Ghana's dormant accounts hold $31 million in forgotten funds Story on page 2

State-owned cocoa processor slumps to $13.08m nine-month loss

on page 2

Betpawa to invest $10m in African sports development over next five years Story on page 4

… expands ‘locker room’ bonus to women’s league and technical sta in Ghana

Sustainable Insurance: The Dilemma of SMEs in Africa

Africa's built environment leaders to converge at ACEACRES 2024 Summit

Story on page 3 Story on page 5

Copyright @ 2019 Business24 Limited All Rights Reser ved

Your subscription along with the suppor t of businesses that adver tise in Business24 -- makes an investment in journalism that is essential to keep the business community in Ghana wellinformed.

We value your suppor t and loyalty

Contact : editor@business24 com gh Newsroom: 030 296 5315

Adver tising / S ales: +233 24 212 2742

Ghana's dormant accounts hold $31 million in forgotten funds

By Benson Afful

The Institute for Liberty and Policy Innovation (ILAPI) has uncovered signi cant sums in dormant accounts with the Bank of Ghana (BoG). Between 2016 and 2023, over GH¢167.8 million, $14.6 million, GBP 2.4 million, and EUR 2.3 million accumulated in these accounts. Additionally, 1,448,660 dormant accounts were transferred to the BoG between 2021 and July 2024.

ILAPI's Next of Kin project aims to facilitate access to these funds, streamlining legal proce-

dures and addressing complexities. Currently, securing Letter of Administration, Death Extract, and navigating probate processes can be cumbersome, leading to abandoned claims and prolonged poverty.

The BoG transfers dormant accounts to its registry after ve years of inactivity, as per Section 92 of the Banks and Specialized Deposit-taking Institutions Act, 2016. ILAPI recommends:

- Enhancing public education on next-of-kin appointments

- Issuing directives for banks to request Ghana Card information

- Clearly de ning dormant account management policies

- Reviewing laws to enable BoG to trace bene ciaries

- Releasing annual reports on dormant accounts

- Collaborating with local government to identify bene ciaries

ILAPI commends the BoG's literacy campaigns but urges proactive measures to address transparency, nancial governance, and economic challenges faced by eligible families.

State-owned cocoa processor slumps to $13.08m nine-month loss

The state-owned Cocoa Processing Company Limited (CPC) continues to grapple with deepening nancial challenges, posting a substantial $13.08 million loss for the nine-month period ending September 30, 2024.

This marks a 5.6% increase from the $12.38 million loss recorded in the same period last year.

The increase in losses is primarily attributed to escalating operational costs, especially in selling, distribution, and nancial expenses.

According to its September 2024 Unaudited Financial Statement,

CPC’s total revenue for the third quarter of 2024 declined to $31,096,542, down from $32,344,232 for the same period last year, re ecting a 3.86% decrease.

Additionally, the company’s production signi cantly dropped during the period under review.

Cocoa beans processed plummeted to 3,256 metric tonnes from 7,051 metric tonnes in 2023.

Semi- nished products packed fell to 2,483 metric tonnes from 5,836 metric tonnes, and confectionery products packed also declined, recording 1,429 metric tonnes from 1,699 metric tonnes.

To address its mounting challenges and steer towards pro tability, CPC has secured a commitment from COCOBOD to continue supplying cocoa beans to meet its operational needs.

Crucially, COCOBOD will not demand repayments in a manner that jeopardizes CPC’s operations.

The Board of Directors has implemented several measures aimed at turning the company around and achieving pro tability.

These measures include cost-cutting, investing in infrastructure and machinery, and expanding

the revenue base.

In a bid to bolster its nancial position, CPC’s management is in discussions with the African Export-Import Bank (Afreximbank) to secure an $86.7 million loan facility.

This loan is intended to settle outstanding amounts due to a syndicate of banks, support working capital requirements, and upgrade property, plant, and equipment to expand production capacity.

Management anticipates signing the agreement by December 2024, with the rst tranche of the loan to be disbursed by March 2025

Betpawa to invest $10m in African sports development over next five years

By Eugene Davis

… expands ‘locker room’ bonus to women’s league and technical sta in Ghana

Betpawa, a prominent online betting and gaming brand, has announced plans to invest $10 million across Africa over the next ve years to support sports development, aligning with its broader growth strategy on the continent.

During a press brie ng in Accra on Tuesday, Betpawa's Chief Commercial O cer, Ntoudi Mouyelo-Katoula, highlighted the brand’s commitment to expanding its initiatives beyond Ghana. "We are extending the Locker Room Bonus to other competitions across Africa. Our goal over the next ve years is to channel over $10 million into impactful initiatives throughout the continent," he stated.

In Ghana, Betpawa has already established itself as a key supporter of local sports, sponsoring winning teams in the domestic league through an innovative “Locker Room” initiative, which provides players with instant bonuses via online payment. This year, Betpawa has expanded the initiative to include the women’s league, starting from the Round of 16 up to the nals.

Emphasizing the importance of its partnership with the Ghana Football Association, Mouyelo-Katoula noted, “We have committed to continuing this initiative to incentivize players and recognize the Ghana Football Association’s ongoing e orts to improve

league organization. This year, we’re extending our support to women’s teams for the rst time, o ering a 400 Ghana cedi bonus to each player on winning teams, delivered instantly from the pitch to the locker room.”

Mr. Mouyelo-Katoula revealed that during the 2022–2023 season, Betpawa disbursed 600,000 Ghana cedis in direct payments, positively impacting nearly 4,000 players throughout the season. Following the success of this initiative, the company increased its investment to 1.3 million Ghana cedis for the 2023–2024 league season, reaching approximately 3,000 players.

For the ongoing 2024–2025 season, Betpawa plans to extend the Locker Room Bonus to include three technical sta mem bers from each winning team, further broadening the scope of its support for Ghanaian football.

In addition to the Locker Room Bonus, Betpawa is advancing its investment in sports infrastruc ture at the Ghanaman Sports Centre in Prampram. Phase two of this project will see the installa tion of seating for fans, enhancing the spectator experience. Once completed, the Betpawa Stadium is intended to be made available to premier league teams as a venue for o cial games, marking a lasting legacy for Ghana’s sports landscape.

Ntoudi Mouyelo-Katoula

Sustainable Insurance: The Dilemma of SMEs in Africa

In today’s rapidly changing world, sustainability has become a critical component of business strategy across all industries. The nancial industry, which plays a critical role in the nancing and protection of businesses and their assets is now expected to drive greater sustainability by investing and protecting ventures which are sustainable. This trend therefore presents, the insurance industry which is an integral core of the nancial industry a unique opportunity to drive positive change and sustainability by incorporating Environmental, Social and Governance (ESG) considerations into its operations. Before I delve into the subject, one may ask; what is sustainability and how can the insurance industry drive sustainability and expected positive change?

Sustainability in business practice refers to strategies and operational processes that meet the needs of the present without compromising the ability of future generations to meet their own needs. It involves integrating environmental, social, and economic considerations into decision-making processes to create long-term value for both the business and society.

Sustainable insurance involves integrating environmental, social, and governance (ESG) factors into insurance products, policies, processes, solutions and practices. This includes promoting green technologies, supporting climate resilience, ensuring fair, ethical and governance practices. For businesses, especially SMEs, this means not only protecting assets and lives but also contributing to broader sustainability goals.

Sustainable insurance is increasingly recognized as a vital component of responsible business practices worldwide. For Small and Medium Enterprises (SMEs) in Africa, the integration of sustainability into insurance presents both signi cant opportunities and formidable challenges. This article delves into how African SMEs perceive and engage with sustainable insurance, highlighting the unique factors in uencing their adoption of eco-friendly and socially responsible insurance solutions.

Barriers to Sustainable Insurance Small and Medium Scale Enterprises (SMEs) in Africa are faced with enormous challenges in the eld of sustainable insurance. Limited awareness and understanding:

One of the signi cant barriers for sustainable insurance among SMEs in Africa is the lack of

awareness and understanding of sustainable insurance. Many small business owners are unfamiliar with the concept and how it can bene t their operations. The focus for many SMEs remains on traditional insurance products that address immediate risks rather than long-term sustainability. A medium sized real estate company may not prioritize sustainable practices due to a lack of awareness about how green insurance products could help mitigate environmental impacts and improve operational e ciency.

High costs of sustainable insurance:

Sustainable insurance products often come with higher premiums compared to traditional policies. SME operations are often very sensitive to cost due to their lower volumes and margins. Therefore, these increased costs can be a signi cant deterrent. The higher upfront cost may outweigh the perceived bene ts, pushing SMEs to opt for less sustainable but more a ordable options. An SME in the agriculture industry might nd the cost of a climate-risk insurance policy prohibitive compared to standard coverage, impacting its ability to invest in sustainable practices. Not just the higher premiums, some of the practices that leads to sustainable business in themselves come at a high cost. For example, the cost of installing and maintaining green houses could be prohibitive to an SME in the agricultural industry just as the cost of installing green energies such as solar is very high to the average SME in the services industry.

Limited availability of sustainable insurance products:

In many African countries, the insurance market is still developing, and there is a limited range of sustainable insurance products available. This scarcity makes it di cult for SMEs to nd products that align with their needs and sustainability goals. A tech startup in Ghana might struggle to nd insurance policies that cover risks associated with innovative green technologies or sustainable business practices.

Regulatory and policy gaps:

The regulatory environment for sustainable insurance in Africa is often underdeveloped. Without supportive policies and regulations, insurers may be reluctant to o er sustainable products, and SMEs may lack incentives to adopt them. The absence of regulations supporting green insurance products means insurers have little motivation to develop

such o erings, leaving SMEs limited or unsuitable options. In dealing with the barriers to sustainable insurance, raising awareness about the bene ts of sustainable insurance is crucial. Insurance providers and related stakeholders can play a signicant role in educating SMEs about how sustainable insurance can mitigate risks, enhance resilience, and contribute to long-term nancial stability.

Developing a ordable and tailored sustainable insurance products for SMEs would help overcome cost barriers. Insurers could design products that cater speci cally to the needs of small businesses, providing coverage that is both sustainable and economically viable. Parametric insurance for instance is a growing trend, particularly in regions vulnerable to climate change. It provides payouts based on prede ned parameters like weather conditions or natural events, rather than actual losses. A farmer in Kenya could purchase insurance that automatically pays out if rainfall drops below a certain level, protecting against drought. According to the World Bank, parametric insurance can reduce the time it takes to receive a payout by up to 90% compared to traditional claims, making it highly bene cial for SMEs in agriculture, which are exposed to climate-related risks.

Insurance for Renewable Energy Projects: SMEs involved in renewable energy projects, such as solar installations, can bene t from specialized insurance that covers both equipment and operational risks. The African Development Bank estimates that Africa could see over $7 billion in investments in renewable energy by 2025, and insurers are creating products speci cally to cover these growing sectors.

Climate-Related Losses and Insurance Uptake: According to Swiss Re, global losses from natural catastrophes reached $270 billion in 2021, of which only 40% were insured. This insurance gap is even larger in Africa, where climate risk insurance could mitigate signi cant economic damages. The adoption of climate risk insurance, such as ood or drought coverage, could reduce losses for SMEs by up to 30%, providing a safety net for vulnerable sectors like agriculture Microinsurance o ers a ordable and accessible insurance options for low-income individuals and businesses, making it a suitable model for SMEs in Africa. Companies like BIMA and Hollard in

Ghana have introduced micro / SMEs insurance products that are tailored to the needs of small businesses. These initiatives provide essential coverage for business risk and could be expanded to include sustainable insurance products, o ering lower-cost options that support green practices. Microinsurance programs have reached over 60 million individuals globally, with a signi cant portion in Africa. Public-private partnerships can facilitate the development and distribution of sustainable insurance products. Governments and its agencies such as Environmental Protection Agency (EPA), development partners like the IFC, GIZ, GIRSAL, World Bank to mention a few, and the Insurance industry can collaborate to create incentives and frameworks that support sustainable practices among SMEs. The African Development Bank’s Climate Risk Insurance Initiative aims to enhance access to climate risk insurance for SMEs through collaborative e orts between public and private sectors. Advocating for supportive policies and regulations is essential to foster a conducive environment for sustainable insurance. The African Risk Capacity (ARC), an African Union initiative, provides weather-based insurance products to African countries and SMEs to improve disaster preparedness. ARC estimates that every $1 spent on insurance results in $4 of bene ts through reduced economic losses and quicker recovery times. Sustainable insurance products are experiencing rapid growth. A report by the Insurance Europe Federation found that the global market for green insurance products grew by 20% in 2022. In Africa, however, only about 10% of SMEs currently have access to these products. Expanding availability could increase resilience in sectors like energy and agriculture, which are crucial to economic development Below are some examples of Sustainable Business Practices SME’s can adopt.

• Implementing energy-ecient technologies in operations.

• O ering eco-friendly products or packaging.

• Partnering with suppliers who follow ethical and sustainable practices.

• Committing to reducing carbon footprints through renewable energy and carbon o set initiatives.

• Encourage carpooling, use electronic/ hybrid vehicles.

• Diversity and inclusion, foster a diverse workforce, promote equal opportunities.

• Usage of recycled and biodegradable materials Incorporating sustainability into business practices not only benets the environment and society but would also drive innovation,

resilience, and pro tability. In conclusion, the journey towards sustainable insurance for SMEs in Africa presents both challenges and opportunities. While the nancial vulnerability of SMEs is evident, the need for insurance solutions that align with the unique risks of these businesses is equally urgent.

ment organizations, must collaborate to create policies and products that are not only accessible but also adaptable and a ordable to the dynamic needs of African SMEs. By integrating sustainability into insurance frameworks, we can support the growth and resilience of this vital economic

sustainable insurance in Africa depends on a collective e ort to innovate, invest, and ensure no business is left behind.

Writer: Iddrisu Nashiru, MD Hollard Life Assurance, 1st Vice President of Ghana Insurers Association. A chartered Insurer (CII UK and Ghana) a fellow of the Chartered Institute of Ghana (FCIIG) and a certi ed ESG

Africa's built environment leaders to converge at ACEACRES 2024 Summit

The African Continental Engineering, Architecture, Construction and Real Estate Summit (ACEACRES) 2024 is set to bring together industry leaders, innovators, and stakeholders from across the continent and beyond. Scheduled for November 27-28, 2024, at the Berliner Platz Conference Centre in Accra, the summit aims to integrate the African built environment for socio-economic transformation.

Under the theme "Integrating Sustainable Built Environment for Socio-Economic Transformation through New Generation Technology and Arti cial Intelligence," ACEACRES 2024 will provide a platform for over 400 in-person and 100 virtual participants to share knowledge, network, and explore business opportunities.

Keynote speaker Engr. Margaret Aina Oguntala, National President of the Nigerian Society of Engineers, will share insights on the industry's future. Other notable speakers include Dr. Daniel McKorley, Executive Chairman of the McDan Group.

"The African built environment is at a crossroads," said Daniel Kontie, Founder and CEO of the Africa Continental Engineering & Construction Network Ltd, the summit's organizer. "We must harness innovative technologies and arti cial intelligence to drive sustainable growth and development."

The summit's attendees will include building contractors, engineers, architects, project managers, real estate developers, and government agencies from Nigeria, Rwanda, Kenya, Uganda, South Africa, Canada, Australia, New Zealand, the UK, and the US.

ACEACRES 2024 is made possible by principal sponsors Ger or Ghana Limited, Meprolim Ghana Limited, Premier Steel Ltd, McDan Group, Jemba Solutions Ltd, Fort Doors, Primus Group, Alusynco Hellas Services Ltd, Marbelino Marble Stones Décor, Mayfair Estate Ltd, Reroy Cables Ltd, Viva Fiberglass Ltd, and J2 A able Properties.

The event will culminate in the

African Continental Built Environment Industry Excellence Awards (ACBEIEA) Ceremony, recognizing outstanding achievements in construction technology, innovation, and sustainability.

By fostering collaboration and knowledge sharing, ACEACRES 2024 aims to propel Africa's built environment toward a more sustainable and prosperous future.

Absa Bank organises third ‘Change Your Story’ draw in Ho

Absa Bank Ghana has organised the third draw of its ongoing “Change Your Story” campaign. The event took place at the bank’s branch in Ho, where ve Absa customers were announced as winners, each to receive GHS 40,000.

Running from July to October 2024, the “Change Your Story” campaign o ers customers the opportunity to win signi cant cash prizes every month. By com-

pleting at least 10 transactions per month online or at Point-of-Sale terminals, customers automatically enter the monthly draw.

Each month, ve winners receive GHS 40,000, totalling a monthly giveaway of GHS 200,000. Absa Bank is leveraging the National Lotteries Authority’s Caritas platform to ensure transparency and fairness.

The winners for September are Oheneba Kobina Baah, Lewis

Ackah, Jujie Xi, Big Godwin Design and Derrick Nii Ayikai Aryee.

During the event, Absa Bank Ghana highlighted its Signature and In nite cards, which o er cardholders exclusive bene ts such as concierge services, comprehensive multi-trip travel insurance up to $2.5 million, discounts from over 40 Absa Bank Ghana partner institutions, and access to over 1,200 airport lounges globally.

In an exciting twist, clients who use the new Signature and In nite cards frequently between now and October could win an all-expenses-paid trip for two to the ‘Absa Champagne in Africa Festival’ in Johannesburg, South Africa. The festival is a prestigious event that features rare Champagnes from 40 exclusive French Champagne Houses.

ENDS

CIDAN INVESTMENTS LIMITED

WEEKLY MARKET REVIEW FOR WEEK ENDING November 1, 2024

Trend in Market Indices - 2024

STOCK MARKET REVIE

W

The Ghana Stock Exchange closed higher this week on the back of price increases by 7 counters. The GSE Composite Index (GSE-CI) grew by 160 27 points (+3.67%) for the week to close at 4,529 30 points, reflecting a year-to-date (YTD) gain of 39.58%. The GSE Financial Index (GSE -FI) also gained 24.68 points (+1.11%) for the week to close at 2,239.89 points, reflecting a year-to-date (YTD) gain of 17 79%

Market capitalization edged higher by 2 46% to close the week at GH¢101,938 10 million, from GH¢99,493.22 million at the close of the previous week. This reflects a YTD gain of 37 95%

The week recorded a total of 5,920,591 shares valued at GH¢73,473,078.87, compared with 801,810 shares, valued at GH¢12,890,891.38 traded in the preceding week.

MTNGH dominated the volume of trades while New Gold Exchange Traded Fund dominated the value of trades for the week accounting for 91.28% and 82 70% of the volume and value of shares traded respectively

The market ended the week with 7 advancers, as indicated in the table below.

Volume and Value of Trades for Week Ending 01/11/2024

CIDAN INVESTMENTS LIMITED

WEEKLY MARKET REVIEW FOR WEEK ENDING

November

1, 2024

CURRENCY MARKET

The Cedi furthered its depreciation run for the third straight week. It traded at GH¢16.3001/$, compared with GH¢16.1500/$ at week open, reflecting w/w and YTD depreciations of 0.92% and 27.12% respectively. This compares with a loss of 25.44% a year ago.

The Cedi also depreciated against the GBP for the week. It traded at GH¢21.1126/£, compared with GH¢20.9579/£ at week open, reflecting w/ w and YTD losses of 0 73% and 28 32 % respectively This compares with a depreciation of 27 57% a year ago

The Cedi slipped against the Euro for the week It traded at GH¢17 6852/€, compared with GH¢17.4605/€ at week open, reflecting w/ w and YTD depreciations of 1.27% and 25.78% respectively. This compares with a depreciation of 25.95% a year ago.

The Cedi lost grounds against the Canadian Dollar for the week. It opened at GH¢11.6352/C$ but closed at GH¢11.6916/C$, reflecting w/w and YTD losses of 0.48% and 22.93% respectively. This compares with a depreciation of 24.86% a year ago

CIDAN INVESTMENTS LIMITED

WEEKLY MARKET REVIEW FOR WEEK ENDING November 1, 2024

Source: Bank of Ghana

Exchange Rates: Ghana Cedi vs Selected Currencies

Source: Bank of Ghana

YTD Performance of the Ghana Cedi against Selected Currencies

Source: Bank of Ghana

COMMODITY MARKET

GOVERNMENT SECURITIES MARKET

The government raised a sum of GH¢4,078.20 million for the week across the 91 -Day, 182-Day and 364-Day Treasury Bills. This compared with GH¢4,421.54 million raised in the previous week.

The 91-Day Bill settled at 26.56% p.a. from 26.19% p.a. last week whilst the 182 -Day Bill settled at 27.58% p.a. from 27.29% p.a. last week. The 364Day Bill settled at 29.04% p.a. from 28.97% p.a. last week.

The tables below highlight primary market activity at the close of the week.

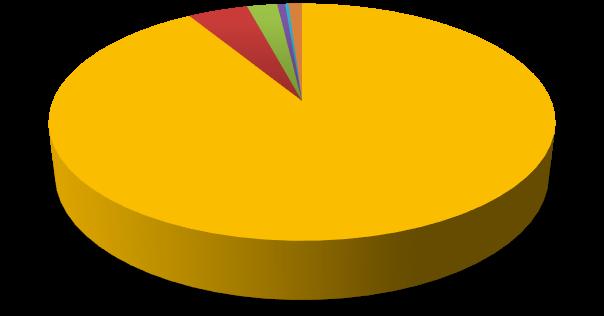

Oil prices closed slightly lower , on a report that Israeli Prime Minister Benjamin Netanyahu will hold a meeting for a diplomatic solution to the war in Lebanon Brent futures traded at US$73 10 a barrel, compared to US$75 63 at week open, reflecting w/w and YTD depreciations of 3.35% and 5.11% respectively.

Gold prices edged higher , trading close to record highs as the run-up to the 2024 presidential election and uncertainty before upcoming data prints kept safe-haven demand in play . Gold settled at US$2,749.20, from US$2,742.20 last week, reflecting w/ w and YTD gains of 0.26 and 32.70% respectively.

The price of Cocoa increased for the week. Cocoa traded at US$7,321.50 per tonne on Friday, from US$6,789.50 last week, reflecting w/w and YTD appreciations of 7.84% and 74.49% respectively.

International Commodity Prices

CIDAN INVESTMENTS LIMITED

WEEKLY MARKET REVIEW FOR WEEK ENDING November 1, 2024

ABOUT CIDAN

YTD Performance of Selected Commodity Prices

CIDAN Investments Limited is an investment and fund management company licensed by the Securities & Exchange Commission (SEC) and the National Pensions Regulatory Authority (NPRA).

RESEARCH TEAM

Name: Ernest Tannor

Email: etannor@cidaninvestments.com

Tel: +233 (0) 20 881 8957

Name: Moses Nana Osei-Yeboah

Email: moyeboah@cidaninvestments.com

Tel: +233 (0) 24 499 0069

Name: Julian Sapara-Grant

Email: jsgrant@cidaninvestments com

Tel: +233 (0) 20 821 2079

CORPORATE INFORMATION

CIDAN Investments Limited

CIDAN House

House No. 261

Haatso, North Legon – Accra

Tel: +233 (0) 27 690 0011/ 55 989 9935

Fax: +233 (0)30 254 4351

Email: info@cidaninvestments com Website: www.cidaninvestments com

INVESTMENT TERM OF THE WEEK

Moving average convergence / divergence (MACD): It is a technical indicator to help investors identify price trends, measure trend momentum, and identify entry points for buying or selling

Source:

h�ps://www.investopedia.com/terms/m/macd.as p

Disclaimer : The contents o f this report have been prepared to provide yo u with general info rmation o nly Information provided in a nd available from this report does not constitut e a ny inv estment recomm endation.

The info rmation contai ned herei n has b een obtained from sources that we beli eve to be reliable, but its accuracy a nd complet eness ar e not guaranteed.

Gold Cocoa Brent Crude

Gold Cocoa Brent Crude

Letshego Ghana Savings and Loans secures GHc 100m through debt capital market

Letshego Ghana Savings and Loans Plc has successfully listed its GHS100m Senior Unsecured Dual Bond O er on the Ghana Fixed Income Market, marking its second issuance this year under its expanded GHS500 million Medium-Term Note Programme.

This demonstrates the company’s commitment to diversifying its funding base and providing alternative investment opportunities to the local debt capital market.

With this latest issuance, Letshego has raised a total of GHS 200 million in 2024, having earlier secured GHS 100 million in March.

The issuance saw signi cant interest, with total bids peaking at GHS131 million re ecting an oversubscription rate of 1.31 times. The transaction was priced at 22.50% for the 3-year xed rate note, while the 4-year oating rate note was priced at 182-day T-bill rate plus a margin of 100 basis points.

Overall, the success of this issuance rea rms Letshego Ghana’s standing as a trusted corporate bond issuer in Ghana’s active capital market.

Commenting on the bond issuance, the Country Chief Executive O cer of Letshego, Nii Amankra Tetteh, noted, “We would like to express our gratitude to our investors for the continuous con dence and trust posed in the Letshego team.

With this funds injection, we can continue to work on our strategy of providing increased access to inclusive nancial solutions across the country. We appreciate the ongoing support of our investors, who remain valuable partners as we ful ll our brand purpose to improve more lives in Ghana.”

Stanbic Bank Ghana LTD and Black Star Brokerage Limited were joint lead arrangers and co-sponsoring brokers to the issue.