STUDENT INVESTMENT PORTFOLIO

Each year, the student investment team is chosen by our peers and a faculty advisor to manage the funds. We focus on different industry sectors and are dedicated to managing portfolio risk. Weekly meetings involve in-depth presentations on potential acquisitions and divestments, which include detailed analysis of the company and industry, debate on potential impacts and explanation of risk-adjusted returns.

This hands-on learning experience allows our team to actively trade shares while gaining key skills in areas such as valuations, ratio analysis, and portfolio management strategies. We regularly present our decisions and performance in meetings, with presentations made accessible to the funds’ advisory boards, the Dean of the College of Business Administration, CMU alumni, employers and other guests. Additionally, we prepare this annual report that evaluates the performance of each fund, which we present and discuss with industry professionals at the Quinnipiac Conference in New York City.

The Celani Endowment Fund was started in 2005 with a generous donation of $1M by CMU alumnus Tom Celani. The fund is a student-managed endowment fund with oversight from university faculty. The fund has a focus on large-cap equities with 32 equity positions and 33 total positions. Since inception, the fund has grown to hold $3.1M in assets under management as of Dec. 2024.

The Seger Endowment Fund was established in honor of Martha Seger in 2007, a former CMU professor who served on the Federal Reserve Board of Governors from 1984 to 1991. The fund is a studentrun endowment focusing on mid-cap and small-cap equity investments. The endowment allows students to work with a portfolio benchmarked to the Russell 2000 Index. This fund currently holds 10 investments totaling $363k.

The Oros Endowment Fund was established in 2021 with a generous donation of $225,000 by CMU alumnus Bob Oros. The fund is a student-run endowment with oversight from university faculty. The endowment was created to give students experience managing a portfolio of fixed income and alternative investments. The fund currently holds 9 positions across fixed income, municipal investments, and alternative investments totaling $304k.

In 2024, our student investment funds took a step forward by seeking guidance from industry experts to improve our funds’ long-term strategy and decision-making processes. Understanding the impact that experienced finance professionals and alumni could have on our fund, we sought out individuals with strong ties to CMU and extensive backgrounds in investment management, financial strategy, and capital markets. Their readiness to share their expertise and guidance resulted in the creation of our advisory board, a collection of professionals who contribute significantly to enhancing our strategies and enriching the overall educational experience for our students through their feedback and informative seminars.

During the first meeting with our new advisory board, we presented our funds’ performance and vision as well as our technical and qualitative approach to evaluating potential equity and fixed income investments. We are incredibly grateful for their generosity and commitment to mentoring the next generation of finance professionals. Their insights will leave a lasting impact on our funds’ continued success, and we look forward to deepening this partnership in years to come.

CMU alumnus Matthias Berning is a member of the Global Client Solutions Team at KKR Capital Markets, bringing extensive experience in investment strategies and financial analysis. Before joining KKR, Matthias spent 9 years at J.P. Morgan’s Asset Management Group, working as a Vice President, analyzing mutual funds, ETFs, and SMAs. Holding both CFA and CAIA designations, he provides our group with valuable insights into market strategy and professional development. Matthais is committed to the professional development of CMU Finance students and has created a scholarship for students to pursue their CFA level 1 Certification. His insights and commitment to CMU students continue to inspire and guide the growth and direction of our fund.

Bruce George is a CMU alumnus with over three decades of experience in private equity and asset management. Bruce holds multiple professional certifications and charters such as the CFA, CAIA, etc., and currently is a partner at the P/E firm Investment solutions. Bruce also serves on the board of several foundations, giving him access to a network of professionals whose insights allow us to refine and enhance our strategic processes and decision-making skills. His extensive background in new business development and alternative assets provides valuable insights into our fund, enhancing our strategic initiatives and fostering growth.

As the Senior Managing Director and Co-Founder of Azimuth Capital Management LLC, Jan Hewlett has vast experience in investment research and portfolio management across various asset classes. A dedicated CMU alumna, Jan earned both her undergraduate degree and MBA from CMU, showing a strong commitment to our university. Her previous role as Director of Equities at The Dow Chemical Company Pension Fund further shows her expertise in managing substantial investment portfolios. Jan’s expertise in investment strategies and asset management provides our fund with invaluable insights, shaping our investment decisions and strengthening our long-term strategic vision.

As an Investment Banking Associate at P&M Corporate Finance (PMCF), Peter Konyndyk brings extensive experience in financial advisory services and investment banking. Prior to joining PMCF, he spent 6 years at Plante Moran, where he served as a manager in wealth management. A dedicated alumnus, Peter earned his Bachelor of Science in Business Administration, majoring in Finance with a minor in Spanish, from Central Michigan University. After graduating, he contributed to the university’s Finance Department as a member of its Advisory Board, helping set the program apart from other universities. Peter’s dedication to CMU, as well as his professional accomplishments, makes him a vital asset to our advisory board, playing a key role in guiding our fund’s growth.

Tim Magnusson is the Co-Founder and Chief Investment Officer of Garda Capital Partners and has built an exceptional career in fixed-income investment management and risk strategy. Tim is a dedicated CMU alumnus and has remained deeply involved with the university, creating a lasting impact through his support of academics and athletics alike. As a charterholder, Tim brings a wide range of insights across all areas of the markets, which he has shared with our members. Tim brings decades of experience in fixed-income portfolio management and has already begun guiding us on evaluating broader market trends and making strategic investment decisions.

Chris Moberg is the Dean of the College of Business Administration at Central Michigan University, a role he has held since 2019. Before joining CMU, he was Senior Associate Dean and Professor of Marketing at Ohio University’s College of Business, where he joined the Marketing Department in 1999 and held various leadership roles. A recognized leader in business education, he has supported AACSB accreditation efforts and led innovations in curriculum development, academic policy, and student success initiatives. Dean Moberg’s expertise includes supply chain management, logistics, business ethics, sales performance, buyer-seller relationships, and marketing strategy. His leadership has expanded opportunities for professional development, industry competitions, and realworld learning.

As the Chairman and CEO of Hightower Advisors in Chicago, as well as a committed CMU alumnus, Bob Oros has been instrumental to bringing hands on experiences to CMU students through the creation of the Bob Oros Multi-Asset Investment Fund. He has a wealth of experience, having served as CEO of HD Vest, EVP and Head of the RIA Segment at Fidelity Clearing and Custody, and in various leadership positions at LPL Financial and Charles Schwab. Bob is deeply committed to expanding opportunities for CMU students and excels at developing and executing strategic visions. Bob’s ability to transform ideas into actionable growth strategies has been instrumental in shaping organizations and will undoubtedly provide our fund with strong guidance, culture, and direction.

Our faculty advisor, Brad Taylor, has spent nearly a decade shaping CMU’s finance program. With 25 years as a CFO across three international companies, he brings invaluable industry insight.

Beyond leading the student-managed funds, he oversees the Wall Street Journal Club, connects students with professionals, and runs CFA Study Sessions to prepare for the Level 1 exam. He also organizes professional development trips to major finance hubs like Chicago and New York City and provides opportunities to compete in prestigious competitions such as the RMA Commercial Lending Challenge, ACG Cup, and CFA Research Challenge. His guidance and real-world experience have been instrumental in preparing us for careers in finance.

From fund management to research challenges, our student leadership team represents our broader student cohort that represents the future of finance. This group of students has immersed themselves in experiential learning to be able to graduate ready to hit the ground – and trade floor – running.

This past summer, Derek interned at Bluprint Ventures as an analyst, researching incoming startup deal flow. Additionally, Derek trains Artificial Intelligence models through the reinforcement learning process, analyzing and evaluating LLM generated content. Outside of the funds, Derek is very involved in the Michigan Finance Scholars program and the Wakeling-Gendron Entrepreneurial Scholars program. In addition to this, Derek also has competition experience by being a competitor in the New Venture Challenge and a 2x competitor in the ACG Cup.

Last summer, Owen interned at RBC Capital Markets where he will be returning postgraduation joining their Rotational Analyst program. Outside of the funds, Owen is involved in the business fraternity Alpha Kappa Psi, the FPA of CMU, and the overall Michigan Finance Scholars program. Owen also represented Central Michigan University at the 2025 CFA Research Challenge and was part of the winning team of the 2025 ACG Cup Case Competition.

Jack is a senior in the honors program at CMU, majoring in Finance. This past summer, he worked as a Product Development Intern with SEALK- AI-Powered M&A Deal Sourcing in Paris, France. This upcoming summer, he will intern with RBC Capital Markets as a summer analyst. In addition to serving as a co-chair and being involved in the Michigan Finance Scholars Program, he also competed in the CFA Research Challenge and ACG Cup competitions in 2025. Jack has also been attending the CFA Study Sessions since early 2024 in preparation for his Level 1 examination.

Sam’s summer prior to returning to CMU last fall was spent with Hantz Group in a Personal Financial Planning Assistant role. Post graduation Sam will be returning to Hantz Group to begin a role on the Hantz Asset Management Team. Outside of his leadership role, Sam participated in the 2024-2025 CFA Challenge and maintains heavy involvement in the Michigan Finance Scholars Program.

This past summer, Corinne worked as an Internal Audit Intern with Lands’ End. She continued working with both the Internal Audit and Financial Planning & Analysis teams throughout the school year. Following graduation, Corinne will be joining International in the Finance and Accounting Leadership Development Program. Outside of the leadership board, she also competes in a variety of finance competitions and was a part of the winning ACG Cup team in 2024 and the 2025 CFA Research Challenge winners, advancing to the Midwest regional competition.

Over the past summer, Carter interned at RBC Capital Markets in a Syndicate Operations Analyst Role where he underwrote several different financial products and learned to understand the funding process for corporations. Outside of funds, Carter has participated in both the RMA Commercial Lending challenge, where he took home 4th place, and the CFA Research Challenge.

The team of students that lead and participate in the Student Managed Investment Funds are no strangers to strategic change and informed decision making. 2024 was a year of improvement. Kicking off the year, the Leadership Board took charge by creating a brand-new filing system within Microsoft Teams to keep operations organized and allow new members the freedom to explore previous presentations and models, increasing the cohesion of Fund Members overall.

Establishing a solidified Advisory Board was the next task handled by the leadership board. Recruiting and securing Chris Moberg, Bruce George, Tim Magnusson, Bob Oros, Peter Konyndyk, Jan Hewlett, and Matthias Berning as Advisory Board Members for students to consult with was a key project and milestone for the endowment funds. Having access to world-class knowledge and experience has been instrumental for innovation within the funds, benefiting members tremendously.

Managing membership growth was another bottleneck that the Leadership Board members handled. Previously, the fund averaged around 20 students at any given meeting. However, 2024’s meetings yielded an average of 37 members and has grown to 39 voting members. To manage this influx of membership, increase participation, and accountability, the Leadership Board implemented a voting member status. New members are required to take a base knowledge exam to prove competency. Along with this, voting members’ attendance is required to be above 75% to maintain voting rights. This mitigates the risk of voting on acquisitions or divestments being affected by members with low accountability or knowledge.

Furthermore, the three investment funds and their holdings have been imported into Bloomberg to ensure consistent monitoring. This also helps the fund members track what the portfolios moves are day to day. Additionally, risk return metrics of Jensen’s Alpha, Sharpe, and Treynor Ratios were implemented as a requirement for pitch decks moving forward since the start of the fall semester. Having the portfolios in Bloomberg streamlines the process of calculating these three metrics, saving members time when creating a pitch deck. Moreover, putting the portfolios in Bloomberg challenges members to learn how to navigate and utilize Bloomberg software, thus boosting their abilities and making their skill set more attractive to potential employers post-graduation.

Establishing an official advisory board, voting membership, and portfolio input within Bloomberg have been crucial to the fund’s growth throughout 2024.

Celani Fund Monthly Return Compared to Benchmark

Entering 2024, the Celani Fund maintained a low-risk strategy with a strong Consumer Staples weighting amid recession concerns. As inflation cooled, the Fed began lowering interest rates, targeting 2%-2.25%, though potential inflationary risks from tariffs remain. To optimize risk-reward, the fund increased exposure to Financials, Tech, and Energy while expanding Consumer Discretionary to 23.01% of market value, reflecting confidence in consumer resilience. Additionally, a strategic consolidation to approximately 25 holdings aims to enhance risk assessment and long-term alignment with CFA insights on diversification efficiency.

Seger Fund Monthly Return Compared to Benchmark

The Seger Fund remains focused on small and mid-cap equities, reducing benchmark holdings from 85.11% to 58.84% to strengthen underweight sectors. Key weightings in energy, industrials, and consumer staples were maintained, while exposure to tech and financials increased. To enhance efficiency, the fund is streamlining to approximately 30 holdings.

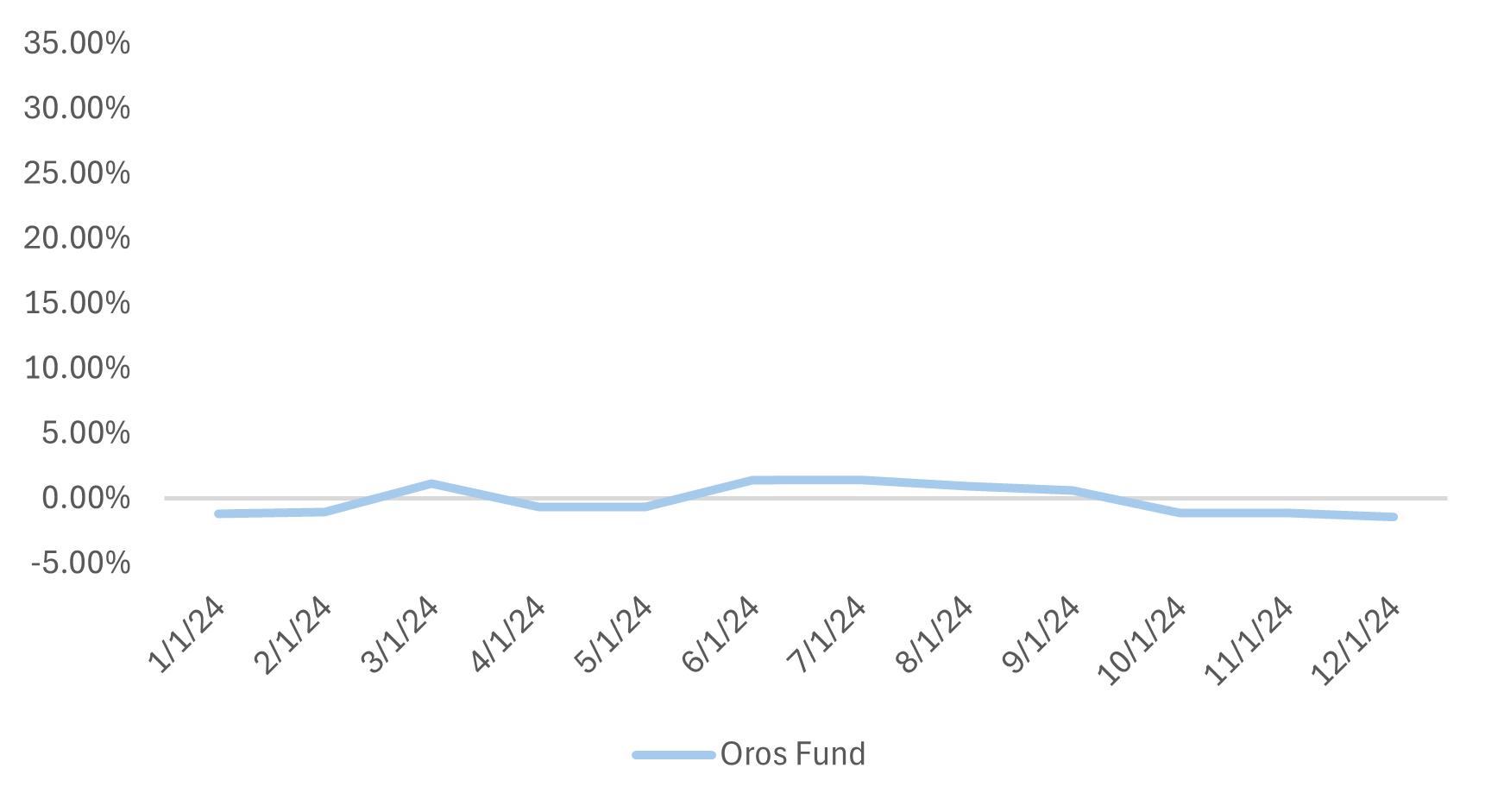

In early 2024, the Oros Fund maintained a diversified allocation in real estate and fixed-income securities, divesting under performing real estate holdings while preserving bond exposure. The portfolio included U.S. Treasuries, municipal bonds, and inflation-protected securities, with managers closely monitoring interest rate trends. Despite debates on adjusting duration exposure, the fund retained long-duration bond positions and will continue to assess fixed-income market dynamics moving forward.

In 2024, the fund performance was strong for the Celani and Seger Funds, both achieving solid returns relative to the respective benchmarks of the B500T and the B2000T. The Celani Fund posted a return of 19.7% with a lower volatility profile (10.7% standard deviation) and a Sharpe Ratio of 1.71, reflecting robust risk-adjusted returns. Furthermore, the fund’s beta of 0.85 and Jensen’s Alpha of ~4% shows the funds excellent risk management and ability to generate value above expectations. The Seger Fund excelled with a 22.3% return and a significant 10.7% alpha, although Seger is more risk aggressive with a 20.4% standard deviation and higher beta of 1.01.

In contrast, the fixed-income and alternatives fund in the Oros Fund faced a difficult environment, resulting in a –1.46% return as the macroeconomic landscape caused headwinds and heavy rate volatility. The fund runs a lower standard deviation of 7.4% but struggled to run positive risk-adjusted returns due to the uncertainty of the macro landscape.

Overall, the Celani/Seger/Oros Funds demonstrated an equilibrium of risk and return, with the equity-based Celani and Seger Funds managing positive risk-adjusted returns, and Oros Fund navigating a difficult fixed-income landscape.

The Celani/Seger/Oros Funds market outlook for 2025 is derived from analysis of popular financial institutions’ insights on the upcoming calendar year and student members forecasting. Recent market outlooks from financial institutions claim a moderate growth environment in 2025, a decline from the ultra-growth that we have seen in the past two years in the equity markets.

Inflation is projected to continue its decline as central banks finalize or faintly unwind their tightening cycles, however uncertainty around tariffs with the Trump administration possess a potential threat to the thesis surrounding inflation in 2025. Popular contention is for cyclical sectors such as energy and industrials to see prospects improved as supply chain issues ease, and global consumer demand remains steady. Earnings and robust corporate fundamentals remain crucial in sustaining current historically high valuations, particularly in technology and consumer discretionary sectors where premium valuations exist.

The geopolitical landscape is a crucial variable that could sway the markets in 2025, considering the clashing of political ideologies with different world leaders and the Trump administration along with the transitions of power being seen throughout the world from the heavy election year that was 2024.

Celani Fund maintains a balance between high growth technology holdings (Amazon, Apple, Meta Platforms) and stable cash-flow generative sectors (Procter & Gamble, Walmart). We deem this a fitting approach for the Celani Fund to capitalize on potential digital expansion opportunities while having the ability to weather any headwinds in the macro environment.

The financial sector holdings such as JPMorgan and BlackRock could see improved margins and deal flow if short-term rates stabilize, and the Trump administration follows through with deregulation of the sector. If the consumer continues portraying resilience in 2025, industrials (Caterpillar Inc, Waste Management, etc.) and consumer discretionary (Light & Wonder Inc, Lowe’s, Amazon, etc.) could see an uptick in household spending providing significant tailwinds.

The Seger Fund maintains a heavy position in the Russell 2000, which could lead to significant upside potential as small and mid-cap equities tend to thrive in moderate inflation and a stable rate environment. High conviction holdings like Golar LNG, SoFi Technologies, and Six Flags Entertainment provides exposure to forecasted growth themes of 2025.

Forecasted supply chain improvements, deregulation of certain industries, and bolstering of domestic manufacturing should lead to value creation for the small-mid cap space which is more reliant on local economic conditions.

Financial institutions believe fixed income will play a greater role if yields are to stabilize, providing potential investment opportunities for the fund. With the Oros Fund deploying positions in varying durations of U.S. Treasuries, corporate bonds, and taxable municipal bonds allows the fund to experience income generation while retaining potential for price appreciation if rates ease. Inflation risk that could be seen in 2025 due to potential Trump administration tariffs, are hedged through the funds TIPS and silver holdings.

By synthesizing outlooks from major financial institutions and the funds own insights, we believe that diversification and a balanced allocation will be key to approaching the markets in 2025. Our funds exert this contention, through numerous sector exposure in large-cap equities, small and mid-caps, and diversified fixed income/alternatives.

Although inflation seems likely to continue moderating (although tariff risk is a variable the fund is closely monitoring), potential catalysts for market volatility remain, including shifting geopolitical dynamics and variations in global growth. Nevertheless, our positioning across the Celani, Seger, and Oros Funds seeks to capture upside from a stabilizing monetary backdrop while maintaining the diversification necessary to manage unforeseen risks.

Celani Fund Weightings

Benchmark Weightings

Going into 2024, the Celani Fund was positioned for a low-risk strategy, due to the fact we had most of the portfolio’s market weighting in the Consumer Staples sector with 18.86% of market value allocated. This was due to the fact that market sentiment towards a recession was at a peak going into the fiscal year 2024.

The forecast for interest rates and how they interact with the broader equity market was quite dynamic. The Federal Reserve had kept the federal funds rate at a range of 5.25% to 5.50% from July 2023 to August 2024 and as inflation started to finally cool, they began the process of bringing interest rates back down, with a half-point rate cut that brought the federal funds rate to 4.75%-5% in September of 2024.

The expectation of rates going forward has been constant since the goal of the Fed has been to get rates and inflation to a level around 2% to 2.25%, although we do see risk to this goal with Trump administration tariffs potentially having a fueling effect on inflation. The fund believes that we should position based on this forecast and the goal the Fed has set.

The fund decided that it would be best to move towards Financials, Tech, and Energy due to the fact we believed we could get the most risk to reward within these sectors. While being underweight in these sectors, we felt we needed to fill some positions to match weightings more efficiently with our benchmark. These sectors trade at significantly lower multiples than other sectors yet have shown surprising earnings resilience and growth. All sectors have been able to greatly reduce the number of shares outstanding through share buybacks in recent years. Moreover, we bolstered our position in the Consumer Discretionary sector throughout 2024, to the point where it is now the most exposed sector in the portfolio with a market value of 23.01%, due to the belief in resiliency of the consumer.

Furthermore, the main goal of the Celani Fund is to reduce portfolio holdings to approximately 25 names. The reason behind this push to consolidation of holdings is to simplify portfolio tracking and the CFA’s insights on how the advantage of diversification dwindles away in a large-cap equity portfolio after 20-25 holdings. Implementing a more streamlined approach to the Celani Fund improves our ability to assess the risks associated with each individual holding and align the fund to our long-term goals and objectives.

Communication Services Sector (XLC) Return

Communication Services Sector Holdings Performance

Energy demands have risen substantially due to AI data centers. According to Barclays’ Research, AI data centers are expected to triple in demand by 2030 which will require a significant investment into the energy sector. Many companies and countries have begun investments in alternative energy sources, primarily nuclear. Some notable moves in the nuclear industry include small scale nuclear reactors (SMRs) hitting the market and Microsoft investing in 3 Mile Island. The Trump Administration is also very supportive of oil and fossil fuels, and we should see domestic production in oil increase in the coming months.

One of our goals as a fund was to be overweight in the energy sector due to the need for significant investments into energy infrastructure and production. Our outlook on the energy sector is overall positive, however we will continue to analyze this sector very closely to see what president Trump decides to do with the EV mandate/tax credits, the Inflation Reduction Act, domestic oil production, and Executive Order 14156 the “National Energy Emergency” order.

Meta Platforms experienced quite large stock growth in 2024, increasing around 65% in the year, outperforming the broader market. Prices opened the year around $345 and closed at around $585. This future growth has stemmed from advancements in artificial intelligence and the metaverse, while we see risks in high capital expenditures in emerging technologies. They reported revenue of $164B in 2024, giving them an 18% YoY increase. Meta’s attractiveness stems from their expansive user base and dominance in digital advertising. We currently own 199 shares of Meta that had a value of $116,516 at the end of 2024.

We currently own 641 shares of DIS valued at $111.35 per share at the close of 2024, which represents a 2.47% portfolio weight. Disney saw some growth in 2024, with a 3.8% increase in revenue YoY, in free-cash flow growth, along with a strong operating margin of 14.5% in 2024. DIS has slightly higher volatility than the broader market with a beta of 1.41. Looking into this, they started their fiscal year with a closing price on October 1st of $80.59, and since then have increased around 19.36%, on September 30th to $96.19.

The consumer discretionary sector delivered a strong performance in 2024, outpacing the broader market as consumer spending remained resilient and helped drive robust returns. The S&P 500 rose ~25% for the year, but the consumer discretionary sector posted a more impressive 26.6% gain. The overall job market remained solid, allowing consumers to reclaim some of the purchasing power eroded in recent years.

However, a deeper look at consumer behavior in 2024 revealed a bifurcation in spending trends. Higherincome households, benefiting from surging stock prices and rising home equity, fueled much of the discretionary sector’s growth, sustaining demand for luxury goods, travel, and premium services. In contrast, lower-income consumers, more acutely affected by inflation and higher borrowing costs, exhibited signs of spending fatigue, cutting back on discretionary purchases such as dining, apparel, and entertainment. This divergence led to mixed performance within the sector’s various industries.

While home-improvement and auto-parts retailers struggled as consumers postponed extensive home renovation projects, homebuilders saw a strong rally. This was driven by investor optimism that anticipated Federal Reserve rate cuts in 2025 would eventually translate into lower mortgage rates and increased housing demand.

Looking ahead to 2025, the sector’s trajectory will likely hinge on broader economic conditions. Should inflation continue to moderate, and the Fed proceeds with rate cuts, consumers may find themselves with greater financial flexibility to make larger purchases, such as vehicles and home upgrades. Additionally, if economic expansion persists and labor markets remain healthy, discretionary spending could remain heightened. However, a potential recession or weakening job market could dampen consumer confidence, applying pressure to the sector.

Amazon saw strong results in 2024. The stock increased by 44% due to the success of financial results throughout the year. Net Sales in FY 2024 increased by 11% from the previous year. The fund increased Amazon’s position in September to $150,000 and Amazon’s stock price increased by 18% by the end of the year. Amazon has expanded Amazon Web Services, which remains the biggest profit driver for the company. Amazon’s investments in artificial intelligence have enhanced service offerings and attracted more customers. The company’s advertising segment also saw growth which led to revenue diversification, which is due to successful streaming events such as Thursday Night Football. Amazon continues to expand its Prime membership, which exceeded 250 million subscribers in 2024.

H&R Block ended 2024 at $52.84, a 7.84% increase throughout the year. H&R had a P/E ratio of 12.97, showing a 45% increase from last year. For their EPS in 2024, it increased over 13% to $4.41. This positivity was caused by an increase in the company’s revenues. They also showed an increase in net assets of $147 million and of $59 million in shareholders’ equity. If H&R can maintain an increase in revenue through outsourcing its services and improving customer retention, they should be able to control their debt and maintain the path of improvement they have set themselves on during 2024.

Since the fund purchased Light & Wonder Inc. in April, the stock price has decreased by about ~15% by the end of 2024, the stock is trading at $87.96 and has a weight in our portfolio of around 1.04%. Their Q3 2024 earnings report, released in November 2024, Light & Wonder announced a 12% year-overyear increase in consolidated revenue, marking the 14th consecutive quarter of revenue growth and the 9th consecutive quarter of double-digit growth. The gaming segment saw a 15% revenue increase, driven by a 38% rise in global gaming machine sales. Additionally, the iGaming division reported record revenues of $74 million, up 6% year-over-year.

Light & Wonder poses some risks when it comes to holding their shares. They have faced many legal troubles. In September 2024, a U.S. District Court granted a preliminary injunction to Aristocrat Gaming, alleging that Light & Wonder’s “Dragon Train” slot machines infringed upon Aristocrat’s trade secrets. Overall, Light & Wonder Inc serves as a company that has a relatively low weight in our diverse portfolio. Light & Wonder does have potential for long-term growth over time, but their legal troubles pose a risk to this investment and should be considered. We will analyze their legal developments and upcoming earnings reports to track this investment in the long term.

In 2024, Lowe’s Companies, Inc. (NYSE: LOW) delivered a total stock return of 13.01%, reflecting its resilience in the home improvement sector. The stock reached an all-time high closing price of $282.85 on October 16, 2024. Despite a 1.1% decrease in comparable sales during the third quarter, the company reported net earnings of $1.7 billion and diluted earnings per share of $2.99 for the quarter ending November 1, 2024. Analysts remain optimistic about Lowe’s growth potential, highlighting its plans to reduce debt, enhance merchandising, leverage technology through AI, and focus on professional customers. These strategic initiatives, paired with the company’s solid financial performance, position Lowe’s for continued success in the home improvement market.

In 2024, we reinvested into Mercado Libre, a company we had high growth projections for throughout the year. Before this reinvestment, we held a position of 15 shares, which was nearly a 330% gain from our original purchase at around $330 per share years prior. Despite this growth in previous years and significant growth of 30-40+% across all departments in the most recent year, the price of MELI stock was down nearly 25% YTD into Q1 24 due to one off potential lawsuit expenses that had already been accounted for on the balance sheet as of Q3 23. These one-off expenses caused Mercado Libre to report an EPS of $3.25 when EPS estimates were around $6.65 which is a very significant earnings miss. We purchased 30 more shares of MELI at around $1,400 per share. MELI is currently selling for $2070.41 per share which equates to nearly a 43% gain since the purchase of this reinvestment.

SCI is headquartered in Houston, Texas, and is North America’s leading provider of funeral, cemetery, and cremation services, as well as final arrangement planning, serving more than 600,000 families each year. SCI had an impressive year boasting a 15.56% gain in 2024. On top of that, they also introduced a quarterly dividend in their filings on November 6th that pays 30¢ per share which will be nice passive income throughout the year. Q3 earnings were positive overall - although revenues of $1B were in line with what the analysts predicted, SCI surprised by delivering a statutory profit of $0.81 per share, greater than expected. As it appears, analysts are keeping SCI as a strong buy with the highest analysts’ price target, expecting another 13-20% upside. This instills confidence in our portfolio as it is weighted at 1.95% adding moderate portfolio value.

The Celani Fund currently holds 4,730 shares of Stellantis N.V. (STLA US), which equates to 2.09% weight in our Celani Fund Portfolio. As of the end of 2024, STLA US was priced at $13.05 per share. Despite a 6% year-over-year revenue increase in Q4, net profits fell 8%. Looking ahead, Stellantis aims to strengthen its position by launching 8 new EV models in 2025, targeting a 30% increase in EV sales. Focusing on cost-cutting and successful EV rollouts, Stellantis could stabilize margins and improve investor sentiment, positioning the stock for a potential rebound.

Over the past year, Wolverine Worldwide made a strong recovery after 2023’s negative return, outperforming the broader market by a substantial margin in 2024. Wolverines’ closing stock price on the last trading day of 2024 was around $22.20 while they closed 2023 at around $8.70. Its focus on e-commerce growth and core brands has it positioned well for long term success. However, economic uncertainty and competition remain as challenges to monitor. Wolverine is expected to report a decline in revenue in Q4 but improve profitability with gross margins rising in its first three quarters. In May of this year, they appointed Taryn Miller as Chief Financial Officer, succeeding Michael Stronant, who retired after almost 30 years with the company.

eBay is a stock we recently sold. eBay had a great year in 2024, appreciating 45% since the start of 2024. The stock’s current share price is at $67.87, and a dividend yield of 1.59%. eBay reported earnings up 3% from 2023 and returned over $881 million dollars to shareholders. Though eBay had a great year, it also had challenges, such as its sales projections not meeting expectations, leading to an initial decrease in stock price that the company was able to rebound from. In 2025, eBay is making changes to its structure, such as new fees for first-time sellers of 4% of the item price. Some analysts see eBay underperforming in the long term due to higher marketing expenditures and a decrease in advertisement spending. It is noted that eBay is partnering with Meta to integrate listings into the Facebook marketplace, which is an attempt to increase sales and visibility for both companies and overall strengthen their market positions moving forward. Also, as we consolidated this fund, we decided to divest from eBay, as they had a portfolio weighting of ~.8%.

McDonalds had a total return of 0.55% on the year; however, we voted to sell our shares of MCD in fall of 2024. They had earnings per share that beat experts’ estimates in Q3 and had an estimated increase in revenue of $496.4 million. There were concerns with E. coli cases in late September and early October in restaurants; that said, CEO Chris Kempczinski stated in a Q3 earnings report that the situation appeared to be contained and did not affect Q3 numbers. Our reasoning for selling McDonalds was to continue with our fund’s strategy of trimming the number of holdings to simplify fund management. When we sold MCD, it was only .79% of our portfolio’s weight which made it a prime candidate to sell to decrease our number of holdings. On September 30th, we voted to sell our 80 shares of MCD with a total gain of 228%.

The consumer staples sector maintained relatively stable throughout all of 2024. Navigating economic challenges such as changes in consumer behavior and adjustments in the global supply chain, the consumer staples sector remained resilient.

Firms faced ongoing inflation which led to higher costs, thus, many firms introduced price hikes to preserve profit margins. The growing consumer resistance to increased prices prompted some companies to explore different cost-cutting solutions. To manage supply chain uncertainty, companies reduced product ranges and focused on higher-demand items. The sector appealed to risk-averse investors seeking lower volatility in a fluctuating market.

We currently own 732 shares of PG valued at $167.65 per share as of the close of 2024, which represents a 3.78% weighting in our portfolio. PG also experienced some minor growth with a 2% increase in net sales, and a 4% growth in organic sales in FY 2024. PG is seen as a relatively low risk investment with a Beta of 0.41 which is significantly below that of the broader S&P 500.

Walmart Inc. (WMT), a leader in consumer staples, has shown strong financial performance in 2024, outperforming the S&P 500 with a 70% stock price increase, reflecting resilience amid inflation and supply chain challenges. Its leadership in retail, broad geographic reach, and investments in e-commerce and supply chain infrastructure make it an attractive investment. However, risks such as margin compression from rising wages, increasing competition, and slower consumer spending in a high-inflation environment remain. In Q3 2024, Walmart reported revenue of $156.7 billion (+5% YoY) and EPS of $1.55, exceeding expectations. The company continues to expand its digital capabilities and enhance operational efficiency through leadership changes.

Looking ahead, Walmart is poised to benefit from strong consumer demand in groceries and essentials, alongside its expanding e-commerce presence. Growth drivers include digital expansion, supply chain improvements, and potential international growth. However, risks include competition from discount retailers and digital-first giants, as well as margin pressures from higher wages. Walmart represents 6.68% of the portfolio, with a market value of $201,359 (2061 shares), providing stability, strong cash flow, and dividends. Its strategic focus on e-commerce and supply chain improvements supports long-term growth despite near-term risks.

Energy Sector Holdings Performance

Energy demands have risen substantially due to AI data centers. According to Barclays’ Research, AI data centers are expected to triple in demand by 2030 which will require a significant investment into the energy sector. Many companies and countries have begun investments in alternative energy sources, primarily nuclear. Some notable moves in the nuclear industry include small scale nuclear reactors (SMRs) hitting the market and Microsoft investing in 3 Mile Island. The Trump Administration is also very supportive of oil and fossil fuels, and we should see domestic production in oil increase in the coming months.

One of our goals as a fund was to be overweight in the energy sector due to the need for significant investments into energy infrastructure and production. Our outlook on the energy sector is overall positive, however we will continue to analyze this sector very closely to see what president Trump decides to do with the EV mandate/tax credits, the Inflation Reduction Act, domestic oil production, and Executive Order 14156 the “National Energy Emergency” order.

Chevron is a multinational energy company focused on exploration, production, refining, marketing and distribution of petroleum and related products. As one of the world’s largest oil and gas companies, it operates in almost 200 different countries and is involved in all aspects of the energy sector. Headquartered in California, Chevron is a key player in the fossil fuel industry and is exploring investment in alternative energy sources like biofuel and hydrogen. Included in the Dow Jones Industrial Average (DJIA), Chevron is widely recognized for its global impact on the energy industry. Chevron started off 2024 at a stock price of $149.99 on January 2 and ended the year at a stock price of $143.07 leading to a slight decrease in the price of CVX of 4.61%. This decrease is notable, however, not extreme. The energy sector faced a multitude of challenges in 2024, including declining oil prices and tightening refining margins. Chevron’s stock decline can be attributed to decreased earnings and challenges in its refining segment. Chevron is currently trading at around $156 a share and has announced a capital expenditure budget of about $15 billion. The 2025 outlook is centered around the company’s strategic focus on cash flow optimization over aggressive production growth.

With its stock price rising 45.87%, ONEOK substantially outperformed the rest of the energy sector. This strong performance was driven by robust earnings growth, increased natural gas and NGL volumes, and the successful execution of acquiring Magellan Midstream in 2023. The acquisition led to cash flow stability and diversified revenue streams, positioning ONEOK as a more resilient energy infrastructure company.

Fund managers were pleased with the company’s strong operational execution and financial discipline, viewing its strategic growth initiatives and commitment to shareholder returns as key factors in sustaining long-term value creation. With strong demand for natural gas and NGLs, alongside ongoing growth in energy exports, ONEOK remains well-positioned to deliver continued growth in 2025. However, the managers remain cautious of any regulatory changes under the new Trump administration, such as new energy policies, pipeline regulations, or shifts in trade agreement.

Huntsman (HUN) is an American firm that manufactures and distributes chemicals. Huntsman’s stock has not performed well on a total or relative basis. Over the last five years, the stock has seen a return of –18.06% and is down –29.63% since the firm’s IPO. The stock has significantly underperformed relative to the S&P 500 index.

Huntsman faces multiple operational headwinds including weakening demand for key products and increasing energy costs. The firm is susceptible to fluctuations in commodity prices and supply chain disruptions. Despite the bull market, the stock dropped substantially this last year. The firm’s revenue declined 6% year over year. In 2024, the position was liquidated to raise capital for other investments.

A combination of macroeconomic challenges, regulatory changes, and evolving market dynamics displayed a period of transition in 2024. High interest rates and persistent inflation were central to the sector’s performance, influencing borrowing costs, consumer spending, and corporate investment. While financial institutions benefited from increased net interest margins, volatility in equity and credit markets, along with tightening liquidity conditions, posed significant challenges to profitability and stability.

For fintech and payment companies, 2025 may be a transformative year marked by increased flexibility and growth opportunities. With the newly appointed Trump administration, deregulatory measures are expected to benefit banks, fintech firms, and alternative lenders by reducing compliance burdens and fostering innovation. This shift could accelerate the adoption of digital payment solutions, blockchain-based financial services, and alternative lending platforms, expanding market opportunities for both established players and startups.

Additionally, potential policy changes surrounding cryptocurrency, open banking, and data privacy may reshape the competitive landscape, influencing investment trends and technological advancements. Investors should remain cautious of potential regulatory uncertainty, as abrupt policy shifts or legal challenges could create volatility and impact the long-term profitability of fintech firms.

Through 2024, BlackRock maintained its dominance with total assets under management surpassing $10.5 trillion. The company has seen strong growth due to investors’ demand for ETFs and fixedincome products. Operating income increased by just under 13%, which is great in reference to having operating income decreased slightly from 2022 to 2023. BlackRock’s dividend increased for the 16th year in a row and is yielding 2.12%. Lastly, BlackRock continued to buy back shares for the fourth consecutive year.

CME Group Inc. currently holds an AA- rating as of 2024, reflecting its strong financial stability and market position. In Q3 2024, CME Group reported its best-ever quarter, achieving $1.6 billion in revenue, demonstrating continued robust performance. The company has also seen significant growth in share price, with its share price now trading at approximately $232.23 at end of 2024, up from $209.23 at the same time last year. This represents a $23 increase in price per share, or a 10.9% rise in value.

CME Group’s success is partly attributed to its diversified portfolio of both long- and short-term bonds, which have contributed to the recent positive performance. The risk profile associated with these bonds remains low, given the company’s strong operational results and market position. Given these factors, we intend on holding CME Group shares and potentially adding to the position before prices rise further. This strategy will allow the portfolio to continue benefiting from the impressive performance.

JPMorgan’s stock rose 42.6% in 2024, significantly outpacing the broader market’s ~25% gain in the S&P 500. The bank’s strong performance was driven by resilient earnings, solid revenue growth, and improving investor sentiment toward the financial sector. JPMorgan exceeded Wall Street expectations in the third quarter, reporting total revenues of $42.7 billion, up 7% from the previous year, fueled by higher credit card balances, wholesale deposits, and a favorable balance sheet mix. Non-interest revenue, excluding the markets segment, posted an impressive 17% gain, led by strong asset management fees and a notable rebound in investment banking activity. However, net income dipped slightly by 2% to $12.9 billion due to increased provisions for credit losses. Despite this, JPMorgan continued its streak of outperforming the broader market for the third consecutive year.

Looking ahead, the outlook for JPMorgan appears promising, with expectations for improving net interest income in the fourth quarter, supported by the Federal Reserve’s rate cuts beginning in September. Additionally, the election of Donald Trump for a second presidential term has fueled optimism in the financial sector, as investors anticipate a more favorable regulatory environment, potential tax cuts, and increased capital market activity. As a result, JPMorgan remains wellpositioned to capitalize on these tailwinds heading into 2025.

Visa stock is currently weighted at 3.09% of our portfolio at a dollar value of $88,491. Visa Inc. had a strong year in 2024 as the company reported a 10% increase in revenue for Q4 2024 and a 5% rise in net profits. Visa’s stock price ended 2024 at $316.04, resulting in a ~22% return in 2024. In 2024, they also increased dividends by 13%, increasing their dividend yield to 0.76%. Visa, a leader in the U.S. payments market, grew its market share even more significantly, reaching up to 52% of that market. Visa has a high EPS at $10.05 and is considered slightly less risky than the market with a beta of 0.95.

2024 was a strong year for Wells Fargo, as earnings grew about 47% over the past year while also indicating strong investor confidence. In Q4 2024, Wells Fargo reported a net income of approximately $5.1 billion, about a 50% increase from the same quarter in 2023. Total revenue for 2024 was about $125.4 billion, an increase of about 9% from 2023. Wells Fargo’s success in 2024 mainly came from a heavy focus on diversifying revenue streams, particularly through investment banking and trading activities. The Board has approved an increase in the quarterly common stock dividend from $0.35 to $0.40 per share in the Q3 of 2024. Looking to 2025, the bank’s market positioning and diversification suggest a favorable and profitable future for the company.

At a market valued around $4 trillion, the healthcare sector has seen large influential factors, such as an aging population and economic factors that largely contributed to a global rise in spending. Many aspects of the Covid-19 pandemic brought many issues to light that the healthcare system is still learning to navigate, even by the end of 2024.

Healthcare providers faced difficulties regarding labor shortages and general costs along with an increased competition with technology. A rising need for an increase in wages as well as employee benefits added to a staffing shortage, causing tension between big companies and their employee retainment. Alternatively, the merging and consolidation of these big healthcare providers has allowed for patients to receive care from an integrated system, rather than multiple independent parties. This causes reduced competition and could possibly result in higher costs but also increase operation efficiency and help in underserved areas. One major concern from this is the ability for rural areas to receive access to the same healthcare as urban locations would.

Technology has also proven to be a key element focus on the future status of the market with AI and digital health applications leading the way with regulatory changes to follow. Meanwhile, social assistance in the U.S. has seen a struggle to meet demand of an increasing need for healthcare. Anti-competition mergers have been put in place by the Federal Trade Commission, indicating their concern as well for the negative effects of consolidation in the market.

Moving into 2025, the compound annual growth rate is 3.1% over the past five years from 2024 YE and is expected to increase throughout the next 5 years. Consumer spending is also not expected to slow down with contention dealing with pre-existing federal programs related to Covid-19, however, focus should be on technological advancements and their integration along with other demographic and economic factors.

AbbVie (ABBV)

AbbVie has a price-to-earnings ratio of ~80, reflecting an expensive valuation especially when compared to its top competitors Johnson & Johnson and Pfizer, which have PE ratios of 26.6 and 18.3 respectively. AbbVie has a dividend yield of 3.7% and maintains a semi-strong track record of growth and consistency, although there may be a concern with their high payout ratio. Throughout the year the stock remained relatively flat with slightly increased earnings. Looking ahead, AbbVie’s ability to navigate Medicare pricing reform and bring new products to market will be key to sustaining longterm earnings growth.

The Celani Fund currently holds 1,121 shares for CVS US, which equates to a market value of $50,322 at end of 2024. In turn, CVS maintains about 1.76% weight in the Celani Fund Portfolio. Examining their performance for the past year, CVS Health delivered mixed results in 2024, reflecting its strategic pivot toward integrated healthcare services.

In Q4 2024, the company reported a 7% year-over-year revenue increase, driven by growth in its pharmacy services segment and contributions from recent acquisitions (Oak Street Health and Signify Health). However, net profits declined 3% due to higher integration costs and inflationary pressures on labor and supply chains.

Looking at the Year-to-Date, CVS has decreased by 0.42%; Accompanied by a beta of 0.53, CVS displays stagnant returns yet potential for future growth. Currently, CVS is priced at $44.89 per share. Going forward, if CVS can find a way vertically integrate their recent acquisitions, Management expects revenue growth of 5-7% in 2025.

2024 saw slowed growth for Stryker, as earnings only grew about 10% over the past year (which the 2023 annual report predicted). However, despite the low stock growth, EPS rose about 15% while net sales grew by about 10% from 2023. A notable recent decision in the company was to divest its spinal implants business in hopes of aiming to operate in higher-growth areas. Exploring new areas can bring either positive or negative results, making it difficult to assess the impact of this decision. Looking to 2025, while inconsistencies may exist, the company’s proactive management could still have a profitable future.

In 2024, TMO’s revenue was $42.88 billion, remaining unchanged from the prior year, while net income and EPS grew by 5.7% to $6.34 billion. The company continues to strengthen its market position and drives future growth through continued investments in new product launches and strategic partnerships. The company completed the acquisition of Olink, a leading provider of advanced solutions for proteomics research. Additionally, TMO returned $4.6 billion of capital to shareholders through stock buybacks and dividends. Given these strategic investments and strong operational performance, the company is well positioned for strong performance in 2025.

Our position in UnitedHealth Group (UNH) has experienced significant growth since our initial purchase. We acquired 261 shares at $313.35, with a total principal investment of $137,554.83. As of YE 2024, the stock has risen to $505.86 per share, reflecting strong performance driven by the company’s continued expansion in healthcare services and consistent earnings growth.

Recently, (UNH US) faced an unexpected leadership transition following the passing of its CEO, Andrew Witty, which has raised some concerns regarding executive stability. However, the company has a well-established leadership structure and succession plan in place, ensuring continuity in its operations and strategic direction. Despite this development, UnitedHealth remains a dominant force in the healthcare industry, benefiting from rising demand for managed healthcare services and its ability navigate regulatory landscapes.

Industrials Sector (XLI) Performance

Industrials Sector Holdings Performance

The industrial sector currently makes up 17% of the Celani fund. The industrials sector delivered a return of 16.8% in 2024, slightly lagging the S&P 500 at ~25%. This performance was driven by several factors such as demand in data centers, alternative energy production, industrial automation, and U.S. manufacturing projects. Companies invested heavily in AI-driven automation, improving efficiency. The industrials sector is still attracting investors due to its several benefits in manufacturing reshoring and AI data centers. Caterpillar Inc., Delta Air Lines Inc., and FedEx Corp. led industrials in returns in the fund in 2024.

The Celani Fund purchased around 300 shares of CAT US at $155.24 in September 2009. The main incentives for the purchase were the strength of Caterpillar Inc. In its industry, the fund saw how smaller firms would not be able to enter the market and projected that bigger companies would end up acquiring such. Caterpillar Inc. especially showed strong numbers, as it led the industry in ROA, ROE, and EBIT Margin, and concentrated a large percentage of the market’s value. In 2024, CAT performed well, finishing the year with a total return of around 24.66%, even after a decline of almost 4.6% post Q4 earnings, mostly due to concerns over sales growth. Still, it showed strong financial results and promising initiatives. Since the initial purchase, we have seen a total return of 133.7%, a dominant industrials position in our portfolio.

Due to industry issues and macroeconomic conditions, Delta Air Lines (DAL), saw a volatility in 2024. Despite this, DAL has remained resilient, shown by its strong domestic and international demand, rapid sales growth, and improved EPS. The stock price’s significant rise from roughly $40 last year to ~$61 at the close of 2024, reflecting strong investor confidence and excellent financial performance. Key revenue drivers included the creation of premium products and calculated investments in sustainable aviation fuel (SAF). Risks include shifting petroleum costs, economic volatility, and geopolitical risks. Although there are now no plans for rebalancing with DAL, performance will be monitored so that any future modifications can be made as needed. All things considered, Delta’s market leadership and operational efficiency make it a strong holding with encouraging growth potential.

FedEx, a major freight and delivery company, exhibited an 8.66% year-over-year return, marked by substantial price volatility. The stock fluctuated this year from $240.79 at its lowest point at around $313.84 at its peak then eventually settling at $281.33 to end 2024. Although FedEx had a good YoY return on share price, FedEx’s recent earnings show inconsistent performance. While Q4 2024 slightly exceeded expectations (+$0.08, or 9.51% better than expected), Q1 2025 significantly missed projections, falling $1.22 short of the expected EPS. Q2 2025, however, showed a positive surprise ($0.17 above expectations). Revenue also displayed inconsistency, slightly missing estimates in both Q1 and Q2. This volatility highlights the need to carefully analyze Q3 2025 results before drawing conclusions about long-term trends.

For reference, FedEx has a fiscal year calendar that starts on June 1st before the calendar year and ends on May 31st of the calendar year. The large swings between quarters highlight the importance of monitoring FedEx closely, especially given its 2.44% portfolio weight. Understanding the factors driving this volatility is crucial for assessing the investment’s risk and potential reward. Future outlook for the company internally seems to be good as the company expects to repurchase an additional $500 million of common stock during fiscal 2025, for a buyback total of $2.5 billion which is historically a good outlook although it can have an impact on dividends.

Lockheed Martin accounts for 2.39% of the overall investment portfolio. In 2024, the company had a total return of 10.03%, less than the 16.8% total return of the S&P 500 Industrials Sector GICS Level 1 Index. Importantly, the company’s F-35 program was consistently behind schedule in 2024, leading the Pentagon test director to question service reliability. Q1, Q2, Q3, and Q4 had adjusted earnings per share (EPS) of 7.66, 7.11, 8.18, and 3.54, respectively. Notably, the fourth quarter saw a substantial decrease in EPS from the previous quarter because of an increase in the cost of goods and services. However, CEO James Taiclet has confidence in the continued production of 156 aircrafts per year starting in 2025, up from 110 total deliveries in 2024. Additionally, 96.3% of expert analysts recommend buying or holding LMT going into 2025. Ultimately, a large portion of LMT’s success will depend on the U.S. government’s geopolitical priorities, specifically with the F-35 program.

Waste Management (WM) has continued to perform well. In 2024, revenue grew to $22.05 billion, representing a 8% increase from 2023, with net income also rising by 19% to $2.75 billion. Additionally, the Q4 revenue of WM saw a 13% YoY increase. The year also marked significant progress in growth investments by an expansion into the solid waste disposal market through the acquisition of Stericycle, the largest provider of medical waste services in North America. The momentum across all these areas provides WM with a strong foundation for success in 2025.

L3Harris Technologies ticker symbol (LHX) is an American defensive contractor and technology firm. Over the last five years the stock has been down –10.36%. The firm reported a 3% increase in revenue this last quarter at $5.52 billion. Additionally, they reported EPS of $3.47 this last quarter, coming in slightly above expectations of $3.42. L3Harris is well positioned to benefit from increasing defense spending and global conflict. However, the firm faces risks of supply chain disruptions and policy uncertainty. In 2024, we sold out of this position in the firm’s stock, freeing up cash the fund’s managers wanted to use elsewhere.

Information Technology Holdings Performance

In 2024, the information technology (IT) sector demonstrated great performance; significantly contributing to broader market gains. The S&P 500 Communications Services and Information Technology index achieved a 37.39% return; following a 57% gain in 2023. This performance highlights the sector’s pivotal role in driving market growth.

The year began with heightened enthusiasm for artificial intelligence (AI) as generative AI technologies spurred innovation across various industries. However, mid-year developments introduced challenges including concerns over AI model reliability, ethical considerations, and escalating operational costs. These issues reduced initial optimism, shedding light on the complexities of integrating AI into business operations.

Cybersecurity emerged as a critical concern, with high-profile breaches uncovering vulnerabilities in critical infrastructure. Incidents such as the attack on Seattle-Tacoma International Airport and defenselessness exposed by cybersecurity providers like CrowdStrike emphasized the urgent need for robust defense strategies. This environment accelerated the adoption of compliance frameworks like CMMC 2.0, prompting organizations to implement proactive, threat-aligned defense measures. Cloud computing faced its own set of challenges, with service disruptions from major providers like Microsoft and AWS highlighting the necessity for resilient, diversified cloud strategies. The sector’s performance in 2024 underscores the importance of adaptability and strategic planning in navigating the evolving technological landscape.

Overall, 2024 was a year of significant transformation for the IT sector, characterized by substantial growth, emerging challenges, and a renewed focus on resilience and strategic innovation.

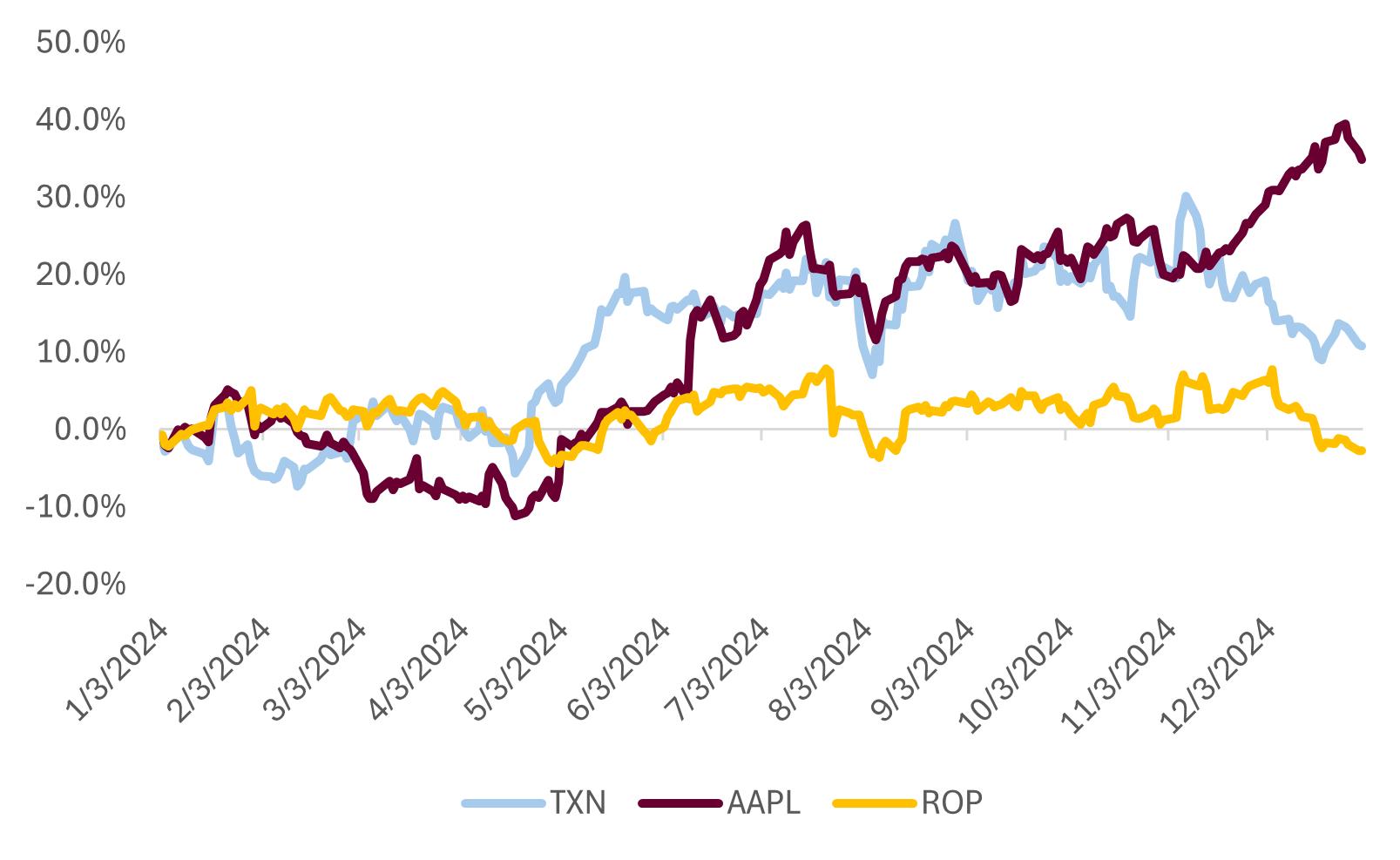

L3Harris Technologies ticker symbol (LHX) is an American defensive contractor and technology Apple’s stock performed very well in 2024 with a return of 30.71%, leading Apple stock to uncharted territory reaching new highs of $260.10 per share. This unwavering success can be attributed to its continuous growth in the consumer services market. With the launch of its newest iPhone, Apple has created significant noise around the implementation of AI, into their products. In 2024, Apple experienced revenue growth of 4% YoY from 2023. With new AI advancements and Apple’s fast-growing sector, their services sector has seen considerable revenue growth of 14% year over year from 2023 to 2024. Not only did their services sector experience significant revenue growth, but the company’s net profit margin increased 10% from 2023 to 2024. Apple’s ability to increase profit margins, maintain steady revenue growth, and consistently meet or surpass analyst expectations during the earnings season, contributed to a sharp increase in value in Apple’s stock during 2024. From now on, Apple will work to utilize AI in their hardware and services sectors to continue exceeding earnings expectations going into 2025.

We currently own 50 shares of ROP valued at $519.85 per share or ~$26,000 as of the close of 2024, which represents a 0.92% portfolio weighting. As for Q4, ROP was strong as they beat their estimated EPS of $4.53 by $.08 and revenue for the quarter reached $1.88 billion. In August 2024 ROP acquired Transact Campus in August for $1.5 billion while deploying a total of $3.6 billion towards acquisitions in 2024 indicating a strong M&A strategy and positioning ROP for strong growth in 2025.

We currently own 562 shares of TXN valued at $187.50 or $105,380 as of the close of 2024 with a current portfolio weight is 3.7%. Over the year, Texas Instruments stock price rose by ~15% which slightly lagged the broader semiconductor market for the same period. TXN is a strong cash generating company with extensive exposure to the industrial and automotive sectors. Some risks include fluctuation in cyclical demand as well as macroeconomic challenges. Q4 Revenue was $4 billion which is down nearly 2% from Q4 2023 with EPS of $1.30. Texas Instruments was awarded a portion of the $1.6 billion CHIPS and Science Act funding which can significantly offset R&D costs in 2025. The new CEO of the past year Rich Templeton stepped down on April 1st with Haviv Ilan being appointed to take over the next phase. Texas Instruments remains to be steadily growing with a Hold recommendation from many analysts.

Sector Returns

In 2024, the materials sector was the lowest performing among the S&P 500’s 11 sectors, declining 0.6% while the broader index rallied ~25%, weighed down by concerns over U.S. economic growth, China’s slowdown, and high interest rates. The energy transition drove demand for copper, lithium, and rare earth elements, but raw material price volatility and weaker global industrial activity affected prices, especially in steel and iron. Despite these headwinds, the sector has historically rebounded after down years. Falling global interest rates alongside potential stimulus from China could create a more favorable environment in 2025. However, President Donald Trump’s potential tariff policies on Chinese imports create uncertainty which can have a large impact on raw material costs and trade dynamics. While some industries, such as containers and packaging, outperformed in 2024, we will continue to analyze the materials sector as their recovery will depend on economic conditions, trade policy, and infrastructure investments.

The real estate sector in 2024 navigated a challenging yet potentially transformative landscape, with key trends continuing to shape the market. In the residential real estate segment, high mortgage rates, driven by central banks’ tightening monetary policies, have significantly slowed down the pace of transactions. Home sales and price growth have faced headwinds, though some regional markets continue to show resilience due to limited inventory and strong local demand. On the commercial side, the office space market remains under pressure due to the hybrid work trend, which has kept demand for traditional office buildings lower than in pre-pandemic years. However, certain sectors like industrial real estate, driven by the growth of e-commerce and supply chain optimization, remain buoyant. Additionally, the ongoing trend of urbanization in emerging markets presents long-term opportunities for both residential and commercial development. In terms of investment, REITs have faced mixed performance, influenced by interest rate hikes and inflationary pressures. However, a greater focus on sustainable and energy-efficient properties is attracting investor interest, particularly in markets where sustainability regulations are tightening. Overall, the real estate sector in 2024 is marked by challenges in some sub-sectors but offers targeted opportunities, particularly for investors focused on industrial, logistics, and sustainable property investments.

Utilities Sector (XLU) Return

Our current portfolio allocation in the utilities sector stands at 0.86%, significantly underweight compared to the S&P 500’s 2.32% weighting, leaving us 1.46% below the benchmark. In 2024, utilities rallied, recovering from 2023 losses, driven by surging AI-related energy demand, electric vehicle adaptation, and government incentives for renewable energy. However, the rally paused in Q4 2024 due to concerns regarding an increase in energy-efficient AI models, which could lower long term electricity consumption. Top performing companies in the sector included Vistra Corp (VST), Constellation Energy Corporation (CEG), and NRG Energy (NRG), all benefiting from increased demand from AI-powered data centers.

Looking ahead, key opportunities in utilities include rising electricity demand from AI-driven infrastructure and ongoing government contracts, such as the $1 billion federal investment into Constellation Energy. However, risks remain, including uncertainty over tax credits for renewable energy, interest rate pressures, and advancements in energy efficient AI that may reduce longterm power demand. Valuations are currently elevated, with a median P/E ratio of 18, nearing a 20-year high. Given our underweight position and the sector’s role in powering AI data centers, increasing our exposure would provide greater alignment with long-term growth trends and government backed energy initiatives.

NextEra is recognized as the world’s largest generator of renewable energy, which includes wind and solar. The company has reported a total revenue of $6.9 billion in 2024, which was a 4.97% decline compared to $7.3 billion in 2023. The stock has seen an increase of 25.18% over the past year, underperforming the benchmark (Utilities Select Sector SPDR Fund) which saw a gain of 29.15%. Even though the company missed its earnings in December of 2024, the company is still currently the leader in investing in renewable energy infrastructure and plans to add 5.4GW of solar and 3.4 SW of battery storage between 2026-2029. NextEra Energy is well-positioned for long-term growth as the company is aggressively expanding and demand for clean energy is increasing.

We sold out of our 280 shares of ED in early fall of 2024. In the fall semester, we had a series of small divestments in the Celani Fund, looking for a more concentrated, yet well diversified portfolio. At the time, the fund had 40 holdings, many of which were under 1% weighting, like ED, and the goal was to reduce this to around 25 holdings. We bought the shares of ED at $61.25, back in May 2013, and had seen a 70% gain on it since, making it worth around $30,000, which would be small in the portfolio. From September 2023 to September 2024, ED stock had seen 1.55% growth and showed stability but not much vision. Also, Consolidated Edison Inc. Is in the Utilities sector where we already were overweight by 2.17%. Even though it had performed well over the years, it was close to reaching its target price, and to follow with the fund’s goal we voted to sell it and use its funds to purchase more AMZN stock, on September 30th, 2024.

The GLD (US) investment has seen significant improvement since our initial purchase. We acquired 119 shares at $102.45, with a total principal investment of $31,404. At the end of 2024, this holding had risen to $242.13 per share, reflecting a strong upward trend in gold prices. This increase is driven by ongoing economic uncertainty, persistent inflation concerns, and global geopolitical tensions, all of which have strengthened demand for gold as a safe haven.

Recent signals from the Federal Reserve regarding potential rate cuts have supported gold’s rally, as lower interest rates tend to weaken the dollar and boost gold prices. With a low beta, this investment serves as a great hedge for the fund, and has performed exceptionally well, reflecting the broader strength in gold prices with a low beta due to economic uncertainty and inflationary pressures.

The Seger Fund continues to benchmark itself against the Russell 2000 ETF/B2000T, maintaining its focus on small and mid-cap equities. While the benchmark remained consistent, fund managers actively monitored all new small-cap positions to ensure alignment with investment objectives.

The fund maintained a significant weighting in energy, industrials, and consumer staples throughout the year. Exposure to information technology and financials increased, while the benchmark holding declined from 85.11% to 58.84% over the year. This reflected our goal of divesting out of the benchmark and investing appropriately into sectors that were underweight.

Similarly to the Celani Fund, we want to position the fund at approximately 30 names for simplicity of portfolio tracking and the CFA’s insight on how the advantage of diversification dwindles away in a small-mid cap equity portfolio after 25-30 holdings.

Russel 2000 Index

The Russell 2000 returned ~12% in 2024, slightly higher than its 9% 10-year average annual return. Small and mid-cap companies struggled at the beginning of 2024, due to the federal funds rate being at 23-year highs of 5.25%-5.5%, creating an increased cost of debt and, therefore, making it more difficult for small and mid-cap companies to innovate and drive growth. However, halfway through the year the markets began to expect the Fed to cut rates, and throughout the second half of 2024, small and mid-cap stocks collected 9.60% of the 11.38% return generated in 2024. Going into 2025, there is likely to be some volatility surrounding the small and mid-caps sector, particularly due to federal fund rate uncertainty, a potential uptick in inflation, and the expected “tariff wars” led by the current presidential administration.

Amicus Therapeutics (FOLD) was acquired in November 2024 and was purchased to offset our underweight holdings in the healthcare sector. FOLD was a unique option for an otherwise small corner of the health sector with large upside potential. Specializing in the global biotechnology industry, they focus on developing and delivering novel high-quality medicines for people living with rare metabolic diseases. The company generates more than 35% of its revenue from domestic operations with their highest earning product being their staple drug Galafold, which attributes more than 95% of the company’s total revenues. Pombiliti + Opfolda, the company’s second and newest drug with large upside potential, attributes to less than 5% of total revenues. Overall, company revenues have risen 119% in the last five years, with estimates showing steady growth. However, the company had a total loss of 32%, which could be attributed to unresolved challenges within the fundamentals of the business.

Throughout 2024, Clear Secure experienced heavy volatility, peaking at $38.70 on November 8th and finishing the year around $26. Ultimately, Clear Secure returned roughly 30% to its shareholders in the year 2024. During Q3 2024, Clear Secure reported revenue of $198 million, marking a 6.25% increase from the prior quarter. This growth was derived from an increase in demand for secure identity verification across the industries of aviation and financial services. The company’s entrance into financial services with its reusable KYC solution demonstrates its commitment to innovation and growth. Considering this, potential risks include market competition and the need to continually adapt to evolving security threats. As it stands in our portfolio, Clear Secure serves as a diversification into the growing field of biometric security and identity verification. Taking its recent performance and strategic initiatives into account, we will consider maintaining or slightly increasing our current holding in an attempt to capitalize on anticipated growth. Clear Secure’s focus on secure identity verification positions itself well for future growth. While the company has shown positive financial performance and is expanding its service offerings, investors should remain aware of the complex landscape and technological advancements in the security sector.

Comfort Systems USA’s stock price was $202.08 one year ago, and at the end of 2024, stood at $424.06 end of 2024, reflecting a price increase of ~$222 over the course of just one calendar year. During this period, the stock reached its highest price, peaking at $504.12, right before experiencing a significant drop to its current level. With a price-to-earnings (P/E) ratio of 35.44, the valuation is notably high. However, given the company’s strong growth potential, there is a compelling argument for maintaining the position and even increasing the investment to strengthen the portfolio. Currently, Comfort Systems USA represents 2.15% of the portfolio. Increasing this allocation to 5% could provide meaningful long-term growth, aligning with strategic objectives for portfolio advancement. With 18 shares currently held, increasing the position to 22-23 shares could be highly beneficial in capitalizing on the company’s prospects.

Golar LNG is a leading innovator in the LNG space, offering floating mobile processing and storage solutions (FLNG) to the oil and gas industry. GLNG performed very well throughout 2024, finishing the year at $42.32, generating an 82% return for the Seger Portfolio and outperforming the benchmark by 69.3%. Considering this, GLNG positioned itself as one of the best performing holdings in the portfolio and played a key role in generating positive alpha as well as moving the Sharpe Ratio in the correct direction. This expansion was generated by top line revenue growth, resulting from an increase in demand for FLNG via the clean energy movement. GLNG was also able to mitigate spot rate risk in the LNG market by locking in stable mid to long term contracts. All things considered, the future looks bright for GLNG as analysts foresee more FLNG conversion opportunities as the market’s preference pivots towards flexible LNG infrastructure, an area of expertise where they are the sole pioneer.

Perimeter Solutions (PRM) saw an outstanding 178% return in 2024, driven by strong growth and strategic advancements. The company, a leader in fire safety and industrial solutions, capitalized on its expanding product portfolio and increasing demand for its fire protection services. The upward momentum was fueled by significant investments in both innovation and market expansion. PRM’s stock price soared from $4.59 to $12.78; reflecting strong investor confidence and market optimism. This exceptional return demonstrates the company’s ability to generate significant value for shareholders and highlights its successful execution throughout the year.