Tomorrow’s UNI, by your side

REPORT ANNUAL2022

UNI Financial Cooperation Headquarters

295 Saint-Pierre Boulevard West

P.O. Box 5554

Caraquet NB E1W 1B7

© UNI is a registered trademark licensed to Caisse populaire acadienne ltée for use in Canada.

2 Annual Report 2022

UNI Financial Cooperation 3 Table of contents Year in brief Message from the president and CEO Message from the chair of the board 2022 Achievements 19 Strategic priorities achieved 20 UNI fully growing into where it is great to work 25 Business development 26 Together with the community 28 Cultural change 29 Community presence Management’s discussion and analysis Consolidated financial statements 9 5 13 16 34 60

4 Annual Report 2022

Year in brief

UNI is a financial cooperative that focuses on the sustainable prosperity of UNI and its members. Since 86 years, UNI contributed to the economic stability of the communities in which it operates. Through its cooperative mission, it encourages and promotes citizen participation in a changing world.

187 200 members and clients

Financial results

1000 employees

58 business locations and regional offices

$5.4 B $30 M $235 M in assets

Community impact

We invest in initiatives and causes that create and enhance local prosperity and vitality.

$2.7 M in donations, sponsorships and scholarships

$7.5 M

in individual dividends

36 members

on 3 regional cooperative committees

Year in brief I UNI Financial Cooperation 5

surplus of in operating income up 2.7% up 7.4% up 8.6%

What drives us

Our Purpose defines us and gives meaning to our actions.

Our core values are the guiding lights we follow to achieve our Purpose.

Solidarity Responsibility Courage

At UNI,

Solidarity means we are UNIted in the pursuit of a common goal

Responsibility means we lead and take ownership for our decisions, even in challenging times

Courage means we reject complacency

UNIted for a prosperous UNI and its members

6 Annual Report 2022 I What drives us

Solidly rooted across the province

www.uni.ca/en/uniassist

VIRTUAL CAISSE Online and mobile services available around the clock, 365 days a year.

ONLINE SERVICES

CLIENT CONTACT CENTRE 1-888-359-1357 Monday to Friday | 9 a.m. to 5 p.m.

Business locations

Edmundston Clair Bathurst Petit-Rocher Beresford Paquetville Saint-Quentin Kedgwick Campbellton Eel River Crossing Caraquet Tracadie Sheila Neguac Baie Sainte-Anne Shippagan Lamèque Grand-Sault Saint-Léonard Fredericton Richibucto Saint-Louis Bouctouche Cocagne Saint-Antoine Moncton Memramcook Shediac Grand-Barachois Cap-Pelé Rogersville Dieppe

Log in 24/7

UNI

UNI Business UNI Wealth

Find us at facebook.com/unicooperation linkedin.com/company/uni-cooperation-financiere instagram.com/unicooperation twitter.com/UNIcooperation

Solidly rooted across the province I UNI Financial Cooperation 7

Insurance

Management

youtube.com/caissespopulaires

8 Annual Report 2022

Message from the president and CEO

Dear members and clients,

Our financial cooperative had another remarkable year in 2022. Remarkable in an economy that remains turbulent and in a financial industry that is undergoing rapid technology transformation. Our current successes are an opportunity to appreciate the road travelled over the past five years.

Let’s say it. Ever since 2017, the UNI team has looked ahead to anticipate what UNI would need to continue operating confidently in a larger and more complex financial ecosystem than ever before. We boldly came up with innovative solutions and strove for excellence. We also developed internal talent and recruited new ones. Our strength is rooted in the pride of our employees. We have built a solid corporate culture that has garnered acclaim and awards in Atlantic Canada and across the country.

Our exceptional growth—from $4.2 billion to $5.4 billion in assets between 2018 and 2022—has given us the leeway to make strategic technology choices. These choices will make us more agile and flexible for years to come. Our prosperity over the past five years will give us the means to succeed in the future.

That same prosperity has enabled us to distribute $25 million in individual member and group dividends to our members and communities over that period.

The road we have travelled since UNI was created is one of solidarity, responsibility and courage. It has led to our success today, a reflection of the resilience so typical of the Acadian people.

Financial highlights

In 2022, our consolidated financial results showed significant growth. Surplus earnings before other items as at December 31, 2022, were $30 million, up $2.1 million compared with 2021. These are the best consolidated financial results of the past eight years. The member loan portfolio passed the $4 billion mark in 2022.

For the first time in its history, the UNI board of directors authorized, in 2021 the payment of individual dividends totalling $7.5 million. With the addition of enhanced group dividends to $2.7 million, a total of $10.2 million will have been distributed in 2022.

As of December 31, 2022, UNI’s total assets were $5.4 billion, up 2.7% over 2021. Given this outstanding performance, the board of directors has authorized, for a second consecutive year, the payment of individual dividends. These individual dividends will total $5 million and will be distributed in 2023.

Being there for you

Your needs are changing, and that is why UNI is changing. As we continue our business development and the evolution of our service offerings, we are moving towards a new generation of online services aligned with our increasingly digital world. This shift, like our technology transition, comes with a promise: We’ll be there supporting, guiding and advising you.

UNI highly acclaimed

The core of a successful business is the employees. In 2020, we launched a major overhaul of our corporate culture and talent management. Two years later, our collective efforts have earned wide acclaim. UNI earned four major awards. To me, they show that it is possible to succeed here at home in New Brunswick.

Message from the president and CEO I UNI Financial Cooperation 9

10 Annual Report 2022 I Message from the president and CEO

UNI was awarded the Impact Award from Opportunities NB for its positive impact on the province. This award recognizes a company that demonstrates its commitment to New Brunswick and continues growing its local presence through reinvestment.

UNI is also the recipient of Waterstone Human Capital Canada’s Most Admired Corporate Cultures recognizes best-in-class Canadian organizations with outstanding corporate cultures that provide a competitive edge.

Atlantic Business Magazine

Atlantic Canada’s Best Places to Work recognizes nearly 200 Atlantic Canadian employers who have the best practices as rated by their own employees. An award based on the appreciation of UNI employees that helped UNI to rise to the rank of 2nd best employer in Atlantic Canada.

Atlantic Canada’s Top Employers recognizes the Atlantic provinces employers that lead their industry, those whose culture is tailored to the needs of their employees and communities.

These awards celebrate our hard-working, dedicated staff for their know-how, commitment to clients and active presence in the community day in and day out.

UNI: Initiatives that matters

One of the strengths of the cooperative movement is our involvement in our communities. For the third year running, UNI’s Voilà! contest awarded up to $300,000 to five visionary and sustainable projects. Because we’re building tomorrow today, we handed out $150,000 in scholarships to New Brunswick post-secondary students. The Bénévolat de l’année contest enabled our 3 award-winning volunteers to give a total of $9,000 to the causes they support.

Tomorrow’s UNI, by your side

In closing, I would like to express my heartfelt appreciation to each member of the board of directors for their vigilance in ensuring that the modernization of our financial cooperative is a success. I am grateful for the board’s support

and confidence in the senior management team as we fulfill our duty of keeping UNI running smoothly and contributing to the vitality of our communities. In our fast-growing industry, it continues to be an honour for me to be accompanied by people who are deeply committed to the cooperative movement and believe in New Brunswickers’ talents.

I would also like to warmly thank all the employees who, through their tremendous commitment to UNI, bring our corporate culture to life as they build the UNI of tomorrow. Launching a technology modernization initiative two years into a pandemic requires courage, resilience and solidarity, as well as an ongoing commitment to serving our members and clients. For all these qualities, I dedicate the four awards UNI received to our employees.

I also want to thank our members and clients for their trust. It is an honour to support you in the activities that matter to you.

Robert Moreau President and CEO

Robert Moreau President and CEO

It is a privilege to build the UNI of tomorrow with you all.

Executive Committee

SUPPORT INSTITUTIONS

Fondation des Caisses populaires acadiennes

ACADIA SERVICE CORPORATION Acadia Service Centre

ACADIA FINANCIAL HOLDINGS

UNI INSURANCE

Acadia Life

Acadia General Insurance AVie

Robert Moreau, FCPA, CGA, ICD.D President and CEO

Derrick Smith Chief Information Officer

Éric St-Pierre, CPA, CMA Vice-President, Finance

Gilles Lanteigne Chief Operating Officer

Marc-André Comeau, Vice-President, Personal Solutions

Stéphane Dorais Vice-President, Commercial Banking & Strategic Partnerships

Mario G. Patenaude, CHRA Vice-President, Talent Management

UNI FINANCIAL

UNI BUSINESS UNI WEALTH MANAGEMENT operated

business locations

4 regional offices

2 regional offices

Sylvain Fortier, CERA, ASA Chief Risk Officer

COOPERATION

35

operated

operated

Executive Committee I UNI Financial Cooperation 11

12 Annual Report 2022

Message from the chair of the board

Despite global socioeconomic uncertainty 2022 was another exceptional year for UNI. This past year has bolstered our confidence in the future and empowered us to bring the strength of New Brunswick’s cooperative movement to life. The past 3 years have shown us how resilient UNI can be in order to stay close to our members and clients.

A forward-looking board of directors

Once again this year, the board of directors supported senior management in advancing major projects. Every decision the board makes is about UNI’s prosperity— consolidating it and making it sustainable. The members of the board of directors wish to continue in the footsteps of our predecessors who built the movement we know today. We want to leave a solid business to future generations, one that can continue to be a leader in supporting community development.

Success takes planning, so those who achieve it—especially during periods of inflation and the uncertainty it brings—show great talent.

In recent years, UNI has been fortunate to have a responsible board of directors with an unflagging focus on growing and moving our institution forward. I would like to acknowledge the courage of the forwardlooking directors who keep UNI vibrant and prepare it for the 21st-century world

of finance. To empower our directors to continue growing the company, certain rules were changed.

A visionary president and CEO

We are proud to have a president and chief executive officer who does an excellent job of oversight and has a remarkable ability to anticipate changes in the financial industry.

I can attest to the board’s confidence that the ongoing transformation of our financial cooperative is aligned with our strategic direction. Thanks to our CEO and the senior management team, we now have a corporate culture that shines throughout Atlantic Canada and across the country. Our culture makes us better and readies us for upcoming changes in the industry and at UNI.

Preparing for the future

Preparing for ongoing growth and change in our organization requires strategic choices. We want UNI to be able to make decisions here, by people here and for people here. We also want to diversify our activities to ensure the long-term viability of our business. This vision is nothing new. It’s what drove the builders who boldly developed our movement. It’s why the board of directors supported the diversification of UNI’s business interests and investments. This fundamental choice now opens the door to new expertise and gives our financial cooperative the independence it needs to modernize our services. Diversification allows us to preserve our gains as a francophone Acadian institution.

Message from the chair of the board I UNI Financial Cooperation 13

That’s why the major projects we are working on to safeguard our long-term prosperity ensure that our communities, members and clients remain central to the decisions we make. We still carry the dream and aspirations of our founding members, who saw collective wealth as the best guarantee to a future where our young people can thrive in our communities and our seniors will feel supported. Preparing for the future means keeping this promise.

Another year of individual member dividends

Prosperity is best shared. The outstanding results of 2022 enabled our directors to make a decision that honours the cooperative tradition. Thanks to our vigilance in recent years, we were able to vote in favour of individual member dividends for the second year in a row. These dividends were especially important to us because they are a way to show our solidarity with all members by telling them that UNI is a choice that matters.

Hosting Canada’s biggest credit unions

In September 2022, UNI hosted the LCUC (Large Credit Union Coalition) at the annual meeting of Canada’s 20 largest financial cooperatives, including UNI. This major event was held in Atlantic Canada for the first time ever, in Moncton. The theme was “Connecting Coast to Coast.” It was an ideal opportunity to share Acadian culture with our colleagues from other provinces.

Let’s be proud of these successes—they show that UNI is a major financial cooperative with a place in the big leagues.

I would like to sincerely thank all members of the board of directors for their commitment and care, which perfectly embody our value of responsibility.

Thanks also to UNI’s members, clients, employees and leaders for your loyalty and trust. Let’s stay UNIted for the sustainable prosperity of UNI and its members.

Pierre-Marcel Desjardins Chair of the Board

Pierre-Marcel Desjardins Chair of the Board

14

Annual Report 2022 I Message from the chair of the board

of Directors I UNI Financial Cooperation 15 Director Director Director Director Director Director

Guy Ouellet, MBA

Chair Vice-Chair Director Director Director Director

Pierre-Marcel Desjardins, ICD.D

Jean-François Saucier, M. Sc., CPA, CA

Brian L. Comeau

2021 – 2024 2021 – 2024 2020 – 2023 2022 – 2025 2020 – 2023 2021 – 2024

Performance Evaluation

of the President

CEO,

Risk Management Audit,

Nomination Risk Management

Plan

Audit

Roland T. Cormier Sébastien Deschênes, CFA, CPA, CA, ICD.D Resources

Caroline Haché, MBA

Nomination

& Remuneration

and

Chair

Chair

Conduct Review & Governance, Chair Pension

Performance Evaluation & Remuneration of the President and CEO Audit Human Resources, Chair Pension Plan, Chair

Pension Plan Risk Management, Chair Human

Nomination, Chair Performance Evaluation & Remuneration of the President and CEO

Board

Kevin J. Haché Marc Henrie Wanita McGraw, FCPA, CA, ICD.D

2022 – 2025 2021 – 2024 2020 – 2023 2022 – 2025 2020 – 2023 2022 – 2025 Conduct Review

Governance

Risk Management Audit

Performance

Diane Pelletier Allain Santerre

&

Human Resources

Conduct Review & Governance Human Resources

Evaluation & Remuneration of the President and CEO

Conduct Review & Governance

Audit,

Pension

Human Resources Nomination Conduct Review & Governance Human Resource Risk Management

Nomination

Plan

Board of Directors

Achievements 2022

18 Annual Report 2022

Strategic priorities achieved

Grow our business and develop our offering

Adapt our offering and increase profitability

1 Expand our digital offering Attract and retain our young clients

Review our wealth management model

Support decision-making based on reliable business data

Continue developing our subsidiaries

Foster external strategic partnerships

Enhance organizational performance and develop member and client

interaction channels

Improve our performance to interact even more effectively with our members and clients

2 Streamline and simplify our operations to generate more value for our members and clients

Review the client experience to capitalize on opportunities for attraction and retention

Develop our talent and effect cultural change

Leverage our business intelligence to better understand our members and clients and focus our efforts

Develop our tools for interacting with our members and clients

Develop our talent and foster and maintain an engaging workplace

3 Strengthen our connections to, and impact on, the communities we serve Shape the employee experience with a focus on engagement and mobilization in connection with the target client experience

Promote the overall development of our talent

Build our organizational culture

Strategic priorities achieved I UNI Financial Cooperation 19

UNI, fully growing where it is great to work

UNI, fully growing where it is great to work

UNI continues to support its employees in moving the organization forward. We are committed to developing our talented team and taking them to greater heights. We have implemented numerous programs to ensure healthy retention, talent acquisition, skills development, and succession planning. All these initiatives let us continue offering simplified and personalized support to our members and clients.

Referral Program

The referral program we introduced in 2022 is paying off. To date, many employees have submitted good leads. In 2023, we will extend the program to retirees, who will also be eligible for a bonus for each referral leading to a hire.

Training portal

In 2021, UNI developed the UNIversity platform, an essential tool for managing employee training and skills development. In the past year, the focus was on learning this new tool, creating new courses and adding targeted new training sessions. An important accomplishment was the repatriation of all cybersecurity training, which greatly facilitated management from both an administrative and employee perspective.

Leadership development

Horizontal development focuses on knowledge and skills required for a job, the acquisition of knowledge and abilities that translate into specific, measurable behaviours and actions. Vertical development, on the other hand, addresses our thinking and look at things in complex, systemic, strategic and interdependent ways. It enhances our ability to make sense of and respond to a given situation. While horizontal development still has its place in business, UNI has instead launched a vertical strategy to help our leaders develop mindsets capable of guiding how we think and behave. Mindsets refer to the mental models we draw

22 Annual Report 2022 I UNI, fully growing where it is great to work

on when we think, as well as our sense of identity. In connection with our organizational values and behaviours, we introduced our leaders to the work of Dr. Carol Dweck and Dr. Ryan Gottfredson on vertical development through a series of workshops and meetings. Vertical development calls on leaders to be adaptable, mindful and more collaborative in a complex world. Vertical development and leadership mindsets will be part of the employee development strategy in 2023.

Leadership coaching

Leadership coaching was an important development strategy in 2022. It was introduced through regular one-onone discussions with a certified inhouse leadership coach. More than 30 leaders took advantage of self-assessment tools to explore development needs and opportunities. Coaching helped them see their work in a new light, provided support and empowered them to improve their performance. The goal is to help leaders achieve their objectives more effectively, while improving their overall leadership style. Participants confirmed that coaching helped them cultivate strong leadership skills that benefit them and their teams alike.

Coaching circles

To maximize the impact of coaching in 2022, UNI implemented an initiative to develop the coaching and peer support culture within our financial cooperative. Launched as part of International Women’s Day, this coaching circle pilot project targeted women leaders and professionals at UNI. Two six-participant circles were created to facilitate and accelerate peer-to-peer development and support throughout the year. Coaching was carried out by an in-house coach in small groups, with occasional one-on-one sessions to enhance learning. Participants noted that the initiative was helpful for them, their teams and the organization.

UNI,

to work I UNI

23

fully growing where it is great

Financial Cooperation

UNI among Canada’s Most Admired Corporate Cultures in 2022

This national program recognized UNI as one of the top ten Canadian organizations whose corporate cultures enhance performance and sustain a competitive advantage in the MidMarket category (revenues of $100 million to under $500 million). We are so proud of this mark of excellence, which speaks to the quality of our employees and is an exceptional asset to us as an organization committed to our values. It acknowledges and celebrates our ongoing pursuit of excellence with respect to organizational development and talent.

At UNI, we are blessed with employees who choose to spend many years in our service. In October we held a virtual celebration to recognize the years of service of 150 employees, 47 of whom have celebrated 25 years or more with UNI.

24 Annual Report 2022 I UNI, fully growing where it is great to work

A revamped, redesigned business location at Tannery Place

On November 28, a new business location opened its doors at Tannery Place. This fresh and modern space in downtown Moncton offers members and clients personalized and simplified financial advisory services. Building close relationships with our members and clients—to understand their needs now and in the future—remains a fundamental key to our success as a financial cooperative. Our goal is to continue staying true to our modernization plan.

With a design that promotes responsible consumption, we are looking to make a positive impact on the communities we serve.

The St. George Street building, home to the former business location, will have a second life and remain an integral part of the history of our institution’s history.

Employees from Tannery Place’s business location in Moncton, posing proudly in their new premises during the official opening on November 28, 2022. Committed to contributing to the vitality of the communities in which it operates, UNI is proud to innovate in a sustainable and eco-responsible way.

Business development I UNI Financial Cooperation 25

Together with the community

Serving the community is one of our main missions. Whether through donations and sponsorships, supporting local businesses or promoting forward-thinking, transformative and sustainable projects, UNI is committed to helping our communities thrive and prosper!

Volunteering plays an important role in our initiatives. We encourage all our employees to get involved with organizations that matter to them. This year, Lison Guignard won the Bénévolat de l’année 2022 contest at UNI for her involvement with Operation Red Nose in the Acadian Peninsula.

From left to right: Joannie Benoit, Honorary President of the Operation Red Nose 2022 Campaign, Gaétan Germain, Development Coordinator at Operation Red Nose New Brunswick, Mario G. Patenaude, Vice-President, Talent Management, Lison Guignard, Contest winner Bénévolat de l’année 2022, Rudy and Brahim Benhamed, president of the Operation Red Nose organizing committee, Acadian Peninsula.

From left to right: Joannie Benoit, Honorary President of the Operation Red Nose 2022 Campaign, Gaétan Germain, Development Coordinator at Operation Red Nose New Brunswick, Mario G. Patenaude, Vice-President, Talent Management, Lison Guignard, Contest winner Bénévolat de l’année 2022, Rudy and Brahim Benhamed, president of the Operation Red Nose organizing committee, Acadian Peninsula.

26 Annual Report 2022 I Together with the community

A pool of volunteer hours

30% of employees gave their time

Every year, each of our employees has a seven-hour pool of paid time to volunteer for the cause of their choice and support an organization or activity in the community. Many UNI employees volunteer in a variety of ways every day. In 2022, we had received 351 applications for a total of 1 463 hours invested in the communities.

La Journée Solidarité

This initiative was born out of our dream to bring together the largest number of UNI employees once a year around the same regional environmental cause. For everyone involved, it’s all about giving back.

Together with the community I UNI Financial Cooperation 27

Since 86 years, UNI contributed to the economic stability of the communities in which it operates

Cultural change Soyons UNI

The culture change UNI undertook in 2020 continued through 2022. At all levels of the company, our Purpose and core values guide our employees in their daily interactions with members and clients, in our major modernization projects and in our community outreach. We take pride in our Purpose and our three core values championed by our president and CEO in his speeches and by other UNI representatives on many occasions. A corporate culture draws strength from the concerted efforts of all its members. With that in mind, we appointed Soyons UNI coordinator to ensure that our various projects and initiatives foster and support the sustainable prosperity of UNI and its members.

Everyone’s renewed commitment to our culture change helped make UNI a proud recipient of a Canada’s Most Admired Corporate Cultures award in 2022.

28 Annual Report 2022 I Cultural change

Community presence

From the beginning, UNI has been committed to making a positive impact on the lives of individuals, businesses and the community. Our positioning underlines how important supporting sustainable development is to the community impact we want to have.

Recognition as a financial institution central to local prosperity

We want to invest more in the initiatives and causes that create and enhance local prosperity and vitality in New Brunswick.

Prospering together

Support organizations committed to working together for the local economy

Encourage buying locally by showcasing the diversity of local products and services

Attract partners and businesses that want to invest in our local prosperity and vitality efforts

Creating vibrant communities together

Support organizations that care about the region’s arts, culture, sports, education and socio-economic well-being

Ensure that our investments directly or indirectly support local prosperity.

Community presence I UNI Financial Cooperation 29

You’re the driving force behind the vitality and prosperity of our communities!

UNI makes a major donation to help New Brunswick youth achieve their full potential

UNI is proudly committed to making a difference in the lives of young people with a major $1 million donation to Sistema NB’s 10 000 Children campaign. Some 40 children benefit from this innovative music education program. Solidarity, responsibility and courage take on their full meaning with this investment by the whole UNI family for the good of our community and its future. That future is in the hands of ALL of us.

30 Annual Report 2022 I Community presence

From left to right: Ken MacLeod, President and CEO of the New Brunswick Youth Orchestra; Robert Moreau, President and CEO of UNI Financial Cooperation; and the orchestra made up of 40 young people from Sistema NB.

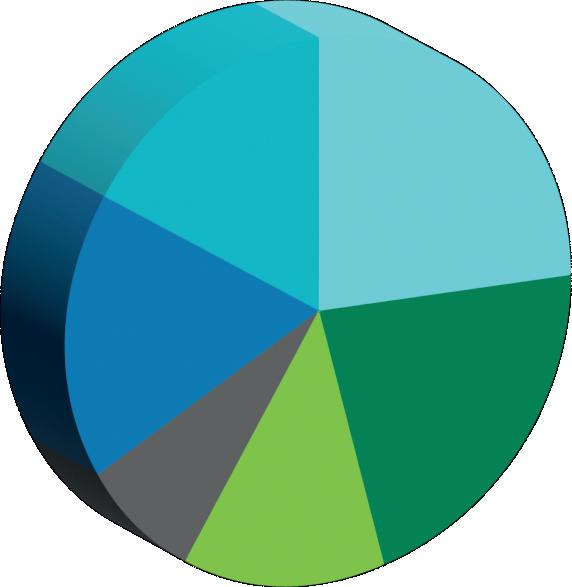

16%

Arts and culture

$425,350 $460,287

Education and youth 25%

$695,367

Sports and recreation 17%

8%

Mutual aid and solidarity 21% Economic development

$220,129

Health 13%

$347,739

Arts and culture

Promoting the fostering of new talent and boosting the cultural industry

Economic development

Creating synergy with the business community

$2.7 M in donations, sponsorships and scholarships

Education and youth

Contributing to the development of youth

Mutual aid and solidarity

Supporting community and social development projects

$568,041

Health

Facilitating access to healthcare services and research for a better quality of life

Sports and recreation

Contributing to community vitality

$7.5 M in individual dividends

3 Cooperative committees

The 36 members of 3 cooperative committees are attuned to the specific needs of each region and ensure the successful completion of projects

Community presence I UNI Financial Cooperation 31

UNI invests up to $300,000 in New Brunswick

The Voilà! contest is back for the third year in a row, delivering meaningful, visionary, sustainable projects that drive change and contribute to the well-being of New Brunswick communities. Grand and secondary prizes totalling up to $300,000 will be awarded across the province to organizations selected by a vote of members and clients.

Here are the Winners of 2022:

Chaleur and Acadian Peninsula Region Camp jeunesse Richelieu

$50,000

Kent and Miramichi Region ForêStation café Inc.

$46,000

West Region Société culturelle régionale Les Chutes $50,000

South Region École Sainte-Bernadette $25,000

Restigouche Region Camp Canak Inc. $50,000

Secondary prizes totalling $50,000 will also be awarded to organizations selected by a vote of members and clients.

32 Annual Report 2022 I Community presence

UNI’s commitment

Did you know that one child out of 5 and 19% of New Brunswick household knows food insecurity?

UNI, its members and clients have always been commited to making a positive impact on the lives of individuals and their communities. For those reasons, we donate over $200,000 to 55 food banks and shelters for victim of abuse in New Brunswick.

$200,000 in donations

55 to food banks and shelters for victim of abuse in New Brunswick

To learn more about our social mission, please visit www.uni.ca/communityimpact

Community presence I UNI Financial Cooperation 33

Management’s discussion and analysis

Year ended December 31, 2022

Note to the reader

This management report offers the reader a general overview of UNI Financial Cooperation. It is a complement and supplement to the information provided in the consolidated financial statements of Caisse populaire acadienne ltée. It should consequently be read together with the combined financial statements, including the accompanying notes, for the year ended December 31, 2022.

This report also presents the results analysis and main changes made to UNI Financial Cooperation’s balance sheet during the fiscal year ended December 31, 2022. Additional information about UNI Financial Cooperation is available on our www.uni.ca website.

36 Annual Report 2022

Table of contents Financial Position 38 MANAGEMENT’S DISCUSSION AND ANALYSIS Economic and financial outlook Review of financial results 41 Surplus earnings in 2022 42 Net financial income 44 Operating expenses 45 Life and health insurance Balance sheet review 46 Summary balance sheet 50 Capital management Risk management 39 46 41 51 UNI Financial Cooperation 37

Financial position 38 Annual Report 2022 I Financial position ($000s and %) 2022 2021 Profitability and productivity Surplus earnings before other items $30,006 $27,933 Equity $472,491 $469,646 Return on equity 7.8 % 5.4% Business development Assets $5,371,828 $5,230,528 Business volume $12.0G $11.6 G Business volume growth 3.0% 6.9% Risk Loan losses (recovery of provision for loan losses) $95 ($3,086)

Financial position as at December 31, 2022

Economic and financial outlook

Canada

Canada’s economy continued to recover from the effects of the COVID-19 pandemic but faced challenges such as rising inflation, supply chain disruptions and the global impact of the war in Ukraine.

Canada posted moderate growth, with gross domestic product (GDP) up by about 3.6%. The country’s strong economic performance was boosted by a rebound in consumer spending and exports. Employment increased by 4.0% in 2022. The unemployment rate continued to fall, hitting around 5.3%, while the vacancy rate continued its trend, reaching 5.9% in the second quarter.

In March 2022, the Bank of Canada raised its benchmark interest rate—which had remained unchanged for almost two years—then increased it seven times, from 0.50% to 4.50%.

In 2022, the United States was the source of more than 49% of our imports, and the destination of 76.5% of our exports. The significant trade activity between Canada and the United States influence our currency. In 2022, the Canadian dollar hovered around $0.77 U.S. dollars, on average. It reached its highest level in early April, at $0.80, and its lowest in mid-October, at $0.72.

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 0.6000 0.7000 0.7500 0.9500 1.1000 1.0500 1.0000 0.9000 0.8500 0.8000 0.6500 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Bank of Canada Rate, 2012-2022

Canadian Dollar vs. U.S. Dollar, 2013-2022

Economic and financial outlook I UNI Financial Cooperation 39

New Brunswick

New Brunswick’s population passed the 800 000 mark in 2022. The province experienced an estimated population growth of 2.7%, well above the national rate of 1.8%. Employment in New Brunswick increased by 2.8% in 2022. The province gained 10 000 jobs, including 13 100 full time, and lost 3 100 part-time jobs. The Northeast saw an increase of 2 000 jobs, including a gain of 2 800 full-time jobs and a loss of 900 part-time jobs. The Northwest added 2 600 new jobs, a gain of 2 900 full-time jobs and a loss of 300 part-time jobs. The Southeast region recorded a gain of 1 800 full-time jobs and lost 100 part-time jobs. The provincial unemployment rate dropped from 9.2% to 7.2% in 2022. The Northeast had the highest unemployment rate at 11.5%, the fourth highest of Canada’s 69 economic regions. As elsewhere in Canada, the number of job vacancies continued trending upward, peaking at 5.3% in the second quarter of 2022.

The inflation rate was above the national average, with the Consumer Price Index (CPI) at 7.3% in New Brunswick versus 6.8% in Canada as a whole. Housing starts in the province increased by 22.2% in 2022 but fell 3.4% nationally. Increases of 31.3% in multi-unit housing and 49.9% in apartments and other housing contributed significantly to growth in the province.

The province’s exports were up 26.9%, with the United States remaining the main international market, accounting for 92.4% of exports, followed by China (1.1%). The province’s top exports were energy products (30.4%), basic and industrial chemicals, plastics and rubber products (31.4%), forest products and building and packaging materials (19.8%). Imports followed a similar trend, up 36.1% in 2022. Imports came mainly from the United States (56.2%) and Saudi Arabia (19.9%). Energy products accounted for 77.8% of New Brunswick’s imports.

Unemployment (%) Jobs (‘000) 2021 2022 2021 2022 Northwest 6.7 5.5 34.9 36.1 Northeast 13.5 11.2 60.4 62.4 Southeast 8.6 5.9 114.5 116.3 Southwest 9.2 7.3 81.4 85.4 Centre 7.5 6.0 70.7 73.3 New Brunswick 9.2 7.2 363.5 373.5 40 Annual Report 2022 I

financial outlook

Economic and

Review of financial results

Surplus earnings in 2022

Consolidated financial results remained at the same level as the previous year. Surplus earnings before other items at December 31, 2022, were $30 million, an increase of $2.1 million compared with 2021. It was a remarkable fiscal year. Given this outstanding performance, which is among the best ever achieved, the UNI Board of Directors has authorized, in 2022, the payment of individual dividends totalling $5 million in 2023.

The life and health insurance line contributed $9.6 million to surplus earnings in 2022 compared to $5.9 million in 2021. Increases in yield curves pushed up revenue for the life and health insurance subsidiary.

Surplus earning, before other items for the fiscal year, were $30 million at December 31, 2022, while net surplus earnings totalled $33.3 million. This difference is due to other items, individual member and client dividends and income taxes for 2022.

Other items consisted of a change in the market value of our derivatives, which in 2022 generated a gain of $23.3 million, mainly due to changes in market interest rates and the amortization of capital gains from the interest rate swap portfolio. We paid $16.4 million in income tax in 2022, representing approximately 31% of our surplus earnings before taxes.

($ thousands) 2022 2021 Life and health insurance $9,577 $5,866 Personal and business 20,429 22,067 Surplus earnings before other items $30,006 $27,933

Review of financial results I UNI Financial Cooperation 41 See the table below for a more in-depth analysis.

Net financial income

Net financial income corresponds to the difference between the financial income earned on assets, such as loans and securities, and the financial expenses associated with liabilities, such as deposits and borrowings. Net financial income also includes income from insurance and annuity business.

Net financial income was $128 million at the end of 2022, up $8.6 million from $119.4 million in 2021. This variation is mainly explained by the seasonality of our business development strategies, as lending growth occurred much earlier in the year. In addition, the Bank of Canada rate hikes generated additional financial margin income in 2022. Conversely, our investment income did not benefit from a favourable market environment in 2022. The financial margin between loans and deposits improved, as interest income increased faster than interest expenses.

Loans

Interest income on UNI’s loan portfolio increased by $24.5 million over 2021. Interest income on loans was $161.4 million in 2022, compared with $136.9 million in 2021. This increase was the result of higher interest rates and growth of $283.2 million in the loan portfolio.

Deposits

Interest expenses on member and client deposits rose from $24.1 million in 2021 to $32.6 million in 2022. The increase was due to higher interest rates and the product choices made by members and clients. Our pricing remains competitive, as reflected in the $141.5 million growth of our deposit portfolio in 2022.

Borrowing

UNI has had an active securitization program since 2014. In 2022, two tranches reached maturity in June and December, for a total of $19.7 million. UNI issued $55.2 million in new loan securitizations in 2022. Growth in securitization volume during the year increased the interest expenses of the securitization program, but low rates caused the average borrowing rate to drop by 0.24%.

Other income

Other income comes from a number of sources, as shown in the table below.

Other income continued to grow. It rose from $68.7 million in 2021 to $70 million in 2022, an increase of $1.2 million.

($ thousands) 2022 2021 Deposit and payment services charges $16,183 $16,111 Net insurance and annuity premiums 18,018 18,442 Gain on the disposal of securitized mortgages 16,114 14,819 Commissions 13,463 13,432 Foreign exchange income 733 626 Sales of related services 2,918 2,833 Other income 2,540 2,478 Total other operating income $69 969 $68,741

42 Annual Report 2022 I Review of financial results

Provision for credit losses

The provision for credit losses was $0.09 million, up $3.2 million from 2021, as UNI recovered credit loss provisions last year. Since January 1, 2018, it has been calculated as per International Financial Reporting Standard IFRS 9, which sets out requirements concerning the classification, evaluation and depreciation of financial instruments. The standard is based on expected credit loss information (forward-looking information). With this standard, our loan portfolios are segmented into three separate stages, based on risk trends. The stages are each assigned different default probabilities based on their risk. Mortgage and commercial loan products in Stage 3 are calculated in the same way as the former individual provisions.

Review of financial results I UNI Financial Cooperation 43

Operating expenses

Salaries and employee benefits

Since UNI is a service-based company, its payroll is its biggest expense. Expenses related to employee salaries and benefits increased in 2022, to $81.2 million, up $8.4 million or 11.5% over the previous year. This increase was caused by the cost of inflation and additional resources to support our growth and various strategic projects.

Other operating expenses

The following table presents a detailed look at our operating expenses.

Our operating expenses increased by approximately $1.6 million over the previous year due to resumed travel after the pandemic, inflation costs and increased donations and sponsorships.

($ thousands) 2022 2021 Employee travel, training and wellness $3,660 $2,260 Professional fees 6,288 6,280 IT costs and telecommunications 42,345 41,942 Building and equipment rental, maintenance and depreciation 12,921 15,823 Cash management and compensation 2,100 1,892 Dues and regulatory fees 2,634 2,492 Promotion, advertising, donations and sponsorship 7,235 6,111 Office expenses and postage 2,546 2,370 Governance 750 600 Insurance 1,425 1,343 Other 3,881 3,037 $85,785 $84,149

44 Annual Report 2022 I Review of financial results

Life and health insurance

The subsidiaries Acadia Life and AVie make up this line of business. Acadia Life is a significant contributor to UNI’s overall results, and 2022 was no exception.

Operating income was satisfactory in 2022, at $9.3 million compared with 2021 net income of $5.9 million.

The table below presents Acadia Life’s main sources of income and fluctuations in actuarial reserves. Income from insurance premiums and commissions declined slightly in 2022 compared with 2021.

The decrease in investment income is counter balanced by a decrease in insurance benefits paid out and the variation in actuarial reserves.

($ thousands) 2022 2021 Income from premiums $18,018 $18,442 Financial income (44,593) (5,016) Total revenues (26,575) 13,426 Insurance benefits and changes in actuarial reserves ($43,730) ($1,290)

insurance

Review of financial results I UNI Financial Cooperation 45

Life

income

Balance sheet review

Summary balance sheet

3.0 3.5 4.0 4.5 5.0 5.5 2020 2021 2022 Changes in the balance sheet ($ billlions) Assets Loans Deposits ($ thousands) 2022 2021 2020 Assets Cash $163,878 3.1% $120,374 2.3% $132,987 2,8% Securities 573,262 10.7% 896,684 17.1% 829,196 17.3% Loans 4,068,190 75.7% 3,780,399 72.3% 3,512,487 73.2% Other assets 566,498 10.5% 433,071 8.3% 321,157 6.7% Total assets $5,371,828 100.0% $5,230,528 100.0% $4,795,827 100.0% Liabilities and equity Deposits $4,341,350 80.8% $4,199,803 80.3% $3,864,613 80.6% Borrowings 278,958 5.2% 256,346 4.9% 163,729 3.4% Other liabilities 279,029 5.2% 304,733 5.8% 301,455 6.3% Equity 472,491 8.8% 469,646 9.0% 466,030 9.7% Total liabilities and equity $5,371,828 100.0% $5,230,528 100.0% $4,795,827 100.0% 46 Annual Report 2022 I Balance sheet review

Total assets

As of December 31, 2022, UNI’s total assets were $5.4 billion, up $141 million, or 2.7%, from 2021. The loan portfolio grew significantly in 2022, by 7.4%, while securities declined.

Liquidity management

The objective of liquidity risk management is to guarantee that UNI will have timely and profitable access to the funds necessary to fulfill its financial commitments when they become payable, both under normal circumstances and in crisis situations. Managing this risk requires an acceptable level of liquid securities, a five-year financing plan, a liquidity crisis simulation, liquidity stress testing, daily liquidity position management and quarterly reporting to UNI’s Board of Directors. This reporting process is supported by liquidity risk management and investment policies, both of which are reviewed annually by the Board.

Liquidity management is governed by a UNI in-house policy. It ensures proper monitoring of UNI’s liquidity through multi-level management and therefore adequate short-term liquidity. A financing plan is used to anticipate long-term liquidity needs.

As a financial institution regulated by the Office of the Superintendent of Financial Institutions (OSFI)—and to ensure its liquidity risks are well managed—UNI must maintain a short-term liquidity ratio above 100%. A lower ratio does not necessarily mean the institution has a financial problem but may simply arise from an adjustment to liquidity management or changes in operations or the liquidity guidance standard that governs how calculations are done. We take a conservative approach to determining minimum liquidity levels and regularly update our investment strategy to maximize the return on our cash assets.

The end of the pandemic and strong growth in the loan portfolio in 2022 allowed UNI to redistribute a large portion of its excess liquidity. This reduced the securities portfolio and lowered the short-term liquidity ratio to a level considered more normal and still well above the regulatory minimum of 100%.

Loans

The loan portfolio, net of provisions, continued to grow in 2022, passing the $4 billion mark. It was $4.1 billion at December 31, 2022. Compared with 2021, this was a $288 million increase, representing a growth rate of 8%. Most of the growth comes from business development.

$3,780 $4,068

2022 2021 Ratio 163% 186% Balance sheet review I UNI Financial Cooperation 47 Loans to members and clients net of provisions ($ millions) 2020 2021 2022 $3,512

Short-term liquidity ratio

The table below presents the breakdown of the loan portfolio by business line.

Residential mortgages

Despite less growth in the residential mortgage portfolio in 2022, it remained at $50.1 million, compared to $76.2 million in 2021. With good growth in the first half of the year, rising rates have dampened the mortgage market in recent months. House prices have remained historically high in New Brunswick, and the number of home sales has declined significantly.

Consumer loans and other personal loans

This loan portfolio increased by $8.3 million in 2022, after shrinking by $11.1 million in 2021. Record growth in point-of-sale financing in 2022 (+$65.3 million) was a major contributor to overall portfolio growth.

($ thousands) 2022 2021 2020 Personal Residential mortgages $1,807,273 $1,757,208 $1,680,975 Consumer and other 597,996 559,659 570,738 Total personal $2,405,269 $2,316,867 $2,251,713 Business Real estate 830,621 691,227 528,214 Health care and related services 122,167 135,861 150,227 Construction 88,801 74,118 65,316 Forestry 46,905 42,474 40,601 Fishing and trapping 167,328 144,718 124,334 Retail 60,997 56,618 49,014 Manufacturing 85,585 63,300 56,516 Accommodation and food 96,040 108,323 111,409 Transportation and warehousing 31,284 33,763 34,454 Other 159,832 144,332 138,434 Total business 1,689,560 1,494,733 1,298,520 4,094,829 3,811,600 3,550,233 Allowance for credit losses (26,639) (31,201) (37,746) Total loans by category of borrowers $4,068,190 $3,780,399 $3,512,487 48 Annual Report 2022 I Balance sheet review

Business loans

The business loan portfolio experienced solid growth in 2022, up $194.8 million. This portfolio is now worth $1.69 billion, up 13% from $1.49 billion in 2021. Multi-unit real estate performed particularly well, with growth of $139.4 million. The fisheries, manufacturing and construction sectors also performed well with growth of $22.6 million, $22.2 million and $14.6 million, respectively.

Deposits

The deposit portfolio continued to grow in 2022 to 3.4%, up $141 million over 2021. Rate increases changed member and client behaviour and affected product choices in 2022.

Deposits ($ millions) 2020 2021 2022 $3,865

Balance sheet review I UNI Financial Cooperation 49

$4,200 $4,341

Capital management

Governance

UNI recognizes the importance of sound capital management and has put in place a series of measures:

Annual review of the capital risk management policy by the Board of Directors

Annual internal process for assessing capital adequacy

Quarterly capital management reports to the Board of Directors

Monthly monitoring of various capital indicators

Annual five-year capitalization plan, updated quarterly, to ensure long-term capital adequacy

UNI uses two ratios to ensure capital adequacy:

Capital to at-risk assets ratio

This ratio assesses risk-weighted capital adequacy. OSFI’s Capital Adequacy Requirements guideline prescribes a minimum ratio for financial institutions. UNI easily achieves this minimum. Our capital is also mainly composed of shares and retained earnings.

Annual fluctuations in the CET1 ratio

(in %)

In 2022, UNI achieved good financial results (profits) which helped increase its capital ratio. Record loan portfolio growth led to an increase in assets. The growth combined with the delivery of strategic projects had a considerable impact on UNI’s CET1 regulatory capital ratio and regulatory leverage ratio. The CET1 capital ratio had decreased by 1.18% at December 31, 2022.

($ thousands and %) 2022 2021 Capital stock value $472,491 $469,646 Deduction (33,524) (13,842) Regulatory capital (CET1) 438,967 455,804 Tier 2 capital 18,002 16,034 Total regulatory capital $456,969 $471,838 Total risk-weighted assets $3,192,872 $3,091,702 CET1 risk asset capital ratio 13.8% 14.7% Total risk asset capital ratio 14.3% 15.3%

50 Annual Report 2022 I Balance sheet review

Leverage ratio

OSFI’s Leverage Requirements Guideline calls for compliance with another capital ratio, namely the leverage ratio. Capital must be at least 3% of non-risk-weighted assets. UNI meets OSFI’s requirements with a ratio of 8.2%.

Leverage ratio

Risk management

UNI has a risk management oversight function that reports to the Chief Risk Officer (CRO). The CRO oversees the implementation of a risk management framework for UNI and its subsidiaries to ensure compliance with requirements established by OSFI and other regulatory authorities.

ACCOUNTABILITYDIRECTIONS

Board of Directors and committees

Executive Committee and oversight functions

Three lines of defence

Common risk infrastructure

People

Process

Tools

•

• Policies and mandates of committees and oversight functions

• Risk Management Committee

• Risk appetite and tolerance

• Risk culture and general guidelines

Guidelines

•

Accountability

• Risk management process

Procedures

•

Expertise and training

•

Communication

Internal controls

Data and tool availability

Risk management cycle

Identify Evaluate and measure Menage Control Monitor

Risk identification and taxonomy

($ thousands and %) 2022 2021 Regulatory capital CET1 $438,966 $455,804 Risk-adjusted assets $5,379,146 $5,042,491 Leverage ratio 8.2 % 9.0%

Balance sheet review I Risk management I UNI Financial Cooperation 51

Risk management framework

UNI’s risk management framework is supported by a governance structure aligned with its organizational and legal context. The Board of Directors has a risk management committee, an audit committee and other committees to oversee the organization’s specific activities and the associated risks. It also makes use of oversight functions such as risk management, compliance, finances, internal audit and credit to oversee risk and to obtain the information required to fulfill its mandate.

The Board of Directors expresses its strategies, including those related to risk, through the Risk-Taking Propensity Framework (RTPF). UNI manages risk by adopting three lines of defence to provide the Board of Directors and the Executive Committee assurance that all risks remain within the tolerance levels set out in the RTPF. In other words, it is the level of risk that

UNI is willing to take. The RTPF covers all activities of UNI and its subsidiaries. The risk management oversight function provides day-to-day coordination of the framework in accordance with the orientations of the Board of Directors. UNI continues to improve the efficiency of its three lines of defence in order to guarantee a truly efficient risk governance system tailored to the needs of the organization and the strict requirements of the industry, which are also constantly evolving.

Risk culture

The Board of Directors promotes a balanced risk-taking approach offering adequate return on equity to maintain a high level of capital while not eroding the collective objectives of its members and clients or communities.

Risk-Taking Propensity Framework

Risk appetite (target): Corresponds to UNI’s target level or the level it wishes to maintain in order to achieve its strategic and business goals.

Risk tolerance (threshold and limit): Corresponds to the threshold and limit established by taking into consideration risk-taking ability. UNI does not want to be in this zone.

Capacity: Corresponds to the equity, forecast and actual profits, tools, experts, knowledge and UNI personnel needed to manage a risk. In terms of risk level, regulatory thresholds also limit UNI’s capacity.

A successful and rigorous risk culture can be defined by the use of a common language. Being able to categorize risks and consistently and cohesively define them across the organization goes a long way toward establishing a solid foundation for the common language of risk management. UNI classifies its risks under eight main categories. Operational risk, due to its disparate nature, has 12 additional subcategories, including third party outsourcing risk and cybersecurity risk..

52 Annual Report 2022 I Risk management

Risk taxonomy

Strategic risk

The material gap between the financial results of UNI and its subsidiaries and the anticipated results set out in its strategic plan. This financial gap may be linked to:

inappropriate choices of strategies, business models, strategic partners or operation plans depending on its financial situation, operational capacity, expertise, competitive positioning, or business or economic environment

adequacy of the allocation of human, financial and material resources to realize its strategy

misalignment of sectoral plans with UNI’s strategic plan

voluntary or involuntary inaction in response to a significant change in the economy or in the competitive or business environment

Undercapitalization, overcapitalization or inadequate use of UNI’s equity loss of income or balance sheet value due to an unfavourable external environment (e.g., economic crisis)

The Board of Directors adopts a strategic plan that contains both quantitative targets and organizational objectives. The Board of Directors conducts a quarterly review of the status of this strategic plan in conjunction with the members of the Executive Committee. The Executive Committee implements action plans to ensure that strategic objectives will be reached.

UNI has a level of capital consistent with its risk appetite. It takes pride in the financial soundness it offers its members and clients, and takes the appropriate actions to maintain a level of comfort that ensures the sustainable prosperity of UNI and its members.

Every year, UNI carries out crisis simulations to determine the organization’s resilience level in the event it had to manage extreme situations. UNI, using management measures, successfully remains above regulatory capital ratios in all scenarios tested.

Risk management I UNI Financial Cooperation 53

Reputation Regulatory Credit Liquidity Market Strategic Insurance Operational Other OR Cybersecurity Outsourcing

Reputation risk

Revenue losses due to activities, actions or practices undertaken by UNI that are significantly below the expectations of members, clients, employees or the general public. This risk often arises due to ineffective management of one or more other risk categories, which causes a loss of confidence or significant negative comments in traditional or social media and in the community.

UNI takes its reputation very seriously. It continuously ensures that its actions, methods and behaviours are aligned with its cooperative values and fiduciary responsibilities. The Executive Committee closely oversees the marketing of new products, services and other initiatives as well as changes to our existing products and services.

Liquidity risk

Possible losses resulting from the use of expensive and unplanned sources of funding in order to continue honouring UNI’s financial obligations in a timely manner. Financial obligations include commitments to depositors, borrowers (disbursement of approved loans), suppliers, members and clients or insureds. This risk is due primarily to asymmetry between the cash flows related to assets and those related to liabilities, including the payment of monies owed to suppliers and individual member and client dividends.

UNI presents a favourable liquidity level among Canadian financial institutions. The main source is personal and business member and client deposits, but it also uses CMHC-backed mortgage securitization channels to diversify its sources.

UNI also has lines of credit with other Canadian financial institutions. UNI and its life insurance subsidiary, Acadia Life, follow an asset-liability matching strategy to help ensure that inflows are commensurate with outflows. UNI has established risk indicators, alerts, thresholds and limits, and a contingency funding plan to ensure that its liquidity level is always at a comfortable level and always exceeds regulatory requirements. The specific purpose of alerts is to detect a potential liquidity crisis.

Compliance risk

Losses that may or may not result from litigation, penalties, fines or financial or other sanctions (increased surveillance by regulatory organizations) linked to inappropriate practices that do not comply with applicable regulations. This risk is due to the possibility of UNI or its subsidiaries straying from the expectations set out in laws, rules, regulations, standards or other regulatory requirements. This risk also includes significant unplanned charges incurred to remain in compliance with current regulation or regulatory modifications.

UNI has implemented a regulatory risk management framework adapted to the nature of its operations, whose purpose is to demonstrate that its activities fall within the applicable regulatory frameworks while respecting the risk-taking propensity framework. This includes monitoring, identifying, measuring and managing changes to legislation, regulations and other regulatory requirements. When applicable, UNI adjusts its policies and procedures as promptly as possible to comply with regulations.

54 Annual Report 2022 I Risk management

Combating money laundering and terrorist financing.

Credit risk

Unplanned financial losses due to the inability or refusal of a borrower, endorser, guarantor or counterparty to fulfill its entire contractual obligations to repay a loan or to meet any other preexisting financial obligation.

Credit risk includes the risks of default, concentration and exposure to major commitments with a single counterparty.

Credit risk is the biggest risk for UNI. Our credit portfolio is made up of residential mortgage loans, personal loans and business credit.

UNI’s Board of Directors establishes the policy on credit risk management, which is implemented by the teams responsible for granting loans and managing credit products.

Credit granting

UNI’s Board of Directors establishes approval limits for the Credit Committee and Chief Credit Officer (CCO). The CCO then delegates the approval limits for the various staff members responsible for approving credit applications.

Credit decisions are based on a risk evaluation and on factors such as the credit risk management policy, credit practices and procedures, compliance and available collateral.

Loans to retail clients – Personal

Our personal loan portfolio is composed of residential mortgages, loans and personal lines of credit as well as point-of-sale financing. Each decision is assigned to a different level within our independent risk management teams business line. The goal of credit approval and portfolio management methods is to standardize the creditgranting process and rapidly detect problem loans.

As a reporting entity under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA), UNI has a mechanism in place to meet the regulatory obligations expected by the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC).

Risk management I UNI Financial Cooperation 55

Business loans

The business loan category is made up of portfolios of loans to small (retail businesses), mid-sized and large businesses.

For these main portfolios, the ratings process includes 17 ratings consolidated into 10 categories.

The following table compares internal ratings with external agency ratings.

The following table shows the credit quality of the business loan portfolio (amounts shown were calculated before the impact of provisions for credit losses and without account overdrafts).

($ thousands and %)

Business loans 2022 2021 Prime quality $602,408 36% $592,214 40% Satisfactory quality 974,010 58% 787,654 53% Under supervision 63,631 4% 45,543 3% Impaired and defaulted loans 49,523 3% 69,325 5% Total $1,689,572 100% $1,494,736 100%

Rating S&P Description 1 to 2 AAA to A 2.5 A- to BBB+ Prime quality 3 to 4 BBB to BBB4.5 to 5.5 BB+ to BBSatisfactory quality 6 to 7 B+ to B7.5 to 9 B- to C Under supervision 10 D Impaired and defaulted loans

56 Annual Report 2022 I Risk management

Credit risk mitigation

When a loan is granted to a member or client, UNI secures collateral for certain products in order to mitigate certain borrowers’ credit risk. This collateral typically takes the form of assets, such as capital, accounts receivable, stocks, investments, government securities or shares. As needed, UNI uses available risk-sharing mechanisms with other financial institutions.

Mortgages Consumer and other personal loans Business loans Breakdown of loans by borrower category at December 31, 2022 44% 15% 2022 41% 39% 46% 15% 2021 Loan portfolio quality at December 31, 2022 Gross impaired loans ($ thousands and %) $0 $20,000 $40, 000 $60,000 $80, 000 $100,000 0.0% 0.5% 1.5% 1.0% 2.0% 2.5% 3.0% 2018 2019 2020 2021 2022 1.52% 1.31% 2.53% 2.04% 1.41% $50,796 $45,085 $89,878 $77,686 $57,608 Gross impaired loans Ratio of gross impaired Risk management I UNI Financial Cooperation 57

UNI’s loan portfolio continues to be very sound. At December 31, 2022, total gross impaired loans were $57.6 million, down $20.1 million from 2021. This decline is linked to the fact that the adverse effects of the pandemic continue to subside. In 2020, a number of individuals and businesses were granted loan payment deferrals to mitigate the effects of the pandemic. Those with deferrals exceeding six months had to be classified as impaired. The hotel sector had the largest number of payment deferrals in 2020 and accounted for the majority of the increase in impaired loans since then. Although still fragile in 2022, the hotel sector has been recovering over the past two years.

UNI’s operations are concentrated in New Brunswick. At December 31, 2022, the loans granted to members and clients in this province represented 94% of our total loan portfolio. Due to this geographic concentration, these earnings depended heavily on the prevailing economic conditions in New Brunswick. A deterioration of conditions could have a negative impact on:

Past

due loans

Foreclosed assets

Claims and legal proceedings

The value of guarantees available for loans

UNI is nevertheless pursuing a prudent diversification strategy for its business credit portfolio outside of New Brunswick.

Market risk

Possible losses resulting from potential changes to the interest or exchange rate, the market prices of shares, credit gaps or desynchronization of market indexes or liquidity. Exposure to this risk arises from trading activity or investments creating on- and off-balance sheet positions.

Interest rate risk

UNI has adopted a strategy through which it takes on a very low level of risk associated with interest rate fluctuations. This strategy uses interest rate swaps to reduce the duration gap between assets and liabilities while keeping it within the parameters set by the Board of Directors.

Interest rate risk is managed using deterministic scenarios that show the potential impact of interest rate fluctuations on the capital ratio and the financial results.

Risk limits have been established to ensure that the company’s risk profile corresponds to the risk appetite determined by the Board of Directors.

Foreign exchange risk

UNI does not maintain any significant position on exchange markets. It holds only the foreign currencies (mainly US dollars) required to meet the anticipated needs of its members and clients. UNI assumes very little currency risk, and therefore, does not require protection against exchange rate risk.

Investment management

An investment policy covers the composition and quality of securities in our portfolios as well as the various portfolio management parameters for all funds under management associated with liquidity risk management.

Insurance risk

Possible losses incurred when paid compensation differs in practice from the actuarial assumptions (mortality, lapse, etc.) incorporated into the planning and pricing of insurance products.

UNI assumes life insurance risks (mortality, morbidity) only for life insurance and annuity products offered by Acadia Life. This subsidiary does not offer complex insurance products. Acadia Life maintains a capital lev exceeding regulatory requirements.

Operational risk

Losses resulting from shortcomings or defects related to procedures, employees, internal systems or external events. Outsourcing and cybersecurity sub-risks are treated separately due to their significance for UNI. Because of its heterogeneous nature, this risk is divided into 10 distinct sub-risks:

Internal fraud

External fraud

Damage to or limited access to tangible assets and buildings

Service interruptions and IT system malfunctions

Information security

Project management

implementation, delivery and management

Products, services and commercial practices

Human resources

Financial and management information integrity

58 Annual Report 2022 I Risk management

UNI has established policies, guidelines, procedures, computer systems, rules, standards, business continuity plans and internal controls to mitigate any losses that might arise from various sources associated with its operations.

Additionally, UNI has extensive corporate insurance coverage to cover any significant financial losses.

Third party risk

Possible losses (financial or other) due to failure of a third party to fulfill all or part of its non-financial contractual obligations (contractual misunderstanding). In such a case, potential costs associated with the implementation of an alternative solution to the services of the supplier in question could be incurred. UNI and its key third parties maintain excellent business relationships supported by management processes that provide for adequate risk management, among other considerations.

Cybersecurity risk

The loss of company or member and client data and/or limited system availability as a result of impairment to the company’s computer system security (e.g., computers, mobile devices, data centres, cloud storage, etc.). Losses attributable to the theft of or damage to hardware, software or data in computer systems, as well as the disruption or improper use of the technology services they supply.

Damage may occur as a result of network access, data or code injections. Losses may also result from social engineering, which refers to deceptive practices intended to manipulate our employees into committing fraud.

UNI regularly verifies that its third parties are properly managing cybersecurity risk. UNI implements strategies and security and preventive mechanisms to adequately mitigate risk. UNI makes significant investments to continuously improve its cybersecurity risk management maturity posture and periodically obtains independent certifications to confirm its posture.

Complaint and Dispute Management

Business locations, regional offices and the Client Contact Centre are the first point of contact for member and client complaints, as they are qualified and available to address concerns efficiently. If a complainant feels that their complaint has not been resolved to their satisfaction, they can contact the Office of Dispute Management. If a complainant feels that they have not received a satisfactory response from the Office of Dispute Management, they can contact UNI’s Office of the Complaints Commissioner. The Complaints Commissioner can provide an alternative to remedy any unresolved complaint in a neutral and impartial manner.

Lastly, if a complainant wishes to escalate their complaint, they can contact an external complaints handling body, either the Ombudsman for Banking Services and Investments (OBSI) or the Financial Consumer Agency of Canada (FCAC).

Details on complaints handled by the complaints commissioner in 2022:

1 A number of factors can affect processing time, including the timeliness of the member or client in allowing access to information, the complexity of the matter and work to obtain a settlement agreement. When we review member and client complaints, we make sure we have all the relevant information so we can make a fair and equitable decision for both parties.

2 Final decision concluded in favour of the member and client.

Complaints processed 1 Average1 processing time 8 days Resolution rate2 0 % Risk management I UNI Financial Cooperation 59

Consolidated Financial Statements

31, 2022

As of December

62 Annual Report 2022 I Consolidated financial statements

Table of contents Management’s Responsibility for Financial Information Independent Auditor’s Report Consolidated statement of financial position Consolidated statement of income Consolidated statement of comprehensive income Consolidated statement of changes in equity Consolidated statement of cash flows Notes to the consolidated financial statements 64 70 65 68 69 71 72 73 Consolidated financial statements I UNI Financial Cooperation 63

Management’s Responsibility for Financial Information

The consolidated financial statements of Caisse populaire acadienne ltée as well as the information included in this Annual Report are the responsibility of its management, whose duty is to ensure their integrity and fairness

The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards The consolidated financial statements necessarily contain amounts established by management based on estimates that it deems to be fair and reasonable These estimates include, among other things, the valuation of actuarial liabilities performed by valuation actuaries of Caisse populaire acadienne ltée, the valuation of the employee benefit liability, and the fair value measurement of the Caisse populaire acadienne ltée’s financial instruments All financial information presented in the Annual Report is consistent with the audited consolidated financial statements.

The Board of Directors of Caisse populaire acadienne ltée ensures that management fulfills its responsibilities with regard to the presentation of financial information and the approval of the consolidated financial statements of Caisse populaire acadienne ltée. The Board of Directors exercises this role mainly through the Audit Committees, which meet with the auditor in accordance with their mandates.

The consolidated financial statements were audited by the independent auditor appointed by the Board of Directors, Deloitte LLP, whose report follows The auditor may meet with the Audit Committee at any time to discuss its audit and any questions related thereto, notably the integrity of the financial information provided

Robert Moreau, FCPA, CGA, ICD D President and Chief Executive Officer

Éric St-Pierre, CPA, CMA Vice-President, Finance

Caraquet, Canada

March 2, 2023

64 Annual Report 2022 I Consolidated

financial statements

Tel.: 506-389-8073

Fax: 506-632-1210 www.deloitte.ca

Independent Auditor’s Report

To the members of Caisse populaire acadienne ltée

Opinion

We have audited the consolidated financial statements of Caisse populaire acadienne ltée (the “Caisse”), which comprise the consolidated statement of financial position as at December 31, 2022, and the consolidated statements of income, comprehensive income, changes in equity, and cash flows for the year then ended, and notes to the consolidated financial statements, including a summary of significant accounting policies (collectively referred to as the “financial statements”).

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Caisse as at December 31, 2022, and its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards (“IFRS”).

Basis for Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards (“Canadian GAAS”). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of this auditor’s report. We are independent of the Caisse in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Other Information

Management is responsible for the other information. The other information comprises the information in the Annual Report other than the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon. In connection with our audit of the financial statements, our responsibility is to read the other information identified above and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated.

We obtained the Annual Report prior to the date of this auditor’s report. If, based on the work we have performed on this other information, we conclude that there is a material misstatement of this other information, we are required to report that fact in this auditor’s report. We have nothing to report in this regard.

Deloitte

LLP 816 Main Street Moncton, New Brunswick E1C 1E6 Canada

Consolidated financial statements I UNI Financial Cooperation 65

Responsibilities of Management and Those Charged With Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with IFRS, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Caisse’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Caisse or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Caisse’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements