P ub LISH er Century 21 Australia Pty Ltd CONT r I bu TO r S Chris Gray CoreLogic Realestate.com.au

Century 21 Australia (02) 8295 0600

er TISING e NQ u I r I e S

Century 21 Australia (02) 8295 0600

DISCL a IM er

We have in preparing this information used our best endeavours to ensure that the information contained therein is true and accurate, but accept no responsibility and disclaim all liability in respect of any errors, inaccuracies or misstatements contained herein. Prospective buyers and sellers should make their own enquiries to verify the information contained herein. All information contained in the CENTURY 21 Australia Pty Ltd website is provided as a convenience to clients. All links to property prices displayed on the website are current at the time of issue, but may change at any time and are subject to availability.

For more information on our Privacy Policy please refer to: www.century21.com.au/privacy

N aTION a L HOM e

Va L ue S HOLD ST ea Dy aS re GION a L au ST ra LI a P u SH e S TO N e W re CO r D HIGHS

National dwelling values were steady in January (-0.03%) with the headline result weighed down by the capital cities, where values fell 0.2%.

Dwelling values across the combined regional areas of Australia rose a further 0.4% in January, reaching new record highs.

Three of the eight capitals recorded a decline in home values in January, with Melbourne recording the sharpest decline (-0.6%), followed by the ACT (-0.5%) and Sydney (-0.4%). Hobart home values were steady in January.

Brisbane and Perth have continued to record growth in home values, but there has been a clear and steady loss of momentum in these markets, especially in the detached housing sector where value growth has eased more noticeably.

“Perth is now recording a slower rate of growth than Brisbane and Adelaide over the rolling quarter,” said CoreLogic's research director,

Tim Lawless. “In the June quarter of 2024, growth in Perth home values was 7.1%, easing back to just 1.0% growth in the three months to January.”

Adelaide has shown a more resilient trend, although the pace of gains is slowing, value growth has led the capitals over the past six months with a 4.8% gain.

Annual growth in national home values has more than halved since moving through a cyclical peak over the 12 months ending February 2024 (9.7%), slowing to 4.3% in January. Melbourne (-3.3%), ACT (-0.5%) and Hobart (-0.4%) are all recording annual declines in home values, while Sydney (1.7%) is recording the lowest annual gain since June 2023. Regional Victoria was the only broad rest of state region where values have declined over the past 12 months, down -2.6%.

Regional housing markets have also shown a slowing trend in value growth, however, the aggregate ‘combined regionals’ index has been recording a stronger monthly

growth trend relative to the capitals through most of 2024 and now into 2025.

“Regional markets seem to be benefiting from a second wind of internal migration, along with an affordability advantage in some markets, and what looks to be some permanency in hybrid working arrangements across some occupations and industries,” Mr Lawless said.

Late last year, ABS reporting on working arrangements revealed 36.3% of employed people usually worked from home, which was down from COVID-highs, but still above the 32.1% reported in 2019.

A shallow downturn? Factoring in the downward revision to previous months, CoreLogic’s national Home Value Index (HVI) is now down -0.3% from the record highs recorded in October last year. However, with the first rate cut likely to be imminent, alongside improving consumer sentiment, we could see some renewed support for housing prices over the coming months.

“Lower mortgage rates and a subsequent lift in borrowing capacity as well as an under supply of newly built housing could be setting the foundations for a relatively shallow housing downturn,” Mr Lawless said.

“But the easing cycle for interest rates is likely to be a gradual one, and we also have the ongoing headwinds of affordability constraints, normalising population growth and generally soft economic conditions to contend with.

All things considered, the likelihood of a significant growth cycle over the coming year remains low.”

Easing turnover alongside slowing value growth. In other signs of a slowdown, the national volume of home sales also appears to have passed its peak. Annual sales moved through a cyclical high at just under 535,000 in the year to October and have since eased to 526,000 over the year to January.

W H y Wa ITING CO u LD COST yO u

BY CHRIS GRAY, CEO, YOUR EMPIRE

As we kick off a new year, there’s been a lot of noise in the property market about interest rates and this week we had our first 0.25% drop.

This should have a significant impact on the market - not just financially, but emotionally as well.

A lower cash rate means cheaper monthly mortgage repayments, making property more affordable. It also increases buyers' borrowing power - meaning the same repayment could now service a larger loan. But beyond these

practical benefits, the biggest shift will be in consumer sentiment.

For years, I believed that property investors, being more analytical than homebuyers, would react logically to market conditions. But over the past 20 years, I’ve seen quite the opposite. Emotions drive markets far more than people like to admit.

THE PSYCHOLOGY OF PROPERTY BUYERS

Most people believe they make rational financial decisions. In reality, they follow the crowd. We saw this play out during the Global Financial Crisis, the

credit crunch, the Royal Banking Commission, and most recently, COVID-19.

Each of these events created uncertainty, and buyers hesitated. Yet, those periods turned out to be some of the best times in history to buy property. Why? Because competition was low, meaning prices were more lower, and long-term growth opportunities were huge.

But instead of seizing the moment, most people sat on the sidelines, waiting for a sign that “things were improving.” By the time they felt confident enough to act, the best deals were long gone, everyone jumped in together and it was even harder to buy.

FEAR VS. OPPORTUNITY: WHAT HISTORY HAS TAUGHT US

When interest rates were at record lows, buyers had a golden opportunity. Yet many didn’t take action. Instead, they kept waiting - perhaps for even lower rates, perhaps for someone to tell them it was the “right” time.

Then, rates climbed, doubling or even tripling. Suddenly,

buyers who could have comfortably afforded a property were priced out. Their borrowing capacity dropped by 30-40%, and what could have been a $1m purchase turned into a $600K or $700K ceiling.

Fast-forward to today: we’re potentially at the start of the next major shift in the market. Consumer confidence is likely to rise with a rate cut, and once that happens, demand will increase. Buyers who wait too long will find themselves competing again - just like they did in past cycles.

THE bEST TIME TO bUY?

bEFORE EVERYONE ELSE DOES The market doesn’t wait for people to feel comfortable. It moves ahead while they hesitate. Some of the best purchases I’ve made were during periods of uncertainty -when most people were too afraid to act.

Half of my current portfolio was purchased during the Global Financial Crisis, a time when the media was predicting disaster and many people were convinced property would never recover.

In hindsight, would you have bought a two-bedroom apartment in Coogee or Bondi for $600K – $700K in 2009? Of course you would.

That’s the power of making decisions before the crowd catches on.

THE RIGHT TIME IS ALWAYS NOW —IF YOU bUY THE RIGHT PROPERTY

If you’ve been waiting for a sign, this is it. Whether we get another rate drop in April, May or later this year, it doesn’t really matter. What matters is buying the right property in the right location at the right price.

SQM Research predicted late last year that Sydney might drop between 1% and 5% based on certain scenarios. After the rate drop on Tuesday it revised it’s predictions for Sydney to rise by 3% to 7%.

Markets move in cycles, and those who hesitate during uncertainty end up paying a premium later. The best opportunities don’t come when the headlines are positive and everyone

feels good. They come when smart investors or homebuyers step in while others sit on the sidelines.

So, ask yourself: Are you going to wait for things to be “perfect,” or are you going to act before the next wave of competition pushes prices higher?

Because in 10 years, you don’t want to be looking back at 2025, saying, "I should have bought when I had the chance."

A b OUT THE CONTRI b UTOR

Chris Gray is CEO of Your Empire, a buyers’ agency that buys homes and investments for time-poor professionals – searching, negotiating, renovating and managing property on their behalf. Chris has spent over 10 years as the host of ‘Your Property Empire’ on Sky News Business channel, where he’s interviewed various heads of property research companies and major industry figures. Chris is a qualified accountant, buyers’ agent and mortgage broker. For more information, visit www.yourempire.com.au and follow Chris on Facebook: @ChrisGraySydney

r ba C u TS C aSH raT e FO r TH e FI r ST TIM e SINC e

2020

FO

–

WH aT IT M ea NS

r buyer S, S e LL er S,

a ND INV e STO r S

The Reserve Bank of Australia (RBA) has kicked off 2025 with a major announcement: a 0.25 percentage point cut to the cash rate, bringing it down to 4.10%. This decision marks the first-rate reduction in over four years and the first-rate change since November 2023, when the RBA raised rates to 4.35%.

With interest rates finally moving downward, many Australians – whether buying, selling, or investing – are wondering: What does this mean for the property market?

WHY DID THE RbA CUT INTEREST RATES?

The RBA adjusts the cash rate based on several economic factors, including inflation, employment and consumer spending. While inflation has been a significant concern in recent years, recent data suggests a slowdown in price growth, giving the RBA room to ease borrowing costs.

Lower interest rates typically aim to:

• Stimulate economic activity

• Make borrowing more affordable

• Support property buyers and businesses

But how does this affect you?

IMPACT ON PROPERTY bUYERS

For those looking to purchase a home, a lower cash rate could mean cheaper mortgage repayments. As banks pass on the rate cut, home loan interest rates may drop, improving borrowing capacity and making home ownership more accessible.

• Potential benefit: Easier loan approvals and lower monthly repayments

• What to watch:

Increased competition as more buyers enter the market

IMPACT ON SELLERS

If you're selling a property, lower rates can drive up demand, as more buyers feel confident entering the market. This could lead to stronger competition, higher offers, and potentially quicker sales.

• Potential benefit: Higher property values due to

increased buyer demand

• What to watch:

A potential shift in market conditions as rates fluctuate

IMPACT ON PROPERTY INVESTORS

For investors, rate cuts often make property investments more attractive, as lower interest rates can improve rental yield and overall affordability. However, this may also mean increased demand from other investors, affecting property prices.

• Potential benefit:

Lower financing costs for investment properties

• What to watch:

Potentially rising property prices as more investors re-enter the market

Whether you're looking to buy, sell, or invest, staying informed is key. The latest RBA decision signals a potential shift in market conditions, as such now could be a good time to review your options.

S HO u LD yO u

re NOVaT e O r S e LL aS-IS? S e V e N

DVa NTa G e S OF S e LLING WITHO u T re

If you’re planning to move – whether upgrading, downsizing, relocating for a job, or simply seeking a lifestyle change – it’s crucial to consider what truly needs to be done to prepare your property for the market. While the idea of renovating might be tempting, selling your home as-is could be the better option.

Major operational issues, such as a leaking roof, faulty heating system, or outdated electrical and plumbing, must be addressed before listing, as these are legal disclosure requirements. If left unresolved, a home inspection will likely reveal them, potentially leading to a withdrawn offer.

Here are some important points to consider when selling your property:

1. RENOVATION RETURNS MAY NOT bE WORTH IT

Many home improvements do not deliver an immediate financial return. While full kitchen and bathroom renovations add the most value to a property, they are costly and highly disruptive. If these spaces have not been

updated, it might be best to leave them as they are. Instead, focus on maintaining existing features and ensuring the property is in good condition.

2. LIVING IN A RENOVATION ZONE IS STRESSFUL

For those in spacious homes with extra bathrooms and spare rooms, renovations may be manageable. However, for smaller homes, the inconvenience is significantly greater. Unless you are handling all the work yourself, you are also at the mercy of suppliers’ schedules. If you won’t be the one enjoying the upgrades, investing $20,000 in a last-minute kitchen makeover might not be worth it. Simple updates like painting, replacing cabinet doors, and updating handles

can be extremely cost effective and have a high impact.

3. PERSONAL TASTE IS SUb JECTIVE

Buyers have diverse preferences. A prospective homeowner may not see your vision for a space, whether it’s a study, nursery or potential ensuite. Instead of attempting to predict buyers’ tastes, create a neutral space that allows them to imagine their own possibilities.

4. YOU’VE ALREADY DECIDED TO MOVE

Once you’ve made the choice to leave, don’t let sentimental attachments influence your decisions. If you always intended to add a skylight but never did, let it go – your next home may offer better natural lighting or even

floor-to-ceiling windows. The goal is to move forward, not dwell on past home improvement dreams.

5. FIRST IMPRESSIONS START OUTSIDE

No matter how much effort you put into interior updates, they won’t matter if the home’s exterior is uninviting. Prioritise curb appeal by tidying up the front yard, removing clutter like unused bikes, reseeding patchy grass, and creating an inviting entryway. If you choose to invest in an outdoor upgrade, you might consider new patio furniture that you can take with you to your next home.

6. CLEANLINESS TRUMPS

bRAND-NEW FEATURES

A well-maintained home will always appeal more than one with signs of

wear and tear. Prospective buyers are put off by dirty walls, scuffed floors, stained carpets, cracked tiles, and smudged appliances. Your goal is to present a clean, well-kept space that potential buyers can picture themselves living in. If you can’t bring yourself to paint over a sentimental feature - such as the height markings of your children on a doorframe - replace the frame and keep it as a memento.

7. FIT THE MARKET, DON’T OVERDO IT

Luxury additions like pools, home theatres, or built-in bars might suit your lifestyle but you should consider if they align with what buyers are actually seeking.

A family that loves the outdoors might not want a game room, and an investor looking to rent the

property may not see the appeal of a hot tub. Avoid making excessive upgrades that price your home out of the local market – this could lead to financial losses in the long run. While renovations can be worthwhile in some cases, selling as-is will save time, stress and unnecessary expenses. Instead of sinking money into last-minute changes, focus on ensuring the home is well-presented, clean and market ready. By keeping things simple, you can streamline the selling process and maximise your return without the hassle of renovations.

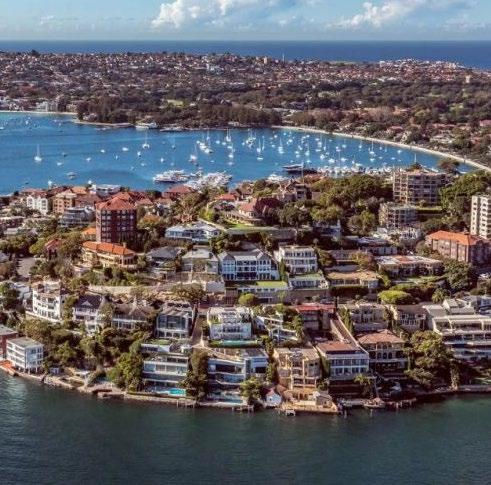

au SSI e CO aSTa L HOTSPOTS

Finding a beachside suburb where prices are set to surge is a property investor’s dream, and the latest data shows buyers won’t need to look far to find the next contender.

Data from PropTrack has revealed the coastal suburbs buyers are most keen on, highlighting the hotspots around Australia that have the potential to be the next Byron Bay.

Home values in the sought-after northern NSW town surged over the past decade, especially during the pandemic, putting it at the top of the list of the Australian suburbs with the strongest 10-year price growth.

To attract wealthy buyers of the calibre that splurge on multi-million dollar Byron Bay mansions, homes need stunning ocean views or beach access, agents say. This newly-built home Byron Bay home recently sold for more than $30 million, breaking the suburb price record.

Prices in Byron Bay quadrupled in that period, with the once-sleepy surf town swamped by cashed-up city slickers and even Hollywood celebrities buying holiday homes, causing values to skyrocket.

The warm climate and natural beauty of Byron Bay were two major factors attracting buyers real estate agent and Sotheby’s Byron Bay director Will Phillips said, but he said there was more to picking a winner than just sunny days and golden beaches.

“There are other places that have those things, but I think what makes Byron special is it has that sort of laid back lifestyle, but you're within 45 minutes’ drive of a major city,” Mr Phillips said. “The restaurants, the produce and the nightlife are important as well.”

While values in Byron have surged to levels that are out of reach for most–the suburb has a median house price of more than $3 million –the data shows there are plenty of in-demand coastal suburbs that are much more affordable.

Jump ahead to see the most in-demand beachside suburbs in:

• New South Wales

• Queensland

• Victoria

• Western Australia

• South Australia

• Tasmania

HOW TO SPOT THE NEXT BYRON BAY

REA Group senior economist Paul Ryan said changing demographics and the arrival of wealthier buyers were key drivers of price growth in coastal hotspots such as Byron Bay.

“It’s gentrification that starts that process,” Mr Ryan said. “The demographics start to change and that becomes this snowball effect.

“Once there's a few interesting restaurants, or people from wealthy parts of the country who know people who live there, word of mouth spreads.

Continued over page

“This could have happened to other parts of the coast, and it could still happen to other parts of the coast.”

A growing foodie scene is a sure sign that a town is gentrifying and may be a precursor for price growth.

Real estate agent and First National Byron director Su Reynolds said an evolving food and beverage scene is a key sign of a suburb on the up.

“One of the things you start to see changing is the availability of quality food,” Ms Reynolds said.

“Once you start to see the evolution of the commercial creator and an eclectic mix of cafes and restaurants, that is one of the indicators. It shows increasing demand and increasing numbers of customers.”

Byron Bay McGrath director Nick Dunn said the supply side of the equation was just as important in predicting future price growth.

“The biggest driver of growth in our area is that classic statement of demand over supply,” he said.

“Our council is so strict with further development that there's only so much available. That’s why the prices continue to grow.”

What $30 million buys in Byron Bay – ocean views from every room at Watermark, the priciest property to sell in the suburb last year.

Wealthy buyers are willing to pay more for homes that take advantage of the natural beauty of their surroundings, Mr Philips said, meaning the topography of the area and the way homes are built and oriented was crucial for supporting a high-end market–think beachfront blocks or hillside homes that capture coastal vistas.

“When you’re spending that kind of money, to have a beautiful view, privacy and peace and quiet are really important, and something buyers in the high end will expect,” he said.

THE MOST IN-DEMAND COASTAL TOWNS AND SUbURb S

For buyers looking to take advantage of surging price growth in the next coastal hotspot, demand data is a good place to start.

Tracking the number of enquiries per property listing can provide a gauge for demand in an area, revealing the suburbs where homes are most highly sought, Mr Ryan said. “It tends to indicate that there's a lot of buyer interest on the number of homes that are available for sale, which generally is the case for up and coming suburbs that have caught the eye of lots of people,” he said.

Bucasia north of Mackay is regional Australia's most in-demand beachside suburb, and with a median value of $510,000, one of the most affordable too.

We’ve crunched the numbers to compile a list of the most in-demand coastal suburbs outside the capitals across the states.

While some are already well known, others are still flying under the radar, potentially allowing buyers to get into the market before prices really take off. Click