong Kong listed bonds. Combined with the volatile inflation market, the government de-leveraging policy whilst trying to manage to not sink the country into a recession, and also maintain covid-zero, the fixed income space in general has seen considerable volatility in recent times. However, many market commentators now see many fixed income products as priced unrealistically bearish with relation to rate hikes and market risks, so despite the dire circumstances through 2021 and the start of 2022, there is potential for upside opportunity.

RISKS

Economists forecast Hong Kong to fall into its second recession within three years, with predictions revealing Hong Kong’s economy could contract for the third time in four years. These bleak forecasts come as a result of Hong Kong’s strict adoption of Beijing’s ‘Zero-COVID’ regime, whilst a slump in trade, surging interest rates and imminent geopolitical tensions threaten economic growth, with Fitch Ratings Inc. revising its annual growth forecast to -0.5% in 2022 down from their early April forecast of 1.0%.

Hong Kong is one of the last in the world to still be enforcing strict COVID restrictions and regulations, most notably the enforced hotel quarantine for incoming travellers. Economists critique that such a stringent regime has resulted in the deterioration of Hong Kong’s status as a commercial hub whilst most certainly slowing economic activity, as locals and expatriates leave and cross-border travel to the mainland has been cut off, severely harming Hong Kong’s trade and overall growth. This prediction is only reinforced by the recent wave of COVID that significantly reduces the chances of the border reopening with China.

Early August saw a much-anticipated decision by the government to loosen mandatory quarantine requirements, from seven days quarantine to three, in hopes of restoring its status as an economic hub and improving the economy. Despite this ease in restrictions that will likely lighten the burden for international travellers, economists note that it will do very little to change the current foreboding forecast, indicating that the government would have to do much more to offset this risk and encourage the return of tourists and businesses.

In addition to the COVID challenges, Hong Kong has had to grapple with rising interest rates. The US Federal Reserve has hiked interest rates several times this year to counteract inflation, forcing Hong Kong to follow the same to maintain the local dollar’s peg to the US dollar.