ADVISORS MAY 2022 ISSUE 108 magazine FINANCES: Make it a Family Affair CRYPTO REGULATIONS 5 TACTICS TO BOOST RETIREMENT STRATEGIES THE PROS & CONS thomas lee WALL STREET ANALYST WORRIED ABOUT MARKET VOLATILITY? DON’T BE.

VION Receivable Investments, headquar tered in Atlanta, Georgia, is an international provider of receivable investment ser vices to businesses managing consumer and commercial receivables VION provides a single , comprehensive source of exper tise in commercial receivable factoring and consumer receivable purchasing, valuations, and process consulting VION Receivable Investments 400 Interstate North Parkway Suite 800 Atlanta, GA 30339 877.845.5242 phone 678.815.1557 fax Mesquite Corporate Center 14646 N. Kierland Blvd. Suite 122 Scottsdale, AZ 85254 480.729.6419 phone 866.260.1826 fax 123 North College Avenue Suite 210B Fort Collins, CO 80524 877.845.5242 phone 970.672.8714 fax 11921 Freedom Drive Suite 550 Reston, VA 20190 703.736.8336 phone VION Advisory Services 18017 Chatsworth Street Suite 28 Granada Hills, CA 91344 818.216.9882 phone 818.891.8738 fax VION Europa Paseo de la Castellana 95-15 (Torre Europa) Madrid 28046 Espanha +34 91 418 50 88 phone www.vioneuropa.es Atlanta • Phoenix • For t Collins • Reston • Los Angeles • Madrid RECEI V ABLE INVESTMENTS

Headquartered at: 2598 E. Sunrise Blvd., Suite 2104, Fort Lauderdale, Florida, 33304 (718) 675 4060

Advisors Magazine is published bi-monthly and printed by Magcloud, Inc. Reproduction of any material from this print issue or our digital issue or transmitted in any form of by any means without prior written consent of the publisher in whole or in part is strictly prohibited. ©2022 by Advisors Magazine. All rights reserved.

For a free digital subscription email: editorial@advisorsmagazine.com To obtain a print issue, visit: www.magcloud.com/user/advisorsmagazine

ADVERTISING lsubasic@advisorsmagazine.com

QUESTIONS & COMMENTS info@advisorsmagazine.com

ADVISORS MAGAZINE / 3

LETTERS TO THE EDITOR editorial@advisorsmagazine.com

CEO & Publisher Managing Editor Editor-in-Chief Writer-at-Large Billing Creative Director Business Reporter Feature Writer Senior Feature Writer Feature Writer Business Reporter Ty Young, Gabriella Kusz, Mark

Chris Morgan, Tim Sheehan

& GUESTS

ADVISOR MAGAZINE PUBLICATION @advisors.magazine @advisorsmagazin @advisorsmag

Erwin E. Kantor Michael Gordon Jude Scinta Lucas Rivera Eric Daniels Sean Rome Robert Jordan Regina Johnson Joe Innace Bill Millar Harold Gonzales

Zinman,

CONTRIBUTORS

AN

30 contents may 2022 10 Worried About Market Volatility? Don’t Be. Peace of mind is just a click away. 42 Cryptocurrency Regulations Implementing financial regulation and compliance 6 Finances Should Be A Family Affair Avoid financial issues later 44 5 Tactics to Boost Retirement Strategies Too many people rely on their company 401(k)s or IRAs for retirement income, the reality is that simply contributing to these vehicles is often not enough to save for retirement. 18 Interview with top-ranked Wall Street analyst and Fundstrat Global Advisors founder Thomas Lee Taking Care of Others 26 ADVISOR INTERVIEWS Keeping Employees Happy 30 MADE FOR YOU Our picks from the around the globe 36 Simplifying 401-k’s for Success 34 Relationships Fuel Freedom to Invest 38 4 / ADVISORS MAGAZINE MAY 2022 18 10 42 The heart of financial planning Figuring out what they want Due diligence and approachability are vital More tools today than ever before features ON THE COVER THOMAS LEE

By Regina Johnson

By Regina Johnson

Finances: A Family Affair Avoid Financial Issues Later

As of April 22, over 70 million people used tax professionals to file their individual tax return forms and over 62 million people self-prepared their taxes, according to statistics from the Internal Revenue Service.

Regardless of how you submitted the forms, Mark Zinman, managing partner at Pennsylvania-based Zinman and Company, a full-service accounting and advisory firm, encourages his business clients to include family members in tax preparation meetings.

“While the goal of the tax preparation meeting is to prepare the returns and ensure they are in compliance with all federal, state, and local regulations, it also provides an opportunity to educate family members and prepare them for the future,” Zinman told Advisors Magazine.

When Zinman and his team meet with clients, they focus on a variety of financial issues such as estate and retirement planning, savings, funding education, life and disability insurance, as well as the clients overall financial goals.

If the client happens to be a family business, the meeting is an opportunity to discuss transition and succession planning. It serves as an opportunity to discuss the vision the client has for their company and for family

members to learn how they fit into that vision going forward. These meetings are also a good time to identify any areas of conflict and proactively work to resolve them, according to Zinman.

But the meeting with family members shouldn’t be a oneoff, according to Zinman.

“By having these meetings regularly, family members feel informed and included, and it is an important step in aiding our clients so that their legacy remains intact for future generations,” he said.

It’s been the experience of Chris Morgan, vice president and senior portfolio manager at Floridabased Members Trust Company, that meetings with family members can help avoid confusion about finances.

Morgan’s advice, share even the basic details of finances with family members because sometimes assets are spread between multiple banks, credit unions, and brokerage departments. This information would help avoid discrepancies in knowledge about financial affairs between the person

primarily responsible for the family’s finances and the rest of the family.

“A common solution is to simplify the family’s financial situation by consolidating assets to a trust company such as MTC, where those insurance limits are irrelevant given that our client’s balances could not be compromised in any amount if MTC were to become financially insolvent,” Morgan told Advisors Magazine.

The team at MTC asks simple questions about the involvement of various family members because those members will feel a greater sense of ownership, understanding, and engagement when the time comes to become stewards of those assets for the family, according to Morgan.

MTC often partners with advisors and trust officers at credit unions to offer trust and investment services to credit union members. The growth in MTC’s assets under management from about $50 million in 2004 to over $4.3 billion today is due to clients consolidating their assets to MTC over time.

Perhaps there is no better time to talk about a family’s finances

6 / ADVISORS MAGAZINE MAY 2022

given the recent Gallup poll that found Americans are more pessimistic about their finances thanks in part to rising inflation and higher energy costs.

Forty-six percent of U.S. adults, down from 57% last year rate their financial situation as either “excellent” or “good”

while 38% describe their financial situation as “only fair” and 16% describe it as “poor”, according to the Gallup poll released April 28.

Thirty-seven percent say their financial situation is getting better while 48% say it’s getting worse, according to the poll.

Gallup, a global analytics firm surveyed 1,018 adults aged 18 and older living in all 50 U.S. states and the District of Columbia. The findings are from Gallup’s annual Economy and Personal Finance poll that was conducted April 1-19, 2022.

ADVISORS MAGAZINE / 7

Everest Consulting is a management and growth strategy consulting company that focuses on advising consumer branded lifestyle companies, from Fortune 500 companies to mid-sized organizations. With over 25 years of operating management expertise, Everest Consulting provides the industry expertise along with the strategic and operational know how to help your brand achieve its fullest potential.

Everest Consulting is a management and growth strategy consulting company that focuses on advising consumer branded lifestyle companies, from Fortune 500 companies to mid-sized organizations. With over 25 years of operating and management expertise, Everest Consulting provides the industry expertise along with the strategic and operational know how to help your brand achieve its fullest potential.

www.everestconsultingcompany.com

www.everestconsultingcompany.com

Actionable

Breakthrough Strategies

www.everestconsultingcompany.com

feature written by: joe innace

WORRIED ABOUT MARKET VOLATILITY?

10 / ADVISORS MAGAZINE MAY 2022

BE.

DON’T

Peace of mind is just a click away.

ADVISORS MAGAZINE / 11

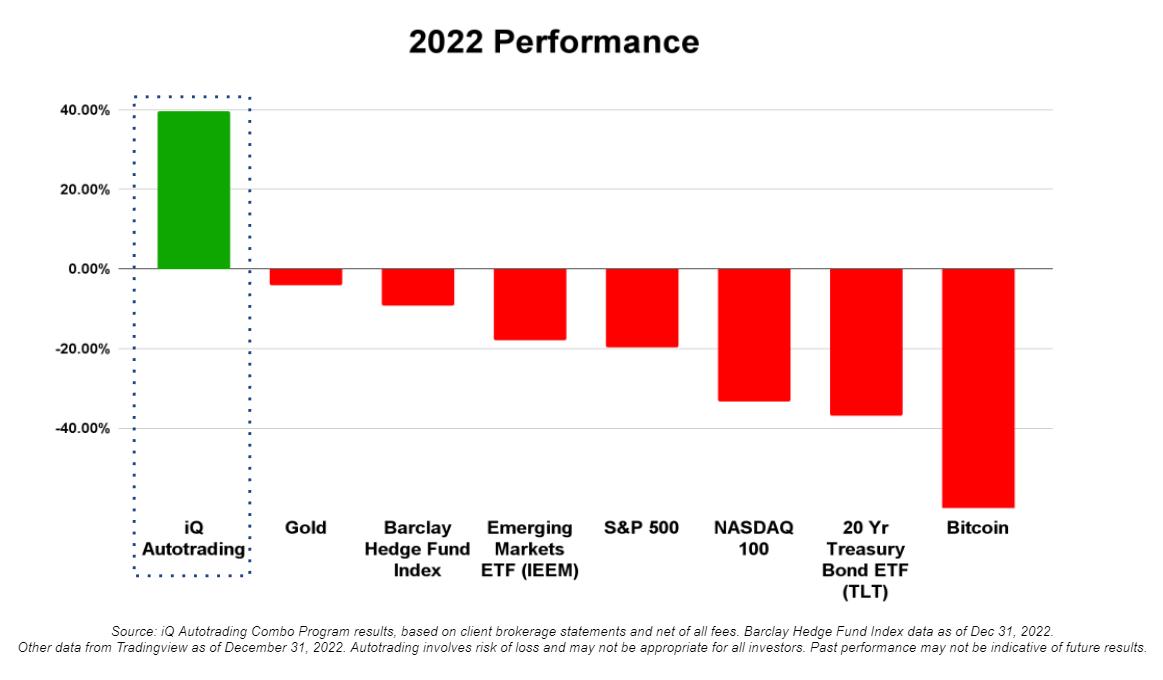

“I got crushed personally, as well as friends and family and nearly everyone in the equity markets, back in 2000 when the dotcom market crashed,” Scott Andrews, CEO and co-founder of InvestiQuant told Advisors Magazine in a recent interview. “Almost everything sold off; virtually any combination of stocks, bonds, ETFs, funds, commodities, emerging markets,” he continued. “No matter how well-diversified people thought they were, most got crushed.”

Andrews said his firm coined the phrase ‘crisis correlation,’ and it’s at

the heart of his business, which has been providing statistically-based diversification and autotrading solutions to investors and traders since 2008. No software or programming is required. Clients can have their broker’s system trade Andrews’ strongest signals in their accounts for them.

The factors behind crisis correlation and the reasons why most assets tend to sell off during times of market stress is well known by many people in the financial planning/investment advice industry. But for Andrews’ InvestiQuant, it’s a

passion.

“We love to connect the dots for people around this whole phenomenon,” he said, emphasizing, “Crisis correlation is real and it’s something you need to think about, and plan for. If you wait until you’re getting hammered, it’s probably too late. Plus, it’s a tremendous opportunity for the prepared investor.”

The key is to diversify your portfolio with a solution that can take advantage of volatility in an manner that is uncorrelated with equities, according to Andrews. In his view, the best solutions are short-duration or short-term active investment programs, similar to what his business provides.

A devastating setback led Andrews on a path to becoming a crisis correlation expert and to founding InvestiQuant. Some 22 years ago, just prior to the DotCom Crash, he was CEO of a public tech company trading on the NASDAQ exchange. His portfolio was heavily weighted in his own company, and he also held stock in other leading technology companies like Intel, Amazon and Ebay. At its peak, Andrews says his portfolio was worth more than $50 million. Only in his thirties, he thought he had made it.

The war in Ukraine. The pandemic. The subprime mortgage crisis. The DotCom bubble bursting. These are all crisis events that created varying degrees of market volatility. They are painful, unforeseen times when investors tend to seek safe havens — but often no asset class is safe. And such events have given rise to a financial planning and investing concept known as crisis correlation.

feature

12 / ADVISORS MAGAZINE MAY 2022

Scott Andrews InvestIQuant CeO and CO-FOunder ADVISORS MAGAZINE / 13

But then came the DotCom crash and within two years his holdings were decimated. The NASDAQ plunged 80 percent, to a level virtually no one had fathomed. “I went — in what felt like one day — from being completely set for the rest of my life, to feeling like I had been kicked in the gut,” Andrews recalled.

He said the worst part was the collateral damage on family and

SCOTT ANDREWS

friends whom he had urged to get heavily invested in the stock market. He had encouraged them to load up on technology stocks because it was obvious the internet was about to change everything.

“It destroyed the hopes and dreams of a lot of those closest to me,” Andrews lamented. “It was a really, really rough time that few saw coming; the market had been rising for five, six years in a row.”

Fortunately, his company did survive but valuations did not. Never again would he be “all in” on stocks and just rely on a buy-and-hold strategy. So, he went in search of ways he could put his money to work that could avoid the catastrophic selloffs. Over the next few years, Andrews found hedge funds to be viable solutions, but they required large minimum investments and had long lock up periods.

Seeing the need and the opportunity, he decided to take matters into his own hands. After stepping down as CEO, he immersed himself in a markets ‘deep dive,’ learning everything he could. Andrews eventually joined forces with a partner, a classmate from West Point and the original software developer of his first company, who had similar interests.

“He and I started building systematic trading strategies on the index futures markets,” Andrews said. “We wanted to build a diverse basket of statistically-based strategies that could profit in both rising and declining markets.

He explained they migrated to intraday trading to maximize statistical significance and avoid overnight volatility. Realizing the looming threat and opportunity of the mortgage crisis in early 2008, Andrews began sharing his strategies and started a business called Master The Gap, which developed quite a following and morphed into InvestiQuant.com a few years later.

“We attracted a bunch of investors who wanted the same things we wanted: the ability to take advantage of market crises,” he said. “And our mission—our goal—was to help regular investors better protect and grow their investment portfolios in all market environments.”

After helping clients successfully navigate the financial crisis, some urged him to automate his strategies

“WE ALL SAW THE OPPORTUNITY TO TAKE THIS TO THE MASSES BECAUSE EVERYONE NEEDS PROTECTION FROM VOLATILE AND DECLINING MARKETS.”

Money Show: The International TradersExpo

14 / ADVISORS MAGAZINE MAY 2022

and turn it into a bigger business. He ended up raising about $3 million in outside equity capital and collaborating with Duke University’s Center for Quantitative Modeling.

“We saw the need for this on ‘main street’ because black swans and bear markets are impossible to predict and most investors are not diversified enough to weather the storm during a recession,” he said.

The company name was changed to InvestiQuant in 2015 and its infrastructure and technology made more robust. “We had to build out and automate our solutions if we were to help the masses,” Andrews said, “that was the key.”

A bidirectional automated system

As for the process, a client will open an account with one of In-

vestiQuant’s specialized execution brokers. “In this scenario, we are the signal provider, and the broker oversees the automated trading of our strategies in the client’s account for them,” Andrews explained, noting that InvestiQuant does not have access or visibility to the client’s account or funds.

“What this means is when our strategies trigger, the broker electronically executes and monitors the trade on behalf of every subscribing client’s account until it is finished, which is always by the end of the day,” Andrews explained.

“It’s an elegant solution. Every account gets traded exactly the same. The only difference is the funding and trading level used by each,” Andrews said. “Whatever happens in my personal account

also happens in every client account simultaneously. And no account is ever exposed to overnight risk or surprises, which provides a lot of peace of mind.”

The bidirectional nature of their strategies to go long or short, Andrews noted, is designed to take advantage of market selloffs, while also reducing correlation with buy and hold investments.

“Our strategies have a long history of outperforming equities during turbulent periods and a client doesn’t have to do anything other than set up an account and monitor it from time to time,” he said. “The broker helps them with client support, moving funds in and out, and so on. We just focus on the strategies. So, it’s really a win for everyone in that regard.”

iQ ADVISORS MAGAZINE / 15

CEO Scott Andrews monitoring InvestiQuant’s automated trades

What’s more, Andrews’ clients never lose visibility of what’s happening with their money.

“With every client account, they can actually see what’s going on day to day,” he explained. “And they’ve always got access to it — 24/7 — it’s just a button click, and funds can be wired in or out.”

That’s a big selling proposition for

InvestiQuant.

“With the markets the way they are today,” Andrews mentions, “and with the internet, you expect transparency and there is no reason you should not be able to see exactly what’s happening at a given time. So, we’re able to fill that need as well—while providing real diversification and a growth opportunity.”

In fact, Andrews says his company is seeing a high level of what he describes as “grassroots” interest – especially from sophisticated investors, family offices and retail firms.

InvestiQuant’s algorithmic strategies are constantly monitoring massive amounts of market data. Some 1,000 factors are considered every day and fed into its system, so the company’s program trades only opportunities that meet its strict performance criteria. Targets and stops are automatically tailored for the current conditions.

“We love market volatility because typically that’s when we do best,” Andrews added, “But it’s also important for compliance teams to know that people in an ivory tower are not making the decisions that drive the program; these are all fully automated, statistically based, updated every single day, and adapting to changes in the market as they happen.”

There is also a risk management filter for times of excessive volatility, when there is a lack of historical market data that can be studied, or the

risk required is beyond tolerances. In short, the program automatically reduces the daily risk level until more suitable conditions return.

“The algorithms actually ‘selfpaused’ briefly during the pandemic,” Andrews recalled. “As a trader, I was somewhat disappointed because I wanted the algos to keep trading. But we couldn’t risk capital when the data was not supportive.”

Turned out, the algorithms made the right call—all automatically, objectively, and unemotionally.

“That was a huge advantage for everyone involved — the algos side-stepped the most extreme of the market instability and then turned back on to take advantage of the residual volatility,” Andrews said. “And in that [pandemic] envi-

ronment, volatility was much higher, and we had a fantastic year.”

He emphasized: “So, that’s how we manage risk. We’re doing everything statistically based. Our program only trades when it sees a mathematical edge based upon robust analysis of contextually similar scenarios.”

Said another way: sit back and let the crisis correlation begin.

For more information, visit: InvestiQuant.com

16 / ADVISORS MAGAZINE MAY 2022

L/R: Founders Scott Andrews & David Skowron

by joe innace

by joe innace

TOP-TIER INVESTMENT RESEARCH FOR THE MASSES

Tom Lee’s FSInsight delivers

Anyone tuning into CNBC, Bloomberg, Fox Business or following the markets in the major financial press has most likely seen or read about Tom Lee. He founded New York-based Fundstrat Global Advisors in 2014, after more than 20 years and having received numerous accolades as a Wall Street strategist with Kidder Peabody, Saloman Smith Barney and J.P Morgan. Most recently, in 2020, he launched FSInsight as an offshoot company of Fundstrat.

feature cover

feature cover

18 / ADVISORS MAGAZINE MAY 2022

ADVISORS MAGAZINE / 19

While Fundstrat serves more than 250 institutional clients around the world, FSInsight is a subscription-based service focused on delivering top-level research to registered investment advisors (RIAs), family offices and individual investors. FSInsight has grown quickly in two short years by offering smaller firms and individuals a reasonable price point for the type of quality investment research usually reserved for major banks and hedge funds.

“We’re an independent boutique investment research firm that make clients feel we’re on their side,” Lee told Advisors Magazine in a recent interview.

“Being independent means that we can be a hundred percent unconstrained in our views,” he added. “We don’t trade or have any funds; our business is purely research advice, allowing us to be aligned completely with our clients.”

And that’s very comforting to Lee, who acknowledges that he is able to sleep soundly—which is also the

unstated mission of FSInsight.

“I love when I hear that we’ve made a client feel smarter, or that we’ve taken the anxiety out of the market for them,” he said. “Because the stock market can make people so anxious, and we just want them to sleep at night—to trust that their money is going to work for them. To me, that’s probably the most important service we can provide—allowing people to be confident about investing.”

An evolving research perspective

Lee grew up in the Midwest and received his BSE from the Wharton School at University of Pennsylvania with concentrations in finance and accounting. His first job on Wall Street was with Kidder-Peabody in 1993 and he was designated as the firm’s wireless industry analyst.

And as a wireless industry analyst, he had a number of epiphanies that prompted him to view the sector differently than most other equity analysts.

Lee recalled that in the early

1990s, wireless was a fast-growing technology business, but with a very uncertain future. He said that there were just 34 million cell phones around the world in 1993. The wireless companies were not in a strongly capitalized position, and they were operating in a telecommunications market favoring the likes of AT&T.

“Most analysts covering the wireless industry thought the future was bleak,” Lee said, “because they thought cell phones would only become extended cordless phones as part of the traditional telecoms sector.”

Lee was young—in his twenties— compared to most equity analyst peers in their 40s. As such, he came to view the wireless industry very differently.

“I saw how it made communication with my friends,” he said, “how it improved our social lives dramatically.”

He explains that most people at that time still left voicemails on home answering machines. They

20 / ADVISORS MAGAZINE MAY 2022

played phone message tag when wanting to get together on weekends, for example. Payphones were still around.

But this new wireless cell phone technology also allowed the sending of text messages in addition to voice calls and messages. And today, that’s how virtually everyone connects and meets up.

“I came to see wireless as being far more transformational,” Lee said, who continued to cover the wireless sector from 1993 through 2007—and has been consistently top-ranked by Institutional Investor magazine every year since 1998.

Reflecting today on those early years, Lee told Advisors Magazine of two major lessons learned.

“A big lesson I learned from my time doing wireless is that the world is driven by young people,” he said.

Lee explains that most businesses are created by those between the ages of 20-40. They are the ones

coming up with new ideas, disrupting established players. Social media is another great example. Initially, most people in their fifties thought Facebook, Twitter and more recently TikTok were silly ideas.

“So, as an analyst and a Wall Street strategist, I’ve learned to look at a growth industry through the eyes of someone 20 years old,” Lee said.

His second big takeaway from that early experience was how important credit markets are to funding equities. At that time, wireless companies didn’t make money. But they were borrowing a lot of capital, and they were viewed as having a number of valued positives.

“They had subscribers and the network,” Lee said, “And I realized that the credit markets were generally a good leading indicator for stocks.”

Those two important takeaways

paved the way for Lee’s successful career. By age 28 he had been ranked by Institutional Investor as a top analyst—a rare, young age for such recognition. In 1998 he joined Salomon Brothers and was named their youngest research managing director ever at age 29.

The fuel for Fundstrat and the

FSInsight genesis

Lee’s years at Salomon and surging reputation as an equity strategist led to his joining J.P. Morgan as a managing director. It was while at J.P. Morgan that the idea for Fundstrat was first hatched.

“J.P. Morgan is a great place,” Lee said with fondness. “But while there, I was realizing that I was about 45 now and hadn’t started an independent business—and my chances of ever doing so were slim. I decided I wanted to start my own business.”

In effect, the early lessons as a

ADVISORS MAGAZINE / 21

ADVISORS MAGAZINE / 21 March 9, 2022 Slide 13 2022: Better 2H… YE S&P 5,100 For Exclusive Use of Fundstrat Clients Only Source: Fundstrat, Bloomberg -5% -5% -4% -4% • COVID surges • Supply chain glitches • Labor shortages

Fed “liftoff” • Midterm elections -10%

S&P 500 5,100

•

• Inflation flattens out • Labor tightness eases • Fed “bandaid” pulled • Midterms done COVID better

wireless analyst drove that decision. He believed that business growth was largely fueled by young people and that most new businesses are started by those in their twenties through forties.

In 2014, Fundstrat Global Advisors was created as an independent research boutique and based in New York. Its third-floor office today is located at 150 East 52nd Street.

Fundstrat was founded to serve a broad array of clients, including institutional investors, wealth advisors, pension funds and high net worth individuals. Its mission was and remains to provide the best fundamental, technical and quantitative research with the top priority being clients’ needs and interests.

The approach is data intensive and, as noted on the website www. fundstrat.com, the company “seeks to exploit anomalies to identify sectors and stocks we feel should outperform the market. Our tools are aligned with this focus and helps our clients to make better informed decisions.”

The focus is on delivering analysis, not opinions. And as an independent research provider, its clients are assured that Fundstrat’s work is tailored to provide fresh and innovative intelligence to aid in their investment process.

In fact, Fundstrat is considered by the media to be among the first ma-

jor Wall Street firms to actually write about cryptocurrencies, according to Lee, who initiated its crypto research in 2017. “We were one of the first to see crypto as a new emerging growth industry that Wall Street would care about,” he said.

“From the start, the Fundstrat business did well,” Lee said. “We noticed we kept getting a lot of inquiries from folks that were family offices or RIAs who wanted to have access to our research—but it was too expensive for them because Fundstrat was priced as an institutional service.”

The decision was made to create a second unit, now known as FSInsight, as the more family office/ RIA-friendly enterprise. It was launched in 2020.

“Instead of having a dense and technical research product, we made it a lot more user friendly,” Lee noted. “And we provide sector-investing recommendations as part of a very comprehensive product.”

As for the FSInsight leadership team today, Lee oversees the macro market research work. Head of Technical Strategy is Mark Newton, CMT. The Washington Policy strategist is Tom Block, the former head of government relations at J.P. Morgan. Adam Gould, CFA, is on board as a quantitative strategist. Brian Rauscher, CFA, leads Global Portfolio

Strategy and Asset Allocation.

“On top of all that expertise, we actually have a crypto and digital asset research group,” Lee said. Sean Farrell heads that team.

“So, it’s a very comprehensive set of services and we have now about 27 research professionals full time,” Lee added.

“The FSInsight clients feel like we’re giving them an extremely high-quality service that really helps them level the playing field,” Lee said, explaining, “We’re equipping them with a lot of the information that institutions get, but in a way that they can easily access.”

The FSInsight website, www.fsinsight.com, is a subscription-based service, and the top tier of access can be provided for about $2,500 per year, according to Lee.

The original Fundstrat, with its institutional research, is a negotiated contract service and the level of tailored work and customized engagement can vary, depending on the institution’s needs.

Tom’s Takes

Lee’s verified Twitter account shows he’s jovial and armed with a sense of humor. His handle is: Thomas (Tom) Lee (not the drummer) FSInsight @fundstrat.

Advisors Magazine found the same during our recent interview with him. He touched on a number

22 / ADVISORS MAGAZINE MAY 2022

of current market and economic conditions, providing his perspectives:

• On the general U.S. economy…

“I see the underlying economy as still quite strong. There is a lot of excess savings and pent-up demand, and COVID restrictions are ending. I don’t think the economy is busted. I think we’ll eventually emerge from this malaise stronger.”

• On the stock market…

“I think the stock market is in no man’s land at the moment. (Ed. Note: Interview was conducted April 7) “It’s consistent with our research view for this year. We advised clients in December that the first half of 2022 would be treacherous and for all the obvious reasons—the supply chain issues, risk of further inflation, and the Fed’s expected actions. More recently the war in Ukraine amplified all these things. So, until the markets have either discounted in the worst case, or things start improving consistently, stocks are a bit stuck.”

• On President Biden’s recent digital asset executive order…

“It’s really a sign of further legitimizing [crypto]. I think once the rules are fully established, that will open the door for banks and companies

to really start plumbing into crypto. And once that happens, then the number of people who use crypto will grow and the amount of crypto as part of commerce in the U.S. will grow.”

• On Bitcoin reaching a value of $200,000…

“Looking at Bitcoin’s value, 97 percent of its price can be explained by just the number of wallets and the activity per wallet; Since 2009, there is a 97 percent correlation between those two variables. If those two variables hold, then Bitcoin could easily get to $200,000—not anytime soon, possibly in 12 to 18 months, with a lot depending on how rules and regulations are properly put together.”

• On what investment to avoid…

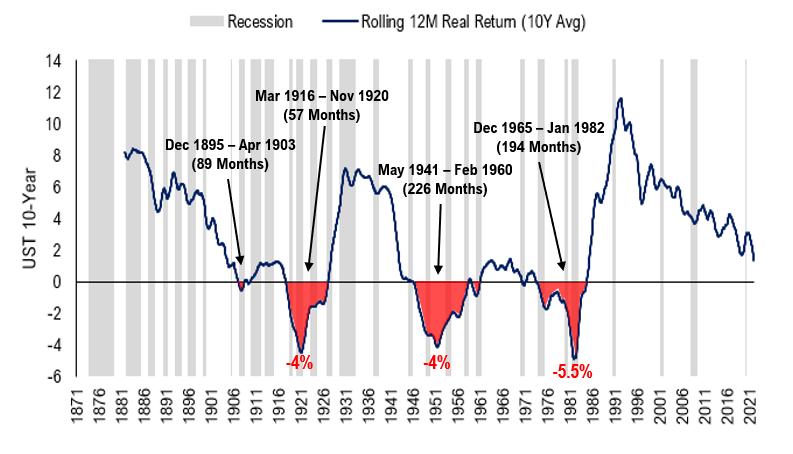

“If the CPI over the next two years averages 6 percent, you are going to lose money within your bonds. That’s because the nominal yield needs to be pricing in a real return plus inflation. Even with investment-grade most people aren’t going to make money.”

• On recommended equity sectors…

“Our favorite sector last year was energy and that remains our favorite sector in 2022. We think energy equities are still attractive because

there’s a positive tailwind for oil. Also, the equities themselves are underpriced because they’re not discounting for current oil. So, we think there’s a pretty big runway for the energy stocks.”

• On other stocks…

“In the second half of this year, we think the FAANG group of stocks (Facebook, Amazon, Apple, Netflix, Google) is going to be pretty attractive. Because once the worst is priced in, investors in the second half will want to find companies that can grow faster than GDP on a real basis, that have good margins and reasonable P/E ratios. And I think they’re all going to notice and say, for example, ‘You know, Facebook has like a 16 PE right now.’ And I think investors will come back to such stocks.”

• On the crypto sector overall…

“We like crypto. It’s a little bit tied to NASDAQ, but it’s an industry that still has a huge growth ramp in front of it. There will be a lot more penetration, a lot of new services. The actual revenue opportunity is quite large and it’s an under-owned space.”

In fact, Lee and the team at FSInsight produce a quarterly report titled ‘Granny Shots’, which are investment stock picks that aim to outperform the S&P 500.

“It’s a list of 31 stocks that commonly appear in fixed portfolios,” Lee explained. “We run these thematic and quantitative portfolios and the ones that appear the most become our Granny Shots. For four years now it has outperformed the S&P, and this year it’s outperforming by 275 basis points.”

In a nutshell, Lee is confident about the markets and the economy going forward.

“I’m slightly more positive now because I think we’ve just front-loaded so much of the bad news already this year,” he summarized.

ADVISORS MAGAZINE / 23 March 9, 2022 Slide 32

Source: Fundstrat, Bloomberg, Robert Shiller Online Data Figure: Rolling 12M Real Return of

10-year 10-year moving average

“guaranteed” TINA: Bonds lose money when inflation rises

UST

For Exclusive Use of Fundstrat Clients Only

INSIDE FSINSIGHT

The available research and tools for subscribers

Tom Lee’s motivation for co-founding New York-based FSInsight is to provide top-tier Wall Street research to individuals, family offices and registered investment advisors, which is usually only available to hedge funds and banks. Armed with a wealth of data analysis, graphs and charts in a user-friendly format and presented in clear terms, subscribers can better make their own investment decisions.

As such, it’s helpful to understand he and his team’s approach to research and analysis.

So, during the interview with Advisors Magazine, Lee shared FSInsight’s evidence-based research mantra, which was also presented in its 2022 outlook to clients.

“First, there is nothing new under the sun; it’s important to look at cycles,” Lee said. “Next, equities are the junior in the capital structure and bonds lead stocks.”

He added: “We don’t shout at the market; the market doesn’t care about our opinion. Also, it’s vital to avoid cognitive bias, so stop carrying a ‘Lehman hammer.’”

Another key to the mantra: confidence drives markets. “Confidence changes faster than fundamentals,” Lee said. “And demographics are destiny—every market cycle is a demographic cycle.”

Lastly, don’t fight the Fed. “The Fed is the most powerful entity in the world,” Lee emphasized.

“So that's kind of how we live with the world,” he said. “We're trying to be as objective in a market that makes people very emotional.”

Those tenets underpin the range of available research from FSInsight, which includes:

• Macro Research—Timely and actionable investment insight and strategy

• Crypto Research—Industry leading, dynamic perspectives on digital assets

• The FSI Academy—No matter an investor’s skill level, the research team provides educational guides

• A COVID-tracking Map—reports all COVID-19 cases in the United States on a state-by-state basis

• Onboarding phase—All research reports are

fully explained to help investors navigate the financial markets

• Community Activities—Subscribers become part of the full FSInsight community and can participate in a range of fun activities

What’s more, there are regular updates on stocks, including:

• Brian’s Dunks—The latest stock list regularly researched and presented by Brian Rauscher, FSInsight’s head of Global Portfolio Strategy and Asset Allocation. The selections are based on an established quantitative model used by leading institutional investors.

• Epicenter Stocks—A compilation of the most robust companies closest to economic and social consequences of COVID-19.

• Granny Shots—The equities selected for their congruence with the long-term thematic strategies that FSInsight sees influencing markets.

• FSI Sector Allocation—More perspective from Brian Rauscher in which he shares his sector allocation strategy to help investors outperform the market.

• Signal From Noise—The team spotlights a stock or ETF each week, presenting investment opportunities through the lens of their research.

22 / ADVISORS MAGAZINE MAY 2022

By Advisors Staff

Attorney Advertisement Elite N.Y. attorneys with over 40 years of combined experience! P: (914) 686-1500 • M: (914) 686-1504 E-mail: russell@yankwitt.com Please visit us a: www.yankwitt.com The Law Office of Civil | Commercial | Financial Securities | Healthcare 140 Grand Street, White Plains, New York 10601

TAKING CARE OF OTHERS

The HEART of financial planning

In his State of the Union address on March 1, President Biden made an appeal to end the nation’s political divisions inflamed by COVID-19 safety restrictions. “We’ve lost so much in COVID-19 — time with one another and, worst of all, much loss of life. Let’s use this moment to reset,” Biden said. “So stop looking at COVID as a partisan dividing line.”

After nationwide masking-versusunmasking and vax-

versus-unvax debates, Biden’s underlying message was that it’s high time to show some caring and respect for each other. In fact, many people insist that beyond the politics, the pandemic has shown some of the best of humanity.

One of those people is James Rukstalis, president, CLU, ChFC, CFP® at J.R. Financial & Insurance Services in Santa Clara/San Jose, California.

“When the pandemic first happened, our first

focus wasn’t actually on reaching out to our clients,” Rukstalis told Advisors Magazine in a recent interview. “It was to make sure our staff felt safe.” And the county’s mandatory quarantine affected them all.

“We made a personal commitment—and every employee knew—that no employee would be terminated during the mandatory quarantine,” he said.

Everyone could rest easy that their jobs were secure. “We would all figure it out together,” Rukstalis noted, adding, “We sent weekly gifts to our staff, and we even did some fun team building by setting up

TALK

EMPLOYEE

"IT IS LITERALLY TRUE THAT YOU CAN SUCCEED BEST AND QUICKEST BY HELPING OTHERS TO SUCCEED."

— Napoleon Hill

By Joe Innace

INTERVIEW 26 / ADVISORS MAGAZINE MAY 2022

James Rukstalis, CLU, ChFC, CFP®

a weekly Dungeon & Dragons meeting to keep up the morale.”

Such an approach reflects a personal credo of Rukstalis: If you take care of others, you’ll be taken care of as an entrepreneur/business owner.

“It’s not just about trying to maximize profit,” he explained. “First and foremost, it’s about taking care of people, taking care of staff, and taking care of your clients. As long as my focus is truly on helping people—my staff, my clients— everyone will be better off and that’s a win-win situation.”

With J.R. Financial & Insurance Services’ staff reassured and upbeat at the outset of the pandemic, they could then turn their attention to putting clients’ minds at ease and providing better service.

Like most financial planning practices before the pandemic, Rukstalis and his team met with clients in person at the office. Most of the firm’s clients are in California, but clients are also situated in several other far away states like Florida, Ohio, Minnesota, Washington and Texas. “Getting signatures, even a simple initial, created big hurdles for our clients that lived far away,” he recalled.

Regarding clients who were concerned about the stock market’s massive drop when COVID-19 hit, J.R. Financial & Insurance Services called them, but also adopted the technology and tools to connect with clients everywhere in an ongoing manner— using things like video conferencing as well as DocuSign.

“This streamlined the

business,” Rukstalis said. “It made it really easy to meet clients anywhere; no one had to leave their homes. It allowed us to reach out to more clients and respond to issues much quicker.”

There is no minimum investment required by J.R. Financial & Insurance Services – and the reason why is simple.

“I believe that everyone deserves financial planning, and everyone needs financial planning,” Rukstalis emphasized. “We believe in taking a broader view of someone’s estate to

identify clear goals for our clients’ wants and desires.”

Rukstalis’ own specialties include planning for retirement, setting up guaranteed retirement income, estate transfer planning, FERS & CERS Governmental planning, and planning social security strategies.

He has worked with individuals from all types of professions including federal employees, Bay Area Rapid Transit, Kaiser, San Jose State teachers and football coaches, Cal Berkeley football coaches, and

James Rukstalis, president, CLU, ChFC, CFP® at J.R. Financial & Insurance Seminar

ADVISORS MAGAZINE / 27

James Rukstalis, CLU, ChFC, CFP® / J.R. Financial & Insurance Seminar

several San Francisco 49ers.

“We don’t want to simply help people with lessons,” he stressed. “We want people to succeed in their planning. Our goal is to help clients reset their own potential and the life they could be living, rather than being handcuffed to their investments and current circumstances.”

Far more than lessons, education is a major aspect of the work done by J.R. Financial & Insurance Services.

One of his clients is a doctor, surgeon and a professor at Stanford University, and Rukstalis is astounded by the fact that through all his client’s training and experience, from childhood through the doctorate level, he has never once had a required financial course.

In fact, when considering the growth of online trading platforms, handheld investing apps, and robo-advisors along with a general lack of financial knowledge, Rukstalis said: “Without understanding finance, all the tools in the world aren’t going to help you.”

He acknowledges that the more information someone has, the better decisions they will make.

“And if someone

is structuring a plan for their financial life and future, the right investments tend to make themselves known to the client as the best available options,” Rukstalis said.

He also doesn’t think anyone should be pressured to invest in anything.

“I find that there is rarely a strong sense of urgency to do something right away,” Rukstalis observed. “I think the most important thing to do is figure out their plan and for how they want to live their life. It’s important that before anyone makes a decision to move forward, that they evaluate all of the available options and understand the benefits and drawbacks of each.”

Every J.R. Financial & Insurance Services client gets a custom-built report for their estate because, as Rukstalis says, no two estates are alike. “We also do a custom laddering plan to structure retirement income,” he said.

Over the last year, the company has expanded and doubled in size. The office is now more than 6,000 square feet, and four new hires are planned for this year. Recently hired was a director of education. There will be an emphasis on podcasts and webinars

as marketing tools. Rukstalis said, however, the role of the director of education is to actually go out into the community and provide pro bono education to local schools.

more information visit: www.jrfis.com

Investment advisory services and financial planning offered through ESG Planning, a SEC registered investment adviser. J.R. Financial & Insurance Services and ESG planning are affiliated companies owned by James Rukstalis. This communication is in no way a solicitation or an offer to sell securities or investment advisory services.

28 / ADVISORS MAGAZINE MAY 2022

Peter Bradshaw & James Rukstails

For

We made a personal commitment—that no employee would be terminated during the mandatory quarantine. " "

Preserve your wealth with CitiTrust’s knowledge and Financial Management Solutions Belize | BVi | Malta | UK | SaMoa | BrUnei | BritiSh angUilla | CyprUS | giBraltar | iSle of Man | geneVa | JerSey | lieChtenStein | lUxeMBoUrg | United araB eMirateS | China | Switzerland | MarShall iSlandS international inc. www.cititrust.biz

THE KEY TO KEEPING EMPLOYEES HAPPY

Figuring out what they want

The pandemic and the labor market’s ensuing Great Reset have created upheaval for employees, businesses and the economy. On the plus side, claims for unemployment benefits across the United States clocked in at 187,000 for the week ending March 19, according to the U.S. Labor Department—the lowest level since 1969. Professionals, however, are losing 10 hours per week on unproductive tasks, driving stress among nearly 80 percent of U.S. employees, according to Reclaim.ai, the intelligent calendar assistant and time

management platform for Google Calendar used by over 9,000 companies worldwide.

“We’re living in a world of increasing demands, evershifting priorities and an unprecedented need for clear communication across teams, projects and organizations,” said Patrick Lightbody, CEO and co-founder of Reclaim.ai, in a statement released in late March 2022.

“We have to be happy at work,” Monica Siciliano, partner at De Novo HR Consulting told Advisors Magazine in a recent interview.

Siciliano and Mark Zinman, managing partner, joined forces in 2015 and created the Southampton, Pennsylvania-based HR firm. De Novo HR Consulting takes a comprehensive approach to analyzing the needs of a business and its employees, and then provides strategic, client-centric services.

Zinman’s experience is

30 / ADVISORS MAGAZINE MAY 2022

“It’s where we spend the majority of our waking hours,” she added. “being happy at work and being a high producer are not mutually exclusive.”

FEATURE BY JOE INNACE

in financial advising and accounting. Siciliano’s career has spanned from sales and marketing to human resources. Most of their business clients have fewer than 50 employees. Many are financial advice and money management/investment practices. Early on, Zinman found that HR was an especially important aspect of such businesses, as well as being critical in the area of compliance.

“But there really was no viable alternative for small businesses to obtain those kinds of HR services,” he said. “So, Monica and I developed a full-service HR company where we can use the expertise of the people we have, to provide services on an hourly basis to our clients.”

What’s more, financial services is an industry that reports higher job stress than others, according to Siciliano.

“As HR professionals we can help alleviate that mental burden in a few ways,” she commented. “First and foremost, we set aligned expectations of the team member or employee, their clients and the executive team.”

She maintains that when there are aligned expectations, the fear of missing those expectations dissipates. Open and transparent communication is also vital.

“There are many different data points out there, but the general consensus is that

around 70 percent of people in the financial services industry work remotely at least one day per week, if not more,” Siciliano said.

“This is all the more reason why we want to set those expectations—so that when they are not in the same environment with their peers or with their supervisor, they know and are comfortable with executing upon what’s expected of them.”

Not surprisingly, the key HR questions that De Novo is fielding currently are related to recruitment and retention. There’s been a lot of attention on the ‘Great Reshuffle’.

“As employees are seeking remote work, and as employers are embracing a distributed workforce either exclusively or via a hybrid model, flexible hours have become increasingly required by employees, and employers are learning that this doesn’t hurt the business.”

She emphasized that this work-life integration is the key challenge for both employers and employees.

“We really start thinking about these factors during the recruitment process,” Siciliano added, “because

ADVISORS MAGAZINE / 31

“SOME PEOPLE DREAM OF SUCCESS, WHILE OTHERS WAKE UP AND WORK HARD AT IT.”

Napoleon Hill

Since our inception, De Novo HRConsulting has remained focused on offering strategic, client-centric consulting services - and that means something different for each and every client.

support the employees’ needs while maintaining a strong and positive culture that expands the work environment into home offices.

our belief is that the employee experience starts during candidacy.”

She noted that such engagement can even continue after employment. Should a previous employee move on to alumnus status, they can still be a brand ambassador for their previous company.

It all boils down to employee happiness—and employers being able to get a handle on what makes them happy. In short, the business needs to know what the employee wants, and not everyone wants the same things.

Toward this end, De Novo advocates for something called the stay interview.

“Every six months,” Siciliano said. “all employees on the team are offered a stay interview. It allows us to find out what they want in their career development action plan, where they see themselves going professionally over the course of the next several years, and how to help them get there.”

Siciliano puts the emphasis on the word action. “It’s not just a career development plan, it’s an ACTION plan,” she said. “How do we actually implement—step-by-step— what we say we will do to help our employees grow?”

It’s up to the employer then to provide the opportunities and the mentoring for the employee to fulfill their goal. “For example, if someone aspires to be a manager, the employer should know that ahead of time and help them chart a career path,” she added.

Zinman points out that accounting and financial service advisory firms suffered the same as most other businesses during the pandemic—coping with an abrupt change in their ability to function and adopting new ways to run their businesses. Whether working entirely remotely or in some hybrid arrangement presents similar challenges.

“Remote work can make an employee start to lose touch with their peers and other coworkers,” Siciliano explained. “And some employees may start to feel socially isolated.”

She said it’s important for executive management to

“That requires some very different management techniques,” Siciliano said. “Regular and more frequent communication might be needed. Also very helpful are real-time reviews, real-time performance evaluations, as opposed to the more traditional, quarterly, semiannual or annual reviews.”

Another key HR topic for management nowadays is diversity, equity and inclusion, or DEI.

“A lot of companies are realizing the importance of DE&I and the financial services industry is among them,” Siciliano acknowledged. “I believe recent data indicates that about a third of C-level executives in the financial sector are female, so the industry remains one that skews male. Through awareness, acknowledgement, and training, we can incorporate DE&I initiatives into the workplace, attracting a more diverse candidate plus increasing revenue by attracting new and diverse clients.”

For more information, visit: denovohrc.com

32 / ADVISORS MAGAZINE MAY 2022

STILL PUZZLED

Streamlining supply chains throughout the automotive, retail, pharmaceutical, pulp & paper, logistic, and food industries.

Contact Meade Willis today for a free consultation regarding your e-commerce, EDI, supply-chain requirements: (866) 369-1146 | www.meadewillis.com

... by your supply chain solution?

www.meadewillis.com

By Joe Innace

SIMPLIFYING 401Ks FOR SUCCESS

Due diligence and approachability are vital

Much has been written recently about the wealth gap in the United States. The growth in income in recent decades has tilted to upper-income households, according to The Pew Research Center. “At the same time, the U.S. middle class, which once comprised the clear majority of Americans, is shrinking,” the Center noted in a 2020 report. “Thus, a greater share of the nation’s aggregate income is now going to upper-income households and the share going to middle- and lower-income households is falling.”

Financial consultants and advisors who understand the full income landscape are well-positioned, according to Stamford, Connecticutbased GGA Retirement. GGA Retirement is an experienced, independent consultant for 401(k) plans, serving as a 3(38)-plan fiduciary. In short, GGA provides wholesale 401(k) management services to other financial advisors, as well as 401(k) retirement plan management for employers.

It’s a division of Granite Group Advisors, a wealth management firm established in 2003.

“We look at both the normal and the uberwealthy,” Lyle Himebaugh, co-founder of GGA Retirement, told Advisors

Magazine in a recent interview. “This gives us ideas about what we should be doing for our clients. We don’t want to be complacent…if you are complacent, you are dead.”

Himebaugh said such conversations across the income spectrum help him to better manage his business.

In fact, Himebaugh says his firm is known for its due diligence—whether it be as a 401(k) consultant on the 3(38) side to other financial advisors and employers or serving its private clients.

“We speak directly to the portfolio managers, whether it’s a mutual fund or a separate managed account,” he said. “We look into the eyes of the manager

to make sure that we are understanding their investing philosophy,” Himebaugh added. “It really makes a big difference when you do real due diligence that is 25% quantitative, and 75% qualitative. So, we concentrate on making sure that the manager does what they’re supposed to do so we can allocate efficiently to each individual client.”

As a double major in business and economics major in college, Himebaugh always had an interest in finance, and in how money and markets worked. He and his co-founding partner, Richard Zipkis, received their early training at firms including DLJ, Bernstein and then Credit Suisse.

34 / ADVISORS MAGAZINE MAY 2022

“We just got frustrated with how firms did things for their own benefit over the clients,” Himebaugh recalled. “And we wanted to create an antithetical environment to that philosophy by always putting the client first. People say it, we do it.”

Their own firm started off as a family office practice catering to mostly wealthy families around the country, providing a full complement of services.

About 10 years ago, a private business-owner client of Granite Groups wanted to provide the same money management he was personally receiving within the 401(k) for his employees.

At first, GGA resisted because Himebaugh insisted on maintaining a high-level of ethical standards by not being paid by the mutual fund. After figuring out the proper way to avoid compensation compensated by mutual funds, GGA Retirement was born.

“The ethical standard

really is we don’t have anything to sell,” he said.

“We have a process that works, but we have no proprietary products. And that allows us to go out and pick from any private or public investment in the world,” Himebaugh emphasized.

He noted that his firm sits on the same side of the table as the client. All the vendors, the custodians, the managers, and all the record keepers and everyone else is across the other side. “And that gives us free reign to hire and fire,” Himebaugh said.

That’s an important structural distinction, which is also much safer in his view, from bigger firms.

“Instead of having a vertical as the advisor, the manager and the custodian, we take that model and put it aside,” Himebaugh explained.

“We have independent managers, Granite Group, and an independent custodian. And that creates a system of checks and balances.”

GGA also uses a rigorous quantitative and qualitative fund selection process aimed at delivering strong investment outcomes for your clients. Coupled with the firm’s structural foundation, Himebaugh believes it affords a good combination of safety and great returns over a long period of time.

“So, that’s how we relate to our clients — whether they’re a private client with us that have 10, 20, 30, or 100 million dollars with us or 401(k) with us — the process is the same,” he said.

Himebaugh notes that most investors and advisors tend to look at everything through rose-colored glasses.

“That’s not how we work, and not how things should work,” he said. “We will look for things that can go wrong. “We will look for things that can go wrong. When we can’t find items that are wrong, that is when we buy.”

Assessing the downside is standard operating practice for both arms of the business—whether it’s GGA providing consultation to other financial advisors

and employers on 401(k) management, or Granite Group advising individual clients directly.

On the private side, clients may be wealthy individuals, a foundation, endowment, a family business, or a profitsharing plan. On the 401(k) side, it could be managing a 401(k) or 457(b) plan. Some become clients of

GGA directly, while others come to the firm through advisors and GGA will often partner with the advisors.

“We manage money,” Himebaugh said, “We do our best to duplicate what we do for private clients inside the 401(k). That means managed money and a system for the employee to get the right allocation for them and not a product. That’s why advisors hire us.”

more information on GGA Retirement, visit: granitegroupadvisors.com

ADVISORS MAGAZINE / 35

For

“We look at both the normal and the uber-wealthy. This gives us ideas about what we should be doing for our clients. We don’t want to be complacent…if you are complacent, you are dead.”

L/R: Co-Founders

Richard Zipkis and Lyle Himebaugh

In a world of fast food and one-size-fits-all sensibilities, how often does something feel made especially for you? The "Made for You" section celebrates those items that are created with such high quality of hand workmanship and degree of customization that they become individual to you. In each issue, our editors will endeavor to bring you special things from anywhere on the globe, choosing them solely on the basis of outstanding quality. Our goal is to give you guidance on the best of everything.

1 MONTBLANC — POLYCARBONATE SUITCASE

As well as being able to slip through the tightest of airport queues and squeeze into the overhead cabin lockers, a stylish travel bag should add serious verve to your jetsetting outfit. How you emerge from an arrivalnow been given the OK (for the most part), some quality luggage is a particularly timely investment, too. mrporter.com.com

2 SIDE TRAK SWIVEL — ATTACHABLE MONITOR

New SideTrak Swivel Attachable Portable Monitor for Laptop 12.5” FHD IPS Rotating Dual Laptop Screen, Compatible with Mac, PC, & Chrome | Powered by USB or Mini HDMI (12.5” Single Monitor) MAKE YOUR LAPTOP DUAL SCREEN, Instantly double your laptop screen workspace with this game-changing new attachable portable monitor technology! Securely attaches to the back of your laptop. amazon.com

3 MR PORTER — MELANGE WOOL COAT

This wool coat is the height of sophistication and will keep you looking suave no matter how cold it is outside. Mr P’s Oversized Mélange Wool Coat is truly the dictionary definition of a winter coat. The combination of a smooth grey colourway and the luxe feel of this premium quality wool act as the deciding factor when choosing whether or not to invest in this winter coat. Maybe it’s time to swap the tropical island getaway for a wintery European break this year. MR Porter.com

Designed to show the time in two different time zones simultaneously, the GMT-Master, launched in 1955, was originally developed as a navigation instrument for professionals criss-crossing the globe. The Rolex GMT-Master series is more than just a watch. It evokes a sense of nostalgia just by looking at it. The GMT proves to be a handy watch for everyone around the world. rolex.com

Easliy pair laser projection keyboard for your Iphone, Ipad, Smartphone, laptop or tablets. For devices with bluetooth, operation systems: Windows, iOS, Android, Mac OS. English QWERTY keyboard layout. Rechargeable lithium ion battery is included. The device uses a red laser diode to project a keyboard around 24cm by 10cm -- about the same as most physical keyboards -- and uses Bluetooth to pair with your device, be it a notebook or a smartphone. amazon.com

4 GMT MASTER 2 — ROLEX 5 AGS — WIRELESS LASER KEYBOARD PROJECTION 6 SOLAR ELECTRIC VEHICLE —

APTERA

Electric vehicles have transformed into the mainstream. Aptera’s unique diamond shaped solar panels maximize the energy you get from the sun. This gives fully equipped vehicles 700 Watts of continuous charging power — Aptera is designed to fit you and all of your cargo. With 25 cubic feet of rear storage, Aptera has room to meet your needs. aptera.us

36 / ADVISORS MAGAZINE MAY 2022

made for you

1

4 5

2 3

6

©pingpong56/123RF.COM

By Regina Johnson

By Regina Johnson

Solid Relationships Fuel the Freedom to Invest

More tools today than ever before

In 2021, half the consumers in America thought financial advisors were too expensive, while almost all who used an advisor said they were worth the money, according to a new survey.

MagnifyMoney surveyed more than 1500 Americans to learn if they currently work with a financial advisor, whether they’d consider getting a financial advisor in the future,

or if they think they could find the same information on Google.

The survey found that 42% of respondents thought financial advisors were only for wealthy people, 38% thought the same information can be found online, and 25% thought you don’t need a financial advisor until you’re middle-aged.

When Eddie Ramos launched Freedom Advisory, LLC in 2008 as an independent

financial advisory and wealth management firm, he knew he was making a strategically important market decision.

At the time, the United States was in the middle of the Great Recession, a period of significant financial upheaval in the economy that lasted from 2007 until 2009. Investors from middle-market firms to small family businesses were looking for ways to keep what investments they had afloat and rebuild them up for the future. Investors were looking for help and that personal connection.

In stepped Ramos, then a certified investment management consultant and public accountant with 25 years in the financial arena as an auditor and a financial manager at a fortune 500

38 / ADVISORS MAGAZINE MAY 2022

L/R: Roberto Rivera, CIMA®, CFP® Director of Financial Planning, Karlamary Aleman, CPA, PFS, MBA, Senior Financial Advisor, Eduardo J Ramos, CIMA®, CPA, MBA Managing Director, Giancarlo Diaz-Munio, CFP® CSLP® Financial Advisor

FIDUCIARY

Freedom Advisory® is a fiduciary, fee-only independent advisory firm, serving clients nationwide with offices in Fort Lauderdale, FL & San Juan, PR

DISCOVER OUR DIFFERENCE

We are dedicated to offering unbiased wealth management services and to always act in your best interest. Our collaborative team approach brings multiple, diverse experts to every detail of your wealth management and financial success

OUR CLIENTS

Our clients are successful individuals looking for a team of professionals they can trust to manage the complexities of their financial life. We handle the details with sophisticated solutions while addressing blind spots before they can become problems.

company.

“I saw the opportunity to be of service to clients and to a bigger universe of investors with the option to provide financial services through a fiduciary format that back in 2008, was not as common because the wirehouses and broker-dealers were left and right,” Ramos told Advisors Magazine.

When Ramos opened the firm, there were fewer than 10,000 registered independent advisors, but by 2020 that number had grown to nearly 14,000, according to Statista. com.

The team of professionals he has cultivated over 14 years is like primary care providers. They investigate and review every aspect of a client’s financial health to determine a plan of attack to help that client meet financial goals and needs. Over time, Freedom Advisory has grown to service about 370 families with assets under management of $480 million and growing, according to Ramos.

The firm headquartered in Fort Lauderdale, Florida, with an office in San Juan, Puerto Rico, specializes in wealth and portfolio management, risk management, and estate planning. Its clientele varies and has a minimum of $250,000

to invest. Why that minimum? The firm’s research shows that most people start to seriously consider investing around 40 to 45 when they have reached certain milestones such as marriage, having children, or purchasing their first home. According to Ramos, it’s also a point in their lives when they have sufficient discretionary income to invest.

While Ramos advises everyone to start investing and saving as early as possible to take advantage of compounding interest, he also understands that younger investors often do not earn as much at the start of their careers and find it difficult to start investing.

What’s most important to Ramos is his relationship with his clients. That relationship always starts with a long and thorough conversation. Specifically, to learn the client’s goals, risk tolerance, the type of returns they seek, their liquidity constraints, and why they invest.

The discussion is also an opportunity to learn about the client’s relationship with money.

“Normally, the problem investors have is the short-term thinking clashing with the longterm planning,” he said. “But obviously, when something bad happens in the market, you’re going to be rethinking your position, and that’s where you need to be refocusing. That’s where you must go back to the long-term planning aspect and remain there,” he added.

Part of that relationship is to ensure that fiduciary responsibilities are explained to clients.

“It’s up to the firm to be upfront and disclose all the benefits of working with a firm,”

ADVISORS MAGAZINE / 39

Ramos said. “It’s all about disclosure and providing that statement of fiduciary commitment to the client –that we always put our client’s interest first, and then the firm’s interest,” he added.

Ramos thinks it’s just as important for potential clients to know as much about the firm and the financial advisor as the firm does about the client. Therefore, he strongly encourages clients to ask

questions. For instance, if the advisor works as a team member, that will mean more resources for the same client. The client should find out if the advisor or firm has any complaints filed against them at the Financial Industry Regulatory Authority (FINRA) or with the U.S. Securities and Exchange Commission.

Investing’s paradigm shift

The digital age has changed the tools we use to invest. When Ramos started Freedom Advisory, potential investors walked into an office and met with an advisor but investing today can be done by using an app or laptop. Initially, Ramos thought digital investment apps would be a challenge for his firm. But that turned out not to be the case.

“The human touch is extremely important,” Ramos said. “Our clientele prefers to be talking to a person, a company, to a team of professionals. Even though they don’t call as often as one would think, they still know that they can call anytime and ask the questions that are, concerning to them,” he added.

The ability to invest earlier in life would be a gamechanger, according to Ramos. By the time a person reaches retirement age, they would most likely be independently wealthy.

There’s also a shift when it comes to retirement, according to Ramos. People are living longer and outliving their retirement funds.

“We, suggest our clients

change their attitude and remain equity owners as opposed lenders in the bond market,” Ramos said. “That would be a much better solution for them to at least maintain the capital for a longer period of time than consuming yield from fixed income assets.”

As for the people who are ready to retire but have parents to take care of and children returning home.

“It has always been either you save more, you work longer, or you spend less,” Ramos said. “You need to strike the balance and make sure that you’re going to have sufficient assets to withstand these extra expenses.”

Looking forward, Freedom Advisory is in a growth mode, and the goal is to bring on more capacity to service more clients. The firm is looking to hire two additional financial advisors and two client service personnel.

“We are very thankful for our clients. We have been working together for several years because we get to know our clients,” Ramos said. “Quite often, most of our clients are old-timers as our retention rate is some 99%.”

For more information, visit: freedom-advisory.com

40 / ADVISORS MAGAZINE MAY 2022

REMEMBER THAT YOUR REAL WEALTH CAN BE MEASURED NOT BY WHAT YOU HAVE, BUT BY WHAT YOU ARE.

Napoleon Hill

Eduardo J. Ramos, CIMA®, CPA, MBA

asset-based lending accounts receivable factoring purchase order financing inventory financing $50,000 to 10,000,000 line of credit manufacturing staffing transportation construction wholesale/distribution b2b services high-tech Austin Dallas El Paso Houston Phoenix Do you know someone who could benefit from our services? farwestcapital.com I 888-988-1527 Together, we’re unleashing potential.

By Gabriella Kusz

The Stewardship Approach

Towards Financial Regulation and Compliance

Regulations are going to save the cryptocurrency industry from the volatility that is killing it. Or, at least, that is one opinion. Another is that regulations should be avoided at all costs because they run counter to the core of crypto, as well as the decentralized future it empowers.

While these two views are among the more extreme when it comes to the topic of crypto and regulation, they reveal the two camps that dominate the discussion. Many have reasons for why regulations should be welcomed, whereas others have reasons for why they should be resisted. Finding a consensus has, thus far, been challenging. This provides an opening for discussion around the value of self-regulatory organizations (SROs) and how they may be utilized in the context of complementing formal regulations

to provide sufficient consumer protection and regulatory coverage.

SROs represent a nuanced perspective to the binary discussion for or against regulation. Although regulations for the digital asset industry are necessary, when coupled with a global, flexible and responsive SRO they may be better able to strike the balance needed in protecting consumers while at the same time encouraging innovation and growth in emerging technologies. When SROs are designed as a complement to

right-sized regulations, they can provide up-to-date and highly technical expertise, a nearness and fuller understanding of emerging issues and trends in the industry, and a flexibility and timeliness in responding to the regulatory needs of an industry that builds public trust, fosters market integrity, and maximizes economic opportunity for all participants. Coupled with lean, but strong formal regulations, SROs advance the development of standards and solutions that support the growth of the industry. In short, SROs bring stewardship into the equation.

Stewardship is an uncommon, albeit much-needed, position in today’s business world and draws heavily upon the idea that a modern industry organization should shape and guide the development of an emerging

42 / ADVISORS MAGAZINE MAY 2022

and globally significant industry in harmony with the broader economy, society and public interest. Stewardship does not assume ownership; rather, those with a stewardship mindset typically approach an issue with an understanding that it has been entrusted to their care.

As it applies to the realm of digital assets, a stewardship approach recognizes that anything that makes the industry stronger, including well-crafted regulations, will benefit all stakeholders. It understands that regulators and those in the industry are both pursuing the same goal, but may have different priorities and plans for reaching that goal. Stewardship promotes communication, understanding, and mutual appreciation as keys for making effective progress. Overall, it

empowers and safeguards the highest ethical and technical standards, rather than acting as a facade of governance.

On March 9, 2022, President Joe Biden signed an Executive Order on “Ensuring Responsible Development of Digital Assets.” Among other things, the order puts in motion an effort to “protect consumers, investors, and businesses” from the risks associated with cryptocurrencies. The order specifically says, “The new and unique uses and functions that digital assets can facilitate may create additional economic and financial risks requiring an evolution to a regulatory approach that adequately addresses those risks.”

As US agencies explore whether regulations are appropriate — and, if so, how to apply them — self-regulatory movements can serve the process in a variety of ways, especially ones driven by a stewardship mentality. By providing a compelling forum for unified industry engagement, they can develop and contribute consensusbased solutions for problems identified by regulators.

Facilitating the development of industry-wide professional and ethical standards is one key step that early self-regulatory movements can take as regulations are being considered. Rather than imposing constraints, as regulations often do, principlesbased standards address the lack of clarity and best practices in emerging marketplaces like digital assets. Whereas regulations will typically address certain aspects of an industry's operations in a particular area, industry standards can provide global guidance that

fosters development of businesses across the industry and offers a clear pathway for firms to build resilient and globally competitive firms.

Self-regulatory movements can also build human capacity within the industry by enabling access to materials, resources, and the expertise found within its membership and partners. When these efforts include providing avenues for industry-specific certifications, these movements not only improve the industry’s capacity, but also its reputation within the global community.

When it comes to the development of regulations, and the ongoing enforcement efforts that follow, emerging selfregulatory movements serve as a conduit for dialogue between regulators and regulated. The most effective regulation for the parties involved will be that which grows out of collaboration between all stakeholders. Self-regulatory movements identify opportunities for legal and regulatory engagement, strive to build awareness with key legislators and regulators, and take advantage of opportunities to provide feedback and insight on needed legal and regulatory reforms in countries around the world.

– Gabriella Kusz is the CEO of the Global Digital Asset and Cryptocurrency Association, a global voluntary self-regulatory association for the digital asset and cryptocurrency industry. Global DCA was established to guide the evolution of digital assets, cryptocurrencies, and the underlying blockchain technology.

ADVISORS MAGAZINE / 43

By Ty Young, the CEO of Ty J. Young Wealth Management

5 Tactics to Boost a Retirement Strategy

Setting up a well-designed retirement strategy is not easy. While many people rely on their company 401(k)s or IRAs for retirement income, the reality is that simply contributing to these vehicles is often not enough to save for retirement.

To make your investment dollars stretch further, consider these 5 tips:

Most employers who offer a 401(k) or IRA to their employees also match their contributions up to a certain percentage. For example, an employer may provide a matching benefit of 5% to employees who contribute 5% or more of

their salaries to their 401(k). This means that they will match your contribution up to the 5% amount.

If you’re able to, make sure that you at least contribute the minimum amount to obtain the matching benefit from your

employer. This benefit is literally free money that is put into your retirement account. It’s also free from IRS taxation, as it’s not included as part of your regular income for the year.

Everyone has a different risk tolerance when investing towards their retirement. A mix of investments can be used to achieve high returns while also incurring low fees. Some of the most common types of investments that can potentially result in high returns include:

Stocks

Stocks are issued by corporations that are seeking to raise money by selling equity shares. When you buy a stock, you purchase a percentage ownership in the company.

Over time, you’ll receive dividends from the shares that you purchase. When you finally decide to sell your shares of stock, you may find that they have significantly increased in value.

This growth allows you

to realize a return on your investment. However, realize that the value of a stock may just as easily decline in value. If you decide to hold on to your shares over the long term, make sure you pay attention to the company’s activities and the value of your shares.

ETFs

ETFs are traded on a market exchange just like stocks. However, they usually consist of a variety of investments, such as stocks, commodities, or bonds.