wicpa.org/events.

wicpa.org/events.

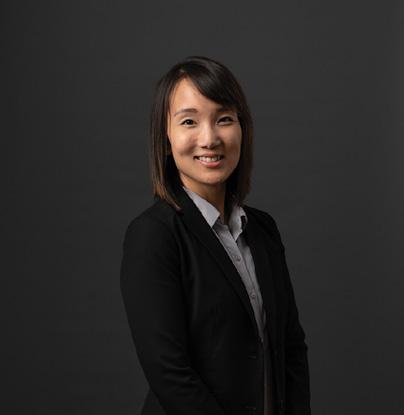

6 The unusual journey of Amanda Hein, CPA

Despite unusual obstacles and a long pathway to CPA, Mandy Hein is truly living her dream as a shareholder of a CPA firm and co-owner of a bison farm.

By Marcia Tillett-Zinzow and Mandy Hein, CPA

10 The cliffs of “more” … taxes?

Many of the changes made by the 2017 Tax Cuts & Jobs Act were not permanent and will unwind next year. Find out what the landscape will look like.

By James D. Brandenburg, CPA, MST

14 Employee or independent contractor?

Getting the answer right is critical because worker misclassification is a hot button for federal enforcement agencies, and penalties can be steep.

By Erica A. Storm, JD

18 Accounting for diversity, equity and inclusion

DEI is about identifying root causes of disparities and working to ensure we are fully tapping into the potential of our very deep talent pool.

By Dan Nash, CPA

22 LEADERSHIP

Managing offshore teams

Many people think offshoring and outsourcing are one and the same. They are not. Read about what makes offshoring different and beneficial.

By Prashant Kothari, CA, CPA, CISA

28 TECHNOLOGY

The future of assurance services in the age of AI

Dive into the fun and fascinating world of auditing’s tech transformation, covering everything from data integration to AIdriven document wizardry and more.

By

Jordan Boehm, CPA, and Rick Krueger, CPA

32 PRACTICE MANAGEMENT

Minding your mid-careerists: Slowing the exodus of experienced talent

It’s a problem. What can CPA firms do to prevent mid-career CPAs — those at the peak of their productive years — from following retirees out the door?

By Teri Saylor

36 HUMAN RESOURCES

Happy employees = happy clients: Strategies to boost happiness

Satisfied employees are more likely to deliver exceptional service, increasing client satisfaction and loyalty.

By Eileen Monesson, CPC, MBA

On Balance is published five times a year by the Wisconsin Institute of Certified Public Accountants (WICPA). Change of address should be sent to: Membership, W233N2080 Ridgeview Pkwy, Suite 201, Waukesha, WI 53188; Phone: 262-785-0445 or 800-772-6939; Fax: 262-785-0838; email: comments@wicpa.org. Statements and opinions expressed are those of the authors and not necessarily those of the WICPA. Publication of an advertisement does not constitute an endorsement of the product or service by On Balance or the WICPA. Articles may be reproduced with permission. © Copyright 2024 On Balance

Chair

Ryan J. Hanson, CPA, CGMA

Chair-elect

Stacy A. Stinson, CPA, MBA

Past Chair

Matthew J. Schaefer, CPA, CGMA

Secretary/Treasurer

Lucien A. Beaudry, CPA, JD

Directors

Christopher M. Cholka, CPA, CGMA

Printing Special Editions 2024-2025

Michael Donahue, CPA

Jessica B. Gatzke, CPA, MST

Tori M. Morrow, CPA, CGMA, MBA

Donna R. Scaffidi, CPA

AICPA Council

Ruth A. Kallio-Mielke, CPA

Neil R. Keller, CPA/ABV

President & CEO

Tammy J. Hofstede

Design & Layout

Brett Stallman

Advertising

Editor

Marcia Tillett-Zinzow

CPACharge is trusted by accounting industry professionals nationwide and provides a simple and secure online payment solution developed specifically for CPAs, offering an affordable way to accept credit, debit and eCheck payments in the office or online, with no equipment or swipe required.

SkillBench helps accounting firms, CFOs and controllers with offshore staffing solutions for accounting, finance, audit, tax and payroll needs. With 25+ years of experience, we help you save over 70% on costs, bridge your talent gap and save you time to focus on practice growth.

Spectrum Investment Advisors cosponsors the annual Retirement Plan Investment Seminar, which offers WICPA members CPE credits at a nominal cost. WICPA members can work directly with Spectrum to receive plan consulting services for their retirement plan program as well as individual wealth/asset management services.

“I am confident that as each of us contributes to the partnership, each of us as members will yield more benefits.”

By Ryan J. Hanson, CPA, CGMA

As we approach fall in Wisconsin, many of us have already started the back-to-school routine. In our family, we have geared up our daughter for her junior year in high school and guided our son off to his first year of college. As we navigate the journey our son has chosen to pursue, I reflect on our changing relationship dynamics, and I sum it up as a partnership. Together, we are guiding him in the career he has chosen — removing roadblocks, providing guidance and explaining options. We are each bringing forth our own abilities and efforts in the interest of a common goal. Effectively, we are partnering on our son’s career journey.

As I reflect on my own career, I think of all those I have been fortunate to call partners, knowing I would not have experienced the same level of achievement without them. I can certainly think of my family and my professional network as partners. Yet one entity I can clearly point to as a career-long partner is the WICPA.

The WICPA supports careers by advocating for and promoting our profession as well as by providing a multitude of development opportunities. We generally do not receive these benefits in our day-to-day roles, yet our development is critical to advancing our careers.

The WICPA brings to the partnership advocacy, networking and development opportunities. In terms of advocacy, the WICPA remains ingrained with our legislative partners to help ensure proposed legislation considers the importance to our profession, to taxpayers and to the public. Beyond legislatively, the WICPA advocates by promoting the profession to the next generation of CPAs. Through networking, the WICPA offers a forum to gather, share information and collaborate. Networking at membership banquets, conferences and social events offers significant opportunities to promote and advance your career and business as well as to teach and learn from each other.

The development opportunities the WICPA offers are immense, ranging from technical education to developing leadership acumen or presentation skills. The WICPA offers opportunities such as leading a conference, learning about public

policy, or participating in business decisions on the Finance Committee. There are opportunities to develop governance expertise serving on the WICPA or Educational Foundation board of directors. In addition to leadership, there are many opportunities to develop and refine presentation skills by presenting at conferences, speaking with legislators or simply networking with other professionals.

These are only a fraction of the ways in which the WICPA is a true and valuable partner in each of our career journeys. Yet as with any successful partnership, the success is the result of each member’s efforts. As partners, we too must give to the partnership. I am confident that as each of us contributes to the partnership, each of us as members will yield more benefits.

We must be engaged and participate in and support the partnership. We can do so in several ways:

• by paying our membership dues so the WICPA can continue advocating for the profession

• by donating to the Educational Foundation so it can continue to promote the profession and the benefits of an accounting career, with the goal of building up the CPA pipeline

• by donating to the legislative PAC so the WICPA can continue its significant legislative efforts

• by participating in as many networking events and as often as possible to ensure other attendees know you by name

• by taking advantage of the development opportunities by attending conferences, speaking at conferences, leading a committee of interest to you or joining a board

Ultimately, I encourage all of you to strengthen your engagement with the WICPA — so you can give and receive the benefits of partnership.

Ryan J. Hanson, CPA, CGMA, is senior vice president and chief financial officer for Pekin Insurance and the WICPA’s 2024-2025 board of directors chair. Contact him at 309-478-2746 or rjhanson@pekininsurance.com.

“It is important that as a profession we continue to have a licensing and regulatory structure and that, at the same time, we recognize the need to continue to evolve and adapt with the current demographic and professional shift.”

This topic is not just complicated; it’s really complicated.

Much about the CPA pipeline has been written and spoken, including possible solutions and creative suggestions. The calls for a response to enact change within the accounting profession continue to grow. This topic is heavily discussed not just among our board of directors but also nationally at AICPA and NASBA meetings as well as state CPA society CEO meetings. We’ve continued to struggle with the pipeline, and we spend a significant amount of time discussing 120 vs. 150 hours of education for licensure.

The demand for CPA services is at an all-time high. There is too much work for too few people, affecting the ability to serve clients, businesses, nonprofits and the public interest. Small businesses and nonprofits have difficulty finding firms to assist them with needed services due to staffing shortages or fees out of their range. Baby boomers are retiring, and the number of new and potential licensees entering the profession is not keeping up at the same pace.

This is not anything new. It has been years in the making, resulting from declines in U.S. birth rates, fewer high school graduates going to college, and a decrease in the number of accounting graduates — with fewer of them pursuing the CPA.

Salaries, work culture, image and perceptions of the profession also have contributed to the decline. We know many firms and organizations continue to make changes in these areas, and the WICPA continues to promote accounting awareness, endless opportunities and positive perceptions to students, educators and the public.

The bigger discussion is that many attribute the shortage to the 150-hour requirement for licensure, which has been in place for over two decades. This requirement is one of the

CPA mobility to practice across jurisdictions without additional

We have heard from our members and others nationally that more than one pathway to licensure is needed, even if mobility is impacted for a period of time. You may have heard some of these ideas, such as an “Experience, Learn and Earn” model; a complex, competency-based program; or 120 hours of education with two years of experience. These and several other alternate pathways are being evaluated.

We know that several other states are working on legislation to create alternate pathways. To add to the complexity, some states are piloting 90-credit bachelor’s degrees, so referencing 120 hours will no longer be applicable; and some of the ideas may put more work on state licensing boards, resulting in further delays and complications with licenses.

Where does this leave us in Wisconsin?

We continue to be vigilant and engaged in what is developing. We know that whatever happens, legislative changes will be coming. The WICPA will be evaluating the multiple changes — and when we propose legislation, we do it once, and we do it correctly. We will include all scenarios for future mobility and, in the meantime, have guidance in place for the disruption to the mobility that will surely occur. As we are connected to 53 other jurisdictions, we know some will move more quickly than others. State CPA societies are working together to provide model language that will work and to ensure that substantial equivalency and mobility are minimally impacted during any transition.

We understand the talent pipeline is a challenge, and there are many pieces to consider in making the profession more attractive. It is important that as a profession we continue to have a licensing and regulatory structure and that, at the same time, we recognize the need to continue to evolve and adapt with the current demographic and professional shift.

Tammy J. Hofstede is president & CEO of the WICPA. Contact her at 262-785-0445 ext. 4518 or tammy@wicpa.org.

On August 20, the federal district court for the Northern District of Texas struck down the Federal Trade Commission’s ban on noncompete agreements, which was set to take effect on September 4. The court had previously granted relief from the FTC rule only for the plaintiffs in Ryan LLC v. Federal Trade Commission. However, the new ruling provides that the FTC cannot enforce the rule against any employer in the country, and the rule will not go into effect as scheduled. The FTC is expected to appeal the ruling, and the resulting litigation could delay a final answer on the rule’s validity for months or years. For now, employers have a reprieve from having to comply with the rule. Please keep in mind that noncompetition agreements are still subject to existing state laws, which are not affected by the court’s ruling. Learn more at www.vonbriesen.com.

The Finance Committee of the WICPA Board has reviewed and approved the WICPA audited financial statements for the fiscal year ended April 30, 2024.

The WICPA Educational Foundation Board has reviewed and approved the audited WICPA Educational Foundation financial statements for the fiscal year ended April 30, 2024.

Members may request a copy of the audited financial statements by contacting WICPA president & CEO Tammy Hofstede at 262-785-0445 ext. 4518 or tammy@wicpa.org.

By Marcia Tillett-Zinzow and Mandy Hein, CPA

Amanda “Mandy” Hein, CPA, a shareholder with Northland CPAs in Rhinelander and an adjunct instructor at Nicolet College, takes seriously her responsibility to uphold the professional and ethical standards of being a trusted advisor. She considers her CPA credential a badge of honor, which she wears with pride.

“It represents the hard work and determination that took years of study and experience in the field to achieve,” she said.

That is a statement that all CPAs should appreciate and honor. But Hein’s credential required a little more time and effort than for many others. She discovered accounting in a most unexpected way, and her journey to CPA was stunted by one huge obstacle most people don’t encounter.

Mandy is the oldest of four sisters. “The greatest gift I received from my parents is my sisters — they are my best friends,” Hein said. All four sisters have remained in the area. Her sister Jesse Shepard (37) is a registered nurse; Becky Selig (35) works in sales; and youngest sister Rachel Nelson (33) is a social worker for Oneida County. “We were close as kids, but our bond grew even stronger when I was faced with a life-threatening illness,” she said. At age 15, Mandy was diagnosed with ovarian cancer and given a less than 50% chance of survival. That year she also met the 17-year-old boy she would eventually marry — John Hein. “As young as I was, it was a pivotal year in my life,” she said.

“It’s very traumatic to go through surgeries, chemotherapy and multiple hospital stays, especially at such a young age — you’re just trying to hide the fact that there’s anything wrong with you and be a teenager.”

Photography by John Sibilski

“

The greatest gift I received from my parents is my sisters — they are my best friends.

Despite the obstacles, she not only continued taking traditional classes at Rhinelander High School but was also enrolled in college courses at Nicolet College.

“It was really nice to take college courses where nobody knew me, and I could try to be “normal,” she said. “Plus, it gave me a head start on my college education.”

In the midst of the cancer battle, her uncle stepped in and provided a welcome distraction. A small business owner himself, he hired Hein to work for his landscaping company.

“It started out with marketing-type projects: assisting with trade shows, identifying prospects, going out on jobs to take notes to help him prepare quotes,” Hein said. “Eventually, he introduced me to office work.”

And that’s when it started. Her uncle taught her how to manually prepare payroll and the quarterly payroll reports. She learned to process accounts payable, and he taught her how to job cost — also all manually at that time. When she took her first accounting class in high school, she was hooked. “I thought, ‘Wow, I really like this,’” she said.

In that class, she was introduced to QuickBooks, and she and her uncle started using it for invoicing. “I started using it more and more until I was doing all of his bookkeeping in QuickBooks, including his payroll, helping him prepare for tax time, doing job costing — it was really kind of a broad education at that point,” she said.

A strong will to live combined with many treatments — some experimental — resulted in the cancer’s remission. It wouldn’t be her last hurdle, though.

Hein enrolled at Nicolet College full time after high school and earned her associate degree in accounting in 2005. Prior to graduation, an instructor informed her about a local firm that was taking applications for a staff accountant position. She applied, fully anticipating it would not amount to anything — but she was wrong. She graduated from Nicolet in May, and in June she had a full-time job at Northland Accounting (now Northland CPAs).

“My boss and the company founder, Mike Hauser, was incredibly supportive of my aspirations to continue my education, so in September I re-enrolled at Nicolet. I started

taking courses I knew would transfer to a college where I could obtain my bachelor’s degree. With my passion for the accounting profession continuing to grow, I knew my ultimate goal was a to become a CPA. I worked to complete additional transfer credits and credits I knew would count toward my 150-credit-hour requirement for the CPA credential.”

With every well-laid plan come obstacles. Hein was about to encounter another. At 24 years old, Hein was once again diagnosed with cancer — this time, breast cancer. More surgeries, chemotherapy and working full time left no energy to continue education. Genetic testing revealed Hein had a rare genetic disorder, called Li Fraumeni Syndrome, that predisposed her to cancer. “The diagnosis has given me a greater appreciation for life,” Hein said. Thankfully, Hein achieved remission once again. “I’ve been cancer-free for the last 15 years. Hopefully, I’m done for good!” she said.

The cancer stretched out her CPA journey — to 10 years on the nose. She graduated with her bachelor’s degree in accounting in 2015 from Upper Iowa University, took the CPA Exam in 2017 (passing all four parts on the first try), and became licensed in 2018.

In 2019, Mandy and her two CPA partners, Ben Hauser and Matt Whalen, purchased Northland CPAs, and she was officially a shareholder — at a “mere” 34 years old.

“That was a surprise,” Hein said. “I had figured it all out very early: I knew who my husband was going to be; I knew where we were going to live; I knew what my profession was going to look like. The only thing I didn’t plan on … as much as I would have aspired to be a shareholder of a public accounting firm, I didn’t really see that one coming!”

“

I cannot express how important it is to me — and to our firm — to be an active and integral part of the community in which we live and serve.

Born and raised in a small town, Hein is committed to serving and giving back while putting her CPA credential to good use. Whether she is in the office as a trusted advisor to her clients, mentoring the next generation of accounting professionals, or teaching at the same community college where her journey started two decades ago, Hein is passionate about supporting her community and those individuals and businesses within. Mandy serves on the Nicolet College Accounting Advisory Committee and is the acting treasurer for the Rhinelander Area Food Panty in addition to donating her time and expertise to many other organizations.

“I cannot express how important it is to me — and to our firm — to be an active and integral part of the community in which we live and serve,” Hein said.

As a result of the firm’s commitment, Northland CPAs was the recipient of the WICPA’s 2024 Community Service Excellence Award.

Wouldn’t you know it — this successful CPA is also an owner of a bison farm! Her husband comes from a family of potato farmers in the Rhinelander area and manages the Sowinski Certified Seed Farm. John was committed to owning his own farm one day. The discussion began when they started dating in 2000 — but the nature of that farm would not be realized for some time.

“It was 16 years of discussions,” said Hein. “So many ideas! ‘We should have a deer farm,’ or ‘We should have a pheasant farm,’ or ‘We should raise dogs.’ We talked about a lot of different options, and then one day John said, ‘I’ve got it! We should have a bison farm!’ And I was kind of like, bison? Hmm ... I’m not sure about this.”

But John had done his research and convinced Mandy that a bison farm was a great idea. Bison are undomesticated, native and hardy animals. Significantly self-sustaining, they do not need shelter, immunizations or much assistance from humans, Mandy explained. “Just keep them fed and happy!” she said.

The couple worked out a business plan to determine exactly how the bison farm would come about, and in 2016, the first fence went up and they purchased their first bison.

“We started with four yearlings, knowing they weren’t going to breed for at least another year, and with a nine-month gestation period, they wouldn’t have babies for almost a year after that. We knew it was going to be a process, but we were

Mandy and John started naming their bison right away. The first four were named Little Girl, Big Mama, Ernie (because she — yes, she — was #3, like Dale Earnhardt’s car), and a breeder bull named Hannibull. Now they also have Long Beard, Crazy Eyes, Buster, Stormy, Sweetheart, Daisy, Sleeter, Weird Horns and Beavis, among others.

“You can tell which ones my husband named and which ones I named,” Hein laughed.

Despite the obstacles and the long pathway to CPA, Mandy is truly living her dream as a shareholder of a CPA

Is the comprehensive TCJA coming to an end?

By James D. Brandenburg, CPA, MST

One of the most significant tax bills in a generation may soon be coming to an end. The Tax Cuts and Jobs Act (TCJA) was signed into law in December 2017. It was a comprehensive piece of tax legislation that provided across-the-board tax cuts for businesses and individuals. It included some simplification but also many complications.

However, many of the changes made by the TCJA were not permanent, and these provisions will unwind next year and revert to the tax law in effect prior to the TCJA. This could result in tax hikes for many, and some have referred to this as going over the cliff. There will be much confusion and debate next year as Congress attempts to deal with the uncertainty. CPAs need to be out in front to help taxpayers navigate the coming choppy waters next year. This article will help you plan for the tax cliff coming next year by focusing on these main areas:

• Background of the TCJA

• Review of TCJA provisions that will sunset or expire next year as well as those that will remain in place

• What Congress might do to resolve this uncertainty

The TCJA ushered in $1.5 trillion in tax relief for individuals and businesses. The bill was passed by the Republicans using special “reconciliation” provision rules in Congress, and essentially closed Democrats out of the legislative process with this bill. There are certain budget requirements that must be followed when using reconciliation. With all the various tax items the Republicans wanted to include in the bill, some of these changes were not permanent but, instead, were scheduled for only a few years (five to 10 years in most cases). This was the best they felt they could produce at the time under the reconciliation rules, and they hoped that down the road they could enact further legislation to keep these changes in place. We have now moved “down the road” and hit a fork — will these tax cuts continue after 2025, will they expire, or will something else happen?

The TCJA was a comprehensive bill with many and various changes, some more significant than others. Here are some selected TCJA items that will expire or sunset as of Dec. 31, 2025:

• Individual income tax rates: The TCJA adopted tax brackets of 10%, 12%, 22%, 24%, 32%, 35% and 37%. These rates were cut from the pre-TCJA rates of 10%, 15%, 25%, 28%, 33%, 35% and 39.6%. The income amounts for these rates were also lowered by the TCJA.

• The 20% qualified business income deduction (QBI, or Section 199A): This special 20% deduction reduced the tax rate for certain businesses operating as S corporations, partnerships and sole proprietorships. While there were many complexities with QBI, TCJA lowered the effective tax rates on these noncorporate businesses and also cut the corporate tax rates (more to follow).

• Standard deduction: The TCJA nearly doubled the amount of the standard deduction from $12,700 to $24,000 for married couples and from $6,350 to $12,000 for single taxpayers. These amounts were indexed for inflation. This sizable jump in the standard deduction led many taxpayers since 2018 to claim the standard deduction instead of itemizing their deductions.

• Child tax credit: This credit was increased from $1,000 to $2,000, with a phase-out for taxpayers with higher incomes.

“

We have now moved “down the road” and hit a fork — will these tax cuts continue after 2025, will they expire, or will something else happen?

• Mortgage interest deduction: The home mortgage interest deduction has been available for many years, with some limitations. The TCJA cut back on this deduction by limiting the mortgage loan amount to $750,000 for married couples filing jointly, single filers and heads of households, and to $375,00 for married taxpayers filing separately. The TCJA also removed the deduction for home equity loans.

• SALT deduction cap: Prior to TCJA, taxpayers could deduct their real estate taxes and state income taxes (or sales taxes in some cases), and there was no limit on the deduction for these taxes. TCJA, however, implemented a deduction cap of $10,000 for state and local taxes (SALT).

• The 2% “miscellaneous” itemized deductions: Before TCJA, taxpayers could combine their miscellaneous deductions (investment expenses, union dues, unreimbursed business expenses and many others), and if these exceeded 2% of their adjusted gross income (AGI), the excess was deductible. The TCJA removed this deduction.

• Elimination of the “Pease adjustment”: Previously, there was an unusual adjustment that applied to middleand upper-income taxpayers: the Pease adjustment. These taxpayers would have to scale back their allowed itemized deductions by 3% — a tax deduction “haircut” of sorts. For those taxpayers in the top tax bracket, this caused their tax rate to be increased by 1.2%; thus, with the Pease adjustment, the top marginal tax rate of 39.6% was essentially increased to 40.8%.

• AMT exemption: One of the most significant TCJA changes impacting individual taxpayers involved the alternative minimum tax (AMT). The TCJA raised

the AMT exemption from $84,500 to $109,400 for married couples (and similar amounts for single taxpayers), and the point where the AMT exemption begins to be phased out was increased from $160,900 to $1,000,000. These two changes drastically reduced the number of taxpayers subject to AMT beginning in 2018. The alternative minimum tax could return with a vengeance if these AMT exemption provisions are allowed to sunset in 2025.

• Estate and gift tax exemption: TCJA change for families involved the estate/gift tax exemption. The TCJA doubled this exemption beginning in 2018 (it had been $5,490,000 in 2017). The estate/gift tax exemption continues to be indexed for inflation and now stands (in 2024) at $13,610,000 (or $27,220,000 for a married couple).

• International tax change (GILTI/FDII): the most significant of TCJA areas involved international tax changes. TCJA established “global intangible low-taxed income” (GILTI) and “foreignderived intangible income” (FDII) tax rates. These tax deductions are scheduled to be scaled back in 2026.

It is important to note that for each of the above items, the tax law in 2026 will revert to what the law was in 2017 prior to the enactment of the TCJA unless Congress steps in and makes changes. Taxpayers and practitioners alike need to refamiliarize themselves with what the tax rules were for these items back in 2017.

TCJA items (select) that are not scheduled to sunset in 2025

There are many TCJA items, however, that are “permanent” and will not expire as of Dec. 31, 2025. They are permanent in the sense that Congress would need to enact new laws to change their provisions. These items are not set to expire or sunset in 2026 or at any other time. Here is a selected list of TCJA items that are not set to expire as of Dec. 31, 2025:

• Corporate tax rates: The corporate tax rate had been at 34% (35% for larger corporations) prior to the TCJA, but was sharply cut to 21% by the TJCA beginning in 2018. The corporate tax rate has remained at 21% and is not scheduled to change at the end of December 2025.

• Bonus depreciation: Bonus depreciation has been around for many years. Pre-TCJA, bonus depreciation permitted businesses to deduct 50% of the cost of eligible assets in the first year they were purchased. The TCJA increased this to 100%. The 100% bonus depreciation, however, is already being

scaled back. As part of a special transition rule, the 100% depreciation was available only through Dec. 31, 2022 — it then dropped to 80% in 2023 and to 60% in 2024; it will drop to 40% in 2025, to 20% in 2026 and to 0% in 2027.

• Section 179 expensing: The Section 179 expensing provision has been available for many years to assist many small and mid-sized businesses. It allows certain property (generally, not real property) to be directly expensed, but there is a cap on overall additions a company can make in a year. Prior to the TCJA, up to $500,000 could be expensed, but this amount was phased out if total additions in the year exceeded $2,000,000. TCJA increased this amount to $1,000,000 with a phase-out beginning at $2,500,000. These amounts are indexed for inflation, so for the 2024 year, the Section 179 expensing limit stands at $1,220,000, and the phase-out threshold is at $3,050,000.

• Research expenditures: Research expenditures have been deductible by taxpayers for many years. The TCJA, however changed this and required research expenditures to instead be capitalized and amortized over five years beginning in 2022 (and fifteen years for foreign research). There has been ongoing legislative activity over the past several years to delay the effective date of this change, but this has not happened yet. Thus, research expenses since 2022 must be capitalized and amortized over five years.

• Interest expense deduction: One of the major business changes adopted by the TJCA related to the deduction for interest expense. Pre-TCJA, business interest expense was generally deductible by the business. TCJA changed this, and now the interest deduction is restricted to 30% of a business’s taxable income before the interest expense deduction — creating an amount referred to as “adjusted taxable income,” or ATI. Prior to 2022, depreciation and amortization deductions could be added back to increase ATI, but this is no longer available and has made deducting interest expense much more difficult.

• Entertainment deductions: Prior to TCJA, business meals and entertainment expenses were generally 50% deductible. TCJA, however, changed this beginning in 2018, and entertainment is no longer deductible, but meals remain 50% deductible.

As noted above, these provisions were not all of the numerous tax changes made by the TCJA. In 2025, Congress will need to address the items that are scheduled to sunset as of Dec. 31, 2025. What will they do? There are several possible routes they could take, but this depends in large part on what happens in the fall 2024 elections. There are various tax-planning strategies that could then be considered in 2025. This will be addressed in an upcoming issue of On Balance. Stay tuned . . .

Jim Brandenburg, CPA, MST, is a tax director with Sikich in Brookfield. Contact him at 262-754-9400 or jim.brandenburg@sikich.com.

Classifying

By Erica A. Storm, JD

Whether a worker is an employee or an independent contractor is an important threshold question for businesses. Getting the answer right is critical because worker misclassification is a hot button for federal enforcement agencies, and penalties can be steep.

Workers who qualify as employees are generally covered by various employment laws and entitled to the rights and protections provided by those laws. Employees also create additional obligations for employers, such as payroll taxes, workers’ compensation and unemployment insurance, and employee benefits.

By definition, independent contractors generally do not fall within the scope of the legal protections that apply to employees and are not eligible for employee benefits. They are also responsible for their own tax obligations.

Employers needing to determine whether a worker is an employee or independent contractor are often faced with a

“

Employers needing to determine whether a worker is an employee or independent contractor are often faced with a confusing array of tests, standards and factors that have to be evaluated in different situations.

confusing array of tests, standards and factors that have to be evaluated in different situations. The U.S. Department of Labor (DOL), IRS and National Labor Relations Board have their own tests for the laws they enforce, and state governments might have different requirements altogether. As the U.S. workforce has evolved — coupled with the increase in remote work, freelancing and the gig economy — the definitions can seem like a moving target.

Earlier this year, the DOL changed things for employers yet again when it issued a new final rule revising its guidance on how to analyze who is an employee (and who isn’t) for purposes of the Fair Labor Standards Act (FLSA). The FLSA provides employment protections such as minimum wage and overtime pay for covered employees. The final rule, which took effect on March 11, 2024, rescinded a version of the rule that was issued in 2021.

The final rule has been challenged by several lawsuits, but it is currently in effect. Depending on the outcome of the pending litigation, the standard could change yet again if a court agrees with the plaintiffs in any of these cases and strikes down the rule. And because different administrations have treated this issue differently, the future of the rule could also be affected by the results of the presidential election in November.

The 2024 final rule identifies six factors that may determine whether a worker is an employee or independent contractor for purposes of the FLSA. This is a change from the 2021 rule, which looked at five factors but gave two “core factors” greater weight in the analysis. Those core factors were 1) the nature and degree of control over the work and 2) the worker’s opportunity for profit or risk of loss.

The 2024 rule adopts an “economic realities” test, which looks at the totality of the circumstances in determining how a worker should be classified. Under this rule, no single factor (or factors) is automatically given more weight than the others.

The six factors to be considered under the 2024 rule are as follows:

Opportunity for profit or loss depending on managerial skill: This factor considers whether the worker has opportunities for profit or loss based on managerial skill, such as determining or negotiating the charge for the work; being able to accept or decline jobs and choose the order or time in which the jobs are performed; engaging in marketing or advertising to expand the business or secure work; and making decisions to hire others, purchase materials or equipment, and rent space.

Investments by the worker and the potential employer: Any investments by a worker that are capital or entrepreneurial in nature and comparable to the investments of the potential employer in its overall business indicate independent contractor status.

Degree of permanence of the work relationship: A worker is more likely to be an employee if the work relationship is indefinite, continuous or exclusive of work for other employers; and more likely to be an

“

The 2024 rule adopts an “economic realities” test, which looks at the totality of the circumstances in determining how a worker should be classified.

independent contractor if it is definite, nonexclusive, project-based or sporadic because the worker is exercising their own independent business initiative.

Nature and degree of control: This factor considers the potential employer’s ability to control the performance of the work and the economic aspects of the working relationship. Relevant facts include whether the potential employer sets the worker’s schedule, supervises the performance of the work, explicitly limits the worker’s ability to work for others, or is able to discipline the worker.

Extent to which the work performed is an integral part of the potential employer’s business: A worker is more likely to be an employee when the work they perform is critical, necessary or central to the potential employer’s principal business and more likely to be an independent contractor when the work they perform is not critical, necessary or central to the potential employer’s principal business.

Skill and initiative: This factor considers whether the worker uses specialized skills to perform the work and whether those skills contribute to business-like initiative.

The rule also provides that, depending on the circumstances, additional factors may be relevant in making this determination. The DOL did not identify specific additional factors that could be considered. Rather, this catch-all provision is intended to allow the consideration of any other relevant facts of a particular situation in light of whether they indicate economic dependence or independence, regardless of whether they fit within one of the specified factors. However, only factors that are relevant to the overall question of economic dependence or independence should be considered.

Under the FLSA, if an employee is incorrectly classified as an independent contractor, the employer would have to pay any unpaid wages it would have owed to the employee. The employer could also have to pay liquidated damages equal to the amount of the back wages, civil money penalties and attorneys’ fees if the situation involves litigation.

There are steps an employer can take to make sure they are incorporating the new guidance into their employment and hiring practices:

• Review all existing independent contractor relationships to determine whether they still qualify as independent

contractors under the final rule. The new factors are more likely to result in workers being considered employees under the FLSA.

• If any workers will be deemed employees under the new guidance, take steps to transition them into employee status, such as formally terminating the independent contractor agreement and completing all required actions for new employees.

• Ensure that relationships with new workers are evaluated according to the revised standard so that workers are not misclassified.

Employers who are concerned about whether their workers are properly classified as employees or independent contractors should consult with experienced legal counsel to ensure compliance with applicable laws and reduce the risks of noncompliance.

Erica A. Storm, JD, is a shareholder at von Briesen & Roper s.c. in Milwaukee, focusing on employment law and employee benefits law and compliance. Contact her at 262-923-8673 or erica.storm@vonbriesen.com.

• Staying up to date on professional issues

Opportunities include:

• Providing strategic governance in accordance with the WICPA strategic plan, mission and vision

• Acquiring new leadership and training skills

To apply, visit wicpa.org/BoardApplication through Nov. 15,

Questions? Contact tammy@wicpa.org.

CAMICO knows CPAs, because we are CPAs.

Created by CPAs, for CPAs, CAMICO’s guiding principle since 1986 has been to protect our policyholders through thick and thin. We are the program of choice for more than 8,000 accounting firms nationwide. Why?

CAMICO’s Professional Liability Insurance policy addresses the scope of services that CPAs provide.

Includes unlimited, no-cost access to specialists and risk management resources to help address the concerns and issues that you face as a CPA.

Provides potential claim counseling and expert claim assistance from internal specialists who will help you navigate the situation with tact, knowledge and expertise.

Does your insurance program go the extra mile? Visit www.camico.com to learn more.

Harris Hauptman Senior Account Executive

By Dan Nash, CPA

Diversity, equity and inclusion (DEI) in the accounting profession is as important today as ever. Four years ago, a wave of momentum in support of DEI swept through the business community. Organizations held employee town halls, launched new programs and established goals intended to drive measurable progress. Today, some organizations find themselves at a crossroads, with the topic itself becoming a political flashpoint. How can we constructively discuss the continued importance of DEI to the accounting profession and ensure that the momentum required to drive long-term progress persists?

A benign illustration comes to mind that is unrelated to racial, ethnic and gender diversity. As journalist Malcolm Gladwell examines in his book, Outliers: The Story of Success, a disproportionately high number of professional Canadian ice

hockey players are born in the first half of the year. This is because youth hockey eligibility is based on the calendar year children were born, so those born in January play against those born in December of the same year. The resulting phenomenon is an overrepresentation of those born earlier in the year at elite levels based on relative advantages at junior levels.

So what? I’m not particularly passionate about ice hockey. The relevant observation here is that there is nothing about people born earlier in the year that makes them inherently better at ice hockey. The existence of significant disparities, in this case by birth month, is an indication of systemic advantages for one subset of the talent pool (i.e., those born earlier in the year) and disadvantages for another (i.e., those born later in the year). The upshot is that these arbitrary advantages and disadvantages ultimately make the sport as a whole worse off because the talent of those born later in the year is not being fully tapped.

DEI is not about preferential treatment. It’s about identifying root causes of disparities and working to ensure we are fully tapping into the potential of our very deep talent pool.

“

DEI is not about preferential treatment. It’s about identifying root causes of disparities and working to ensure we are fully tapping into the potential of our very deep talent pool.

According to the U.S. Census Bureau, approximately 14% of the U.S. population is Black, and 19% is Latinx. By contrast, 2% of CPAs are Black, and 5% are Latinx, according to the AICPA 2021 Trends report, the most recent report that includes demographic information of CPAs. In Wisconsin, 7% of the population is Black and 8% is Latinx, with significantly higher percentages in the Milwaukee metropolitan area, where many of the state’s largest businesses are located. While Wisconsin CPA demographic information is not reported, it is apparent that similar levels of underrepresentation exist. These disparities aren’t simply indicative of advantages for some of us and disadvantages for some of us; they are indicative of disadvantages for the sum of us because talent is not being fully tapped.

The accounting profession has a lot to gain from fully tapping into the potential of diverse talent. The talent shortage facing the profession has been well publicized. Significantly fewer students have selected accounting as a major, and the number of candidates sitting for the CPA exam nationally is down more than 30% since 2016 according to the AICPA 2023 Trends report. Meanwhile, demand for CPAs remains high, with most firms surveyed by the AICPA reporting that they expect hiring of CPAs to increase or remain the same.

How will the math work in the coming years? Fully tapping into the talent pool will be critical. Holding all else constant, if the number of Black and Latinx CPAs increased commensurate with the demographic percentages of the U.S., we would see an increase in CPAs of approximately 26%. That would go a long way to help address the decline in new CPA candidates being observed today.

Of course, a multi-faceted approach is needed to address the root causes of the decline in CPA candidates, which has been observed across demographic groups. Factors such as the 150-hour requirement, cost of education, compensation levels and perceptions about the profession all need to be addressed to comprehensively solve the pipeline problem. As part of that comprehensive approach, let us remember the powerful opportunity that DEI progress presents.

Many organizations have been doing meaningful work to move the needle forward. For example, Deloitte’s Making Accounting Diverse and Equitable (MADE) commitment

involves collaborating with high schools, colleges, state CPA societies and nonprofits to bring accounting to life for thousands of racially and ethnically diverse youth across the country (including in the state of Wisconsin). Outside of public accounting, major Wisconsin-based organizations such as Baird, Northwestern Mutual and Johnson Controls have also been actively engaged with local schools and nonprofits to invest in a diverse talent pipeline. Sustainment of such efforts will be key to driving progress over the long term.

DEI isn’t all about numbers. Focusing on increasing diverse representation without also fostering an inclusive culture will yield diminished returns. To maximize the benefits of a more diverse workforce, organizations should also focus on enhancing the degree to which associates of all backgrounds and orientations are embraced and enabled to make meaningful contributions.

Leading organizations recognize that weaving inclusivity into the fabric of their culture is not only the right thing to do, but it also provides a competitive advantage in both attracting and retaining top talent and in delivering the best client service. This is particularly true in the professional services industry, where businesses are built on the knowledge and unique perspectives of their people. Creating an inclusive culture is essential to ensuring that professionals with different perspectives and backgrounds can deliver the most value to clients and be the best colleagues for each other.

Ultimately, that is the business case for DEI. Organizations should seek to attract the best talent, maximize that talent, and deliver the greatest value to clients. Where significant disparities exist, organizations should seek to identify the root causes and work to ensure that the potential of the talent pool is fully tapped. An inclusive environment helps talent from every background thrive. The organizations, their associates, their clients, their communities and our profession will all be better off.

Dan Nash, CPA, is a financial planning & analysis manager at Baird in Milwaukee. He has more than 12 years of experience in accounting and finance and is a recipient of the 2024 WICPA Excellence Award for Diversity & Inclusion Impact. Contact him at dnash.uwm@gmail.com.

Emily Aleckson, Concordia University

Benjamin Althoff RSM US LLP

Eric J. Andersen Baker Tilly

Matthew Annis

David M. Armstrong Wayland Academy

Saima Bagha

Logan Bagley RSM US LLP

Kathy Barke Association of Equipment Manufacturers

Quinn W. Barkow PwC

Melissa Barnett Vrakas CPAs + Advisors

Gabrielle Bauch RSM US LLP

Stephanie Beardsley Equity Co-op. Livestock Sales Assoc.

Michael Beckwith The Suby Group

Rosemary Bell

Joshua M. Benson City of Milwaukee Office of the Comptroller

Alyssa Benzine UW–Madison

Megan Benzschawel UW–Madison

Brett Berget

Bridget Bishop RitzHolman CPAs

Anna L. Bjornstad Deloitte & Touche LLP

April 1, 2024 – July 31, 2024

Joseph S. Blank Endries Otto LLC

Hunter Bolson Hawkins Ash CPAs LLP

Nathan Borstad McMahon, Schleifer & Wood LLC

Theresa Bradley Ascendium Education Group

McKenzie M. Brandt

Kaitlin M. Brant Ellsworth Cooperative Creamery

Nolan R. Bratt Derse Inc.

Neil Brooks

Cierra S. Brown

Daniel Buchholtz

Victoria Callies RSM US LLP

Madelyn E. Carey

Jack D. Carpenter Cohen & Co.

Christian N. Chin UW–Madison

Anders Clark

Steven I. Concepcion Marquette University

Brittney L. Cose Baker Tilly

Sarah Cutsforth Johnson Block & Co. Inc.

Joshua R. Daggett Office of the Commissioner of Insurance

Nathan Davis RitzHolman CPAs

John B. Davitt RSM US LLP

Gina M. De Sota Wisconsin Hotel & Lodging Assoc.

Samuel DeDecker DeDecker Wertz CPAs LLC

Maria G. DeRocco

Sara Deuman RSM US LLP

Emily K. Di Nardo Baker Tilly

Sam DiVarco III Lucida Tax & Accounting Solutions

Jennifer Dodge KMJ Tax and Accounting Inc.

Kaitlyn Dominguez RSM US LLP

Caitlin J. Eaton Two Rivers Accounting LLC

Conner C. Ericksen AbbVie Inc.

Monica Erickson RSM US LLP

Jenelle E. Falvey Ernst & Young LLP

Jason P. Faschingbauer RSM US LLP

Ashley Faulhaber Schumacher Sama LLP

Victoria A. Fischer Greenheck Fan Corp.

Alexander E. Flater Scribner Cohen and Co. S.C.

Rachel Flynn Schreiber Foods Inc.

Alison M. Galinsky Mukwonago High School

Samuel Gauger Colliers International

Jack Geurts Hawkins Ash CPAs LLP

Thomas Ginther RSM US LLP

Brenda K. Glendenning Johnson Block & Co. Inc.

Micah D. Good

Alexandria Graves Johnson Block & Co. Inc.

Sarah Grenier

UW–Whitewater College of Business & Economics

Jacob Grinnell Quandt Berndt & Co.

Kristi A. Groth

Amy Gumtz MBE CPAs LLP

Nicole Gundrum RSM US LLP

Peter S. Haslam

Chassidy Hastings Hancock & Robinson CPAs

Kevin J. Heim CLA

Israh Hendrix

Grace Henke Johnson Block & Co. Inc.

Allise Henley Quintec Integration Inc.

Carter Holden Bauman Associates Ltd.

Karolyn G. Holloway

Zhen Huang Deloitte & Touche LLP

Candi Huber Toys For Trucks Inc.

Kelly Hurst Johnson Block & Co. Inc.

Raphael Imgrund Hawkins Ash CPAs LLP

Chelsea L. Indra Oconomowoc Area School District

Jordan Janssen

Megan Johnson Johnson Block & Co. Inc.

Abby Kaiser Baker Tilly

Laura Kern Sikich LLP

Mark A. Kimmet Jefferson Wells

Jacob S. Kleiner KPMG LLP

Ben Knetzger RSM US LLP

Will Koehler KPMG LLP

Mike R. Kordasiewicz SVA CPAs S.C.

Steven Kraft KPMG LLP

Raymond E. Krouse Sikich LLP

Nicholas D. Kuchenreuther RSM US LLP

Taylor Kwasny

Luke LaCroix

Terry J. Larkin JRM CPAs

Megan Lazarte First Business Bank

Joua Lee Vesta

Sarah Lenzendorf

Johnson Block & Co. Inc.

Sabrina J. Lloyd Baker Tilly

Camryn Long UW–Milwaukee

Eric A. Lowry Meicher CPAs LLP

Jamie Lumsden RSM US LLP

Brittney Lyga

Holly A. Makowka Vrakas CPAs + Advisors

Tyler D. Mancl Mariani Packing Co. Inc.

Eric Manning

Morrison & Assoc. S.C.

Sam Marsden

Johnson Block & Co. Inc.

Maci McElwee

Riley McMannes

Johnson Block & Co. Inc.

Rebecca Meyer RSM US LLP

Chris W. Mieska Neenah Foundry Co.

Joan R. Miller

Abigail Minger St. Norbert College

Danielle L. Minnema Wipfli LLP

Melissa G. Mirenda

Anthony S. Moore

Hawkins Ash CPAs LLP

Andrew J. Moyer RSM US LLP

Colin Mueller RSM US LLP

Nolan Mueller

Hawkins Ash CPAs LLP

Monica Murphy

Johnson Block & Co. Inc.

Andrew L. Murray

Shannon NachreinerMackesey

Johnson Block & Co. Inc.

Bonnie Nelsen

Catalyst Consulting Group LLC

Alex Neufuss RSM US LLP

Cameron J. Neusen

Morgan Stanley Dean Witter Discover & Co.

Nicholas Noye RSM US LLP

Danny O’Brien RSM US LLP

Matthew P. Ochwat

Douglas J. O’Connor RSM US LLP

Grace Olson RitzHolman CPAs

Skye Olstinski Ayres Associates Inc.

Jordyn H. Ossmann UW–Green Bay

Chloe Otto CLA

Crystal Perez Dairyland Electrical Industries

Adam Petersen Johnson Block & Co. Inc.

Amanda Phanthourath Schumacher Sama LLP

Molly J. Rae Johnson Block & Co. Inc.

Abolfazl Rahmani Lulloff Leben & Taylor LLC

Georgi Raykov CLA

Sameer Rehman

Jordan C. Reilly

Scott Reinert

Karen J. Renner

Ryon J. Riggan BDO USA LLP

Samantha N. Rod Baker Tilly

Theresa L. Rowland

Lirije Rrahmani Deloitte & Touche LLP

Karly Rubenzer Bauman Associates Ltd.

Matthew S. Saager

Marissa Sanchez

Carter Sawdey

Johnson Block & Co. Inc.

Melissa Schmear Batteries Plus

Claire Schmidt

RSM US LLP

Daniel Schmidt RSM US LLP

Lance R. Schofield

Shannon Schottler Schottler Farms

Charissa M. Schulte

KMA Bodilly CPAs & Consultants S.C.

Holden S. Schultz Kohls Corp.

Hayden E. Schumann KPMG LLP

Stephen Shelly Brew City Accounting and Tax

James T. Siedjak

Travis Signer Johnson Block & Co. Inc.

Kurtis Sippy Accenture

Brad Smith RSM US LLP

Madeline C. Sobojinski

Douglas Dynamics

Yvonne Ssempijja

Sebastian Family Psychology Practice Inc.

Mikayla Stacy RSM US LLP

Chloe Stagman Johnson Block & Co. Inc.

Austin Sternbach Uline Inc.

Josalyn T. Stohr McFarland High School

Sui-Nae Stroman RSM US LLP

Alexis R. Strong Chunxia Sun

Sandy Sunalkar Vesta

Courtney Switon Vrakas CPAs + Advisors

Bryce A. Tesarik Hawkins Ash CPAs LLP

Allan Thern

Konkel Accounting LLC

Kaelin Thibodeau Vesta

Erik R. Thurnau RSM US LLP

Brett Tilot Green Bay Packaging Inc.

Joseph Turpin

Johnson Block & Co. Inc.

Ram Vajrala Vesta

Brandon D. VandeHei Baker Tilly

Justin Vredeveld Ontech Systems

Dawn Waara Peshtigo High School

Eugene Wakefield RitzHolman CPAs

Marissa M. Warzynski UW–Stevens Point

Haley N. Wellner CLA

Kendra Whyte Dwayne Johnson & Assoc.

Matthew Wickeham PwC

Bailey Willis NOVII CPA LLC

Ryan Wilson RSM US LLP

Taylor Yandry Wegner CPAs

By Prashant Kothari, CA, CPA, CISA

Many people think offshoring and outsourcing are one and the same. They are not. Outsourcing utilizes thirdparty providers that are, in essence, providing temporary help, while offshoring involves establishing a relationship with a dedicated, cohesive team.

In today’s globalized economy, managing offshore teams has become a common practice for companies seeking to leverage talent, reduce costs and increase productivity. While the benefits are significant, managing an offshore team presents unique challenges that require strategic approaches to ensure success. Following are key strategies for managing offshore teams effectively.

Good offshore hiring practices include clearly defining job roles, using structured interviews, assessing both skills and cultural fit, and implementing unbiased evaluation methods. Prioritize diversity, conduct thorough background checks and engage multiple stakeholders in the decision-making process to ensure the selection of qualified, compatible candidates who align with organizational values. I view offshore teams as an extended team. Therefore, the hiring practices are no different than hiring U.S.-based employees. Mind Your Business Inc., a professional background screening provider, notes the following:

• 10% of all background checks have at least one serious red flag.

• Employers have lost more than 78% of all negligent hiring cases.

Effective communication is the cornerstone of managing offshore teams. Establish clear communication channels and protocols from the outset. Utilize tools such as Slack, Microsoft Teams, Google Meet or Zoom to facilitate realtime communication. Regular video conferences can help

“

While the benefits are significant, managing an offshore team presents unique challenges that require strategic approaches to ensure success.

bridge the gap caused by physical distance, making team members feel more connected and engaged.

Technology plays a pivotal role in managing offshore teams. Use project management tools like Trello or Jira to track tasks, deadlines and project progress. Time-tracking software can help manage productivity and ensure that work hours are utilized efficiently. Cloud-based documentsharing platforms like Google Drive or Dropbox facilitate seamless collaboration and information sharing. Extend the existing email, VPN and document-sharing technology to the offshore teams for data security and privacy purposes.

Time zone differences can be an advantage if managed properly. It can reduce the turnaround time for the deliverables, creating a competitive advantage for the business. Consider the time zone difference of the offshore team members when planning meetings and deadlines. Use shared calendars to coordinate availability, and plan overlapping work hours for real-time collaboration when necessary.

Cultural differences can impact team dynamics, engagement and communication. It’s essential to cultivate cultural sensitivity and awareness within the team, including accent differences. Encourage team members to learn about each other’s cultures, work habits and communication styles. People from different backgrounds can bring new ideas and

perspectives to projects, which can be especially valuable when solving problems or improving processes, fostering creativity and innovation.

Building a cohesive team despite geographic distances requires intentional efforts to foster team building and collaboration. Organize virtual team-building activities, such as online games, virtual coffee breaks or team challenges. Encourage informal communication to build personal connections and create a sense of camaraderie among team members. Motivated, cohesive teams can work faster and smarter, accomplishing more in less time. A Gallup study found that highly engaged and motivated employees can lead to a 17% increase in productivity. According to the U.S. Department of Labor, the cost of replacing an employee can be 30% of that employee’s first-year earnings, so it’s financially important to maintain low employee turnover, whether onshore or offshore.

Clarity in roles and responsibilities is crucial when managing offshore teams. Clearly define each team member’s role, responsibilities and expectations. This reduces ambiguity and ensures everyone understands their tasks and how they contribute to the overall project. Documenting processes, standard operating procedures and workflows can also help to maintain consistency and efficiency.

“

Building a cohesive team despite geographic distances requires intentional efforts to foster team building and collaboration.

Regular performance reviews and feedback are essential for keeping offshore teams on track. Schedule periodic reviews to assess progress, address challenges and provide constructive feedback. Recognize and reward achievements to boost morale and motivation. Constructive feedback helps team members understand areas for improvement and align their efforts with organizational goals.

Investing in the continuous training and development of offshore team members is crucial for their personal growth and the overall success of the team. Offer opportunities for professional development through online courses, workshops

and certifications. Providing access to the latest tools and technologies ensures that the team stays updated and capable of delivering high-quality work. Training and development help to level up the team members, creating a stronger experienced team over time.

Being patient with mistakes fosters a learning culture, encouraging growth and innovation. Recognize errors as opportunities for improvement, provide constructive feedback and support offshore team members in finding solutions. Patience builds trust, boosts morale and ultimately leads to a more resilient and capable team. This is especially important in the early stages of establishing an offshore team.

Finally, continuously monitor the performance and dynamics of your offshore team. Be open to feedback and willing to adapt your strategies as needed. Regularly assess what is working well and what can be improved. Flexibility and adaptability are key to navigating the challenges of effectively managing offshore teams. Businesses often

overlook the importance of receiving feedback from offshore teams. Receiving feedback is crucial for process improvement, enhanced performance and easy adaptation, all of which result in quicker growth.

Successfully managing offshore teams requires a strategic approach that encompasses clear communication, cultural sensitivity, defined roles and leveraging technology. By fostering trust, addressing time zone differences, encouraging team building and providing continuous training, organizations can overcome the challenges of managing offshore teams and unlock their full potential. As the trend of offshore teams continues to grow, implementing these strategies will be essential for achieving long-term success in a globalized workforce.

Prashant Kothari, CA, CPA, CISA, is president at SkillBench Inc. He has more than 25 years of experience sourcing, screening, hiring, deploying and managing remote talent. Contact him at 414-364-8955 or prashant@globalskillbench.com.

Legislators see WICPA members as trustworthy experts, who are knowledgeable and objective when it comes to business and economic issues that impact our state.

As the WICPA continues to navigate through the diverse political climate, we will need to build and invest in new relationships and maintain the current ones that are important to support, protect, defend and defeat policy impacting the accounting profession and Wisconsin businesses. Your financial resources are needed to contribute to election campaigns and sustain our voice in state government.

We anticipate proposed legislation in the following areas:

• Deregulation and elimination of licensing requirements for CPAs and other highly technical professions that would harm Wisconsin businesses and clients.

• Imposing sales tax on professional services that are critical to the well-being of Wisconsin residents and businesses.

• Continued simplification of statutes to conform to the federal tax code so CPAs, taxpayers and businesses benefit from clarification and avoid confusion.

• Evaluation of interest rates on refunds and assessments.

There is strength in numbers and unified voices of WICPA members across the state make the difference. Your voice and your financial participation are key. Contributions to participate in the legislative process to promote responsible law changes are a cost of doing business, similar to insurance.

What is the difference?

Contributions to the WICPA Political Action Committee (CPAC) are used to help get elected political candidates who understand and support our positions. Informed decisions by the WICPA are made about which candidates to support by closely monitoring the political climate, candidates’ platforms and their track records.

Contributions to the Legislative Involvement Fund (LIF) are used only with your consent to help get elected position candidates who understand and support our positions. We will contact you for permission to use your funds for a particular candidate OR you can designate the State Representative, Senator or Governor or preferred political party on the contribution form.

Both forms of contributions are important for success. Amounts needed to contribute to legislators are usually in excess of PAC limits. Contributions to LIF provide the additional financial funding needed to support legislators and our positions. We recommend larger contributions are better suited to LIF and smaller contributions to CPAC.

Michael Amidzich, CPA, an accounting and business instructor at Blackhawk Technical College, Janesville campus, was named Teacher of the Month in May by the Rotary Club of Beloit.

Nathaniel Bartz, CPA, has been promoted to partner at Wipfli LLP in the Wausau office.

Nathan Dreikosen, CPA, has been promoted to principal at SVA Certified Public Accountants.

Bob Flannery, CPA, CFO and senior vice president at UW Health, has received the 2024 Lifetime Achievement Award from In Business magazine.

Kristen Glatzel, CPA, MSA, has been promoted to audit manager at RitzHolman CPAs in Milwaukee.

Kurt Gresens, CPA, CMA, CGMA, managing partner at Wipfli LLP in Green Bay, has been named to Forbes magazine’s annual list of America’s Top 200 CPAs for 2024.

Adam Guernsey, CPA, has been promoted to tax manager at RitzHolman CPAs.

Jared Heimerl, CPA, has been promoted to partner at Wipfli LLP in the Green Bay office.

James Heinrich, CPA, has been elected chair pf the Waukesha County Board. Representing District 9, which includes portions of the city and town of Brookfield, Heinrich has been chair of the board’s Finance Committee since 2014.

Matt Hennig has been promoted to senior accountant at RitzHolman CPAs.

Justin Hoagland, CPA, has been promoted to principal at Baker Tilly in Madison.

Shari Kassube, CPA, has been promoted to director of operations at Novii CPA in Madison.

Robert Keebler, CPA/PFS, MST, AEP (Distinguished), has been named to Forbes magazine’s annual list of America’s Top 200 CPAs for 2024.

Will Koehler, audit associate at KPMG in Milwaukee, has been named a 2023 Elijah Watt Sells Award winner. He graduated in May 2023 with a master’s degree in accounting from UW–Madison.

Lisa Long, CPA, MST, has been promoted to tax partner at Cohen & Company in Milwaukee.

Jake Meckstroth, CPA, has joined Wis-Pak Inc., a Watertown-based soft drink company, as its controller.

Shawn Miller, CPA, has been promoted to principal at SVA Certified Public Accountants.

Shelby Netz, CPA, MST, has been promoted to principal at Baker Tilly in Milwaukee.

Joseph Peikert, CPA, president and CEO of Wolf River Community Bank in Hortonville, has been appointed vice chair of the Wisconsin Bankers Association.

Brad Quade, CPA, has been promoted to executive vice president and chief credit officer at First Business Financial Services Inc., the parent company of First Business Bank.

Lindsey Sabelko, CPA, has been promoted to partner at Wipfli LLP in the Eau Claire office.

Tori Sarazin has been promoted to senior accountant at RitzHolman CPAs.

Victoria Thayer, CPA, founder and president of Novii CPA in Madison, was one of six CPAs in the United States to receive a 2024 Outstanding Young CPA Award from the American Institute of CPAs.

Adam Updike, CPA, has been promoted to senior manager on the tax team at RitzHolman CPAs, Milwaukee.

Peter Van Ermen, CPA, has joined RitzHolman CPAs as a principal on the firm’s tax team in Milwaukee.

Bailey Willis has been promoted to senior accountant at Novii CPA in Madison.

Natalie Zuege, CPA, has been promoted to principal at Baker Tilly in Milwaukee.

Doris E. Brosnan doris.brosnan@vonbriesen.com

Ryan P. Heiden

Kyle J. Gulya kyle.gulya@vonbriesen.com

Jill Pedigo Hall jill.hall@vonbriesen.com

Ann Barry Hanneman ann.hanneman@vonbriesen.com ryan.heiden@vonbriesen.com

Mark S. Kapocius mark.kapocius@vonbriesen.com

Craig T. Papka craig.papka@vonbriesen.com

James R. Macy james.macy@vonbriesen.com

Victoria L. Seltun victoria.seltun@vonbriesen.com

Robert J. Simandl robert.simandl@vonbriesen.com

Maeve G. O’Malley maeve.o’malley@vonbriesen.com

Michael R. Sherer michael.sherer@vonbriesen.com

Erica A. Storm erica.storm@vonbriesen.com

By Jordan Boehm, CPA and

ARick Krueger, CPA

rtificial intelligence (AI) is a term that encompasses various technologies that enable machines to perform tasks that normally require human intelligence, such as learning, reasoning and decision-making. AI has been advancing rapidly in recent years, thanks to the availability of copious amounts of data, powerful computing resources and innovative algorithms. AI has the potential to disrupt many industries and sectors, including the audit and assurance profession. Auditing isn’t typically associated with excitement or innovation, but that’s all changing thanks to some serious tech upgrades. Let’s dive into the fun and fascinating world of auditing’s tech transformation, covering everything from data integration to AI-driven document wizardry and the all-important human touch.

How might AI expand the impact each professional can have in serving clients? Democratizing AI and digital tech will allow everyone to get a slice of the pie. Remember the days when Excel was the coolest tool in town? Well, those days are evolving, and now it’s all about democratizing AI and digital tech. No more massive, one-size-fits-all systems that try (and often fail) to handle every situation. Instead, we get customizable tools that make everyone’s life easier. Think of AI as the new, supercharged version of your trusty calculator. It can do so much more, and it’s available to everyone. Just as

Excel transformed how we handle data, AI is set to revolutionize auditing by letting auditors tailor the tech to their needs. It’s like giving everyone their own personal auditing assistant!

AI can enhance the quality and efficiency of assurance services by automating routine tasks, analyzing large and complex data sets, detecting anomalies and risks, and providing insights and recommendations. It is important to understand that artificial intelligence will initially serve as a tool to enhance the capability of professionals performing these services. By eliminating certain types of time-consuming activities, such as data entry, the younger professionals will have the ability to spend more time developing and honing their skills to progress more quickly in their careers. For example, AI can help auditors do the following:

• Perform data extraction, validation and reconciliation from various sources and formats

• Apply advanced analytics and machine-learning techniques to identify patterns, trends, outliers and anomalies in the data

• Generate audit evidence, conclusions and reports based on the data analysis

• Evaluate the effectiveness of internal controls and compliance with regulations and standards

• Monitor and assess the performance and reliability of AI systems used by the clients

• Communicate and collaborate with the clients and other stakeholders using natural language processing and generation

Despite all this tech magic, humans are still the stars of the show. We always talk about the “human in the loop” because, let’s face it, technology is great, but it can’t replace good old human judgment. Think of AI as your trusty sidekick, always there to assist but never take over completely.

With humans in the loop, AI offers many opportunities for improving the quality and value of assurance services, such as these:

• Enhancing the audit scope, coverage and depth by enabling auditors to examine more data and transactions and to focus on higher-risk areas and complex judgments

• Improving audit accuracy, consistency and transparency by reducing human errors, biases and subjectivity and providing audit trails and explanations for the audit findings

• Increasing the audit relevance, timeliness and responsiveness by enabling auditors to provide continuous and real-time assurance and adapting to changing environments and expectations

• Expanding the audit scope, skills and services by enabling auditors to provide assurance on new types of information and systems, such as nonfinancial data, sustainability reports and AI systems; and offering new services, such as data quality assurance, AI assurance and advisory services

However, AI also poses some challenges and risks for the assurance profession — for example:

• Ensuring the quality, reliability and security of the AI systems and data used by the auditors and the clients and addressing the potential issues of data privacy, ethics and bias

• Developing and maintaining the technical skills, knowledge and competencies of the auditors and the regulators to understand, use and oversee the AI systems and data

• Updating and aligning the audit standards, frameworks and methodologies to reflect the use and impact of AI on the assurance processes and outcomes

• Balancing the benefits and costs of adopting and implementing AI for the assurance services and managing the expectations and perceptions of the clients and other stakeholders

AI will change the way we approach providing assurance services, but it will not eliminate the need for professionals to understand generally accepted auditing standards and how to apply them. Client acceptance, risk assessment, evaluating internal controls, and substantive testing will continue to be skill sets critical to providing quality assurance services. This technology is not able to eliminate the need for professional judgment and the application of that judgment to the services provided. It will serve as a tool to complete tasks within the performance of providing assurance services, which will expand the ability to perform these services in a timely manner.

“ The future of auditing is here, and it’s not just efficient — it’s exciting!

Continual professional development focused on the use of AI in providing assurance services will need to be a focal point for the profession as we move into the future.

The future of auditing is here, and it’s not just efficient — it’s exciting! With technology taking over the mundane tasks, auditors can focus on what they do best: providing valuable insights and making informed decisions. Integrating data, democratizing AI and keeping humans in the loop are key to this transformation.

So, let’s embrace the tech takeover and enjoy the ride. Auditing has never been this fun, and the best is yet to come!

Jordan Boehm, CPA, is a principal at CliftonLarsonAllen (CLA) and a member of CLA’s Regulated Industries team. Contact him at 414-721-7510 or Jordan.Boehm@CLAconnect.com. Rick Krueger, CPA, is managing principal of service at CLA. Contact him at 414-721-7577 or Richard.Krueger@CLAconnect.com.

James (Jim) Miller, CPA, passed away Tuesday, April 30, at age 70. Miller grew up in Plymouth, graduating from Plymouth Comprehensive High School, and then attended the School of Business at Marquette University. After graduating from Marquette with a degree in accounting in 1975, he passed the CPA Exam and obtained his CPA license. Miller was employed at Ladish Co. Inc. (now ATI Forged Products) in Cudahy for over 30 years, serving as an accountant and corporate controller. He was an active member of the WICPA since 1982 and the recipient of the Business & Management Excellence Award in 2011. He served as a member of the following boards, committees or groups: the WICPA board of directors; the WICPA Educational Foundation board of directors; the Wisconsin Taxation, CPAs in Industry, Business & Industry Fall Conference Planning, Excellence Awards Selection, Educational Foundation Nominations, Educational Foundation Fundraising, and KnowledgeShare Planning committees; as well as a member of Advocacy Outreach and Manufacturing Network groups. Miller is survived by his wife, Suzanne; their son and daughter; four sisters and two brothers; many nieces and nephews; and other family members and friends.

Michael Mitchell Berzowski, CPA, JD (1940–2024)

Mike Berzowski, CPA, JD, 84, passed away Wednesday, June 3. He was a lifetime member of the WICPA, attaining his CPA license in 1968 and adding it to his Juris Doctorate degree. Berzowski worked with Price Waterhouse (now PwC) before joining a law firm that eventually bore his name, Weiss Berzowski Brady LLP. After 55 years, Berzowski retired from the firm in 2016, along with several other partners, when the firm dissolved and most of the remaining attorneys and staff joined von Briesen & Roper s.c. Berzowski served his country in the U.S. Army, retiring as a major general. He was a member or life member in numerous professional, honorary, business, civic, religious and fraternal organizations and held multiple leadership positions. He served four terms as the president of the Wisconsin Club and 15 years as the original chair of the Polish Center of Wisconsin’s

Facility Committee. He also was a member of the Sovereign Military Order of Jerusalem, attaining the rank of Grand Croix and receiving the organization’s Distinguished Service Medal. Berzowski received numerous awards and decorations throughout his life, including the U.S. Army Distinguished Service Medal, a Marquette University Law School Distinguished Alumnus of the Year award, and a Leaders in Law award. He is survived by his wife of 57 years, Jan Lee; a brother; one son and two daughters; and five grandchildren.

Jack De Young, CPA (1940–2024)