Roc Lending is solely in the business of providing capital to Private originating. Elevate your return on capital with Roc.

PROGRAM DETAILS:

• Eligible Borrowers: Private Lenders and Investment Funds

• Eligible Collateral: 1-4 Family Non-Owner Occupied Residential Investment Properties

• Maximum Account Size: $50 Million

• No Up-Front Fees

• Advance Rates Up to 90%

• No Personal Recourse

• No Cross-Collateralization

“ Roc has been paramount in helping us grow. They table fund our loans with a higher advance rate than any bank. They have a dedicated team on call to process and approve construction draws and payoffs. With Roc, we can focus on making loans instead of raising money.”

Private Lender 2016

JANUARY / FEBRUARY

CONTENTS

5Private Lender Contributors

9Lender Limelight

Dale Munson

14Kill Two Birds with One Stone: Secure a Second Source of Funding through HSA Accounts

By: Clay Malcolm

16What’s Current News & Updates from Members of AAPL

20Why Investing in Rural Land Can Make Sense Investor’s Perspective by Abhi Golhar

By: AdaPia d’Errico

26Can I Trade or Share my Email List? By Chrissey Breault

PRIVATE LENDER

January/February 2016

CEO Michael Wrenn

Executive Director/ Matt Benson Editor-in-Chief

Production Manager/ Chrissey Breault

Art & Design

Advertising and Sales Dustin Thomas

Private Lender is published semi-bi-monthly by the American Association of Private Lenders (AAPL). AAPL is not responsible for facts or opinions as presented by authors and advertisers.

Visit www.facebook.com/aaplonline or email PrivateLender@aaplonline.com.

For Back Issues: Visit www.issuu.com/aapl, email PrivateLender@aaplonline.com, or call 913-888-1250.

For Article Reprints or Permission to use Private Lender content including text, photos, illustrations, logos, and video: E-mail PrivateLender@aaplonline.com or call 913-888-1250. Use of Private Lender content without the express permission of the American Association of Private Lenders is expressly prohibited.

Private Lender now has upcoming advertisement slots available for future issues.

Advertising in Private Lender is an investment that will pay off with greater visibility that will help your bottom line. Don’t wait to put our message in front of an exclusive collection of private lending professionals. Call us at 913-888-1250 to reserve your space!

PRIVATE LENDER CONTRIBUTORS

•••••MEET A FEW OF THE TALENTED INDIVIDUALS WHO HELPED BRING THIS ISSUE TO LIFE.•••••

CHRISSEY BREAULT

A Pittsburgh native and Hospitality major; Chrissey started a part-time photography and design business in 2009, while working full-time in local government communications. She is currently the Director of Marketing and Education Services with the American Association of Private Lenders. Follow Chrissey @CBExpressions or join her on LInkedIn. Beware: She takes too many pictures of her dog and does not have a filter!

ADAPIA D’ERRICO

AdaPia d’Errico is an entrepreneur, investor, and strategic business advisor. She worked in banking and finance in her early career, transitioning into entrepreneurial ventures in brand development and strategic marketing across the new media, consumer products and entertainment industries. Over the past three years, she has done a deep dive into the high-growth alternative finance space as Chief Marketing Officer at Patch of Land, where she is responsible for driving brand awareness, marketing and communications strategy, and partnerships and business development. She has positioned the company as a recognized leader in real estate crowdfunding, P2RE®, and marketplace lending. AdaPia is a frequent contributor and presenter on these topics, as well as on topics ranging from leadership and marketing, to real estate, economics and crowdfinance.

ABHI GOLHAR

Abhi Golhar is Managing Partner at Summit & Crowne Partners, an Atlanta-based real estate investment firm. Since 2003, Abhi has utilized a “value-added” approach to capitalize on real estate renovation, new construction, and development opportunities in the Midwest and Southeast United States. He actively educates and works with seasoned debt and equity investors to employ market-driven investment strategies that yield success. Abhi holds a BS in Electrical Engineering from the University of Michigan. You may find him tweeting @AbhiGolhar, delivering massive value to investors at #RealEstateDealTalk, sending a market trends newsletter at abhi@summitandcrowne.com, or connecting on LinkedIn

CLAY MALCOLM

Clay oversees most avenues of marketing, teaches Continuing Professional Education and informal classes and webinars, and facilitates the training of business development and client representative teams. Clay has more than 20 years of management experience in various roles, including as the vice president of Jersey Films and as a director for Princeton Review. Clay draws upon his teaching background –including instructor roles with Colorado Outdoor Training Initiative and Ivy West Education – to develop the educational aspects of New Direction IRA and impart knowledge about self-directed IRAs to its clients and prospective clients. Clay received his Bachelor of Science degree in Communications from Northwestern University.” You can contact Clay at cmalcolm@ndira.com

In less than 5 minutes you can open an IRA Services Self-Directed Account. Invest more and do more with an individual retirement account. Open or rollover a Self-Directed IRA today.

Virtually Any Investment

Debt Investments

CrowdFunding Private Equity

Emerging High-Tech Startups

Direct Real Estate Investments

Investments in private REITS, Deeds of Trust/Mortgages

Call (800)

Investments in Privately Held Companies (LLC, LP,C)

Private Notes

Precious Metals

Hedge Funds

Venture Funds

"It is my hope that -togetherwe can create a meaningful outcome for one another."

Dale Munson

In 2008, as a broker, Dale Munson was looking for an alternative to shelter his investors from the volatility and unpredictability of the stock market. With nothing more than an idea and a small group of trusted investors, Cache Private Capital (CPC) was born. In the midst of the “Great Recession,” CPC was able to provide a predictable position senior-secured private real estate loans. They have come a long way since those early days. In 2014 and 2015 they were ranked one of the fastest growing privately held companies in Utah by the Mountain West Capital Network (2014-20th and 2015-24th) and earned a position (2014-851st and 2015-885th respectively) on the Inc. 5000’s national list. Recognition of their growth and success as a company amongst peers is something they are very excited and sincerely honored by.

Although acting as CEO since inception, Munson attribute CPC’s continued success and growth to the talented and capable team of professionals assembled over eight years. With recently converting to a privately held mortgage REIT, their long standing focus on technology, capable staff, and lessons learned, they are well positioned to continue our growth trajectory to serve the investors.

PL: Thanks for taking the time to let our audience learn a little more about you. Let’s start by telling them how you got your start in the industry?

DM: In my early 20s, while attending college with my wife and running a small convenient store, I was fortunate to cross paths with a morning patron who made his living as an “options trader.” Intrigued, I began quizzing him about the markets, strategies employed, economics, etc. With some convincing, he began teaching me the ins and outs

that I knew enough and was convinced I could build

my own fortune by trading my own money. I secured a student loan for $2,000; a seemingly small sum, but at the time given our limited economic means, a great deal of money. Magically, in a matter of weeks, I quickly doubled of days, I lost the entirety of what I had earned, including

Discouraged, but not beaten, I took out a second loan and began again. This time I learned how to protect my funds, how to allocate appropriately, how to assess risk versus reward. Over the next couple of years, I paid back both student loans and a large portion of my college tuition. This began my love for developing investment strategies, understanding economics, and the markets and ultimately set me on my current career path of private lending.

DM: First, read Private Lender magazine and industry thing, but multiple things, in the gaps of my day that give me the information needed on a broad array of topics. In the morning, it is watching and listening to the US news channels instead of music while working out. During the day; I check multiple online news sources and monitor the stock market. In the evening, it is browsing online publications while winding down for the night. It is important to not only keep myself current but to also provide a constant stream and broad array of information available to CPC team members. If you walk into our area on a large big screen TV; well, unless it’s March every TV.

PL: What kinds of mistakes have you seen

•••LENDER

investments?

DM: Fear and greed. As a stock broker for several years prior to founding CPC, I witnessed many investors lose substantial amounts of money because they could not control these two emotions. It became evident to me that if you can learn to remove these emotions from your

is weighted greater to the sincerity of your actions rather than the tactic of your actions. I once heard that “people work for people, not for paychecks.” This has always resonated with me and has been the ongoing theme of what I hope to maintain within CPC. An environment where each team member is excited about the next day and strives to create the success of one another.

At the close of each loan we analyze our outcome and

are included in our proprietary developed management software www.idealsuite.com company fundingdatabase.com fundgdatabase.co managed by Kellen Jones. Over the years, this has greatly improved our underwriting, our processes, and our ability to remove the emotions of fear and greed and make the right decisions more often.

PL: What do you think are some of the biggest mistakes you made and how did you overcome them?

DM: The biggest mistakes I made was when I assumed I knew all there was to know. I quickly learned that what you don’t know will always exceed what you do know.

PL: How would you describe your management style?

DM: I believe my management style is a balance between what I refer to as “book smart” and “street smart” management. Book smart being the ability to learn management styles such as pacesetting, directive, participative, the appropriate time. And street smart, or the inherent and show your sincerity in wanting the best for those that follow and entrust you with their economic futures. With this being said, I believe management effectiveness

what was its outcome?

DM: The last real project I headed up is the formation and development of CPC. This has been my sole focus and endeavor for nearly eight years now and has resulted in a consistent net AROR to investors of greater than 10 percent. The ultimate outcome of this project is still to be determined, but I am optimistic the next eight years will continue to be as positive as the last eight years.

in the last two years and how did you come to that decision?

DM: Whether or not I have time to stop and grab a coffee on the way in to work in the mornings. It sounds crazy, but my days are full from the moment I get up until I can no longer keep my eyes open. Time for simple things has to

to avoid?

1. Avoid a false sense of investment success and portfolio health. It takes time for a portfolio to mature and an economy to cycle. If what you are doing right now is bringing you success, great, enjoy it. However, don’t forget that markets and portfolios are not static, always be preparing for the constantly changing future.

2. Avoid becoming complacent. Don’t be afraid to make the hard choices before they become critical.

3. Avoid following the general crowd. The crowd is often wrong, so be cautious on where you get your advice from, don’t be afraid to form your own opinion and, at times, to go against the crowd.

them establish their credibility with lenders?

DM: Honesty from the beginning. Everything comes out in the wash through the due diligence process. Provide collateral.

PL: What are three things you tell yourself when your

•••LENDER LIMELIGHT•••

DM: When life begins to feel overwhelming and negative occurrences leave me feeling a little dismayed, I tell myself “only focus on and worry about the things you can control.” I try to set aside the things that are out of my control and focus determinably on the things that are within my sphere of control. This gives me a starting point and helps me to organize and prioritize my tasks. Many times just the accepting that there are things outside of relief.

PL: Can you share a life memory or two that you recall most frequently?

DM: The births of my children are the greatest highlight and memory of my life. I was forever and irrevocably changed by my new identity as a father. Prior to their births, I couldn’t imagine loving anyone more than I love my children; they’ve changed the way I see the world and my place in it.

Winning the Idaho State Basketball Championship in 1986 and 1987. Growing up in small town, Rigby, Idaho, basketball was a tradition that put our town on

conquering the state tournament in the second largest division. However, in 1987 our small school was newly included in Idaho’s largest division. With moving up to the largest division, and having lost our 6’9” center halfway through the season, expectations were low. Looking back, our small town team arose to every occasion, and with only three season losses-in unbelievable fashion-won the 1987 state tournament. It had never been done - a team had moved from a smaller division to the biggest division and won back to back championships. It would also be over 20 years before a state championship would be won again by Rigby. I often look back on that time, what was learned, what was overcome, and the catalyst it provided for me to go to college on a basketball scholarship.

DM: Spiderman. I have to go with the superhero and Batman is undoubtedly not a superhero as a superhero by

does not possess.

PL: Can you tell us about the weirdest deal you have

DM

received where the primary source of collateral were two time understanding how to value this unique collateral, how to perfect a lien on a boat, and how to ensure the

request.

about you is and why?

DM: That being a CEO, I have all the answers. Sadly, I don’t. Much like you; my well of information is limited, thus, I have surrounded myself with a competent team of professionals in which I explicitly trust. With the information derived from these individuals, we collectively have (almost) all the answers.

PL: What’s the best advice you’ve ever received? From whom?

DM: I was late to basketball practice once and my coach is showing up.” I’ve thought about that over the years and have come to realize just how broad and true that statement is. How many times have you just not showed up, either from lack of preparedness, it was inconvenient, or because you already decided the outcome. Showing up is sometimes not as simple as it sounds, there are often costs, logistics and obstacles involved. However, the only truly known outcome is derived by showing up.

meaningful?

DM: I’ve never spent much time pondering on what I do or don’t have the power to do, or whether it was ultimately meaningful. Rather my focus is to adequately serve and honor those who have entrust me with their money, futures, careers and friendships. It is my hope that together we can create meaningful outcomes for one another.

made a difference?

DM: Everyone; from athletic coaches, teachers, mentors, co-workers, to family and friends. I have learned something from each and every person at different times in my life, whether it is about myself or my business, which various individuals that I attribute to who I am today. be?

DM: A semi-deserted beach with perfect waves, clear warm water, white sand beach and a cold, clear, mountain river in the background. “Semi-deserted” so I can have just the right amount of catering without the distraction.

trout. If you know of this place, please let me know!

KILL TWO BIRDS WITH ONE STONE: SECURE A SECOND SOURCE OF FUNDING THROUGH HSA ACCOUNTS

By: Clay Malcolm

An HSA, or Health Savings Account, provides those with High Deductible Health Plans (HDHPs) an avenue to save and invest money for all present

were approved by Congress in 2003 during one of the most intensive governmental interventions in medicine in 40 years. The intent behind the inception of HSA accounts is to allow participants of HDHPs to pay out-of-pocket

deductible kicks in.

One of the main perks of an HSA account is that contributions aren’t taxed when they go into the account, and funds aren’t taxed when you take a distribution either. In addition, unlike Health Reimbursement Accounts (HRAs) which are employer-controlled, or Flexible Spending Accounts (FSAs) which offer funding on a “useit-or-lose-it” basis, once contributions have been made into the account, it stays open and retains the money

until the account holder takes distribution of the funds –regardless of whether the account holder is still employed by the employer who offered the HSA.

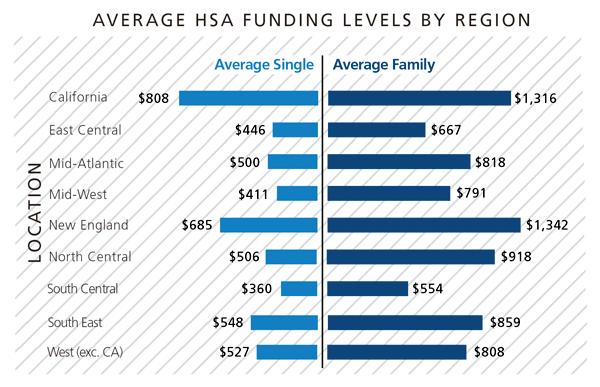

Self-directed HSAs offer the most investing options. It may surprise investors to discover how many options are available to their HSA accounts. Because annual contribution limits of an HSA are lower than those of a 401(k) – the HSA yearly contribution limit is $3,350 a year for individual HDHP coverage, and $6,650 a year for family coverage (including employer contributions), while 401(k) yearly contributions top off at $53,000 (including employee and employer contributions) – investing HSA funds in low-cost assets can help the account realize

for health expenses. These assets can take the form of private lending, private equity, precious metals, real estate, and more.

It’s common for employers to offer HSAs through a provider that offers a very limited scope of investing options for their account. Consequently, many investors will open a second HSA account with a provider that allows for alternative asset investing. From here, investors can turn to an almost limitless array of alternative assets that can potentially bring the account holder a sizeable return on their investments.

As HSAs have continued to grow in popularity and average sum being saved, technology has evolved to provide HSA account holders with more online market places for relevant services, including crowdfunding and locating asset providers. One route for HSA investing is peer-to-peer lending. This type of lending allows investors to sort through consumer loan listings and pick those that

In a similar vein, HSA account holders can originate their own loans. They can invest in private equity opportunities

such as buying private stock in a friend’s promising new enterprise.

Many lenders (especially online lenders) who fund their loans using investor money are becoming aware of the

IRAs can become investors in your operation, either on a private equity or a lending basis. Tax-advantaged retirement accounts can expand your business and, by extension, your potential lending power.

The key to effective interaction with HSAs consists of two main components: strategic education and convenient HSA technology. Education will give HSA holders the IRA investment in your business, while leading-edge technology will make the HSA investment process as easy and convenient as possible for all parties.

It’s not necessary for lenders themselves to be HSA experts in order to educate their investors about selfdirected HSA lending. Lenders can utilize industry-best educational resources provided by self-directed HSA and IRA custodians like New Direction IRA in order to impart HSA lending and private equity knowledge to their investors.

Having a way for investors to set up their HSAs and invest their funds electronically is a huge advantage for

lenders. Disbursing returns back to investors digitally also adds an element of ease and convenience to the HSA lending process.

Source: shrm.org

WHAT’SCurrent

NEWS UPDATES &

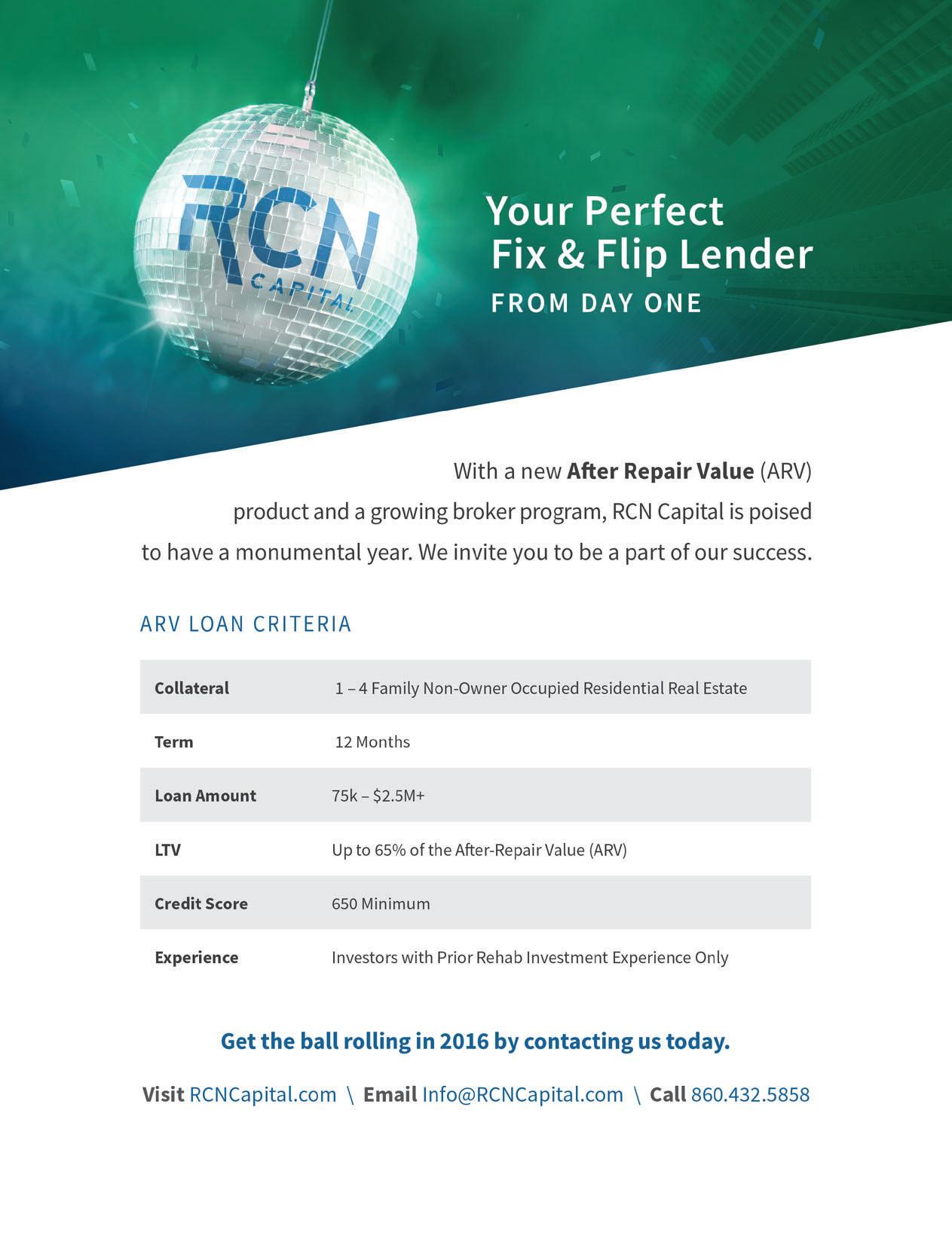

RCN Capital Awarded Finance Lending License in California

RCN Capital, a national, direct private lender, announced that it has been awarded a Finance Lending License in the State of California. As a licensed California Finance Lender under the state’s Department of Business Oversight (60DBO-46258), RCN Capital has expanded its national footprint to one of the nation’s hottest residential and commercial real estate investment markets. Mortgage professionals in California now have access to more creative funding solutions through RCN’s unique loan programs.

Richey May & Co., LLP Promotes New Partner, Alternative Investments Practice

its leadership team with the recent promotion of Stephen Vlasak to the position of Partner in the Alternative Investment Practice with the focus of Business Development.

Stephen develops new client relationships for the Alternative Investment Services group, working and advisory services to hedge, private equity, venture capital, and private money lenders. Stephen enjoys his role as a connector in the business community. He is very involved with providing introductions and advice that help newly launched entities grow and thrive. In addition to the business development role, Stephen is also involved on the audit side of the Alternative Investments Practice and has over 17 years of audit experience within the advises his clients on initial organizational structure, audit processes, the management of operational matters and regulatory needs.

Submit your current news, updates, or job opportunities for possible inclusion in the next issue of Private Lender. Send details to PrivateLender@aaplonline.com

Applied Business Software Announces Website Redesign Launch

Applied Business Software Inc. (ABS), developers of is excited to announce the launch of a revamped website

The Long Beach based software company announced the launch of a redesigned website ( com) to offer its visitors a comprehensive overview of the company’s innovative software. The newly redesigned website, supported by all browsers and mobile devices, and feel. It details all the modules available for its clients’ scalable needs, company news and events, case studies, testimonials and latest publications where Applied Business Software has been featured.

Iknowa lot of you have either heard of or know of the Truth-in-Lending RESPA Integrated Disclosure rule propagated by the CFPB. Title companies have told you about TRID, your customers have, TRID with our clients: what about business purpose loans? Do they apply to TRID?

WHAT IS A BUSINESS PURPOSE LOAN?

Before we get to that question, it may be helpful to review what exactly a business purpose loan is.

IF IT IS A BUSINESS PURPOSE LOAN, THEN WHAT?

Business purpose loans are exempt from the Truth-in-Lending Act’s requirements. There is a fairly well developed body of law in this space, and I can summarize the business purpose exemption as follows: (a) the primary purpose of the loan is for business purposes; (b) borrower is acquiring, improving or maintaining rental property that is not owner-occupied; or (c) borrower is an entity. There are other tests, but these are the most common that we have faced.

Business purpose loans are an exemption from the Truth-in-Lending Act and Regulation Z, the regulations that interpret it. See, e.g., 12 C.F.R. 1026.3(a). Thus, if you have a business purpose loan, you are exempt from TRID, which is an amendment to the Truth-in-Lending Act.

PERSPECTIVE REAL DEAL Abhi’s

WHY INVESTING IN RURAL LAND CAN MAKE SENSE

BY: ABHI GOLHAR

Asingle-family homes in Atlanta and Charlotte. But,

Simply put, my investment strategies shift as the market shifts. Currently, my gut is telling me that investors in new construction and extensive renovations. Therefore, I feel it’s imperative to identify additional strategies to begin implementing.

With an ever-growing American population, land is becoming a scarce commodity in many areas. This scarcity helps to make land values increase over time, which helps to make rural land an interesting investment idea.

Urban Growth

As cities expand, today’s undeveloped rural areas will become tomorrow’s suburbs. This means that a wise investor who buys in the right area can expect to undeveloped land is sectioned off and sold for the development of commercial and residential lots. Areas of interest for investors may be land situated along Interstates near urban areas and land situated between major metropolitan areas as these areas may be the most likely to be developed.

Aging Population

As more and more Americans reach retirement age, they may fuel a larger demand for the development of rural

retirees will be looking for retirement homes in a country setting away from the cities. This residential development will further increase the need for commercial developments for shopping centers, golf courses and other businesses needed to serve the needs of a new population settlement.

Bargain Prices

The recent decline in real estate values had a particularly large effect on rural land. While developed properties declined in value, undeveloped properties took a bigger hit during the downturn. This decline may make rural and other undeveloped land a particularly attractive investment for those who are seeking a long-term investment at a bargain price. Even without new growth in an area, a person can expect rural land to increase in value over time simply due to the land returning to its past values before the real estate market decline.

Farming Demand

The rising concern about the safety and freshness of food crops is another reason that land continues to increase in value. The demand for organically grown foods and freerange poultry and meat of a local origin has helped the value of farmland to rise. As more land is being productively used for farming purposes, less rural land is available for other purposes. This means that the demand for farming land not only makes farms more valuable, it also makes other rural land more valuable as well.

Recreational Uses

Rural land can be used for a variety of recreational road vehicles. Due to scarcity of land and the decline of the family farm, many people do not have access to land for these purposes and are willing to buy or lease land for recreational purposes. This provides investors with just one more reason to consider an investment in rural land. The property can be leased out year-to-year as a way to produce income from the land until the investor is ready to sell.

A Final Thought

Rural land is an investment that requires vision beyond just invisible to others.” Want to chat more about rural land and real estate opportunities you may have? Find me on Twitter @abhigolhar.

As a residential investor, the more sales opportunities you can open, the more you can close. With 5 Arch, our common sense underwriting will enable you to access loans faster, easier and in greater volume. Every day we are opening the door to profit across the country, from AZ, CA, FL, GA, IL, IN, MD, NV, OR, TX to WA.

To find out more visit 5archfunding.com Call us on 866 973 6278 or email info@5archfunding.com

Interested in writing for Private Lender and getting in front of thousands of real estate finance professionals? Contact Chrissey at PrivateLender@aaplonline.com to learn how! (It’s so easy!)

DEFINING THE CROWDFUNDING LANDSCAPE

By: AdaPia d’Errico

It’s 2016, and by now most of us have heard of, or are familiar with, real estate crowdfunding. Alternative lending platforms - whether for real estate, start-ups, or any other aspect of the economy - don’t appear to be going away anytime soon. It has been three years since The JOBS Act was written into law, and two years since the SEC made a historic decision to enact Title II with Reg D 506(c), which opened up new channels of communication and solicitation around private placements. At that time, ‘crowdfunding real estate portals’ launched, aimed at

Short-term real estate debt, essentially bridge and private lending, have emerged as the most successful categories that continue to attract thousands of new investors.

However, real estate is an industry as old as time, while crowdfunded lending, with only a few years in existence, is only in its infancy. At the 2015 Annual AAPL meeting in Las Vegas we asked, “Will this technologyenabled, in-the-cloud model turn out to be a fad, or is it, as many proponents argue, the future?” Today, it seems as though it is more like “the present.” AdaPia d’Errico,

of Land, offers some insights into the trends and changes affecting the new online lending paradigm.

estate crowdfunding. Which of those do you consider

Without a doubt, the number of venture-backed, Series early and leading companies including Patch of Land, after the JOBS Act were about overcoming skepticism, and what we might call the “hardened arteries” of the old boys’ networks, then the venture capital rounds show these online fundraising and syndication platforms are here to stay. At the very least, they now have the capital in place to further penetrate their respective categories, and markets.

preferences related to how they want to transact and interact with lenders, especially in an online environment. Crowdfunding IS the future, and the Internet will continue to attract investors, raising capital from thousands of people and markets that previously had no access to one another. Harnessing technology, communication, openness, and fair and ethical pricing -- what we now call “sunlight banking” -- will continue to offer good quality real estate investments to more people than ever before.

continue to both disrupt, and create opportunities within the real estate sector -- which, let’s face it, is a sector badly in need of updating.

Just as SoFi is taking banks head-on with its “bankless world” campaign and its recent Super Bowl commercial, there is a similar opportunity for someone to take on real better chance of making that happen.

Platforms focusing on technology, data, and excellent customer experience, are even likelier to succeed longterm, as they harness consumer expectations and

How sustainable is Real Estate Crowdfunding? What key elements will allow it to grow?

Some media sites covering the space, have charted and predicted that as much as $10 billion in crowdfunded transactions occurred globally in 2014, quadrupling

crowdfunding industry has an average market potential of around $300 billion by 2025.

increasing by about 26%, from 668 to 842, to close out stood at approximately $155,000. With rising activity in

a period of customers, and capital, responding to the companies and platforms that best serve them.

As I pointed out in my year-end recap for Crowdfund Insider, part of this responsiveness will come from further transparency - providing ample, accessible, coherent information on the topic, product or business being funded. If this doesn’t come from the platforms from which the pool of investors is interacting with, then third parties

Dodd-Frank

Service

Automate

Handle

Built

Enhanced

•••BUSINESS STRATEGY•••

will jump in to attempt to make sense of what might seem like a maze of companies to choose from. Crowdfunding, and marketplace lending, is not lending of last resort, it isn’t lower quality underwriting, and it isn’t exorbitant rates for the desperate.

shaking out? Even distribution? Room for the small guy? Acquisitions by a select few?

I expect the main leaders to continue to break away; many of the dozens that have been popping up will quietly fold. Barriers to entry (for scalable success) are much higher now, as establishing a brand, building trust and an already proven track record are three of the most important aspects to successfully enter an already crowded space.

The latter is especially important for newer investors

interested, who want to make sure they can trust this “new” sector. Of course, the origination of good quality deals plays a key role, too.

Mistakes?

Don’t ignore the “crowd” that gave you market share and new, alternative visions. As a recent Financial Times

the old bricks-and-mortar banks, Lending Club appears to have galvanised them into action, spurring copycat services and all manner of alliances between traditional lenders and the upstarts.”

So it’s important to keep emphasizing what makes us different from those traditional lenders, rather than merely blending in with them.

And tout the tech if you have it. Many marketplace themselves stymied by the need to originate, and wind up dependent upon outside channels. But proprietary channels of both supply and demand will always be extremely important. Using the Internet, and very sophisticated nurture tracks, lead scoring and customer service will prove very valuable in the short and long term.

And while Lending Club’s stock has risen and dipped, change is steadily on the way up, which is why not only traditional lenders, but now, traditional tech companies are circling around the space. As TechCrunch recently said, none of us should “be surprised to see Internet

consumer companies like Google, Facebook or Amazon enter this space and either partner with or acquire existing lending sites.”

But again, what keeps companies in the crowdfunding space attractive is an ongoing focus on good quality. That’s paramount in the real estate sector -- not just posting ‘big numbers’ for the sake of it, for example. Originating $35K consumer loans at scale is a different business model than originating asset-backed real estate across the country, at scale.

And of course, stay focused on transparency. As I previously said to Bankless Times, in today’s day and age of limitless opportunity, there’s no reason to be proprietary or secretive -- except perhaps where intellectual property or trade secrets need protection.

Making a decent investment return – whether you’re an investor or a borrowing developer – is everyone’s expectation. But so are the access and openness we’ve come to expect with “Sunlight Banking,” and online platforms.

In other words, it’s not just the tech, it’s the ethos making

this sector attractive to more “traditional” partners.

1. Non-crowdfunding, traditional real estate operators - lenders, syndicators, and asset management companies - will use JOBS Act regulations, make investments in technology, and try to raise capital for themselves. i.e. less reliance on the operators to raise capital for them. They will embrace the technology and the marketing in order to do it themselves. Big names will continue to enter the space.

2. I expect to see innovative uses of Title III and Title IV crowdfunding regulations. Fundrise, a leading equity crowdfunding platform, recently gained a lot of attention for creating an eReit and is an open ended fund that raises from their tens of thousands of retail and accredited investors, selectively choosing assets.

There is skepticism as to how useful Title III will be to real estate raises, given its $1 million raise limit, but I never discount the innovation and sheer willpower

of entrepreneurs, so we may see some uses of Title III for real estate raises. And, perhaps, someone will attempt a crowdfund that includes rewards, in addition to capital raising, as was the case for the Hard Rock hotel in Palm Springs in 2014.

3. There will be more collaboration between crowdfunding and marketplace lending companies like Patch of Land, and private or hard money lenders. With so much opportunity across the country, and the innovations in technology and data usage that 2016 will bring about deal making and partnerships with private lenders. There are synergies and and take advantage of growing opportunities where or secondary markets that are already heating uplike Sacramento or Charlotte.

CAN I TRADE OR SHARE MY EMAIL LIST?

By: Chrissey Breault

The answer most of the time is “NO!”

Sharing your list probably breaks the privacy policy you’ve created. When people subscribed to your organization’s email list you probably told them in the would not share any information collected from website users with third-parties. Sharing any information, especially personal information (e.g. an email address) that your clients, customers, members and supporters have trusted you with is a direct violation of the very privacy rules you’ve created. Sharing your list makes your organization appear untrustworthy. Your organization should be committed to protecting any information that a customer shares. Even if not explicitly stated, customers assume that you will protect their information. Sharing that information with third-parties is a direct violation of that trust. The price you pay for breaking that trust extends far beyond what a customer thinks about your email program. Customers will start to wonder what else your organization does behind their back with their private information. Clearly, this is not what you want your

customers to think about your organization. Additionally, if email service providers (e.g. Mail Chimp, Vertical you’ve shared your list, or worse yet, emailed a list of people who have not explicitly indicated that they want and the account that owns the list as spammers. Once send, or that the organization you’ve shared a list with sends, will never ever make it to the customer’s inbox again. And if that isn’t enough; sharing your list annoys people. Think about your personal experience with unsolicited email, like when you wonder how a company you’ve never heard of got into your inbox. Does it annoy you? Yes. Do you open it? No. So why risk annoying your customers with an email that they’re probably not going to open anyway?

BACKSCRATCHING FOR CLIENTS

If a partner organization wants to use your list, or if you want to borrow another organization’s email list, you have some options:

Ask the organization whose list you want to use to send an email on your behalf. They can send a dedicated email asking their customers to check out whatever it is you’re trying to “sell.” Or, better yet, they can incorporate a callout about your organization into an email that they’re already planning to send out. That callout can encourage their subscribers to check out your organization and become a subscriber themselves. This approach builds trust among consumers for both the sending organization and the partnering organization. Send an email to your customers with a callout about the organization that wants to use your list. In this case, you should try to incorporate their callout into an email that you are already planning to send (e.g. monthly e-newsletter) and that’s full of relevant content that the subscriber is expecting to see. An email that’s sent from your program, that’s all about another organization could still be considered spam. Tying partner content into your regular email communications will certainly make it appear less spammy and help ensure that your readers know you have their best interest in mind.

How Do I Grow My List?

Email your own list and let them know of the event of the business you want to share lists with. Make sure the link to subscribe is in the email. Make sure they are doing the same for you as well. If you do not post on social media or blog, start immediately. If you are wanting a list of another business who has taken the time to grow their list and/or hire someone to help them, asking them to give you their list is not ethical and frankly, incredibly lame. Make sure you have a sign up form on your website and Facebook page. Make signing up for your email a requirement for a promotion discount or product. If you have an event that includes other businesses, have one main email subscriber list when they check in and that can be shared with everyone participating because the person sharing their email knows that is the case.

If you are not sure, then don’t do it is the general rule. Ask yourself how you would feel if a business did this to you.

Who is covered? anyone who or services by e-mail to or from the U.S.

CANSPAM ACT

What is covered? mail messages” - e-mail messages headers include working return e-mail address identify messages as commercial follow FTC (and FCC) regulations

Each separate email in violation of the CANSPAM Act is subject to penalties of up to non-compliance can be costly!

The American Association of Private Lenders reaches the most tightly targeted audience of Lenders, Fund Managers, Brokers, Investors, Property Managers, and Service Providers in the peer-to-peer lending community. It is the voice of the private lending industry. As such, advertising with the American Association of Private Lenders is an excellent investment and the ideal medium to reach anyone in the private lending industry. Contact us today for more information!