7 minute read

LTC Insurance Alternatives for Your Medicare Clients That May Surprise You

By Marc Glickman, FSA, CLTC

I recently attended the annual Medicarians conference to meet with Medicare agencies about long-term care insurance. The conference once again saw record growth with thousands in attendance. A shout out to Jay Weintraub and Sonya Larson for hosting an amazing show and advocating for LTC planning.

There continues to be significant interest in LTC planning for many Medicare clients. Medicare does not cover most LTC services and LTC planning is an essential part of financial planning for most clients who are 65 or older.

Traditional LTC insurance and life hybrids continue to be leading solutions quoted for clients ages 65 and older. However, the value of these solutions may erode for clients purchasing in their retirement years. Nearly half of all applicants are declined for traditional LTCi based on their health at ages 65 and older. Also, because product pricing rapidly increases with age, the insurance leverage may not to be as compelling especially for females.

A couple of LTC insurance alternatives have emerged to fill the gap including:

Short Term Care insurance for pay-as-you-go funding

Annuities with LTCi riders for single premium funding

Let’s explore the solutions growing in popularity in this market segment.

Short Term Care (STC) Insurance

STC is a health product that offers an affordable alternative to traditional LTCi covering care needs typically up to one year, with some products offering both a year of home care and a year of community care. The underwriting process for STC is less stringent, often involving a simple health questionnaire and drug screen, but without requiring medical records or exams. This makes it accessible to more applicants, including those with pre-existing health conditions.

For clients that can’t health qualify or afford traditional LTCi, STC can provide professional care with indemnity benefits and a 0-day elimination period. A one-year plan can provide a huge benefit for a family even if it doesn’t cover most of the risk. Picture buying family time and money once the care event happens instead of reacting to a crisis scenario that creates even more stress.

Short-term care can also be added to complement other LTCi products. For example, many agents use STC as a supplement to products with a 90-day elimination period or to enhance coverage at the beginning of a claim with the indemnity payout if there is proof of loss for each policy.

Be careful with product selection as contract language is not standardized and STC is not available in all states. As a health insurance product, it may be subject to rate increases or decreases in the future.

In states where STC is not available, we have seen one carrier recently launch in all 50 states, a simplified issue traditional LTC insurance coverage with 1 to 2 years of coverage that works similar to STC.

Case Study 1: Collaborating with a Specialist

Term Care Solution

Client Profile:

Age: 65

Health: Moderate, with a few chronic conditions

Financial: Modest retirement savings and desires an affordable pay-as-you go premium

Coverage: Medicare Advantage

Process:

1.Needs Assessment: The Medicare specialist assesses the client's health and financial situation.

2.Specialist Consultation: The Medicare specialist can refer the client to an LTC specialist who can shop the market and work as an extension of your team to process the case start to finish. At BuddyIns, we help match Medicare agencies with LTCi specialists. To request help for a client, complete this form: BuddyIns Referrals - BuddyIns

3. Finalizing the Case: Compensation on STC products can be split with other licensed agents. Needs Assessment: The Medicare specialist assesses the client’s health and financial situation.

Comparing the Value of STC Insurance

This sample STC product provides up to $12,000/month for one year of facility care and up to $4,800/month for one year of home health care. The product is unisex priced, so females get especially good value relative to traditional LTCi, which is often priced 50% higher for females.

The benefits are available immediately, but if care is needed at age 85, STC may provide tax-free health insurance benefits at 4.1x the premium paid into the plan as is shown in this example:

app.buddyins.com

You can edit the plan and compare the cost of care once you sign up for a free trial to the Buddy System.

STC can be an excellent alternative for clients who are looking for a pay-as-you-go premium who would not otherwise be a good fit for a traditional LTCi solution.

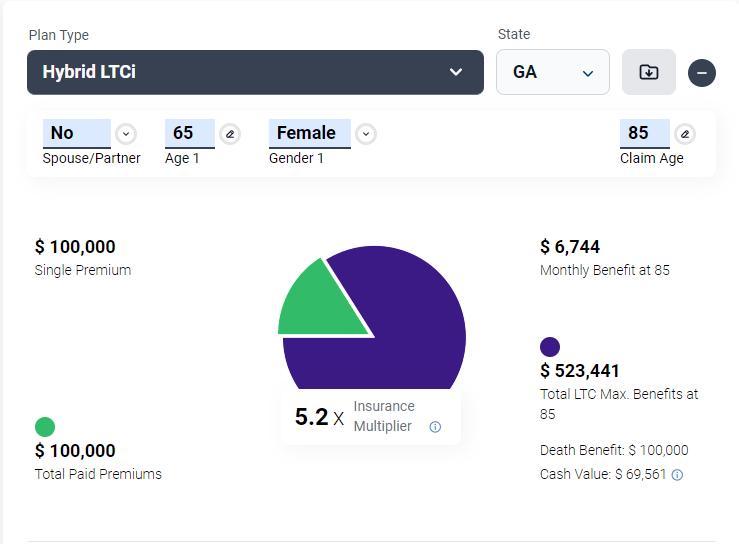

Annuities with LTCi Riders

For clients who have more assets, another alternative solution is an annuity + LTCi hybrid. Whereas the pricing of life hybrids can get relatively expensive at ages 65 and older, the pricing of annuity hybrids does not increase as much with age.

The underwriting process for annuities is much less stringent with a page of knockout questions rather than the full underwriting that life hybrids often require.

While there are not as many carriers offering annuity with true LTCi riders, the ones that offer the product are growing quickly in popularity.

Here are a few reasons why annuity products fit especially well for clients who are 65 and older:

They often have more readily available assets or cash equivalents that can be used to fund the single premium solution.

The immediate LTC insurance leverage can be 3x or more of the initial deposit, which compares favorably to traditional LTCi and life insurance hybrids at these ages.

The underwriting is designed for clients at these ages, and there’s even a carrier with a guaranteed issue option should they not qualify for the best health rating.

Clients with an existing non-qualified annuity can tax-free 1035 exchange the cash value into an annuity with LTCi rider. The gains on the existing annuity being exchanged may not be taxed as ordinary income when used on the tax-qualified LTCi rider.

While not true LTCi, there are also fixed indexed annuities with ADL doublers that create additional income if the client meets the 2 out of 6 ADL eligibility trigger. A few of these products have expanded to cover home health care in addition to facility care. Carriers see these features differentiate their FIA offerings. The true LTCi rider products have the added advantage of tax-free benefits.

Case Study 2: Repositioning Assets to Create LTC Planning Leverage

Client Profile:

Age: 65

Health: Moderate, with a few chronic conditions

Financial: Significant savings in cash, which can be repositioned for long term care needs

Coverage: Medicare Supplement

Comparing Annuity with LTCi Riders to Life with LTCi Riders

This annuity with LTCi rider provides up to $8,792/month for five years of home health, assisted living, or nursing home care paid as an indemnity benefit. It is very competitive to a life-based hybrid policy, but with less strenuous underwriting. This product even has a guaranteed issue alternative should the client not qualify based on health.

You can edit this plan once you sign up for the Buddy System.

Bottom Line

LTC insurance and alternatives are a crucial addition to Medicare coverage for many clients, offering protection against the high costs of long-term care. By collaborating with specialists, Medicare brokers can ensure their clients receive an expanded array of solutions. Understanding different solutions, payment options, and the compensation structure for referrals helps brokers provide comprehensive and informed solutions to their clients.

If Medicare doesn't cover long-term care, what's your plan?

Marc Glickman, FSA, CLTC, is CEO and co-founder of BuddyIns, a leading long-term care insurance education, marketing and technology company. Marc is a licensed insurance agent in all 50 states and serves on the Board of Advisors for CLTC. Marc has over 15 years of experience as an actuary including as the chief investment officer and chief sales officer for a major LTC insurance company. Marc earned his degree in economics from Yale University. In 2019, he was named one of the top 20 innovators in the insurance brokerage space.

818-264-5464