6 minute read

Saving the day

Saving day the

It’s nuts that ordinary folk are depositing more of their income – but earning less and less on it. It made no sense to Simon Rabin, nor to thousands of others who joined savings and investment platform Chip

2020 was a year for squirrelling away cash. With holidays, weddings, and other big-ticket occasions cancelled, UK households’ savings-to-income ratio increased to record levels – from 9.6 per cent in Q1 to 29.1 per cent in Q2, according to government figures.

Not everyone had spare cash to stash. A sizeable number of lower income households, in particular, also ran through reserves at alarming rates. Meanwhile, even those whose deposits grew, often watched them being eroded by real-term negative interest rates. It's why, for those with an appetite for it, Robinhood and the merry band of similar day-trading platforms with a promise of double-digit returns, have attracted such attention from retail investors over the past year.

But their gamified, fast-moving and often high-risk investment tools aren't for everyone. Many savers have more modest ambitions: they don’t want their money idling in a bank deposit account, Rabin founded Chip three and a half but neither do they want to actively years ago, using open banking-powered engage in the markets. auto-saving features to help people put

“They’re not asking for the world. their money away easily, regularly and Right? They don’t need 20 or 25 per cent efficiently. Over the last couple of years, returns per annum. People just want it’s built a 300,000-strong community of to beat inflation, they want to feel that users, who’ve saved more than a quarter they’re leaving their savings in a place of a billion pound, more than 20,000 that it’s going to grow in the medium of whom – the Early Adopters formerly to long term,” says Simon Rabin. known as Chipmunks – have helped

Rabin is co-founder of Chip, an evolve the product. Many are also AI-driven, automated savings and invested in it. Chip has smashed every investment platform that seeks to give Crowdcube funding target it's set – the ‘the little guy’ just that. most recent in September last year when

In the first month of it raised a million in minutes. this year, it brought in They don’t “I think we are the second around £34million of new deposits – a record for the platform – and the need 20 or 25 per cent most equity crowdfunded company in Europe, and we have one of the largest vast majority of those returns per investor communities, as were under £20. annum. People just want to well,“ says Rabin. Chip was born out of Rabin’s personal frustration beat inflation at ‘being unable to save, or being really bad at identifying how much money I should put away each month, and where I should put it’.

For a rainy day:

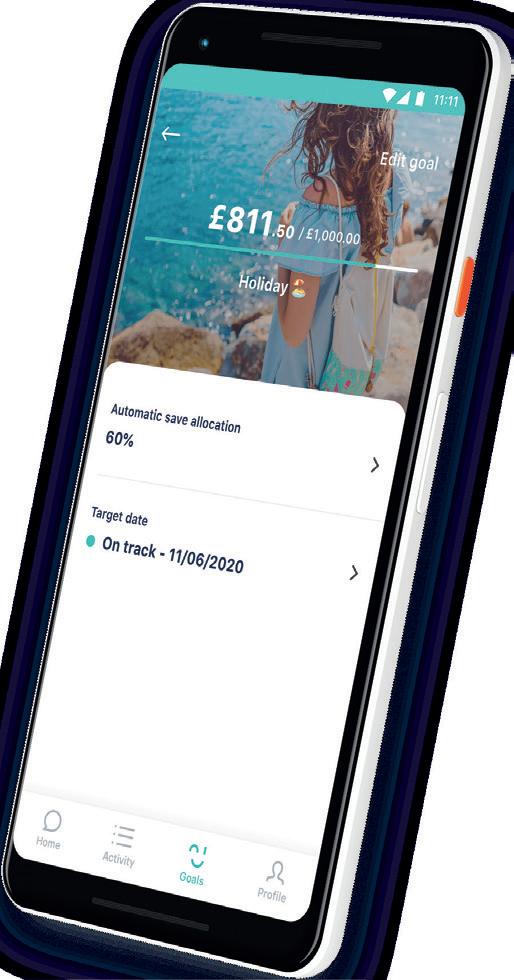

The Chipmunk community has helped design products

An autosave function, which determines how much a user can comfortably put away by plugging into their account to determine their earnings and spending patterns, was relatively simple. The bigger challenge was solving the second part of Rabin’s problem.

“How do you earn the best possible return on those savings? How do you understand investment funds, risk, and what you should be doing with your non-day-to-day money? That’s a problem experienced by the vast majority of what we call the mobile generation,“ he says.

The answer Chip chose was to democratise investments, not by turning ordinary people into mini Belafontes, but by giving them managed, safe access to the world in which he famously moved.

“Our customers have got to ask, ‘why is it that my 1.5 per cent easy-access cash account has suddenly dropped down to 0.1 per cent over the last nine months as a result of the pandemic, yet US markets are up 30 per cent over that same period? What’s going on there? And why am I, as a consumer, being excluded from that?’ Products like Chip are going to answer that question for people,” says Rabin.

And it did it by partnering with one of the leading fund managers in the world, BlackRock, to give access to some of its leading investment funds to consumers.

Meanwhile, Chip’s user experience was designed to be mobile friendly.

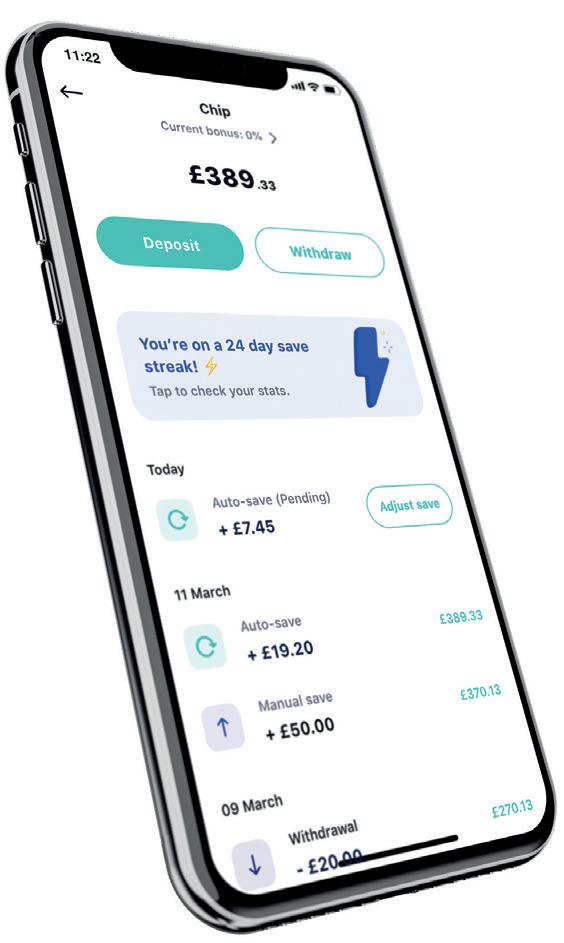

“You can create goals, you can add images, you can see your progress towards them,“ adds Rabin. “With autosaving, our algorithms basically analyse your spending, in your connected current account, and automatically save an amount of money for you into Chip. If that’s not suitable, you can set up recurring payments, with our Payday Put Away feature, or you can just make deposits, as well. It’s as easy to use, if not easier to use than your actual banking app, but provides with you the market’s best returns.”

Much of where Chip is heading has been determined by the feedback and strong connection with its community. “Everything we do – the building, evolving, the pricing of the product, the individual accounts that we introduce – is done hand-in-hand with our early adopter and investor community,“ says Rabin. “That way of building products, and way of building the company, has been incredibly successful for us, and creates a really powerful barrier to entry for others.“

Such a valuable asset needs special care. “I certainly encourage all the functions across the business, from marketing, to product, commercial, finance, design, to try to engage with our community as much as they possibly can,“ says Rabin.

“When you engage your community and they’re very much part of that process up

Easy access:

Chip’s mobile UX was designed to be easier to use than a banking app

front, they’re far more excited, and far more willing to buy and to use the product that they’ve been a part of developing.“

It was the community that wanted investment opportunities that had, historically, not been available to them as ordinary savers, says Rabin, reflecting a wider sentiment in 2020.

“We saw it in what’s been going on with GameStop and WallStreetBets and so on. Consumers are standing up and saying, ‘we’ve had enough of this. There’s no reason why we, as ordinary people, can’t have access to these same financial instruments, can’t play in the market in the same way that the big financial institutions can’, “ says Rabin.

“The vast majority of people, perhaps, don’t feel comfortable actively stock trading, don’t feel knowledgeable enough in that space to be doing that themselves, but they do want to have their money in a place that earns them a decent return, far better than what their bank’s giving them. “Chip is very much focussed on trying to increase that, trying to democratise people’s access to far better returns than they’re being offered in the market at the moment.” This democratisation of access to capital markets, to passive investments, he identifies as a ‘third wave’ of fintech – one that Chip will lead. But for it to be fully realised, open banking principles need to be far more widely embraced in spirit and in practice by financial institutions. “When we built the first version in 2016, we were trying to use all these things that were promised with open banking and there are still issues. We’re seeing the same problems now with payment initiation services – there are quite a few limitations in what they’re able to do.

“Open banking absolutely needs to happen and it will happen, but the pace hasn’t been quick enough and I feel it will continue to be quite slow.“

Chip’s savers aren’t slow, though. They’re still busy hoarding and contributing to the next stage of development – investment accounts, ISAs, potentially any savings pot, including pensions.

“Ultimately, I want to see hundreds of millions of people, across the UK, Europe, and beyond, with Chip on their mobile phones. For it to be the go-to place for them to save, invest, manage their money, and, eventually, leverage that joint community power to buy insurance and access all sorts of other financial services,“ says Rabin.

And the rate it’s going, he’ll crack it.