KALEIDOSCOPE THE ECONOMIC

A publication by the CJC Economics Department VOLUME 1I World Events 2022

To quote French philosopher Simone Weil, “The joy of learning is as indispensable in study as breathing is in running”. What we learn with joy we will never forget. It becomes a part of us.

As an Economics teacher, nothing has been more satisfying for me than to help students uncover the joy and relevance of studying Economics, abstract though the concepts may seem to be at first. Whether it was a discussion in class on why women tend to earn less than men despite having the same educational qualifications, or an overseas trip to learn about various trading ports and industries peculiar to that country, I have learnt as much as my students and the learning stays with me up till this day.

I am happy to see the sustained efforts and growth of this Economics newsletter, created by students, for students. I congratulate you who have worked in teams and undergone an Inquiry-Based Learning approach to analyse recent world phenomena using an Economics lens. This volume II covers a wide range of contexts in which Economics is applied. It makes for an interesting read. I encourage all Economics students to take time to read through the contents of the newsletter and think critically about the issues raised. You can challenge the views raised and discuss them rigorously with your peers. What you learn will also directly move you closer to your short-term goal of getting the A grade for Economics.

It is my and your teachers’ hope term goal of enjoying Economics critical thinkers and concerned contributions to our community.

FMrs. Poon Wai Chin

3

o r e w o r d .

VICE-PRINCIPAL (ACADEMIC)

UK's Post-Pandemic Economy

By: Gao Zhijun (2T28) Raphael (2T16)

Yu Wen (2T25) Ng aii (2T25)

Renee (2T25) Yuan Jun (2T26) Rising Price Level (Yonder, n d )

The UK Parliament sounded the alarm with a stark declaration: the cost of living surged dramatically across the UK. This assertion has cast a glaring spotlight on the pressing cost of living crisis that gripped the nation throughout 2021 and 2022. Yet, what underlying factors contributed to the emergence of this alarming crisis?

Demand-pull & Cost-Push inflation

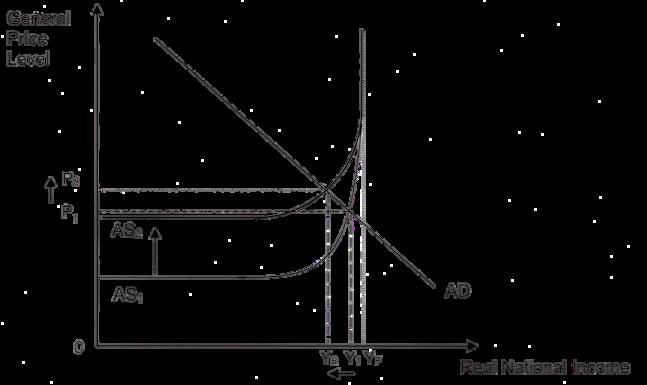

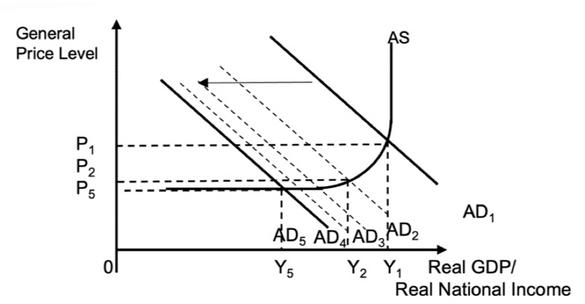

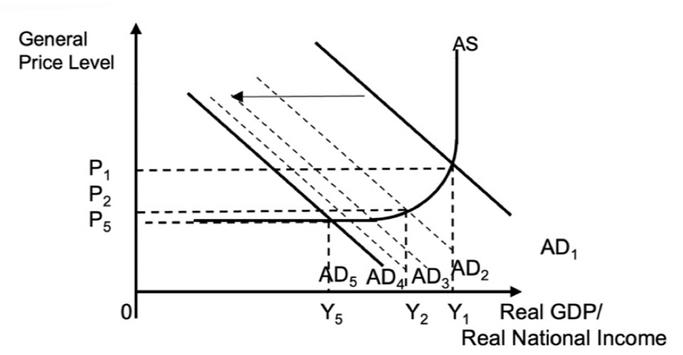

The global energy crisis caused by the Russian-Ukraine conflicts has pushed energy prices, a key factor input across economic sectors in the UK, to an exorbitant level. With the resulting rise in the cost of production, there is a decrease in the short-run aggregate supply (SRAS) of the economy as the SRAS curve shifts upwards from SRAS1 to SRAS2.

This creates a shortage of goods at the prevailing general price level, exerting upward pressure on the GPL as the GPL rises to P2 (Fig.1). This has raised the price of goods, including electricity and food, to a shocking level; the latter nearly tripled its price after the pandemic.

Figure 1: Cost-Push Inflation Using Keynesian ADAS Model

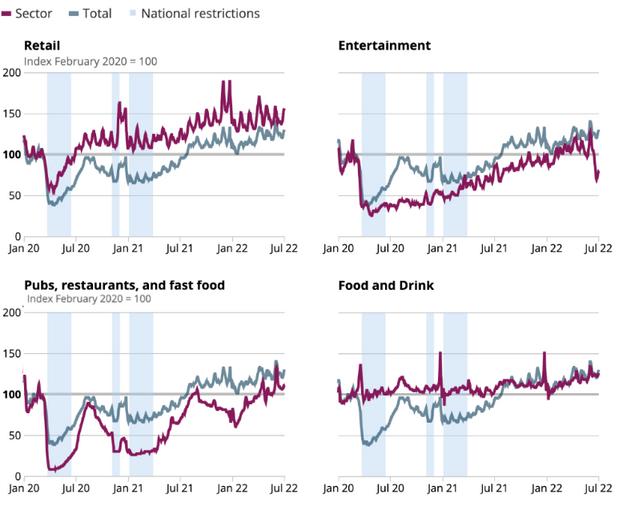

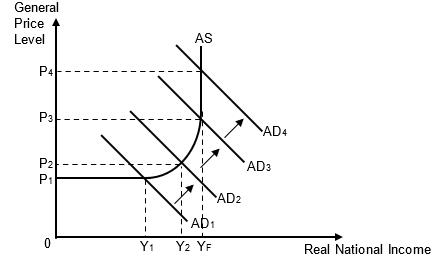

Demand-pull inflation made the UK’s cost of living crisis more prominent. After the relaxation of COVID-19 restrictions, there was a resurgence in interest in travelling to Britain, leading to a surge in tourism in the UK during post-pandemic. The exports and net exports (X-M) rose correspondingly, ceteris paribus. There was also a rising disposable income after the increased transfer payments during the pandemic, and a ‘revenge-buying’ spirit after months of staying at home. UK consumers’ domestic consumption across sectors demonstrated notable increases as the measures were lifted (Fig. 2). The rise in consumption, C and (X-M) increases the AD, creating a shortage of goods at the initial general price level, and exerts upward pressure on the prevailing GPL causing further demand-pull inflation, worsening the UK’s cost-of-living crisis.

Undesired consequences

UK citizens faced deteriorations in purchasing power due to inflation. Only able to afford fewer goods and services, they experienced a fall in their material standard of living. The horrifying housing crisis embodies the hardships of the British during the post-Covid era.

Figure.2: UK’s consumption across sectors

(Croudace, 2022)

Figure.2: UK’s consumption across sectors

(Croudace, 2022)

-Housing Crisis

The cost of housing peaked at a shocking 292,118 GBP in July 2022, reflecting the soaring GPL in the UK. Given the extreme costs associated with purchasing a house, many individuals resort to renting, only to discover that the expenses associated with renting are similarly high. This has left many, around 271,000 households, with no choice but to choose between being a homeless man or a starving man without a roof over their heads.

Figure.3: Rate of homelessness in UK

(Berry,2021)

Possible Policies and Effectiveness

- Cost of Living

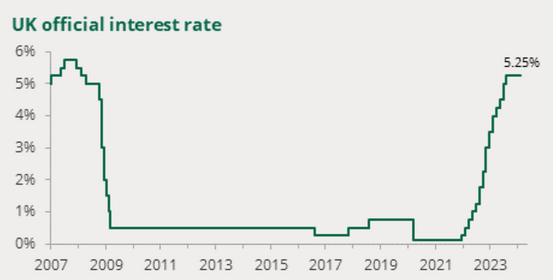

The British government implemented various policies to combat rising living costs, aside from raising the interest rate (Fig.4), the government raised the national insurance contribution (NIC) threshold. This can alleviate the financial strain on lowincome earners, improve income distribution, encourage workforce participation, and boost disposable income for lower income brackets.

(Harari,2023)

Figure.4: UK’s interest rate policy

-Housing Crisis

To tackle the housing crisis specifically, the UK government pushed policies through Thatcher-era rules, forcing local authorities to sell off houses, at vastly discounted prices. In two years, ⅔ of housing were lost to privatisation. However, the policy failed to target the root cause, as the supply of houses remained the same, leading to 1 in 182 homeless in the UK today. Therefore, increasing the number of private houses may be used in tandem with the existing policy.

Concluding Remarks

As time progresses into 2024, the cost of living crisis has become less of a concern. With careful planning and consistent efforts from the British government, it may be just a matter of time before Britain's economy to prosper again.

Bibliography (image source):

Berry, C (2021, December 9) The shocking scale of homelessness in England Shelter https://blog shelter org uk/2021/12/the-shockingscale-of-homelessness-in-england/

Croudace, L (2022, July 10) How our spending has changed since the end of coronavirus (covid-19) restrictions How our spending has changed since the end of coronavirus (COVID-19) restrictions - Office for National Statistics https://www ons gov uk/businessindustryandtrade/retailindustry/articles/howourspendinghaschangedsincetheendofcoronaviruscovid19restri ctions/2022-07-11

Harari, D. (2023, September 27). Economic Update: Have interest rates peaked? https://policymogul.com/library-material/2005/economicupdate-have-interest-rates-peaked-library-material-policymogul

Yonder. (n.d.). How to reach, engage and support vulnerable audiences. https://yonderconsulting.com/whitepaper-page/how-to-reachengage-and-support-vulnerable-audiences/

TRADE SANCTIONS ON RUSSIA

Introduction

Sanctions placed on Russia amidst the Russia-Ukraine war had aims of weakening Russia’s capacity to produce goods for war - the sanctions would reduce the volume of factor inputs entering Russia’s market, reducing their ability to produce goods for military efforts. This prevents the entry of Russian goods into the international market, reducing the export revenue Russia earns, decreasing the funds they have for their war efforts.

Effects on Russia’s export revenue

Dewi, Business Owner

Many countries like the US and Canada imposed stringent sanctions on Russia’s exports, causing Russia’s export revenue to decrease. For instance, US and various European countries banned imports on crude oil, causing a fall in Russian exports of oil where revenue dropped by over a quarter from Jan 2022-2023.

Effects on Investment

Furthermore, MNCs like Nike, Adidas and McDonalds also stopped investing in Russia and pulled out their businesses due to global consumer pressures, causing a decrease in FDI by these firms.

Effects on growth, unemployment and balance of payments

With reference to figure 1, the autonomous decrease in I and (XM) causes AD to decrease and shift leftward from AD1 to AD2.

Initial fall in AD causes a fall in RNY from Y1 to Y2. Assuming economy operates below full capacity, firms will employ less factors of production to decrease output, causing a decrease in income induced consumption, which further decreases AD. This triggers many successive rounds of decreases in RNY and income induced consumption, with the decrease getting smaller after each round. This process occurs until the fall in RNY is too small to generate any further decrease in income induced consumption. Thus, initial autonomous decrease in AD causes a multiplied final decrease in RNY from Y1 to Y5.

Figure 1

Effects on growth, unemployment and balance of payments

(continued)

Thus, there is negative actual economic growth. With a multiplied decrease in aggregate demand, derived demand for labour falls, causing demand-deficient unemployment. A fall in FDI leads to a fall in the inflow of currency, thus worsening the balance of payments through the capital and financial account. As mentioned previously, there is also a fall in the (X-M) which contributes to a BOT deficit.

Effects on Inflation

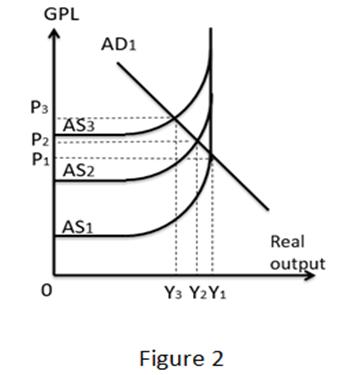

Inflation rate in Russia also rose to about 7.5 percent in November 2023. This could be due to the European Union’s ban on exports to Russia such as factor inputs like lithium batteries, causing the cost of production for many goods in Russia to increase. As such, firms will be willing and able to sell each level of output only at a higher price. With reference to figure 2, the short run aggregate supply (SRAS) of Russia will fall, and SRAS curve shifts upwards from SRAS1 to SRAS2 and further increases in cost of production cause a further shift to SRAS3. This creates a shortage at initial GPL P1, exerting an upward pressure on price until shortage is eliminated and GPL rises to P3, causing cost-push inflation.

Figure 2

Effect on Potential Growth

As mentioned previously, the sanctions against Russia caused a fall in FDI in the country. Furthermore, government expenditure on capital is also limited by heavy military spending. The Russian government is estimated to have spent around $132 billion on direct costs of the war in Ukraine alone. This means that there is a high opportunity cost, as the money that is used for the war effort cannot be spent on supporting research and development, infrastructure upgrades, and investment grants. Assuming the rate of depreciation of current capital stock is more than increase in capital stock, LRAS falls and the full employment level of output decreases, leading to negative potential growth.

"The team provided us with unwavering assistance since Day 1. I will definitely recommend getting your dream home with Warner "

Cahaya Dewi, Business Owner

Conclusion

Overall, sanctions on Russia’s exports as well as imports to Russia have caused a lower overall standard of living for citizens. With negative actual growth, less goods are produced. Consequently, citizens will have less income to purchase goods and services as they become unemployed, and with rising inflation, people’s purchasing power decreases. Thus, they are able to consume a lower quantity of goods and services, leading to a lower material standard of living. Moreover, with government funds being channelled into the war efforts, there are less funds to develop other sectors and an opportunity cost is incurred in other areas such as healthcare and education. This reduced spending could lead to a lower life expectancy and literacy rate, which causes the Human Development Index to fall, and thus non material standard of living falls as well.

KONG CHING WING, KENDRICK (2T01)

WONG JING XUAN KAYLA (2T01)

ERNEST NG KAI YAO (2T05)

DAVID NG JING TIAN (2T16)

CHEN XINGYU (2T01)

MIKAEL HO JIA LEI (2T01) 6.

GROUP MEMBERS

1.

2.

3.

4.

5.

The Effects of Stock Market Declines on the US Economy

Origin of the 2022 US Stock Market Decline

In 2022, Russia started an invasion of Ukraine in a grab for power, affecting the growth prospects and inflationary pressure for the economies of many countries. During the period, the US Federal Reserve also raised its interest rates continuously to lower inflation. Subsequently, the U.S. stock market declined significantly, leaving many investors reeling from the crisis. This had an effect on the general US economy.

Effects on AD of the US economy

The decline of the stock market triggered a fall in wealth for Americans investors as stocks form a part of household assets, and purchasing power of households decreased, subsequently causing a fall in consumption (C). Moreover, as there are many firms in the US economy that also invest in stocks, firms are affected negatively. For example, Amazon is an aggressive investor in the stocks of other companies. Therefore, a decline in the stock market can cause them to make losses in their stocks, and therefore their post-tax profits will fall, and thus they have less ability to invest. Hence, investment (I) also fell, and AD decreased.

How a fall in AD affects economic growth and unemployment

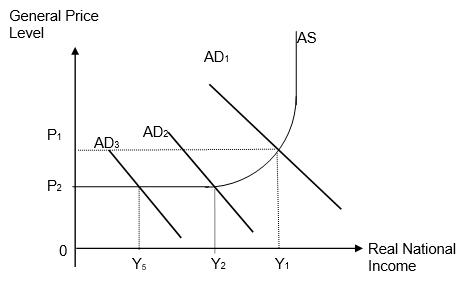

With reference to figure 1, As AD shifts rightward from AD1 to AD2, real national income (RNY) drops from Y1 to Y2, subsequently causing a decrease in income-induced consumption, triggering the reverse multiplier process. AD will experience further decreases through successive rounds of decrease in RNY and income-induced consumption, with the decrease getting smaller each round, stopping when the fall in RNY is too small to generate another round of decrease in income-induced consumption. AD and RNY subsequently fall to AD5 and Y5, respectively. This contributes to overall lower economic growth in the US.

Due to the multiplied decrease in real national income and real output, the derived demand for all factors of production, including labour, will also decrease. Therefore, when AD and real output decrease, demand-deficient unemployment will increase.

Figure 1

A slowing down of the increase in the LRAS

As mentioned in the previous section, I would fall. However, assuming that the rate of increase in capital is still higher than the rate of depreciation of capital, the stock of capital goods still rises overall, but just increases at a slower rate. Hence LRAS also increases at a slower rate, and so potential growth is reduced and the rate of increase in GPL could still be high, meaning that inflationary pressure is not curbed.

Furthermore, a worsening stock market can cause financial speculators to expect further drops in the future. As a result, there can be a fall in the inflow of hot money into the US as financial speculators expect lower return from their stocks, leading to a lower demand for US$ on the FOREX market, and cause the US$ to depreciate.

Currency depreciation introduces uncertainty for businesses, especially those engaged in international trade or with foreign currencydenominated assets and liabilities. Fluctuating exchange rates can make it challenging for businesses to plan and budget effectively, leading to reduced investment and negative economic growth in the Long run.

Possible effects on the USD

Surprising effect on US Wealth Inequality

Compared to other instances of economic decline, the affected population was mainly the highly wealthy. According to the Federal Reserve, the top 10% of Americans lost over $8 trillion in stock market wealth in 2022, which marked a 22% decline in their stock wealth. Meanwhile, the bottom 50% lost about $70 billion in stock wealth. Although this may seem like a large amount, it is much less than the losses incurred by the wealthy. The very wealthy are more affected by this economic decline because they own an outsized share of stocks. Unlike the rich, Americans with lower wealth are less likely to own substantial amounts of stock. Hence, this resulted in a decrease in the wealth of the rich, and wealth inequality was reduced.

Conclusion

In conclusion, the overall effect of a stock market decline on the economy depends on how severe the stock market decline is. The one that occurred in 2022 was not particularly severe and therefore, the overall effects on the economy were rather muted, compared to the stock market crash in 2020, the year when the Covid pandemic started.

DONE BY:

1. CLARE MARIE LAWRENCE (2T02)

2. NGUYEN NGOC UYEN NHI (2T02)

3. ELIZABETH GRACIE NG (2T22)

4 CLAIRE TAN SHAN QI (2T22)

InflationaryPressure SpursDiverseCentral BankPolicies

By: Amber, Clarise, Tia, Zheqi (2T29), Meredith (2T02)

far as it used to? That's inflation at work, the sneaky thief slowly eroding your purchasing power. While Venezuela's whopping 199.9% inflation rate is an extreme example, inflation impacts everyone, everywhere.

There are two main culprits: demand-pull inflation, and cost-push inflation, forcing businesses to hike prices. Can all countries achieve inflation of 2%?

From interest rate adjustments to supply policy shifts, governments fight to keep inflation under control. Why? As Margaret Thatcher wisely said, "inflation is the parent of unemployment and the unseen robber of those who have saved." It can cripple individuals, businesses, and even governments.

So...

the next time you see prices creeping up, remember: inflation isn't just a number, it's a force with real-world consequences. Let’s take a look at a few examples.

Interestrate/Exchangerate monetarypolicy

Despite aggressive rate hikes, 2022 inflation in the US remained high of 9.1% peak due to supply chain disruptions exacerbated by the Ukraine war. With COVID-19, tightening immigration policy and sustained employment growth also produced a very tight labor market. Hence, the interest rates could n from the supply-side.

VS VS USA USA

ARMENIA ARMENIA

Armenia's economy witnessed a significant resurgence, marked by a robust 12.6% GDP growth, and a high initial inflation rate of 10.75%, it gradually decelerated to 8.1%, a trend likely influenced by adept demand management strategies and the influx of labor. The Armenian dram had a strong appreciation in recent months, with an 18.3% increase against the US dollar by the end of October 2022.

The appreciation makes exports more expensive in terms of foreign currency. This will lead to a fall in demand for our exports. Imports will be cheaper in local currency terms. This will lead to a rise in the quantity demanded of the imports, thus leading to a fall in X and a rise in M. (X-M) will then fall, reducing demand-pull inflation. Furthermore, the influx of Ukrainian refugees has contributed to lower production costs by augmenting the labour supply, increasing short-run aggregate supply and alleviating inflationary pressures.

In conclusion, the US case highlights the limitations of rate hikes against supplyside issues while Armenia's success underscores tackling root causes, proactive risk management, and aligning monetary policy with broader economic goals for lasting stability.

Figure 1: USA’s inflation will continue growing (Winn,2022)

Figure 2: Armenia’s economic growth (Strategeast,2020)

Figure 1: USA’s inflation will continue growing (Winn,2022)

Figure 2: Armenia’s economic growth (Strategeast,2020)

Exchangeratebasedmonetarypolicy

Singapore's 2022 inflation at 6.1% highlighted the delicate dance between import reliance, taking 180% GDP, and exchange rate policies. Appreciating the SGD effectively curbed imported inflation, shifting the SRAS curve downward, but risked harming export competitiveness due to higher foreign currency costs. This trade-off between price stability and potential negative growth and rising unemployment demands careful consideration.

VENEZUELA VENEZUELA

Conclusion:

SINGAPORE SINGAPORE

VS VS

Meanwhile, Venezuela's 2022 experience served as a cautionary tale. Excessive government spending fueled inflation, and fixing the exchange rate eaply import backfired, crippling rts (Assume PEDx > 1). The ? A double whammy of skyrocketing prices and declining export revenue.

Exchange rates are versatile tools for managing inflation. However, effectiveness depends on context. Venezuela's high trade dependence initially made it attractive, but ultimately failed due to external factors, highlighting the crucial role of broader circumstances in ensuring the longevity and success of exchange rate policies for price stability.

7

Figure 3: Singapore’s ongoing inflation (NikkeiAsia,2018)

Figure 4: Venezuela’s high inlfation rate (PilotSevas,2018)

Supply-sidepolicy-marketoriented [Deregulation&labourreforms]

KOREA KOREA

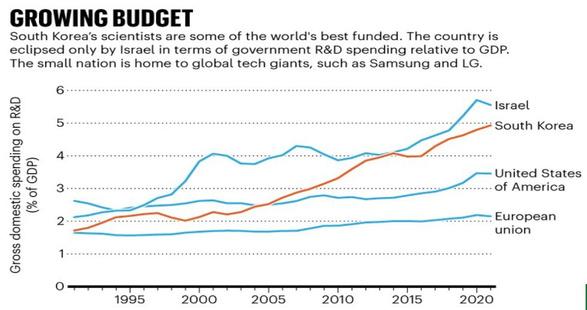

To counter late 2022's stagnation, Korea rolled out deregulation and R&D investments (112 trillion won, up 10.3% from 2021) to boost competition and innovation.

However, pessimistic economic outlook and external pressures raise concerns about long-term effectiveness.

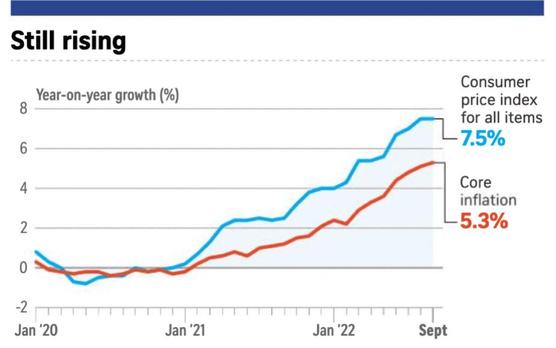

SINGAPORE SINGAPORE

Facing a 2022 inflation surge of 1.8% to 6.1%, Singapore implemented the SGunited Jobs and Skills Package and a $1 billion wage subsidy program. However, workers' receptiveness to training due to program factors and unemployment remains a challenge.

While supply-side policies are crucial, their impact varies. GTCI 2023 ranks Singapore #2 in Asia-Pacific talent competitiveness, making it more receptive than Korea. Effective inflation management requires a comprehensive approach addressing both demand and supply.

Conclusion:

While inflation throws punches, policymakers counter with precise strikes. These policies target different inflation types, but remember, this fight requires strategy, not just brute force.

Figure 5: Comparison of South Korea's R&D Spending with Global Trends (Zastrow,M, 2016)

Figure 6: Singapore’ CPI and core inflation trends (Poems 2022)

https://www.shutterstock.com/image-vector/stock-market-crypto-currency-bitcoin-bubble-1928282264

https://www ellevest com/magazine/investing/inflation-news-explainer-2023

https://fortune com/2024/01/03/federal-reserve-minutes-jerome-powell-cautious-interest-rate-cuts/

https://www.cnbc.com/2022/07/05/hiking-interest-rates-the-wrong-solution-to-inflation-problem-analyst.html

https://tradingeconomics.com/united-states/inflation-cpi

https://interactive-wealth.com/why-usa-inflation-will-keep-growing/

https://www.npr.org/2023/01/26/1151320042/us-economy-recession-inflation- housing-spending-slowdown https://tradingeconomics com/armenia/interestrate#:~:text=The%20benchmark%20interest%20rate%20in,percent%20in %20August%20of%202005

https://www.s-ge.com/sites/default/files/publication/free/economic-report-armenia-eda-2023-10_0.pdf

https://www.strategeast.org/world-bank-forecasts-5-1-growth-for-armenia-in-2020/ https://www.cba.am/Storage/EN/publications/DVQ/Monetary%20overview_II.2022.pdf

https://asia.nikkei.com/Business/Markets/Nikkei-Markets/Singapore-s-core-inflation-stays-at-four-year-high https://images app goo gl/orfpV5p3bsNEpirWA

https://www investopedia com/articles/stocks/09/how-interest-rates-affect-markets.asp

https://www.imf.org/-/media/Files/Publications/CR/2022/English/1KOREA2022001.ashx

https://m.koreatimes.co.kr/pages/article.amp.asp?newsIdx=331155

https://english.hani.co.kr/arti/english edition/e_business/1041268

https://www.mom.gov.sg/newsroom/parliament-questions-and-replies/2022/0912written-answer-to-pq-on-impact-ofinflation-on-workers

https://www nature com/articles/534020a

https://www.poems.com.sg/market-journal/rising-inflation-in-singapore/

References

Host games

VS VS

Don’t Host Games

GAME OF ECONOMICS

By Denise Kareender Jonathan Ethan 2T25

World Cup Location

Welcome to the game of economics where we unravel the economic theories behind the World Cup! Amidst the thrill of this global event, have you ever pondered over the intricate reasons such as the economics behind countries vying to host it? Join us as we delve into the complexities of this game to uncover the economic dynamics driving the World Cup hosting phenomenon. Let the games begin as we explore the economics behind this captivating event!

Introduction

Round 1 ; economic growth

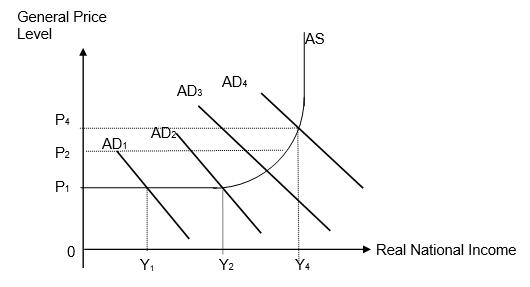

Hosting a major international event like the World Cup creates a surge in demand for tourism services such as accommodation, transportation, food, which causes X to increase , increasing (X-M). Government expenditure (G) would also increase to fund the building of new infrastructure. When 2 components of AD increase, AD curve shifts from AD1 to AD2, ceteris paribus. Assuming the economy has spare capacity, firms will employ more factors of production (FOPs) including labour to increase production, causing an increase in RNY from Y1 to Y2. The increase in RNY from Y1 to Y2 will cause an increase in income-induced consumption , causing further increases in AD. This will trigger successive rounds of increases in RNY and income-induced consumption with each round getting smaller. The multiplier process will end when the increase in RNY is too small to generate further increases in YIC. The autonomous increase in AD from AD1 to AD2 causes a multiplied increase in RNY from Y1 to Y4. Qatar would therefore experience positive actual economic growth. ✅host

However, it depends on the state of the economy. If the economy of Qatar is near full capacity, the increase in AD will result in demand pull inflation. When AD curve shifts right from AD1 to AD2, the increase in AD will create a shortage of goods at the initial GPL P1. Firms in Qatar will thus increase their prices and output. Moreover, since factors of production (FOPs) are scarce, the increase in production will increase the competition for resources which increase factor prices, unit cost of production increase. Thus, the firms will only be willing and able to sell additional units of output at higher prices. This causes the economy to re-equilibrate at a higher GPL. In fact, there was a 5.93% surge in the inflation rate and the consumer price index reached 108.20 points, showing the highest annual jump since September 2022!

❌host

Round 2 ; Price Stability

Round 3 ; Balance of payments

Moreover, the influx of foreigners into Qatar could positively impact the Balance of Payments (BOP). Increased tourism leads to heightened demand for Qatari goods, particularly in sectors such as hospitality, consequently amplifying net exports. Additionally, hosting major events like the Olympics can attract Foreign Direct Investment (FDI) in anticipation of heightened demand for goods and services. Furthermore, the derived demand for Qatar currency in the FOREX will increase, causing it to appreciate. However, since Qatar operates on a fixed exchange rate system, this will result in an under valued currency. The price of exports in foreign currency is now lower, causing an increase in export competitiveness and, thus, an increase in demand for the goods in Qatar, as shown in Figure 3. The price of imports is now more expensive in domestic currency, causing a decrease in the quantity demanded for imports. This would then result in a further increase in net exports (X-M), which could boost the economy since it improves the BOP.

Figure 3 ; Qatar Monthly Exports

✅host

Conclusion

The thrilling conclusion: To Host or Not to Host?

The final tally stands at 1❌ and 2✅! It will serve as a boost to the economy when hosting the World Cup due to there being more benefits than costs. Let's anticipate the World Cup 2026 with excitement, where the games promise to captivate anew!

Credits

https://www goal com/en-sg/news/2022-world-cup-al-janoub-stadium-qatar-inaugurated/fw475bcdsr4t12c26t18whqek

https://www wsj com/articles/world-cup-qatar-culture-clash-alcohol-11668527466

https://www ceicdata com/en/indicator/qatar/trade-balance

Cracking the Covid Code: Inside China's Zero-Covid Policy

Source: www. npr.org

When COVID-19 hit, China’s mass mobilisation of resources and strict lockdowns gained global recognition, a testament to decisive autocratic power. But when Western economies reopened, China maintained its “zero covid” policy. In this article, we explore its impactsthe costs and benefits of “zero”.

What is “Zero Covid?”

The Chinese government recognised having some COVID cases was inevitable, aiming for “dynamic zero” through prevention and containment. Prevention focused on early detection through regular testing. Containment prevented outbreaks through lockdowns, and borders were kept tight.

A Slump in Demand

“Zero Covid” worsened already-weak consumption. Financial, manufacturing, and export centres were shut down, including Shanghai and Guangzhou. China accelerated the closing of foreign-invested firms, like Toshiba and Samsung, leading firms to reduce investment, amidst falling rates of returns and profitability. Service industries including restaurants temporarily closed during the zero-Covid clampdown. Consumers postponed consumption and saved aggressively. The lower consumption and investment expenditure created a fall in China’s AD.

With reference to figure 1, assuming the economy was not operating at full capacity, the fall from AD1 to AD2 resulted in a fall in Real National Income (RNY) from Y1 to Y2. This led to a fall in induced consumption, causing a further fall in AD. This triggered successive rounds of decreases in RNY and induced consumption. At each round, the decrease in both became smaller. The reverse multiplier process ended when the decrease in RNY was too small to generate further decreases in induced consumption. The real national income fell from Y1 to Y5. This explains China’s negative economic growth.

If the rate of depreciation exceeded the rate of increase in capital stock, then the overall quantity of capital may also have fallen, the LRAS would fall and the full employment level of output would be reduced, leading to negative potential growth.

Figure

1

E D I S I 2 0 www reallygreatsite com

Soaring Costs

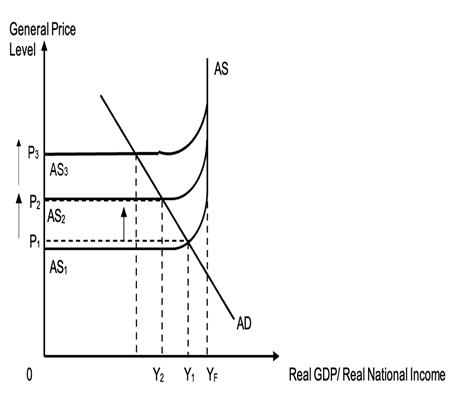

Zero-Covid also increased inflation. China’s overall CPI rose 2.1% in May 2022, as prices of essentials soared. According to Nikkei Asia, “Authorities shut off access to highways to prevent the spread of infections”, and “truck drivers were reportedly reluctant to make deliveries to virus-hit areas, partly to avoid the requirement to isolate at home afterward.” Truck drivers also wanted to be paid more for their deliveries, causing increases in their wages. The rise in wages was not matched by increases in labour productivity, leading to wage-push inflation. Firms’ unit cost of production increased, so they were less willing and able to sell at each level of output. Thus, with reference to figure 2, SRAS decreased from AS1 to AS2. A persistent increase in unit cost of production caused a further decrease in AS from AS2 to AS3. This created a shortage at prevailing GPL levels, resulting in upward pressure on GPL until eliminated at a higher equilibrium GPL, P3. Thus, China experienced cost-push inflation.

As mentioned in the previous section, there was a fall in AD which led to a lower derived demand for factors of production including labour. This led to a rise in demand-deficient unemployment.

Figure 2

Figure 2

Triumph Over Adversity

Of course, there were existing fears and uncertainty about the possibility of recovery, with patients possibly facing ‘‘long-term lung scarring’’ and ‘‘heart damage’’. The “Zero Covid” policy’s tight approach had kept the country largely free from the deadly virus.

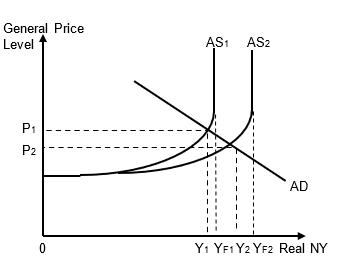

If it were indeed true that contracting the COVID-19 virus would have long-term negative effects on the human body, then the “zero COVID-19” policy would have long-term positive effects on the LRAS. In the long run, health and quality of life would increase, increasing worker productivity. With reference to figure 3, this would expand productive capacity and potential output. LRAS would increase from AS1 to AS2 while full employment of output would increase from YF1 to YF2, and the country would achieve potential economic growth.

Given that so far, there has been no clear data about long term effects of Covid on labour productivity and it was mentioned in the previous section that a fall in FDI will cause LRAS to fall, overall, the Zero-Covid policy is still likely to cause negative potential growth in the long run for China’s economy.

Conclusion

COVID-19 resulted in lower economic growth, a slowdown of new foreign-invested enterprises, and a rise in unemployment. However, prioritising the health of its citizens has boosted China’s potential economic success. Would you have done it differently?

3 GROUP MEMBERS: MAX WEE GWAN SIM (2T06) 1. CHLOE LY KELAART (2T02) 2. LIM JIA YI (2T06) 3. GOH WAN EN (2T25) 4.

Figure