Keyactionstosafeguardagainst Deforestationin theEUTaxonomy

POLICY RECOMMENDATIONS BY CLIMATE & COMPANY

Authors:

Elisabeth Hoch | elisabeth@climcom.org

Max Tetteroo | max@climcom.org

Co authors:

Haseeb Bakhtary | h.bakhtary@climatefocus.com

Ingmar Jürgens | ingmar@climcom.org

Kai Dombrowski | kai@climcom.org

Lena Grobusch | lena@climcom.org

Louise Simon | louise@climcom.org

Malte Hessenius | malte@climcom.org

November 2022

Background:DeforestationintheEUTaxonomy

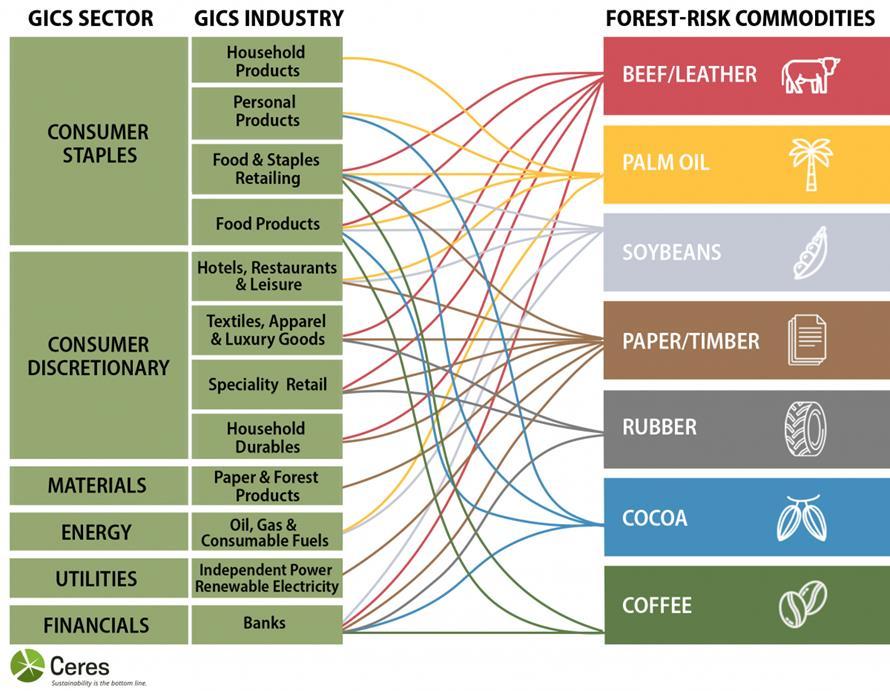

Deforestation is one of the central environmental issues from both a climate change and biodiversity perspective; yet, it represents a particularly tricky challenge for the EU Taxonomy. Deforestation1 is an important threat to the EU Taxonomy’s environmental objectives, not only as a direct result of certain economic activities (such as agriculture, farming,mining or construction), but also because manysectorsandindustriesare(indirectly) responsiblefordeforestationthroughforest riskcommoditiesintheir supplychains(Figure 1)

The EU Taxonomy is structured along different economicactivities andthetechnical screening criteria were developed in parallel by separate sector teams. This made it nearly impossible to capture the complex interdependencies and links across sectors, activities and commodities (as illustrated in Figure 1).

ThisconcernissharedbytheSustainableFinancePlatform: “Environmental objectives such as the circular economy and biodiversity require a systemic approach that allows addressing the entire value chain, rather than an activity oriented structure”.2

We have scrutinized the technical screening criteria of the Taxonomy’s four remaining environmental objectives (Taxo4)fromadeforestationperspectiveandcametothefollowing main conclusions3:

a) The high forest impact activities with a Substantial Contribution (SC) to the Protection and restoration of biodiversityandecosystems(Objective6)havecomprehensivesafeguardsagainstdeforestation,4 b) MostpotentialimpactactivitieswithaSCtoanotherobjectivehavesomesafeguards, c) Butthesesafeguardsvaryandareoftentoolimitedtoaccountfor‘deforestationleakages’

1 as well as the conversion of further primary/high biodiversity non forest ecosystems such as woodlands, grasslands, wetlands and savannahs

2 MethodologicalReport(PartA),p.80.Link

3 Thisscrutinyexaminedthefollowingactivities:(High impact):1.1AnimalProduction,1.2CropProduction,2.5Manufactureoffoodproducts andbeverages.(Potentialimpact)2.4Furniture,2.7Wearingapparel,2.8Footwearandleathergoods,4.1Civilengineering,5.1Newbuildings, 5.2;oftheTechnicalScreeningCriteria(PartB):Link

4 Exceptforasignificantloopholeregardinganimalfeeds,seerecommendation5

November 2022 2

Figure 1: Sector and industry relations to forest risk commodities (Source: CERES) GICS = Global Industry Classification Standard

Based on our analysis and corresponding to the main conclusions, we have derived the following five key recommendations:

• Recommendation 1: IncludeadditionalDoNoSignificantHarmcriteriaforObjective6

• Recommendation 2: Carryoutasector commodityanalysis

• Recommendation 3: Includesupplychainguidance

• Recommendation 4: Alignverificationschemes

• Recommendation 5: ImprovethesourcingrequirementsforanimalfeedsinActivity1.1

In the remainder of this document, we elaborate on each of these recommendations.

Recommendation1:IncludeadditionalDoNoSignificantHarmcriteriaforObjective 6

Currently, the Do No Significant Harm (DNSH) criteria for Objective 6 do not yet systematically account for deforestation. As a first step, activities often reference the generic DNSH criteria of the first Delegated Act (DA), which do neither account for deforestation, nor for supply chain impacts. The Platform indicates that “[r]eferring back to the first DA is not a solution, as some of the generic versions fail to define a specific reference in several sector s.5” Asaresult,certainactivitiesintheTaxo4reportalreadyhaveadditionalactivity specificDNSHcriteriaontopofthe generic DNSH criteria These, however, are not harmonized between activities, and a list of criteria systematically safeguardingagainstdeforestationinthesupplychainsisstillmissing

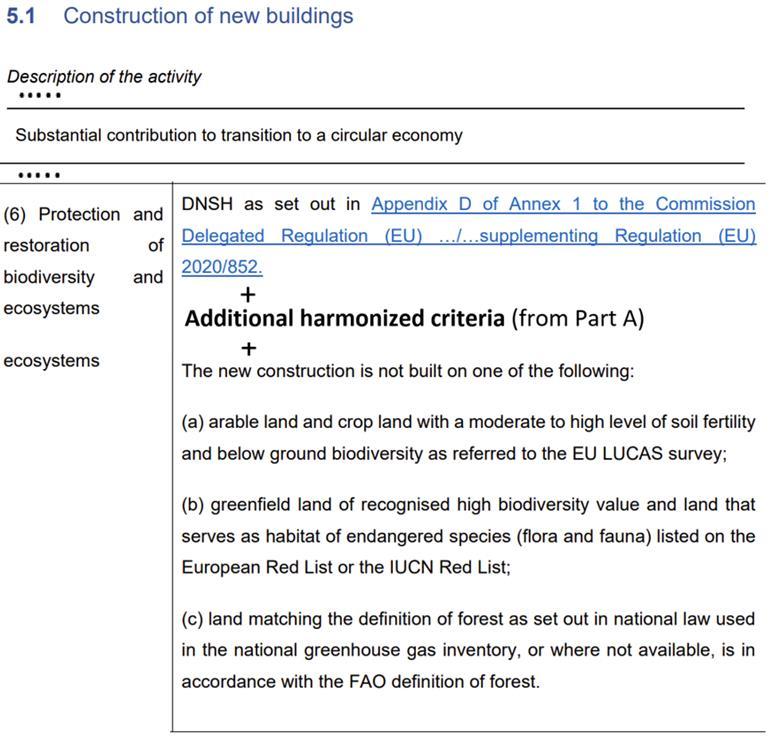

As the generic DNSH on biodiversity of the first DA cannot be modified, we suggest defining a set of additional harmonized criteria to be included in all activities with identified supply chain linkages to forest risk commodities6 . TheseshouldbeconsideredinadditiontothegenericDNSHcriteriaofthefirstDelegatedAct,and theactivity specificadditionalDNSHcriteria (see Figure 2,showinganillustration fortheactivity“constructionof newbuildings”).

There is a great opportunity to safeguard both policy coherence and proportionality by basing these additional criteriaonexistingtextoftheTaxonomyandotherlegislation.Asouranalysisshows,goodsafeguardsarealready in place for certain high forest impact activities, and we recommend building on the “minimum sourcing and manufacturing requirements” for Activity 2.5 Manufacture of food products and beverages7 We also see great synergieswiththeRegulationforDeforestation freeproductstointegratecommodity basedrequirements(which representsyetanothercaseforensuringpolicycoherence).

In line with the above assessment, we propose the following set of Additional Harmonized Criteria:

Theeconomicactivityassuresthat:

• sourced materials were not produced on converted high nature value land, forests, or other lands of high biodiversity value8 since the respective broadly accepted reference period (“cut off date”) for each sourced forest risk commodity;9

• at a minimum, forest risk commodities include soy, palm oil, cattle, cocoa, coffee, wood (the 6 most likely to be in the scope of the Regulation for Deforestation free products), pigmeat, poultry, maize and rubber (the 4 additional commodities likely to be included in the same Regulation);

5 Methodologicalreport(PartA),p.80.Link

6 WesuggesthowtoidentifytheseinRecommendation2.

7 TechnicalScreeningCriteria(PartB),TABLE2,p.179.Link

8 Wetlands,aquatichabitats,moistareas,inorneartobiodiversity sensitiveareas,naturalgrasslands,semi naturalgrasslandsofhigh biodiversity,non productivehigh biodiversitylandscapes.

9 Forexample:‘theAmazonSoyMoratorium’forSoy(withreferencedate2008),and‘theRoundTableonSustainablePalmOil’forPalmOil (with4differentiatedcut offdates);SeealsoAccountabilityFramework’s‘OperationalGuidanceonCutoffDates’ Link

November 2022 3

• if no such reference periods exist yet for certain commodities, compliance with the upcoming Regulation for Deforestation free Products (for which the cut off date is likely to be set for December 31st 2019, 2020 or 2021) is assured; and

• compliance is verified (as a minimum) through the verification schemes to be installed in the frame of the upcoming Regulation for Deforestation Free Products (Art. 14 and 15)10 . 11

GenericDNSHcriteriafromfirstDA

Additional harmonized criteria

Activity specificDNSHcriteria

Figure 2: Example of Additional Harmonized Criteria embedded in a potential forest risk activity

Recommendation2:Carryoutasector-commodityanalysis

TheAdditionalHarmonizedCriteriashouldatleastapplytothehighpotentialdeforestation riskactivitieswehave scrutinized: 2.4 Furniture, 2.7 Wearing apparel, 2.8 Footwear and leather goods, 4.1 Civil engineering, 5.1 New buildings, 5.2 Renovation of existing buildings 12 However, this list is far from exhaustive, considering the Taxo4 consists of around 50 activities, while more activities are being included. Many economic activities have a potential/still unquantified link to deforestation within their supply chain. We,therefore,recommend carrying out a thorough sector commodity analysis13 for all of these activities, to identify which activities require the AdditionalHarmonizedCriteria.

This could be part of the new mandate of the SF platform and should be done together with deforestation experts Alternatively,thesetofadditionalcriteriacouldalsobeappliedtoALLeconomicactivities.

10 RegulationofDeforestation freeProducts,p.43 45 Link

11 MoreonharmonizingverificationschemesinRecommendation4

12 TechnicalScreeningCriteria(PartB):Link

13 Therearealreadyseveralinitiativesthattrytodothis(e.g.GlobalFootprintNetwork,CERES,Encore,Exiobase),butthere isno authoritativesourceyetthatdefinesthiscomprehensively.

November 2022 4

Recommendation3:IncludeSupplyChainGuidance

The Platform acknowledges that supply chains present a challenge to align criteria between different activities14 , and as such stated: “Environmental objectives such as the circular economy and biodiversity require a systemic approach that allows addressing the entire value chain, rather than an activity oriented structure” 15 A strong definition or guidance of how to account for supply chain impacts is still missing and should be included in the Taxo4 report. Much could be integrated from other legislation (existing, or currently in development), which would also serve policy coherence. Table 1 inthe Appendix sets out some suggestions, looking at the Corporate SustainabilityDueDiligenceDirective(CSDDD)andCorporateSustainabilityReportingDirective(CSRD)

Guidance should include the requirement that supply chains of all activities become traceable, back to the origin of sourced materials and commodities. Thetracingshouldbedone(andinformationdisclosed) uptothe granular level needed to exclude significant environmental harm or material risks to cause such harm (in our specific case forest/ecosystem conversion). In some cases, tracing back to the country level is sufficient, inothers tracingbackto thesub nationallevel, source shedofaprocessingfacility,municipalityorevenproductionunitis necessarytobeabletoexcludesignificantharm.16 ThecurrentdraftforESRS1,GeneralPrinciples,Article64gives generalguidanceonboundaries/scopeinordertoidentifywhichrisksandimpactsarematerial(seetable1inthe Appendix) 17

Insomecases,itmightstilltaketimetoacquireandimprovethisdata.TheTaxonomyasanambitiousframework to define what is sustainable should require that Taxonomy compliant activities include active improvement of the traceability of their supply chains (in our case especially regarding the forest risk commodities) year on year (tobedisclosedinthereportingundertheCSRD).18

Regarding policy coherence, we additionally suggest foreseeing a systematic evaluation of the double materiality assessments provided by undertakings through the European Sustainability Reporting Standards (currently developed in the context of the CSRD) toidentifyfurtherpotentialenvironmentalimpactsofdifferent sectors/activities,especiallyinsupplychains,andtoincludetheseinthefutureupdatesoftheTaxonomy.

Recommendation4:Addguidanceforharmonizingverificationschemes

The different verification schemes applicable to each economic activity (as currently proposed in Part B) are very diverse.Wesuggest to conduct a thorough comparative review process on verification schemes to identify the potential for harmonization. Aharmonizedverificationconceptcouldbuildon three verification pillars:1.legal frameworkandverificationmechanismsimplementedintherespectivecountry,2.useofpubliclyavailableand/or governmental data/satellite tools 3. statements/certifications by third parties (e.g. certifiers, traders, and local institutions).

To safeguard against significant harm on forests/ecosystems, there is a high and not yet explored potential to better include know howandinsightsoflocal institutions withgeographical proximity to upstreamactivities.19 The local verification would make data more reliable and less prone to wrongful reporting and thus i) increase

14 MethodologicalReport(PartA),p.72 Link

15 Ibid,p.80

16 This disclosure offers possibilities for accounting/verification. If cross referenced with a land area with forest and/or other natural ecosystemsthathavebeenconvertedinthesourcingitcanbedeterminedifthesourcingareaissubjecttolow orhighriskfordeforestation.

17 CSRD currentdraftforESRS1 GeneralPrinciples(p.15).Link

18 Fordeforestationspecifically,thisshouldincludethe6commoditiesthatareincludedandthe4thatarebeingreviewed(pigmeat,poultry, maize,andrubber)tobecomepartoftheEURegulationondeforestation freeproducts.

19 Forexample:ifacompanydisclosesthatthesoysourcedintheirsupplychaincomesexclusivelyfromspecificproductionunitsinregion x,thathavenotbeendeforestedafter2008,thenthelocalinstitutionwouldhaveto confirmthatthisthresholdwasmaintainedforthe reportingperiodandthattheinvolvedsuppliersdonotengageindeforestationaspartoflandspeculationinotherareasclose by.The disclosingcompanycouldprovideinformationandproofofthelocal verificationprocessaspartoftheirreportand/orsuchcooperation withlocalentitieswouldbecomepartoftheauditors’tasks.

November 2022 5

transparency in the value chain; and ii) complement satellite data in very remote areas and where land tenure schemes are still weak. It would also foster structural strengthening of people andinstitutions in remote areas by grantingthemaccesstobusinessopportunitiesarisingfromtheneedforcompaniestoproofcompliancewiththe Taxonomy(andtheCSRD).Inthecurrentdraft,onlyglobalandexpert drivencertificationschemeswillbenefitfrom theseadditionalbusinessopportunities.

Such an alignmentofverification schemesis similarto recommendation 2 a bigger taskthat could be carried out as part of the mandate of the new Platform.

Recommendation 5: Improve thesourcing requirementsfor animal feeds in Activity 1.1

Activity 1.1 Animal Production, states under Table 3, part 5.1 Limitations on supplementary feed: All livestock that: “When purchasing feeds with large potential upstream impacts, including indirect land use change, for instance soya and oil palm based feeds, selected feeds demonstrably comply with Table 3, Section 1, being certified by a recognised body as not from areas recently converted from natural habitats (from whichever is the earliest date, 2008 or that in the certification).” The standard for animal feeds should be aligned with the sourcing requirements for 2.5. manufacturing of food products.

November 2022 6

Table 1. Guidance on supply chains from the Corporate Sustainability Due Diligence Directive (CSDDD) and Corporate Sustainability Reporting Directive (CSRD)

CSRD currentdraft forESRS1 General Principles (p.15)

Risk. impact under the Material principle and boundary of the CSRD

“Art.63.Theundertaking’sreportingboundaryforits sustainabilityreportingistheoneretainedfor itsfinancialstatementsexpandedtoitsupstreamanddownstreamvaluechain.Associatesandjoint ventures accounted for under the equity method are considered as part of the upstream or downstream value chain. Entities accounted for under the proportional consolidation method are consideredaspartoftheboundaryfortheconsolidatedportion.”

“Art. 64. The undertaking’s reporting boundary is expanded when the integration of information on impacts, risksandopportunitiesonmatters connectedtotheundertakingbyits directandindirect business relationships in the upstream and/or downstream value chain is necessary to: (a) allow usersofsustainabilityreportingtounderstandtheundertaking’smaterialimpactsandhowmaterial sustainability related risks and opportunities affect the undertaking’s development, performance and position; and (b) produce a set of complete information that meets the qualitative characteristicsofinformationquality(seechapter2.1Characteristicsofinformationquality).”

CSDDD, Supply chain due diligence for specific sectors

Article 2 on scope, defines which companies should comply with the CSDDD, based on both companysize,andactivityincertainsectors.TheCSDDDaddressessupplychainDueDiligence,and the list of sectors covered in Art. 2(b) is quite comprehensive and has quite some overlap with the activities covered in the Taxonomy. This would kill two (figurative) birds with one stone as it can provide these activities with supply chain guidance that will be future law for companies anyways, while creating policy coherence with the CSDDD and hence lowering transaction costs for all participants.(p.46)

Supply chain guidance and due diligence compliance

TheCSDDDproposaldefinesobligationsforcompaniesregardingadverseimpactsonenvironment and human rights, stemming from their own operations, their subsidiaries, and operations across the value chain carried out by entities with which the company has an established business relationship

In order to comply with theirduty to apply due diligence throughout their value chains, companies will need to integrate due diligence into their policies; identify actual or potential adverse human right and environmental impacts; prevent or mitigate potential impact; end or minimise actual impact; establish and maintain complaints procedure; monitor the effectiveness of their due diligencepolicyandmeasures;andpubliclycommunicateontheirduediligence(Art.5 11). Studyondue diligence requirements

throughthesupply chain(referred to in CSDDD footnote(8))

Guidance on supply chain and due diligence in the context of business relationships.

“Supply chain” and “value chain”, respectively, will be understood within the broad definition of a company’s“businessrelationships”asdescribedintheUNGPs,andtheOECDGuidelines*.”(p.39).

* = The definition set out the Commentary to Guiding Principle 13 includes “relationships with business partners, entities in its value chain, and any other non State or State entity directly linked to its business operations, products or services to include wider meaning of a company’s business relationships”. It is also noted that the Commentary to Guiding Principle 17 elaborates on the level of due diligence required through the supply chain and value chain: “Where business enterprises havelargenumbers ofentities intheirvaluechainsitmaybe unreasonablydifficulttoconductdue diligence for adverse human rights impacts across them all. If so, business enterprises should identify general areas where the risk of adverse human rights impacts is most significant, whether duetocertainsuppliers’orclients’operatingcontext,theparticularoperations,productsorservices involved,orotherrelevantconsiderations,andprioritizetheseforhumanrightsduediligence”

November 2022 7

Appendix