38 minute read

Industry news

March construction jobs up 7,900 in Saskatchewan

There were 547,700 people working in Saskatchewan in March, an increase of 25,700 (4.9%) over last March. That is the strongest rate of employment growth in Canada and the most people ever working in Saskatchewan in the month of March.

“March was cold this year in Saskatchewan but our job market was hot,” Economy Minister Bill Boyd said. “Today’s numbers show our Growth Plan is working and our government will keep making decisions that encourage job creation in Saskatchewan.”

Saskatchewan had the lowest unemployment rate in Canada in March at 3.9% (seasonally adjusted). That is well below the 7.2% national unemployment rate. Regina’s seasonally adjusted unemployment rate of 3.5% was the lowest among all major cities and Saskatoon’s unemployment rate of 4.0% was the second lowest.

Off-reserve aboriginal employment was up by 2,200 (5.6%) for the second month in a row of year-over-year increases, and aboriginal unemployment dropped 1,600 for the sixth month in a row of year-over-year declines. The aboriginal unemployment rate is now 12.2%, down from 15.8% a year ago.

“There is still more work to be done in closing the employment gap between aboriginal and non-aboriginal people, but today’s numbers show we are moving in the right direction,” Boyd said. “Jobs are tracking higher so far in 2013 which is an encouraging sign that the Saskatchewan economy will have another good year.”

Other highlights include: • Full-time employment increased by 19,800 to a record high of 445,400 for the month of March. • Construction jobs were up 7,900 and

Agriculture jobs were up 7,600 yearover-year. • Regina’s employment increased by 7,100 (5.8%) and Saskatoon’s employment increased by 10,600 (7.2%). • Saskatchewan’s seasonally adjusted employment increased by 2,400 (0.4%) from the previous month with the second highest growth rate in the country. For more information, contact: Deb Young, Economy, Regina; Phone: 306-787-4765; Email: deb.young@gov.sk.ca.

Saskatchewan has committed $2.8 million to address structural problems at the Invermay Health Centre. Saskatchewan Health Minister Dustin Duncan toured the Invermay facility.

In January, long-term care residents and staff at Invermay Health Centre were temporarily relocated to health facilities in neighbouring communities, following the discovery of some structural damage and presence of mould in the building. Temporary relocation of staff and residents to other facilities, including Canora Gateway Lodge, was required while damage to the Invermay facility was assessed and repair work began.

“It is a top priority for our government to provide a comfortable and safe place for long-term care residents to stay, and a suitable work environment that allows health care staff to provide quality care,” Duncan said. “We are pleased to see the Sunrise Health Region has begun repairs at Invermay Health Centre to ensure that residents may return to their home as soon as possible.”

“We expect the repairs will be completed within six months,” Sunrise Regional Health Authority Chairperson Lawrence Chomos said. “We appreciate the understanding and co-operation from residents, families, staff and the community. The safety, health and comfort of our long-term care residents are the region’s priority.”

Duncan also toured the Canora Gateway Lodge, which recently sustained damage in the dining room due to a cracked ceiling beam. The Sunrise Health Region is further assessing the facility and associated costs to repair the damaged area.

Since November 2007, the government has made an unprecedented $814 million investment in provincial health system major capital projects, building improvements and equipment upgrades.

For more information, contact: Tyler McMurchy, Health, Regina; Phone: 306-787-4083.

Granite Developments pleaded guilty to safety violation

Granite Developments Inc., has pleaded guilty to one count under the Occupational Health and Safety (OHS) Act for failure to utilize a fall protection system. The company was fined $980 in Regina Provincial Court on March 11, 2013.

The conviction is related to an incident which occurred on October 12, 2010. Three workers were observed on the roof of a building without a proper fall protection system. Two other charges against Granite Developments Inc. were stayed.

OHS conducts approximately 4,000 worksite inspections annually to ensure standards are known, understood and enforced. OHS has a zero tolerance approach to violations of fall protection.

For more information, contact: Shannon McMillan, Labour Relations and Workplace Safety, Regina; Phone: 306-787-0253.

Quebec Portal

The new regulatory provisions apply to the owners and operators of the buildings, installations and equipment that are subject to the Regulation.

Those provisions, which are contained in the Building section of the Safety Code, introduce new building maintenance and operating standards. They are further to repeated requests from fire safety services providers, and aimed at improving fire prevention, particularly in sleeping areas and private seniors’ residences.

By introducing obligations relating to the maintenance and inspection of façades and parking lots, the new requirements also meet many recommendations made by coroners further to fatal accidents.

Persons wishing to learn more about the new Regulation may: • consult the Regulation to improve building safety published in the Gazette officielle du Québec • visit the RBQ website at www.rbq.gouv.qc.ca/securite • call the Centre de relation clientèle at 1-800-361-0761

Portail Quebec

La Régie du bâtiment du Québec (RBQ) annonce aujourd’hui l’entrée en vigueur du Règlement visant à améliorer la sécurité dans le bâtiment. Les nouvelles dispositions réglementaires s’adressent aux propriétaires et aux exploitants des bâtiments, des installations et des équipements assujettis.

«La sécurité est au cœur des préoccupations de la RBQ et ce règlement s’inscrit dans la mission de notre organisme, qui est de mieux protéger les citoyens. En améliorant la réglementation sur l’entretien des bâtiments, nous souhaitons prévenir des incidents regrettables qui mettent en péril la santé et la sécurité du public», a déclaré le président-directeur général de la RBQ, monsieur Stéphane Labrie.

Pour une sécurité accrue

Consignée dans le chapitre Bâtiment du Code de sécurité, cette réglementation introduit de nouvelles normes d’entretien et d’exploitation des bâtiments. Elle donne suite à des demandes répétées du milieu de la sécurité incendie et vise à améliorer la prévention des incendies, notamment dans les lieux de sommeil et dans les résidences privées pour aînés.

En introduisant des obligations d’entretien et d’inspection des façades et des parcs de stationnement, les nouvelles exigences répondent également à plusieurs recommandations formulées par les coroners à la suite d’accidents mortels.

Le Règlement en bref

Le Règlement visant à améliorer la sécurité dans le bâtiment, dont la responsabilité est confiée à la RBQ, comporte les cinq volets suivants: 1. Des normes applicables en fonction de l’année de construction qui ont pour cible la sécurité, la santé ou la protection des bâtiments contre l’incendie et les dommages structuraux. 2. Des dispositions bonifiant les exigences en vigueur lors de la construction. Ces dispositions s’appliquent aux lieux de sommeil et aux établissements de soins avec des exigences particulières pour les résidences privées pour aînés soumises à la certification du ministère de la Santé et des Services sociaux.

Les propriétaires et les gestionnaires disposeront de 1 à 5 ans pour se conformer à ces différentes dispositions, selon leur nature et leur complexité. 3.L’intégration du Code national de prévention des incendies (CNPI), publié par le Conseil national de recherches

Canada, avec certaines modifications pour tenir compte des particularités du

Québec. 4.Des dispositions relatives à l’inspection et à l’entretien des façades de bâtiments d’une hauteur de 5 étages et plus hors sol. 5.Des dispositions relatives à l’inspection et à l’entretien des parcs de stationnement aériens ou souterrains dont au moins une surface en béton ne repose pas sur le sol.

En savoir plus sur le Règlement

Les personnes souhaitant en apprendre davantage au sujet de ce nouveau règlement peuvent: • consulter le Règlement visant à améliorer la sécurité dans le bâtiment publié dans la Gazette officielle du Québec • visiter le site Web de la RBQ au www.rbq.gouv.qc.ca/securite • communiquer avec le Centre de relation clientèle au 1 800 361-0761. Elles sont également invitées à visiter notre site Web au cours des prochains jours. La RBQ y déposera plusieurs documents et outils afin de faciliter la compréhension du règlement et de guider les propriétaires et les exploitants pour sa mise en application.

La RBQ

Présente partout au Québec, la RBQ a pour mandat de veiller à la qualité des travaux de construction et à la sécurité des personnes dans les domaines du bâtiment, de l’électricité, de la plomberie, du gaz, des équipements pétroliers, des appareils sous pression, des ascenseurs, des remontées mécaniques, des jeux et manèges et des lieux de baignade. La RBQ surveille l’application de la Loi sur le bâtiment et la réglementation afférente dans les différents domaines techniques de sa compétence.

SOURCE: Marie-Claude Masson, Direction des communications. Pour information: Sylvain Lamothe, Direction des communications; 514- 873-0688; 1-866374-7747.

Congratulations

to the following members who have qualified as a PQS or CEC (including reinstatements):

CIQS – Quebec Antoaneta Bancheva, ECC Isabelle Delisle, ECA Benoit Duchesne, ECC Serguei Remeniak, ECC Guillaume Robitaille, ECA André Roy, ECC

CIQS – Ontario Dwight A. Baugh, PQS Deroy Destang, PQS Mehrdad Fakkrjahani, CEC Hanzel Jimenez, CEC Hengmin Li, CEC Christopher Matz, PQS Ryan McGonigle, CEC Stanislav Markovich, CEC Arvindkumar Mishra, CEC Larry Vidinovski, PQS Stephen Wells, PQS Chun Xiao Wei, PQS Mandrew Zhao, CEC CIQS – British Columbia Derek Andrew, PQS Doina Dobre, CEC Timothy Frank, CEC Rachel Harrington, CEC

CIQS – Prairies and NWT Kevin Ellis, PQS Michael Gabert, CEC Ven Richard Guerra, PQS Alex Marsh, CEC Donald Maw, PQS CIQS – Maritimes Brett Kristiansen, CEC Chris Pezzareallo, CEC

CIQS Members at Large Kunaseelan Shanmugarajah, PQS Suthan Shanmugaratnam, PQS

Construction cost trends

Building permits, January 2013

Municipalities issued building permits worth $5.8 billion in January, up 1.7% from December. The increase in the residential sector more than offset a decrease in the non-residential sector. Despite the advance, the total value of building permits has been trending downwards since October 2012.

The increase in construction intentions came from every province except Alberta and Quebec. New Brunswick posted the largest advance followed closely by Saskatchewan and British Columbia.

In the residential sector, the value of permits increased 17.6% to $3.8 billion in January, following six consecutive months of decline. Ontario had the largest gain, with British Columbia a distant second followed closely by New Brunswick. These gains more than offset decreases in Quebec, Newfoundland and Labrador and Manitoba. However, residential construction intentions are continuing a downward trend that began in July 2012.

Construction intentions in the nonresidential sector fell 19.2% to $2.0 billion, following a 7.8% decrease the previous month. Ontario, Quebec and Alberta were responsible for most of the decline. Nonresidential construction intentions rose in Saskatchewan, New Brunswick, Manitoba and Newfoundland and Labrador. The total value of non-residential permits has been on an upward trend since June 2012, following a relatively flat period that began in May 2011.

Residential sector: Higher construction intentions for both multi-family and single-family dwellings

Construction intentions for multi-family dwellings rose 38.0% to $1.6 billion in January. It was the first increase in seven months. The advance was principally attributable to higher construction intentions in Ontario, British Columbia and New Brunswick.

Municipalities issued $2.3 billion worth of building permits for single-family dwellings in January, up 6.6% from December. This was the second increase in seven months. Higher construction intentions in Ontario more than offset decreases in four provinces, led by Quebec and Manitoba.

Municipalities approved the construction of 16,002 new dwellings in January, up 15.6% from December. The increase was largely the result of a 25.9% gain in multi-family units to 9,550. The number of permits issued for single-family dwellings rose 3.0% to 6,452 units.

Non-residential sector: Declines in all components

Construction intentions in the commercial component decreased 15.2% to $1.3 billion, a second consecutive monthly decrease and their lowest level since February 2012. Despite these declines, commercial intentions have been on a continuous upward trend since November 2011.

Construction intentions for commercial buildings were down in every province except Saskatchewan, Newfoundland and Labrador and Manitoba. Ontario and Quebec had the largest declines. The decrease in January came from a variety of buildings, including retail complexes, hotels and restaurants as well as warehouses in Ontario and office buildings in Quebec.

The value of institutional permits declined 26.7% to $366 million in January, falling to their lowest level since January 2012. This was the third decrease in a row. The decline was largely attributable to lower construction

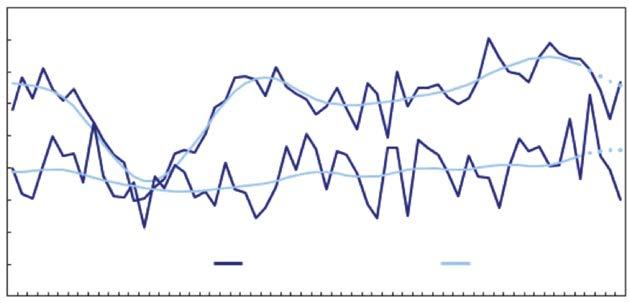

Chart 1 - Total value of permits

billions of dollars 7.8 7.4 7.0 6.6 6.2 5.8 5.4 5.0 4.6 4.2 3.8 3.4 3.0

J J J Seasonally adjusted Trend

J

J J 2008 2009 2010 2011 2012 2013

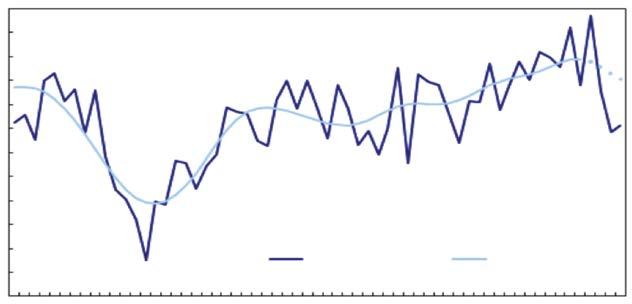

Chart 2 - Residential and non-residential sectors

billions of dollars 5.0

4.5

4.0

3.5

3.0

2.5 Residential

2.0

1.5

1.0 Non-residential

Seasonally adjusted Trend

0.5

J J J J J J 2008 2009 2010 2011 2012 2013

Note(s): The higher variability associated with the trend-cycle estimates is indicated with a dotted line on the graph for the current reference month and the three previous months. See Note to readers.

Canada

Newfoundland and Labrador 802.5 766.4 1,205.2 1,057.3 1,184.6

Prince Edward Island 216.9 178.6 259.9 242.4 281.5 Nova Scotia 1,326.7 1,368.7 1,633.8 1,464.6 1,551.1 New Brunswick 1,113.8 1,148.2 1,133.3 965.9 968.5 Quebec 13,806.7 12,929.7 14,842.3 15,489.6 16,062.5 Ontario 25,414.6 21,880.5 28,138.6 28,024.4 29,547.5 Manitoba 1,636.7 1,560.7 1,757.4 1,842.1 2,485.7 Saskatchewan 2,185.8 1,890.3 2,077.0 2,613.9 3,114.1 Alberta 13,141.2 11,276.9 11,425.4 12,768.1 14,662.9 British Columbia 10,577.2 7,629.9 9,723.8 9,249.8 10,759.6 Yukon 70.0 157.6 130.0 140.9 94.7 Northwest Territories 87.4 164.7 74.4 21.1 44.2 Nunavut 58.0 97.2 44.4 85.6 94.0

2008 2009 2010 2011 2012

All permits $ millions 70,437.4 61,049.4 72,445.5 73,965.7 80,850.7

Source: Statistics Canada, CANSIM, tables 026-0003 and 026-0008, and Catalogue no 64-001-X. Last modified: 2013-03-07.

intentions for educational institutions in Ontario, Alberta and Quebec as well as medical facilities in Alberta. Institutional construction intentions have been trending slightly downwards for eight months.

Construction intentions in the industrial component fell 25.6% to $296 million in January. This was the third consecutive monthly decrease following a record high in October. Industrial construction intentions have been on a downward trend since June 2012. This follows a continuous year-long increase that began in June 2011.

The decrease in January was largely the result of lower construction intentions for mining and primary industry buildings in Ontario, manufacturing buildings in Alberta and utilities buildings in Ontario and Quebec. Industrial construction intentions decreased in seven provinces, led by Ontario, with Quebec a distant second.

Most provinces post gains

Construction intentions advanced in eight provinces in January. New Brunswick posted the largest advance followed closely by Saskatchewan and British Columbia.

In New Brunswick, construction intentions more than tripled following two consecutive monthly declines. The increase was a result of higher construction intentions for residential and institutional buildings.

In Saskatchewan, construction intentions grew on the strength of higher construction intentions for single family dwellings and commercial buildings.

A 10.9% increase in British Columbia was attributable to higher construction intentions for multi-family dwellings and institutional buildings.

In Ontario (+2.1%), higher residential construction intentions offset declines in non-residential components.

The largest decrease occurred in Quebec, where all components except multi-family dwellings fell.

In Alberta, the value of permits for institutional and commercial buildings was behind the decline.

Just over half of the census metropolitan areas post increases

The value of permits was up in 18 of the 34 census metropolitan areas.

Toronto, Vancouver and Saskatoon recorded the largest gains. Toronto reported advances in residential buildings. Vancouver’s gain came from multi-family dwellings and institutional buildings, both of which had decreased the previous month. In Saskatoon, the increase came mainly from higher construction intentions for commercial buildings and single-family dwellings.

The largest declines occurred in Montréal and Kitchener–Cambridge–Waterloo. In Montréal, the decline originated from lower construction intentions for commercial buildings and to a lesser extent single-family dwellings and industrial buildings. In Kitchener–Cambridge–Waterloo, lower construction intentions for institutional buildings were behind the decrease.

Source: Statics Canada The January 2013 issue of Building Permits (Catalogue number64-001-X) For more information, contact us (toll-free 1-800-263-1136; infostats@statcan.gc.ca).

To enquire about the concepts, methods or data quality of this release, contact Jason Aston (613-951-0746), Investment, Science and Technology Division.

Labour Force Survey, March 2013

Following an increase the previous month, employment declined by 55,000 in March, all in full time. The unemployment rate rose 0.2 percentage points to 7.2%.

Despite the decline in March, employment was 1.2% or 203,000 above the level of 12 months earlier, with the increase mainly in full-time work. Over the same period, the total number of hours worked also rose by 1.2%.

Provincially, employment declined in Quebec, British Columbia and Alberta, and edged down in Ontario. The only province with an increase was Nova Scotia.

In March, there were fewer people employed in three industries: accommodation and food services, public administration and manufacturing. At the same time, there was little change in the other industries.

There were 85,000 fewer private-sector employees in March, while the number of self-employed rose by 39,000 and the number of public-sector employees was little changed. Compared with 12 months earlier, the number of private-sector employees increased by 1.0% or 111,000, while the number of self-employed was up 2.1% or 55,000 as a result of the gains in March. Public-sector employment was little changed over the 12-month period.

Employment in March decreased among people aged 25 to 54, while there was little change among youths and people aged 55 and over.

Provincial summary

Employment in Quebec declined by 17,000 in March, and the unemployment rate rose 0.3 percentage points to 7.7%. Despite this decrease, employment in the province was 1.6% above the level of 12 months earlier,

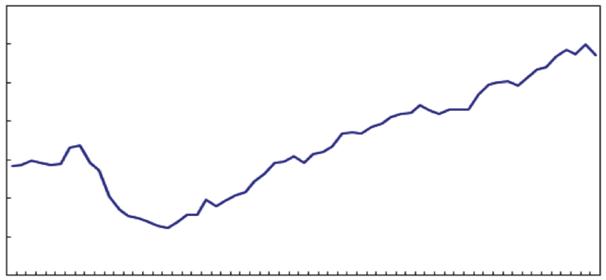

thousands 17,900

17,700

17,500

17,300

17,100

16,900

16,700

16,500

M J J J J J M 2008 2009 2010 2011 2012 2013

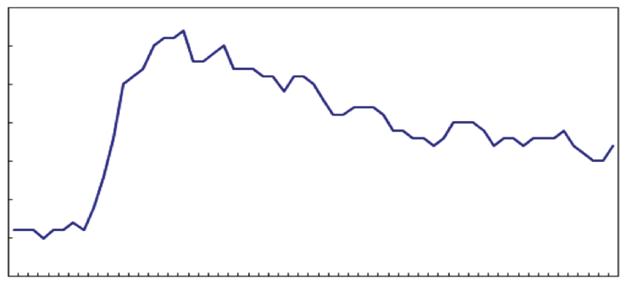

Chart 2 - Unemployment rate

% 9.0

8.5

8.0

7.5

7.0

6.5

6.0

5.5

M J J J J J M 2008 2009 2010 2011 2012 2013

compared with a national growth rate of 1.2%.

Employment in British Columbia was down 15,000, offsetting most of the increase in February. This pushed the unemployment rate up 0.7 percentage points to 7.0%. Compared with 12 months earlier, employment in the province was little changed.

In Alberta, there were 11,000 fewer people employed in March, the first notable decline in more than two years. The unemployment rate in the province rose 0.3 percentage points to 4.8%, still one of the lowest in the country. While there were fewer people working in March, Alberta experienced employment growth of 1.7% on a year-over-year basis.

In Ontario, employment edged down by 17,000 in March, following an increase of 35,000 the month before. The unemployment rate held steady at 7.7%, a result of fewer people participating in the labour force. Year-over-year employment growth in the province was 0.8%.

Nova Scotia was the only province with an employment increase in March, up 2,900, following a similar increase the month before. The unemployment rate in the province was 9.5%. Despite the recent gains, employment was little changed compared with 12 months earlier.

While employment in Saskatchewan was little changed in March, the province experienced the strongest year-over-year growth in the country, at 4.6%. The unemployment rate was 3.9% in March, still the lowest among all provinces.

Industry employment

In March, there were notable employment declines in accommodation and food services, public administration and manufacturing.

Employment in accommodation and food services fell by 25,000, offsetting an increase the month before. This left employment in the industry similar to the level of 12 months earlier.

Public administration employment decreased by 24,000 in March, leaving employment in this industry down slightly from 12 months earlier.

The number of workers in manufacturing declined by 24,000 in March, following a similar decrease the previous month. Employment growth in the spring of 2012 was followed by losses since the summer, leaving employment in this industry down 2.8% from 12 months earlier.

Employment declines among people 25 to 54

Among people aged 25 to 54, employment declined by 47,000, equally divided between men and women. Compared with 12 months earlier, employment for this age group was up 0.6% or 68,000.

Employment among those aged 55 and over was little changed in March. On a yearover-year basis, employment among people in this age group rose by 4.2% or 135,000, partly a result of population ageing.

Among youths aged 15 to 24, employment was also little changed in March, while their unemployment rate increased 0.6 percentage points to 14.2%, as more youths searched for work. Employment among youths has been on a slight upward trend since August 2012.

Quarterly update for the territories

The Labour Force Survey also collects labour market information about the territories. This information is produced monthly in the form of three-month moving averages. The following data are not seasonally adjusted; therefore, comparisons should only be made on a year-over-year basis.

In the first quarter of 2013, employment and the unemployment rates in Yukon and the Northwest Territories were similar to those of the first quarter of 2012. The unemployment rate was 7.6% in Yukon and 8.0% in the Northwest Territories in the first quarter of 2013.

In Nunavut, employment increased by 700 in the first quarter of 2013, compared with the same quarter in 2012, and the unemployment rate fell from 15.3% to 11.4% over the same period.

Source: Statistics Canada, Labour Force Information (Catalogue number71-001-X), The next release of the Labour Force Survey will be on May 10.

For more information, contact us (toll-free 1-800-263-1136; infostats@statcan.gc.ca). To enquire about the concepts, methods or data quality of this release, contact Vincent Ferrao (613-951-4750; vincent.ferrao@ statcan.gc.ca) or Jeannine Usalcas (613951-4720; jeannine.usalcas@statcan.gc.ca), Labour Statistics Division.

CB ROSS

COST CONSULTING

JOB OPPORTUNITIES

- Senior Cost Planner - Project Monitor

C.B. Ross Cost Consulting is a consulting firm located in Toronto, Ontario offering consulting services to a wide spectrum of clients from project inception through to completion. We have job opportunities in our Project Monitoring and Cost Planning/Estimating departments. Candidates must have:- - relevant experience in the construction industry - strong communication skills - time management skills - be working towards (or have interest in) RICS and CIQS membership. In return, we offer an extensive employee package commensurate with expertise, qualifications and skills. If you are interested, please submit your resumé by email: mail@cbross.ca or by fax: (416) 487-3017 Only select candidates whose resumés best match our requirements will be contacted.

Prince Edward Island new revenue tax changes

ON APRIL 1, 2013 the provincial revenue tax (PST @10%) and the goods and service tax (GST @ 5%) were replaced in Prince Edward Island by the harmonized sales tax (HST). The HST tax rate is 14% and is a combination of a provincial portion (at 9%) and a federal portion (at 5%).

During the sitting of the Legislative Assembly in the fall of 2012, amendments to the Revenue Tax Act were passed which, effective April 1, 2013, remove the requirement for businesses to charge, collect and remit the PST.

There are a number of provisions of the Revenue Tax Act that will remain in force for a period of time as the administration of the PST is wound down. Please refer to the Canada Revenue Agency website (www.cra-arc.gc.ca) for assistance with the application of HST in Prince Edward Island,or call 1-800-959-5525 or visit www.peihst.ca.

Here are some things businesses may want to consider when preparing for the HST: 1) Determine whether your supplies will be subject to the HST. You may be required to charge HST on goods and services that were not subject to revenue tax. 2) Review the transitional rules to determine whether the HST will apply to any payments that become due or are paid on or after February 1, 2013, for your supplies. Also, determine whether you will have to self-assess the 9% provincial part of the HST on any payments that become due or are paid after

November 8, 2012, and before

February 2013 for your purchases. 3) Update your point-of-sale systems (e.g. cash registers), computer systems, manual accounting or invoicing systems, etc. in order to properly charge and account for the

HST on your supplies. Examples of these updates could include: • amending software and tax codes to accommodate the various tax rates; • amending automated systemgenerated entries to reflect the correct tax amount; • ensuring software and systems can accommodate PEI’s point-ofsale rebates; or • modifying systems to track the federal and provincial components of the HST, if necessary. 4) Ensure your accounting systems can properly record and account for any eligible input tax credits on your purchases, and properly report any recaptured input tax credits, if necessary. • Update tables/codes for accounts payable systems that automatically record input tax credits based on embedded taxes. 5) Ensure your accounting systems can properly record and account for the

HST that may apply to any payments that become due or are paid on or after February 1, 2013. Generally, if the HST applies to any such payments, the 9% provincial part of the HST on both your supplies and purchases will have to be reported or claimed, as the case may be, in your GST/HST return that includes April 1, 2013. • Ensure your accounting system is able to account for both GST/PST and HST on the same invoice, if necessary. 6) Modify pre-printed lists or internet web sites containing sales tax information. • Ensure your invoices properly state whether HST is applicable, the HST rate, your GST/HST registration number, and all other information required by the Excise Tax Act and the Input Tax Credit Information (GST/HST) Regulations. 7) Take steps to ensure that you stop collecting revenue tax on April 1, 2013, and that the final returns are prepared and submitted by April 20, 2013. Make sure: • any PST paid or payable after March 31, 2013, is remitted on a supplemental tax return; and • all supplemental returns are filed no later than August 20, 2013.

Digitize Directly on your screen from files with . . .

eTakeoffs of ePlans in Microsoft Excel. The drawing and measurement are saved with any cell.

You don’t work for our software, it works for you.

On-Screen Site Excavation Software

Calculate cuts & fills by digitizing on your screen.

Our Canadian distributor

www.vertigraph.com Interworld: 800-663-6001

Order online at http://interworldna.com/vertigraph/siteworx_os.php and get FREE SHIPPING with this code: shp_qs2013 Valid through July 31 of 2013

GST/PST AND HST SUMMARY

UNDER GST/PST SYSTEM

You pay

15.5 %

5 %

Government pays you back

UNDER HST SYSTEM

You pay

14 %

14 %

Government pays you back

Benefits of HST

1) Contractors will experience tax savings under HST • Input Tax Credits put Island businesses on a level playing field in the region

2) Tax savings can be used to: • Increase bottom line • Re-invest in business and enhance economy • Reduce prices

Reference: The Impact of Sales Tax Reform on Ontario Consumers: A First Look at the Evidence; Michael Smart.

Discover how you could enjoy greater savings

Join the growing number of members of your organization who enjoy greater savings from TD Insurance on home and auto coverage.

Most insurance companies offer discounts for combining home and auto policies, or your good driving record. What you may not know is that we offer these savings too, plus we offer preferred rates to members of the Canadian Institute of Quantity Surveyors. You’ll also receive our highly personalized service and great protection that suits your needs. Find out how much you could save.

Request a quote today

1-866-296-0888

Monday to Friday: 8 a.m. to 8 p.m. Saturday: 9 a.m. to 4 p.m. ciqs.tdinsurance.com

Endorsed by:

The TD Insurance Meloche Monnex home and auto insurance program is underwritten by PRIMMUM INSURANCE COMPANY. The program may be distributed by Meloche Monnex Insurance and Financial Services Inc. in Quebec and by Meloche Monnex

Financial Services Inc. in the rest of Canada except Ontario.

Due to provincial legislation, our auto insurance program is not offered in British Columbia, Manitoba or Saskatchewan. *No purchase required. Contest organized jointly with Security National Insurance Company and open to members, employees and other eligible persons belonging to employer, professional and alumni groups which have an agreement with and are entitled to group rates from the organizers. Contest ends on October 31, 2013. Draw on November 22, 2013. One (1) prize to be won. The winner may choose between a Lexus ES 300h hybrid (approximate MSRP of $58,902 which includes freight, pre-delivery inspection, fees and applicable taxes) or $60,000 in Canadian funds. Skill-testing question required. Odds of winning depend on number of entries received. Complete contest rules available at group.tdinsurance.com/contest. ®/The TD logo and other trade-marks are the property of The Toronto-Dominion Bank or a wholly-owned subsidiary, in Canada and/or other countries.

Real property contractors –

PROVINCIAL SALES TAX ACT IN BRITISH COLUMBIA

This notice provides an overview of how the provincial sales tax (PST) applies to goods purchased, brought, sent or received in BC by real property contractors and used to improve real property.

This notice does not provide information related to owners of real property who purchase, bring, send or receive goods in BC for their own use, including when they hire a contractor to install those goods. For information on goods purchased in BC, see Notice 2012-011, Purchases of Tangible Personal Property (Goods) in British Columbia, and for information on goods brought, sent or received in BC, see Notice 2012-013, Tangible Personal Property (Goods) Brought Into British Columbia.

For additional information on how the PST applies to real property contracts and to purchases and use of materials and equipment in BC that straddle April 1, 2013, please see PST Notice 2012010, General Transitional Rules for the Re-implementation of the Provincial Sales Tax.

DEFINITIONS

Real property is land and any items permanently attached to the land (buildings and structures). Goods that become permanently attached to the land, buildings or structures on installation are called improvements to real property.

Improvements to real property include integral components of buildings or land, such as windows, doors, plumbing, electrical and heating systems structures permanently affixed to land, including concrete driveways and sidewalks. They may also include very large machinery or equipment that is constructed on site, such as machinery used in sawmills, pulp mills or other industrial locations, unless the machinery or equipment is affixed machinery.

Affixed machinery is machinery, equipment or apparatus that is used directly in the manufacture, production, processing, storage, handling, packaging, display, transportation, transmission or distribution of goods, or in the provision of software or a service, and is affixed to, or installed in, a building, a structure or land so that it ceases to be personal property at common law.

Although affixed machinery as defined ceases to be personal property at common law upon installation (i.e. it would normally be considered to be an improvement to real property), for purposes of the PST it is, with the exceptions noted below, generally taxable as tangible personal property (goods).

The following are specifically excluded from the definition of affixed machinery so, for purposes of the PST, they are taxed as improvements to real property (see General Rule below): • machinery, equipment or apparatus that is affixed to, or installed in, a building, structure or land for the purpose of heating, air conditioning or lighting a building or structure, sewage disposal for a building or structure, or lifting persons or freight within a building or structure by elevator or escalator; or • machinery, equipment or apparatus that is: - of such a size that it must be constructed on the site where it is to be used, - by its nature or design, would normally be expected to remain, for its useful life, on the site at which it is constructed, - does not run on rails or tracks, or does not otherwise move around on or from the site at which it is constructed, and - cannot be moved from the site at which it is constructed without ♦ dismantling the machinery, equipment or apparatus, or ♦ dismantling or causing substantial damage to the building or structure to which it is affixed or in which it is installed.

Therefore, sales or leases of affixed machinery, other than the specific exceptions outlined above, are generally taxable for PST purposes as tangible personal property. More information on how PST applies to affixed machinery will be provided in the near future.

You are a real property contractor if, under a contract, you construct buildings, or supply and affix or install goods that become improvements to real property or affixed machinery. This includes contractors and subcontractors in the construction industry, as well as other businesses that make improvements to real property under a contract.

REAL PROPERTY CONTRACTORS AND PST General rule

If you are a real property contractor, you are required to pay PST on the goods you purchase, bring, send or receive delivery of in BC for the purposes of fulfilling a contract for the supply and installation of affixed machinery or improvements to real property, unless a specific exemption applies.

As a real property contractor, you must pay PST because you are the user of the goods used to fulfill the contract. For the purposes of the PST, supplying and installing goods under a contract to improve real property is NOT a sale of those goods to your customer. Therefore, you are not eligible for the exemption for goods acquired for resale.

You must pay PST regardless of whether your contract is a time and materials contract or a lump sum contract, unless a specific exemption applies.

Real property contractors who sell goods at retail

A person who acquires goods for the sole purpose of resale is exempt from PST. Real property contractors who also operate a retail or wholesale facility selling goods may purchase goods for resale exempt from PST.

If a person acquires goods for resale and then subsequently uses the goods for another purpose, including fulfilling a contract as a real property contractor, the person using those goods is required to self-assess PST on the goods, unless a specific exemption applies.

The PST must be self-assessed by the last day of the month following the month in which the goods are first used or, if you are a PST registrant, with the return for the reporting period that includes the date the goods are first used.

EXEMPTIONS FOR REAL PROPERTY CONTRACTORS Agreements that specifically require the customer to pay PST

A real property contractor is exempt from the PST on goods the real property contractor purchases, brings, sends or receives delivery of in BC for the purpose of fulfilling a contract to supply and affix, or install, affixed machinery or improvements to real property where, under the terms of the contract, the goods are used such that they cease to be personal property at common law, if: • the contractor and their customer enter into an agreement that specifically states that the customer is liable for the PST on the goods, and • the agreement sets out the purchase price of the goods. There must be written evidence of the agreement that specifically states that the customer is liable for the PST on the goods. The customer must pay PST on the greater of the contractor’s purchase price of the goods and the purchase price set out in the agreement.

Real property contractors who enter into agreements that specifically state that their customers are liable for the PST must be registered as PST collectors before the goods are supplied. As collectors, real property contractors must collect and remit PST to the government that their customers are required to pay, whether collected or not.

For more information on PST registration, please see Bulletin PST 001, Registering to Collect Provincial Sales Tax (PST). For more information on the requirement to charge and collect PST, please see Bulletin PST 002, Charging, Collecting and Remitting PST.

Contracts with persons exempt from PST

A real property contractor is exempt from the PST on goods the real property contractor purchases, brings, sends or receives delivery of in BC for the purpose of fulfilling a written contract to supply and affix, or install, affixed machinery or improvements to real property where, under the terms of the contract, the goods are used such that they cease to be personal property at common law, if the contract is with: • the Government of Canada (except where the Government of Canada has entered into an agreement with the government under which the

Government of Canada has agreed to pay PST), or • a person who would be exempt from

PST if they had purchased, brought, sent or received the goods instead of the contractor under: • the Provincial Sales Tax Act , or • Section 87 of the Indian Act (Canada).

Documenting exemptions for real property contractors

Where a real property contractor is exempt from the PST on goods in the above circumstances, the contractor may purchase the goods exempt at the time of sale, provided that the contractor provides the required information to their supplier at or before the time of sale.

Where there is a specific agreement transferring liability for the PST to the customer, a contractor must provide their PST registration number or, if the real property contractor has not yet received a PST registration number, they must provide an exemption certificate.

Where the contractor has entered into a written agreement with a person who is exempt from PST (as noted above), the contractor must provide their PST registration number or, if the real property contractor is not registered, an exemption certificate and a declaration completed by their customer that states the person is exempt from PST.

More information about exemption certificates will be provided in the near future.

TRANSITIONAL RULES PST payable on goods used by a real property contractor to improve real property on or after April 1, 2013

A real property contractor must pay PST on goods purchased or brought,

sent or received in BC prior to April 1, 2013 that are used for the purpose of fulfilling a contract under which the real property contractor is required to supply and affix, or install, affixed machinery or improvements to real property on or after April 1, 2013 such that the goods cease to be personal property at common law, unless a specific exemption applies.

The PST must be paid by the last day of the month following the month in which the real property contractor uses the goods. If the contractor is a PST registrant, the PST must be paid with the return for the reporting period that includes the date the goods are first used.

The amount of PST payable is calculated on the purchase price (regardless of when the consideration was paid or payable) of the goods and is reduced by the amount of: • PST otherwise paid under the

Provincial Sales Tax Act, • tax paid under the Social Service Tax

Act (i.e. PST paid before July 1, 2010) if the real property contractor has not obtained and is not eligible to obtain a refund, and • tax paid as the provincial portion of the HST if the real property contractor has not obtained and is not eligible to obtain a refund, rebate or credit, including input tax credits.

PST payable by customers

A real property contractor will be exempt from PST on goods used to supply and affix, or install, affixed machinery or improvements to real property on or after April 1, 2013 if there is a specific agreement transferring liability for the PST on those goods to the customer as set out above.

As set out above, there must be written evidence of the agreement transferring liability for the PST to the customer. The PST payable by the customer is the greater of the contractor’s purchase price of the goods and the purchase price set out in the agreement. The PST will be reduced as noted above.

The PST payable by the customer must be paid on or before the last day of the month after the month in which the contractor uses the goods such that they cease to be personal property at common law, regardless of when the customer is required to pay the real property contractor under the terms of the contract.

Real property contractors who enter into agreements that specifically state that their customers are liable for the PST must be registered as PST collectors before the goods are supplied. As collectors, real property contractors must collect and remit PST to the government that their customers are required to pay, whether collected or not.

For more information on PST registration, please see Bulletin PST 001, Registering to Collect Provincial Sales Tax (PST). For more information on the requirement to charge and collect PST, please see Bulletin PST 002, Charging, Collecting and Remitting PST.

PST payable on goods incorporated into certain residential homes that are subject to tax under the New Housing Transition and Rebate Act

A person who purchased goods or brought, sent or received goods in BC that are incorporated, on or after April 1, 2013 into property that could be the subject matter of a taxable sale or taxable selfsupply under the New Housing Transition Tax and Rebate Act must pay PST on the purchase price of the goods, unless a specific exemption applies.

The amount of PST payable is reduced by the amount of: • PST otherwise paid under the

Provincial Sales Tax Act, • tax paid under the Social Service Tax

Act (i.e. PST paid before July 1, 2010) if the person has not obtained and is not eligible to obtain a refund, and • tax paid as the provincial portion of the HST if the person has not obtained and is not eligible to obtain a refund, rebate or credit, including input tax credits. The PST must be paid by the last day of the month following the month in which the goods are incorporated into the property, or if the person is a PST registrant, with the return for the reporting period that includes the date the goods are incorporated into the property.

The PST on these goods will be eliminated on April 1, 2015 with the repeal of the New Housing Transition Tax and Rebate Act.

PST payable on mobile homes affixed to real property on or after April 1, 2013

Unless a specific exemption applies, a person must pay PST on the purchase price of the mobile home if the person: • acquired or manufactured a mobile home as defined in the Excise Tax Act (Canada) before April 1, 2013, and • the mobile home is affixed to land in BC for the purpose of use and enjoyment of the mobile home as a place of residence for an individual within the meaning of Part IX of the

Excise Tax Act (Canada). The amount of PST payable is reduced by the amount of: • PST otherwise paid under the

Provincial Sales Tax Act, • tax paid under the Social Service

Tax Act (i.e. PST paid before July 1, 2010) if the person or real property contractor has not obtained and is not eligible to obtain a refund, and • tax paid as the provincial portion of the HST if the person or real property contractor has not obtained and is not eligible to obtain a refund, rebate or credit, including input tax credits. The PST must be paid by the last day of the month following the month in which the mobile home is affixed to land in BC, or if the person is a PST registrant, with the return for the reporting period that includes the date the mobile home is affixed to land in BC.

The PST on these mobile homes will be eliminated on April 1, 2015 with the repeal of the New Housing Transition Tax and Rebate Act.

FURTHER INFORMATION

If you have any questions, please call us toll free at 1 877 388-4440 or email your questions to CTBTaxQuestions@gov. bc.ca or visit our website gov.bc.ca/pst.

The information in this notice is for your convenience and guidance and is not a replacement for the legislation. You can access the legislation and regulations on our website under Forms and Publications.

QUANTITY SURVEYORS, ESTIMATORS, PLANNERS

A leading Cost Consulting and Project Management firm requires the following candidates for its Montreal and Ottawa offices:

Junior, intermediate and senior level Q.S.’s, Estimators and Planners with experience on:

• Commercial and institutional projects • Industrial projects (oil/gas, refineries, mining, metallurgical).

We offer competitive salaries, benefits, training and potential for growth. Relocation assistance will be provided. We sincerely thank all applicants, but only those candidates which meet our requirements will be contacted.

Please send resume in strictest confidence to: LCO - Construction and Management Consultants Inc.

Fax: 514-846-8913 | Phone: 514-846-8914 | E-Mail: MONTREAL@LCOGROUP.COM

We are seeking a SENIOR ASSOCIATE LEVEL PROJECT MONITOR

Candidates should have a minimum of ten (10) years related experience, have an established track record in the Project Monitoring field, and be active in business development.

Being a Senior Associate level position at Pelican Woodcliff, the renumeration package will include a profit share component. Future ownership/partnership opportunities are a distinct possibility for the successful candidate.

Please e-mail your resume and cover letter in confidence to: ronnie@pelicanwoodcliff.com for the attention of Mr. Ronnie Mandowsky

Cost Consultants and Project Monitors

100 York Blvd., Suite 608, Richmond Hill, ON L4B 1J8 Tel 905.889.9996

www.pelicanwoodcliff.com