December 2017

SPRING 2015 HIA RENOVATIONS ROUNDUP P1

HIA

Renovations activity is currently being affected by subpar economic growth with delicate consumer sentiment also holding the market back. There are favourable features of the current economic environment – interest rates are very low and stable and areas of the labour market are strong. Overall, the conditions affecting renovations work have moderated and slowed activity.

Renovations activity took a step backwards in 2017. Latest data suggest that renovations totalled $33.36 billion during the year, a reduction of 3.1 per cent on a year earlier. A majority of those included in our survey regard market conditions as being about the same as a year ago, although over one third have detected improvement.

The current economic setting means that renovations activity is forecast to suffer another 3.1 per cent reverse in 2018 before growth resumes in 2019 (+3.2 per cent). The volume of economy-wide renovations activity is determined by dozens of different factors, the most important of which is the age profile of the detached house stock. Over the next few years, the number of houses aged between 30

and 35 years will increase significantly – widening the scope for growth in renovations demand over the coming years. Accordingly, the volume of renovations activity is forecast to rise by 5.7 per cent in 2020 and grow by another 0.9 per cent in 2021 taking the total value of the market to $35.57 billion.

This edition of the HIA Renovations Roundup includes the results of the market survey which received a total of 595 responses from those operating in the industry. The main findings of the survey are that:

The renovations industry is made up of a very large number of small-scale operators and represents a highly competitive market structure

Labour and materials are the largest sources of cost pressures in the market although 15 per cent of operators experienced no cost pressures over the past year

Kitchen renovations and repairs/maintenance jobs are the largest sources of renovations work

The global economy continues to improve steadily with unemployment down below the levels it had been at prior to the outbreak of the GFC a decade ago. Job creation is being sustained by the still exceptionally accommodative monetary policies on offer in advanced economies – low interest rates are boosting demand while subdued wage pressure has made it more attractive for firms to hire additional labour. There have been interest rate increases in the US and Britain over the past six months but these have been small and measured – the cost of borrowing is still very low by historic standards.

For Australia’s economy, the favourable global environment has helped conditions in areas of the economy that rely on demand from overseas. The weaker exchange rate has also been welcome from this perspective. Tourism, international education, commodities exports, financial services and consultancy are but a few of the activities that are reaping the dividends of the global recovery. The structure of the NSW and Victoria economies means that these states have been best positioned to benefit – the remarkable employment gains in both bear this out.

At 5.4 per cent in October, the rate of unemployment is at its lowest in about five years. This is a clear sign that things are moving in the right direction – further improvements would bring the labour market close to full employment. The pace of job creation in the Australian economy is very robust, with the number of people employed in the economy up by 2.9 per cent over the past year and full-time employment growth running at its fastest pace in a decade. Considering that GDP growth was just 2.8 per cent over the year to September, the labour market is getting very good bang for its buck in terms of the conversion rate from economic activity to jobs growth.

The uplift in new home building from its trough in 2012 to the all-time high in 2016 has been a major source of growth for Australia’s economy at a time when mining project investment was coming off the boil quite rapidly. Now that new home building activity is moving back towards lower levels, a gap is opening up on the economic growth ledger. Government capital and infrastructure investment is helping to plug some of the void, but several areas of demand like household consumption and business investment have yet to gain sufficient traction.

General price pressures in the Australian economy are still very weak - the headline rate of inflation was just 1.8 per cent during the September 2017 quarter. The fact that Australia has avoided a major bout of inflation over recent years is very fortunate in the context of the significant depreciation in the dollar’s exchange rate and the considerable dwelling price gains in key markets over the past five years.

The combination of below par economic growth, subdued price and wage pressures and an exchange rate in a fairly optimal position means that the RBA has little basis for increasing interest rates over the short term

About one quarter of firms typically work on jobs worth less than $40,000. For another quarter the typical job size is in excess of $200,000.

Seven out of eight firms experienced cost pressures over the past 12 months, most commonly for labour and materials.

About three quarters of survey respondents typically engage in renovations work on dwellings that are at least 20 years old

The HIA Renovations Roundup report includes a survey of the market conducted on a quarterly basis. The current survey took place during November 2017 and received a total of 595 responses. It included renovators active in all eight states and territories. The largest proportion of responses was received from New South Wales and Victoria (each accounting for 30 per cent of the total) followed by Queensland (17 per cent of responses).

Based on the 595 responses received to the latest HIA renovations market survey, the profile of the home renovations industry again suggests a highly competitive structure made up of a very large number of small firms and

operators. The survey reveals that:

One fifth (20 per cent) of renovations market operators are sole traders;

The most common scale of firm involved the employment of no more than five staff (59 per cent);

One in eight renovation firms (12 per cent) employ between six and ten staff;

A tiny proportion (1 per cent) have 50 or more employees.

The implications of this market structure is very favourable from a consumer’s perspective. It ensures that the market outcomes will tend to gravitate towards good value for money and that considerable diversity exists in terms of the breadth of services offered

Cost pressures have been experienced by most firms in the renovations market over the past 12 months (85 per cent of the total). This is against what appears to be relatively subdued cost pressures across the economy –the rate of inflation is currently at 1.8 per cent and wages growth is close to a 20-year low (+2.0 per cent).

The interest rate environment is already extraordinarily positive: never before has the cost of borrowing been so low and so stable. Despite these positives from a ‘cost of doing business’ perspective, there is a clear pattern to the cost pressures suffered by the 595 renovations market survey participants

Labour costs are the single largest source of cost pressures for renovators, with 62 per cent of survey participants being affected over the past 12 months;

Materials were the source of cost pressures for 39 per cent of market participants;

Taxation and government charges affected 37 per cent of those in the survey;

Other sources of cost pressure included professional fees (19 per cent) and finance costs (10 per cent)

Encouragingly for them, 15 per cent of those included in the survey did not experience cost pressures from any source over the past 12 months. This is a little higher than in the survey this time last year (13 per cent)

Have you found any of the following to be a source of cost pressure to you over the past three months?

The scale of individual renovations jobs varies widely and it is therefore difficult to conceive of the ‘typical’ renovations job. The vast bulk of renovations jobs are not substantial enough to require local authority approval – only a minority of jobs require permission to proceed.

The chart below summarises the responses of the 595 renovations market participants with respect to the value of the typical renovations job done by them over the past three months.

About one in seven renovations jobs are small in that they are valued at no more than $12,000;

The single most common price bracket for a renovations job is between $12,000 and $40,000

about one in five are estimated to lie in this category;

A substantial portion (24 per cent) of renovations jobs are on the large side – valued at $200,000 or more. Almost 30 per cent of renovations jobs lie in a wide price range between $70,000 and $200,000

Over the past three months, what was the average value of your renovation jobs?

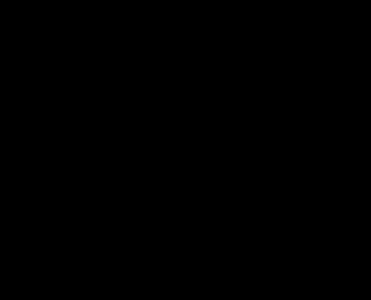

There is a strong relationship between the age of a dwelling and the likelihood of it receiving renovations work. Detailed HIA research indicates that the strongest linkage is between detached houses in the 30 to 35 year age group and the amount of renovations work which takes place across the economy. The nature of this relationship acts as one of the key bases for our forecasts of renovations activity.

The survey results shown below highlight the relationship between renovations activity and the age of

a dwelling. According to this, a majority (59 per cent) of renovations jobs are performed on homes aged between 16 and 40 years (age as estimated by the survey respondent). About one in five jobs (19 per cent of the total) were performed on homes aged 50 years or more. Less than one in ten renovations jobs were conducted on homes built 15 years ago or less. This is explained in greater detail in the Future Prospects for Renovations Activity section of the report

What do you estimate was the typical age of dwellings you undertook renovation jobs on during the past three months?

Older than 50 years

Between 41 and 50 years old

Between 31 and 40 years old

Between 21 and 30 years old

Between 16 and 20 years old

Between 11 and 15 years old

Between 6 and 10 years old

Less than 5 years old

Kitchen renovations accounted for the largest share of jobs done in the latest survey round with respondents indicating a 33 per cent share for this kind of work. Repairs and maintenance jobs continue to be a very important source of demand in the home renovations market, making up 23 per cent of the total. Bathroom renovations account for 9 per cent of the total.

Kitchens

Repairs / Maintenance

Other renovations work

Bathrooms

External Work

Ground floor extensions

Roofing & Cladding

Garages/Carports

Multi-level extensions

Large structural renovations work accounts for a surprisingly minor share of the recent work load. External work makes up 6 per cent of total jobs, followed by ground floor extensions (4 per cent), garages/carports (3 per cent) and multi-level extensions (2 per cent)

It is estimated that renovations activity will have shrunk by 3.1 per cent during 2017 – following an expansion of 2.1 per cent in 2016

Renovations activity fell back by 5.0 per cent during the September 2017 quarter to reach $8.12 billion in value

Just over one half of survey participants did not experience any significant change (for better or worse) in market conditions over the past year

The employee headcount remained unchanged in a majority of renovations firms over the past year (56 per cent of the total)

The ABS data indicates that the value of home renovations totalled $34.01 billion over the 12 months to September 2017. This is the highest total for a 12-month period since 2012 and is consistent with the trend of recovery that has been active in renovations activity over recent years. During the September 2017 quarter itself, the volume of renovations activity suffered a 5.0 per cent reverse compared with the previous quarter – falling to $8.12 billion. This was 4.8 per cent down on the same period last year, a period which saw lukewarm growth in household consumption generally. It is important to note that that the official ABS data on renovations activity have recently been revised substantially and rebased. This means that discrepancies exist

between the data in this edition of Renovations Roundup and figures reported in previous editions.

Being a ‘big ticket’ expenditure item, renovations activity does tend to fluctuate more dramatically than most other components of consumer demand. In this way, the fate of home renovations activity tends to travel a similar path to vehicle sales, which also fell - by 3.0 per cent - over the year to October 2017.

As the chart below shows, the home renovations market is still engaged in a fairly hesitant recovery and the volume of activity is still well below the peak reached during 2011 when renovations activity totalled some $36.54 billion over the course of the year. Renovations activity is still some 6.9 per cent below this peak

The perceptions of those active in the market are largely consistent with the official data suggesting that little change in the home renovations market has occurred. A majority of respondents (56 per cent) did not discern any major difference (for better or for worse) in market conditions over the past year.

Amongst those that did experience changed conditions over the past year, those sensing improvement (38 per cent) easily outnumbered those seeing deterioration in the market (9 per cent of the total)

Employment developments in the renovations industry are also a good barometer of the sector’s health. On this score, the impression is of fairly flat conditions: a majority of firms (56 per cent of the total) neither increased nor reduced the employee headcount over the

Howdoes activity in the current renovations market compare with this time last year? Fewer

past 12 months. Of those that did alter the size of their workforce, 25 per cent increased the number of employees while slightly fewer (19 per cent) cut back on staff numbers. The general impression is one of an industry which has been largely static over the past year.

Are you employing more or fewer people than this time last year?

Overall, we anticipate that the size of Australia’s renovations market will increase by 6.6 per cent between 2017 and 2021

The short-term outlook for home renovations demand is weighed down by sluggish pace of economic growth and the low volume of turnover in the established house market

Home renovations activity is projected to decline by 3.1 per cent in 2018 with growth resuming in 2019 (+3.2 per cent)

The medium term outlook for renovations activity will benefit from the significant expansion in the stock of 30-35 year old dwellings underway

During 2020, the pace of expansion is set to accelerate to 5.7 per cent before decelerating to 0.9 per cent in 2021

As touched on by some of the survey results, developments with respect the age of the detached house stock have a major impact on the volume of renovations work done. Specifically, detailed analysis by HIA indicates that detached houses in the 30 to 35-year age group have the greatest influence on the amount of renovations work done and our medium/long term forecasts for renovations activity are made on this basis.

Between 2017 and 2020, the number of houses in this key age bracket is set to expand by 8.3 per cent as a result of the record volume of new detached house building in the late 1980s. Growth in the main renovations cohort will slow between 2020 and 2023 with a 1.9 per cent expansion in the stock being followed by a 2.6 per cent increase between 2023 and 2026. Accordingly, the volume of renovations activity is projected to decline by 3.1 per cent during 2018 with growth of 3.2 per cent returning in 2019. Activity will speed up in 2020 (+5.7 per cent) before a deceleration to 0.9 per cent occurs in 2021. Overall, this is anticipated to bring the volume of renovations activity from $32.32 billion in 2018 to $35.57 billion in 2021. The amount of ‘major’ renovations work (requiring local authority approval) is projected to rise from $7.53 billion in 2018 to $7.87 billion in 2021.

Like most facets of economic activity, home renovations in Australia is determined by a large number of factors – not all of which are moving in the same direction. The most important of these are summarised in the colour-coded table below. At present, a handful of settings are favourable from the

point of future renovations demand:

Interest rates are still remarkably low and the likelihood of increases in the near future has retreated. This means that the cost of borrowing for home renovations work remains manageable and keeps a lid on the interest outgoings of renovation firms. Some homeowners will also decide that using cash savings to fund valueenhancing home renovations work is preferable to the very low return on bank deposits

Full-time employment growth is currently the strongest it has been in a decade – meaning that substantial numbers of people are moving from part-time to full-time work. A portion of the large cohort of people who have secured fulltime jobs will leverage off their improved earnings capacity and commence home renovations work

Economic growth remains in positive territory and the world economy is continuing to demand resources from Australia, pulling our economy forward

A further set of economic conditions are less favourable and will tend to dampen growth prospects for the sector.

The deceleration of dwelling price growth is slowing the accumulation of home equity – an important financing channel for home renovations work

Wages growth remains close to a 20-year low and is flat in real terms

Australia’s economy is still growing below the longterm average and large portions of business investment are stuck in the doldrums

Commodities prices have lost huge ground in the last few years and appear shaky at present

Economic Growth

Interest Rates

Consumer Sentiment

Exchange Rate

Commodities Prices

House Prices

Renovations Lending

Major Renovations Approvals

Unemployment

Employment Growth

Established House Sales

Renovations Market Expectations

Wages Growth

Household Consumption

Vehicle Sales

Rental Price Growth

2017 to 2020

2020 to 2023

2023 to 2026

Consumer sentiment has been stuck on the wrong side of glum over the last 12 months

Rental inflation is at its slowest since late 1993 and restricts the scope for landlord-funded renovations work in investment properties

Established house market turnover appears to have plunged over the past year, depriving the renovations market of one of its most important triggers for new jobs.

Our forecasts for renovations activity take account of all of these factors and reflect a balanced view as to the likely short-term growth trajectory. Ultimately, this will see the market activity contract again during 2018 before recovery takes hold in 2019.

September 2017

December 2017

November 2017

December 2017

December 2017

November 2017

Annual rate of GDP growth remains below trend at 2.8 per cent - up by 0.6 per cent on previous quarter.

RBA's interest rate is very low at 1.50 per cent and unlikely to increase in near future.

Has been in slightly pessimistic territory every month since December 2016.

Exchange rate has weaken a little over recent months to approach 75c v USD.

Well below the highs reached earlier in the decaderecovery has run out of steam.

Capital city house prices up by 5.5% year-on-year - up by 0.2% during the quarter. Marked deceleration appears to be underway.

September 2017 Latest quarter is 4.9% higher than a year earlier.

October 2017 3 months to October is 7.8 per cent up on a year earlier.

October 2017 Unemployment rate at 5.4% - lowest since January 2013.

October 2017

Annual employment growth at 2.9%; full-time employment growth is strongest in a decade.

November 2017 Down 44.2 per cent on a year earlier.

November 2017

September 2017

September 2017

October 2017

Those expecting improvement (38%) outnumber those anticipating deterioration (3%). Majority (59%) foresees no major change.

Annual wage growth at 2.0%, up 0.5% on previous quarter.

Annual growth has slowed to 2.2% with a minimal 0.1% increase in quarterly terms.

Passenger vehicle/SUV sales down 3.0 per cent year-onyear.

September 2017 At 0.5%, annual rental inflation is at its lowest since 1993.

December 2017 Set to increase by 8.3 per cent between 2017 and 2020

December 2017 Projected to rise by 1.9 per cent over 2020 to 2023 period

December 2017 Will grow by 2.6 per cent between 2023 and 2026

The balance of economic settings described above suggests a subdued outlook for renovations activity over the short-term – the expectations of firms in the renovations market largely fit with this. Of those taking part in the latest renovations market survey, a firm

majority (59 per cent of the total) do not expect market conditions to improve or deteriorate. It is worth emphasising that those anticipating improvement (38 per cent) far outnumber the 3 per cent of respondents anticipating deterioration

Howdo you expect renovations activity to be in one years time?

The hiring intentions of renovation firms also offer a perspective on how much scope for expansion the market is perceived as offering over the near term. The November 2017 survey responses indicate that expectations are mildly positive: a majority of

respondents (54 per cent) does not see their employee headcount changing over the next year. However, 40 per cent of renovation firms intend to increase their headcount over the next 12 months compared with just 6 per cent who intend to reduce staffing levels.

Are you expecting to employ more next year?

For the NSW renovations market, 2017 has been a tough year with activity expected to have fallen back by 5.1 per cent following a 1.6 per cent contraction during 2016

The big dip in established house transactions in Sydney appears to be squeezing the local renovations market

Compared with the rest of Australia, the expansion in the stock of houses of key renovations age in NSW will be modest over the next few years.

We project that renovations activity will decline by another 5.9 per cent in 2018 followed by growth of 1.1 per cent in 2019. In 2020, the market is predicted to increase by 3.7 per cent with a 0.8 per cent expansion in 2021.

Accordingly, the size of NSW’s renovations market is forecast to increase from $11.31 billion in 2018 to $11.95 billion in 2021.

Major renovations activity is projected to rise from $2.66 billion to $2.83 billion over the same timeframe

Sydney prices up by 5.0 per cent year-on-year - down 1.3% over the quarter

Renovations Lending September 2017 Up by 8.4% on a year earlier. Major Renovations Approvals

with

Having grown during 2015 and 2016, renovations activity in Victoria is likely to have expanded by 3.4 per cent during 2017 to reach $8.81 billion

The home renovations market in Victoria is benefitting from the continued strength of house price growth in Melbourne and the remarkable degree of job creation in the local labour market

Over the period to 2020, the stock of detached houses in the key renovations age bracket will rise very substantially providing the fuel for further growth in renovations demand

The volume of renovations activity in Victoria is projected to inch up by 0.2 per cent in 2018 with the growth rate accelerating to 6.4 per cent in 2019 and reaching 6.6 per cent in 2020. The pace of expansion is then projected to slow to 1.0 per cent in 2021.

This means that Victoria’s home renovations market is predicted to expand from $8.84 billion in 2018 to $10.13 billion in 2021. The ‘major renovations’ component of the market is anticipated to grow from $2.67 billion to $2.83 billion over the same timeframe

House Prices

Renovations Lending

Major Renovations Approvals

Unemployment

Employment growth

Established House Sales

November 2017

September 2017

October 2017

October 2017

October 2017

November 2017

Melbourne house prices up by 10.1% year-on-year - up by 1.9% over the quarter.

Up by 10.1% on the same period a year earlier.

Up by 3.6% on 12 months previously.

At 5.7%, unemployment is at a 15-month low.

Total employment up 3.1% year-on-year; Full-Time jobs up 3.6%.

Down by 45.5% on a year ago.

2017 to 2020

2020 to 2023

2023 to 2026

December 2017

December 2017

December 2017

Set to rise by 14.7 per cent between 2017 and 2020.

Predicted to fall by 8.0 per cent between 2020 and 2023.

Renovations

Investment

25%

20%

15%

10%

5%

Stock of -15%

30-35 -10%

0%

-5%

30% Jun-1994 Jun-1995 Jun-1996 Jun-1997 Jun-1998 Jun-1999 Jun-2000 Jun-2001 Jun-2002 Jun-2003 Jun-2004 Jun-2005 Jun-2006 Jun-2007 Jun-2008 Jun-2009 Jun-2010 Jun-2011 Jun-2012 Jun-2013 Jun-2014 Jun-2015 Jun-2016 Jun-2017

Renovations activity in Queensland is expected to have declined by 3.9 per cent in 2017 following growth of 10.2 per cent during 2016

Compared with other states, unemployment in Queensland is above the national average and dwelling price growth has been slower than in other markets. This has taken its toll on the local renovations market over the past year and will depress activity over the short term

Over a longer horizon, demand for renovations work in Queensland will benefit considerably from a substantial increase in the pool of detached houses within the prime renovations age group.

We project that renovations work will decline by another 4.4 per cent in 2018 with growth returning in 2019 (+3.7 per cent). In 2020, the pace of expansion is anticipated to accelerate to 5.9 per cent with growth easing to 1.2 per cent in 2021.

Accordingly, the state’s renovations market is forecast to grow from $5.82 billion in 2018 to $6.67 billion in 2021. In contrast, the ‘major renovations’ portion of the market is anticipated to slide from $1.02 billion to $965 million over the same period

House Prices

Renovations Lending

Major Renovations Approvals

Unemployment

Employment growth

Established House Sales

2017 to 2020

2020 to 2023

2023 to 2026

November 2017

September 2017

Brisbane house prices up by 2.4% year-on-year - up by 0.6% over the quarter.

Down by 2.7% on the same period a year earlier.

October 2017 Up by 16.5% on 12 months previously.

October 2017

October 2017

Unemployment rate has edged up from 5.9% to 6.0% over past 12 months.

Total employment up 4.7% year on year; Full-Time jobs up 2.9%.

November 2017 Down by 56.4 per cent on a year ago.

December 2017 Set to rise by 5.1 per cent between 2017 and 2020.

December 2017 Predicted to expand by 16.8 per cent between 2020 and 2023.

December 2017 12.4 per cent growth forecast over 2023 to 2026 period.

Conditions in South Australia’s renovations market have been recovering, with growth of 9.2 per cent in 2016 and another increase of 1.2 per cent in 2017

The local market’s short term growth prospects are being frustrated by weak dwelling price growth, and a shrinking number of houses in the most renovation-intensive age group

There is real scope for growth in renovations demand in SA over the medium term with the stock of detached houses in the crucial 30-35 year age group set to expand strongly from about 2020 onwards

For SA, we project that renovations activity will slip by 0.1 per cent in 2018 and ease back by another 0.6 per cent in 2019. An emphatic recovery will take hold in 2020 (+5.7 per cent) with further growth of 1.1 per cent projected for 2021

This means that the size of the SA renovations market is expected to grow from $2.15 billion in 2018 to $2.28 billion in 2021. The ‘major renovations’ segment of the market is expected to remain static at around $420 million over the same period

House Prices

Renovations Lending

Major Renovations Approvals

Unemployment

Employment growth

Established House Sales

2017 to 2020

2020 to 2023

2023 to 2026

November 2017

September 2017

October 2017

October 2017

October 2017

November 2017

December 2017

December 2017

December 2017

Adelaide house prices up by 3.4% year-on-year - rose by 0.1% over the quarter.

Down by 1.6% on 12 months ago.

Fell by 1.2% compared with the same period a year earlier.

Unemployment rate has fallen from 6.5% to 5.8% over past 12 months.

Total employment up 1.6% year-on-year; Full-Time jobs increased by 2.0%.

Down by 5.8 per cent on a year earlier.

Projected to fall back by 1.8 per cent between 2017 and 2020.

Set to expand by 8.3 per cent between 2020 and 2023.

Forecast to rise by 9.9 per cent over 2023 to 2026 period.

WA’s renovations market has endured yet another year of difficult conditions in 2017. The level of activity is shaping up to have declined for a second consecutive year, this time by some 11.8 per cent.

Declining dwelling prices amid the painful economic adjustment to post-mining boom economic conditions are key factors behind the persistent weakness in the state’s renovations market.

The stock of houses of key renovations age in WA is set to expand substantially between 2017 and 2020, providing a major source of support for activity in the market over the near to medium term.

We expect that the period of declining renovations activity in WA is almost over. We are forecasting renovations activity to edge lower by 1.0 per cent in 2018 before growth returns to the market in 2019 (+4.0 per cent) and then gathers momentum in 2020 (+10.6 per cent). The pace of growth is forecast to moderate to 1.6 per cent in 2021.

The size of WA’s renovations market is forecast to increase from an estimated $3.01 billion in 2017 to $3.48 billion in 2021. Major renovations activity is projected to rise from $452 million to $531 million over the same timeframe

House Prices

Renovations Lending

Major Renovations Approvals

Unemployment

Employment growth

Established House Sales

2017 to 2020

November 2017

September 2017

October 2017

October 2017

October 2017

November 2017

December 2017

Perth house prices down by 2.6% year-on-year - up by 0.3% over the quarter.

Down by 21.3% on the same period 12 months earlier.

Up by 5.5% on the same period of last year.

Unemployment rate has fallen from 6.4% to 5.9% over the past 12 months.

Total employment up by 2.9% year-on-year; Full-Time jobs increased by 4.3%.

Down 44.4% on a year earlier.

Projected to expand by 22.3 per cent between 2017 and 2020.

2020 to 2023

December 2017

Set to decline by 2.7 per cent between 2020 and 2023. 2023 to 2026

December 2017

Forecast to rise by 5.5 per cent over 2023 to 2026 period.

Source: ABS 5206

2017 has emerged as yet another difficult year for Tasmania’s renovations market. Following a sharp contraction in 2016 (a fall of some 26.1 per cent), the level of total renovations activity is estimated to have declined by 11.3 per cent in 2017.

The broader economic rejuvenation taking place in Tasmania has yet to filter through to the renovations market. Factors that would otherwise be supportive of renovations activity – rising house prices, low interest rates and an improving labour market – have not yet given the industry a boost in activity.

The stock of houses of key renovations age in Tasmania is set to expand between 2017 and 2020, providing a major source of support for activity in the market over the near to medium term.

The recessionary conditions in Tasmania’s renovations market are nearly at an end. We are forecasting renovations activity to edge lower by 0.9 per cent in 2018 before growth returns to the market in 2019 (+2.3 per cent). We project that this burst of growth will continue into 2020 (+3.2 per cent) and 2021 (+0.2 per cent).

The size of Tasmania’s renovations market is forecast to increase from an estimated $519.8 million in 2017 to $544.7 million in 2021. Major renovations activity is projected to shrink from $100.1 million to $91.2 million over the same timeframe

House Prices

Renovations Lending

Major Renovations Approvals

Unemployment

Employment growth

Established House Sales

2017 to 2020

2020 to 2023

2023 to 2026

November 2017

September 2017

October 2017

October 2017

October 2017

November 2017

December 2017

December 2017

December 2017

Hobart house prices up by 11.5% year-on-year - up by 3.3% over the quarter

Down by 4.7% on the same period last year.

Down by 10.0% on a year earlier.

Unemployment has eased from 6.4% a year ago to 6.1% today.

Total employment up by 3.2%; Full-Time jobs fell by 0.3%.

Down 50.8 per cent on a year earlier.

Projected to expand by 7.7 per cent between 2017 and 2020.

Set to grow by 1.6 per cent between 2020 and 2023.

Forecast to rise by 4.1 per cent over 2023 to 2026 period.

Despite the painful economic adjustment to post-mining boom conditions, the NT’s renovations market performed reasonably well in 2017. It appears likely that the volume of work expanded by 1.3 per cent during the year,

While the increase in activity was relatively modest, it is quite an achievement given the unfavourable state of a number of important economic indicators in the NT

Crucially, the most influential driver of activity – the stock of houses of key renovations age – is set to work against growth prospects over the near to medium term, with the number of houses in this age group set to fall substantially until 2023

We are forecasting renovations activity to decline by 5.7 per cent in 2018 and by another 2.7 per cent in 2019. Some lost ground will be won back in 2020 (+1.5 per cent), before the trend of decline returns in 2021, with activity forecast to shrink by 5.2 per cent

The size of the NT’s renovations market is forecast to contract from $264.5 million in 2017 to $233.4 million in 2021. Major renovations activity is projected to shrink substantially, from $84.2 million to $65.9 million over the same horizon

House Prices

Renovations Lending

Major Renovations Approvals

Unemployment

Employment growth

Established House Sales

Stock of 30-35 Year Old Houses

2017 to 2020

2020 to 2023

2023 to 2026

Source: ABS 5206

November 2017

September 2017

October 2017

October 2017

October 2017

November 2017

December 2017

December 2017

December 2017

Darwin house prices down by 5.5% year-on-year - down by 2.7% over the quarter.

Down by 17.5% on the same period last year.

Down by 27.9% on a year earlier.

Unemployment has risen to 18-month high of 4.2%.

Total employment down 1.8% year-on-year; Full-Time employment fell by 3.1%.

Down 20.9% on a year earlier.

Projected to contract by 26.3 per cent between 2017 and 2020.

Set to decline by a further 20.6 per cent between 2020 and 2023.

Forecast to rise by 23.8 per cent over 2023 to 2026 period.

2017 has emerged as yet another difficult year for the ACT’s renovations market. Following a sizeable decline in 2016 (-6.7 per cent), total renovations activity is estimated to have edged lower again by 0.3 per cent in 2017

The key factors that drive renovations activity were mixed during 2017 and have ultimately proven to be of little support to the renovations market. There have been modest increases in house prices and mixed signals from the labour market, while established house sales are down quite significantly

The stock of houses in the key renovations age group however is set to expand over the near to medium term, which should provide some support for a recovery in the market

We are forecasting the downturn in activity to continue into 2018 (-5.6 per cent). We expect a return to growth in 2019, with activity forecast to rise by 1.6 per cent, followed by further growth of 4.1 per cent in 2020

We expect the shrinking stock of houses in the key renovation age group to then weigh on activity in 2021, with total renovations forecast to decline by 3.0 per cent

The size of the ACT’s renovations market is forecast to shrink from an estimated $498.3 million in 2017 to $482.6 million in 2021. Major renovations activity is projected to decline from $144.9 million to $136.4 million over the same timeframe

House Prices

November 2017

Renovations Lending September 2017

Major Renovations Approvals

Unemployment

Employment growth

Established House Sales

2017 to 2020

2020 to 2023

2023 to 2026

Canberra house prices up by 5.8% year-on-year - up by 1.3% over the quarter.

Down by 14.7% compared with the same period last year.

October 2017 Has fallen by 13.1% since the same time 12 months ago.

October 2017

October 2017

Unemployment has drifted from 3.6% to 3.8% over past year.

Total employment up 2.6% year-on-year; Full-Time jobs growth at 1.7%.

November 2017 Down 19.1% on a year earlier.

December 2017

December 2017

Set to increase by 5.6 per cent between 2017 and 2020.

Projected to fall by 18.7 per cent over 2020 to 2023 period.

December 2017 Will grow by 3.2 per cent between 2023 and 2026.

This publication is produced by HIA Economics based on information available at the time of publishing. All opinions, conclusions or recommendations are reasonably held or made as at the time of its compilation, but no warranty is made as to accuracy, reliability or completeness. Neither HIA nor any of its subsidiaries accept liability to any person for loss or damage arising from the use of this report.

Confidential Information: This report is confidential to the addressee. It may not be copied or transmitted in whole or in part in any form, including by photocopying, facsimile, scanning or by manual or electronic means. Multiple copies can be supplied by arrangement/for an additional charge. Unauthorised copying is a breach of HIA’s copyright and may make you liable to pay damages.