Berlin, January 2022

Corporate Non-Financial Disclosure:

How can the EU and the US align? A comparative analysis by Climate & Company

Authors1 Christian Bakken Blerita Korca Simon Lehmann-Leo Katharina Erdmann Ingmar Jürgens Amanda Schockling

The authors would like to express their sincere gratitude to Prof. Dr. Frank Schiemann, Theresa Spandel and Raphael Tietmeyer from the University of Hamburg for their valuable comments and insightful contributions. 1

ABSTRACT The objective of this paper is to provide a comparative overview of the current state of corporate non-financial disclosure (or sustainability reporting) in the European Union (EU) and the United States (US). Greater alignment between two of the world’s largest economies on non-financial disclosure could provide the basis for global efforts to increase transparency on sustainability risks, impacts and opportunities. This is only possible if both the EU and the US are willing to work together to improve corporate transparency and accountability. To date, non -financial disclosure is at different stages of development in the US and the EU. While the EU has been enforcing various mandatory requirements for years, learning from implementation and adjusting the policy framework over time, the US is just beginning to plan for mandatory provisions. This study provides an overview of the current state of non-financial corporate disclosure, conceptualizes reasons for greater international alignment, and derives a set of recommendations and potential next steps for both the EU and the US. Elements such as materiality (which sustainability information is material and to whom), scope (who needs to report), disclosure conte nt (what needs to be reported), forward-looking perspective (how best to capture corporates’ transition efforts), assurance, how to deal with non-compliance, digitalization/data sharing, and sub-national regulations are identified as critical junctures for further discussion, with the aim of better aligning non-financial disclosure in the transatlantic sphere. This paper concludes that despite the significant differences between EU and US non-financial disclosure policies, there are strong public and private sector trends towards and economic arguments for greater disclosure, but close bilateral cooperation in the near future and strengthened disclosure standards in the US especially is essential for progress towards a more sustainable economy.

1

DEFINITIONS Mandatory vs. voluntary reporting Whether reporting follows a prescribed and consistent set of regulations with legal obligations or occurs voluntarily, follow ing reporting formats not required by the national authorities (e.g., privately developed reporting frameworks). Entities might be subject to both mandatory and voluntary disclosure measures simultaneously.

Materiality Materiality determines which ESG issues are included in reporting by identifying which ESG issues are “material”. There are two types of materiality: financial materiality (ESG factors and risks are material if they substantially affect the financial performance of the entity) and double materiality (ESG issues are material if they are financially material or if entities have substanti al impacts on society or the environment through their activities around an ESG issue).

Scope The criteria that determine which entities are subject to (“in scope” of) the respective ESG disclosure measure, such as enti ty size, public/private status, or industry.

Disclosure content “What is included” in reporting. Topics covered under ESG, whether reporting is qualitative or quantitative, the level of specificity of reporting requirements, which metrics or KPIs are required.

Forward-looking information and risk disclosure Information companies provide relating to future goals, risks, and activities, especially in the context of climate risk. Distinct and more complex than traditional yearly/quarterly calculations, there are various methodologies for calculating future risk expo sure and measuring expected emissions, some of which may be incorporated into reporting regulations.

Assurance Whether or not firms are obliged to receive verification on their disclosed non -financial information, and the format of this verification (e.g., via third-party auditors).

Reporting standards/frameworks Reporting standards are guidelines for which ESG issues should be reported on and in which manner, both voluntary and mandatory. There are multiple standards developed by different governmental and non-governmental organizations, such as GRI or SASB, with different underlying objectives.

Penalties for non-compliance If a jurisdiction has mandatory reporting regulations, how are entities which fail to meet these regulations treated? Penalties are generally financial in the disclosure context.

2

TABLE OF CONTENTS INTRODUCTION

4

BACKGROUND ON NON-FINANCIAL DISCLOSURE

5

COMPARATIVE PERSPECTIVE

6

Non-financial disclosure in the EU

6

Non-financial disclosure in the United States

8

Non-financial disclosure and data availability in practice

10

ESG disclosure beyond listed companies and beyond climate

11

REASONS FOR INTERNATIONAL ALIGNMENT OF NON -FINANCIAL DISCLOSURE REQUIREMENTS 13 Creating a level playing field

13

Raising the level of ambition

14

RECOMMENDATIONS TO POLICYMAKERS

15

1. Materiality

15

2. Scope

16

3. Disclosure content

16

4. Forward-looking perspective

16

5. Assurance/verification

16

6. Reporting standards/frameworks

17

7. Penalties for non-compliance

17

8. Digitalisation and data sharing

17

9. Sub-national regulations

18

10. Future revision

18

CONCLUSION

19

REFERENCES

20

3

INTRODUCTION After some delay, the United States has agreed, as has the

Given the market-driven surge in activity by financial and non-

European Union, on the goal of zero net emissions of

financial corporates and regulators around non-financial

greenhouse gases by 2050 (Plumer & Popovich, 2021). This

disclosure in the EU (and beyond) and the environmental

goal, under the premise of inclusion of all social groups,

goals of the US’ Biden Administration, now is a crucial period

requires a substantial shift of investments toward more

for developing a common understanding about what

sustainable and less-carbon intensive economic activities. To

determines the effectiveness of ESG disclosure and what

do so, one thing necessary above all is to unleash the power

delivers

and flexibility of the marketplace with good and accessible

Cooperation between two of the world’s largest economies, its

data – or in the words of Nobel Laureate George Akerlof,

administrations, and its political and economic actors ca n set

reducing information asymmetry (Akerlof, 1978) - in this

the stage for a globally coordinated effort toward more

case, about environmental or ESG (environmental, social and

transparency about the sustainability risks of private and

governance) performance. The allocation of scarce resources

public investments in general, and the massive publicly

by market participants as well as environmental, economic,

funded recovery programs. However, this only works if

and financial policies are only as good as the public

administrations on both sides of the Atlantic are able to agree

availability and quality of the information necessary for the

on a common way forward and if they are guided in this

corresponding economic and policy decisions. Therefore, the

process by market participants (to consider their perspectives

disclosure of ESG criteria is the central prerequisite for

on feasibility, market needs and practice) and scientists (to

pursuing this mid-century ambition. The transatlantic sphere

consider the state of knowledge and vast body of research and

offers exceptional prospects for achieving this ambition due

policy evaluation) as to what is required, what is feasible and

to its already deep integration today: in 2019, calculated on a

what is effective in facilitating a shift towards more

historical cost basis, together the US and Europe “accounted

sustainable finance. This paper examines the current state

for 64% of the outward stock and 61% of the inward stock” of

and potential next steps for non-financial disclosure in both

global foreign direct investments (FDI), about 64% of global

Europe and the US to pinpoint key opportunities and

FDI that flowed into the US came from Europe, while 60% of

challenges which need to be discussed by decision makers as

the t otal US global investment position is directed to Europe

part of a transatlantic dialogue on sustainable finance. The

(Hamilton & Quinlan, 2021 p. V-VII).

paper closes with a set of recommendations to contribute to

1

2

the

data

and

transparency

markets

need.

an optimal degree of alignment of non-financial disclosure frameworks between the two regions (and beyond).

1

For the exact geographical definition of Europe in this data please see Hamilton & Quinlan, 2021 p. 173.

4

BACKGROUND ON NON-FINANCIAL DISCLOSURE

Non-financial disclosure 3 is a broad and evolving term, but here we focus particularly on corporate disclosure of data about ESG issues like greenhouse gas (GHG) emissions or labor conditions. Voluntary non-financial disclosure dates back to the 1970s (Hahn & Kühnen, 2013), but has grown enormously in the past two decades following renewed public and policymaker interest in the role corporations play in climate change, deforestation, treatment of marginalized groups, and other sustainable development goals. Various third-party non-financial disclosure standards have emerged (e.g., the Global Reporting Initiative [GRI]; Integrated Reporting [IR]) and are adopted by companies on a voluntary basis. In the wake of this growing interest, a growing number of countries have been turning to mandatory reporting frameworks since 2003 (e.g., Australia, France, UK) (Krueger, Sautner, Tang & Zhong, 2021). Yet, despite these developments, the disclosed sustainability information still varies significantly and is difficult to compare (Cort & Esty, 2020), which limits its effectiveness in terms of enhanced transparency and efficient capital allocation.

•

Forward-looking information and risk disclosure

•

Assurance

•

Reporting standards/frameworks

•

Penalties for non-compliance

How these building blocks are combined to form an effective disclosure framework can differ between regions and respective disclosure measures. Accordingly, rather than attempting to compare the disclosure regimes in their entirety, it is at the level of these building blocks that the following sections present a streamlined comparison of disclosure regimes between the US and the EU, to define key elements of any meaningful transatlantic conversation about cooperation and, eventually, policy coordination and alignment.

Therefore, while non-financial disclosure differs according to national law and accounting frameworks, thanks to the significant experience with ESG disclosure (regulation) around the world and the corresponding, vast body of analytical work, a set of key building blocks have been established as pillars of effective ESG disclosure. They include the following: 4 •

Mandatory vs. voluntary reporting

•

Materiality

•

Scope

•

Disclosure content

In this paper, non-financial disclosure and sustainability reporting (another commonly used term) are viewed as synonymous, given varying approaches to terminology by region, time period, or actor. 4 As defined in Annex 1. 3

5

COMPARATIVE PERSPECTIVE Non-financial disclosure in the EU The EU initiated sustainability-related recommendations for European entities in the early 1990s. Signed in 1992, against the backdrop of the United Nations’ Rio Declaration 5 , the “Towards Sustainability” treaty aimed at promoting sustainable development with a focus on environmental issues (EU, 1992). This program focused mainly on five specific sectors, namely manufacturing, energy, transport, agriculture, and tourism to monitor and assess their sustainable development. Furthermore, the EU started discussing how traditional reporting could better reflect the environmental impacts and non-financial performance in general. As a result, in 2001, the European Commission (EC) issued recommendations on the recognition, measurement, and disclosure of environmental issues in the annual accounts and annual reports of companies (EC, 2001). Moreover, in 2003, the EC extended the focus to social-related disclosure as well. Directive 2003/51/EC highlighted that when appropriate, companies should include environmental and employee information in their annual reports for stakeholders to understand companies’ respective performance. This directive was labelled as the “Accounts Modernization Directive” and has paved the way for future more stringent regulations. 2014 saw a milestone on the EU’s corporate reporting journey, with the adoption of the Non-Financial Reporting Directive (NFRD). The NFRD targets large public-interest companies 6 in the EU with more than 500 employees and mandates the disclosure of non-financial information (EU, 2014). Compared to voluntary disclosure which has been criticized for lacking standardization and comparability (Hibbitt and Collison, 2004; Jeffrey and Perkins, 2013), the objective of the NFRD is to ensure transparency and comparability. Specifically, the

NFRD requires the disclosure of environmental, social, employee, human rights, and anti-corruption and bribery matters (see Table 1). In a first step to supporting companies improve the quality and relevance of their non-financial disclosures, the EC in 2019 issued non-binding guidelines. More recently, criticism has been emerging about the guidelines’ effectiveness (Masiero, Arkhipova, Massaro, & Bagnoli, 2020; Korca and Costa, 2021) and several studies identified shortcomings of the NFRD (See Korca et al., 2021; Matuszak & Różańska, 2017; Tarquinio, Posadas & Pedicone, 2020). Against this backdrop and in light of an increasing body of research confirming the superiority of mandatory over voluntary disclosure in providing higher-quality data to investors (Kalesnik, Wilkens & Zink, 2020), the European Commission initiated a revision process for the NFRD in 2020 (EC, 2020). In April 2021, the EC tabled a proposal for the Corporate Sustainability Reporting Directive (CSRD), including significant changes to the EU’s mandatory reporting framework. The CSRD, if adopted in its current form by the colegislators (i.e., the European Council and Parliament) will expand the reporting scope from all large companies to all listed companies (including listed SMEs) by removing the threshold of 500 employees. Furthermore, the new directive adds requirements such as supply chain disclosure, digitalization of information, mandatory assurance, and forward-looking disclosure (see Table 1), which are highlighted as relevant in the vast and growing body of scientific literature on disclosure. For instance, assurance of non-financial disclosure facilitates access to financial capital (García‐Sánchez, Hussain, Martínez‐Ferrero & Ruiz‐Barbadillo, 2019) and decreases capital market information asymmetries (Fuhrmann, Ott, Looks, Guenther, 2017). Furthermore, forward-looking disclosure is useful to all stakeholders to better understand companies’ targets for the future (Kiliç and Kuzey, 2018). Therefore, the CSRD aims to significantly

https://www.un.org/en/development/desa/population/migration/generalassembly/docs/globalcompact/A_CONF.151_26_Vol.I_Declarati on.pdf 6 The definition of large companies is taken from the Accounting Directive which defines large undertakings as those exceeding at least two of the three following criteria: i) a balance sheet greater than EUR 20,000,000, ii) a net turnover of more than EUR 40,000,000 and iii) an average number of employees above 250 throughout the financial year. 5

6

improve availability and quality of sustainability information (EC, 2021a) and respond to concerns raised by market participants and stakeholders in general.

Table 1. Overview of NFRD and CSRD

In contrast to the NFRD, which did not lay down specific reporting requirements (Masiero et al., 2020; Korca & Costa, 2021), the CSRD aims to set clearer requirements. In this regard, the European Financial Reporting Advisory Group (EFRAG) is developing the EU reporting standards for all entities falling under the CSRD scope. In contrast to the nonbinding guidelines for the NFRD, the EU reporting standards will be mandatory and tailored to specific industries and company size. In addition, companies complying with the

CSRD will have to report in line with the Sustainable Finance Disclosure Regulation (SFDR) (EU, 2019) and the EU Taxonomy Regulation (EU, 2020). The SFDR aims to increase transparency on sustainability matters by targeting financial institutions and market participants. Specifically, from March 2021, the SFDR requires disclosure of sustainability information both at the entity and product level.

The EU Taxonomy Regulation entered into force in July 2020 setting out six main objectives which entities must meet to be classified as environmentally sustainable. The EC continues to require companies to measure the impact and identify risks and opportunities related to non-financial aspects. While the previous regulations on non-financial disclosure received criticisms on several aspects, the upcoming directives such as the CSRD might overcome some limitations of previous regulations.

7

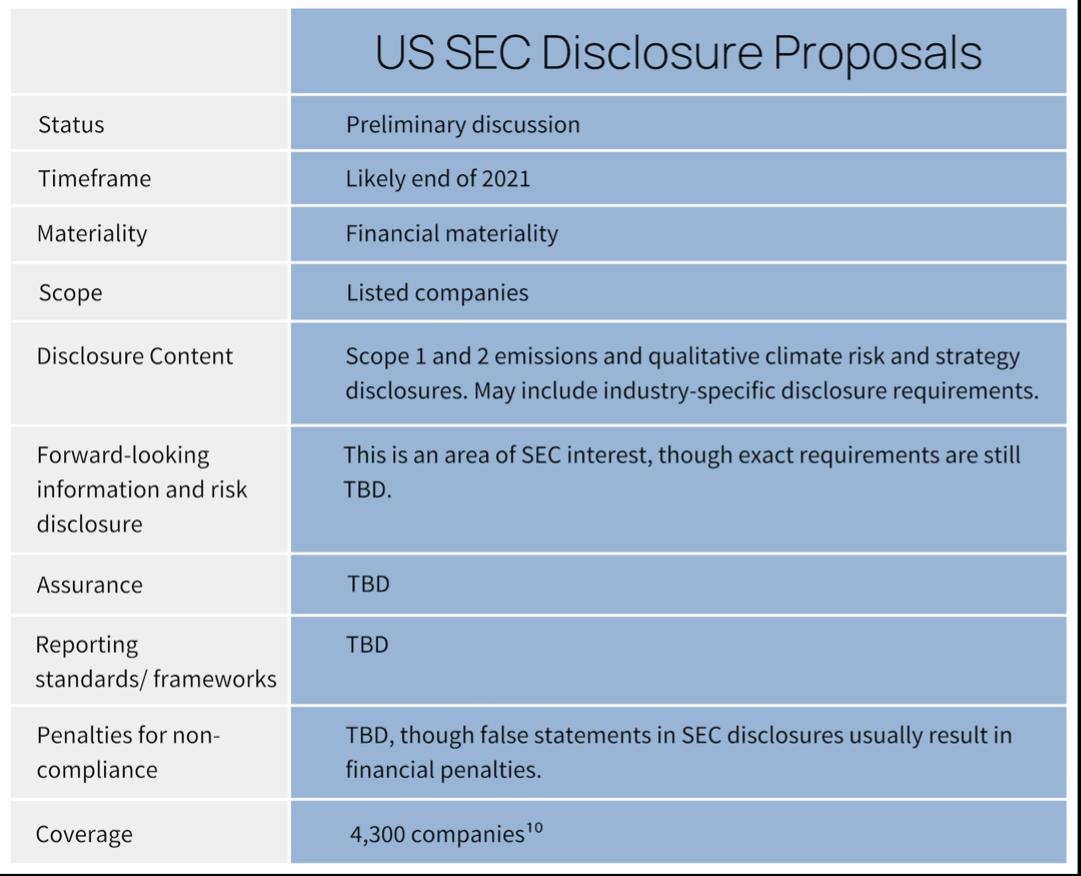

Non-financial disclosure in the United States The Securities and Exchange Commission (SEC) has authority over the type and content of reporting required for US listed companies through Regulation S-K, part of the Securities Act of 1933. Regulation S-K covers qualitative disclosures and is mandatory for all companies registered with the SEC. Per SEC guidance in 2010, principles-based (e.g., qualitative) climate change disclosure (and other material environmental considerations) could be covered in one or more of Item 101, Description of Business; Item 103, Legal Proceedings; Item 503I, Risk Factors; and Item 303, Management’s Discussion and Analysis (SEC, 2010). Environmental litigation and compliance are well-established components of these disclosures and climate change-related risks may be included if financially material to the business (Cleary Gottlieb, 2020). However, reporting on climate change and other ESG factors without clear material risks to the company are not legally required and even material disclosure is insufficiently enforced (Gelles, 2016). As a result, these are still inconsistently incorporated in SEC reporting, even as voluntary but non-standardized non-financial disclosure is increasingly common (Lee, 2020). The Sustainability Accounting Standards Board (SASB), a nonprofit organization, has developed a set of standards outlining financial materiality for sustainability issues in different industries tailored to SEC reporting requirements. However, in 2020 less than 350 U.S. companies reported using SASB, almost all in sustainability reports separate from their regulatory filings (SASB, 2021). 7 Separately, the Environmental Protection Agency (EPA) requires direct GHG emission reporting for facilities with large emissions under the Greenhouse Gas Reporting Program (GHGRP) authorized under the Clean Air Act (40 C.F.R. §98.2). This data is publicized at the facility level but is not aggregated by company, nor does the GHGRP require data collection for smaller emitters or incorporate Scope 2 or 3 emissions. 8 Many companies also collect emissions data for participation in state or regional emissions trading schemes (e.g., the Regional Greenhouse Gas Initiative in 12 Northeastern states). Thus, although specific climate or other environmental qualitative or quantitative data at the corporate level is not required due to federal-level regulations

in the US, many large companies have experience collecting emission data at the facility level. Therefore, adapting that to other disclosure mandates, which require data on an aggregated level, would not be especially burdensome, especially given the prevalence of voluntary non-financial reporting among major US companies (KPMG, 2020). As discussed above, the SEC has broad legal authority to adopt more stringent standards for non-financial disclosure, even if ESG-related reporting is not explicitly prescribed at present. The SEC has been active early in the Biden Administration gathering public input and strengthening an in-house focus on ESG. A recent request for public comments on climate change disclosure received over 5,000 responses and was open to comments both on adapting Regulation S-K (and its counterpart Regulation S-X, which deals with quantitative financial reporting requirements) and potential new regulations (Lee, 2021). These may include industryspecific disclosures, standalone sustainability reports, or mandatory compliance with global standards, among others. The SEC or other US actors (e.g., the Department of Treasury or the Federal Reserve) have not signified preference for any existing disclosure standards but have demonstrated clear interest in international cooperation and alignment for any upcoming rules (Shalal & Lawler, 2021). Given these actions and public commitments from the Biden Administration to expanding ESG disclosure such as an executive order in May 2021 directing all US financial regulatory bodies to review and develop strategies for treatment of climate risk in the US financial system (The White House, 2021), new SEC rules are highly likely to be implemented under the administration, with current expectations for detailed proposals to be released in 2022 (Quinson, 2021; Nicodemus, 2021). In September 2021, the SEC released a sample letter to public companies detailing several areas of interest within climate risk – outlining specific climate-related risks and costs to be included, asking for detail on carbon offsetting/credits, and probing disclosure alignment between SEC reporting and voluntary ESG reports (SEC, 2021). In October 2021 the Biden Administration released a whole-of-government strategy to address climate risk building off the earlier executive order and announcing new proposed rules or practices on climate risk considerations for insurance, pensions, public company reporting, public lending, federal procurement, federal budgeting, and infrastructure (White House, 2021). However,

2020 used as most recent full year of data availability. Reporting increased in 2021, with approximately 400 companies listed to date, though several of these companies are not publicly listed or are headquartered outside the U.S. 8 Scope 2 emissions are emissions from purchased electricity, heating, and cooling. Scope 3 emissions are emissions produced upstream in a product’s lifecycle (e.g., via raw material production). 7

8

the rulemaking process may last several years during which time stakeholders will have the opportunity to provide additional comment on the proposed regulatory text (US Courts, n.d.).

Table 2. US Disclosure Proposals (Quinson, 2021)

9

While disclosure mandates can be implemented through the SEC’s regulatory authority, legislative mandates such the recently passed House bill (HR 3623) mandating ESG disclosure would strengthen these requirements from future litigation or a change in executive administration (Weiss, 2021). Additionally, other financial regulatory bodies have their own authority on disclosure requirements that can be applied to their regulated products (e.g., the Commodities Futures Trading Commission (CFTC) with derivatives) (Latham & Watkins, 2021). A broadened GHGRP is possible under the Biden Administration but has not been publicly discussed to date, however the SEC’s potential actions would align more directly with international corporate disclosure mandates. State-level disclosure requirements (e.g., in California) may also be implemented, especially if Congressional action continues to be obstructed (Broome et al, 2021). Disclosure requirements at major US stock exchanges are also likely. 9 Table 2 summarizes potential disclosure requirements under the SEC but is subject to significant change given the early stage of these proposals. Currently, the state of play of ESG disclosure measures significantly differs between the EU and the US. While ESG disclosure in the EU is mandatory for large entities (soon for all listed entities with the CSRD), in the US it is still treated as voluntary due to inconsistent measurements of materiality. 10 Regardless of the national regulations, ESG data is available from data providers which usually collect information from reports provided by companies, either on a mandatory or voluntary basis. The following section offers empirical insights of non-financial disclosure in practice, in both the EU and the US, despite the different regulatory setting.

Non-financial disclosure and data availability in practice

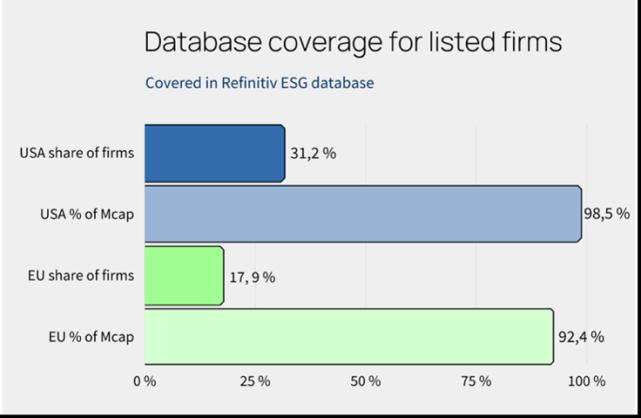

transparency. This can have various reasons, for example, because the respective regulations are not specific about the precise disclosure content, the authorities do not enforce the regulations, or companies face difficulties in (and are not sanctioned for delays in) implementation (e.g., due to limited resources). Furthermore, the extent of voluntary disclosure plays a crucial role, implying that differences in data availability between the EU and the US might not be as significant as the different regulatory environments suggest. The global context shows that disclosure requirements often lack specific key performance indicators (KPIs), do not define the materiality perspective, and that assurance is rare (IPSF, 2021). These factors could contribute to the p roblem that disclosure requirements could still lead to non-comparable and incomplete ESG data. Professional investors usually rely on data providers for their company assessment. To analyze how well data is accessible for them, it is thus not sufficient to outline the currently implemented sustainability-related disclosure measures but to examine ESG data availability in databases which are used by investors. Through a descriptive empirical analysis with data derived from Refinitiv, which includes a database for ESG data (formerly Asset4, in total including over 400 individual ESG-related variables) 11 , the availability of sustainabilityrelated variables is presented. Figure 1 shows that although only a third of US listed companies is covered by the ESG database, this represents 98% of US market capitalization. While the firm coverage for the EU is lower, a similar picture evolves: Over 90% of the market capitalization is covered. Since market capitalization is not the only driver (or explanatory variable) for corporate carbon emissions, many firms with a high impact on, for example, global warming, may be not included in the database.

Although regulation is considered as one of the main drivers of ESG data availability (Juergens and Erdmann, 2020; CDP & CDSB, 2018), it does not automatically generate full market

E.g., the NASDAQ’s August 2021 rule regarding board diversity reporting (NASDAQ, 2021). The SASB provides definitions of financially material sustainability impacts but is not universally adopted or explicitly endorsed by the SEC or other regulators. Even among companies providing non-financial disclosure, about 50% of SECregistered companies provide fairly generic or boilerplate sustainability information in their regulatory filings (Christensen, Hail & Leuz, 2018). 11 The database is based on publicly available company data. When a firm is included in the database, this does not imply that individual ESG data points are available. 9

10

10

Figure 1 – Database coverage US and EU

Figure 1 shows the share of firms that is covered (as of August 2021) in the Refinitiv ESG database and which share of market capitalization (Mcap) the covered firms represent. It is differentiated between share of firms and market capitalization, because the absolute number of covered firms does not show how large these firms are and what share of the domestic capital market is covered. The database only covers firms for which ESG data is publicly available. The sample of firms consists of all active and listed firms in the US and the EU.

However, if a firm is covered by the ESG database, this does not mean that (all) individual data points are available. Figure 2 shows the data availability of 2019 data for selected individual data points. The data coverage regarding the share of firms and by market capitalization is considerably higher for the EU than the US. CO 2 emissions are crucial to track the climate impact of companies. However, this data is available for less than 6% of the firms listed in the US. Nevertheless, these firms represent over two thirds of market capitalization. Over 11% of EU firms, representing 80% of market capitalization, have available data. A similar picture evolves for other ESG disclosure building blocks; the information about the presence of assurance, if there is a link to disclosure standards/frameworks (e.g., GRI or SASB), and the availability of forward-looking information. The overall picture shows that even though the share of covered firms is lower for EU firms (Figure 1), more specific information is available. On the one hand, the lower data availability of specific ESG information, such as emission data or information on the presence of assurance, for the US might be due to fewer disclosure requirements. On the other hand, the descriptive statistics showed that a high number of large firms in the US is covered in the database. Therefore, many firms already disclose sustainability data even in absence of a specific disclosure regulation, which suggests that the

implementation of a mandatory disclosure regime would not come without an additional burden for these firms. Further, the finding that the data availability for specific data points is limited for the US non-financial disclosure regime is in line with the academic literature, which presents a lack of comparability and standardization without mandatory disclosure (see, e.g., Hibbitt & Collison, 2004; Jeffrey & Perkins, 2013; Korca & Costa, 2021). The insights from the descriptive analysis above are supported by other studies. For example, a recent survey showed that 98% of the 100 largest US companies by revenue report sustainability information (KPMG, 2020). Specific mandatory reporting could increase the comparability between and level of detail of the already existing information and would extend the data availability beyond only the largest companies.

Figure 2 – Availability of specific data items

Figure 2 shows the availability of specific data points for the US and the EU. All data was retrieved from Refinitiv and represents data for 2019. The specific data points were chosen along the building blocks described above. The sample of firms consists of all active and listed firms in the US and the EU.

ESG disclosure beyond listed companies and beyond climate The ESG disclosure building blocks “Scope” and “Content” are crucial for the discussion about disclosure in practice. In most jurisdictions, (mandatory) reporting requirements are restricted to large, listed firms. However, in many economies, small and medium sized enterprises (SMEs) are of major importance (Clark 2021) and have a high impact on climate- or

11

other sustainability-related factors. SMEs represent 44% of GDP in the US and 56% in the EU (US Small Business Administration, 2019; Statista, 2021). In some carbonintensive sectors, for example, agriculture, the number of large, listed entities is low (WPSF, 2021). To achieve overall transparency, it is therefore not sufficient that disclosure focuses on large, listed firms. For instance, in the US, 10% of all greenhouse gases are emitted in the agricultural sector (EPA, 2019) where most firms have less than 500 empl oyees (SUSB, 2018) and would thus not be addressed by reporting regulations targeted at large companies. Within the EU, the CSRD takes a first step towards including SMEs in reporting regulations (WPSF, 2021). Furthermore, disclosure should not only focus on climate, but should also address other environmental dimensions, such as biodiversity or water. So far, it was shown that although the relative coverage of firms in the ESG database is higher for US listed firms, the availability of specific information items (see Figure 2), is higher for EU firms. One way to increase data availability, is to extend the scope of reporting regulation beyond large and listed firms towards ESG disclosure by SMEs, in particular those in high environmental and social risk/impact sectors. Besides the benefits of mandatory ESG disclosure for any individual constituency discussed above, there is a particular case to be made in favour of international alignment and comparability, which need to be considered when taking a comparative (EU-US) perspective.

12

REASONS FOR INTERNATIONAL ALIGNMENT OF NON-FINANCIAL DISCLOSURE REQUIREMENTS

Ideally, the degree of internationalization of regulation aimed at reducing negative externalities of economic activity, for example via enhancing the public good of efficient financial markets by reducing information asymmetries, should be consistent with the degree of internationalization of the respective economic activity causing these externalities. This holds true for financial stability (Schoenmaker, 2013) as well as for environmental stability 12 . However, whereas closed economies in conjunction with national standards still allow for a stable economic and financial system (Rodrik, 2000) the outcome for global public goods such as climate is less favorable. So, how much international economic policy integration is needed in terms of common standards for nonfinancial disclosure to overcome the collective action problem?

Creating a level playing field One perspective is to create a level playing field. From a sustainable finance perspective, financial markets need to become more interconnected and integrated: accelerating private cross-border risk sharing and capital flows is essential for completing the European Capital Markets Union (Bhatia, Mitra, & Weber, 2019) and even more so in the transatlantic sphere. This requires, among others, enhancing data availability and comparability. “Exchanges that cross national jurisdictions are subject to a wide array of transaction costs introduced by discontinuities in political and legal systems” (Rodrik, 2000, p. 179) and thereby pose limitations to further

global economic integration, welfare gains and efficient capital allocation that all would, when set in the right direction, contribute to a successful green transition. It is therefore imperative to provide for a level playing field for the disclosure of non-financial information in order to prevent companies from avoiding sustainability valuations and to deter regulatory arbitrage and free riders, and effectively implement sustainability policy goals that might otherwise be hindered by mobile factors of production, e.g., via carb on leakage. The responses to the global financial crisis show that the creation of a global regulatory framework is indeed feasible under favorable conditions. In addition to the Basel Committee and the Financial Stability Board’s alignment of disclosure and reporting requirements for significant credit institutions as a minimum requirement to improve financial stability, another analogy between central banks’ financial stability policy and carbon pricing is ensuring credible forward guidance (Group of Thirty, 2020). If financial markets know in advance, with reasonable certainty, the path for international carbon pricing, they may anticipate adjustment because they have a better sense of the corresponding cash flow implications. Managing the macro-level transition, therefore, requires the necessary empirical micro-level database for sustainability that is further aggregated and risk-adjusted by market participants such as sustainability rating agencies. Several approaches to international non-financial disclosure exist, varying in terms of scope and materiality (Adams & Abhayawansa, 2021). EFRAG’s cooperation with GRI is described above; the IFRS Foundation also announced the establishment of a new board based in Frankfurt to deliver a “global sustainability reporting baseline” (IFRS, 2021) in order

A distinction should be made here between the degrees of internationalization in the regulation of negative externalities of climate, water, and biodiversity, the latter being clearly more local, and a desire to make the financial resources internationally available to thus provide positive externalities, an internationally functioning capital formation, to mitigate the previous negative externalities and invest in economic transformation. 12

13

to enable greater comparability and consistent application of the standards. 13 The US, however, does not require domestic reporting according to IFRS standards, which underlines the need for stronger multilateral alignment in a context of lessthan-global carbon pricing. As US Treasury Secretary Janet Yellen has suggested, the US could join the International Platform on Sustainable Finance or work through bodies such as the G20 to facilitate further alignment based on the TCFD recommendations (SSE, 2021).

Raising the level of ambition Another perspective is to lead by example in raising the level of ambition. Any substantial increase in unilateral disclosure requirements above an inter- or multinationally agreed baseline would risk being criticized as a protectionist measure favoring domestic businesses. Yet a shift from an origin-based environmental policy to a destination-based framework could trigger a race to the top in non-financial disclosure practice. This is because domestic polluters would not pay differently for domestic emissions depending on whether the goods and services produced are sold domestically or on the global market. In a destination-based policy, each polluter, regardless of origin, must pay when the goods and services are routed to the domestic market (Aussilloux, Bénassy-Quéré, Fuest & Wolff, 2017). This paves the way for economic incentives that promote greater upward convergence of disclosure regulation and practice over time, combining reduced disparities between disclosure frameworks with an overall improvement in the level of ambition (Barro & Sala-iMartin, 1992). Businesses’ and in particular multinational companies’ preferences for unified disclosure requirements provide important backing and hence leeway for like-minded jurisdictions to move toward policy coherency at a level commensurate with the corresponding climate and sustainability challenges. Thus, comprehensive non-financial disclosure will be a crucial tool for addressing these challenges. Doing so would represent a considerable step further towards a system of international pricing that

preserves the price signal of sustainability risks in financial market transactions and hence promotes the more efficient and risk-adjusted allocation of capital. Notably, the EU has with its Fit for 55 package proposed to establish a Carbon Border Adjustment Mechanism that, while still vague on detail, will need to be WTO-consistent and dovetail with the current strategy on carbon pricing, especially the ETS. Its success and impact on disclosure is highly dependent on international climate policy equivalence and the ultimate sectors covered (Sapir, 2021). While enhancing disclosure requirements may be regarded as burdensome in the US, on the contrary, disclosures strengthen the ability of the market to select for positive non-financial performance by reducing information asymmetries. Given existing investment trends favoring ESG, this not only lowers the burden on investors in reducing uncertainty but can replace other top down regulation that may be otherwise necessary to achieve this net-zero goal with even higher corporate cost. In addition, a 2019 call by numerous U.S. economists to introduce a carbon border adjustment system in the US (Climate Leadership Council, 2019) and the moderate reactions from Washington to the EU Commission’s draft (EC, 2021b) might set the scene for further cooperation. A collective EU-US framework of border mechanisms or different approaches with similar levels of ambition that would thus allow for equivalence and exceptions of border taxes would create important incentives for internationally oriented companies worldwide to invest in low-carbon technology. Deepening and connecting the transatlantic financial markets while at the same time mainstreaming transatlantic sustainable finance is deeply intertwined with a transatlantic green trade agenda, which all seem increasingly feasible as it is the cost of “zero ambition” (Carney 2021, p. 1) and not zero emission, that is too high to bear. These various initiatives raise optimism that further convergence of disclosure standards between the EU and the US and equivalence of sustainability regulation can emerge, potentially allowing for a higher degree of integration between these two major economies.

Also refer to the “Statement of Intent to Work Together Towards Comprehensive Corporate Reporting” (2020) by the Carbon Disclosure Project (CDP), the Climate Disclosure Standards Board (CDSB), the Global Reporting Initiative (GRI), the International Integrated Reporting Council (IIRC), and the Sustainability Accounting Standards Board (SASB). 13

14

RECOMMENDATIONS TO POLICYMAKERS

Non-financial disclosure policies in the EU and the US are moving forward, even if currently the EU’s policies are at a more advanced stage. Given the current gulf between the two sides of the transatlantic relationship and the lack of transparency, significant effort is needed to standardize and enhance reporting requirements, especially within the US. We recommend the US to align any new regulations as closely as possible with the CSRD, as two differing standards would increase the compliance burden on businesses, decrease information comparability for investors or other corpo rate stakeholders, and complicate the work of regulatory authorities. This aligned framework can also form the basis for future cooperation between the US and EU on ESG issues. This is not to discount advanced disclosure standards in countries outside the US or EU or developed by third parties such as the SASB or GRI – expanded cooperation and broader alignment is highly valuable. But given existing challenges transnational corporations have adapting data to multiple disclosure standards (Bakken, 2021), one overarching standard is preferred, and the US and the EU have the economic and political clout to lead development of this standard – a clout that may diminish if action is delayed given their predicted declining share of global GDP in upcoming years. While the CSRD is a work in progress, it is based on many years of experience with its predecessor, the NFRD. This experience has resulted in greater EU institutional knowledge around non-financial disclosure and an existing regulatory setting that large companies are already adapting to, and as such should serve as the starting point for reporting alignment. Given corporations are already adapting to the CSRD and Taxonomy in the EU, the US’ adaptation of similar guidelines in the near future would result in a largely level playing field instead of forcing US companies to catch up at a later date; non-EU companies could leapfrog intermediate steps to a clearer and more relevant final stage of non-financial disclosure. This level of international financial cooperation has clear precedent with the work of the Financial Stability Board, the convergence of international accounting standards under IFRS, and regular discussion of financial and environmental affairs through the G20 and other global forums.

The following elements are critical areas of discussion, incorporating both the ESG disclosure building blocks and few other key considerations:

1. Materiality Overview: Traditional disclosure is based on financial materiality only, but the growing interest in non-financial disclosure is linked to the emerging adoption of double materiality. Climate and other ESG issues are rarely incorporated within current financial materiality standards in the US. Adopting a double materiality principle in the US could increase the salience of non-financial data and help with filling the data gap for investors with ESG performance and impact preferences in relation to their investments. Key Questions: With materiality definitions playing such a crucial role in determining the content and comprehensiveness of non-financial disclosure outcomes, how should materiality guidance be structured to ensure equal treatment of companies regardless of size or industry? Should the US adopt the EU’s double materiality principle? Recommendations: We recommend the US to adopt a double materiality principle in order to broaden the scope of material ESG information disclosed and align itself with emerging global trends in this direction. In the EU, double materiality was more systematically introduced through the non-binding nonfinancial reporting guidelines to comply with the NFRD (EU, 2017) and would become mandatory with the adoption of the CSRD proposal. In the long-run, when all externalities are adequately priced and public awareness is rising, the outside in and inside-out perspective is likely to converge. But as this may take a very long time, it will be important to facilitate transparency about the impacts of a reporting entity on its natural and social environment, and/or, to inform investment decisions in line with individual sustainability/ESG preferences (e.g., for so called “impact investors”).

15

2. Scope

more than the EU based on political or economic interests (e.g., diversity)? On which KPIs to focus?

Overview: As shown above, a significant share of the economy and emissions in both the EU and the US is derived from SMEs or non-listed companies. In the EU, the CSRD proposal would significantly expand the number of companies required to report ESG information, including all large and all lis ted entities (including SMEs). SEC regulations on the other hand apply to publicly listed companies only (just as the NFRD previously did in the EU).

Recommendations: We believe in all parts of non-financial disclosure, the US should adopt an ambitious reporting structure that aligns as closely as possible to the EU Taxonomy, in order to avoid falling more behind in this important field or neglecting key ESG considerations. However, we recognize the challenges in adopting a similarly strict taxonomy in the US context so any ESG reporting requirements in the US would be an improvement from the current status. However, we also support mandatory disclosure for certain ESG KPIs (e.g., GHG emissions, energy use, gender wage gap, etc.) to promote a level playing field. Regulations should outline the specific KPIs to promote greater consistency and comparability and limit risks of misleading or ill-defined data.

Key Questions: Will the US find ways to require (public) reporting from non-listed companies, even if this goes beyond the SEC’s regulatory authority? Is the CSRD’s proposal of a simplified reporting standard for SMEs a reasonable compromise for US policymakers wary of adding regulatory burden on small business or should the US go beyond the CSRD in applying requirements to SMEs? 14 Recommendations: We recommend for ESG reporting requirements to apply to all entities based on the materiality of ESG factors, not its legal status of public or private company, to achieve transparency among entities with the highest (potential) ESG impacts and risks. Reflecting the principle of proportionality and in line with the CSRD proposal, we recommend for the US to consider simplified reporting standards for SMEs.

3. Disclosure content Overview: ESG data and disclosure cover a broad range of environmental, social, and governance factors related to business activities, but not all ESG factors are equally relevant for or affected by all businesses. Current US proposals focus primarily on climate reporting, while the EU Taxonomy and CSRD cover multiple environmental (and social) areas. Moreover, the EU Taxonomy and the CSRD define clear key performance indicators (KPIs) which increase the comparability of the disclosures. Key Questions: Can the US incorporate the EU Taxonomy or its covered issues into its own frameworks or is it preferable to start with aligning climate reporting, which is more developed in both regions? Are there ESG issues the US may prioritize

4. Forward-looking perspective Overview: In the EU, the taxonomy and disclosure discussions have been very much focused on how sustainable finance can help companies to transition out of harmful activities and, where possible, to green or sustainable practices. As a result, the CSRD introduces requirements on more forward -looking disclosure. Key Questions: In how far can mandatory disclosure capture the ability and intention of the reporting entity to transition toward a better ESG performance (such as carbon neutrality by 2050)? How are sustainability targets set? Recommendations: We support clear rules and presentation of evidence for forward-looking statements. Research shows that forward-looking statements such as setting targets could induce better sustainability performance in the future (Rezaee & Tuo, 2017). Therefore, disclosure of forward -oriented information could better highlight companies’ objectives and allows to assess their achievements in the future.

5. Assurance/verification Overview: Assured non-financial data is more valuable to

SMEs represent 44% of GDP in the US and 56% in the EU (US Small Business Administration; Statista). Accordingly, attempts to green the economy will be incomplete without addressing impact from SMEs, but policymakers in both jurisdictions traditionally feel pressure to avoid burden on these businesses. 14

16

investors and regulators alike and financial reporting is traditionally subject to assurance requirements. The CSRD introduces mandatory assurance for non-financial disclosure in the EU. However, there are no mandatory third-party assurance requirements for non-financial disclosure in the US. Key Questions: Should third-party assurance of non-financial data be mandatory in the US? Should assurance apply to qualitative reporting as well? If so, at what level? Recommendations: In the long term, we recommend the same assurance requirements for financial data in the US apply to all non-financial disclosure, both for qualitative and quantitative data. We recommend non-financial disclosure be incorporated into annual regulatory filings (e.g., 10-K reports), which are already audited. As a first step in this direction, an audit of non financial information, which only includes consistency checks, could be introduced. Similarly, we recommend that the EU sticks to their CSRD proposal on mandatory assurance for all entities in all member states, in contrast to the NFRD which allowed member states to make changes on this aspect when transposing the regulation into national laws.

7. Penalties for non-compliance Overview: Meaningful penalties for non-compliance and consequently, non-disclosure, are very likely to improve compliance and put pressure on companies with inaccurate or incomplete reporting. But given the novelty of non-financial reporting in certain contexts, penalties should not be excessively harsh and should be proportionate to those for existing financial reporting. Key Questions: Will strengthened reporting requirements be accompanied by strengthened enforcement? Will the urgent demands of the green transition spur stricter penalties? Recommendations: Both the EU and US should carefully scrutinize non-financial reporting to confirm it aligns with the CSRD and US regulations as implemented, though some leeway should be allowed as companies adapt to a new regulatory framework. Egregious failure to disclose accurate non -financial data should result in significant penalties to ensure adequate compliance. Given the novelty of non-financial reporting in certain contexts, penalties should not be excessively harsh and should be proportionate to those for existing financial reporting.

6. Reporting standards/frameworks Overview: Existing third-party reporting standards such as GRI or SASB could provide a widely accepted and mutually agreeable reporting framework in both the US and EU, as could reporting standards under development by IFRS and others. In the EU, the EFRAG is co-working with the GRI to develop the EU sustainability reporting standards. Key Questions: However, do these existing frameworks meet the higher ambitions of the European Green Deal and connected legal frameworks and align with realistic reporting pathways in the US? How should regulators select a standard and what are the benefits and disadvantages of third-party vs. internally developed standards? Recommendations: We are cognizant of legal differences between the US and the EU, but support using the same framework for the reasons outlined in the introduction of this section. Research shows that when companies report with no clear guidelines and use different reporting frameworks, the information might be cherry-picked and thus limit comparability (Korca & Costa, 2021; Bingler et al., 2021). We do not take a stance on which existing framework is preferable as the final result may be one that does not currently exist.

8. Digitalisation and data sharing Overview: The analysis above showed that data availability is limited and often restricted to firms with the highest market capitalization. However, market capitalization is not necessarily correlated with the carbon footprint or other sustainability-related variables. The CSRD introduces for the first-time digital tagging of sustainability information through the European Single Access Point. In the US, the EDGAR database applies to financial data. Key Questions: Will the US adopt similar digital formats and/or expand existing ones? Can reporting templates and databases be linked in a way that facilitates data exchange between governments and/or streamlines data analysis for third-party reviewers of corporate reports? Recommendations: We encourage the US to clearly delineate form and content of non-financial disclosure to streamline data analysis within the US and continue conversation to improve data comparability, though significant updates to the technical requirements in the US might not be realistic at this time. One possibility would be to expand the EDGAR database to cover non-financial data.

17

9. Sub-national regulations Overview: EU member states can go beyond the CSRD and other EU regulations, while US states can also develop their own disclosure requirements. In some cases (e.g., California) sub-national actors have led climate and regulatory action. However, independent action by sub-national actors may further fragment the market instead of promoting alignment. Key Questions: How can alignment be maintained when taking these semi-distinct actors into account? Recommendations: We recommend the US and the EU maintain ambitious-enough requirements to preempt additional activity at lower levels of government. However, we also recommend incorporating state-level policymakers or state feedback in EU-US planning discussions to be aware of their interests and goals and thus develop policy measures which consider and satisfy state-level needs.

10. Future revision Overview: ESG is a rapidly evolving field in both political and financial contexts. As the transition from the NFRD to the CSRD shows, changing goals and practices will likely create openings for future regulation in both the US and the EU. Key Questions: How will the US and the EU continue their partnership and communication on these issues in future years in order to ensure existing regulations continue to meet stakeholders’ needs? Recommendations: We recommend non-financial disclosure to be included as an annual discussion topic in G-20, G-7, and other multilateral or bilateral interactions on related fields. We recommend non-financial disclosure be managed by organizations that are largely independent of political changes to reduce the impact of electoral cycles and ensure stability.

18

CONCLUSION For US policymakers, the lessons learned from the NFRD and CSRD in the EU should be reviewed during this early stage of non financial disclosure policy development. Adopting reporting templates and KPIs already used in the EU would lower the burden on multinational companies adjusting to multiple reporting requirements and increase economic competitiveness by reducing information asymmetry. For EU policymakers, non-financial disclosure policies should be promulgated in multilateral forums or while engaging with US policymakers or business organizations to reinforce the value of disclosure alignment. As the CSRD is further developed, adopting reporting requirements and templates that are transferrable in international contexts is recommended to strengthen the case f or the US and other jurisdictions to meet higher EU standards when developing their own regulations. For multinational businesses, increased data collection and reporting requirements should be planned for in both the US and EU. Engagement with US policymakers to support strengthening and aligning disclosure requirements would be valuable at this early stage of policy development. Fundamental differences not just in the political process but even the base accounting frameworks of the US and EU make full reporting cohesion ambitious, but continued partnership between the US and the EU on these issues will build political unity, enhance corporate transparency and ESG activity, and serve as a model for the rest of the world. Therefore, immediate action is encouraged for both parties in order to ensure higher transparency and enable more efficient cooperation in the sustainable finance landscape.

19

REFERENCES

Adams, C. A., & Abhayawansa, S. (2021). Connecting the COVID-19 pandemic, environmental, social and governance (ESG) investing and calls for ‘harmonisation’ of sustainability reporting. Critical Perspectives on Accounting, 102309. https://doi.org/10.1016/j.cpa.2021.102309. Akerlof, G. A. (1978). The market for “lemons”: Quality uncertainty and the market mechanism. In Uncertainty in economics (pp. 235-251). Academic Press. Aussilloux, V., Bénassy-Quéry, A., Fuest, C. & Wolff, G. (2017). Making the best of the European Single Market. Bruegel Policy Contribution Issue n ̊ 3. Retrieved from https://www.bruegel.org/wp-content/uploads/2017/02/PC-03-2017-single-market010217-.pdf. Bakken, C. (2021). Shedding Light on Sustainable Shipping: Examining Content and Motivations for Sustainability Reporting along the Shipping Value Chain. Master’s Thesis, Lund University. Retrieved from http://lup.lub.lu.se/studentpapers/record/9057340. Barro, R. J. (1992). Convergence. Journal of Political Economy, 100(2), 223–251. https://doi.org/10.1086/261816. Bhatia, A. V., Mitra S., & Weber A. (2019). A Capital Market Union for Europe: Why It’s Needed and How to Get There. IMFBlog. Retrieved from https://blogs.imf.org/2019/09/10/a-capital-market-union-for-europe-why-its-needed-and-how-to-get-there/. WPSF (2021) Wissenschaftsplattform Sustainable Finance/Sustainable Finance Research Platform. Bossut, M., Hessenius, M., Juergens, I., Pioch, T., Schiemann, F., Spandel, T., & Tietmeyer, R.. Why it would be important to expand the scope of the Corporate Sustainability Reporting Directive and make it work for SMEs. Policy Brief 8/2021. Retrieved from https://wpsf.de/wpcontent/uploads/2021/09/WPSF_PolicyBrief_8-2021_Scope.pdf Broome, S., Kimpel, S., Brown, S., McSweeney, D., & Knauss, C. (2021). Actions on Climate Change Disclosure in California and New Report Indicate Spring May Be In Like a Lion and Out Like One Too!. Hunton Andrews Kurth. Retrieved from https://www.natlawreview.com/article/actions-climate-change-disclosure-california-and-new-report-indicate-spring-may-be. Bingler, J. A., Kraus, M. & Leippold, M. (2021). Cheap Talk and Cherry-Picking: What Climate Bert has to say on Corporate Climate Risk Disclosures. Available at SSRN: https://ssrn.com/abstract=3796152. Carney, M. (2021). The Price of (Net) Zero Ambition. Speech held at Columbia University on 23 September 2021. Retrieved from https://news.climate.columbia.edu/wp-content/uploads/2021/10/The-Price-of-Net-Zero-Ambition_Published_final-1.pdf CDP & CDSB (2018). First Steps: Corporate climate and environmental disclosure under the EU Non -Financial Reporting Directive. Retrieved from https://www.cdsb.net/sites/default/files/cdsb_nfrd_first_steps_2018.pdf . CDP, CDSB, GRI, IIRC, & SASB (2020). Statement of Intent to Work Together Towards Comprehensive Corporate Reporting. Retrieved from https://bit.ly/2Flu0Fb. Christensen, H., Hail, L., & Leuz, C. (2018). Economic Analysis of Widespread Adoption of CSR and Sustainability Reporting Standards. http://dx.doi.org/10.2139/ssrn.3315673. Clark, G. (2021). Number of small and medium-sized enterprises (SMEs) in the European Union (EU27) from 2008 to 2021, by size. Statista. Retrieved from https://www.statista.com/statistics/878412/number-of-smes-in-europe-by-size/. Cleary Gottlieb (2020). Sustainable Finance: A Global Overview of ESG Regulatory Develop ments. Retrieved from https://www.clearygottlieb.com/-/media/files/alert-memos-2020/sustainable-finance-a-global-overview-of-esg-regulatorydevelopments.pdf.

20

Climate Leadership Council (2019). Economists’ Statement on Carbon Dividends. Originally printed in the Wall Street Journal o n January 17, 2019. Retrieved from https://www.clcouncil.org/economists-statement/. Code of Federal Regulations (CFR). 40 C.F.R. §98.2. Mandatory Greenhouse Gas Reporting: Who must report? Retrieved from https://www.ecfr.gov/cgi-bin/textidx?SID=a44e17466e578eb4f6d21c4e1751e930&mc=true&node=pt40.23.98&rgn=div5#se40.23.98_12 Cort, T., & Esty, D. (2020). ESG Standards: Looming Challenges and Pathways Forward. Organization & Environment, 33(4), 491– 510. https://doi.org/10.1177/1086026620945342. EU (1992). Towards Sustainability. A European Community programme of policy and action in relation to the environment and sustainable development. Retrieved from https://ec.europa.eu/environment/archives/action-programme/envact5/pdf/5eap.pdf. EC (2001). COMMISSION RECOMMENDATION of 30 May 2001 on the recognition, measurement, and disclosure of environmental issues in the annual accounts and annual reports of companies. Retrieved from https://eurlex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2001:156:0033:0042:EN:PDF . EFRAG (2021). EFRAG & GRI landmark Statement of Cooperation. Retrieved from https://www.efrag.org/Assets/Download?assetUrl=%2fsites%2fwebpublishing%2fSiteAssets%2fEFRAG%2520GRI%2520COOPERA TION%2520PR.pdf EU (2014). DIRECTIVE 2014/95/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 22 October 2014 amending Directive 2013/34/EU as regards disclosure of nonfinancial and diversity information by certain large undertakings and groups. Retrieve d from https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32014L0095. EC. (2017). Guidelines on non-financial reporting (methodology for reporting non-financial information). Retrieved from https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52017XC0705(01) EU (2019). Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability‐ related disclosures in the financial services sector. https://eur-lex.europa.eu/eli/reg/2019/2088/oj. EU (2020). Regulation (EU) 2020/852 of the European Parliam ent and of the Council of 18 June 2020 on the establishment of a framework to facilitate sustainable investment and amending Regulation (EU) 2019/2088. https://eurlex.europa.eu/legalcontent/EN/TXT/?uri=celex:32020R0852 EC (2020). Consultation Document Review of the Non-Financial Reporting Directive https://ec.europa.eu/info/law/betterregulation/have-your-say/initiatives/12129-Revision-of-Non-Financial-Reporting-Directive/public-consultation_en. EC (2021a). European Commission Proposal for a Directive of The European Parliament and of the Council amending Directive 2013/34/EU, Directive 2004/109/EC, Directive 2006/43/EC and Regulation (EU) No 537/2014, as regards corporate sustainability reporting. Retrieved in June 2021 from: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52021PC0189. EC (2021b). Proposal for a Regulation of the European Parliament and the European Council establishing a carbon border adjustment mechanism. Retrieved from https://ec.europa.eu/info/sites/default/files/carbon_border_adjustment_mechanism_0.pdf Jeffrey, C., & Perkins, J. D. (2013). Social Norms and Disclosure Policy: Implications from a Comparison of Financial and Corporate Social Responsibility Reporting. Social and Environmental Accountability Journal, 33(1), 5–19. https://doi.org/10.1080/0969160x.2012.748468. Fuhrmann, S., Ott, C., Looks, E., & Guenther, T. W. (2016). The contents of assurance statements for sustainability reports a nd information asymmetry. Accounting and Business Research, 47(4), 369–400. https://doi.org/10.1080/00014788.2016.1263550. García‐Sánchez, I., Hussain, N., Martínez‐Ferrero, J., & Ruiz‐Barbadillo, E. (2019). Impact of disclosure and assurance quality of corporate sustainability reports on access to finance. Corporate Social Responsibility and Environmental Management, 26(4), 832–848. https://doi.org/10.1002/csr.1724.

21

Gelles, D. (2016). S.E.C. is criticized for lax enforcement of climate risk disclosure. The New York Times. https://www.nytimes.com/2016/01/24/business/energy-environment/sec-is-criticized-for-lax-enforcement-of-climate-riskdisclosure.html Group of Thirty (2020). Mainstreaming the transition to a net-zero economy. Retrieved from https://group30.org/images/uploads/publications/G30_Mainstreaming_the_Transition_to_a_Net -Zero_Economy_2.pdf Hamilton, D. & Quilan, J. (2021). The Transatlantic Economy 2021. Brookings Press. Retrieved from https://www.wilsoncenter.org/book/transatlantic-economy-2021. IFRS (2021). IFRS Foundation Trustees announce working group to accelerate convergence in global sustainability reporting standards focused on enterprise value. Retrieved from https://www.ifrs.org/news-and-events/news/2021/03/trusteesannounce-working-group/ IPSF (2021). State and trends of ESG disclosure policy measures across IPSF jurisdictions, Brazil, and the US. Retrieved from https://ec.europa.eu/info/files/international-platform-sustainable-finance-esg-disclosure-report-2021_en. Hahn, R., & Kühnen, M. (2013). Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. Journal of Cleaner Production, 59, 5–21. https://doi.org/10.1016/j.jclepro.2013.07.005 Hibbitt, C., & Collison, D. (2004). Corporate environmental disclosure and reporting developments in Europe. Social and Environmental Accountability Journal, 24(1), 1–11. https://doi.org/10.1080/0969160x.2004.9651708. Juergens, I. & Erdmann, K. (2019). A short qualitative exploration of the reporting and use of non -financial data in the context of the fitness check of the EU framework for public reporting by compa nies, DIW Berlin Policy Advice Compact 147, https://www.diw.de/documents/publikationen/73/diw_01.c.704204.de/diwkompakt_2020 - 147.pdf. Kalesnik, V, Wilkens, M & Zink, J. (2020). Green Data or Greenwashing? Do Corporate Carbon Emissions Data Enable Investors to Mitigate Climate Change? Available at SSRN: https://ssrn.com/abstract=3722973 or http://dx.doi.org/10.2139/ssrn.3722973. Kiliç, M., & Kuzey, C. (2018). Determinants of forward -looking disclosures in integrated reporting. Managerial Auditing Journal, 33(1), 115–144. https://doi.org/10.1108/maj-12-2016-1498. Korca, B., & Costa, E. (2021). Directive 2014/95/EU: building a research agenda. Journal of Applied Accounting Research, 22(3), 401–422. https://doi.org/10.1108/jaar-05-2020-0085. Korca, B., Costa, E., & Farneti, F. (2021). From voluntary to mandatory non -financial disclosure following Directive 2014/95/EU: an Italian case study. Accounting in Europe, 1–25. https://doi.org/10.1080/17449480.2021.1933113 . Krueger, P., Sautner, Z., Tang, D.Y., & Zhong, R. (2021). The Effects of Mandatory ESG Disclosure Around the World. European Corporate Governance Institute – Finance Working Paper No. 754/2021, Swiss Finance Institute Research Paper No. 21 -44. http://dx.doi.org/10.2139/ssrn.3832745. Latham & Watkins, LLP (2021). CFTC Takes Action With New Climate Risk Unit. Retrieved from https://www.jdsupra.com/legalnews/cftc-takes-action-with-new-climate-risk-4851695/. Lee, A. (2020). “Modernizing” Regulation S-K: Ignoring the Elephant in the Room. Securities and Exchange Commission. Retrieved from https://www.sec.gov/news/public-statement/lee-mda-2020-01-30. Lee, A. (2021). Public Input Welcomed on Climate Change Disclosures. Securities and Exchange Commission. Retrieved from https://www.sec.gov/news/public-statement/lee-climate-change-disclosures. Masiero, E., Arkhipova, D., Massaro, M., & Bagnoli, C. (2019). Corporate accountability and stakeholder connectivity: A case study. Meditari Accountancy Research, 28(5), 803–831. https://doi.org/10.1108/medar-03-2019-0463. Matuszak, U., & Różańska, E. (2017). CSR Disclosure in Polish-Listed Companies in the Light of Directive 2014/95/EU Requirements: Empirical Evidence. Sustainability, 9(12), 2304. https://doi.org/10.3390/su9122304. NASDAQ (2021). Nasdaq’s Board Diversity Rule: What Nasdaq-listed Companies Should Know. https://listingcenter.nasdaq.com/assets/Board%20Diversity%20Disclosure %20Five%20Things.pdf

22

Nicodemus, A. (2021). TCFD recommendations more than building block for SEC climate disclosure rules? Compliance Week. https://www.complianceweek.com/risk-management/tcfd-recommendations-more-than-building-block-for-sec-climatedisclosure-rules/31175.article. Plumer, B. & Popovich, N. (2021). The U.S. Has a New Climate Goal. How Does It Stack Up Globally?. New York Times. https://www.nytimes.com/interactive/2021/04/22/climate/new -climate-pledge.html. Quinson, T. (2021). What the SEC has in Store. Bloomberg Green. Rezaee, Z. & Tuo, L. (2017). Voluntary disclosure of non-financial information and its association with sustainability performance, Advances in Accounting, 39, 47-59. https://doi.org/10.1016/j.adiac.2017.08.001. Rodrik, D. (2000). How Far Will International Economic Integration Go? Journal of Economic Perspectives, 14(1), 177–186. https://doi.org/10.1257/jep.14.1.177. Sapir, A. (2021). The European Union’s carbon border mechanism and the WTO. Bruegel. Retrieved from https://www.bruegel.org/2021/07/the-european-unions-carbon-border-mechanism-and-the-wto/. Schoenmaker, D. (2013). Governance of International Banking: The Financial Trilemma (1st ed.). Oxford University Press. Securities and Exchange Commission (2010). 17 C.F.R. § 211, 231 and 241 Commission Guidance Regarding Disclosure Related to Climate Change; Final Rule. Federal Register. Retrieved from https://www.sec.gov/rules/interp/2010/33-9106fr.pdf. Securities and Exchange Commission (2021). Sample Letter to Companies Regarding Climate Change Disclosures. Retrieved from https://www.sec.gov/corpfin/sample-letter-climate-change-disclosures. Shalal, A. & Lawder, D. (2021). U.S. Treasury's Yellen vows to work with international climate finance ministers group. Reute rs. Retrieved from https://www.reuters.com/article/us-imf-world-bank-usa-climate/u-s-treasurys-yellen-vows-to-work-withinternational-climate-finance-ministers-group-idUSKBN2BT240. Sustainability Accounting Standards Board (2021). Companies Reporting with SASB Standards. https://www.sasb.org/companyuse/sasb-reporters/. Sustainable Stock Exchanges (2021). Model Guidance on Climate Disclosure. Retrieved from https://sseinitiative.org/wpcontent/uploads/2021/06/Model-Guidance-on-Climate-Disclosure.pdf. Tarquinio, L., Posadas, S. C., & Pedicone, D. (2020). Scoring Nonfinancial Information Reporting in Italian Listed Companies: A Comparison of before and after the Legislative Decre e 254/2016. Sustainability, 12(10), 4158. https://doi.org/10.3390/su12104158. The White House (2021). U.S. Climate-Related Financial Risk Executive Order 14030: A Roadmap to Build a Climate -Resilient Economy. Retrieved from https://www.whitehouse.gov/wp-content/uploads/2021/10/Climate-Finance-Report.pdf. United States Courts (n.d.). About the Rulemaking Process. Retrieved from https://www.uscourts.gov/rules-policies/aboutrulemaking-process. US Small Business Administration (2019). Small Businesses Generate 44 Percent of U.S. Economic Activity. Retrieved from https://advocacy.sba.gov/2019/01/30/small-businesses-generate-44-percent-of-u-s-economic-activity/. Weiss, L. (2021). House passes ESG, climate disclosure rules for public companies. Roll Call. Retrieved from https://www.rollcall.com/2021/06/16/house-passes-esg-climate-disclosure-rules-for-public-companies/. World Bank (2019). Listed domestic companies, total – United States. Retrieved from https://data.worldbank.org/indicator/CM.MKT.LDOM.NO?name_desc=true&locations=US

23

IMPRESSUM

PUBLICATION DETAILS

Angaben gemäß § 5 TMG

HOW TO CITE THIS PUBLICATION

Climate & Company - The Berlin Institute for Climate Training and Research gGmbH

Bakken C., Korca B., Lehmann-Leo S., Erdmann C., Juergens I., and Schockling A.: Corporate Non-Financial Disclosure: How Can the EU and the US Align? - A comparative analysis by Climate and Company. 12/2021

Ahornallee 2 12623 Berlin Vertreten durch: Ingmar Juergens David Rusnok

This publication and further information on our ongoig project on EU-US Sustainable Finance are available online on our dedicated webpage.

AUTHORS

Kontakt E-Mail: hello@climcom.org

Christian Bakken, Blerita Korca, Simon Lehmann-Leo, Katharina Erdmann, Ingmar Juergens, and Amanda Schockling

Verantwortlich für den Inhalt nach § 55 Abs. 2 RStV

ACKNOWLEDGEMENTS

Ingmar Juergens & David Rusnok Ahornallee 2 12623 Berlin

www.climateandcompany.org

The authors would like to express their sincere gratitude to Prof. Dr. Frank Schiemann, Theresa Spandel and Raphael Tietmeyer from the University of Hamburg for their valuable comments and insightful contributions.

ANY FEEDBACK? Climate & Company Ahornallee 2 | 12623 Berlin www.climateandcompany.com hello@climcom.de

24

Box 1. Latest Developments: SEC Proposal on Climate-related Disclosure In March 2022, the SEC released a proposed rule governing climate disclosure for U.S.-listed public companies (both domestic and foreign) amending Regulation S-K and Regulation SX (SEC, 2022). The rule will be open for public comments until June 17, 2022, with final regulations expected in late 2022 after incorporating feedback from commenters, though as the SEC posed hundreds of comments to the public there may be significant changes yet to come. The proposed rule is based largely on the Task Force on Climate-Related Financial Disclosures (TCFD) and goes well beyond the SEC’s 2010 climate disclosure guidance, environmental components of existing reporting, or public sustainability reports distinct from annual reporting. It would require qualitative disclosure on the company’s 10-K (annual report) and registration statements of specific details related to corporate governance, risk management, and strategy with respect to climate-related risks. Reports would also need to detail for any climate-related targets or commitments made by a company the scope of activities and emissions included in the target, baselines and units of measurements used, interim targets, and how the company intends to meet these targets. Financial statements would also need to note the quantitative impact of climate-related events and transitions. This information will be reported in a separately labeled section of the report and referenced in preexisting sections. Additionally, all filing companies would be required to publish Scope 1 and 2 GHG 1 emissions, and Scope 3 if (financially) material or if part of a public corporate commitment . GHG data would include aggregate value and disaggregated by GHG in both absolute and intensity terms 2. All data needs to be published in a consistent and comparable manner following the GHG Protocol and attested by outside attestation providers3. Disclosures would be phased in depending on corporate size and filing status between fiscal years 2023 4 and 2025 . The SEC proposal comes at a time with various other international developments. In November 2021, the International Financial Reporting Foundation (IFRS) announced the foundation of the International Sustainability Standards Board (ISSB). The ISSB intends to develop a global baseline of sustainability reporting standards – the first draft of standards was launched in March 2022. In addition, the European Financial Reporting Advisory Group published the first set of the European Sustainability Reporting Standards (ESRS). Until June 2022, both organizations ask for comments in a public consultation. Rule text: https://www.sec.gov/rules/proposed/2022/33-11042.pdf.

[1] Scope 3 reporting is not necessary for small reporting companies (companies with public float of less than $250 million or annual revenues less than $100 million and a public float of less than $700 million) and would be phased in one year after the other requirements. [2] Companies must provide methodology and data sources used for their GHG calculations. Major data gaps and means of accounting for these must also be disclosed. If data is estimated it may be corrected to actual results in subsequent filing periods. [3] Attestation is also not required for small reporting companies. Attestation providers do not need to be public accounting firms. [4] As annual reports generally cover the last three years of financials, this would require reporting to be phased in essentially immediately.