32 minute read

COVER STORY

Future and Fortunes of Grade A Warehousing

Warehousing is a key pillar of any organization’s value chain. In the advanced economies, the warehousing quality & delivery efficiency scaled-up & transitioned due to the combined push from modern industrial growth and advancement of technology. The quality of the warehouse has severe impacts on the movement of goods, on storage and retrieval of materials and achieving sustainability in safe and healthy environment in the warehouse. However, in the developing economies, this scenario is still evolving. Though the principles of warehousing have not changed much over the years, warehousing solutions have evolved a few notches higher especially in the last decade. The major contributors of this change are changing customer dynamics, advancement in technology, demographic changes in demand and supply, and proliferation of e-commerce, just to mention a few. Organizations like Amazon have revolutionized the concept of warehousing from a STORAGE function to FULFILMENT function, contributing significantly to an organization’s efficiency in delighting their customers. All such intriguing insights & more were part of our recently held webinar on the future & fortunes of Grade A Warehousing in India where industry leaders shared and deliberated upon what lies ahead and how solution providers can make the BIG DIFFERENCE in realizing the dream of an organized warehousing segment.

Advertisement

SINCE the global pandemic sent supply chains into a tailspin, delivery delays have affected everything from toilet paper to bicycle parts. Wary of continued disruption, logistics and manufacturing businesses are hunting for larger warehouses, where bigger inventories can provide greater resilience during difficult times. Globally, business demand for larger warehouses is expected to be significantly higher over the next three years, according to JLL’s Future of Global Logistics Real Estate survey, particularly for warehouses between 10,000 to 50,000 sqm. Though demand for more space has prevailed over the past decade, COVID-19 emphasized the need to transform supply chain models. The pandemic has reversed the trend of streamlining inventories, adopting a ‘just-in-case’, rather than the traditional ‘just-in-time’ delivery method.

Big box and mega box (100,000 sqm and over) warehouses are playing crucial role to the supply chain response. Often, they are complemented with smaller suburban delivery stations, a model referred to as ‘hub & spoke’.

While this was an evident global scenario, back home too the scenario is pretty much the same with the warehousing stock in India expected to touch 380 million sqft by 2024, due to increased logistics and storage requirements particularly in urban settings. The covid-19 pandemic has caused a paradigm shift in consumer behaviour from offline to online shopping, leading to an increased activity in sectors like e-commerce and thirdparty logistics. About 27 million sqft of warehousing stock was added during the January-September period, bringing the total stock to 265 million sqft in the year 2021. The total stock of Grade A and B warehousing space in the top 8 cities increased at CAGR 16% from 2018 to September 2021.

India has a per capita warehousing stock of just 0.02 sqm compared to the USA, China and the United Kingdom that have 4.4 sqm, 0.8 sqm and 1.09 sqm respectively. Even in terms of transaction volumes, USA's industrial and warehousing market saw 20.4 mn sqm (220 mn sq ft) transacted during 2020, 7 times that of India in FY 2021.

The story of modern Indian warehousing is a little over a decade old when logistics companies such as Future Value chain built the first Grade A warehouses in the country. The entry of institutions, lured by the vast opportunity presented by a growing economy with a consumption base of over 1.3 bn people, made the Indian warehousing market a compelling investment proposition. The introduction of the GST and the prolific growth seen in the e-commerce and 3PL sectors caused warehousing demand to grow at a CAGR of 44% in the FY 2017 - 2020 period. While the pandemic in FY 2021 has caused demand to drop during the year, the longer-term demand potential for warehousing properties continues to remain strong.

According to a recent Knight Frank report, while transaction volumes were subdued in FY 2021, occupiers showed a marked preference for Grade A properties as they are much better geared toward tackling exigencies such as those posed by the pandemic. The inherent operational efficiencies, adherence to safety standards and better contingency planning because of greater expertise of personnel due to higher institutional participation are some of the factors that drew occupier interest even during the challenging environment of FY 2021. E-commerce players have always coveted the value additions that Grade A properties bring into their supply chain operations and the increase in their share of total transaction volumes also had a significant role to play in the increased take-up seen in Grade A properties. Around 64% of the area transacted during FY 2021 was located in Grade A properties. Except for Bengaluru and Ahmedabad, more than half the area

transacted in all the top markets occurred in Grade A properties.

The development of Grade A warehousing facilities has been increasing in recent years, currently constituting 35% of the total stock compared to 34% in FY 2020. The larger warehousing markets of Mumbai and NCR have a significantly lower proportion of Grade A warehouses as they are much older markets and a bulk of their stock had been built before the demand for Grade A warehousing gathered momentum. Pune and Chennai have the highest concentration of Grade A stock due to their primary demand base of auto and auto ancillary occupiers. Notably, Mumbai, NCR, Bengaluru, and Ahmedabad have more than a 50% share of Grade B properties. Interestingly, despite having a high proportion (82%) of Grade B stock, the fact that Mumbai still enjoys market level occupancy of close to 87% underscores the strength of the market and need for quality supply.

Vacancy in Grade A properties is significantly less than the total vacancy for the eight primary markets under coverage. In fact, Grade A vacancy has also reduced or stayed the same YoY for all markets except Ahmedabad which saw a significant speculative development during FY 2021.

Growth in supply of Grade A spaces over the years is due to high demand for spaces with high specifications, citing increased inclination for high-grade structures and introduction of new players in the market. The Indian market has now firmly established itself for a more predominant position in Grade A space as opposed to Grade B spaces. Net absorption was hit in 2020 due to the pandemic but started recovering in 2021 especially for Grade A spaces – from 56% last year to 73% in this year. JLL said this shift is due to the high demand for quality spaces complying with covid-19 norms. Of the total absorption till the September quarter, more than half the share is taken up by third-party logistics and e-commerce (55%).

More than $6.5 bn have been committed by private equity players in the warehousing market since the GST reforms were applied in 2017. However, the relative dearth of supply of high quality warehousing facilities that conforms to contemporary compliance norms, continues to be a challenge. The availability of suitable land is the biggest impediment in creating supply as lands with clear title continue to be scarce and digitisation of land records which can address this issue is still a long way from becoming a reality. Bhiwandi and the Nashik Highway in the Mumbai market are a case in point where there is very strong occupier demand but issues with land titling curtail institutional interest. Additionally, persistently high land prices and the complexity and time taken for acquiring regulatory approvals continue to impact the viability of warehouse projects and are significant impediments in creating warehousing capacity.

It is estimated that the e-commerce sector will consume the most space in the next five year block of FY 2022 – 2026 at 9.1 mn sqm (98 mn sqft), 165% more than the preceding period of FY 2017 – 2021. Similarly, 3PL and Other Sector companies are expected to take up 56% and 43% more space in the next five years compared to the preceding period. These three occupier groups are expected to account for 86% of the total transacted space in the next five years compared to 78% of the transacted space earlier.

Market traction was seen improving toward the end of FY 2021 as vaccine availability improved and occupiers looked to revive expansion plans. However, the second wave of COVID-19 infections in FY 2021 slowed the momentum again. Occupier activity in FY 2022 will clearly be dictated by the intensity of the pandemic and should regain lost momentum as vaccine deployment improves and restores normalcy to economic activity. The Indian Government's focus on manufacturing with the Make in India initiative and Production Linked Incentive (PLI) scheme among others, and with India being among the possible beneficiaries of global companies looking to disperse manufacturing capacity from China across Asia, should enable warehousing demand from other sectors to grow at a CAGR of 16% in the next five years compared to 15% in the preceding period.

Sanjay Desai, Co-founder & Regional Director, Humana International (S) Pte. Ltd.

What is Grade A Warehouse? Can you briefly cover few technical details? Grade-A warehouses are facilities, which offer efficient operations to organizations in a synchronized manner regardless of customers or industry segments. These facilities are designed for additional height and better floor quality. Innovative materials handling equipment can be used as the flooring allows for such implementation. Better time management is achieved due to provision of better loading & unloading docks with wider dock aprons. Overall, a planned and systematic infrastructure

ensures a compliant and safe and secure movement of men and materials. In most cases, the true, technical design and basic specs for Grade-A warehouses are standardized, major ones are identified below… • Minimum height at an eave of 11m, • The building aspect ratio of a Grade-A

Park would range from 1:1.5-1:3. • The number of docks in such a park is 1 in 10000 SF on plinth area or lesser • The warehouse flooring is at a level of FM2 with a minimum floor load (UDL) of 5T/SQM. • An apron length of a minimum of 25.5 m in concrete • Support movement of 40 FT trailers including internal roads will support such trailers • The number of lanes in total should be 2-4, depending on the size of the warehouse • Amenities (i.e.) fire-fighting systems, CCTV surveillance, building insulations, LED lights, security system, Fire alarm and

Sprinkler system will be part of this infrastructure • An adequate number of entry / exit gates and parking slots based on traffic study

Which factors are responsible to drive this growth in Grade A warehousing demand in India? There are several factors that are responsible for driving the shift in demand from Grade B and Grade C warehouses to Grade-A Warehouse. Primary factors responsible to drive this demand growth are customer expectations on the last mile delivery, the scale & complexity in fulfilment operations, EHS of employees housed in the facility, advancing compliance scenario and lastly proliferation e-commerce. For any large, emerging e-commerce, modern retail or food grocery business, the scale and complexity will assume greater importance in the next 2-3 years. These few factors alone are crucial to increase the demand of using Grade-A warehouses in India and a cardinal shift from C & B Grade to A Grade Warehousing.

What is the scenario in India with reference to demand supply of Grade A warehousing?

In general, it can be said at 30,000 feet, that it is a combined play with real estate availability and strategic thinking ability of an organization. It is estimated that India's current quality Grade A warehousing stock in top eight cities (ONLY) will be close to 180~190 mn sqft, which is expected to grow to 250 mn sqft by year 2024. This spurt in demand has led to real estate prices as well as rentals on escalated path in regions like Maharashtra and Bengaluru. The demand for quality warehouses is far outstripping supply at the moment. While new warehouses are coming online every month, the supply scenario is not going to change anytime soon. According to industry watchers, it could take nearly two-three years for the market to be flooded with enough 'Grade A' warehouses.

India has 504 million active internet users, of which 50% (230 mn) are based in rural areas. What this means is companies need to develop an efficient backend supply chain / fulfilment infrastructure in rural or tier II / III cities in the next couple of years, very similar to the one that is available in urban India. For example, mall cities like Coimbatore, Ambala, Siliguri, Visakhapatnam, Kochi, Indore, Jaipur, Vijayawada, Nagpur, Guwahati are projected to emerge as warehousing clusters.

Added to this is the ‘Make in India’ – manufacturing initiatives hasten their scale; tier II and III cities will see emergence of smaller / nodular warehousing clusters. Presence in more locations for warehousing gives them the flexibility to create value chains, which will ensure higher productivity, optimized operations and a seamless supply chain network that will work like clockwork. Finally, with the various initiatives taken by the Indian Government, the warehousing and logistics sector is now steadily marching towards growth. Granting infrastructure status to the logistics industry along with GST, National Logistics Policy have created a favourable regulatory ecosystem.

What is the value that Grade A Warehousing brings to the table in the value chain? There are huge opportunities for Grade A Warehousing in India given the growth that we will see in next 3-4 years across many industry segments. Companies are looking at warehouses with international standards, which ensure efficient operations of the supply chain and a lower Total Cost of Ownership. Grade A warehouses offer tangible benefits such as 50% additional floor-load capacity, 40% more operational efficiency, efficient material handling space, safety & security of employees and adherence to international standard compliance. Companies can align their operational requirements to warehouse availability, while also having flexibility as they build a robust supply chain.

Is there a role for e-commerce in this shift? In a recent survey, KPMG India mentioned that the “Online” market in India is close to US$20 bn in transactions value. COVID pushed Indian population off-the-cliff and forced them to embrace new ordering patterns using increased internet enabled platforms. Customer satisfaction is critical and a key differentiator when ordering via online platform. Most online customers are reluctant to reorder in case there was a problem with their last order. e-commerce platforms will become increasingly demanding of their logistics supplier in an increasingly competitive landscape. It is important to establish a new ecosystem to address three interconnected components: out of town storage, smaller advanced stock locations nearer the city centre and intracity last mile delivery. Supply chain organizations need to integrate a more sustainable long-term approach from order to customer delivery bringing together all the elements required to develop a coordinated end-to-end customer delivery system.

What is a Grade A warehouse? How is Logos aiming to transform the landscape? It is a simple but a complex question because the devil is always in the detail. In Grade A, we look at it in two components (1) functional and then (2) Estate level (external development and infrastructure) provisions, which we aptly call “beyond the building” at Logos. There are two facets on what transpires in the Indian market – one is what we perceive as Grade A and the other is what is actually Grade A. Perceived Grade A warehouse is regulatory compliant, adequate floor loading and fire protection system and suitable docking and road access for serviceability of that facility.

From a global perspective, grade A strictly adheres to regulatory compliance, the performance characteristics of warehouse facilities being building height, floor quality, docking depth and internal road width are consistently upheld and defined in the market as Grade A parameters. Materiality selection, quality of construction and Estate level design are further defining quality parameters distinguishing the standard of Grade A warehousing.

Grade A is upgrading with the advancement in water and energy management, greater feasibility of battery technology will enable renewable power generation during the day extend to night usage. The provision of electrical vehicle charging stations is becoming standardized, this will further evolve as cars, trucks etc., convert to EV. Water treatment, recycle and capture are enhancing sustainability parameters. Safety in design in both the construction (methodology used to build the facility) and in operation for users and employees at the Industrial Estate has vastly improved, ensuring segregation of people and vehicles. Monitoring platforms at an Estate level provide live tracking and feedback on aspects such a vehicle movement and mapping, temperature monitoring, energy and water usage enabling live performance monitoring of the Estate. This further enables evaluative analysis of the effectiveness of initial design and planning parameters, and to derive learnings to factor into the design for future industrial Estates.

In a competitive landscape park level amenity such as landscape, illumination and transportation facilities or provision creates an environment that people enjoy working in or “want” to work in which is important when warehouses require high amounts of staff. Considered landscaping further counteracts ‘heat island effect’ which is a direct effect from largescale industrial development. Logos has adopted the ‘Miyawaki Plantation Scheme’, which adopts the methodology of the maximum efficiency of tree plantation in a given area, we have further devoted a higher apportionment to green space.

What are the peculiarities between warehouses in the western countries vs. warehouses in Asia?

The defining differentiators constitute: • Regulatory compliance and adherence, James Anderson, Head of Development, Logos India

• Extent of automation, • Specification, • Quality.

Singapore & Hongkong have the best entrepôt trading. India is not a very strong entrepôt trading country. Can this be the reason for the lack of Grade A warehouses in the country? I don’t think India has promoted its ports in Chennai or Kochi well enough, the Government could further support the development of infrastructure to enhance port facilities. Singapore and Hong Kong geographically very well located with strong regulatory enforcement, which derived the benchmark for Grade A warehousing to be defined far earlier. Coupled with a limitation on land availability, buoyant demand has enhanced the level of technology and quality of development being produced in these entrepot trading posts.

Don’t you think it is the right time for the companies and the government to invest in Grade A warehouses? Absolutely it’s the right time. There is such a need for Grade A warehouses with an inherent undersupply and the demand of the huge and growing Indian market. Anomalies associated with land acquisition make it difficult to develop Grade A warehousing at the required speed which the market needs, henceforth demand will remain robust over the next decade.

Grade-A warehousing, quality and time would be the major contributors. What technological changes would be likely in coming years? Speed of execution and shortening this timeline for the construction of a warehouse is critical for a developer while maintaining fundamental performance standards of safety and quality. Coupled with a push towards sustainability and waste minimization offsite prefabrication and “assembly” at the construction site enables achievement of all these facets.

The pre-engineered building process for warehousing is highly efficient as the above ground structure is made entirely offsite and assembled at the site. Contrastingly precast concrete can produce the same for the below ground structure “substructure” i.e., footings/ pedestals, plinth beams, etc., and further superstructure (above ground) components of walls panels etc., enabling most of the building to be fabricated offsite under controlled conditions and arrive in site as a ‘plug and play’ solution. This reduces construction timelines significantly as materials are fabricated in parallel, improves quality, minimizes waste, and inherently makes the site safer taking activities offsite into controlled environments and reducing workforce numbers. Precast concrete and further developing material advancements will evolve that will continue to improve both functionality and durability of warehouses.

Hemaraju Vasanthakumar, Leader, Udaan

As a user, is there a real advantage in using Grade A warehouse? How do you weigh the cost component while selecting a grade A warehouse? Grade A warehousing holds promise from an end user viewpoint. In India, the way warehousing has grown in the last two decades, people earlier never understood the real meaning and importance of a warehouse. In the early 2000, the first warehousing revolution happened where the cube utilization came into picture. That was the time when PEB vendors started coming to India and set up their bases. As an end user, it’s a trade-off because ultimately most of the facilities are leased. When it is leased, the developer always looks for optimizing his profits while as an end user, I will try to optimize my throughput per square feet. One can have low cost of construction and bad quality of building, and you

can get it at cheaper rent, but it will have long-term negative implications – be it maintenance issue with respect to floor, roof, availability of the adequate apron space, truck manoeuvrability, etc. Thanks to institutional players, last 5-6 years have set the ball rolling for organized warehousing in the country as the new age players understand the market demands. They bring global best practices and as the country readies itself for the global players to set shops, they need to have warehouses which are compliant with the global benchmarks. An ideal warehouse should always aim at reducing truck turnaround time, which ultimately results in better throughput as same dock can churn more trucks from the same dock door. Developers also need to address the ideal plinth height. Building interior should have good column spacing of 16 x 24 m. The most important thing that everyone neglects is the right flooring. Flooring is the heart of warehouse, and it can’t be changed throughout the life cycle of a warehouse. The quality of the floor and the roof must be so high that it can withstand any wear & tear for at least over 50 years. There are constant material handling equipment working round the clock in the modern warehouse. Equipment performance depends on the quality of the floor. Unfortunately, in India, we don’t have set standards for warehouse flooring. Hence, we have borrowed it from Europeans.

In warehouses and logistics buildings, the concrete slab and flooring are critical to the effective functioning of the operations. However, it is often the perception that the concrete floor is one of the most straight forward elements of the project, and many times the overall attention paid to design and construction detail is less than proportional to its ultimate importance in the efficient

operation of the facility. To ensure that the concrete floor will continue to carry its design loading successfully, it is vital to design and construct the subgrade as carefully as the floor itself. Pressures exerted on the subgrade due to loading are usually low because of the rigidity of concrete floor slabs and loads from forklifts wheels or high rack legs are spread over large areas. However, subgrade support must be reasonably compacted to 95% proctor density which can be confirmed by plate load test.

Is this view specific to any industry such as e-commerce or FMCG? The requirement of such advanced and sustainable warehouse is paramount across the industry. If you look at the e-commerce industry, automation is quite prevalent there. In that case, quality of the floor or levelling is not that important, whereas for FMCG players or other manufacturers, quality of floor is extremely important because they use pallet trucks. The moment they start using industrial pallet trucks of 17m height, quality of floor becomes crucial. Otherwise, throughout the life of the warehouse, occupiers of the warehouse suffer due to suboptimal quality. That’s the reason we have to educate investors who are getting into warehousing as a developer. They need to build warehouses as per special industrial needs. What used to be the scenario two decades back has completely transformed today and we need to move ahead and not behind if we want to be in the race to survive and sustain our market share. What impact do you envisage on the quality of warehousing? Are there any benchmarks that companies follow? It’s not only e-commerce, though it has today become the key driver. Quality of warehousing is extremely important because time is money in e-commerce, now-a-days people are talking about 15-minutes delivery. If that’s the kind of demand that are intending to generate, it all boils down to the throughput. If companies want to achieve such a decisive initiative, then everyone in the supply chain right from the warehouse to middlemen to the retail fronts need to have fantastic facilities that can churn out products faster without any hiccups. I would like to draw your attention to one of the most striking aspects of a warehouse in India – have you ever realized that the warehouses in India today are getting airconditioned. What does this entail? Unless you have the right infrastructure in place, you can’t achieve your set objective and not only this, but it also percolates down the value chain and hamper the product availability in the market and the loss of equity for the company. Additionally, the right warehouse also helps in reducing wastages and the maintenance cost and deploy capital where it’s needed to get the right equilibrium.

Udaan is an e-commerce company. We are strong supply chain technology driven company. Our growth depends on the rural market penetration. The rural penetration is growing at the lightning speed. With 5G coming into picture, the penetration will see a further boost. Our main business line is grocery. It is estimated that in 5 years’ time, it will be US$1 trillion business in India. At Udaan, our target is to achieve 10% share of such burgeoning market. We are targeting US$100 billion business in the next 5 years. We will see traditional players move to e-commerce, all thanks to COVID-19 pandemic.

Does asset-light model have any impact on Grade A warehouse in India? Asset-light model may not be suitable for everyone in the industry. For the start-ups, this is fantastic model because it is light on the Capex. Though there are players for the past 15-18 years in this field, it has not picked up so much. Having said that, there is a demand and there are service providers. The problem in India is that when the equipment is taken on hire, the developer always looks in for a minimum lock-in period. Otherwise, he looks out to write-off all his investments in 5 years’ time. Though the life of MHE is at least 10 years, the developer wants the quick RoI, which implies that the cost of rental per month could be higher, making it unaffordable for the player in the long run. That’s why initially people start with the rental model, once their strategies are clear and have accumulated funds, then they move to Capex model. Today there is a whole gamut of refurbished MHE available on rent, which are either imported or manufactured in the country.

Chandranath Dey, Head - Operations, Business Development, Industrial Consulting & PAGI India, JLL

Warehousing is among the most resilient real estate asset class in India and is likely to bounce back soon once the pandemic is over.

Is there a desired build quality that can withstand wear & tear? Are there any standards that we must adhere to? Warehousing is on a three-dimensional growth path. The three dimensions are length, breadth, and height. In terms of length, growth across the length of the city – suburban to urban. In terms of breadth – growth across the breadth of the nation from Tier I to Tier II & III cities. In terms of height, it is the increasing importance of mezzanine floors in warehouses and development of multi-storey warehousing facilities.

Over the last 10 – 15 years, India has evolved from going-down era or 'Go-down Era' to modern ‘Grade-A Era’ in warehousing. While the standards are not actually laid out by the governing authorities, the warehousing fraternity including users have been working on creating all-encompassing standards, which are not only quality-intensive but are also forward looking and sustainable in the long run. The warehousing who’s who have come together and prepared a very practical Good Warehousing Practices (GWP) document that serves as the ready-reckoner for the new players in the industry.

Grade A building or PEB structure has a lifespan of 50 years. During the course of this time, gauging the wear & tear such buildings is a crucial aspect. The National Logistics Policy draft, once it comes into fruition, will expected to streamline the warehousing operations in the country and might concretize such operational nitty-gritties as we move along. The good part is that the users are also well aware of the changing warehousing paradigms and are pushing service providers to offer them such new-age propositions which prove to be highly effective in the long run.

At JLL, we are honoured to be able to provide inputs to the Department of Logistics in harmonizing the various logistics aspects including standardizations in logistics parameters and warehousing in due consultation with the industry players on various topics including but not limited to FSI norms, Master Planning Area Distribution for Logistic parks with area more than ~ 15 acres.

Use Warehouse Building Utility (Roads, common infrastructure, circulation, open space, truck apron area, excl. parking) Dedicated Truck Parking Area Share (%) 50%

20% - 35%

Min 15%

Source: JLL Logistics & Industrial

GOOD TO HAVE FACILITIES/ AMENITIES (PARK LEVEL FACILITY) AS CHOICE OF VALUE-ADDED SERVICE (OPTIONAL)

• Additional benefits to developers for green rating of Warehouse (e.g.:

Rooftop Solar PV Panels, Rainwater

Harvesting, EV Charging Station, etc.) • Benefits for additional amenities such as conference room, food court/ refreshment joint/ cafeteria, display area/ experience center for product,

ATMs, Billboard panel (provision for additional revenue collection source), retiring rooms, creche/ playrooms/ baby care rooms, etc.

Logistics and industrial park developers are finding it difficult to make financial sense in such developments with the rising cost of construction and thinning rentals. Additionally, what would help is any favourable structural / policy level change would help developers navigate two primary constraints i.e.

‘DOUBLE A’ CONSTRAINTS FOR DEVELOPERS / INVESTORS;

• Acquisition: Hurdles in land acquisition • Approvals: Hurdles and delays in statutory approvals.

While the government has taken several corrective measures in recent times like National Single Window System, ‘PM GatiShakti’, etc., which is expected to make some positive changes, the perfect world is still a distant cry.

How will changing market dynamics be having a significant impact on the growth of Grade A warehousing in India? E-commerce and GST implementations are two good reasons to catapult warehousing industry in the country. Warehousing will be closer to the customers with supply chain being the king of the value chain. We are seeing significant upward trends in warehousing activities in tier I and tier-II cities.

India is growing its portfolio of world-class Grade A warehouses in the past 4-6 yeas. A correlation with the global markets shows the potential of growth is even higher. If we compare the warehousing stock of USA, we are talking about a total stock in excess of 13 billion sqft. Chicago as a city has 1.2 billion sqft of warehousing supply. It implies that the potential of warehousing in India is humungous.

On the demand / absorption side, absorption in Top 8 cities is expected to have a ‘V-Shaped recovery post COVID. What’s important is that this pandemic

Source: JLL Logistics & Industrial

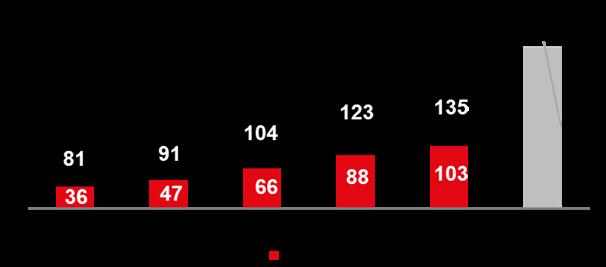

has pushed the demand of Grade A even more as it offers a platform for technology implementation that can reduce human intervention. There has been a quantum leap in demand for Grade-A space over Grade-B over the years from 42% in 2016 to almost close to 73% in favour of Grade A warehousing in the last year till 2021 Q3 (i.e. Jan-Sep 2021), It is expected to further grow as occupiers look for spaces with higher specification as per requirements. The liquidity infused by global investors is prompting the market to move towards organized and globally accepted warehousing space. We expect technology to be one of the most important aspects to optimize and bring in the much needed efficiency enhancement inside the warehouse operations.

Is there a possibility to have mini grade A warehousing facility? The economics of scale doesn’t fit in when you try to develop some 4k-5k sqft warehouses vis-à-vis mega warehouses. In order to achieve the efficiency level of Grade A warehouses, one needs to have scalability intact.

How would you like to compare Grade A and Grade B warehouses in terms of returns to users / tenants? A JLL Industrial research on comparing Grade-A & Grade-B warehousing cost to end users/occupiers reveals the following:

While the above comparison shows that while Grade A might have a rental premium on the space, , but when comes to rent per pallet it is ~50% cheaper than Grade B warehouses. Additionally, there are several other tangible and intangible benefits that Grade-A warehouses bring over Grade B in a platter; • Better infrastructure to increase operational efficiency by mechanization & automation • Better fire detection & prevention systems in the warehouses also bringing down the insurance cost • More safety to the goods in the warehouses • Cleaner, cooler, and hygienic environment to people handling operations in Grade A warehouses. • Better out-side the box facilities like truck parking areas and truck manoeuvrability

How do you see growth of warehousing in Tier 2 cities in India? GST implementations and ever increasing consumer demand in tier 2 cities are taking warehouses in such

GRADE A VS. GRADE B BENEFITS TO USERS:

Details / Assumptions Grade A Grade B Height of warehouse (Mts) 13 8 Floor Strength (Tons/sqm) 6 3 Actual Storage space / Total Area 65% 75% Assumed Rentals (INR / sft / month) 20 15 *Rent / pallet positions (INR / month) 57 87

Source: JLL Logistics & Industrial (*Note: Taking into consideration several assumptions on racking, cargo churnings etc.) locations. If we leave out the 8 top Tier 1 cities (NCR Delhi, Mumbai, Chennai, Kolkata, Bengaluru, Pune, Hyderabad & Ahmedabad), at JLL, we are experiencing strong demand in tier 2 cities with increasing sizes in nearly 30 cities in the country. A few cities that stand out include; • North India – Rajpura- Chandigarh,

Jaipur, Lucknow • East India - Patna, Guwahati • West India - Indore, Nagpur, Surat • South India - Vijayawada, Coimbatore,

Kochi

This is probably the inflection point in tier II cities in India to develop Grade A warehouses as most of the requirements for Built-to-Suit (BTS) warehouses are GWP complaint / FM Global complaint.

What are the key trends in warehousing in India?

Some trends in warehousing in India

are: E-commerce is going In-City: Faster last mile delivery focus of e-commerce boosts the in-city / urban logistics sector, where conventional retail spaces, workshop sheds, banquets, marriage halls are being considered for alternative usage for in-city warehousing across top cities. As per

JLL estimates, there is a demand in excess of 7 mn. sqft demand from top players in tier 1 & 2 cities in next 2 years. Developers are exploring investments in

Multi-storied / In-city WH: To cater to urban logistics requirements and

Point of Delivery (POD), dark stores, etc. No major success stories yet. Rise of third-party logistics: Outsourcing of logistics is being evaluated by many companies to achieve better efficiency in logistics. Automation is now considered a ‘Good

Cost’: The cost of automation in warehousing is gradually coming down due to technological advancements and most users are considering automation as a ‘good cost’ to incur that can yield long term benefits Warehousing box sizes are growing:

Average sizes of warehousing boxes have come a long way from 25K – 50K sqft, 3-5 year back, now hovers ~ 100K sqft + for Grade A spaces.

Low rental and higher construction cost are compressing developer returns. High steel price and other commodities have increased construction cost up 20% - 30%. On the other hand, 5 years, CAGR of rental growth is around 3.5% per annum. This is unsustainable in long term, upward correction is expected in medium to long term for equilibrium. Large players are taking long-term positions: For very large boxes in hub locations, e-commerce, 3PL are even buying land from government / private and building their own WH.

In such warehouses, tenants are spending heavily in automation, AS/

RS, VNA, etc. Palettized cold storage demand on the rise: Frozen is the New Fresh.

Temperature Controlled storage

requirements are gaining with consumers looking for ‘hygienic and safer’ frozen commodities. While the demand is floating high, but prices / rentals doesn’t tally for a good investor return for development of such spaces. Manufacturing is going asset light:

Manufacturing firms, especially in the ancillary and assembly space, are finding solace in built manufacturing spaces on lease. Manufacturers are positioned to realize the benefits of conversion of CAPEX (land & building) to OPEX (rent), ready-tooccupy and built-to-suit industrial spaces, higher specifications, faster entry, and pre-approved usage associated with built spaces. JLL estimates show close to 12 mn. sqft. of manufacturing leases in top cities. Early days of Multi-modal logistics in e-commerce: Multi-modal Logistics

Parks are having a real capacity to bring down the logistics cost as it relies on rail for long haul transportation which can bring down the transportation cost significantly.

Some e-commerce companies are now seen to go for such rail & road linked logistics facilities to reap the benefits in the long run.