Morning Agenda

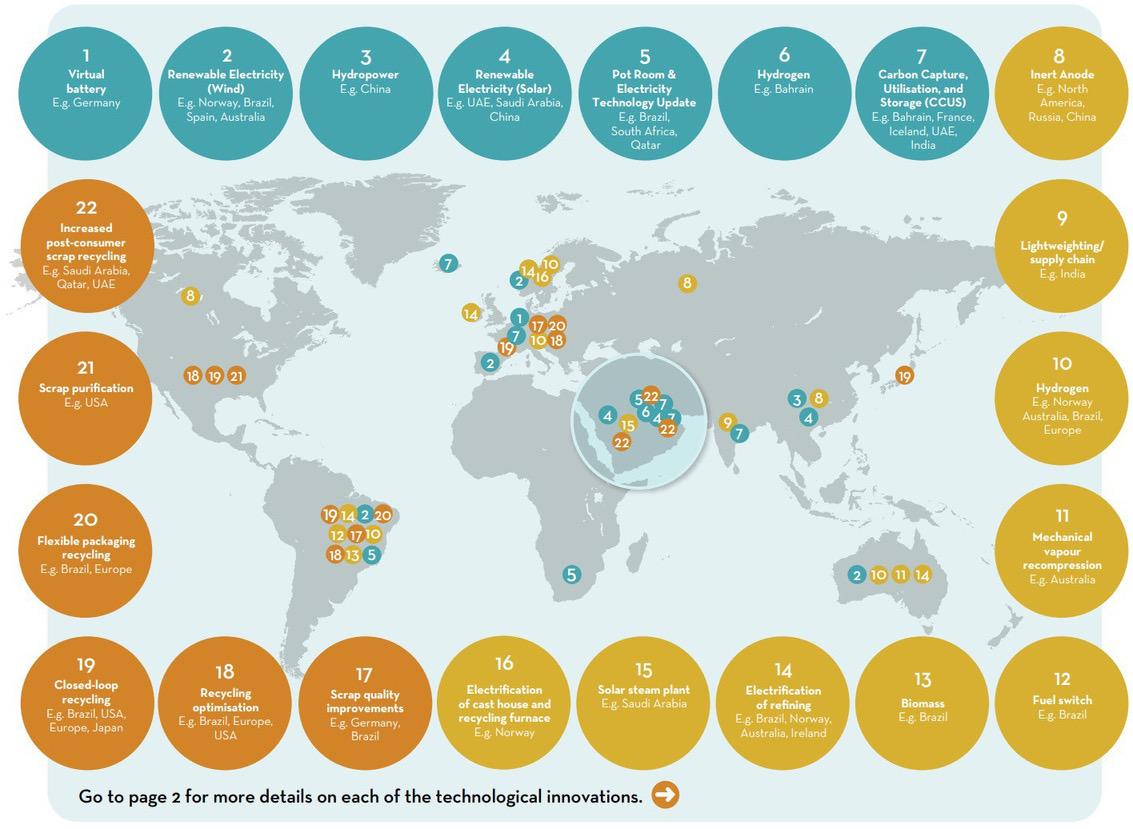

8.30am – 9.30am

REGISTRATION & NETWORKING BREAKFAST

11am – 11.15am

REFRESHMENT BREAK

9.30am – 9.35am

Welcome Address

Nadine Bloxsome, Membership & Sustainability Manager, ALFED 9.35am – 10am

OPENING KEYNOTE

How Soon Will Companies Win or Lose Business on the Carbon Content of their Product? Lord Rupert Redesdale

10am – 10.20am

UK Net Zero Strategy

Henry Green, Head of Net Zero Delivery

Net Zero Strategy Directorate

10.25am – 11am

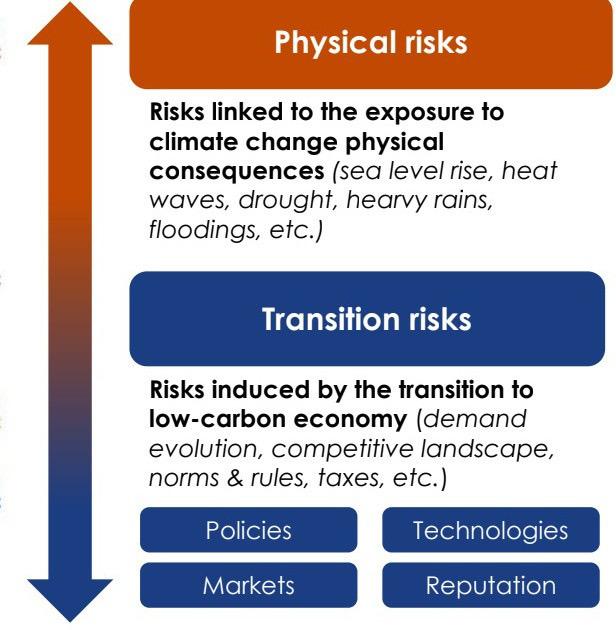

Addressing Carbon Leakage Risk to Support

Decarbonisation

Timothy Stock, Head of Embodied Emissions ReportingIndustrial Decarbonisation at Department for Business, Energy and Industrial Strategy (BEIS)

11.15am – 11.45am

A Global Sustainability Pathway for Aluminium – UK Opportunities

Miles Prosser, Secretary General, International Aluminium Institute

11.45am – 12.15pm

Powering a Sustainable Future

Cameron West, Carbon & Energy Analyst, Zenergi

12.15pm – 1pm

How to Make Carbon Reduction

Commercially Viable

Chris Maclean, CEO, Open Energy Market & Guests

1pm – 2pm

LUNCH & NETWORKING

Afternoon Agenda

2pm – 2.45pm

Panel Discussion: Greenshoring – UK Aluminium

Moderator - Dr Mark Jones, Head of Business Development, BCAST Brunel

Panellists - Paul Cantwell, Head of Net Zero Programs, National Manufacturing Institute of Scotland

Rachel Wiffen, Senior Process Engineer, Innoval Technology Ltd

Tom Giddings, Executive Director, Alupro

Kilian Schneider, Process Metallurgist, Constellium

2.45pm – 3.30pm

Panel Discussion: Addressing Competitiveness and Carbon Leakage in UK Aluminium Production

Moderator - Jo Milligan, Head of Government Relations & External Affairs, GFG Alliance

Panellists - Emanuele Manigrassi, Senior Manager, Climate & Energy, European Aluminium

Andy Doran, Senior Manager, Sustainability & Recycling Development, Novelis Europe

Katie Doubleday,HM Treasury

Tom Jones, CEO, ALFED

3.30pm – 3.45pm REFRESHMENT BREAK

3.45pm – 4pm

Fast Forward Zero

Jerome Lucaes, CEO Fast Forward Zero

4pm – 4.30pm

Smart Sorting Technology for a Green Future

Terence Keyworth, Segment Manager Metal, TOMRA

Recycling Sorting

4.30pm – 5.15pm

Panel Discussion: Eliminating Waste

Moderator - Elle Bennett-Runton, Knowledge

Transfer Manager - Circular Economy, Innovate UK KTN

Panellists - Jan Lukaszewski, Technical Manager, ALFED

Mike Dines, Director, Tandom Metallurgical Ltd

Laura Downey, Innovation Manager (Sustainable Manufacturing), WMG, University of Warwick

5.30pm – 6.30pm

NETWORKING RECEPTION

Sponsored by Zenergi

Sustainability Strategy Day

Thursday, 1st June 2023

KEYNOTE

How Soon Will Companies Win or Lose Business on the Carbon Content of their Product?

Lord Rupert Redesdale

Lord Rupert Redesdale

Rupert Redesdale 25 years of carbon campaigning

How soon will companies win or lose business on the carbon content of their product?

Drivers

for Carbon Reporting

Net Zero

Procurement

Company climate change carbon targets

Carbon Reporting

ESG (Alfed ESG Officer training)

•

•

•

•

•

net zero – definition

Step

Advisory

Compulsory

Current Legislation

Consequence of taking no action

Energy White paper –powering our Net Zero Future

Increased costs due to future carbon taxation, public image and new contracts

GHG Reporting - Annual Mandatory GHG emissions reporting

None compliant directors report

Compulsory

SECR - Annual Streamlined Energy and Carbon Reporting (SECR)

None compliant tax return

Compulsory

ESOS - Energy Savings Opportunities Scheme

Upto £50,000 penalty every 4 years

2

Future Legislation

Consequence of taking no action

Step 2

NZC 2050 – Net Zero Carbon by 2050 Advisory

Increased costs due to future carbon taxation, public image and new contracts

Compulsory

TCFD 2025 – Taskforce on Climate

Related Financial Disclosure

None compliant tax return

Advisory

SBTi – Science Based Targets Initiative

Competitor advantage and public opinion

Potential

UK ETS –

UK Emissions Trading Scheme

Potential future taxation currently at £25/tonne of CO2

net zero - industry take note

net zero – supplier pressure

net zero – employee pressure

Procurement

• How many companies have require carbon data as part of their procurement process?

• How long before that is a mandatory element of procurement requirements?

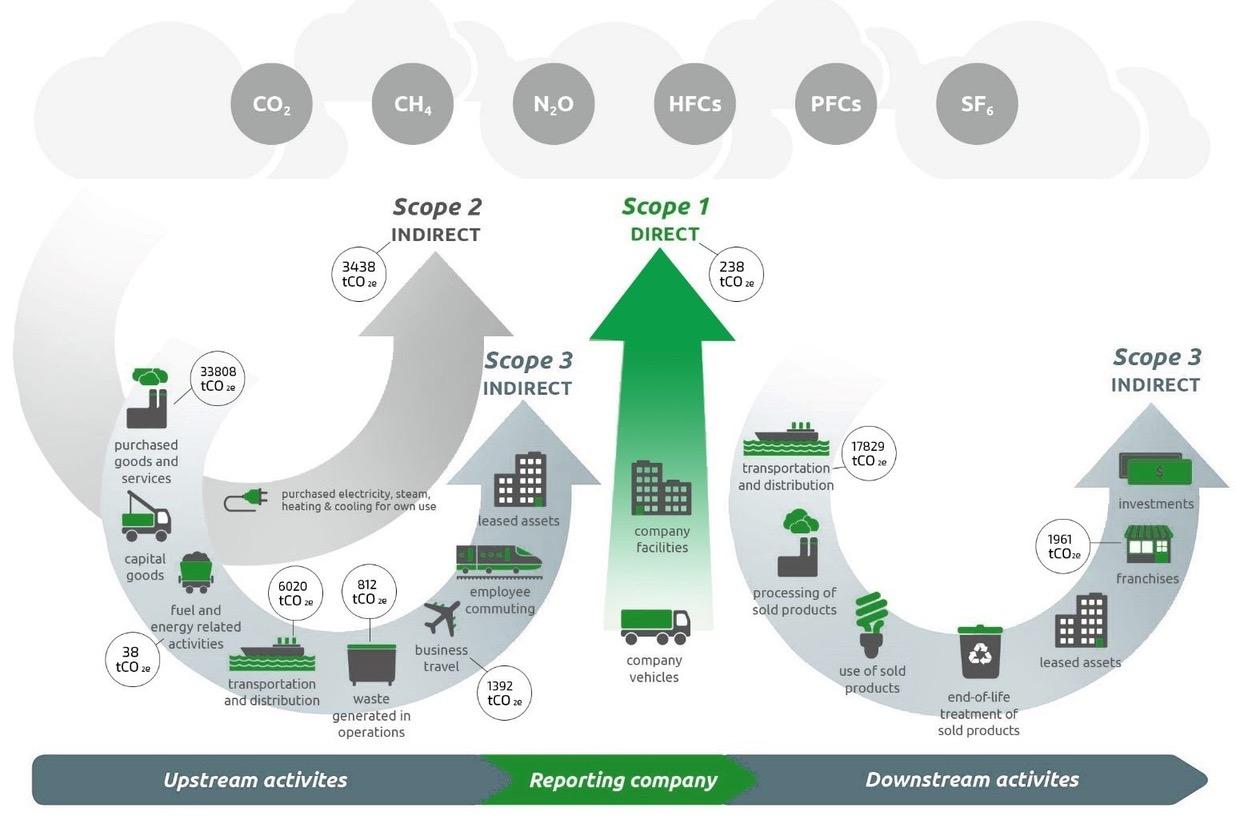

TO BE NET ZERO, WE NEED TO UNDERSTAND –GHG Emissions – THE SCOPES

OH S**T MOMENT

How many companies in the supply chain?

NET ZERO – WHAT DO WE NEED?

• STRATEGY

• POLICY

• BUY-IN

• COMMITMENT

• DATA

• DATA

• DATA

• NET ZERO PLAN

• THE PLAN MAY INCLUDE SOME OR ALL OF THESE AREAS…….

Who in the company is responsible for Carbon reporting and ESG?

"Intrinsically linked"

Q: What is the current position? What is the ambition?

Alfed ESG Officer

• Alfed training to be able to:

• Understand all elements needed to be ESG compliant

• Focus on companies carbon profile, environmental and societal policies

• Formulate necessary policies in all ESG areas

• Ability to integrate all policies into company governance and risk register

Who should go on the course?

• Those who wish to be ESG officers

• Those who are tasked with creating and implementing ESG policies

• Those tasked with carbon reporting

• No prior qualifications needed

Alfed ESG Course

• Course will be based on online webinars

• In person training

• Online materials

• Access to online forum

• CPD

• Please sign up….

Sustainability Strategy Day

Thursday, 1st June 2023

UK Net Zero Strategy

Net Zero Strategy Directorate

Head of Net Zero Delivery

Henry Green

Overview of the UK’s net zero strategy

Henry Green, Head of Net Zero Delivery Department for Energy Security and Net Zero

Henry Green, Head of Net Zero Delivery Department for Energy Security and Net Zero

overall_0_132346355324815878 columns_1_132346355324815878 ‹ # › 1

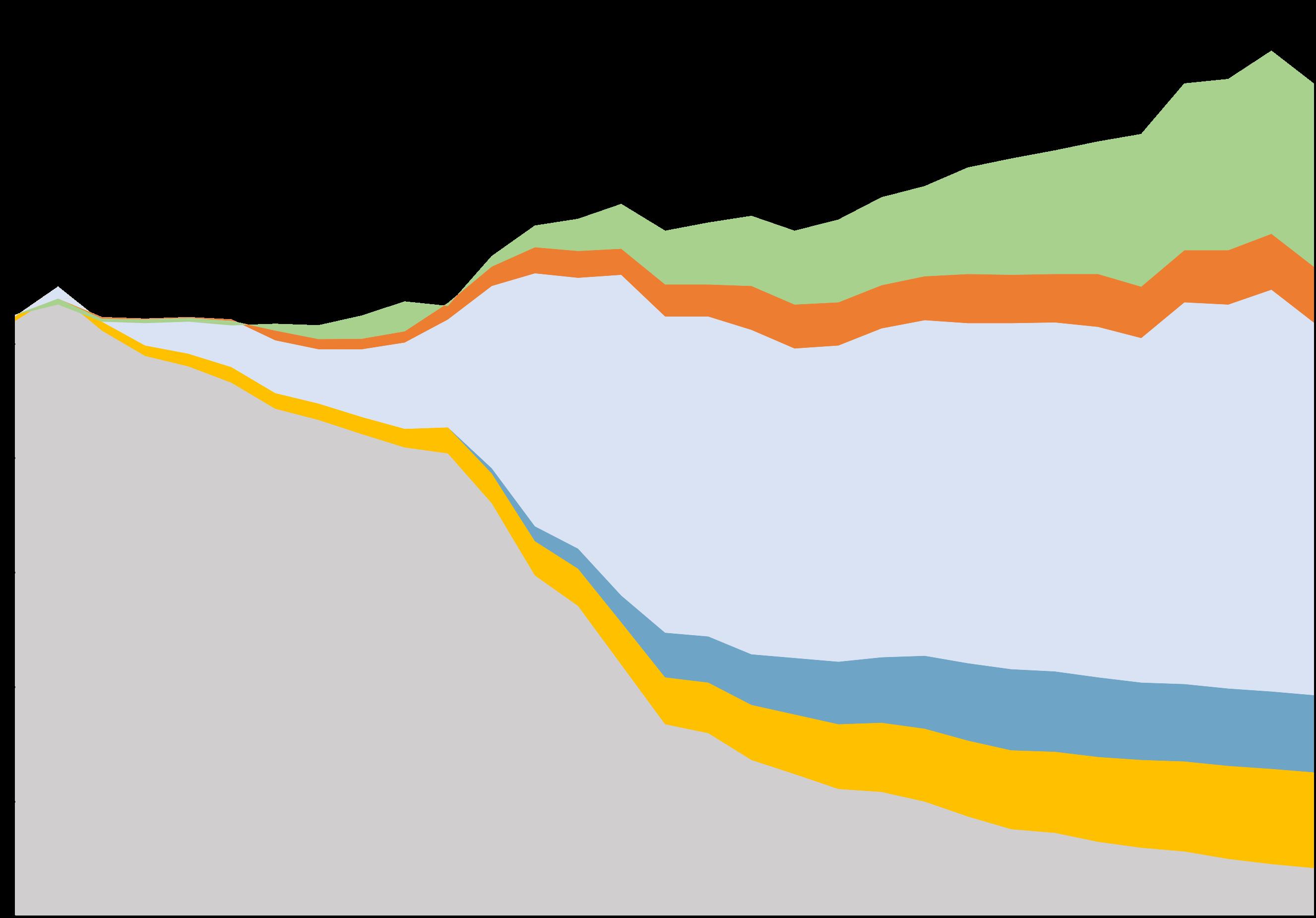

Reducing fossil fuel use and increasing renewable energy has been key

Growing renewables and falling demand have pushed out coal in the UK

overall_0_132346355324815878 columns_1_132346355324815878 ‹ # ›

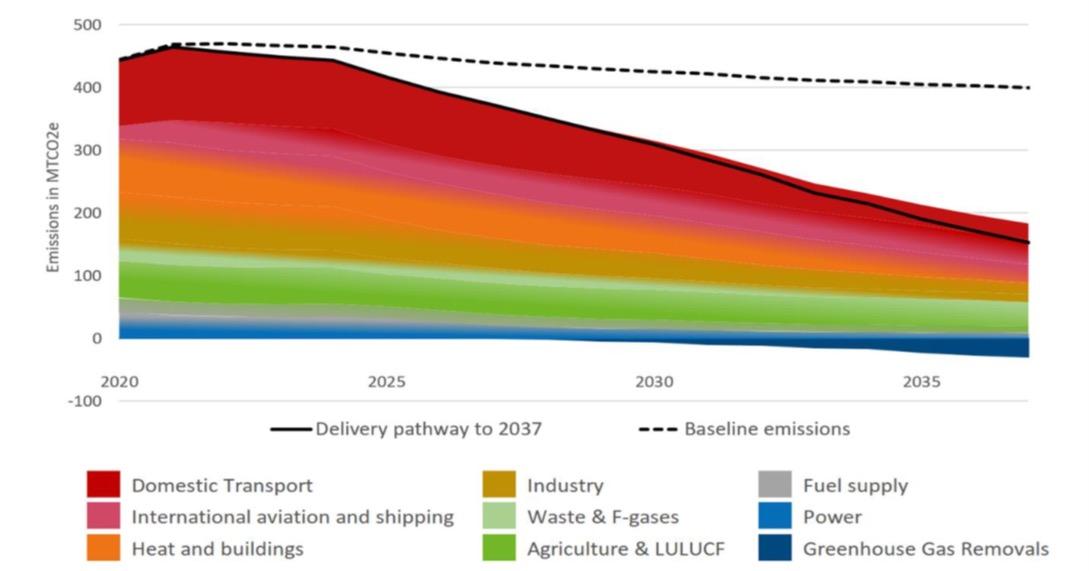

The 2021 Net Zero Strategy set a path to reduce emissions across all sectors

overall_0_132346355324815878 columns_1_132346355324815878 ‹ # ›

The 2023 Powering Up Britain plans brought energy security and net zero together

• We published the Powering Up Britain plans in March 2023.

• Energy security and net zero are two sides of the same coin – we can secure reliable energy supplies whilst cutting carbon and reducing prices.

• Putin’s illegal war destabilised global energy markets and led to an energy crisis. (Figure 1).

• The Government provided unprecedented support to consumers and firms (Figure 2).

• To meet Britain’s future energy needs, and bring down prices, we set out a plan to diversify, decarbonise and domesticate energy production.

overall_0_132346355324815878 columns_1_132346355324815878 ‹ # ›

Figure 1: Destabilised global energy markets

Figure 2: Government support for business and consumers

overall_0_132346355324815878 columns_1_132346355324815878

The Independent Review of Net Zero set out the economic opportunities of net zero

• An independent review, led by Chris Skidmore MP, a Conservative Member of Parliament

• Focused on ‘Delivering a pro-growth, cost-effective net zero in the context of global economic shocks’

• Over three months, the Review led 52 evidence sessions, meeting more than 1000 businesses, universities and other organisations. It received more than 1800 written evidence submissions.

• In January 2023, it published its report ‘Mission Zero’. It made 129 recommendations, including:

⚬ Review UK incentives in the context of the Inflation Reduction Act

⚬ Clear plans to deliver 70GW of solar

⚬ A public engagement plan

• Its major conclusion: net zero is the growth opportunity of the 21ˢᵗ century

overall_0_132346355324815878 columns_1_132346355324815878 ‹ # ›

• The UK has a long-term plan for reaching net zero – as set out in its 2021 Net Zero Strategy

• This is driving decarbonisation across the economy

• Net zero and energy security are two sides of the same coin – brought together in the Powering Up Britain plans

• 2023 is another important year of action

• The UK’s strategy is built on growing the economy while responding to climate change

overall_0_132346355324815878 columns_1_132346355324815878 ‹ # › To conclude…

Sustainability Strategy Day

Thursday, 1st June 2023

Addressing Carbon Leakage Risk to support

Decarbonisation

Timothy Stock

Head of Embodied Emissions

Reporting - Industrial Decarbonisation at Department for Business, Energy and Industrial Strategy (BEIS)

Addressing carbon leakage risk to support decarbonisation

Consultation overview

Carbon leakage consultation: an overview OFFICIAL-SENSITIVE OFFFFIICIIALL--

HMG’s approach to carbon leakage

Carbon leakage is the movement of production and associated emissions from one country to another due to different levels of decarbonisation effort through carbon pricing and climate regulation. As a result, the objective of decarbonisation efforts –to reduce global emissions –would be undermined.

• •

The UK is working with international partners to address carbon leakage -this remains our priority.

However, this will take time, so we are also considering domestic policies to ensure UK efforts lead to a true reduction in global emissions.

The government is therefore exploring a package of potential measures to mitigate carbon leakage risk at all stages of the UK's net zero transition.

ETS reform is being explored in parallel by the UK ETS Authority; any carbon leakage policy would be designed to work cohesively with our existing carbon leakage policy measures.

Carbon leakage consultation: an overview OFFFFIICIIALL-OFFICIAL-SENSITIVE

•

•

About the consultation

Timing and audience

Consultation opened on 30 March, running for 12 weeks to 22 June.

Welcome inputs from all stakeholders, including industry in UK and overseas.

Accessing and responding:

Consultation online

at:https://www.gov.uk/government/consultations/addressing- carbon-leakagerisk-to-support-decarbonisation

Respond online at:https://beisgovuk.citizenspace.com/trade/addressingcarbon- leakage-risk/

Email for consultation: carbonleakage.consultation@beis.gov.uk

Carbon leakage consultation: an overview

OFFFFIICIIALL-OFFICIAL-SENSITIVE

Exploring a potential policy package

This exploratory consultation will inform decision making on which policies, if any, should be introduced, and does not commit the government to adopt any specific policy.

We are inviting views and evidence from stakeholdersonthe best possible mix of policies to manage carbon leakage risk.

New measures wouldneed to:

•

• Promote and encourage increased climate action both in the UK and globally, including

Respond to carbon leakage risk in a proportionate, targeted, evidence-based, and effective way, aligning with relevant UK decarbonisation policy. international action to address carbon leakage and taking into consideration countries’ differing levels of development,particularlyfor leastdeveloped and low-incomecountries.

Be compatible with, and deliverable alongside, the government’s key domestic priorities, such as supporting sustainable and balanced growth, by minimising business compliance costs.

Be consistent with ourcommitment to free and open trade and be designed in line with the UK’s international obligations and commitments,including World TradeOrganisation (WTO)obligations.

OFFFFIICIIALL--

Carbon leakage consultation: an overview

• •

OFFICIAL-SENSITIVE

Part 2: Emissions reporting requirements

An embodied emissions reporting system could support the implementation of carbon leakage mitigation policies. A key consideration is to minimise and consolidate burdens on business including by making requirements streamlined and non-duplicative as far as possible.

An emissions reporting framework may be needed to underpin policy with reporting of product-level embodied emissions.

Options for embodied emissions reporting

Use of Emission Factors

Possible use of default values

Designing the mechanism for embodied to standardise

emissions reporting

approaches and ensure robust outcomes while minimising burdens for businesses

Delivery of reporting system

for collecting and processing product-level embodied emissions data

Methodology and metric Data collection period

Sectoral coverage and where to target in the manufacturing chain

IT system options

Frequency of reporting

Verification and disclosure

OFFFFIICIIALL-OFFICIAL-SENSITIVE

Carbon leakage consultation: an overview

• • • • • • • • •

Carbon leakage consultation: an overview OFFICIAL-SENSITIVE OFFFFIICIIALL-Q&A Accessing and responding: Consultation online at:https://www.gov.uk/government/consultations/addressing- carbon-leakagerisk-to-support-decarbonisation Respond online at:https://beisgovuk.citizenspace.com/trade/addressing-carbonleakage-risk/ Email for consultation: carbonleakage.consultation@beis.gov.uk

Sustainability Strategy Day

Thursday, 1st June 2023

A Global Sustainability

Pathway for Aluminium: UK Opportunities

Miles Prosser

Secretary General

International Aluminium Institute

A Global Sustainability Pathway for Aluminium – UK Opportunities

‹#›

Miles Prosser Secretary General

About the International Aluminium Institute (IAI)

Since its foundation in 1972, members of the IAI have been companies engaged in the production of bauxite, alumina and aluminium, the recycling of aluminium and/or fabrication of aluminium, or as joint venture partners.

The

International Aluminium Institute

(IAI) is the only body representing the global primary aluminium industry.

Current IAI membership represents all major regions of global bauxite, alumina and aluminium production.

The IAI has been key to bringing the industry together on shared purpose over the past 50 years.

What we do

Raise awareness of Aluminium’s unique and valuable properties

Foster collaboration for sustainability

Support informed decision making

Contribute to Aluminium wide standards and regulation

• Why sustainability is important?

• Applying sustainability to aluminium.

• Greenhouse Gas Pathways.

Today

Context

COVID RECOVERY CLIMATE CHANGE INTEREST RATES

ENERGY CRISIS

Aluminium Is Sustainable

RENEWABLE ENERGY

TRANSITION TO ELECTRIC VEHICLES

THE MOST RECYCLED DRINK CONTAINER

Shaping A Better Tomorrow

DURABLE

Alloys are weather-proof and corrosion-resistant resulting in very long lifetimes

ALUMINIUM

Shaping a better tomorrow

CONDUCTIVE

High thermal conductivity minimises the time and energy to process, chill and heat food

PROTECTIVE

Barrier properties preserve food, drink and medicines, reducing wastage

LIGHTWEIGHT

High strength-to-weight ratio makes it possible to design light, strong & stable structures

FORMABLE

Flexibility and formability enable unlimited design potential

RECYCLABLE

Recycling saves 95% of the energy required for primary production.

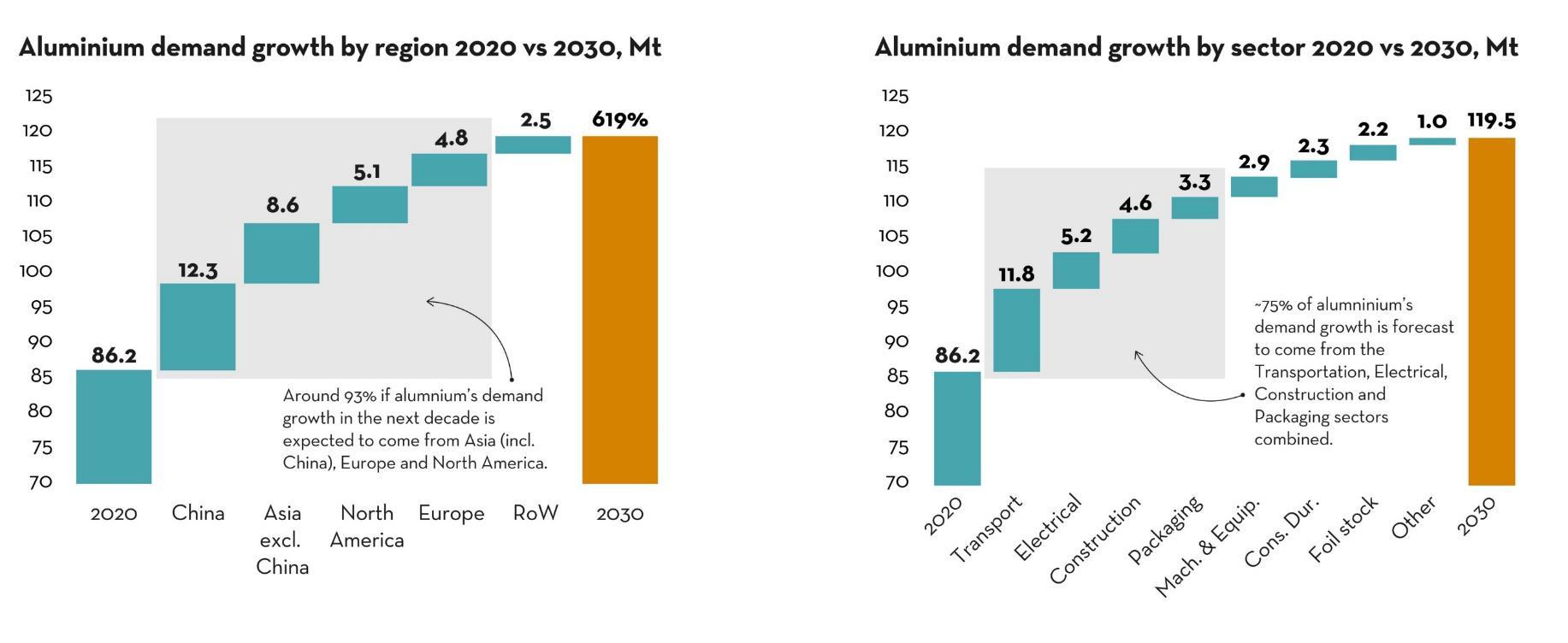

Aluminium consumption in main regions and sectors

Main Drivers Of Demand Growth

Transportation Electrical Packaging Construction

Decarbonisation policies and the shift towards more aluminium intensive electric vehicles will have a positive impact in the metal’s consumption coming from the Transportation sector.

The transition from traditional sources of power towards nonconventional renewable energy sources represents one of the most substantial opportunities for the aluminium industry over the coming years

Driven mainly by the rise in popularity of canned drinks in North America, Europe and China, the packaging sector is experiencing a surge in demand of aluminium

In contrast to other sectors, the construction sector is not expected to be driven by ESG trends and decarbonization policies.

Automotive - The transition to EVs

Source: Aluminum Association and DuckerFrontier:

Source: Aluminum Association and DuckerFrontier:

ICE to Battery

Aluminium Demand For Electricity

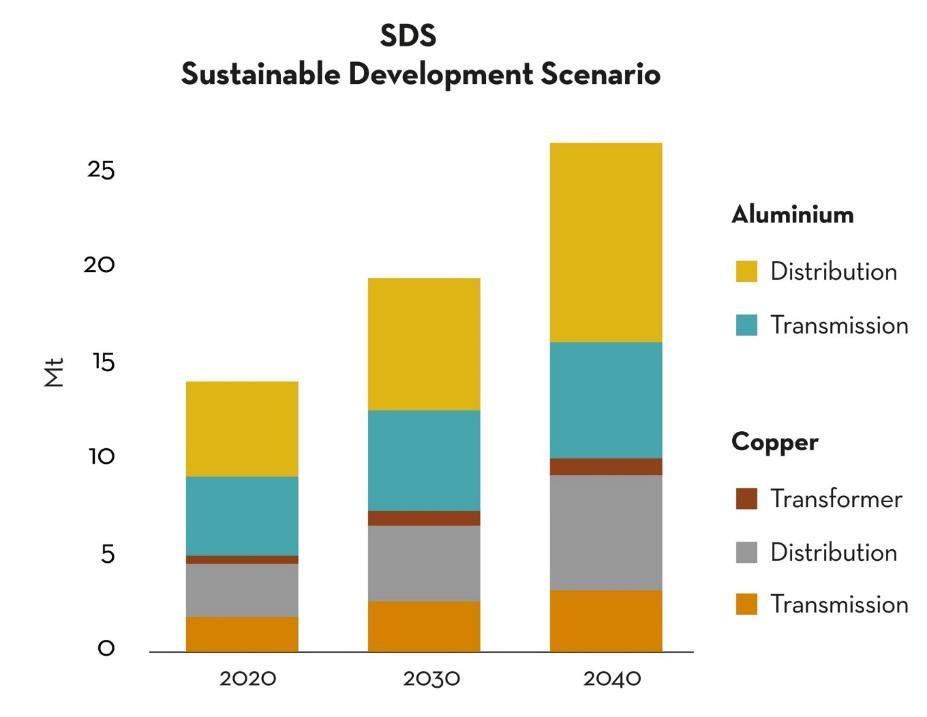

Projected aluminium demand for electricity grid additions and replacements increasing from 9 Mt to 13-16 Mt by 2040.

Source: The Role of Critical Minerals in Clean Energy Transitions, IEA World Energy Outlook Special Report, May 2021

2040 13-16 Mt 2023 9 Mt

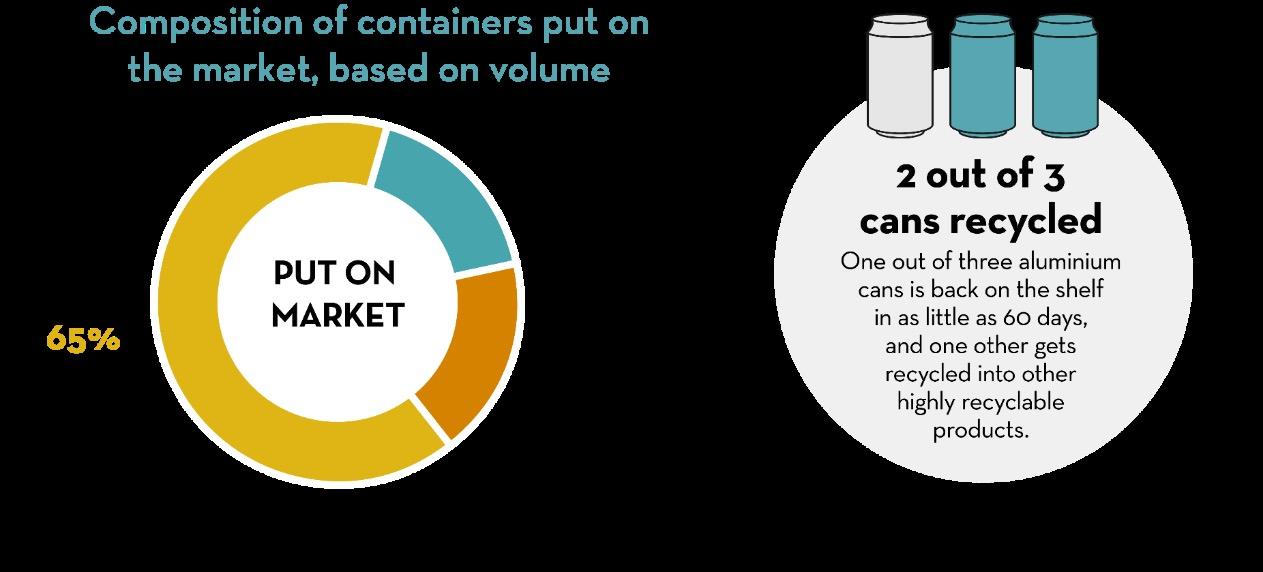

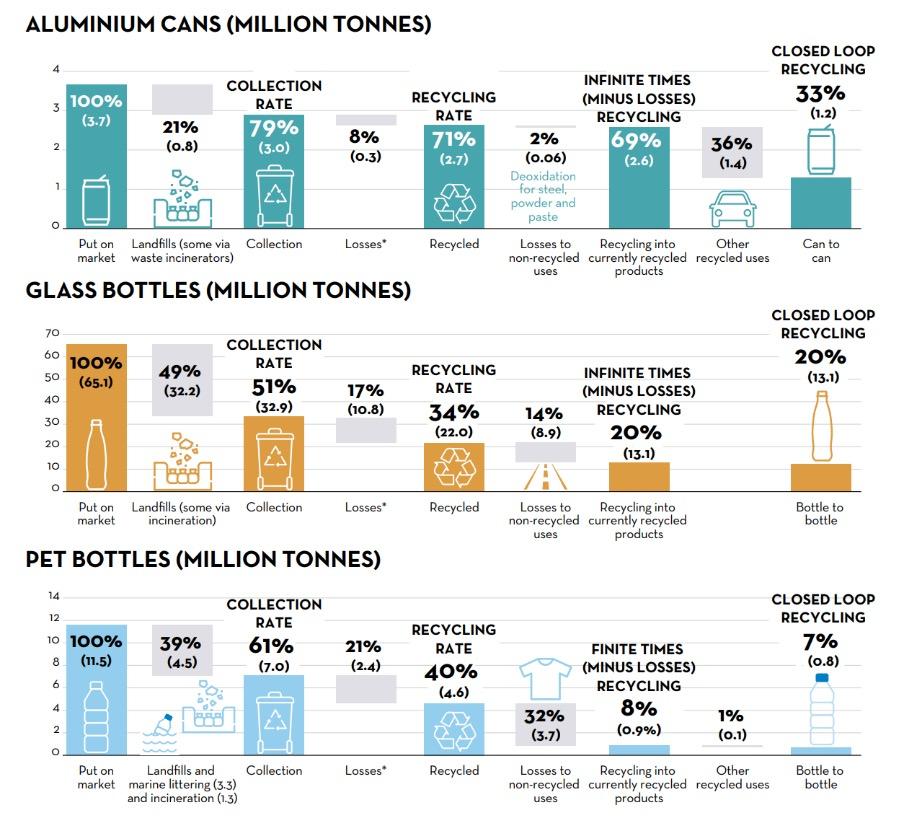

Aluminium Cans: The Best Solution For A Circular

Economy

Source: https://internationalaluminium.org/resource/aluminium-beverage-can-study/

2019 Real Recycling Rate Includes USA, Brazil, Europe, Japan, China 2019 Recycled Products

A Circularity Case For Aluminium Compared With Glass And Plastic

Aluminium’s contribution to sustainable development

2 & 3: Barrier properties to preserve & deliver food & vital medication

11: Durable aluminium building components with lifetimes >120 years

7: Al essential in renewable energy systems, cabling & energy storage

12: Sustainable production, sharing of good practice & improving recycling

13: 1 kg of Al replacing heavier materials in a car saves 20 kg CO2 over the vehicle’s life

8: Approximately 8 million direct & indirect high quality & skilled jobs across the sector

17: Collaboration across the value chain & cross-sector

Sustainability challenges for aluminium

1,2 & 3: Ensure communities benefit from industry.

4, 5, 8 & 10: Ensure workforce benefits from industry.

12: Sustainable production, sharing of good practice

13: Reduce GHG emissions – to zero

14 & 15: Minimise & manage impacts on land & water

17: Collaboration across the value chain & cross-sector

“Green” Is More Than Greenhouse Gas Emissions

Climate change Emissions & Waste People Biodiversity Circularity Water

IAI Greenhouse Gas Pathways to 2050

Data driven approach

Establish the sector baseline

Consider the different positions

700 million

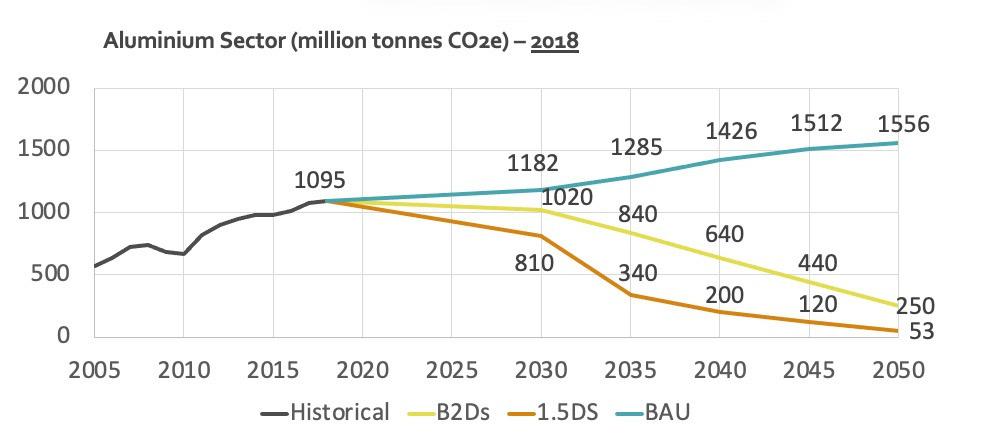

2018: 1.1 billion tonnes of CO₂e

Electricity

Industry data & input

Top-down scenario analysis – IEA

Identify variety of pathways

300 million

<100 million

Process & Thermal

Ancillary & Transport

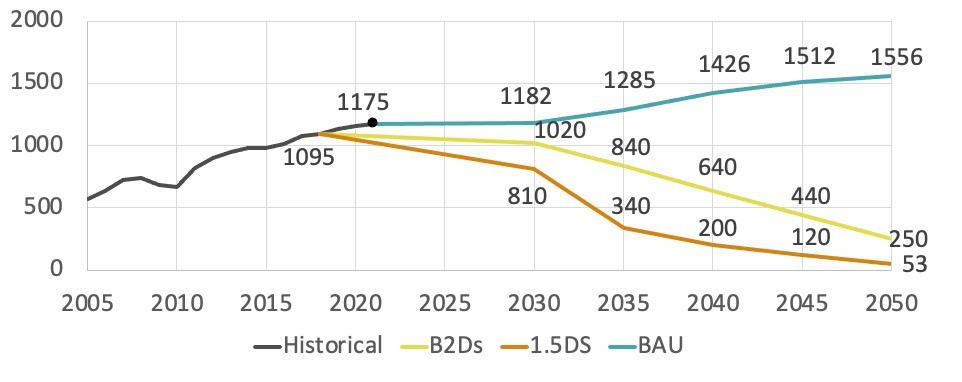

IAI Emissions Scenarios

Aluminium Sector (million tonnes CO2e) – 2018

1.5DS

IAI GHG Pathways

2050 (IAI, 2021)

BAU B2DS

to

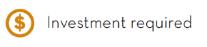

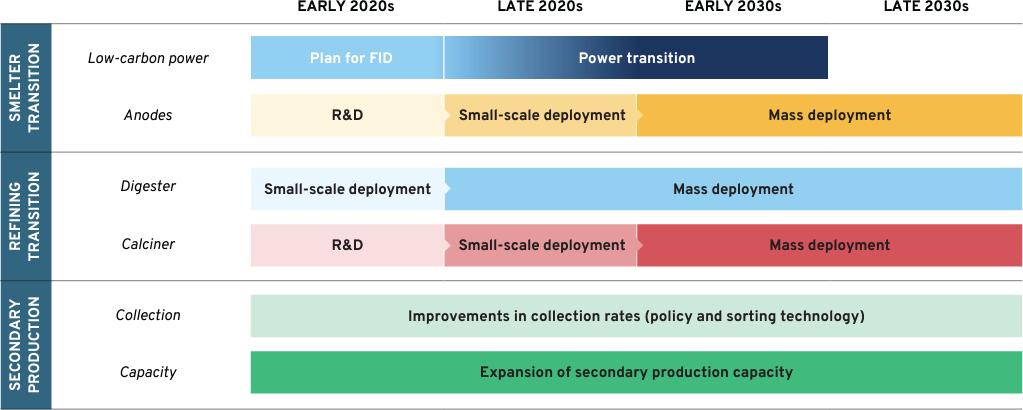

Greenhouse Gas Pathways To 2050

Sectoral Transition Strategy by Mission Possible Partnership

2020-2050 direct and indirect emissions for the aluminium sector

% of cumulative emissions reduction (20222050)

Material & Resource Efficiency

Low Carbon Refineries

Improved recycling rates

Higher design efficiency

Heat recovery and zeroemissions boilers

Zero-emissions calciners

Low Carbon Power

New grid connections or CCS

Low Carbon Smelters

Nuclear small modular reactors Inert anodes

CCS retrofits

Additional Fuel Switching

Low-carbon electricity or hydrogen across wider value chain

1. 2 1. 4 0. 2 0. 4 0. 6 0. 8 1. 0 1. 6 ₂₀₂₀ ₂₀₂₅ ₂₀₃₀ ₂₀₃₅ ₂₀₄₀ ₂₀₄₅ ₂₀₅₀

e/yr

GtCO₂

1520% 510% 55-60% 10% 1015%

Greenhouse Gas Pathways To 2050

2021 GHG Emissions not on 1.5DS Track

Aluminium Sector (million tonnes CO2e) – 2021 Update

IAI GHG Pathways to 2050 (IAI, 2021), IAI Statistic (IAI, 2022)

BAU B2DS 1.5DS

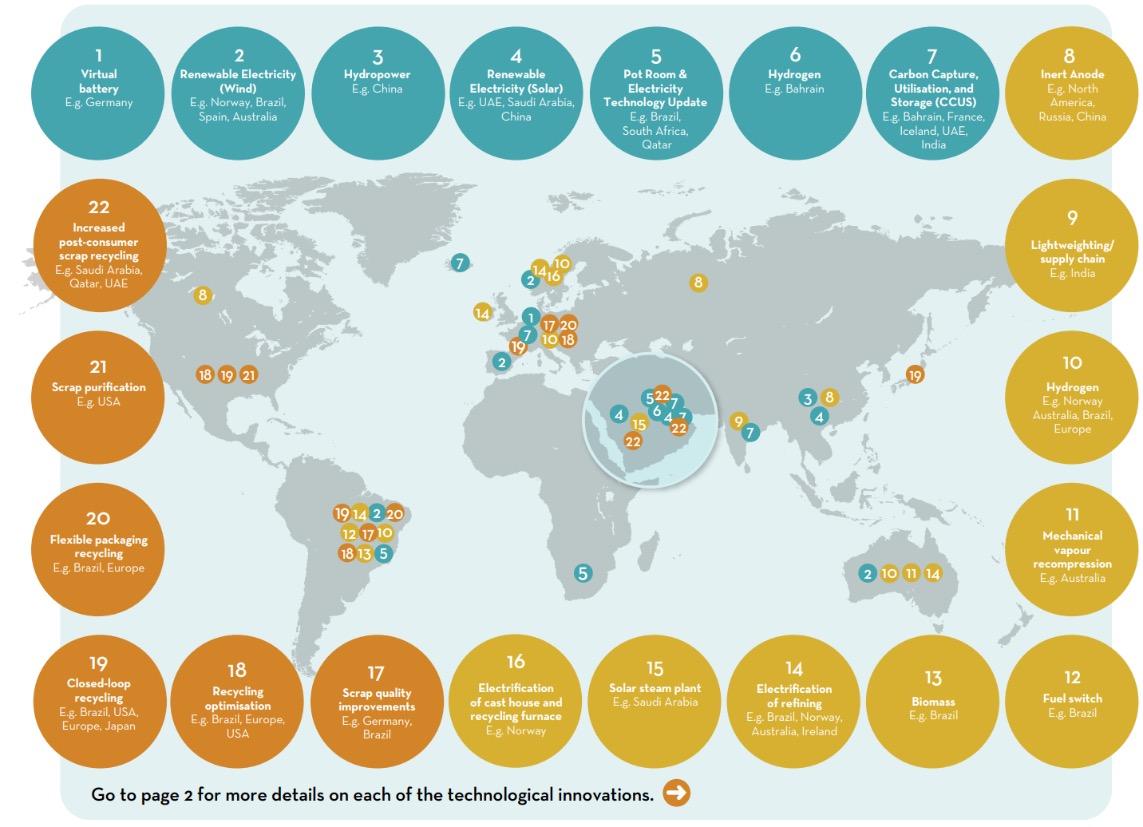

GHG Reduction Projects

2022/2023 -> 50 Projects

Electricity

decarbonisation

Direct emissions

Recycling

IAI GHG Technology Map (IAI, 2023)

IAI Membership Decarbonisation Plans

Decarbonisation Plan 2050 Net-Zero Pathway Endorsement of MPP Aluminium Transition Strategy 72% 36% 84%

Sustainability and the Aluminium Industry

Aluminium is part of the sustainability solution.

Aluminium has natural advantages over other materials.

To grasp opportunities we must demonstrate that aluminium is sustainable.

Decarbonisation is a significant challenge for the aluminium industry.

‹#› international-aluminium.org @Int_Aluminium linkedin.com/company/international-aluminium-institute/ @TheAluminiumStory Thank you

Sustainability Strategy Day

Thursday, 1st June 2023

Powering a Sustainable Future

Carbon & Energy Analyst

Cameron West

Carbon & Energy Analyst

Cameron West

Powering a Sustainable Future

Social Value Strategy

Cameron West ALFED Sustainability Strategy Day BMA House, London

+

NetZero-2050

+

26: years 07: months 05: days 15: hours 40: minutes 02 seconds Until Next Saturday -2050

NetZero

The path to net zero ambition

The path to net zero reality

+

Whatisnetzero?

Balancing the amount of greenhouse gases emitted with the amount removed from the atmosphere (offsetting).

+

Netzero

How many people have a written Net Zero Strategy in place?

How many people have considered Net Zero but haven't written it down and are not sure where to start?

Is the want there but just restricted by finance and resource?

What is more important Net Zero or to simply Reduce Consumption?

Is anyone just not interested in Net Zero?

Poweringasustainablefuture

+

Poweringasustainablefuture

+

Thepathtonetzeroisa marathon

Zen Zero is Zenergi’ s market-leading solution which helps organisations to not only define their carbon footprint, but also provides a glidepath to net zero with the relevant expertise and tools, every step of the way.

Phase 1: Measure

Ensure compliance

Data collection

Create baseline

Stakeholder workshop

Zenergi’ s three-stage Zen Zero framework, Measure,

Prepare, and Deliver, is a proven approach that will deliver sustained benefits across your organisation – from increased profit through strategic energy efficiency programmes, while reducing the risk from rising energy and carbon prices, to assisting the UK nationally to provide security of energy supplies and supporting the transition to a low-carbon economy.

Phase 2: Prepare

Detailed site audits

Identify opportunities

Industry benchmarking

Establish ambition level

Agree net zero target

Carbon roadmap

Phase 3: Deliver

Launch net zero plan

Engage stakeholders

Commence delivery

Technical support

Regular reporting

+

Keepitsimple

Appoint an Expert Partner

Define your Expectations Early

Choose your Scopes

1, 2 & 3

Plan your Strategy

Measure, Prepare & Deliver

Survey your Buildings

Understand the Challenges

Verify Savings

+

Nextsteps

Chief Executive Officer Chris Maclean CEO and Founder Planet Mark Steve Malkin UK Commercial Manager Energy Gain Paul Meaden Head of Strategic Partnerships Ripple Energy Joe Wadsworth How to Make Carbon Reduction Commercially Viable

Greenshoring

Business

Innoval

UK Aluminium Head of

Development BCAST Brunel Dr Mark Jones Senior Engineer, Quality Systems Manager

Technology Ltd

Rachel Wiffen Executive Director Alupro Tom Giddings Lead Material Technologist, Constellium Kilian Schneider

BCAST Brunel University London Uxbridge, UB8 3PH, UK Dr Mark Jones LiME Hub Manager 1ˢᵗ June 2023

Advanced Solidification Technology

Dr Mark Jones Head of Business Development mark.jones@brunel.ac.uk +44(0)7881 079441 Greenshoring Secondary Aluminium into the UK

Brunel Centre for

(BCAST)

Greenshoring puts sustainability at the core of location choice for manufacturing, shifting the focus from low cost onto sustainable manufacturing.

Greenshoring will reduce the emissions of the current manufacturing base and attract new manufacturers to make products with the lowest possible environmental footprint, and ensure security of the supply chain.

*Objective of today is to focus on greenshoring the secondary aluminium industry into the UK*

Greenshoring

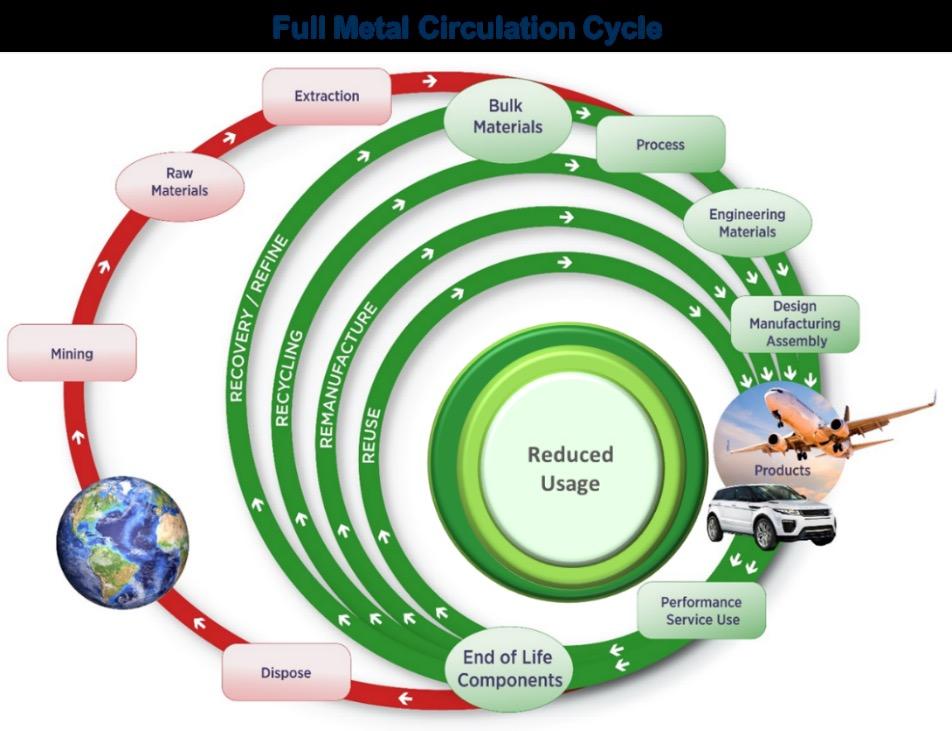

BCAST Circular Metals Centre

Part of the government £30M NICER initiative to make the UK a Circular Economy Leader

BCAST’s long-term vision is Full Metal Circulation

BCAST Circular Metals Centre

Part of the government

£30M NICER initiative to make the UK a Circular Economy Leader

Innovate UK collaborative research & development fund

£30M Total Funding

34 Universities

64 Senior Academics

Textiles

Construction Minerals

Metals Technology Metals

42 Early Career researchers

Chemicals

60+ PhD Students

120 Industrial Partners

Wider academic, industry, third-party, policy community (including DEFRA, BEIS, devolved administration)

BCAST Circular Metals Centre Strategy

Part of the government £30M NICER initiative to make the UK a Circular Economy Leader

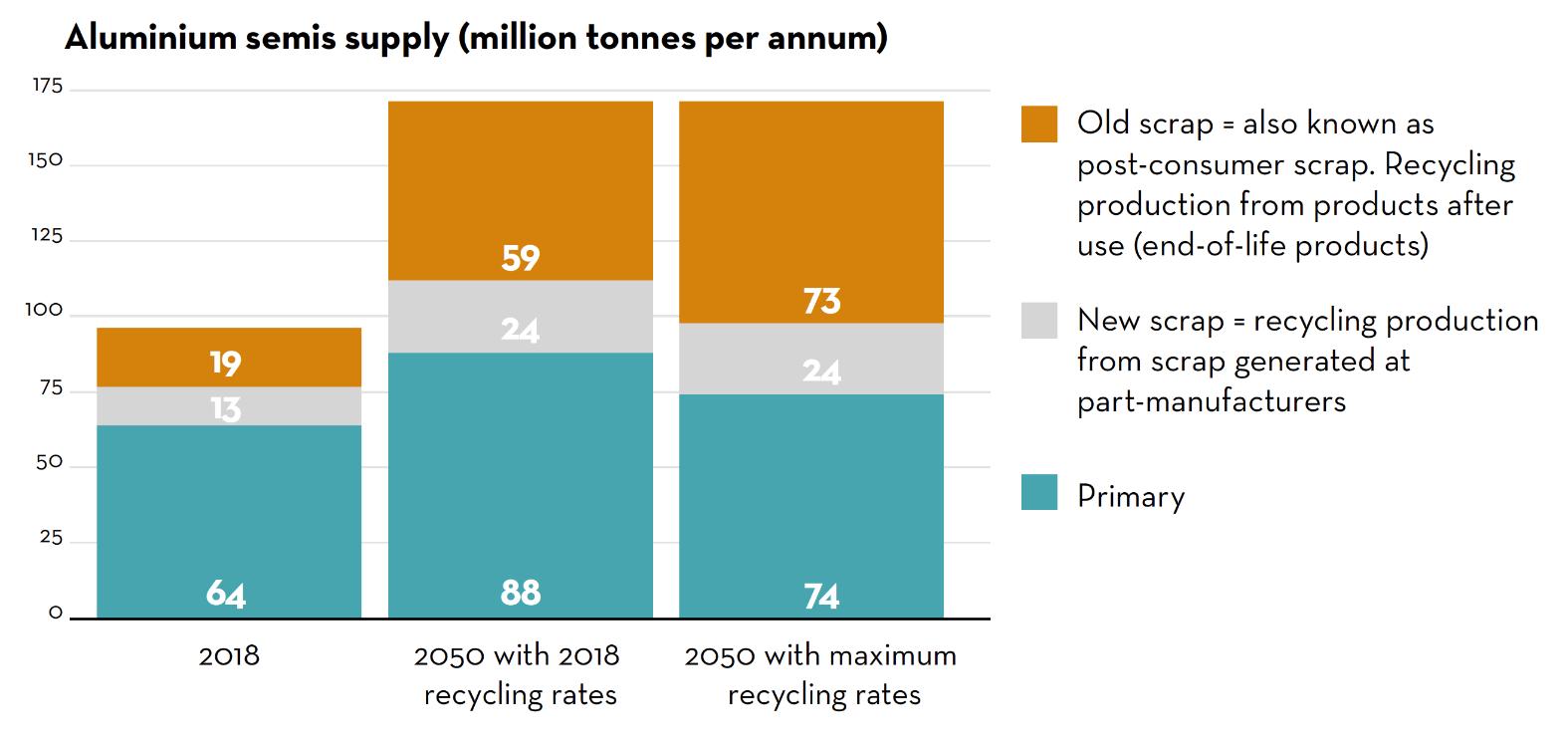

World is still producing 68mt of primary aluminium in 2022 100mt+ estimated to be used pa, including post consumer scrap

Source: International Aluminium Institute statistics 2022

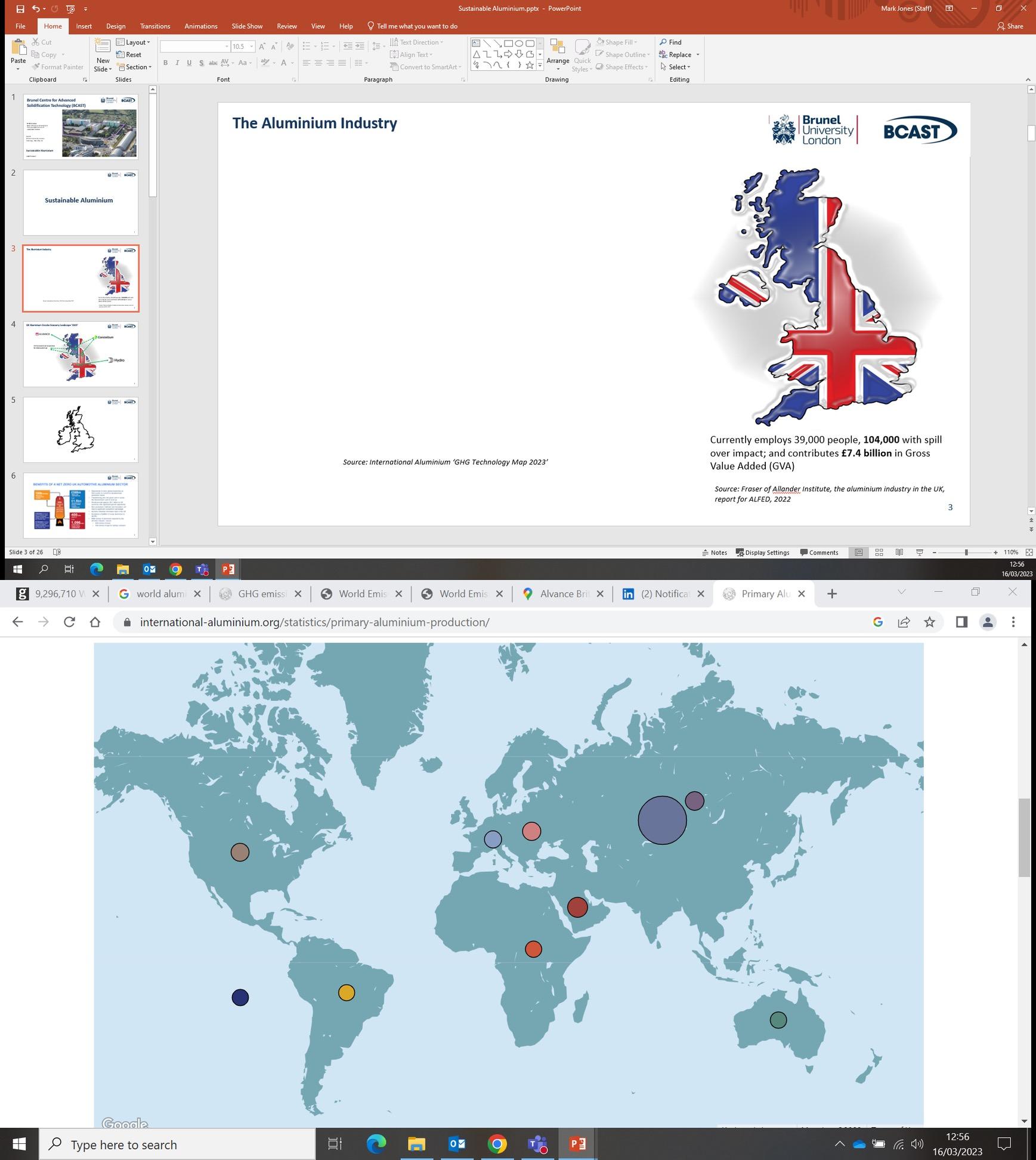

1.2mt, and exports up to 800kt of secondary aluminium

Currently employs 39,000 people directly and 104,000 with spill over impact; and contributes £7.4 billion in Gross Value Added (GVA)

Source: Fraser of Allander Institute, the aluminium industry in the UK, report for ALFED, 2022

‹›

China 2022 40.5mt Asia (ex China) 2022 4.6mt Oceania 2022 1.8mt Gulf Cooperation Council 2022 6.1mt Africa 2022 1.6mt Western and Central Europe 2022 2.9mt Russia and Eastern Europe 2022 4.1mt South America 2022 1.3mt Estimated Unreported 2022 1.9mt North America 2022 3.7mt

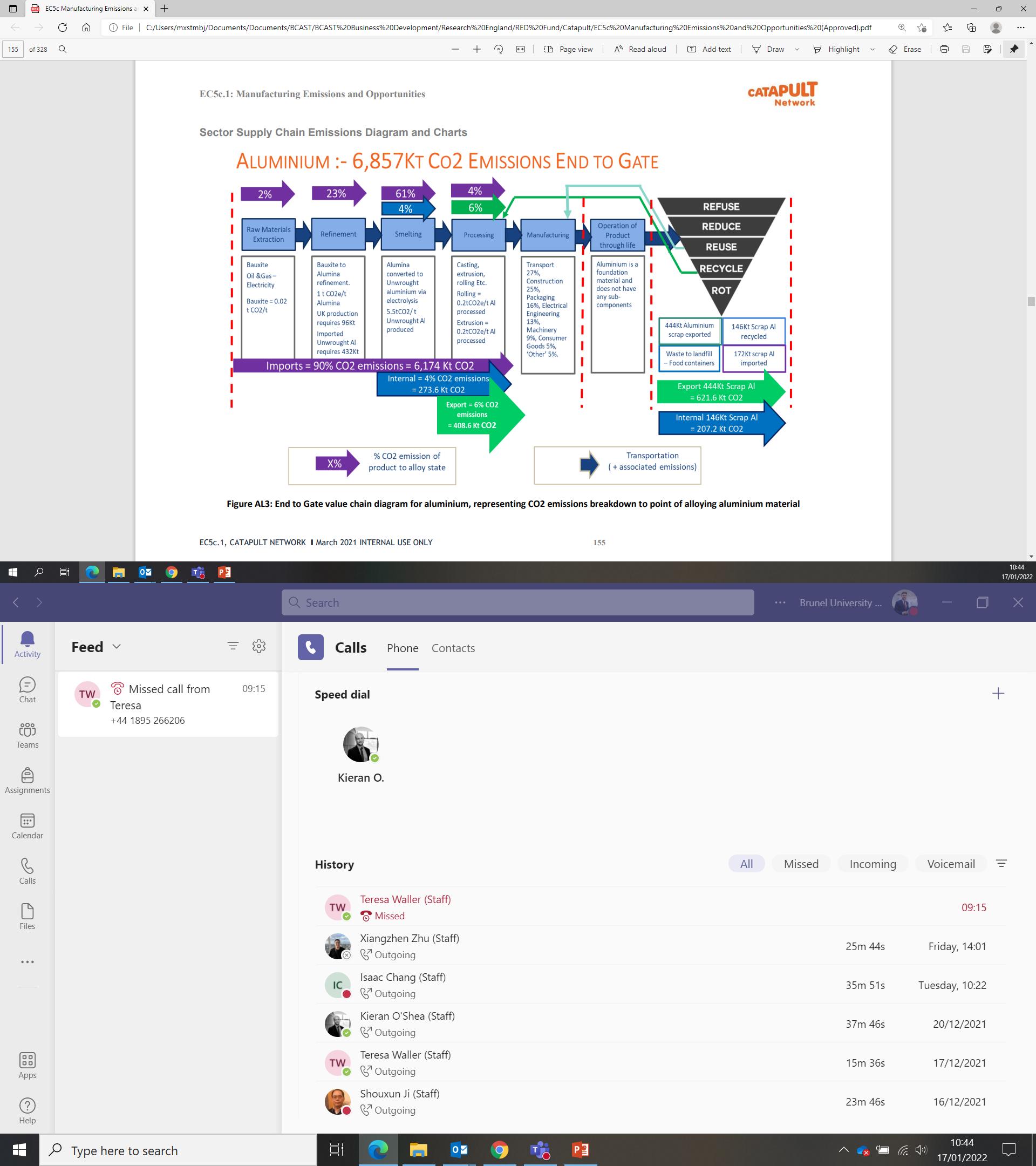

Aluminium Sector

Co2 emissions end to gate

85% CO2 emissions reduction

Circular Economy

Source: High Value Manufacturing Catapult

UK Secondary Aluminium New Manufacturing Announced

Doubling their capacity in Lochaber, from 50kt primary, by using secondary for extrusions for windows for a volume of 50kt, totalling 100kt output.

New packaging secondary aluminium rolling plant (2026).

Expansion of Hydro global recycling centres, based in Wrexham, to produce 100kt of secondary aluminium, for feeding into CircAL extrusion alloys and into primary reduction cells in Norway.

CirConAl – project to develop lower carbon, lower cost recycled aluminium alloys with automotive manufacturers and suppliers, focussed on extrusion.

Currently import 1.2mt, and export up to 800k of secondary aluminium (this will expand)

• 400kt of automotive sheet - rolling

• 50kt of castings – will increase e.g. aerospace

• 50kt of extrusions

• 150kt of can sheet - rolling

There is a desperate need for low carbon aluminium – UK opportunity to act rapidly to become a world leader in the use of secondary aluminium.

Opportunity to become self sufficient, and then grow as demand increases.

British Aluminium Corporation for Advanced Alloys (BACALL)

UK Secondary Aluminium R&D Opportunity

• Industrial scale forming

• UK manufacturing Net Zero activities

• Analytical equipment

• Industrial scale casting

• Industrial scale extrusion

• Analytical equipment

• Secondary aluminium specialist

• Circular Metals Centre

• LiME Hub

• Metal Heath Service (MHS)

Offer a UK sustainable aluminium R&D capability, to drive forward via government and industrial support: ‘Sustainable Aluminium Innovation Hub’

Greenshoring the Secondary Aluminium into the UK Interactive Discussion

Panel will introduce themselves, and speak for 5 mins on major challenges and opportunities for their speciality/sector

Wider audience participation:

• Major challenges for the UK

• Opportunities for the UK

We are forming an R&D capability, pulling everyone together, proving the science, investigating industries and supply chains BCAST & High Value Manufacturing Catapult will be hosting a workshop in July 2023

a. How can industry work together (not working in silos, what are the tensions)?

b. What would the perfect policy be – carbon border tax, energy price?

c. Magic investment, what would this look like?

d. Future directions

Sustainability Strategy Day

Thursday, 1st June 2023

Fast Forward Zero

CEO Fast Forward Zero

Jerome Lucaes

Tow ard s a de carb on i z e d, m ore c i rc u l ar an d i n c l u s i v e e con om y ALFED Sustainability day –1 ˢ ᵗ June 2023 The climate emergency toolkit For the aluminium industry

FAST FORWARD ZERO

Jerome

Lucaes , CEO

Jerome LUCAES bio highlights

CEO, FAST FORWARD ZERO (FFZero) - Business transformations, creation of coalitions, for a low carbon, circular and inclusive economy

Strategic Advisor, IAI

• Created/Facilitates the ALUMINIUM FORWARD 2030 coalition

Director - Low carbon aluminium program - En+ Group / RUSAL – 2016 – 2022

• Led the low carbon aluminium program

• Creator of the ALLOW brand

• WORLD FIRST commitment to net ZERO CARBON

Global Product sustainability director at Rio Tinto (2011-2016)

Co-creator of the Aluminium Stewardship Initiative (2011-2014)

Experience of 25 years in the aluminiuum industry with Pechiney, Alcan, Rio Tinto, RUSAL

⚬ net 0 carbon transformation

⚬ innovation to market, marketing strategies, brand creation and development, product life cycle management

⚬ energy, climate, SDGs, biodiversity, social, sustainability impact assesments, risks based analysis,

⚬ metals and mining, energy, raw materials, supply - chains

⚬ Business development, Partnerships

FA S T FO R W A R D ZE R O

CARBON

FA S T FO R W A R D ZE R O

The world is in a CLIMATE CRISIS, and in a RACE TO ZERO

Human activities generate more GHG emissions

Only wars, recessions, fuel shocks & pandemics have dented the rise of fossil fuel emissions

Source: Global Carbon Project/ Nat

FA S T FO R W A R D ZE R O

Bullard

Atmospheric carbon dioxide is higher than at any time in 800,000 years

Source: EPA/ Nat

Bullard

FA S T FO R W A R D ZE R O

All business are impacted

Carbon Price

Source: graph based on EEX EUA spot price data

FA S T FO R W A R D ZE R O

Decarbonisation is not an option anymore

FA S T FO R W A R D ZE R O

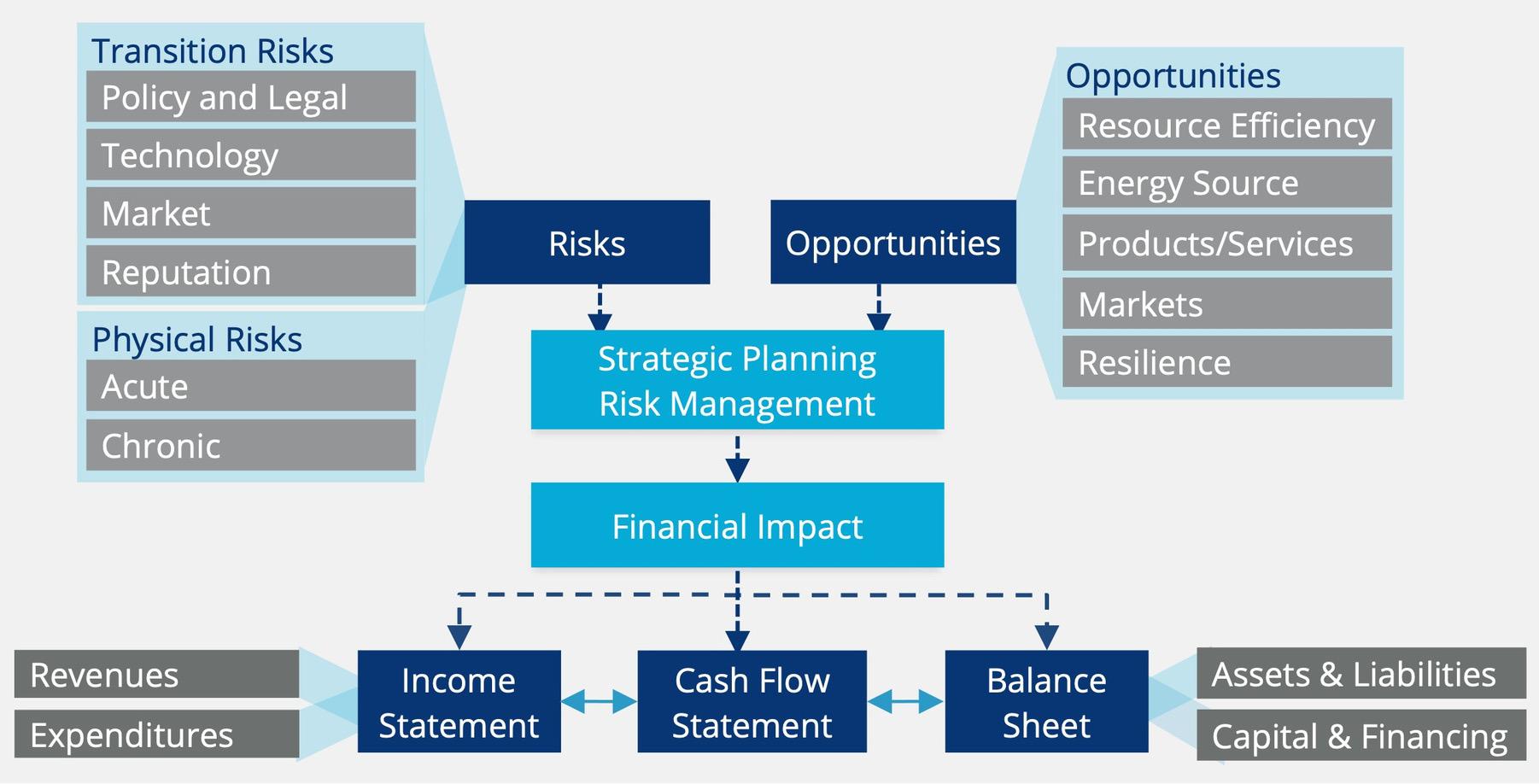

Climate related risks, opportunities and

Financial impact

FA S T FO R W A R D ZE R O

Source: TCFD

HOW to EAT an ELEPHANT?

FA S T FO R W A R D ZE R O

The aluminium industry pathway to net zero

2020-2050 direct and indirect emissions for the aluminium sector

% of cumulative emissions reduction (2022-2050)

• Improved recycling rates

• Higher design efficiency

• Heat recovery and zeroemissions boilers

• Zero-emissions calciners

• New grid connections or CCS

• Nuclear small modular reactors

• Inert anodes

• CCS retrofits

• Low-carbon electricity or hydrogen across wider value chain

FA S T FO R W A R D ZE R O

1.2 1.4 0.2 0.4 0.6 0.8 1.0 1.6 2045 2020 2025 2030 2035 2040

2050 Material & Resource Efficiency Low Carbon Refineries Low Carbon Power Low Carbon Smelters Additional Fuel Switching

Source: IAI, Aluminium Sector Transition Strategy Model (2022).

15-

510% 55-60% 10

1015%

20 %

%

GtCO₂e/yr

The industry decarbonisation readiness

FA S T FO R W A R D ZE R O

Source: Mission Possible Partnership

More than 50 decarbonization projects have been identified globally

2020 -> 16 Project

2023 -> 50 Projects

Electricity decarbonisation

Direct emissions

Recycling

Source: IAI GHG Technology Map (IAI, 2023)

FA S T FO R W A R D ZE R O

The primary aluminium industry is moving ahead

• Reduce scope 1 & 2 emissions by 15% and emissions intensity by 30% by 2030 (vs 2018) - Group

• Power transition - Gas to solar & wind in Australia smelters (4 GW RFP)

• Hydrogen feasibility study at Yarwin refinery

• AP60 LCA plant expansion

• ISAL carbon capture project -

CARBFIX

• ELYSIS

Recycling ≥50Kt

• PFA production with EOL wheels

• Billets with recycling content >25% (NZAS)

Hydro power expansion

INERT ANODE (INERTAL)

• Switch oil & coal fuel to gas at alumina refinery. Change alumina source

• Upgrade smelting technology (exit Soderberg)

• Divestments

RHEINFELDEN, 30 kt

• PrimarywithPCSpilot at Kubal

• To reduce CO2 emissions by 10% 2025, 30% by 2030 and zero emissions by 2050.

• Hydrogen at alumina refinery in Brazil

• Hydrogen at Casthouses in Norway

• HALZero R&D development

• Ardel/ Sunndel tech upgrades

• Reduxa 2.0 by 2030

• BIO ANODES

• To reduce GhG emission intensity by 30% by 2025, 50% by 2030 vs 2015.

• San Ciprian, Spain => Wind power by 2024

• Sao Luis, Brazil = > restart by 2022, Hydro power

• Alumina = > MVR technology

• Smelter renewable energy use from 78% 2020 to 85% 2025

Recycling >500Kt

• Add EOL into primary aluminium VAP, pilot in Norway by 2022

• 75R – Billet with >75% PCS

2.0Mt

full scope

Source: compannies websites and FFZero analysis

• 80 kt based on solar energy

• Upto 2Mt based on nuclear energy source

• Divestment of GAS POWER PLANT

• Alumina refinery based on nuclear energy

• Joined AbDhabi Hydrogen initiative

• ELYSIS <4.0 full scope <2.0 full scope

Recycling ≥ 50Kt

• ASTRAE. Purification EOL scrap upto 99.98%. Pilot in Canada by 2023

• Brand. Billets with recycling content >50%

Aluminium recycling coalition withTadweer, Coca-Cola, Pepsico, Canpack, Crown, Veolia.

• Decarbonize alumina supply

3.8 ? full scope

FA S T FO R W A R D ZE R O

2023 2030 <4.0 full scope < 3.8 full scope

3.0

<4.0 Scope 1, 2, partial 3 <

full scope

RECYCLING

3.8

1.6Mt 1.7Mt 0.08Mt 1.8Mt 2.1+ Mt 2.1Mt 0.2 –2.2Mt 4.5Min – 7.3Max

2.6Mt

3.4Mt PRIMARY

ALUMINIUM

3.0Mt

2.0Mt LOW CO2 BRAND

Yunnan Aluminium

The approach to succeed

Measure

Develop a decarbonization roadmap Set Targets

• CO2 / energy measurement system

• Quality/relevance/achievability of solutions,

• $ - carbon price

• Timelines, Long term vs short term

• Risks identification and management, options

• Management focus – ownwership, priorisation

• Set targets - Assignments, Individual KPIs, rewards,

IMPLEMENT and EXECUTE

Manage and Influence external factors & Collaborate

• Adapt Resources (education, transformation)

• Mobilize with a sense of urgency - time pressure

• Monitoring of CO2 reductions, certifications

• Reporting & Communication & External recognitions (SBTi, CDP),

• Markets, customers

• Engage Suppliers, technology partners

• Regulations, standards, CBAM

S T FO R W A R D ZE R O

FA

A few concrete steps if you are just starting

Measure your carbon footprint

• With the help of an expert

Mobilize your team

• Run a “climate fresk” workshop

Identify the quick wins

• Low carbon material

• Green energy

• home – work commuting

Evaluate the carbon footprint of my business

Organisational boundary (equity share or control approach)

Establish

Organisational Boundary

Establish Organisational Boundary

Calculate Emissions

FA S T FO R W A R D ZE R O

Evaluate the carbon footprint of your business

FA S T FO R W A R D ZE R O

Emissions Activity Data Emission Factor = X

Carbon Footprint Calculation

Evaluate the carbon footprint of you business

Footprint Calculation

FA S T FO R W A R D ZE R O

Carbon Footprint =

Scope Activity Data FU = Functional Unit Emission Factor X n Σ i = 1 A i F U FE i kgCO2e/FU

Carbon

How to add up emission types:

• We use a conversion factor : Global Warming Potential (GWP), over 100 years .

• It measure the contributions to global warming over 100 years, of 1 kg of gas compared with CO 2 (CO 2 e) .

• Figures are based on calculations updated in each IPCC report .

• Other indicators exist . Most of the regulations use GWP at 100 years .

FA S T FO R W A R D ZE R O

All GHG emissions count

GAS Carbon Dioxide CO2 Fossil Methane CH4 Biogenic Methane CH4 Nitrous Oxide N2O SF4 GWP OVER100YEARS (CO2 eq) 1 30 28 265 23 500

Product carbon footprint boundaries

GATE-TO-GATE

MATERIALS TRANSPORT MANUFACTURING DISTRIBUTION RETAIL USE END OF LIFE RECYCLING

FA S T FO R W A R D ZE R O

Product carbon footprint boundaries

CRADLE-TO-GATE

MATERIALS TRANSPORT MANUFACTURING DISTRIBUTION RETAIL USE END OF LIFE RECYCLING

FA S T FO R W A R D ZE R O

Product carbon footprint boundaries

CRADLE-TO-GRAVE

MATERIALS TRANSPORT MANUFACTURING DISTRIBUTION RETAIL USE END OF LIFE RECYCLING

FA S T FO R W A R D ZE R O

Product carbon footprint boundaries

CRADLE-TO-GRAVE INCL. RECYCLING (ALSO KNOWN AS LIFE CYCLE ASSESMENT)

FA S T FO R W A R D ZE R O MATERIALS TRANSPORT MANUFACTURING DISTRIBUTION RETAIL USE END OF LIFE RECYCLING

Establish a net zero carbon roadmap

What Net zero carbon mean?

To limit global warming to 1.5ºC, we must reach net-zero emissions no later than 2050

FA S T FO R W A R D ZE R O

?

Identify your emissions reduction levers

New technologies and opportunities emerge

FA S T FO R W A R D ZE R O

Source: European Aluminium

Engage your suppliers

Invite customers & suppliers to join you on your journey.

Leverage the benefits to create a low carbon offering. Celebrate progress & milestones.

FA S T FO R W A R D ZE R O

Create a story around your decarbonisation

Lifetime carbon neutral

Inspiring

By 2041, VELUX will remove all emissions since the company was created in 1941

Be prepared for a lot of resistance to change

FA S T FO R W A R D ZE R O

Ready?

FA S T FO R W A R D ZE R O

Thank you

FA S T FO R W A R D ZE R O

TOWARD A DECARBONIZED, MORE CIRCULAR AND INCLUSIVE ECONOMY

Advises business leaders, boards of directors

• industrial companies

• investors and funds

Helps and partners with start-ups

• Equity participation

• Business plan and commercial development

• Connect people

Key experience and expertise:

• Over 20 years in the aluminium industry, primary and downstream

• net 0 carbon transformation,

• innovation to market,

• marketing strategies, brand creation and development, product life cycle management

• sustainability impact assesments, risks based analysis,

• metals and mining, energy, raw materials, supply - chains

• Business development and partnerships

FA S T FO R W A R D ZE R O

FA S T FO R W A R D ZE R O

Sustainability Strategy Day

Thursday, 1st June 2023

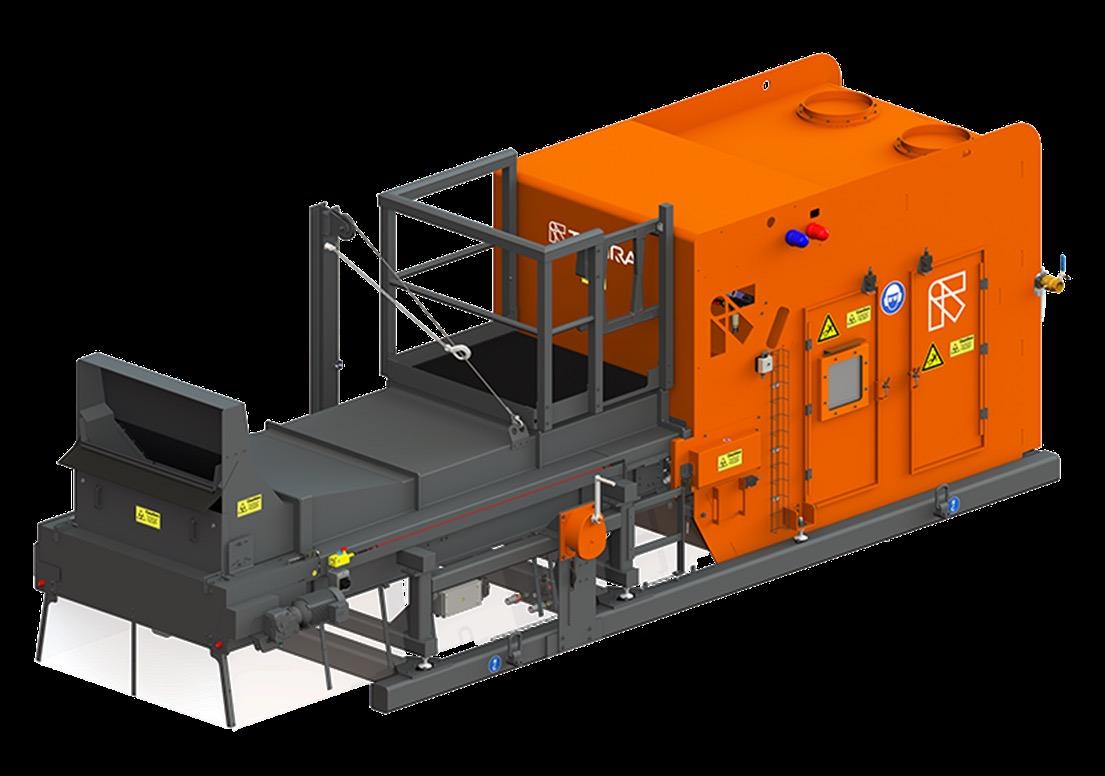

Smart Sorting Technology for a Green Future

Terence Keyworth

Terence Keyworth

Segment Manager Metal

Segment Manager Metal

Agenda

•

• Technology portfolio

• Applications

• Market trends

TOMRA introduction

Technology & Products

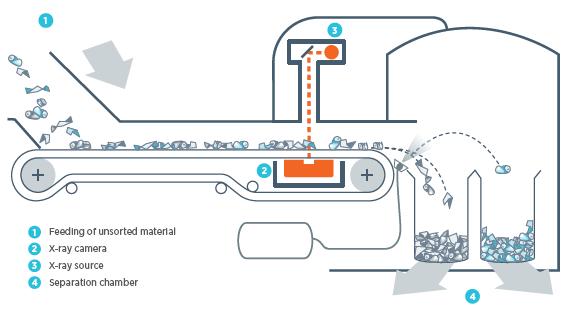

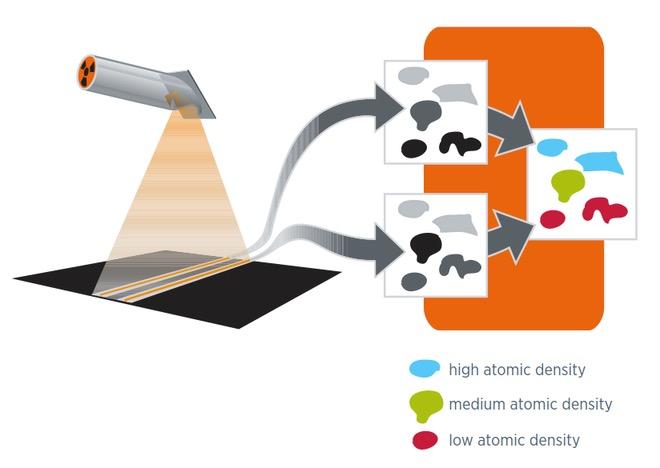

X -TRACT XRTX - ray transmission technology

rays penetrate the sorting material rays are collected by TRACT Advanced Duoline® sensor

TOMRA data processing from X-ray image to converted image

X - TRACT

XRT – sorting principle

AUTOSORT PULSE -

LIBS technology

AUTOSORT™ PULSE

Dynamic LIBS solution for sorting aluminum scrap by alloy.

AUTOSORT™ PULSE

Dynamic LIBS solution for sorting aluminum scrap by alloy.

LIBS working principle

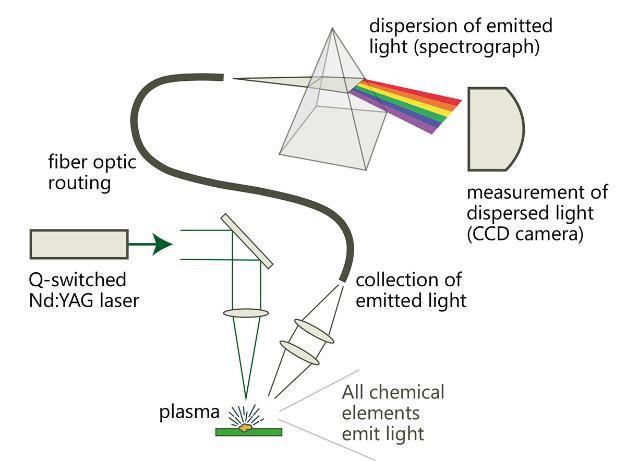

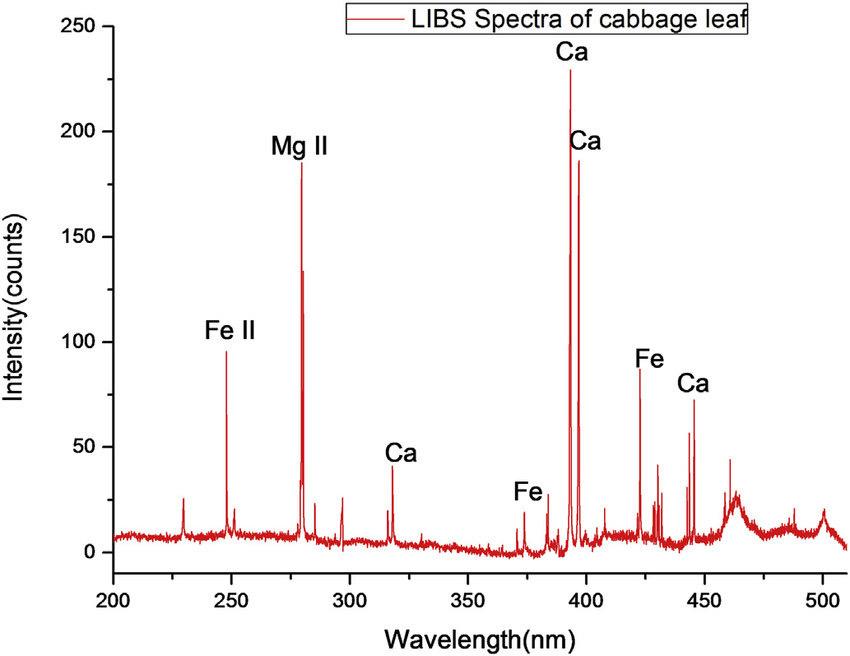

Laser Induced Breakdown Spectroscopy

https://en.wikipedia.org/wiki/Laser-induced_breakdown_spectroscopy

https://www.researchgate.net/publication/312476192/figure/fig2/AS:866938993524745@1583705771852/LIBS-spectra-of cabbage-leaf-in-spectral-range-200e500-nm.jpg

10

LASER

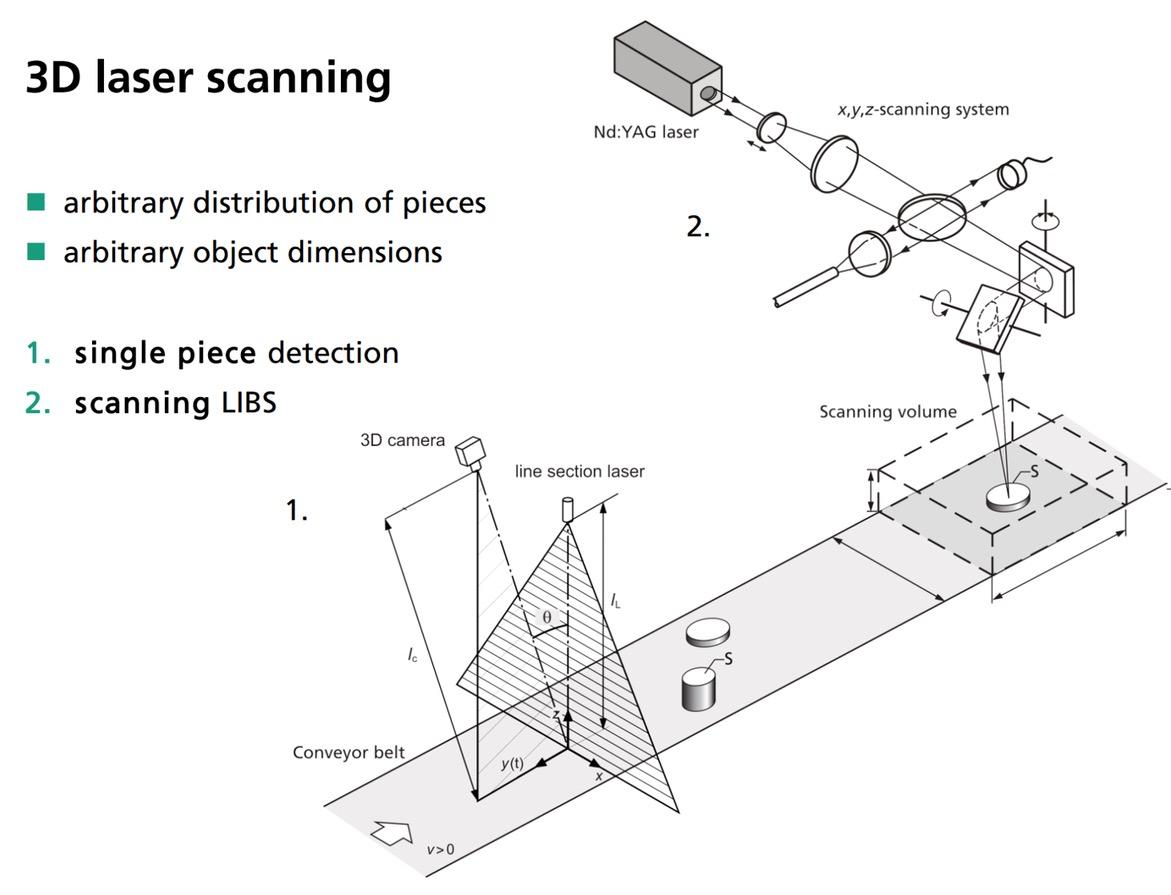

Dynamic Laser – TOMRA LIBS

3D Object Detection

https://www.parilas.eu/en/consortium.html

Scanning system

LIBS Detection

12

GAIN -

Deep Learning technology

Artificial intelligence (AI) is any technique that enables computers to mimic human intelligence, using logic, if-then rules, decision trees and machine learning.

Artificial Intelligence

Machine learning (ML) uses statistical techniques to give computer systems the ability to "learn" from data, without being explicitly programmed.

A full AI is the intelligence of a machine that could successfully perform any intellectual task that a human being can.

Machine Learning

Today narrow AI, a machine trained to do one particular task, is becoming widely used.

Deep Learning

Deep learning (DL) is a class of ML algorithms that uses a hierarchical level of artificial neural networks.

What is Deep Learning?

In Development: GAIN S Metals

Market Drivers

Market drivers & trends in metal recycling

• Huge cost impact on (primary) aluminum industry

• Focus on reducing operational costs

• Availability of human resources

• Staying local due to high transportation costs and more stringent regulations for transboundary shipments (EU)

• Need for sorting ‘waste’ (WEEE plastics, ASR) & further upgrading NF metals

• Continuing market pull for Green Aluminum & recycled content

• High demand for XRT & alloy sorting

• Global trend

‹#›

The global trend: the race to carbon neutrality

Several states have pledged/projected for carbon neutrality by:

EU Green Deal and “Fit for 55 Initiative”

• European climate law formulates legal obligation to reach climate neutrality by 2050

• Commitment by EU member stats to reduce greenhouse gas emissions by at least 55% by 2030 (compared to 1990 levels); legally binding

• Agreement reached in EU Parliament 04/2021 and EU Council approved in 05/2021

https://www.consilium.europa.eu/en/infographics/fit-for55-how-the-eu-will-turn-climate-goals-into-law/

Source: HARBOR Aluminum with Energy & Climate Intelligence Unit data; June

‹#›

2022

Canada 2050 USA 2050 UK 2050 UAE 2050 Japan 2050 EU 2050 Russia 2060 China 2060 India 2060

A few conclusions towards carbon neutrality

• The aluminum industry is spending tremendous efforts to reach the goal!

• Without a significant utilization of scrap, carbon neutrality cannot be reached!

• In order to utilize more scrap in aluminum production, clean scrap fractions are needed!

Scrap sorting by alloy is essential!

‹#›

Applications

X-Ray Transmission (XRT) technology

• Sorts metals based on atomic density

• Recovers different products

Low density

High density

Magnesium Wrought aluminum

Cast aluminum

Heavy metals

Low grade Alu (Cast)*

* Mg can be sorted into Heavy metals or Cast Alu

Alu profiles

Mixed sheet

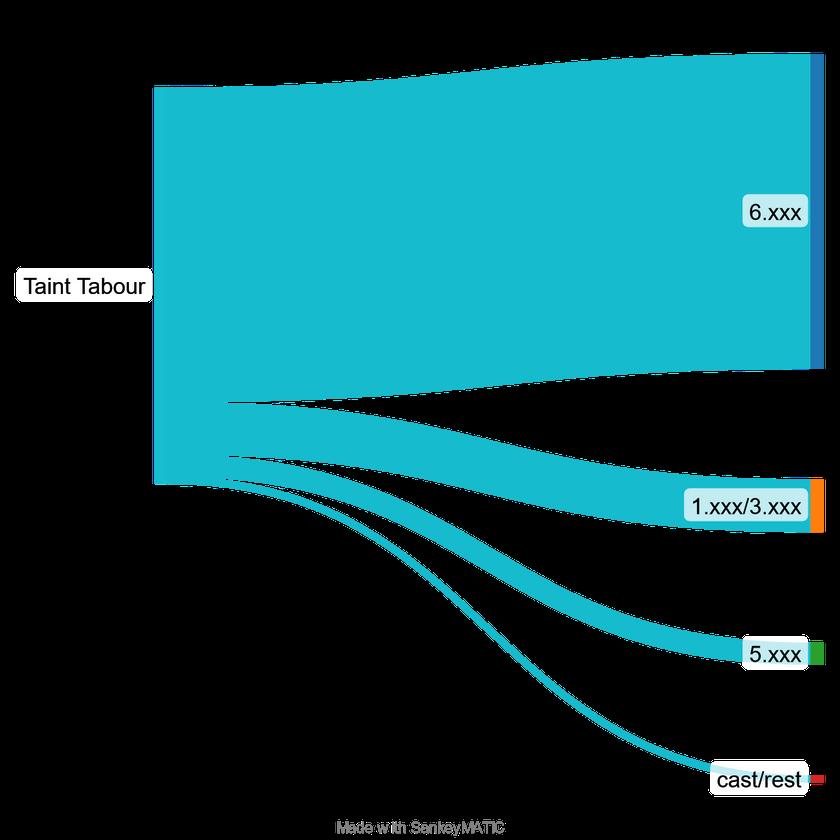

Taint Tabor

Transmissio n Heavy metals* Premium Wrought Alu

Cu ≈ 0,05-0,15% Zn ≈ 0,05-0,15% Si ≈ 0,4-1,5% Fe ≈ 0,2-0,4%

Transmissio n Heavy metals & cast alu Premium Alu Cu ≈ 0,03-0,1% Zn ≈ 0,03-0,1% Si ≈ 0,3-0,5% Fe ≈ 0,1-0,3%

Transmissio n

X-Ray

Zorba

X-Ray

X-Ray

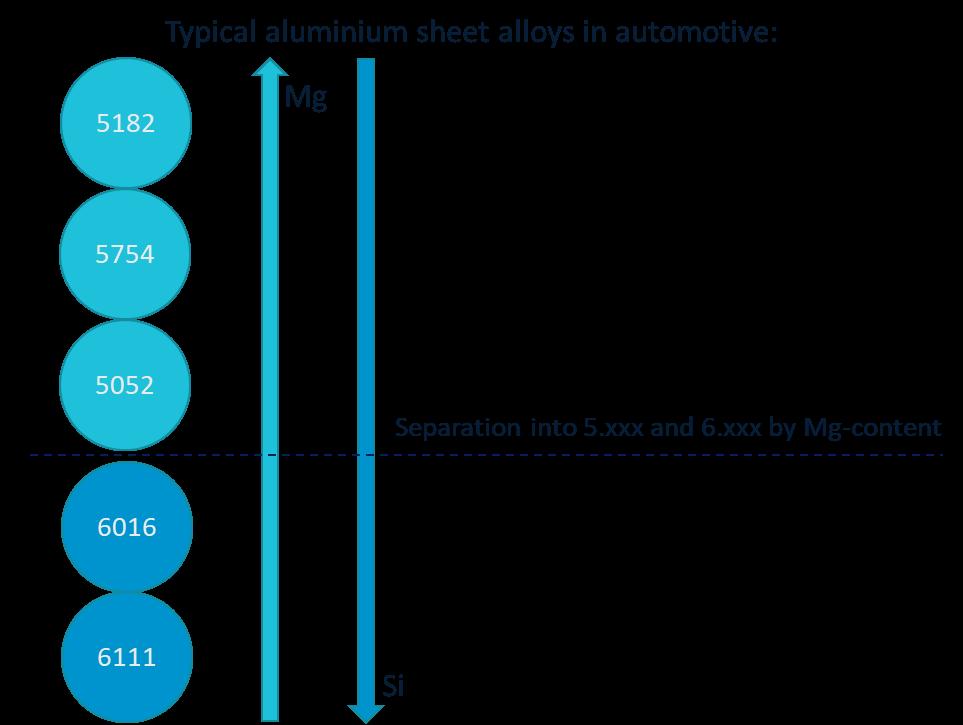

Aluminum alloys that need separation

Aluminum wrought Alloys 1xxx Al 2xxx Cu 3xxx Mn 4xxx Si 5xxx Mg 6xxx Mg, Si 7xxx Zn 8xxx Others Solved with X-Tract

Combining XRT and LIBS sorting technology

• The X-TRACT is a good sorting step in order to decrease Cu, Zn and partly Si

• This removes the 2.xxx and 7.xxx as well as the cast alloys high in copper

• In aluminium from car shredder a high content of Si typically remains

• The LIBS step can help to lower the Mg and Si level

X-TRACT Free heavy metals Cast alloys high in Cu+Zn (mainly 3xx.x) Wrought 2.xxx + 7.xxx 1.xxx 3.xxx 5.xxx 6.xxx LIBS 5.xxx 6.xxx 4.xxx Cast low in Cu/Zn

1.xxx 3.xxx 4.xxx Cast low in Cu/Zn High in Al > 5 % Si Magnesium

Opportunities for post consumer scrap

• The machine produced the groups 6.xxx, 5.xxx, 3.xxx and cast in 4 steps

• Main challenge for the future is to work on these alloying groups with:

⚬ Lacquer

⚬ Dirt

⚬ Swim - sink- flotation residues

⚬ Organic remains

⚬ Blank pieces

• The more groups are defined the better the purity and recovery results will become

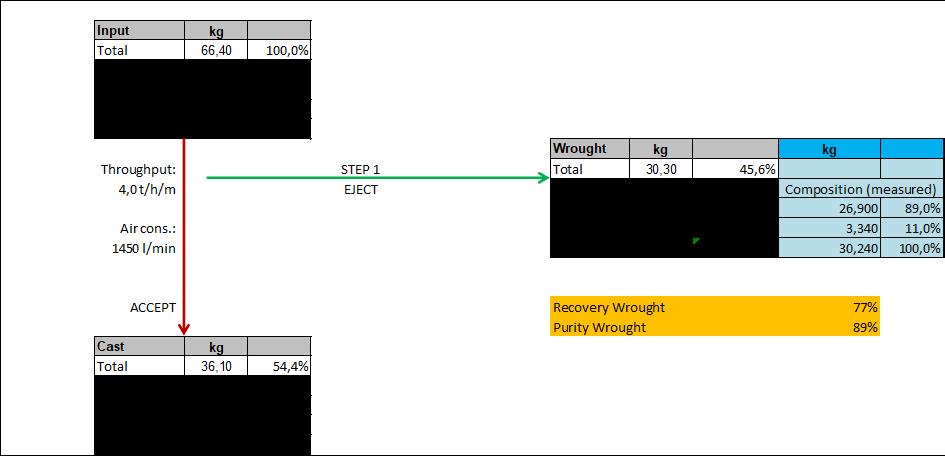

Step

Alloy group Purity Throughput (tph)

1 6.xxx 97,5% 3.8

2 5.xxx 97,7% 3.9

3 3.xxx

Step

Step

Step

89,1% 4.3

4 cast

91,0% 3.5

Opportunities for Zorba

• The main influence on the heavy metal content was done by the XRT

• A lowering of Mg and Si could be achieved by the LIBS

• An influence on the surface could not be identified

• Low alloyed cast remains in the drop fraction

Zn Cu Mg Si

4 3 2 1 0

Input step 1 (X-TRACT) step 2 (LIBS)

LIBS sorting on stamping scrap

Results matching the industry requirements:

• High throughputs that match industry standards

• High purities that enable direct scrap utilization in aluminum production.

5xxx 6xxx

Shredder Over belt Magnet Screen (30 mm)

• Results are indicative and show only one example

• Better Recovery can be achieved via adjustment of sorting settings

• Target of this attempt was to reach 90% quality with one single sorting step

Wrought vs. Cast using GAIN technology

Cast Aluminum Wrought Aluminum

Twitch Into ..

Summary

• Global market trends in metal recycling

⚬ Energy costs

⚬ Stay local

⚬ Green aluminum

• Technology & applications are developing

⚬ XRT & AS Pulse

⚬ GAIN

• Partnering for a circular future!

Eliminating Waste

Knowledge Transfer Manager -

Circular Economy

Innovate UK KTN

Mike Dines

Elle Bennett-Runton Director, Tandom Metallurgical Ltd

Laura Downey

Innovation Manager

(Sustainable Manufacturing), WMG,

University of Warwick

Jan Lukaszewski

Technical Manager, ALFED