The Marine Insurer

l Red Sea: Houthis rebels still posing threat

l Casualties: Risk management essential

l Market cycles: Do statistics reflect the reality

l Essential parts: Changing technology improving paints

l Claims: How to manage a claim end to end

04 Renewals

What marine insurance buyers can expect in coming renewals in the Hull & Machinery and P&I markets

08 Red Sea risks

The Red Sea will continue to be a maritime hot spot in 2025 and thus stakeholders must collaborate to navigate the evolving security landscape

10 Key risks for 2025

Identifying five key risks that the international maritime sector must prepare for in 2025

14 Data-driven underwriting

How underwriter’s data-driven strategies have kept global trade moving in an eventful year

17 Wind assisted propulsion

Will 2025 be the year when wind-assisted propulsion systems (WAPS) become a technology of choice for decarbonisation compliant shipowners

22 The supply chain challenge

We focus on the the key supply chain trends to look out for in 2025

26 Application programming interfaces (APIs)

How APIs can help with risk assessment, measurement and transfer in the marine insurance sector

29 Emission trading

Examining the complexities of the EU’s ETS system

Analysing recent marine casualty trends and an overview of some of the key concerns to be addressed following an incident involving a vessel on-risk

Claims

Analysing a recent cargo loss case with a positive outcome for the clients

40 Embedded AI and claims

How the integration of embedded Generative AI (GenAI) and Large Language Models (LLMs)can transform the way insurers operate

44 Wreck removal

Looking at WRECKSTAGE 2024, the latest version of BIMCO’s standard wreck removal agreement based on payment of a lumpsum in stages.

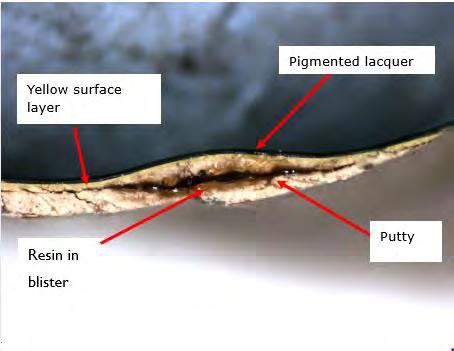

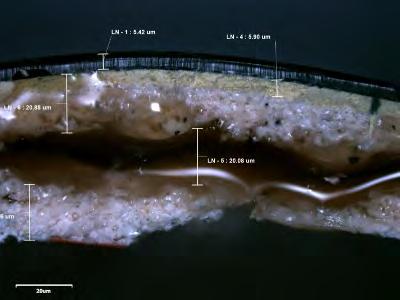

The importance and science of proper shipping coating

Ship arrest, a legal mechanism to secure claims before resolution of a dispute, plays a significant role in maritime law

Welcome to 2025!

Who knows what this year will bring. The regime change in Syria at the end of last year showed us just how quickly global politics can be re-arranged. What we do know is that in 2025, there will be change, not least because of a new president in the White House and expectations that he will bring Ukraine and Russia to the table and possible force through changes in the Middle East.

But no-one is expecting world peace to break out – it is much more likely that the conflicts will remain, albeit in different places and in different ways. That brings us to the marine sector, a sector which always reflects the world in which it operates – think of the continuing threat in the Red Sea and the need to reroute vessels around the Cape, bringing with it a range of other risks.

The threat of new trade tariffs from the US on regions such as Europe and countries such as China, may well mean new routes for the shipping sector and other new relationships being developed, such as between the EU and Latin America.

For the marine insurance industry, there will be plenty of risks to foresee, whether it is new war risks or the risk of default. There are new vessels to insure and new technologies to contend with from alternative fuels through to the potential of an AI colleague sitting at the desk next door to you. Technology can also reduce risks, such as the use of technology to develop new paints, as we explore in this issue.

The other issue that is always in the minds of insurers is the general state of the market. Will rates be heading down in 2025 or upwards again? Will new capital bring new competition? Will claims force market shifts?

As you can tell, it might be a new year but for the marine insurance market, it looks like it will be much the same as 2024. Either way, I hope you enjoy this read and wish everyone a successful and prosperous 2025.

Liz Booth, Editor, The Marine Insurer

Bozidar Ljubisavljevic , regional

marine

chief

client officer for the Middle

Howden Insurance Brokers, uses statistics to help explain what marine insurance buyers can expect in coming renewals in the hull and machinery and P&I markets and how data can be used to achieve favourable results

An approximate answer to the right problem is worth a good deal more than an exact answer to an approximate problem. This was a phrase attributed to John Wilder Tukey, an American mathematician and statistician who pioneered many of the key foundations of what came later to be known as data science.

Numbers, statistics and their analysis will continue to remain vital in decision-making across industries and in our small (but important!) corner of the marine insurance industry we will seek to define today’s question as whether insurance markets are rational, and whether there is sufficiently robust demand pressure across hull and machinery (H&M) and protection and indemnity (P&I) insurance at the point of transaction.

The marine insurance industry does not lend itself to straight-forward statistical analysis. The reason for this is four-fold:

1. Marine insurance statistics produced by major markets such as Lloyd’s of London are done on a consolidated basis to include hull, war, cargo and aviation (‘MAT’ – marine, aviation and transport). Some of these can be counter cyclical to pure marine (eg aviation), while some are significant net positive contributors in most recent years (eg war) that might mask underlying actual H&M class performance;

2. General insurers’ statistics are produced on a consolidated basis where marine is usually included as a small part of a general insurance portfolio;

3. International associations’ data is either skewed towards the experience of insurers that contribute to it in those geographies writing a non-holistic marine portfolio, or, subject to variances in the quality and consistency of data by contributing authorities; and,

4. Multi-line P&I Clubs increasingly report consolidated

financial results.

One must nevertheless applaud the relevant individuals, relevant bodies and associations, insurers, their processes, their initiatives and their ever-greater transparency in collating such data and making it available to a broader readership. When data points are assessed, trends start to emerge and analysis of such trends enables more informed decision making for insurance buyers.

Results to which this article refers are either stated in or have been converted to US$ and therefore mild variance will be inevitable with certain results that are reported in GBP or other currencies. In addition, Lloyd’s of London, IUMI and CEFOR all have individual disclaimers and notes to results, which we would encourage are read for context.

Results for the period to January 2024 show a combined ratio of 84%, the best result since 2007 (FY22: 92%). Underwriting profit was US$7.9bn (FY22 US$3.5bn) while investment results rebounded to a gain of US$7.1bn (FY22 loss US$4.1bn). The return on capital was approximately 25%, markedly beating the 10-year average of 6%, supported by underwriting discipline that has been the backdrop of 24 consecutive quarters of risk-adjusted rate rises.

Marine (including the consolidated classes of MAT), has seen written premium increase by 12%, a slowdown from the +32% for FY22. The combined ratio has seen a deterioration by 9% to 99%, however this includes a ‘tail’ reserve strengthening for FY22 of 11%, predominantly linked to the aviation segment.

The six month period to mid-2024 has seen slowing market premium growth of 7% (HY23: 22%) but an equally good combined ratio of 84%. AM Best has upgraded its finanancial strength rating of the market to A+.

Marine (+A+T) results for the six month period to mid-2024 stood at US$159m (HY23: US$348m).

The Nordic Association of Marine Insurers has reported a mild uptick in claims, though keeping in mind fleet utilisation rates, the uptick has, at a broad level, not risen beyond pre-pandemic levels.

There has been a long-term trend of reducing claims frequency from 30% of all vessels having a claim to under 20% of all vessels pre-pandemic. While frequency has increased since then, it is still below pre-pandemic levels. By type of vessel, car/ro-ro, container and tanker vessel types have a more pronounced 10-year drop, while passenger and offshore vessels are showing a pronounced three-year rise. By type of claim, there has been an uptick in machinery claims last year, with a moderate reduction in collision, contact and grounding claims. The frequency of total losses has also settled between 0.05% to 0.10% since 2010.

The association also reports that fire frequency claims have outpaced other claim types, and using 2014 as a benchmark, fire claims are showing the same frequency while other claim types are showing a 25-30%

“Statistics demonstrate that at a macro (ie, market) level, 2023 and mid-year 2024 underwriting results are healthy and the upwards trend in claims inflation has not come at the expense of these results, with claims mostly hovering at around pre-pandemic levels.”

reduction in frequency.

Claims severity has increased in the last four years and, for the first time in more than 10 years, CEFOR members have declared claim losses exceeding US$50m per claim. Four out of the eight losses reported above US$10m were due to fire. The average cost of claims relating to fire has increased substantially since pre-pandemic, with spikes in 2018, 2019, 2020 and 2023.

Claims inflation continues to show an upwards trend,

however with a strong footnote that the 10-year average partial and total claims cost denoting claims inflation corresponds with a 10-year similar increase in insured value and vessel average gross tonnage increases.

The average cost of nautical related claims excluding fire is stable, with only a slight increase post-2020, while heavy weather claims have seen a trebling of average cost since 2020. The average cost of machinery damage claims has doubled since 2014.

Premium statistics issued by the International Union of Marine Insurance show an estimated US$9.2bn total hull premiums worldwide for the year ending January 2024, an increase of 7.6% from the previous year. The Nordic insurance market, still the largest beneficiary of marine premium movements since 2019, has seen a decline in overall marine premiums for the first time in five years, while insurers in China, Singapore, Japan and the UK have continued to show notable year-on-year growth.

The report shows key marine market overall premium shares led by UK (Lloyd’s and the IUA) at 15.7% share, Nordic markets at 13.5%, China at 11.1% and Singapore at 9%.

IUMI’s loss ratios for hull show that 2022 started at the lowest level of claims since 2017, but showed steeper than average increase in a subsequent period, indicating unforeseen cost inflation with a need to adjust claims estimates upwards.

For the period to 2023, IUMI’s commentary centres around increased claims costs, though there is an acknowledgement that the first half of 2024 is showing a benign claims impact, with a nod to increasing capacity that is putting pressure on premiums.

“Critically, however, insurance buyers need to objectively assess where on the ‘demand’ scale they sit. While generally speaking capacity for the right risks has significantly increased, there does remain greater discipline among international insurance providers for risks that are difficult to place.”

SO, HOW WELL DO STATISTICS TELL THE H&M TALE?

Statistics demonstrate that at a macro (ie market) level 2023 and mid-year 2024 underwriting results are healthy and the upwards trend in claims inflation has not come at the expense of these results, with claims mostly hovering at around pre-pandemic levels.

This is not surprising – freight rates across vessel types have on average been excellent and owners are probably aiming to not take vessels out of service at such times.

There is also not only a moderate increase in underwriting capacity (both number of market participants, and the quantity of business underwritten), but also how widely insurers are allowing their capacity to be deployed, notably through an increasing number of managing general agents (MGAs).

The risk/reward basis for MGAs is such that insurers create a broader distribution channel quickly, however they do lose absolute underwriting control. This is not uncommon for the current part of the market cycle, where supply rapidly expands. Both H&M and War risks classes of insurance have seen substantial MGA capacity enter in the last 24 months.

At a micro (ie, risk) level, the right ‘in-scope’ risk can usually be presented to a new entrant insurer at more competitive pricing than existing levels. Fleets with poorer records are not penalised as harshly as 12-18 months ago.

Owners should take advantage of what seem to be aggressive growth targets by insurers to secure favourable renewals.

On the counter side, for risks that are unique or difficult to place, there remains a smaller collection of specialist insurers willing to offer insurance at a (usually high) price and/or less favourable terms. This is one differentiating factor of the current market cycle compared to the last market cycle, where, at its peak, “most insurers were underwriting most risks”.

A key difference between H&M and P&I insurance purchasing is that H&M insurance is substantially more transactional in nature than P&I insurance. This means that if the price is wrong, or if the terms are unacceptable, the buyer can ‘choose’ to insure elsewhere without notice and take advantage of a more advantageous offer.

This is not the case in P&I insurance because a policyholder becomes a ‘member’ of a P&I Club where usually exit penalties apply and a longer-term purchasing strategy covering both objective and soft factors needs to be taken into account.

As insurance is offered on a mutual basis, P&I Clubs can also ask for additional premium to be paid should their balance sheet become weaker than is mandated by their boards or rating agencies. Accordingly, a comparative review of club results becomes an important step in a member’s annual insurance renewal process – no such review is perfect

but it can offer insight into the likely future financial performance of a P&I Club.

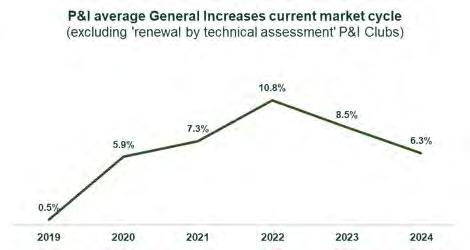

12 months ago P&I Clubs were approaching the February 2024 renewal period against a background of not only marginal underwriting results but significant investment losses.

While the same number of Clubs reported underwriting result losses (four), financial year underwriting results this year (see graph) show an average greater positive result (if excluding Gard) of US$12m vs US$2m last year (US$15m vs US$12m if including Gard), and policy year combined ratios improved from an average of 106% to 97%.

Investment results swung from an average loss of US$44m to an average gain of US$64m.

Financial year five-year cumulative results (excluding Gard) average a gain of US$17m per year (US$41m if including Gard) (see graph above). The ‘pool’, or the intra-club shared claims layer between US$10m and US$100m is also at a low level in the last two years, with 2023 at 12 months of development being at its lowest level since 2016.

Is the market being ‘talked up’ in advance of renewal, what happens when variables are introduced about future impacts of current or future events that are yet to be fully quantified or quantitatively assessed and those variables relied on to create pricing pressure today.

A question for a broker to challenge, a question for the insurance buyer to assess, and a question that deserves a substantive reply from a P&I Club if such reasoning enters renewal discussion.

The sorts of soundbites that have crept into renewal discussions include the impact of the vessel Dali’s bridge collision – impact not yet known, longer voyages for a greater portion of the commercial sailing fleet – impact not yet known, decarbonisation technologies and initiatives –

impact not yet known, claims inflation – see H&M CEFOR: not really yet notable, rising pool contributions in 2024 –maybe, but too early to tell after two historically low years, rising International Group reinsurance costs – not relevant as they are charged at cost separately.

At the time of writing (October 2024), Clubs have started announcing their general increases for the February 2025 renewals and it is quite likely that most Clubs will request a general increase. The current market cycle is past its peak: while it should arguably have ended, it was last year extended due to investment return uncertainty (see graph below).

For 2025 that graph should arguably average back to zero, excluding premium return impacts from last year.

This is unlikely. We are more likely to experience another year of a ‘soft’ general increase for most P&I Clubs. For the right risks in the right club with the right story, against a suitable renewal strategy there are deals to be made this year.

The tale never really ends, and for followers of ‘the infinite game theory’ there rarely has to be an end to achieve a successful outcome. The nature of marine insurance and its need as a ticket to trade, is such that buyers’ aims are to keep spotting market opportunities and lock in favourable deals that prolong the benefits of opportunities at the current part of the market cycle. Such opportunities exist today, across both H&M and P&I insurance.

Critically however, insurance buyers need to objectively assess where on the ‘demand’ scale they sit. While generally speaking capacity for the right risks has significantly increased, there does remain greater discipline among international insurance providers for risks that are difficult to place.

We believe it is incredibly important to identify how to manage the approach to the insurance market: with abundant insurance availability for select risks, savings can usually be achieved through the right data-backed presentation, the right level of energy and engagement to challenge the status quo, the right international placement strategy and the right tale.

The Red Sea will continue to be a maritime hot spot in 2025 and thus stakeholders must prioritise collaboration, risk mitigation and technological innovation to navigate the evolving security landscape and ensure the safe and efficient operation of maritime routes advises

Häderle

, partner at law firm SANDS, Oslo

The Red Sea, a critical maritime route connecting the Suez Canal to the Indian Ocean, has long been a focal point for global trade and geopolitical tensions.

In 2024, the region continues to face significant risks that impact the shipping industry, including geopolitical conflicts, technological advancements by non-state actors and economic disruptions.

As we look ahead to 2025, understanding these risks and developing strategies to mitigate them will be crucial for shipping companies, policymakers and international stakeholders.

The Red Sea has historically been a hotspot for maritime security threats. Notable events such as the Gulf War and the Iran-Iraq conflict have highlighted the region’s vulnerability to geopolitical tensions and military operations in recent times.

In recent years, the ongoing conflict in Yemen has exacerbated these risks. While Somali pirates have long posed a threat to commercial shipping, Houthi rebels have enhanced their capabilities, increasingly targeting commercial vessels and employing advanced technologies.

In 2024, the security situation in the Red Sea remains precarious. The presence of various international naval forces patrolling the waters aims to ensure the safety of

maritime routes, but the risk of targeted attacks and accidental confrontations persists.

Shipping companies operating in the region must navigate a complex security environment, balancing the need for safe passage with the potential for significant disruptions.

The Red Sea’s strategic importance as a maritime route makes it a focal point for geopolitical rivalries in the Middle East.

The involvement of global powers, including the US, China and European nations, adds to the complexity of the security environment. These tensions can lead to sudden escalations and increased risks for shipping operations.

Disruptions in the Red Sea can have significant economic repercussions, affecting global trade and leading to increased shipping costs and insurance premiums.

Attacks on maritime infrastructure, such as ports and shipping lanes, can further exacerbate these economic impacts, making it essential for stakeholders to develop robust risk management strategies.

Navigating the Red Sea requires heightened security measures and potentially rerouting vessels to avoid high-risk areas.

Shipping companies must coordinate with international naval forces for safe passage, adding operational complexity and increasing costs. The presence of naval mines and the risk of direct attacks on vessels further complicate maritime operations.

The Houthi rebels have made significant technological advancements, including the use of drones, missile systems

and naval mines to target vessels.

These advancements have increased the sophistication and reach of their attacks, posing new challenges for maritime security in the region.

The Houthis’ ability to deploy these technologies effectively has made the Red Sea a more dangerous area for commercial shipping.

While the primary focus has shifted to the technological advancements and threats posed by the Houthis, piracy remains a significant concern in the Red Sea, particularly near the Gulf of Aden. Somali pirates continue to pose a threat to commercial shipping, necessitating ongoing vigilance and security measures.

In 2024, several significant developments have shaped the security landscape in the Red Sea.

The international community has ramped up naval patrols in the Red Sea to deter attacks and ensure the safety of maritime routes. This increased presence has helped mitigate some risks but also raises the potential for confrontations.

The insurance industry has responded to the heightened risks by adjusting premiums and coverage terms for vessels operating in the Red Sea.

War underwriters, such as DNK (Norwegian Shipowners’ Mutual War Risks Insurance Association), have stopped quoting for Red Sea transits, reflecting the increased perceived risk.

The Houthi rebels have continued to enhance their technological capabilities, employing drones and missile systems with greater precision and effectiveness. These advancements have increased the threat level for commercial vessels and necessitated more sophisticated countermeasures.

Advances in maritime surveillance and security technologies have improved the ability of shipping companies to monitor and respond to threats in real-time. These technologies play a crucial role in enhancing situational awareness and mitigating risks.

As we move into 2025, several trends and developments will be significant in shaping the security landscape in the Red Sea.

The geopolitical landscape in the Middle East is likely to continue evolving, with potential shifts in alliances and power dynamics. These changes could impact the security environment in the Red Sea, necessitating ongoing vigilance and adaptability from shipping companies and international

“Shipping companies will need to invest in robust risk mitigation strategies, including enhanced security measures, comprehensive insurance coverage and contingency planning.’’

stakeholders.

Greater collaboration between international naval forces, shipping companies and regional authorities will be essential to address the complex security challenges in the Red Sea.

Joint exercises, information sharing and coordinated responses to threats can help enhance maritime security and reduce risks. Shipping companies will need to invest in robust risk mitigation strategies, including enhanced security measures, comprehensive insurance coverage and contingency planning. Implementing best practices for navigating high-risk areas and managing potential disputes during claims will be crucial for minimising disruptions.

The evolving security landscape may prompt regulatory changes aimed at enhancing maritime safety and security. These changes could include stricter requirements for vessel tracking, reporting, sanctions and compliance with international maritime security standards.

Continued advancements in maritime security technologies, such as autonomous vessels, advanced surveillance systems and cybersecurity measures, will play a critical role in mitigating risks and enhancing operational resilience.

The Red Sea remains a region of significant strategic importance and complex security challenges. In 2024, the risks associated with geopolitical tensions, economic disruptions, operational challenges and Houthi technological advancements continue to impact the shipping industry.

As we look ahead to 2025, stakeholders must prioritise collaboration, risk mitigation and technological innovation to navigate the evolving security landscape and ensure the safe and efficient operation of maritime routes in this critical region.

By understanding the historical context, current situation and future trends, shipping companies, policymakers and international stakeholders can develop effective strategies to address the new risks in the Red Sea and contribute to the stability and security of global maritime trade.

.

In 2024, the maritime industry confronted geopolitical tensions, climate change and rapid technological shifts. As shipping routes became riskier and cargo values surged, robust marine insurance emerged as essential for protecting investments and ensuring operational resilience. We look at five highlights to follow in the coming year.

Seafarers are vital to the maritime industry. The Maritime Labor Convention (MLC) 2006 is an international labour standard administered by the International Labour Organization (ILO) acting as a comprehensive set of rules within the ILO framework that specifically addresses the working and living conditions of seafarers worldwide.

All seafarers, working on board ships that fly the flag of countries that have ratified the MLC 2006, are covered, once the convention is in force in the relevant country. As of 2024, MLC 2006 has been ratified by 170 parties.

In 2014, the Joint Maritime Commission Subcommittee on Wages of Seafarers discussed updating the minimum monthly basic wage figure for able seafarers and the ILO Governing Body approved the recommendation. From 1 January, 2025, the ILO minimum basic wage for an able seafarer will be increased to US$673 from the 2024 rate of US$666.

The subcommittee was prompted to increase seafarer wages primarily due to a growing shortage of qualified seafarers, leading to a more competitive job market where employers need to offer higher salaries to attract and retain crews. This is coupled with concerns about the cost of living, the demanding working conditions at sea and tightening labour regulations globally, strengthening seafarers’ rights for adequate compensation.

The International Maritime Solid Bulk Cargoes (IMSBC) Code exists to facilitate the safe stowage and shipment of solid bulk cargoes by providing information on the dangers associated with the shipment of certain types of solid bulk cargoes and instructions on the procedures to be adopted when the shipment of solid bulk cargoes is on board. The three groups of cargoes as per the IMSBC Code category, are:

Group A: Cargoes that may liquefy

Group B: Cargoes that possess chemical hazards

Group C: Non-hazardous cargoes (cargoes that do not meet Group A or B).

In 2023, it was discovered that there was a discrepancy between the IMSBC Code and regulation XII/10 of the International Convention for the Safety of Life at Sea (SOLAS), 1974, concerning the omission of bulk density information in the form for cargo information for solid bulk cargoes.

The short-term solution was to approve the revised form for cargo information for solid bulk cargoes, pending formal entry

Teni Olowu , claims executive, SCB, Inc. (Houston), Managers, The American P&I Club identifies five key risks that the international maritime sector must prepare for in 2025

into force of the amendments to the IMSBC Code. From 1 January, 2024, parties were told to bring the revised form to stakeholders’ notice and begin voluntary application until the amendment’s entry into force.

From 1 January, 2025, amendments (07-23) (also referred to as “bulk density”, as required by SOLAS regulation XII/10) mandates shippers, among others, to declare the bulk density of their cargo and include it in the cargo declaration. Failure to comply means that such vessels are in violation of the latest regulations regarding the safe carriage of such cargoes, which could result in potential safety hazards, legal repercussions (shortage claims) and non-compliance with international maritime standards. All discretionary oversight port state control officers had prior to the entry into force will cease and the vessel will be held liable to the full extent of the law.

Geopolitical risks, including the Middle East conflicts, the South China Sea dispute, the Red Sea risks, the RussiaUkraine war, and the Israel-Hamas war, among others, have caused negative impacts on ocean shipping and marine insurance demand. These events have resulted in limited port access, outright bans on specific cargo imports and exports, heightened scrutiny during vessel inspections and even the seizure of ships.

Attacks on ships in the key Red Sea route from Asia to

Europe since November 2023 have caused many shipping companies to reroute around the Cape of Good Hope in South Africa, adding days to voyages and increasing costs. The Russia-Ukraine war that started in 2022 has disrupted maritime activities in the Black and Azov seas, causing the suspension of Ukrainian port operations and agricultural exports. In addition, international sanctions targeted Russian ships and shipbuilders, restricting their access to ports and freezing foreign assets. 2025 will see an increase in more geopolitical events with major elections, eg the US 2024 election, and others in 2025 - Germany, Argentina, Australia, Canada, Japan – which will play a role in determining the climate for the new year. However, insurers can weather geopolitical risks and mitigate the impact of trade sanctions, regional conflicts and piracy incidents in the various global hotspots, through their premium setting, management of exposures and by strengthening loss prevention measures.

It is an unwritten understanding that every major maritime event brought about the enactment of legislation to tackle the same.

The International Convention for the Prevention of Pollution from Ships (MARPOL) was enacted in response to a rise in oil tanker incidents and resultant pollution. To pursue the IMO 2018 Initial Strategy for the reduction of greenhouse gas (GHG) emissions from ships, Annex VI of the MARPOL was enacted, providing for mandatory requirements for ships to reduce their carbon intensity by 40% by 2030, compared to the 2008 baseline.

In 2023, the European Union (EU), as part of the Commission’s Fit for 55 legislative package to reduce EU greenhouse gas emissions by at least 55% by 2030, adopted the FuelEU Maritime Regulation (Regulation (EU) 2023/1805) which promotes the use of renewable, low-carbon fuels and clean energy technologies for ships, essential to support decarbonization in the sector.

FuelEU Maritime will enter into force from 1 January 2025, except for Articles 8 and 9 on monitoring plans, which shall apply from 31 August 2024 and set maximum limits for the yearly average greenhouse gas (GHG) intensity of the energy used by ships above 5,000 gross tonnage calling at European ports, regardless of their flag.

On October 1, 2024, the International Longshoremen’s Association (ILA) embarked on a strike of longshore workers, along all the US East Coast and Gulf Coast ports in the US. The strike was because of the breakdown in negotiations between the ILA and the US Maritime Alliance (USMX). The ILA demanded a significant pay rise for dock workers for the six-year life of the contract, as well as increased contributions to their retirement plan and a say in the role of automation in their industry. The ILA represents approximately

“On October 1, 2024, the International Longshoremen’s Association (ILA) embarked on a strike of longshore workers, along all the US East Coast and Gulf Coast ports in the US. The strike was because of the breakdown in negotiations between the ILA and the US Maritime Alliance (USMX).”

45,000 workers who manage the unloading of massive shipping containers from large cargo ships.

On October 4, 2024, the ILA and the USMX reached a temporary agreement to suspend the ILA’s planned strike until January 2025, allowing for continuing negotiations. While this provides temporary relief, there are concerns about the impact of the three-day strike (October 1-3), and the impending January strike, which will raise issues such as increased demurrage and off-hire costs, reliance on deviation and delay provisions, cargo loss/damage claims, force majeure claims in some instances. It will be prudent for shipowners and charterers to plan accordingly to avoid further issues that may arise.

In summary, the maritime industry is set to navigate a complex landscape in 2025, characterized by rising wages, regulatory changes, geopolitical tensions, environmental legislation and labour negotiations. Stakeholders must remain agile to adapt to these evolving challenges.

Stefan Schrijnen , chief commercial officer, Insurwave, explains how underwriter’s data-driven strategies have kept global trade moving in an eventful year

Insurers have always played an important role in supporting resilience against risks. In the 2024 edition of the AXA future risks report, 91% of experts stress the importance of the role of insurers in protecting people against new kinds of risks that are emerging today.

This year has seen the continued effects of the global polycrisis affecting trade, geopolitical stability and society but despite these challenges, many insurers have, where possible, continued to maintain the cover that kept businesses moving.

In this article, we take a look back at the major flashpoints of 2024 and how insurers’ innovative and information-

“As the complexity of managing risks, making decisions and tackling challenges in a world marked by rapid technological advances and increasingly interconnected risks grows, so too does the need for insurers to partner with technology providers that will look beyond fixing past issues for their clients and look to the present.”

informed approach to underwriting supported critical functions.

Economic uncertainty, an increase in armed conflicts and civil disturbances, set against a backdrop of the biggest election year in decades has created a dangerous cocktail of geopolitical conflict that poses great risk to an interconnected world that relies heavily on supply chains.

Militant attacks and heightened tensions near the world’s busiest maritime waterways, including Houthi attacks on ships in and near the Red Sea, have resulted in the rerouting of shipping vessels to longer and safer alternative paths. These alternate routes are likely here to stay for the foreseeable future, with shipping giant Maersk expecting Houthi disruption to last until the end of this year.

In addition to the threat of armed conflict, there have been several incidents of GPS interference recorded in the northern part of the Red Sea, as well as cases documented outside Jazan, Saudi Arabia and near the Yemen border within the Red Sea. According to our own data, we have identified Beirut-Rafic Al Hariri International airport in Lebanon as a common hotspot, with more than 30,000 spoofing incidents this year affecting both maritime and aviation operations for our clients.

However, despite this disruption, insurers are making use of threat intelligence providers to get granular data insights and risk alerts tailored to specific routes, vessels and proximity settings to help with risk mitigation.

As geopolitical turmoil continues, the insurance industry must embrace technology as a vital ally. By enhancing risk assessment, streamlining data processing, and improving operational efficiency, technology not only supports insurers in navigating current uncertainties but also prepares them for future challenges.

Such a rise in events often triggers one of two outcomes. Either insurers do not have the information they need to provide cover, nor the basis to confidently underwrite it and must withdraw their cover, or, a combination of access to the best data sets and an innovative approach to underwriting allows them to maintain continuity of cover and pursue opportunities in the market.

In our journey to help provide this confidence to our clients, we partnered with Ambrey, the global leader in maritime security. By combining Ambrey’s extensive experience in providing operational and digital maritime security services with Insurwave’s specialty insurance technology platform, risk managers, underwriters and exposure managers gain access to a comprehensive, global

view of marine perils and risk.

As part of this relationship, we helped our marine clients with alerts specific to their vessel routes to help them plan and react to events in real time and vessel affiliation checks to directly combat the militant groups now targeting shipping vessels based on company trade and vessel affiliations.

Reflecting on the current rise in conflict and its effects on the marine market, James Havard, head of exposure management at specialty insurer and reinsurer Convex, explained: “Today’s world poses a significant challenge to the marine insurance market, with shifting conflicts creating ongoing events across the globe. However, technology platforms such as Insurwave give us the ability to be more closely aligned with our clients and derive meaningful insights from a consolidated data source complete with the latest threat intelligence, allowing us to take action quickly.”

The challenging risk landscape and business environment in the past year has resulted in a number of firms looking to incorporate more additional layers of data to ensure their insights are as granular and comprehensive as possible.

As a specialty insurance platform ourselves, we see the value inconsolidating and correlating many different exposure data sets, an area in which we excel. One of the ways we have achieved this is by partnering with a large selection of different data providers across the market to integrate their functionalities into our platform.

Be it Ambrey’s threat intelligence capabilities or Spire as our vessel tracking provider, we understand the value technology providers can bring in terms of additional detailed data points.

For example, security and risk management firm Osprey Flight Solutions provides real-time alerts and detailed reports on emerging events affecting countries, airports and airspace to help aviation operators enhance their risk assessment and mitigation efforts. Most recently, the firm secured a deal with TUI Airline to use their insights.

Similarly, ShipsDNA, a provider of maritime data and information, also offers a wide range of data related to vessels, ports, routes and maritime events that can further enhance insurer’s insights. In the dynamic and complex maritime industry, accurate and timely data is crucial for insurers to effectively assess risks associated with these areas, to not only help insurers with comprehensive insights into maritime activities, but also assist them with evaluating risks and optimising underwriting strategies.

Ultimately, the value of this data extends well beyond operators to the underwriters taking on these risks. And as the complexity of managing risks, making decisions and tackling challenges in a world marked by rapid technological advances and increasingly interconnected risks grows, so too does the need for insurers to partner with technology

“Militant attacks and heightened tensions near the world’s busiest maritime waterways, including Houthi attacks on ships in and near the Red Sea, have resulted in the rerouting of shipping vessels to longer and safer alternative paths.”

providers that will look beyond fixing past issues for their clients and look to the present.

Insurers looking to establish a competitive edge are now embracing innovative, data-driven underwriting approaches. Rather than sticking with legacy technologies, which often focus on outdated risk profiles and solutions, insurers of tomorrow are turning to advanced data analytics, real-time risk assessment tools and artificial intelligence-powered insights to make more informed decisions.

As a technology provider, I find this evolution encouraging, as it demonstrates the value of converting raw data into actionable insights. This makes modern solutions not only relevant but essential in sustaining long-term success and, more importantly, the long-term functioning of essential shipping routes and ports across the world.

Neil Henderson , industry liaison, Gard, asks whether 2025 will be the year when the wind-assisted propulsion system (WAPS) becomes a technology of choice for shipowners looking to comply with the everincreasing roster of decarbonisation regulations and ongoing uncertainty around alternative fuel viability?

In August 2023 the CEO of a major wind equipment supplier boldly predicted that by 2025 “half the newbuild ships will be ordered with wind propulsion”.

While 2024 has seen a significant increase in large commercial vessels being fitted with some form of WAPS, approximately 50 to date, the newbuild numbers are still a long way short of that prediction. But is there reason for optimism that 2025 will be the year of the WAPS?

2024 has seen a host of announcements from shipowners in almost every segment of the market about the inclusion of WAPS on newbuilds or the retrofitting on existing vessels.

For example, in May, Mitsui O.S.K Lines (MOL) stated that seven newbuild bulk carriers and multi-purpose vessels would be fitted with WAPS equipment. In June, Union Maritime announced that BAR Technologies would be installing its WindWings rigid sails on 34 newbuilds, comprising installed 14 LR2 tankers, 12 chemical tankers and eight MR tankers.

In October, Klaveness Combination Carriers announced that it would be installing two bound4blue suction sails on its third CABU III newbuild. And in November, Maersk Tankers announced that it would be retrofitting five separate MR tankers with 20 of bound4blue’s 26-metre tall suction sails through the course of 2025 and 2026.

The International Windship Association recently stated that it anticipates there will be more than 100 large wind-assisted

powered vessels by the end of 2025, a doubling from current numbers. The rationale for the deployment of WAPS is becoming clearer.

More installations are reporting significant fuel savings achieved. The Pyxis Ocean, an 81,000dwt bulk carrier fitted with two BAR Technologies rigid sails, recorded fuel savings of up to 32% per nautical mile and achieved overall savings of 3mt/day in a six-month test period operating worldwide.

The TR Lady, an 82,000 dwt Kamsarmax bulk carrier retrofitted with three Anemoi rotor sails, recorded fuel savings on its 2023 maiden voyage which led to predictions of an average annual fuel saving of 10%.

“Incidents have included failures during the installation and testing phase, heavy weather damage, and collisions with berth equipment.”

The regulatory environment is becoming more conducive to fitting WAPS. From January 2024 the EU ETS trading scheme expanded to include shipping. This has seen actual figures for GHG emissions and corresponding payments to owners or purchase of EU allowances by charterers.

Those costs are presently only at 40% of the emissions reported for 2024, increasing to 70% for 2025 and 100% from 2026. Fuel savings from the deployment of WAPS will also result in reduced EU allowances having to be surrendered.

Similarly, the introduction of the FuelEU Maritime regulations in January 2025 brings the potential for significant financial penalties if the GHG intensity of the energy used exceeds the permitted level.

Those penalties will be determined, in part, by the quantity of fuel consumed. In the near term, a ‘Wind Reward Factor’ of between 1-5%, depending on the design power of WAPS installed onboard, can ensure compliance with FuelEU and avoid penalties up to 2030. In the longer term, the reduced fuel consumption should lessen any penalties.

Also on the horizon are the IMO’s mid-term measures, which should be finalised in Spring 2025. While there are competing options, the solution is likely to comprise some form of GHG fuel intensity element and a carbon pricing

mechanism (similar to the FuelEU and EU ETS, respectively).

While there is some degree of confidence in the likely regulatory developments, the same cannot be said for the geopolitical situation. The increasing global tensions, in particular in the Middle East, may lead to higher fuel prices regardless of any regulatory-imposed costs.

A further factor pointing towards the faster deployment of WAPS is the slower-than-needed progress of alternative fuel projects leading to greater uncertainty about future fuel availability and cost. This means that decisions on which technology to invest in are likely to be delayed.

Even if a shipowner might have been willing to make that choice now, across all sectors the order-to-delivery times are growing: approaching three years for tankers, more than three years for containerships and close to five years for LNG carriers. In these circumstances, retrofitting WAPS is a potential solution to extend the life of the vessel.

In an August 2024 report, Lloyd’s Register identified that the WAPS market was nearing a tipping point for rapid adoption.

Its analysis suggested that this requires standardisation of

the measurement of the propulsive energy of differing systems to enable effective comparison and a scaling-up of the supply chain, together with a great number of shipyards developing their capabilities to retrofit WAPS equipment.

The installation of WAPS equipment should be compatible with scheduled maintenance and therefore it offers a potential new source of revenue to shipyards without requiring additional berthing or drydocking facilities (albeit space will be needed for storage of the WAPS equipment before it is fitted).

There is a risk that as WAPS equipment is manufactured at scale and more shipyards undertake these activities, the quality of components and installations drops. But this should be balanced by greater knowledge of potential problems from the prototype projects both in terms of the equipment itself and its operation.

To date, there have been relatively few incidents and claims involving WAPS. These have been fewer than might have been expected with the introduction of new equipment, especially given that large sails and rotors are fitted on decks, often positioned alongside hatch covers and other cargo-related equipment.

Incidents have included failures during the installation and testing phase, heavy weather damage and allisions with berth equipment.

“In November, Maersk Tankers announced that it would be retrofitting five separate MR tankers with 20 of bound4blue’s 26-metre tall suction sails through the course of 2025 and 2026.”

The former two should be reduced through alterations to designs or their operation, while the latter are likely to be reduced through changes to ship-shore interactions.

The proliferation of WAPS onboard existing vessels and scheduled for newbuilds and retrofits means that insurers will inevitably be approached during the 2025 renewal season to provide insurance for the equipment. Their willingness to do so should ensure that 100 installations are passed during 2025. That milestone should make it possible to say that 2025 was the year of the WAPS.

21 March 2025

21 March 2025

Launched in 2018 and now in its eighth year, Marine Insurance London is Cannon Events’ flagship conference. With Lloyd’s at its heart, London is a global hub for marine insurance and our leading conference regularly attracts global heads and c-suite executives from across the marine industry to the speaker faculty. Our aim is to bring together insurers, reinsurers, brokers, shipping companies, service providers and others from the marine world to examine the current state of the marine insurance market and in this case, London’s role in it.

Co ee breaks: 11.00-11.30 & 15.00-15.20 Lunch: 12.30-13.20

08.55-09.00 Welcome Address: Daniel Creasey, Managing Director, Cannon Events

09.20-10.00

Panel Discussion: State of the Market – Going Too Well?

The marine insurance market cycle never sleeps and after a few good years, it appears some sections of the market are on the brink of turning downwards once more. In this session, we analyse the results of the 1/1 reinsurance and the 20th February P&I renewal season, before looking at its impact on the primary market.

Moderator: Louise Nevill, Chief Executive O cer, Marine, Cargo and Logistics, Marsh

Panellists: Ilias Tsakiris, Chief Executive O cer, Hellenic Hull and Chair, Ocean Hull Committee, International Union of Marine Insurance

John Owen, Head of Specialty, AXIS Global Markets

10.00-10.20

Fireside Chat: Biting o More than You Can Chew – Market Appetite

Managing general agents make up a sizeable component of the market, willing to take a considerable sum onto their books. However, as claims become more frequent and costly, the question that is emerging is whether MGAs are biting o more than they can chew, or whether it is time to scale back on the risk-taking.

Participants: Manos Lorentzos, Executive Director, Seascope Europe and Chairman, Hellenic Committee, Lloyd’s Brokers Associates

10.20-10.40 Presentation: TBC

10.40-11.00 Presentation: 2025 – The Year of the AI Work Colleague

In this session we consider how AI might change the lives of underwriters and whether they are ready to accept that AI colleague.

Presenter: Andy Yeoman, Chief Executive O cer, Concirrus

11.30-11.50

Presentation: Pollution – One Step Away from a Major Disaster

The Sounion case o the Yemeni coast almost proved the point as we discuss in this session, in which we ask whether salvors will always be prepared to go into such dangerous situations and how that question should impact insurer behaviour.

15.20-16.10

11.50-12.30

Panel Discussion: War – It’s All in the Wording

This session will explore the di erence in war risks between markets to see whether, given the tests of the last few years, the products are still fit for purpose or whether more work is needed.

Panellists: Anders Hovelsrud Insurance Director (CEFOR Chair), Den Norske Krigsforsikring for Skib (DNK)

Annabel Davies, Head of Marine Hull, Lancashire Insurance

13.20-14.00

Panel Discussion: LOF

Moderator: Faz Peermohamed, Partner, Stann Law

Panellist: Francesco Zolezzi, Claims Manager, Cambiaso Risso

14.00-14.20 Fireside Chat: Calling Time on Sanctions?

In this session, we take a hypothetical scenario of a tanker hitting the Spanish coast and spilling its sanctioned oil and consider who bears the ultimate responsibility and who would be left footing the bill.

Participants: Mike Salthouse, Head of External A airs, NorthStandard

14.20-14.40

In Summary: Legally Speaking

In recent times, a number of high-profile cases have gone through the courts. In this session, we provide a summary of those major cases and ask whether they will be market changing events.

Presenter: Peter MacDonald Eggers KC, Barrister, 7 King’s Bench Walk

14.40-15.00

Presentation: Is Nuclear Power Viable for Shipping?

Many in the market believe nuclear power will be the future for shipping if it wants to go green. However, beyond understanding the technology itself, there are plenty of questions to answer before nuclear becomes a viable alternative for the industry, including the need to revamp the legal frameworks, as well as policy wordings and availability of reinsurance for such vessels.

Presenter: Neil Henderson, Senior Executive Industry Liaison, Gard

16.10-16.30

Fireside Chat: Training for Fires

In this session, we investigate why this is happening and consider the impact of cutting training budgets. We also consider the risk of downsizing the numbers of crew on board as vessels become more automated.

Participants: Jacob Damgaard, Divisional Director – Head of Loss Prevention, Britannia P&I Capt. Simon Hodgkinson, Global Head of Loss Prevention, West of England P&I Club

16.30-16.45

Presentation: The Insurers Role in Enabling Change

Geopolitics and the increasing use of sanctions and now tari s are reshaping the trading environment and manipulating commodity markets. The legal requirement to reduce GHG is forcing shipowners to adopt new untried technologies each with their own unique claim profiles.

Presenter: Helen Barden, Director- External A airs, NorthStandard

16.45-17.00 Presentation: Eyes on the Bridge

The use of technology is changing rapidly, with artificial intelligence moving to the centre of the world of work. In this session, we ask how often AI is already being used as an extra pair of eyes on the bridge and whether the insurance industry is keeping up with these changes. Are insurers truly aware of the emerging risks that sit alongside this technology?

15.20-16.10

Roundtable sessions: Each roundtable will run for 20 minutes. There will be a 5-minute break to allow delegates to change tables and the tables will then be repeated in a second 20-minute seating.

From increased threats to the supply chain to a larger focus on technology,Jim Heide, COO/Co-founder Loadsure identifies the key supply chain trends to look out for in 2025

The pace of the global supply chain showed no signs of slowing in 2024. In fact, the global freight and logistics market is forecast to be worth $18.69bn by 2026.

It was, however, another year of considerable disruption in many different forms, from increasingly sophisticated cargo theft to evolving geopolitical situations, as well as frequent instances of extreme weather.

But how did the industry respond and what can businesses do to manage risk, minimise loss and bolster their resilience in the year ahead?

Keep reading for my predictions on the key supply chain trends we’re likely to encounter in 2025.

1. Renewed focus on cost-efficiency.

The ongoing cost of living crisis has become a global issue and, while it looks different in every country, businesses around the world are attempting to counter high inflation by cutting costs in an effort to stabilise their bottom lines.

In transport and logistics, we are likely to see SMEs ramping up measures like load consolidation and route

optimisation (eg to reduce deadhead miles) and I hope we will also see fewer loads being stored and shipped without the right coverage.

Taking out a policy that is designed to cover the actual value of the load, as well as the specific risks applicable, is one of the best steps supply chain businesses can take to insulate themselves from loss.

With data-priced policies available through providers such as Loadsure, the upfront cost of the insurance is undoubtedly worthwhile.

2. Enhanced visibility of the supply chain, through data & AI. For the last few years, artificial intelligence (AI) tools have slowly but steadily infiltrated business workflows. Today, these tools are seamlessly optimising any number of processes within the supply chain.

Through historic and predictive data, AI can forecast fluctuations in capacity and raw materials, enabling businesses to adjust their procurement strategies accordingly.

You can map the shipping routes that pose the lowest risk and even minimise the chance of cargo damage in transit through AI-modelled loading configurations.

It’s a core part of our holistic freight protection offering too. We collaborate with a number of innovative data partners to deliver actionable insights that predict and prevent loss for our assureds.

3. Increased commitment to sustainability.

The impacts of climate change are only becoming more evident, with extreme weather events such as Hurricane Milton causing huge financial losses.

The European Environment Agency has predicted that global logistics will cause 40% of global carbon emissions by 2040. Sustainability has also gone from a compliance tick box to a central component of business strategy.

In 2025, I expect businesses to further prioritise the

“Agility is crucial to survival in such a tumultuous landscape, and the businesses equipped to adapt to evolving market conditions, comply with new regulations, or meet unexpected customer demands will fare best.”

reduction of environmental impact, embracing alternative fuels, investing in low and no-emission vehicles, while taking steps to cut last-mile emissions too.

4. Continued navigation of geopolitical events.

2024 was a year of considerable political upheaval. As well as several key elections in the west, we saw the continuation of the war in Ukraine and the escalation of the conflict in Gaza.

The economic impact of these geopolitical events cannot be understated. From boycotts and trade sanctions to changing tariffs, there is so much for supply chain businesses to navigate.

Agility is crucial to survival in such a tumultuous landscape and the businesses equipped to adapt to evolving market conditions, comply with new regulations, or meet unexpected customer demands will fare best.

As we welcome a new year, we urge supply chain businesses to harness emerging technologies that are improving agility and resilience, and join us at the new frontier of risk management: holistic freight protection.

Our 360-degree risk management solution starts at the source, with the prediction and prevention of loss through data insights.

Through our dynamic pricing model, we then deliver data-priced insurance products for almost every risk, including shipper’s interest, stock throughput and motor truck cargo insurance.

Lastly, we ensure that when unavoidable loss does occur, recouping that loss is quick and painless, thanks to our transparent automated claims process.

08.55-09.00 Welcome Address: Daniel Creasey, Managing Director, Cannon Events 09.00-09.30 09.30-10.15

Keynote Address: Becoming and Staying a Digital Leader

This keynote will explain Gard's digital journey, how to modernise the technical foundation and how digitalisation is revolutionizing the marine insurance industry by improving customer experience, taking better decisions and improving e ciency.

Presenter: Catherine Hopstock, Vice President, Head of Technology, Gard

Panel Discussion: Future Trends in Marine and Energy Insurtech

This session will discuss how insurtech might transform the way risks are assessed, priced, and managed in the Marine and Energy sectors.

Moderator: Mark Bennett, Senior Vice President of Global Business Development, ACORD

Panellists: Ronny Reppe, Chief Executive O cer, Noria Digital Jonathan Humm, Deputy Head of Marine & Energy, AEGIS

Adam Starling, Senior Vice President, Data Programme Leader, MARSH

10.15-11.00

Panel Discussion: The Elephant in the Room: legacy Ine ciencies and how to address them

On average underwriters spend 40% of their time on tasks that don’t add value to their business, this provides a huge opportunity that can directly influence an Insurers bottom line, but how best to go about tackling these ine ciencies, especially when processes and procedures maybe engrained in an insurers cultural and physical operations.

Panellists: Andy Yeoman, Chief Executive O cer, Concirrus

Alexander Brill, Chief Technology O cer, DNK

Ed Davies, Chief Information O cer, West of England Insurance Services

11.30-11.50 Fireside Chat: The Future of Recruiting

This session will discuss how technology will a ect recruitment withing energy and marine insurance. Attracting di erent talent outside of underwriting and claims, Changing tech landscape and what will the new generation of marine & energy insurer look like?

11.50-12.30 12.30-12.50 12.50-13.15

Panel Discussion: The Rise of the Tech Based Insurer

By leveraging technology, insurers can enhance risk assessment, provide more personalized policies, lower costs, and improve customer satisfaction. However, challenges related to data security, regulatory compliance, and the need for human expertise in complex situations must be carefully managed.

Panellists: Farris Salah, Head of Smart Follow, APOLLO

Ed Colcough, Underwriter, Parsyl

Tony Hildrew, Chief Executive O cer, Ceto AI

Fireside Discussion: Shipshape Technology Needed to Keep Your License Compliance and audit put new stress on core systems and surrounding capabilities. In this session we discuss what it takes to be shipshape for meeting regulations like Solvency II, DORA, IFRS, PRA, FCA, GDPR, and IFRS 17.

Participants: Lars Ola Rambøl, Product Director, Noria Digital

Fireside Chat: Modelled Emissions Data in Sustainability Reporting

Insurers across Europe are grappling with the Corporate Sustainability Reporting Directive (CSRD) – a sweeping new EU regulation reshaping corporate reporting requirements. As the industry debates how to adapt, one of the key questions remains: how can insurers calculate scope 3 emissions from their insured portfolios? This session will discuss how the PPMI’s work with modelled emissions data has helped its Signatories to navigate and comply with new reporting requirements.

Participants: Sigvald Fossum, Vice President, Head of Analytics, Gard Ralf Garn, Managing Director, OceanScore

14.15-15.15 Workshop: Technological Innovations in Risk Assessment

Marine & energy insurance risk aggregation software provides insurers with the tools they need to better understand, quantify, and manage complex risks associated with the marine & energy insurance industry.

Participants: Matthew Twist, Commercial Director, Concirrus

15.15-16.00 Workshop: Claims Management Innovations

This workshop will discuss how marine and energy insurers can streamline claims operations, reduce fraud and ultimately improve profitability. Fraud, Making the claims team life easier through automation, Tracking of longtail claims, Speed of information transfer from third parties.

11.00-11.30: Co ee break 13.15-14.15: Lunch 16.00-17.00: Drinks Reception

Zhi Chin Lim , data and analytics product owner at Seamless Insure, explains how APIs can help with risk assessment, measurement and transfer in the marine insurance sector

Application programming interfaces (APIs) are essential tools that enable seamless data exchange across systems, allowing software applications to communicate. In the insurance industry, APIs facilitate real-time data access, automate workflows and enhance decision-making and operational efficiency.

APIs provide insurers with real-time data on cargo movement, location and status, supporting risk assessment during quotations and monitoring accumulation risk, especially for temporary storage coverage. They also automate policy issuance and claims validation,

improving customer satisfaction and reducing administrative costs.

For hull insurance, APIs offer critical vessel data, including physical characteristics, ownership, incident history, maintenance and operational behaviour.

This information helps insurers evaluate risks, set premium pricing and continuously monitor a vessel’s status for incidents or mechanical issues.

Real-time data allows insurers to adjust coverage and pricing strategies based on ongoing risk assessments.

APIs provide access to various types of data that are crucial for the marine insurance industry. These data types include:

Vessel data: Information about a vessel’s physical attributes, such as its age, size, type, and construction details, etc. Additionally, vessel data may cover performance history, ownership details and management records, which can be vital for risk assessments; Cargo data: Data on the cargo being transported, including its nature, value, weight and packaging. This information is crucial for cargo insurers in their risk assessment process where appropriate insurance coverage and pricing is determined; and,

Voyage data: Details about the vessel’s route, estimated time of arrival, ports of call, and any deviations from the planned route. This data is essential for tracking the movement of cargo and vessels in real time, identifying potential risks such as exposure to piracy or extreme weather conditions.

The key use is through automation and streamlining processes.

APIs streamline record-keeping by providing accurate, up-to-date vessel information, automating tasks like registry updates, maintenance tracking and ownership management. This reduces manual data entry and improves record accuracy.

Another key area is risk assessment and pricing.

Data accessed via APIs allows insurers to conduct comprehensive risk assessments using data on a vessel’s performance history, operational behaviour, and physical characteristics (eg age, size).

Ownership and management data offer insights into reliability, refining risk evaluation and pricing strategies.

APIs can help insurers automate compliance checks by accessing updated sanctions information on vessels, owners, and operators.

This helps insurers meet regulatory requirements, avoid penalties and quickly identify compliance risks through regular automated checks, reducing administrative burden.

Here’s an overview of six prominent data providers offering API solutions that help insurers access critical maritime data for risk assessment, underwriting and regulatory compliance.

> Windward

Windward leads in Maritime AI, offering a platform for risk management and maritime awareness. Its APIs provide data on vessel behaviours like dark activities, ship-to-ship transfers and port calls, along with inspection histories. AI-driven insights support underwriting, compliance and due diligence, delivering go/no-go risk recommendations and enabling pre-bind sanctions screening. This allows insurers to integrate real-time risk assessment and compliance checks seamlessly.

> The Signal Group

The Signal Group combines shipping expertise with analytics through its Signal Ocean platform, offering APIs for tracking vessel activities. The daily vessels state API provides data on position, speed, and cargo status for portfolio monitoring. The vessels API includes specifications and ownership data, while the voyages API covers ship movements and cargo details since 2014, aiding in risk reporting and exposure assessment.

> Kpler

Kpler specialises in data and analytics for energy and shipping markets. Its AIS tracking API enables real-time monitoring of vessel movements, backed by a historical archive. This supports compliance, trend analysis and portfolio monitoring. The real-time events API covers port calls and bunkering activities, providing insights for dynamic risk management. The ship database API offers vessel information for underwriting and documentation.

> RightShip

RightShip is an ESG-focused platform promoting maritime safety and sustainability. Its vessel API delivers data on

safety scores, GHG ratings, inspection status and restrictions, aiding sanctions checks and risk management. This information supports the assessment of safety scores during sanctions checks, evaluates inspection outcomes and helps to enforce restrictions for better risk management.

> Datalastic

Datalastic offers maritime data through its vessel tracker API, combining historical and real-time AIS data. The Vessel API provides records on movements, ownership, and speed for exposure monitoring, while the ship inspections service gives details on past inspections and outcomes. Additional data on ship sales and casualties supports informed underwriting.

> S&P Global Maritime

S&P Global Maritime provides vessel data via API, including ownership, tonnage, dimensions, and ship type. This data automates underwriting processes and maintains accurate records for risk assessments, streamlining data integration across systems.

Integrating with data providers allows insurance companies to leverage external maritime data effectively within their systems.

There are two primary methods for integrating with data providers: core system integration via API calls and database integration.

Connecting APIs directly to the insurer’s core platform allows real-time data flow, enabling dynamic updates and automated processes. Key benefits include:

> Risk assessment: Real-time vessel behaviour, inspection history, and voyage data streamline underwriting and pricing decisions;

> Sanctions status check: APIs provide instant access to compliance data, enabling pre-bind screening and ongoing monitoring;

> Post-bind updates: Continuous updates on vessel condition, ownership and voyage status support proactive coverage adjustments; and,

> Claims validation: Real-time data on events like port calls and cargo incidents enhance claims accuracy and reduce fraud through efficient data retrieval.

This approach involves direct data exchange between the insurer’s and provider’s databases, ideal for large datasets or established systems. Key considerations include:

> Bulk data loading: Facilitates transferring large datasets, such as historical AIS records, for long-term analysis;

> Periodic updates: Allows batch data synchronisation for

“Real-time data allows insurers to adjust coverage and pricing strategies based on ongoing risk assessments.’’

non-real-time processes; and,

> Data consistency and standardisation: Ensures uniform data structure across systems for effective analytics, reporting, and compliance.

Integrating through APIs or database connections enables insurers to optimise risk management and regulatory compliance by using comprehensive, timely maritime data. The choice depends on technical infrastructure, data needs and processing requirements.

Beyond integrating with data providers, Seamless offers a built-in and customisable risk assessment matrix designed specifically for marine insurers.

This matrix enables insurers to assess and score risks across five key segments: vessel information, performance history, operational characteristics, ownership and management, as well as regulatory compliance.

Each segment contains defined data fields that are rated against a pre-established risk matrix, generating an overall risk score to guide underwriting decisions.

The matrix allows for flexibility and customisation, enabling insurers to tailor risk factors to their specific requirements.

For instance, the port of registry may influence the risk score, as different ports have varying safety standards and facilities. Vessels registered in ports with stricter safety regulations might score more favourably, reflecting lower risks.

Similarly, the year of build can be a critical factor, as older vessels may be prone to structural fatigue and may lack modern technology, resulting in a higher risk score.

By leveraging Seamless’ risk assessment matrix, insurers can dynamically adjust risk variables to better reflect the evolving nature of maritime risks, enabling more informed decision-making and optimising the risk assessment process.

One year with the EU Emission Trading System (ETS) from a P&I perspective

Simone Vitzthum , assistant V ice P resident, loss prevention, lawyer, at Skuld explains the complexities of the EU’s ETS system

Since 1 January 2024 the EU ETS Directive (EU ETS) includes maritime transport. It puts a price on greenhouse gas (GHG) emissions from ships. For the calendar years 2024 and 2025 this will only include CO2 emissions, while from 2026 onwards the scope will include other GHGs, for example, methane (CH4) and nitrous oxide (N2O).

The EU ETS applies to all vessels of 5,000 GT or above which commercially carry cargo or passengers and call at a port within the European Economic Area (EEA).

For each metric tonne of CO2 emitted one EU emission allowance (EUA) must be surrendered to the competent EU administering authority. GHGs other than CO2 are converted into their CO2 equivalent (CO2e) to standardise their impact.

To help the shipping community a phase-in period was included. For the compliance year 2024 only 40% of the overall CO2 emissions released must be compensated by the equivalent numbers of EUAs; for 2025 it is 70%, thereafter 100%.

The EU ETS is flag-neutral and route-based. This means that it only applies to port calls within the EEA. To constitute a ‘port of call’ stop under the EU ETS, a vessel must either engage in commercial cargo operations or, if it is a passenger ship, the embarking or disembarking of passengers within the port limits of an EEA port. For ‘intraEU voyages’ 100% of the GHG emissions must be covered by the equivalent number of EUAs, and for ‘extra-EEA voyages’ only 50% of the GHG emissions produced must be compensated by the corresponding number of EUAs.

In Commission Implementing Regulation (EU) 2023/2297 which also entered into force on 1 January 2024 an exception was codified for container vessels. It stipulates that if a container vessel calls any of the ports named in that regulation for the sole purpose of transshipping the containers, then such a stop constitutes an exclusion from the definition of ‘port of call’ of stops of container ships.

It is the shipping companies which need to be compliant with the EU ETS. The default position under the EU ETS is that the registered shipowner is the shipping company. But

the shipowner can delegate the EU ETS responsibility with explicit contract to an ISM-company (the DOC holder).

The shipping company must record all the ship’s GHG emission data for any commercial voyage which starts or ends at an EEA port via the Thetis-MRV system.

By either 28 February or 31 March 2025, the recorded emissions data for 2024 must be verified by EU accredited verifiers.

On the basis of the verified emission data, the required number of EUAs for the compliance year 2024 will be calculated and must then be surrendered by the shipping company to the competent administering authority by latest 30 September 2025 on a ‘fleet level’.

Under the EU ETS, all ships for which a shipping company carries the EU ETS responsibility for constitute one fleet, regardless of the ships’ ownership or flag. If an insufficient number of EUAs are surrendered for only one ship, the whole fleet will become non-compliant.

Any EUAs owed must still be surrendered plus a fine of €100 must be paid for each EUA short. In addition, the EU will publish the name of the shipping company which did surrender an insufficient number of EUAs.

If the outstanding EUAs are not surrendered and the fine not settled for two consecutive years, the EEA countries have the possibility to issue port bans against a shipping company and its fleet.

There are several recurring questions we have seen from assured’s since the EU ETS came into force, especially about how to obtain and surrender EUAs which are a tradeable commodity on the EU carbon market.

They can be obtained by auction via the European Energy Exchange (EEX) or purchased via a bank or broker. They can be saved for a later day, as EUAs issued on or after 1 January 2013, remain valid indefinitely until they are surrendered to cover GHG emissions.

EUAs can only be surrendered to the competent administering authority from a Maritime Operator Holding Account (MOHA) which only the shipping company can open, never a charterer. A charterer can only open a trading account.

A common question has been whether STS operations constitute a commercial port call under the EU ETS, which

“The EU ETS is flag-neutral and route-based. This means that it only applies to port calls within the EEA. To constitute a ‘port of call’ stop under the EU ETS, a vessel must

either engage in commercial cargo operations or, if it is a passenger ship, the embarking or disembarking

of passengers within the port limits of an EEA port.”

they do if the cargo operations are carried out within the geographical scope of an EEA port.

For charterparty queries, the most frequent recommendation to the assureds has been, to ensure that they cover themselves with EU ETS charterparty clauses, especially if they are in the middle of a charter chain (back-to-back clauses), to avoid any exposure or contractual uncertainties.

Compliance should be taken seriously. Shipping companies that have not yet been assigned an administering authority,

may contact the European Maritime Safety Agency (EMSA) to help them navigate this.

EMSA can help with setting up a Thetis-MRV account which is the necessary platform to which all GHG emission data must be submitted to ships calling or departing EEA ports.

We recommend that shipowners obtain EUAs to use in situations in which charterers may not have (yet) provided owners with enough EUAs due to an underlying a charterparty dispute. Such EUAs in reserve can be used to bridge any gaps and thereby minimise the risk of being non-compliant.

Matthew Dow left, Shipping Partner and Donal Keaney Partner and Marine Master at Hill Dickinson analyse recent marine casualty trends and provide readers with a high-level overview of some of the key considerations to be addressed following an incident involving a vessel on-risk