29 minute read

Katharine Wilkinson

VOICES OF THE PANDEMIC

What We’ve Learned

Advertisement

We’re not connecting the dots between the pandemic and the climate crisis enough.

So much of what we have done is paint the picture of unfolding catastrophe, but we’ve done very little to paint the picture of what could be.

—Katharine Wilkinson

Writer, climate change activist, editor in chief of Project Drawdown, and cohost of the podcast A Matter of Degrees pulling in readers whom major news organizations hadn’t reached before. Google was founded in 1998, making those opinions easier than ever to find. Outlets’ audience sizes were poised to expand, but digital advertising rates amounted to a fraction of what they were for print, so large publishers mostly left those crumbs to the growing number of upstarts attempting to break through. Talking Points Memo, 2000. Gawker, 2002. Facebook arrived in 2004.

In 2005, at the spring meeting of the American Society of Newspaper Editors (now known as the American Society of News Editors), in Washington, DC, Rupert Murdoch, the founder of News Corp, gave an address. He told his colleagues that they were being “remarkably, unaccountably complacent” in the face of the digital revolution. “Like many of you in this room,” he said, “I grew up in a highly centralized world where news and information were tightly controlled by a few editors, who deigned to tell us what we could and should know.” Young people, he explained, were “no longer wedded to traditional news outlets or even accessing news in traditional ways.” He cited a report by Brown, published through the Carnegie Corporation, that found that people between the ages of eighteen and thirty-four were increasingly using the Web for news consumption; just 9 percent described newspapers as “trustworthy”; 8 percent found them “useful.” Murdoch concluded, “They want a point of view about not just what happened, but why it happened,” and “they want to be able to use the information in a larger community—to talk about, to debate, to question, and even to meet the people who think about the world in similar or different ways.”

The next month, the Huffington Post went live. Headed by Arianna Huffington—a writer, socialite, and former California gubernatorial candidate—the site was conceived as a liberal response to Drudge, with a splashy homepage full of stories cribbed from legacy publications. Huffington brought in Jonah Peretti, a former scholar at the MIT Media Lab, who coined the term “contagious media.” Under Peretti, the staff constantly monitored Google and generated stories tailored to show up in popular searches. Huffington also leaned on opinion pieces, by celebrities she knew

(George Clooney, Deepak Chopra, Nora Ephron) and anyone else who had something to say. Those submissions were unpaid, tremendous in volume, and highly clickable. “Opinions are essentially a form of rewrites,” Vijay Ravindran, a former chief digital officer at the Washington Post Company, told me. “Opinion is the easiest way to create breadth of content and then build the machine around that to get traffic.”

In 2006, as a side project, Peretti began working on what would become BuzzFeed. (“Originally, BuzzFeed employed no writers or editors, just an algorithm to cull stories from around the web that were showing stirrings of virality,” a profile in New York magazine explained.) The same year, Twitter launched and Facebook debuted its “share” button. Even if legacy publications didn’t yet want to believe it, the power of influence was shifting to those who best understood how to exploit the emerging technology. In 2007, the first iPhone shipped, signaling a new era of obsessive social media consumption; the following March, Facebook hired Sheryl Sandberg, from Google, to help the company grow. And soon it was the fall of 2008, when the Great Recession pushed print media’s advertising revenue off the side of a steep and deadly cliff.

Between 1999 and 2009, weekday newspaper circulation dropped by nearly ten million. In the first six months of 2009, more than a hundred newspapers shuttered; ten thousand newspaper jobs were lost. The New York Times was more than a billion dollars in debt. Increasingly, people were accessing the news not through traditional outlets, or their homepages, but by using search engines and social platforms. Facebook introduced the “like” button, making it possible to track what individuals were reading and to determine which posts to display prominently in news feeds. The effect on publishing, which until now had coasted on brand advertising, was severe. Digital advertising for newspaper websites “collapsed,” Ravindran said. “Facebook and Google had way more inventory and better targeting because of the amount of data they were working with.”

Publishers began to invest in trying to reach people—how to get shared and liked—and thus earn a cut of social media’s direct-response ad revenue. The most obvious strategy was to produce more stuff; the simplest way to do that with a dwindling bank account was to minimize reporting costs. BuzzFeed continued to develop virality algorithms (in 2010, the site’s most popular post was “Watch Miley Cyrus Take a Bong Hit”); the less sophisticated outlets commissioned pieces of interpretive analysis. Newspapers, seeking to distinguish themselves from the aggregators, began encroaching on the territory once held by the newsweeklies, which in turn drove more magazines into the chase for relevance, with commentary an obvious route. Opinion writing made sense editorially—it seemed a natural fit for the Web—as well as financially. “A huge factor in this is budget,” a longtime magazine editor told me. “Reporting is expensive, and it is just not as expensive to publish opinion writing.” More and more takes went up, in pursuit of clicks; by mid2010, Facebook had five hundred million users. “If your most fiery opinion story got a ton of page views, that was considered a huge success and that would help you drive up advertising rates,” Megan Greenwell, now the editor of Wired magazine’s website, said.

But even as publishers came to understand the dynamics of social media, that wasn’t enough to sustain a newsroom. In 2011 and early 2012, ten major papers, including the New York Times, erected paywalls; several hundred smaller outlets did the same. Between 2011 and 2013, the number of visitors to the Times homepage plummeted from more than one hundred forty million to around sixty million. By then, more than a billion people were on Facebook, which changed its algorithm to emphasize journalism in the news feed. Jeff Bezos bought the Washington Post and expanded its digital presence. Every media outlet was now eagerly feeding the beast, yet it was clear that the revenue trickling in from direct-response ads couldn’t replace brand marketing. “You can’t think about editorial product in isolation from technology and business,” Kinsey Wilson, the former editor for innovation and strategy and executive vice president of product and technology at the Times, told me recently. “It doesn’t mean that you violate ethical norms, that you allow business to have undue influence over your editorial product. But there has to be a level of coordination.”

In June 2014, the Times introduced NYT Opinion, a stand-alone subscription and app that offered access to opinion coverage (including editorials, columns, op-ed pieces, and “Op-Docs”) along with additional features like Q&As in which writers responded to reader questions and comments. NYT Opinion also offered commentary from elsewhere around the Web, curated by Times editors. The idea was to draw an audience that wanted to read more than the ten free articles available per month, and liked opinion, but who weren’t yet ready to commit to a full Times subscription. (NYT Cooking went live around the same time.) But it was a short-lived experiment, discontinued just four months after it began. NYT Opinion “hasn’t attracted the kind of new audience it would need to be truly scalable,” the bosses wrote in a memo to staff. Ben French, who held various product roles at the Times, told me, “The truth is, what we found is that people didn’t really want to just buy a chunk of our coverage. It needed to have some utility and some sense of purpose, and opinion sitting by itself—you want to be able to read a news story and then read an opinion story about it.”

The next fall, the Times decided to commit fully, announcing that it would pursue a subscriber-first business strategy aimed at

multiplying its “deeply engaged” digital audience. The hope was that, if the Times could double its digital revenue by the end of 2020, the newsroom would be in healthy enough shape. The opinion section—a place to experiment ambitiously with voice and subject matter, where columnists could forge lasting connections with their followers—was a promising department for growth. “If you go back to the idea of the habitual reader, opinion columnists are precisely the kinds of writers who attract repeat visits and drive habitual behavior,” Wilson said. To lure new subscribers, the consensus was that the Times would need a greater variety of opinion contributors. “People should see themselves reflected in the Times,” Tyson Evans, a senior editor for opinion product and strategy, told me. “I think opinion is a pretty powerful place to do that at scale, quickly and effectively.” No matter whether a newsroom was chasing virality or subscriptions, it seemed, commentary was king.

The 2016 presidential election was rough. Afterward, amid widespread criticism that Facebook had allowed itself to be used as a vehicle for Russian meddling, the company quietly began tinkering with its algorithm to de-emphasize posts from media outlets. In 2017, Facebook-driven traffic to media companies dropped by 15 percent. At Slate, between January 2017 and May 2018, traffic from Facebook fell by 87 percent. By then, for the first time, more Americans were getting their news from social media than from newspapers. “We’ve all been buffeted by the changes and the force of the algorithms, and the force of competition,” David Shipley, who heads Bloomberg Opinion, told me.

But the New York Times was doing okay. Bennet, who had been hired in 2016, was tasked with expanding the opinion section’s domain. Donald Trump’s victory—and the shortfalls of the Times and other news outlets in covering the story—led Bennet to a conclusion about the political orientation of his writers: “There wasn’t really an advocate for the Bernie Sanders view of the world formally in our pages,” he told colleagues at a staff meeting. “And we’ve had fewer voices to the right for quite some time.” He hired Lindy West, an author who contributed to Jezebel; Michelle Goldberg, a former writer for The Nation; Bret Stephens, a Wall Street Journal conservative skeptical of the climate crisis; and Bari Weiss, another Journal expat, who has a Zionist focus. (The Intercept observed that the additions “hardly” brought diversity to the editorial page.) The new columnists spoke to specific audiences that the Times—through data analytics and interviews with demographic groups, as well as a general envy of the Journal’s hold on conservative readers—had deemed promising subscriber targets. By December 2017, when it was announced that A.G. would be made publisher, the Times story covering the news declared, “With 3.5 million paid subscriptions (2.5 million of them are digital-only), The Times is one of the few newspaper companies whose newsroom is growing at a time when the industry is struggling.” The opinion section was producing less than 10 percent of the Times’ total output, yet opinion pieces represented 20 percent of all stories read by subscribers—which meant that the takes were punching well above their weight.

The subscriber model attracted more believers, with commentary an inexpensive way for an outlet to assert its value and build customer loyalty. The Washington Post launched a global opinions section, hiring a slate of new columnists to weigh in on international affairs; after that proved successful, the Post hired a half dozen more, running an additional page of opinion in its print edition three days a week. A Post spokesperson told me that opinion has accounted for “some of the top subscriber-converting content from the newspaper.” In March 2018, The New Yorker announced its intention to double its paid circulation, to more than two million, and hired more writers who could chime in online with their thoughts about American democracy, “Insta-celebrity engagements,” and everything in between. Editors talked less about virality and more about the number of minutes readers spent with each article. “In the time I’ve run newsrooms,” Greenwell told me, “deeper engagement is certainly what’s strived for and certainly what business partners—whether they’re advertisers or sponsors of some sort—seem to care about.”

Still, consciously or not, social media remained an important factor in everyone’s judgment. “You look at the Twitter competition for followers among pundits—it’s intense,” Brown told me. “In the world of punditry and opinion, it drives things. Writers are hired, and raises are given, based on Twitter engagement. It’s in many ways defining.” Plus, there’s fomo. Having adapted to a relentless pace, it now feels impossible to drop out. “There was a time when the president was giving his acceptance speech at the convention on a Thursday night, the editorial board would listen, and on Friday morning they would meet and discuss it; somebody would write an editorial, the editor would edit it, and we would publish it thirty-six hours later, on Saturday morning, and that would be fine,” Hiatt said. “If I did that now, I’d be a laughingstock. It’s gone from No, we have to be in the next morning to If we’re going to have a response, we have to have a response that night.”

When opinion writers publish pieces that contrast with facts reported by journalists under the same banner, staffers have little recourse. Vox argued that, in the Bennet era, opinion had “elevated trolling the Times’s liberal readership into a kind of raison d’être.” Opinion is separate from the newsroom— Bennet reported directly to A.G.—but most readers have never made that distinction. “Does op-ed care at all about how its actions affect the newsroom whose legitimacy and sweat it trades on in order to sling hot takes?” a Times staffer complained. “It’s not clear that they do.” Even within the paper’s opinion section, Bennet’s sense of mission differed from others’—and the Cotton piece proved how far apart they were. There was a feeling of being “disempowered in ways that may have prevented this from happening,” a Black employee, who spoke on the condition of anonymity, told me. “Of all the people in opinion who could’ve read it, there were no people of color who did a first read. James didn’t find it important enough to read.” (A Black photo editor had voiced objections that went unheeded.)

The Cotton op-ed was so offensive that Times employees were moved to act; a Twitter campaign, created by Black staffers and amplified by colleagues, protested the piece. An apologetic editor’s note was appended to the top; Bennet was replaced. A.G. managed, mostly, to ride out the uproar—vowing in meetings, emails, and calls to make a lesson of the op-ed fallout. Dean Baquet, the executive editor, said he felt proud of how members of the newsroom banded together to stand up for what they believed. (Though they had all tested the limits of the company’s social media rules, no one seems to have been punished; there was strength in numbers.) What, exactly, the Times learned from the episode remains uncertain, however. To what extent did the editor who shepherded the Cotton piece, a young man who’d come from the Weekly Standard, believe that he’d be rewarded for delivering virality? Where did the leaders of the Times set their limits on opinion—and where will they, in the days ahead? In October, with Bennet long gone, the Times published yet another stinker: an opinion piece by a Chinese apparatchik advocating a crackdown on protesters in Hong Kong.

Budget-wise, the outlook is clearer: the New York Times met its ambitious digital revenue goal a full twelve months ahead of schedule. Today, with more than six million subscribers, it’s safe enough, one might infer, for A.G. to commit to diminishing the opinion output to protect the reputation of the Times. (BuzzFeed is now in the more difficult position; in the past two years, hundreds of employees have been laid off, and Peretti told the remaining staff that he hopes to keep 2020 losses below $20 million.) “Trying to publish hot takes that go viral on Twitter for being most outrageous is sort of a sucker’s game,” Ben Smith—the former editor in chief of BuzzFeed News, now a media columnist for the Times—told me. “It always struck me as an unsustainable thing. Brands are defined by their highest-profile work, and if it’s a bad take, that’s a problem.” He added that “places still tend to be defined by their opinion writers, even if they are doing less of it.”

It occurred to me, as I surveyed the world of takes, that John B. Oakes would be satisfied—there is no question that we now have “diversity of opinion,” which he called “the lifeblood of democracy.” Nobody is worried anymore about a lack of published thoughts. The problem today is democracy, and making sure the opinions that circulate are those that serve it. cjr

Enrique Abeyta, a former hedge-funder, goes all in on metalhead media

AUTHOR Alex Norcia

ILLUSTRATOR Esther Wu M att Saincome was used to ignoring people. In 2014, he and his friend Bill Conway cofounded The Hard Times, a satirical website often described as a hardcore version of The Onion, and ever since they had been shooing away potential buyers. There were Hollywood types who wanted to turn The Hard Times into a BuzzFeed-like YouTube channel, tech companies that hoped to optimize the ads, larger magazines that offered to remake the site as a comedy show. For almost six years Saincome, a former music editor at SF Weekly and the more business-savvy of the two, listened to every proposal and rejected all of them. So far, he and Conway had been self-reliant, with no outside funding; they weren’t looking to sell. And that was an accomplishment. Especially when you consider that their scrappy enterprise had survived the media industry’s most tumultuous time—as hedge funds and private equity firms became notorious for buying up suffering local newspapers and digital properties, then stripping them for parts. Saincome likes to say The Hard Times was “born in the shit”; a more pleasant image is that it was nimble and slim, relying on a stable of paid freelancers who believed in the vision. Layoffs, pivots to video, Hulk Hogan: Saincome and Conway didn’t have to deal with any of that. They had the luxury of not being in financial trouble.

Saincome’s thinking hadn’t changed last October, when a stranger cornered him during a Hard Times book launch at Saint Vitus, a metal bar in Brooklyn. It was yet another guy saying that his company—some firm created by Wall Street shakers—was keen on buying The Hard Times. As usual, Saincome agreed to chat. He figured he had nothing to lose from hearing the man out.

By May, The Hard Times had been sold to Enrique Abeyta, a former hedge fund manager, who acquired the site through Project M Group, his digital media and e-commerce company. Founded in 2017, Project M is helmed by Abeyta, who serves as the CEO, and Skip Williamson—a

financial strategist turned independent record label executive and Hollywood producer, whose title is chief creative officer. “These guys quit Wall Street,” Saincome told me. “They’re huge metalheads.” The name Project M is an in-joke, an allusion to the fact that investment bankers don’t label their projects what they actually are, fearing that documents might leak into the market. The M might stand for metal, media, monetization. Abeyta won’t say. “If you want to paint Enrique as a guy who is investing in publications and not harming them, that’s a hundred percent correct,” Saincome said. “He really is more similar to me than you would expect.”

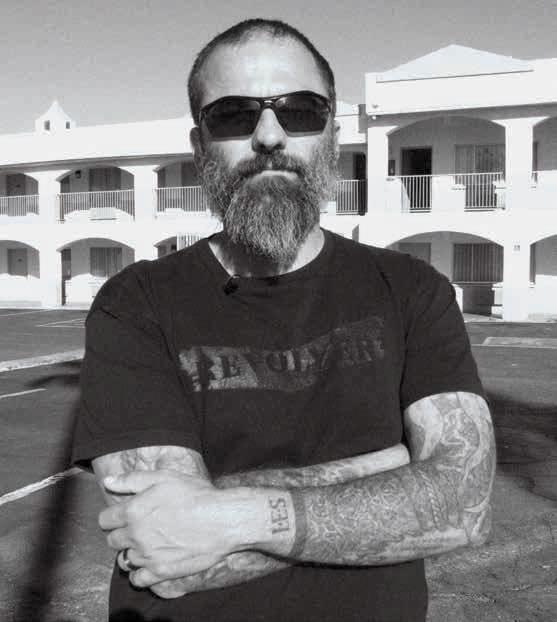

A self-made millionaire and secondgeneration immigrant with tattoos on the side of his head, a mangy beard, and unkempt hair that resembles a mohawk, Abeyta, who is forty-eight, jokes that he looks like a pirate. He has seen the band Tool in concert at least forty times. His buddies call him Rick. When we met, he wanted to show me he isn’t like any other hedge-funder I may have come across. He rattled on with the assured vulgarity of a Guy Ritchie character—“fucking Yelp,” “fucking tattoos,” “the fucking Yankees”—and at times sounded like a slam poet. His favorite metaphors involve the ocean: he rode the nineties hedge fund wave, saw the tide of local news “going out in front of a tsunami,” showed his employees how to surf the startup waters. He does not do well with silences; he is constantly about to say one last thing. “People like goblins and ghouls and witches and gods,” he told me. Then he added, “Everybody wants a bad guy.” He doesn’t believe he is one.

It was only a few years ago that Abeyta put on a tie for work. At the end of his hedge fund days, he was a senior analyst at Falcon Edge, in Manhattan, earning seven figures. (The chairman, Rick Gerson, is a good friend of Jared Kushner’s and later became wrapped up in the Robert Mueller investigation.) Abeyta’s attention often wandered toward media properties and direct-to-consumer companies; in 2016, he closely followed the success of the Chernin Group, the investment advisory firm that bought a majority stake in Barstool Sports, and the CHIVE, a photo blog that slapped Bill Murray’s face onto T-shirts. Seeing vertical integration—of journalism and consumer goods—piqued Abeyta’s interest. So when a mutual friend introduced him to Williamson, and Williamson made him a proposition—a venture in publishing that would capitalize on the fan base of metalheads, their kin—it lured him. He’d already had years, he said, when he “made seven figures, lost seven figures, and made something in between”; he was accustomed to volatility and ready for the next thing. He abandoned his comfortable salary and invested what became $2 million in Project M.

Abeyta and Williamson set off with a mission: first, they would buy struggling or underperforming media companies with passionate, niche audiences with whom they identified; second, they would resurrect those companies with capital; third, they would sell merchandise to their enlarged reader base. Before The Hard Times, they acquired Revolver (heavy metal) and Inked (tattoos). “My life’s work has been to study strategy in media, as part of my investing,” Abeyta said. “I’ve always been a student of the game. At my last firm, they called me the master of the ‘Game of Thrones,’ because through time, I had a great ability to identify moves in the media space by thinking strategically.”

Abeyta was indeed different, though he fit a type: he reminded me of Bryan Goldberg, the founder of Bustle Digital Group, and Shane Smith, my old boss at Vice—bloviating men whose braggadocio could eclipse common sense. It’s considered prudent to be wary of those guys, yet by making Project M in his image, and insisting to editors that his hedge fund days are behind him, Abeyta has managed to sell people on his alt-finance-bro brand. “What we try to do as a great partner is, we say, ‘Here’s how you can own a stake in this, here’s how you can do more of what you love to do, and we can do all the crap that you don’t like to do and also put you in a position to do more cool shit,’ ” he said. It helps that Project M has managed to turn a profit. Saincome told me, “It seemed like a perfect fit.”

n late July, I drove north of Phoenix, past thousands of acres of untouched Sonoran desert, to a small town called Cave Creek, where Abeyta was living with his wife and children. He compared Cave Creek to Marin County, by which he meant that it’s

ENRIQUE ABEYTA A media investor who left hedge funds for heavy metal, he’s moved from Arizona to Wall Street and back again.

far enough away from Phoenix (an increasingly liberal-leaning city) to maintain its own libertarian idiosyncrasies. Sometimes Cave Creek makes national news: in 2009, for instance, a judge decided the outcome of a tied council election with a deck of cards; this year, as Arizona became a hot spot for covid cases, the Wall Street Journal reported that a popular saloon in Cave Creek waited until the end of June to require masks. Abeyta asked me to have lunch at a Wild West–themed restaurant in town called the Horny Toad. After we sat down, and there was a brief lull in our conversation, he took out his George Costanza–size wallet and showed me a deposit slip: it was the first million in his bank account, he explained. He’d kept it for years, as a memento, the numbers faded from rubbing against credit cards. He continued on, narrating the story of how he amassed riches. A few times, I heard him say, “I made money on 9/11.”

Abeyta has always been driven by a desire to earn. His father, a Mexican American from New Mexico, was often out of work and suffered from alcoholism; his mother, born in Uruguay, left her homeland in the late sixties, a few years before a military dictatorship took over. They bounced around; as a child, Abeyta lived in Utah, Colorado, and Spain before settling in Phoenix. For a few nights, his parents couldn’t afford the motel where they were staying, and they were kicked out, homeless. They slept in the car. “Being poor sucked,” he said. “I wasn’t really anything except poor. I don’t really know that you get a chance to develop much of a personality in that situation.”

He did, anyway. He collected comic books; he played Dungeons and Dragons. He was gifted and popular, he told me, while maintaining a self-proclaimed “edge.” In high school, he was the freshman treasurer, the sophomore president, the junior president; his senior year, in 1990, he was the salutatorian and voted “most likely to succeed.” He interned in the office of Sen. John McCain. When it came time for college, what he wanted most was to learn the quickest, surest way to get rich. So he chose to attend the University of Pennsylvania’s Wharton School, where he earned a BA in Asian and Middle Eastern Studies and a BS in economics. His friends were pedigreed; they liked chatting about stocks. He pledged a frat (Sigma Alpha Epsilon), signed up for investment management clubs, and rose to be the editor in chief of The Red and Blue, a conservative newspaper. He met a Jewish woman and adopted her religion. (He continues to pray.)

In 1993, Sponsors for Educational Opportunity, a nonprofit that helps young people from underserved communities land jobs, placed him in an internship at Lehman Brothers, which led to a full-time position.

Bad Boys

When investors show up, promising to reinvent or save the news industry, it often portends chaos. Some of the most notorious figures have cost thousands of journalists their jobs. —Feven Merid

Heath Freeman Known as a “vampire,” Freeman owns more than two hundred outlets through his hedge fund, Alden Global Capital. Since taking control of Digital First Media, in 2011, Alden has cut two out of every three staff positions in its newsrooms. After the Denver Post went through Alden’s layoff procedures, Freeman bought a $4.8 million mansion, the price of which could have paid the salaries of twenty-five Post reporters for more than two years.

Shane Smith A cofounder of Vice, Smith presents himself as a punk pioneer of digital media; his antics and lies have attracted investors, but also resulted in financial disaster. His former girlfriend told New York magazine, “Shane would talk all the time about how stupid people were for giving them money.”

Bryan Goldberg A founder of Bleacher Report, Goldberg went on to become a media slumlord with the Bustle Digital Group, which owns Bustle, Elite Daily, Mic, and other outlets. He slashes and burns and union-busts; in 2018, he bought Gawker. Elizabeth Spiers, a founding editor of Gawker, has called Goldberg’s strategy “Lazy Entrepreneur Solipsism.”

Jim Spanfeller In the aughts, Spanfeller oversaw the website of Forbes; in 2019, when Great Hills Partners, a private equity firm, acquired G/O Media, he was installed as CEO. At Deadspin, Spanfeller ran headfirst into conflict; after the site’s editor submitted her resignation, he “let out a cruel barking laugh.” Soon, all twenty people working for Deadspin quit.

Anthony Melchiorre As the founder of Chatham Asset Management—the hedge fund that owns American Media Inc.— Melchiorre publishes the National Enquirer and other tabloids. Chatham acquired McClatchy’s newspapers, including the Miami Herald, the Kansas City Star, and the Sacramento Bee. Melchiorre has been called (by his former boss at Morgan Stanley) a “street fighter”; as a press boss, he’s kept a lower profile.

Guy Gilmore The COO of Digital First Media Inc., a newspaper publisher owned by Alden Global Capital, Gilmore waited just a week after the East Bay Times and the Mercury News had won a Pulitzer Prize to cut twenty positions from those newsrooms. Recently, Gilmore opted to outsource news design of Digital First’s California newspapers to the Philippines, shrinking the staff even more. A former colleague of Gilmore’s told The Street, “He may not be that popular with those who work for him, but he makes his numbers.” He started as a technology media telecom banker, then transferred to hedge funds. At the time, the World Wide Web was beginning to emerge, and hedge funds were booming— not only because of penny stock fraud, but also thanks to legal data gathering; smaller funds could make big money fast. Abeyta began at Atalanta Sosnoff, where he became fascinated by the consolidation of radio stations and newspapers. His boss had voting shares in the New York Times; Abeyta sat in on some meetings with the paper’s management, taking notes. Fox News debuted in 1996, and when the parent company, Fox Entertainment, went public, Abeyta, then in his mid-twenties, met Rupert Murdoch in a conference room at the World Financial Center. He was enamored. “Whatever you may think of men like Murdoch, he was an incredible business and value builder,” Abeyta said. “My views on journalism and media weren’t made up with me in front of a fucking screen, blogging.” Abeyta’s other idol is John Malone, the chairman of Liberty Media Corporation, which controls SiriusXM, among other holdings. Over the years, Abeyta told me, he invested between $2 billion and $3 billion of his clients’ money in Liberty Media, and flew out to Denver to meet with Malone. (Through a spokesperson, Murdoch declined to comment for this article; Malone’s flack did the same.) When I pressed Abeyta on what, specifically, he learned from these men, he compared himself vaguely to a line cook shadowing a great chef. “It’s a million things,” he said. He seemed to be overstating his proximity to his heroes, but in any case, a lesson stood out: both Murdoch and Malone had a knack for constructing “flywheel” businesses—grouping media assets together. They were rulers of kingdoms.

Abeyta came to view the stock market as “the most fascinating intellectual monetary competition in the history of humanity” and to pride himself on being “a great intellectual athlete.” In the aughts, he continued to play. In 2001, he built his own fund with a few partners; in late 2007, he cashed out and started another. He developed a reputation for being able to extract commitments from institutions and high rollers. (“He says that he’s a ‘make money’ investor—I loved that phrase,” Whitney Tilson, an ex–hedge fund manager who runs a newsletter service called Empire

In Abeyta’s view, the problem with Wall Street plundering the press hasn’t been the downfall of journalistic scrutiny, but that nobody’s earned enough money to make the effort worthwhile.

Financial Research, told me.) Abeyta was an active short seller. Then the Great Recession hit, in 2008, which marked the end for many newsrooms across the country, their demise accelerated by Abeyta’s colleagues.

In the past decade, hedge funds and private equity firms have colonized the media, as the main bidders for financially strapped local newspapers and digital properties that were now distressed assets. Abeyta observed two ways in which his cohort approached the press. First, there was slashing: buy a declining business with an assist from the bank, cut costs, and recoup more than originally invested. This has been a popular tactic at local newspapers, where reporters have lost their offices and careers by the thousands. (“Newspapers are dead,” Abeyta told me. “I hate to say what they’re doing was going to happen one way or the other.”) The most feared and despised predator in this category may be Heath Freeman, the president of Alden Global Capital—which owns or has a stake in some two hundred newspapers, including the Chicago Tribune and the Denver Post. In a major bid in August, Chatham Asset Management, an investment advisory company, won the bankruptcy sale of McClatchy and its dozens of local papers (the Miami Herald, the Sacramento Bee). It’s difficult to estimate just how much money these firms are making, but in 2017 Ken Doctor, a news industry analyst at Nieman Lab, reported that Alden was enjoying profits of almost $160 million from Digital First Media, just one of its assets.

The second move, Abeyta went on, was the “next-gen version,” or consolidation. “If I own ten newspapers, and all of them have an ad sales person, and all of them have a digital person, and all of them have somebody in logistics, I can ditch nine of those ten people and stick with the newspeople,” he said. “And you used to have twenty tenured reporters, and their”—the investors’—“belief is, ‘I can go find three college kids who are bloggers that can do the same thing.’ ” He gave as an example Maven, a digital-platform company that last June added Sports Illustrated to its roster of titles, which also included Maxim, Ski, and History. The new managers promptly laid off the most respected and best-paid staffers and later revealed that they would hire a few less experienced, lower-compensated replacements.

Abeyta wasn’t impressed by either strategy. “You’re still playing in the same revenue pool,” he told me. The media industry is brutal; advertising is no longer a reliable source of cash. “These hedge funds, they don’t know jack shit,” he said. “I was one of these guys, and I thought I was pretty smart about this. I had so much to learn.” In his view, the problem with Wall Street plundering the press hasn’t