LEARN FROM YOUR MITSAKES MISTAKES

Issue 11 of 2022

E XCE LL ENCE IS D OIN G ORD IN A R Y THING S E XT R AO RD I N A RI LY W E L L

John W. Gardner

Call Saishen Krishnan Head of Hyphen PDA | 071 884 7300 Or call our friendly suppor t centre on 011 303 0060 - Option 2 or visit our website www.hyphenpda.co.za / Unimpaired and automated PDA systems / Integration with top-ranked Debt Counsellor systems / Best customer suppor t in the countr y queries are resolved within 24 hours / Strong compliance and best industr y practice implementation is at our centre WH AT M AKES U S E XCEL L EN T ?

CREDIT PROTECTION

CREDIT PROTECTION

Have you applied to go under debt review? Are you restructuring your monthly expenses? Would you like to insure your debt?

Why not insure all your outstanding accounts in a single ONE Credit Protection Policy?

Have you applied to go under debt review? Are you restructuring your monthly expenses? Would you like to insure your debt?

BENEFITS OFFERED:

• Death – we settle the account

Why not insure all your outstanding accounts in a single ONE Credit Protection Policy?

• Temporary Disability – we pay your installment for 12 months

• Permanent Disability – we settle the account

BENEFITS OFFERED:

• Critical Illness – we pay your installments for 3 months

• Death – we settle the account

• Retrenchment – we pay your installments for 12 months

• Temporary Disability – we pay your installment for 12 months

• Permanent Disability – we settle the account

At a rate of R2.95 per R1000 unsecured/short-term credit and R2.00 per R1000 on mortgages and you can now insure your debt for less.

• Critical Illness – we pay your installments for 3 months

• Retrenchment – we pay your installments for 12 months

The following financial obligations or debt can be covered on the ONE Credit Protection Policy:

At a rate of R2.95 per R1000 unsecured/short-term credit and R2.00 per R1000 on mortgages and you can now insure your debt for less.

The following financial obligations or debt can be covered on the ONE Credit Protection Policy:

• Overdrafts

• Maintenance Orders For further information please speak to your Broker, Debt Counsellor or alternatively contact your regional ONE office.

• Credit Cards

• Overdrafts

• Personal Loans • Home Loans

• Retail Accounts • Rental Agreement

Financial Services Provider

• Maintenance Orders For further information please speak to your Broker, Debt Counsellor or alternatively contact your regional ONE office. 0861 266 562 admin.debt@one.za.com Terms and Conditions Apply ONE Insurance Underwriting Managers (Pty) Ltd Reg No. 1996/008987/07. Authorised

FSP8783 VAT No. 4370160501

Products underwritten by Old Mutual Alternative Risk Transfer Limited a licensed Life Insurer

• Credit Cards

• Personal Loans

• Home Loans

• Retail Accounts

• Rental Agreement

0861 266 562

FROM THE EDITOR

We are almost there, the end of the year is just around the corner and the sense that things will be fine as long as we can just make it to the holidays looms large.

Somewhere they are no doubt busy unthawing Mariah Carey again and holiday tunes are beginning to make their way into the shops. People are tired but there is a glint in their eyes that says…soon.

It has been a rough year and as we approach the end of it I suppose we must congratulate ourselves for making it through the wave of Black Friday adverts and still having a cent to our names. Well done us for not spending money we didn’t have this year. And spending money you don’t have is pretty much how everyone lives these days. Even parastatals run at a huge loss each year. Soon we will be spending more to make up for all the spending people at Eskom have to do so I suppose we can’t be too smug just yet.

The mistakes of the past have finally caught up with the present and we are all paying the (now increased) price. But mistakes are easy to make. The trick is to survive your mistakes and grow. So if you are kicking yourself for getting into debt in the past or

FROM THE EDITOR

perhaps wishing you had never started trying to pay off your debt through debt review then be sure to read our article discussing mistakes in this issue. There may be thoughts which can help you think differently about your mistakes.

This issue we also discuss some industry specific news like recent NCT rulings and news about credit providers and the NCR. We also have tips for you which may well save you some bucks at the shops in the next few weeks so, check that out as well. We may need those bucks to pay for our electricity.

Debt review and dealing with debt can be hard. It can be tiring. It can leave you feeling worn out and exhausted. But not dealing with your debt can leave you totally wrecked so it is good that you are doing something about it. Even if you have to drag yourself through. Try stay positive.

A positive hope for the future, like a holiday or being totally debt free can keep you going when you are tired. You just have to remind yourself that good things lie ahead. So, please make your payment again this month. Make plans to make your payment early next month if you can and just keep going. You are almost there. And hopefully almost debt free.

South Africa’s Leading Debt Solutions Provider

Symington Steyn Coetzee Attorneys

Symington Steyn Coetzee Attorneys

‘‘The reason Zero Debt are industry leaders is that they get 80% acceptances on their initial proposals to credit providers, right away. They also make excellent use of the DCRS proposal system in negotiations with credit providers.

Zero Debt regularly succeeds in convincing credit providers to reduce their high interest rates down to less than 5% on their client’s debts.

This means that Zero Debt clients obtain their court orders and can pay off their debts quickly. They ensure dedicated clients get their clearance certificates and are soon able to start their debt free life.

Zero Debt’s team are very experienced and highly professional. They work hard to ensure clients are totally debt free at the end of the debt review process.’’

087 701 9665 | help@zerodebt.co.za | www.zerodebt.co.za NCRDC1142

Wessel

DEBT REVIEW Did you know... 35% of your credit score is determined by your payment history.

PROFESSIONAL DEBT COUNSELLING ATTORNEYS WESSEL SYMINGTON TEL: 021 872 1968 wessel@steyncoetzee.co.za www.steyncoetzee.co.za Assisting With Debt Review Matters Nationwide

We’ll get your interest rates right down. You’ll make one consolidated payment a month. You’ll have more cash to live on. Your assets will be legally protected. Sorted. 0861 365 910 No more debt-stress. Let’s get it sorted. info@debtbusters.co.za www.debtbusters.co.za NCRDC2484

CONTENTS

LEARN FROM YOUR MISTAKES

SHOPPING TIP CAN YOU RESIST THE TEMPTATION SERVICE DIRECTORY

HELP YOUR CLIENTS STAY ON TRACK THIS DECEMBER

Debtfree Magazine considers its sources reliable and verifies as much information as possible. However, reporting inaccuracies can occur, consequently readers using this information do so at their own risk. Debtfree Magazine makes content available with the understanding that the publisher is not rendering legal services or financial advice. Although persons and companies mentioned herein are believed to be reputable, neither Debtfree Magazine nor any of its employees, sales executives or contributors accept any responsibility whatsoever for their

activities. Debtfree Magazine contains material supplied to us by advertisers which does not necessarily reflect the views and opinions of the Debtfree Magazine team. No person, organization or party can copy or re-produce the content on this site and/or magazine or any part of this publication without a written consent from the editors’ panel and the author of the content, as applicable. Debtfree Magazine, authors and contributors reserve their rights with regards to copyright of their work.

DISCLAIMER

-Secure system-to-system data transfer (no human contact) -Elimination of data exposure from the use of email -Data specification is fit for purpose CONSUMER FRIEND USES SOFTWARE TO ENSURE POPIA COMPLIANCE! POPIA COMPLIANCE IS CRUCIAL!

LEARN FROM YOUR MITSAKES MISTAKES

TO ERR IS HUMAN LEARN

FROM YOUR MISTAKES

We all make mistakes. You cannot go through life without making many. Some mistakes are bigger than others and some will have larger consequences than others, but none of us can ever say we have never made a mistake.

Is that a bad thing? While we would like to avoid the negative consequences of a bad decision, we often learn from our mistakes.

For example, what toddler learns to walk without falling down along the way?

If you watch a young child persistently getting back up and trying again and again to stand or walk, you quickly realise that to fall, is human, as is getting up again.

So, let’s talk about mistakes and how we can use our past mistakes to shape our future.

FROM YOUR MISTAKES

MISTAKES LIGHT UP THE BRAIN LEARN

Research shows that when we make mistakes and recognise it, our brains light up with chemical activity.

While we may experience this as a sinking feeling, or a face-palm moment, your brain is securely storing the information and it makes a leaves a big impression. Almost as if it is saying: well, let’s not do that again.

A study, published in the Journal of Educational Psychology, showed that making deliberate mistakes (like writing down the wrong answer to a question and then correcting it) can help improve our memory.

One source says: “Mistakes are our opportunity to grow and to gain knowledge. Many people say that they wouldn’t have been where they were in life without making mistakes. The all-important part, though, is learning from them, and understanding how to extract the positives from something that many view as a negative.”

LEARN FROM YOUR MISTAKES

STOP THE BLAME GAME

When you constantly think about mistakes and try to blame someone else, it can put you in a very negative mind-set.

It is even harder, of course when we are the ones to blame. Accepting that we made a mistake is very hard for some people, and they will often try to shift the blame to others, or exaggerate other’s role in the mistake.

For example: Taking on a lot of debt is normally something we decide to do (for a variety of good and bad reasons). When something goes wrong, and we struggle to repay that debt, we may get angry with the credit providers who offered us the credit. Yes, they share some of the blame, but are they the main reason why we have debt?

Rather than blaming others, or ourselves for our mistakes, why not focus on making the most of the bad situation and finding the best way forward. This is a more productive use of our brain power and emotional bandwidth.

LEARN FROM YOUR MISTAKES

ADMIT YOUR MISTAKES

People are more likely to forgive others who make mistakes if they bravely, and quickly own up to it.

Not too long ago a Pope famously said the inquisition, and things that went on 350 plus years ago, was a mistake. Oops. You may not be that impressed since the organisation waited 350 years to apologise. So, it is normally better to promptly admit your mistake and move on.

This can help when one member of a household has a lot of debt that others do not know about. It is better to openly and honestly discuss the matter earlier (choosing a wise time and conditions for such a conversation, of course). Delaying such discussions will not improve the situation.

LEARN FROM YOUR MISTAKES

GET BACK UP

When a professional runner, who has trained for months if not years falls during a race, they do not immediately say: “well, that’s it, I can’t go on”.

No, just like that child who is learning to walk, they get back up and get going again.

So, if you have made mistakes that have knocked you down, then get back up and dust yourself off, get going again.

LEARN FROM YOUR MISTAKES

DON’T DWELL ON YOUR MISTAKES

It is good to learn from mistakes, but to constantly dwell on them is not healthy. Rather, cut yourself some slack, we all make mistakes.

For example, you may have over-committed to debt in the past. You may have taken on debt on behalf of other people. You may have felt your income was so secure that you could handle a large debt burden, only to find out later that things change and paying off debt is much harder than getting into debt.

You cannot let that dominate your thinking or planning. You need to acknowledge the lessons of the past, but be able to look ahead to the future.

Constantly dwelling on where you went wrong would be like trying to drive a car, but only look in the rear-view mirror. That is a recipe for disaster.

LEARN FROM YOUR MISTAKES

DEBT REVIEW IS NOT A MISTAKE

Debt review is not easy. Many people start the process and then struggle to make the changes it requires. Living a cash lifestyle in a credit crazy world is hard.

Most of us have learnt to use money to fix problems. Living on less and sticking to a budget takes a lot more work.

Still, if having debt was your problem, then debt review is the solution not a mistake.

So, stay positive about the process even if it is taking some time. Even if things don’t run smoothly due to the actions of a credit provider, or your Debt Counsellor, stay on target.

Keep paying your debt and working towards being debt free. It is worth it.

LEARN FROM YOUR MISTAKES

DON’T REPEAT YOUR MISTAKES

It goes without saying that we don’t want to make the same mistake over and over. That would indicate that we have not learned from our errors, and are doomed to repeat the cycle.

Rather, we want to be able to see the problem coming and make new, better decisions this time around.

So, if you identify something that you have done or tend to do that is bad for you…chose a new way.

For example, if in the past you would always try to use money to solve an issue quickly and easily, you will find that when money is tight, you are not able to do this and you have to look for sustainable solutions.

LEARN FROM YOUR MISTAKES

IN THE FUTURE

In the future you will pay off all your debt, you will be debt free, amazing!

Whether you then go out and take on a lot of debt again, or try stick to a debt free lifestyle is up to you.

Credit use can open many doors that would otherwise be shut. Debt can also weigh you down again so, use the lessons you learnt while paying off debt to shape your future.

Being over indebted (having more debt than you can repay each month) is tough. It is a hard and stressful way to live, and getting out of debt takes a lot of effort.

Try to learn from the mistakes of your past to shape the decisions of your future.

Leaving Debt Review Is Not As Simple As To Simply Stop Paying.

Consumers can only leave the debt review process at certain times and in certain ways.

This free e book will help you navigate this process and avoid many of the common mistakes people make when wanting to leave debt review.

If you are curious about how you can leave debt review properly and with no risk to your assets then be sure to download and read this free booklet

How do you leave Debt Review?

How do you have the Credit Bureau remove the Debt Review listing on your credit report?

DOWNLOAD

SHARE

AND

FREE BOOKLET TO DOWNLOAD AND SHARE

SHOPPING TIP

THE BEST DEAL SHOPPING

We

TIP

After all the media pressure of Black Friday, you may have spent money you had not planned on, and now need to make every cent count while at the shops. Here is a simple tip on how to get the most bang for your buck.

all love to save when we shop.

SHOPPING

TIP

DID YOU SURVIVE BLACK FRIDAY MADNESS?

A lot of people ran out during the Black Friday excitement, and bought many new shiny items. Most did so on credit, with money they have yet to earn. For some it will take months, if not years, to pay off these discounted specials.

When shopping, it is always good to plan ahead and save towards the expense. If you were one of those wise shoppers, who had funds waiting that you had been saving up, and if you then found a great deal: Good for you!

Black Friday reminds us that we can all be tempted into buying things if advertisers show you nice new shiny toys often enough. It may now be time to unsubscribe from all those mailing lists.

THE GREAT PRICE HIKE CUT SHOPPING TIP

Those original prices can often be ridiculously high. Thank goodness for the discount, wow what a saving!! But… if you look a little closer, the “discounted” price looks a lot like the regular price elsewhere.

The shop may be saying they slashed their prices, but actually they are showing you a silly made up price that no one would pay anyway, and their discounted price is simply closer to reality. Shops get bust doing this all the time.

Even then, with it being a more realistic price, you may STILL want to compare that price with what you can get from other suppliers.

DON’T FALL FOR FAKE PRICES!

Beware of falling for clever advertising, where the advert shows the original price crossed out, and a new lower price shown. This is very common at big brand name shops.

TIP

COMPARE PRICES SHOPPING

We know we should and with easy access to the internet and the ability to do online shopping, we tend to do this more often these days when shopping for pricier items.

It is a little tricky to do, when we are already in a shop walking the isles and shopping for groceries for example. After all, you don’t want to have to leave the store and walk to the nearby shop, and then check the price only to find out that the first store had the better price and then have to walk back to the shop and grab that item.

With the cost of fuel and how valuable our time is, it doesn’t make sense to do that, even if it might save significant money. Here is a tip that might help:

Now it might sound obvious that when you shop you should ‘shop around’ and find the best deal.

TOP TIP TO HELP YOU SAVE SHOPPING TIP

Many stores now have online shopping (websites) where you can see the prices of items that you regularly buy. Some shoppers say they are able to use these shopping apps and sites to their advantage.

Shopping online can be a big time saver and help you avoid impulse buying, but there is another way you can use these apps.

What you do is go into Shop A and open Shop B’s website or app. Now, as you shop, you can look at the prices in front of you that Shop A is charging and compare with Shop B on your phone. There is no need to wonder if that pack of chicken, or bag of potatoes is cheaper at Shop B. You can find out immediately.

Wonder how much they are charging for cooldrinks at Shop B? Check the price right away, and make an informed choice. This way you can be confident that you are paying the right price for the right item at Shop A and can either order the other items of Shop B’s app or head over there later, to grab those items with lower prices.

Doing this can quickly save you a lot of money. Money that you may not have, or perhaps could use towards paying for other things.

DEBT REVIEW

Did you know...

NCT stands for the National Consumer Tribunal.

The NCT act much like a specialised High Court and deal with credit related matters (mostly between consumers and their credit providers but also some debt review matters).

CAN YOU RESIST THE TEMPTATION

THE DECEMBER CHALLENGE

Why is that a challenge?

We all know money burns a hole in our pockets. We have all been guilty of it in the past, getting your salary early in December can be dangerous. Can you resist the temptation to not perhaps use just “a little” of those funds for something else?

What if your friends say they want you to come over and bring some braai meat or drinks so you can all relax. After all it is end of the year, or maybe it is a big family reunion. So then perhaps you dip into those funds instead of leaving them for your regular debt review payment. You may even be tempted to think that you will just pay a little less this month than what the court order requires.

See… it’s dangerous!!

Rather than face this nasty temptation this month, speak to your Debt Counsellor and see if you can organise for your debt review payment to go off earlier, when the funds come in? They will be happy to help.

And once the payment is done the temptation is removed.

If you are under debt review, you may find that December can present you with a number of unique challenges. One problem can be that you get paid early.

CAN YOU RESIST THE TEMPTATION

Protect your clients' nancial future with our specialised Credit Life Insurance products made for the Debt Review industry: dawid@creditguard.co.za hennie@creditguard.co.za Professional service & client satisfaction. Quick turn-around time & clear feedback. Competitive commercial agreements. Comprehensive product & easy switching. Expert Broker Services. Specialised broker: lane@f insafe.net Visit creditguard.co.za for more information. Or send an email to: Tel: 084 777 0945

We help care for your clients’ payment needs when they can’t.

Forget and be done with empty brokerage promises and non-existent service. Instead, join the industry professionals to help protect your clients' nancial future.

With CreditGuard, your Debt Review clients' debt is not only taken care of when they cannot commit to payments, but the service-orientated platform that the CreditGuard team provides is essential during your clients’ debt recovery journey. And, don't forget about the ‘insurance load’ taken o your company's shoulders going forward.

CreditGuard Credit Life Insurance (CLI) has taken care of Debt Review consumers' payment needs since 2016. It’s administrated by Siyavika Risk Solutions (an authorised nancial service provider – FSP no. 44999) and underwritten by Guardrisk Life Limited (1999/013922/05) – a licensed life insurer and an o cial nancial service provider (FSP no.76).

Looking for speci c core values is crucial in today's competitive market before partnering with a Credit Life Insurance entity.

Here at CreditGuard, our focus revolves around trusted, considerate client care service & quality products, systems and technology to ensure mutually bene cial and lasting partnerships.

CreditGuard o ers:

• Impeccable service; all (business) day, every (business) day.

• Clear and open communication.

• A comprehensive Credit Life policy and product customised to your expectations.

• A facilitation process between industry professionals and your clients.

• Solid understanding of your client's needs rather than just a 'commercial agreement'.

Our industry and brokerage experts know that life can take unexpected turns, even under Debt Review. With this, our promise is to take care of your Debt Review clients and their debt repayment responsibilities when their lives have changed in such a way that they aren’t able to.

CreditGuard’s comprehensive Credit Life Insurance policy/product allows you to switch from current CLI providers quickly and e ortlessly because it covers your clients’ risks better, for less.

It’s time to get going and partner with the quali ed Credit Life Insurance (CLI) experts of the Debt Review industry.

Contact the CreditGuard team today to get you sorted and your clients covered.

Your Quali ed Service & Insurance Partner

BREAKING NEWS

OLD MUTUAL – THE BANK?

Old Mutual is massive. They have a huge core business, and hold shares in many other businesses. For a long time, they held a majority share in Nedbank before OM split into various smaller self-sufficient operations.

At present, they are primarily making use of Bidvest Bank’s licence to assist their money account clients. This has (supposedly) been a strong earner for OM. OM has around 6 million customers, and has 1.1 million digitally active clients. The banking app has over 1 million downloads on Google Play (for whatever that is worth). Which probably means they have a large number of these banking clients.

But Old Mutual is not a bank…or at least they weren’t. This status is about to change, as Old Mutual has received the go ahead to apply for a banking licence. It is said they have already spent around R830 million developing their transactional banking engine, so they are very ready to formally enter the market.

The banking licence will also allow them to accept retail deposits (a nice way for them to get in some money to use) and be able to closely control their banking services to consumers. It will also allow for broader competition with some of the large banks, which have recently entered the insurance space.

GREEDY GOGO BUSTED

The cops in the Northern Cape have been busy busting people illegally operating as credit providers, and breaking all the rules in the National Credit Act & regulations.

“Operation Mashonisa” is aimed at catching small cash loan sharks who prey on vulnerable communities, and is a joint operation involving the NCR.

Recently, the provincial organized crime investigation unit ran 2 raids in the Kimberly area, and arrested 2 women (one 41 years old and the other a 70 year old) who have been fleecing their communities. These women had been illegally taking documents from consumers (like ID books) and charging all sorts of incorrect and illegal fees.

The cops seized several documents and items, including R25 000 in cash. The matter now goes to court where prosecution and fines are likely to follow.

If anyone loans money (of any amount) for a fee or interest, they have to register with the NCR as a credit provider, and stick to all the rules found in the National Credit Act.

NEW ANTI-TERRORISM LAWS IMPACT ALL CREDIT PROVIDERS

The National Assembly has signed off on the General Laws Amendment Bill. The bill is known as the Anti-Money Laundering and Combating Terrorism Financing Bill and is aimed to keep SA in line with international requirements (which if you do not follow, you end up grey listed apparently).

The Bill will amend 5 current Acts including the Companies Act, Financial Intelligence Centre Act (FICA), Financial Sector Regulation Act (FSRA), Trust Property Control Act and some parts of the Non-Profit Organisations Act.

The big change, is that these Acts will now include an updated definition of what it means to be a ‘beneficial owner’.

The Bill next goes to the National Council of Provinces (NCOP) for consideration (in something of a rush apparently) then will be given to the President to sign into law – hopefully before the end of this year (2022). What does it mean?

It means that all credit providers (including some collections agents who are registered as CPs) now become ‘accountable institutions’ (as per FICA) and have to register with the FIC.

This would include anyone who lends money for a fee or charges interest (as explained in the NCA), regardless of their size. Yet another nail in the coffin of illegal loan sharks, and another reason they can be fined and shut down.

It also means that once under FICA, all such credit providers will have to have a formal Risk Management Program, and can only onboard clients after they have done proper screening to know their client very well.

DCASA & THE NCR

The Debt Counsellors Association of South Africa (DCASA) recently met with the National Credit Regulator (NCR) and among other things asked that CIF meetings get going again. Just a short time later, during November, it was arranged for one of the Credit Industry Forum sub-committees to meet and continue discussions.

The meeting covered several hot topics including the NCR’s complaints department and issues involving what DCASA think may relate to insufficient training of complaints staff. DCASA pointed out that many times, their members get NCR instructions or findings that run contrary to the NCR’s own 2009 Task Team report and subsequent guideline. The NCR undertook to increase training for staff. There was also a discussion about trying to increase efficiencies in issuing annual NCR certificates to Debt Counsellors as delays hurt consumers greatly. The NCR may look to open up a unique email address to help deal with these issues.

The NCR and DCASA both shared their frustration at how some consumers are being taken for a ride by those claiming to offer consumers debt review related services, sometimes referred to as “rogue” debt counsellors within the industry. Some consumers simply call them “scammers”. Both the NCR and DCASA would like to see such operations shut down.

After the very productive meeting, DCASA stated that the NCR is strongly in favour of all Debt Counsellors belonging to associations which hold their members accountable like DCASA do.

+27 (21) 200 5644 adri@kempdubruyn.co.za 21 Station Street, Paarl, 7646 ATLANTIS BELLVILLE GOODWOOD CALEDON CAPE TOWN WYNBERG CERES GRABOUW HOPEFILED KHAYELITSHA KUILSRIVER MALEMSBURY MITCHELLS PLAIN MOORREESBURG PAARL PIKETBERG ROBERTSON SIMON’S TOWN SOMERSET WEST STELLENBOSCH STRAND TULBAGH WELLINGTON WORCESTER We appear in the following courts and act as a correspondent for Dc’s and their attorneys. Please contact adri@kempdebruyn.co.za to enquire about our fees.

DEBT REVIEW

NCT

issue court orders, where all credit providers

agree

restructure

consumer’s debt obligations,

consumer

Did you know... The

can

happily

to

a

to help the

avoid becoming over indebted.

leading Debt Counsellors

Call our national call centre on 086 111 6197 www.creditmatters.co.za NCRDC19 Just got out of debt!

South Africa’s

since 2007

HELLO DECEMBER

As we draw closer to December, we are aware of the festivities that come along with it. Within our industry, consumers should be counselled to spend their money wisely and not to overindulge.

There is a risk that consumers might not honour their debt review repayments. This could leave the consumer in a worse off position than before the start of the festive season.

Missed debit orders not only negatively impacts a consumer’s debt review program, as missed payments to creditors could lead to unnecessary terminations, repossessions or interest accrued, but also impacts your cash flow.

Salaries and bonuses tend to be paid out earlier in December. In an attempt to increase the collections percentage & ensure that consumers don’t miss their debt review payments, consumer engagement during the festive season is critical.

As we approach the last of what’s left of 2022, we would like to encourage you and your teams to join us in pressing through the final few weeks and ending the year triumphant.

Season’s Greetings from the iPDA Team www.ipda.co.za

LEGAL MATTERS

A Curious Case Of Good Faith

A recent NCT case is making Debt Counsellors confused about when they are allowed to stop assisting a problem consumer who refuses to cooperate with the process.

In the matter, a consumer noticed that some of their debts, which were included in debt review, had slowly been increasing because their interest rates had not been lowered by the credit provider but they were paying reduced monthly debt repayments.

The same consumer missed payments planned in their debt review and did not send attorneys needed documents. The Debt Counsellor involved says they tried to help the consumer and the consumer said the Debt Counsellor never told them everything and wants the Debt Counsellor to suddenly pay all their debts for them.

The Consumer tried to complained to the National Credit Regulator who essentially ruled in favour of the Debt Counsellor but told the consumer they could approach the National Consumer Tribunal if they wanted. This the consumer did. The outcome is interesting.

The Ruling

The National Consumer Tribunal (NCT) ruled in favor of the consumer in that it said the Debt Counsellor had not done all the duties as required by the Act and regulations (a point the NCT raised, not the consumer).

The NCT said the consumer had acted in good faith and that, though they refused to fine the Debt Counsellor or order them to pay off the consumer’s debts for them, the consumer could take their ruling to another court and pursue civil damages and see what happens.

The Debt Counsellor is unhappy with the ruling and says they are appealing the outcome*.

Some Key Points To Think About

The Consumer missed at least one payment while under debt review. The Debt Counsellor originally had agreements in place with the credit providers (based on a figure they calculated the consumer could realistically afford) but the consumer came back and asked for a lower monthly instalment.

*Both parties cannot really comment on the matter since the matter is getting appealed.

LEGAL MATTERS

The Debt Counsellor tried to make last minute, slightly lower, monthly repayment agreements for the consumer and had some pretty good success. This however resulted in two credit providers deciding they were not totally happy and they reverted to higher interest rates as agreed with the consumer in the past.

The consumer says they were not informed about the higher interest rate (the Debt Counsellor now says they have a recording) on the affected accounts.

The Debt Counsellor took a long time to organise the court order. The consumer delayed in sending documentation for the court and it appears they may have received a significant pay increase (and could thus pay more monthly) in the interim. The Debt Counsellor was not informed. The Debt Counsellor grew frustrated by the consumer’s non-cooperation.

The consumer wants to the Debt Counsellor to now be punished and have to take over their contracts or obligations to the credit providers and pay off the debts (incl. the capital not just the interest accrued).

Is a Debt that increases Bad?

If debt is bad then more debt is ‘more’ bad. Still, most people have experienced their debts grow due to interest and fees. That is very common.

collect / review / disburse C o l l e c t N e t Tel: +27 12 140 0602 | Email: info@collectnetpda.co.za | Web: www.collectnetpda.co.za Why choose us? New generation technology Fully automated and integrated Dedicated support for DC business growth Knowledgeable staff with extended support hours W e l c o m e t o o u r w o r l d o f e f c i e n c y a n d a u t o m a t i o n

LEGAL MATTERS

Smaller restructured payments to an account with normal higher interest is certainly is not wonderful for the consumer as they may end up paying more than originally hoped for. This is why most credit providers play fair during debt review and lower interest rates to something reasonable though they do not have to. Still this is the credit providers choice.

The current wording of the NCA actually does not address changed interest rates during a debt review, only reduced repayments and longer terms. Lowered interest rates are a real bonus for most consumers. Many times, credit providers do not enjoy it when a debt grows either but they do tend to make more money in interest so will not be too quick to complain too much.

A Debt Counsellor does not work directly for the client (even though they are paid by the consumer). Rather, they perform mandatory, statutory functions, as set out in the National Credit Act, and in many ways actually work for the courts. Debt Counsellors are there to make the court’s life easier in issuing debt restructuring court orders.

Where a debt may increase during a debt review it normally does so until one of two things happens:

1. Other debts are paid off and suddenly large payments are then snowballed or rolled over into that one debt. This sorts the debt out chop chop. or

Introduction to the DC Portal How to Register on the DC Portal Accessing a Consumer's Profile

simplifies the exchange of data and makes managing the debt review process less admin intensive.

below links take you to step-by-step guides on how to use the DC Portal on DREX.

STEP-BY-STEP DREX GUIDE

DREX

The

LEGAL MATTERS

2. The legally binding in duplum or Section 103(5) limit is reached and the consumer no longer has to pay any more than that figure to the credit provider, no matter how long it takes and what rates were charged.

So, the question is, is it always bad when a debt increases somewhat given the above? How does one weigh the consumers need to be able to afford the monthly necessities vs their obligations to their credit providers. Which should carry more weight when a consumer needs food on the table?

Is the Debt Counsellor only ensuring the consumer’s rights under debt review or do they have to balance the needs and rights of credit providers to recover their funds along with legally acceptable fees?

When Can We Say The Consumer Is Acting in Bad Faith?

It has long been the NCR’s view (and the industry view) that the NCA indicates that if a consumer does not provide the Debt Counsellor with the needed information to do their job then they can withdraw their services. This may well include missing required payments.

It seems right that if a consumer is not cooperating and does not intend to make proper use of the process that it is giant waste of time for a Debt Counsellor and all the consumer’s credit providers. Time they could all use to help others who really want to sort out their debts.

The NCT however found that despite such actions the consumer was acting in good faith. This seems curious and will no doubt be one of the points debated and argued in the appeal.

It will be interesting to see how that plays out and may help Debt Counsellors better understand when they can “fire” a bad, non cooperative client.

Keep Your Clients Informed

Whether there is or is not a recording in this matter it is true that consumers should be informed of their debt review as often and much as possible.

Many consumers may prefer to have the Debt Counsellor simply take over and do everything but it is a good idea to always check to make sure your payment is done, that your credit providers are getting their payments and that you are tracking your progress through the process.

While PDA reports cannot be 100% identical to the various statements from credit providers, consumers should keep their finger on the pulse and report any issues that they pick up to their Debt Counsellor. Good communication can keep everyone informed during a debt review.

Debtfree Magazine will continue to report on this story as it develops.

Debt Counselling / Debt Review Completion Debt Review Clearance Certificates We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information. Contact us to if you are ready to enter or finish debt review the proper way. NCR Registration No: NCRDC3106 info@ndrc.org.za www.ndrc.org.za

START YOUR CAREER IN ADR AND MEDIATION Become a Certified Mediator in 5 Days + benefit by accreditation with us (optional International Accreditation) Five Day Mediation Training: NOW R 3 425 instead of R 6 850 www.adr-networksa.co.za

Visit

facebook.com/groups/allprodc

Debt Counsellors Collective

Our members are able to attend the DC & CP Meet up, being held on the 29th Sept, in Cape Town the day before the Debt Review Awards. For more info check our Facebook page.

Email: alanm@moneyclinic.co.za the members Facebook page for the latest updates www.allprodc.org

Be sure to catch all the latest information on the website and in depth articles in the members section NDCA are ready to help consumers who are struggling with debt. Visit our site for more information ndca.org.za www.dcasa.co.za

FINISH

HELP YOUR CLIENTS STAY ON TRACK THIS DECEMBER

STAY ON TRACK IN DECEMBER

DON’T FEAR DECEMBER

December is always a tricky time for consumers. Some drop out of the process due to bad planning and bad budgeting. How can you help your clients make it this year?

Over the last 2 years, December payments have been fairly good due to Debi-Check and the Covid-19 pandemic limiting what people might spend. But with things being more open this year, we may see a change in consumer behaviour.

We asked Hyphen PDA for some advice to help you keep your clients in the process. Here are just 2 of many points they mentioned:

Step one is to talk to your clients and discuss steps they are taking to stay focused this December. Can they pay earlier? Step two would be to extend the DebiCheck tracking days (as salaries come in early).

Communication with clients is important throughout the year, but right now would be a wise time to reach out. Help them plan ahead, and not be complacent about their spending this December.

Let clients know if you are going to be closed on certain days, or running with a smaller staff compliment over the year end. Whatever you do, keep them informed.

STAY ON TRACK IN DECEMBER

PROTECT THEM FROM SCAMS

Scammers often target clients at this time of year. So, another tip is to remind clients that the PDAs do not change their banking details, and will never just ask for smaller payments in December.

Consumers can be reminded that the PDAs can be found as Public Recipients or Public Beneficiaries on consumers online banking or apps. So, if you have not yet done so, reach out to your clients (or PDA) and discuss what steps you can take to help consumers keep on track this December.

Looking for your next adventure? JOBS Do you have a job you would like to advertise? Email us on: jobs@debtfreedigi.co.za

What if... YOUR CLIENT’S VEHICLE IS STOLEN OR WRITTEN OFF? • Is he properly insured? • Could the insurer repudiate the claim due to his debt review status? • Since he cannot get more credit, how does he replace his vehicle? Ensure your client can get a replacement car if their vehicle is stolen or written off with the Meliorleaf Motor Replacement Plan. Did you know you can add the Meliorleaf Motor Replacement Plan to your existing vehicle insurance policy? MIWAY FSP 33970 | OWNSURANCE FSP 21974 | www.meliorleaf.co.za CALL US NOW 010 141 2799

DEBT COUNSELLORS SUPPORT SERVICES INSURANCE FINANCIAL TRAINING CLICK THE CATEGORY SERVICE DIRECTORY

CATEGORY DIRECTORY LEGAL CREDIT BUREAUS PAYMENT DISTRIBUTION AGENCIES CREDIT PROVIDER CONTACT DETAILS & ESCALATION PROCESS DO YOU WANT TO LIST YOUR COMPANY? directory@debtfreedigi.co.za

DEBT COUNSELLORS

NORTHERN CAPE WESTERN CAPE

NORTH WEST

GAUTENG

KWAZULU-NATAL FREE STATE LIMPOPO EASTERN CAPE MPUMALANGA

0861 365 910 info@debtbusters.co.za www.debtbusters.co.za One consolidated payment. Savings on interest rates. More cashflow. Let’s get it sorted! Debt doesn’t have to weigh you down. NCRDC2484 Debt Counselling / Debt Review Completion Debt Review Clearance Certificates Why Us? We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information. Do you want to take the first step to become DEBT FREE? Get started today by reducing your monthly debt repayments into one affordable payment. 021 204 4711 068 279 5951 info@debteezy.co.za www.debteezy.co.za NCRDC3042 GAUTENG Credit Matters South Africa’s Leading Debt Counsellors NCRDC533 14th Floor, The Pinnacle Cnr Strand & Burg St Cape Town Tel: 086 111 6197 Fax: 021 425 6292 info@creditmatters.co.za

debt therapy integrity guaranteed WEBSITE | www.debt-therapy.co.za SCARED OF ANSWERING YOUR CALLS? ake back control of your life in 1 easy step! debt therapy is registered with NCR | NCRDC49 Take the first step to financial freedom by visiting our : | FREE CALL 0800 20 47 28 Drastically reduce your monthly debt repayments Let US help 0861111863 Regain control of your finances NCRDC49 www.debt-therapy.co.za National Debt Advisors Fighting For Consumer Justice Tel: 021 007 1688 www.nationaldebtadvisors.co.za One on one confidential counselling and advice to help you reduce and clear your debts. 261 Surrey Avenue, Randburg, Gauteng 011 100 7192 enquiries@ctrldebtdelete.co.za www.ctrldebtdelete.co.za NCRDC2051 DELETE DEBT CTRL NCRDC1142 Tel: 087 701 9665 Email: help@zerodebt.co.za www.zerodebt.co.za

tlcdebt@mweb.co.za 016 100 8020 079 520 4369 Debt Counsellor Your Legal wings to nancial freedom! Alida Ericah Mtshali NCRDC4049 ericah@mandisam.com 076 578 8660 www.mandisam.com We pride ourselves for excellence and integrity GAUTENG

Do you want to take the first step to become DEBT FREE? Get started today by reducing your monthly debt repayments into one affordable payment. 021 204 4711 068 279 5951 info@debteezy.co.za www.debteezy.co.za NCRDC3042 0861 365 910 info@debtbusters.co.za www.debtbusters.co.za One consolidated payment. Savings on interest rates. More cashflow. Let’s get it sorted! Debt doesn’t have to weigh you down. NCRDC2484 Credit Matters South Africa’s Leading Debt Counsellors NCRDC533 14th Floor, The Pinnacle Cnr Strand & Burg St Cape Town Tel: 086 111 6197 Fax: 021 425 6292 info@creditmatters.co.za NCRDC1142 Tel: 087 701 9665 Email: help@zerodebt.co.za www.zerodebt.co.za KWAZULUNATAL

Why Us?

Debt Counselling / Debt Review Completion Debt Review Clearance Certificates

We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information. debt therapy integrity guaranteed WEBSITE | www.debt-therapy.co.za debt therapy is registered with NCR | NCRDC49 Drastically reduce your monthly debt repayments Let US help 0861111863 Regain control of your finances NCRDC49 www.debt-therapy.co.za National Debt Advisors Fighting For Consumer Justice Tel: 021 007 1688 www.nationaldebtadvisors.co.za

0861 365 910 info@debtbusters.co.za www.debtbusters.co.za One consolidated payment. Savings on interest rates. More cashflow. Let’s get it sorted! Debt doesn’t have to weigh you down. NCRDC2484 Credit Matters South Africa’s Leading Debt Counsellors NCRDC533 14th Floor, The Pinnacle Cnr Strand & Burg St Cape Town Tel: 086 111 6197 Fax: 021 425 6292 info@creditmatters.co.za FREE STATE NCRDC1142 Tel: 087 701 9665 Email: help@zerodebt.co.za www.zerodebt.co.za debt therapy integrity guaranteed WEBSITE | www.debt-therapy.co.za SCARED OF ANSWERING YOUR CALLS? Take back control of your life in 1 easy step! debt therapy is registered with NCR | NCRDC49 Take the first step to financial freedom by visiting our : | FREE CALL 0800 20 47 28 Drastically reduce your monthly debt repayments Let US help 0861111863 Regain control of your finances NCRDC49 www.debt-therapy.co.za

National Debt Advisors

Fighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Why Us?

We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information.

Debt Counselling / Debt Review Completion Debt Review Clearance Certificates

0861 365 910 info@debtbusters.co.za www.debtbusters.co.za One consolidated payment. Savings on interest rates. More cashflow. Let’s get it sorted! Debt doesn’t have to weigh you down. NCRDC2484 Credit Matters South Africa’s Leading Debt Counsellors NCRDC533 14th Floor, The Pinnacle Cnr Strand & Burg St Cape Town Tel: 086 111 6197 Fax: 021 425 6292 info@creditmatters.co.za NCRDC1142 Tel: 087 701 9665 Email: help@zerodebt.co.za www.zerodebt.co.za debt therapy integrity guaranteed WEBSITE | www.debt-therapy.co.za SCARED OF ANSWERING YOUR CALLS? Take back control of your life in 1 easy step! debt therapy is registered with NCR | NCRDC49 Take the first step to financial freedom by visiting our : | FREE CALL 0800 20 47 28 Drastically reduce your monthly debt repayments Let US help 0861111863 Regain control of your finances NCRDC49 www.debt-therapy.co.za LIMPOPO

National Debt Advisors

Fighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Why Us?

We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information.

Debt Counselling / Debt Review Completion Debt Review Clearance Certificates

0861 365 910 info@debtbusters.co.za www.debtbusters.co.za One consolidated payment. Savings on interest rates. More cashflow. Let’s get it sorted! Debt doesn’t have to weigh you down. NCRDC2484 MPUMALANGA Credit Matters South Africa’s Leading Debt Counsellors NCRDC533 14th Floor, The Pinnacle Cnr Strand & Burg St Cape Town Tel: 086 111 6197 Fax: 021 425 6292 info@creditmatters.co.za NCRDC1142 Tel: 087 701 9665 Email: help@zerodebt.co.za www.zerodebt.co.za debt therapy integrity guaranteed WEBSITE | www.debt-therapy.co.za debt therapy is registered with NCR | NCRDC49 Drastically reduce your monthly debt repayments Let US help 0861111863 Regain control of your finances NCRDC49 www.debt-therapy.co.za

National Debt Advisors

Fighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Why Us?

We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information.

Debt Counselling / Debt Review Completion Debt Review Clearance Certificates

0861 365 910 info@debtbusters.co.za

One consolidated payment. Savings on interest rates. More cashflow. Let’s get it sorted! Debt doesn’t have to weigh you down. NCRDC2484

Matters

Counsellors

debt therapy integrity guaranteed WEBSITE |

SCARED YOUR CALLS? Take back control of your life in 1 easy step! debt therapy is registered with NCR | NCRDC49 Take the first step to financial freedom by visiting our :

FREE CALL 0800 20 47 28 Drastically reduce your monthly debt repayments Let US help 0861111863 Regain control of your finances NCRDC49 www.debt-therapy.co.za NORTH WEST

www.debtbusters.co.za

Credit

South Africa’s Leading Debt

NCRDC533 14th Floor, The Pinnacle Cnr Strand & Burg St Cape Town Tel: 086 111 6197 Fax: 021 425 6292 info@creditmatters.co.za

www.debt-therapy.co.za

|

NCRDC1142 Tel: 087 701 9665 Email: help@zerodebt.co.za www.zerodebt.co.za

National Debt Advisors

Fighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Why Us?

We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information.

Debt Counselling / Debt Review Completion Debt Review Clearance Certificates

0861 365 910 info@debtbusters.co.za www.debtbusters.co.za One consolidated payment. Savings on interest rates. More cashflow. Let’s get it sorted! Debt doesn’t have to weigh you down. NCRDC2484 Credit Matters

Africa’s Leading Debt Counsellors

14th Floor, The Pinnacle Cnr Strand & Burg St

Town

Tel:

701 9665

help@zerodebt.co.za

debt therapy integrity guaranteed WEBSITE | www.debt-therapy.co.za SCARED OF ANSWERING YOUR CALLS? Take back control of your life in 1 easy step! debt therapy is registered with NCR | NCRDC49 Take the first step to financial freedom by visiting our : | FREE CALL 0800 20 47 28 Drastically reduce your monthly debt repayments Let US help 0861111863 Regain control of your finances NCRDC49 www.debt-therapy.co.za NORTHERN CAPE

South

NCRDC533

Cape

Tel: 086 111 6197 Fax: 021 425 6292 info@creditmatters.co.za NCRDC1142

087

Email:

www.zerodebt.co.za

National Debt Advisors

Fighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Why Us?

We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information.

Debt Counselling / Debt Review Completion Debt Review Clearance Certificates

0861 365 910 info@debtbusters.co.za www.debtbusters.co.za One consolidated payment. Savings on interest rates. More cashflow. Let’s get it sorted! Debt doesn’t have to weigh you down. NCRDC2484 Credit Matters South Africa’s Leading Debt Counsellors NCRDC533 14th Floor, The Pinnacle Cnr Strand & Burg St Cape Town Tel: 086 111 6197 Fax: 021 425 6292 info@creditmatters.co.za NCRDC1142 Tel: 087 701 9665 Email: help@zerodebt.co.za www.zerodebt.co.za debt therapy integrity guaranteed WEBSITE | www.debt-therapy.co.za SCARED OF ANSWERING YOUR CALLS? Take back control of your life in 1 easy step! debt therapy is registered with NCR | NCRDC49 Take the first step to financial freedom by visiting our : | FREE CALL 0800 20 47 28 Drastically reduce your monthly debt repayments Let US help 0861111863 Regain control of your finances NCRDC49 www.debt-therapy.co.za EASTERN CAPE

National Debt Advisors

Fighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Why Us?

We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information.

Debt Counselling / Debt Review Completion Debt Review Clearance Certificates

0861 365 910 info@debtbusters.co.za www.debtbusters.co.za One consolidated payment. Savings on interest rates. More cashflow. Let’s get it sorted! Debt doesn’t have to weigh you down. NCRDC2484 Debt Counselling / Debt Review Completion Debt Review Clearance Certificates Why Us? We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information. debt@cida.org.za 087 265 8748 065 874 7942 www.cida.org.za We’ll Create A Plan To Get You Out Of Debt Capes Independent Debt Advisors WESTERN CAPE National Debt Advisors Fighting For Consumer Justice Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Credit

NCRDC533

NCRDC1142

Tel: 086 111 6197 Fax: 021 425 6292 info@creditmatters.co.za

Tel: 087 701 9665 Email: help@zerodebt.co.za www.zerodebt.co.za

NCRDC3042

reduce your monthly debt repayments

Drastically

your

Let US help 0861111863 Regain control of

finances NCRDC49 www.debt-therapy.co.za

Matters South Africa’s Leading Debt Counsellors

14th Floor, The Pinnacle Cnr Strand & Burg St Cape Town

you want to take the first step to become DEBT FREE?

Do

Get started today by reducing your monthly debt repayments into one affordable payment. 021 204 4711 068 279 5951 info@debteezy.co.za www.debteezy.co.za

WESTERN CAPE

SUPPORT SERVICES TRAINING Debt Counselling / Debt Review Completion Debt Review Clearance Certificates Why Us? We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information. Octavia Hlatshwayo 084 032 7640 octavia@olwazini.co.za Mpumalanga | Regus Business Centre Nelspruit 11 Van Der Merwe Street | Mbombela www.olwazini.co.za @olwaziniskillsdevelopment Training Provider Accreditation Number: BANK-Ozswn190123

087 109 1164 info@dccp.co.za www.dccp.co.za Credit Life Insurance You make money, your clients save money 086 126 6562 debt@one.za.com www.one.za.com ONE Insurance Underwriting Managers (Pty) Ltd Reg No. 1996/008987/07. Authorised Financial Services Provider FSP8783 VAT No. 4370160501 Products underwritten by Old Mutual Alternative Risk Transfer Limited, a licensed Life Insurer. INSURANCE 50979 BEST RATES IN THE INDUSTRY

Liddles & Associates

“If you do what you’ve always done, you’ll get what you’ve always gotten.”

- Tony Robbins

(T) +27 87 138 3275 (E) quintin@liddlesinc.com www.liddlesinc.com

Steyn Coetzee Attorneys / Prokureurs

Adri de Bruyn

11 Market Street / Markstraat 11, Paarl, 7646

Tel: 021 872 1968 Fax: 021 872 2678 adri@steyncoetzee.co.za

RM Brown and Associates

16th Floor, The Pinnacle Cnr Strand & Burg St Cape Town

Tel: 021 202 1111, f: 021 425 0875 Email: roger@rmbrown.co.za

OUR SERVICES,

US

THE DETAILS

OFFER LEGAL SUPPORT TO DEBT COUNSELLORS WHO HELP OVER-INDEBTED CONSUMERS TO GET THEIR FINANCES BACK ON TRACK.

We have obtained granted court orders in more than 30 Magistrate Courts all over South Africa. TO MAKE USE OF

PLEASE CONTACT

ON

BELOW www.colynlaw.co.za 021 100 4189 info@colynlaw co za 163 Uys Krige Drive, SARU House, Tygerberg Office Park WE

LEGAL

079 6977 259 jus�n��dla�orneys.co.za

We are a Por t Elizabeth based law fir m capable of assisting Debt Counsellor’s throughout South

with matter s within the following areas of jurisdiction:

p 082 974 0866 www.cvlaw.co.za carla@cvlaw.co.za w Brighton; Motherwell; Uitenhage;

and Humansdor p 082 974 0866 www.cvlaw.co.za

CONTACT Jus�n �an Der Linde 1st Floor Icon House 24 Hans Strijdom Street Cape Town 8001

Africa

Por t Elizabeth; New Brighton; Motherwell; Uitenhage; Hankey; Jeffreys Bay; and Humansdor

Hankey; Jeffreys Bay;

carla@cvlaw.co.za

Accountability Group wendy@accountability.co.za Bitventure Consulting compliance@bitventure.co.za Blue Oak Systems enquiry@blueoak.co.za Cession Central admin@cession.co.za Clearscore regulatory@clearscore.co.za Clicknhire christiel@clicknhire.co.za Consumer Profile Bureau marina@cpbonline.co.za Credit Gateway compliance@creditgateway. co.za Cred-IT-Data Online Holdings bureau@creditdata.co.za CreditWatch marina@cpbonline.co.za CrossCheck Information Bureau marina@crosscheckonline. co.za South African Fraud Prevention Service NPC 011 867 2234 maigoshians@safps.org.za www.safps.org.za Credit Bureau Association info@cba.co.za www.cba.co.za sumein@vccb.co.za 087 150 3601 087 803 4798 www.vccb.co.za For Credit Bureau Services for Debt Counsellors contact Get your Credit Report Here CREDIT BUREAUS

Effective Intelligence sardagh@e-intelligence.com

Fides Cloud Technologies craig@fidescloud.co.za

Finch Technologies chris@finchinvestments.co.za

I-Bureau Services abrie@ibureau.services

IDR South Africa shane@v-report.co.za

iFacts sonya@ifacts.co.za

Managed Integrity Evaluation

marelizeu@mie.co.za

Maris IT Development marius@marisit.co.za

National Validation Services info@nvs-sa.co.za

Octagon Business Solutions gregb@octogon.co.za

Omnisol Information Technology info@verifyid.co.za

Inoxico support@inoxico.com

Kudough Credit Solutions chrisjvr@kudough.co.za

Lexisnexis Risk Management kim.bastick@lexisnexis.co.za

Lightstone chrisb@lightstone.co.za

Payprop Capital johette.smuts@payprop.co.za

PBSA seanb@PBSA.CO.ZA

Right Cover Online cto@rightcover.co.za

Searchworks 360 skumandan@searchworks360. co.za

ThisisMe juan@thisisme.com

TPN Group michelle@tpn.co.za

Trans Africa Credit Bureau

clintonc@transafricacb.co.za

Transaction Capital Credit Health DavidD1@tcriskservices.co.za

VeriCred Credit Bureau sumein@vccb.co.za

WeconnectU johann@weconnectu.co.za

Zoia Consulting sipho@dots.africa

Loyal1 tshepiso@loyal1.co.za

Smart Information Bureau info@smartbureau.net

PAYMENT DISTRIBUTION AGENCIES DC Partner 044 873 4530 Hyphen PDA 011 303 0060 COLLECTNET +27 12 140 0602 012 004 2888

Debt Counselling / Debt Review Completion Debt Review Clearance Certificates Why Us? We pledge to deliver the utmost in client service and act with the highest standards of integrity. Visit our social networks for more information. Debt Review Software Tel: 016 004 0031 South Africa’s premier debt management solution www.finwise.biz SYSTEM PROVIDERS MAXIMUS Tel: 011 451 0041 Tel: 0860 072 768 ‘’ I was pleasantly surprised by our experience new system is intuitive and easy Debt counsellor Eastern • • • • • FINWISE - INNOVATIVE DEBT MANAGEMENT

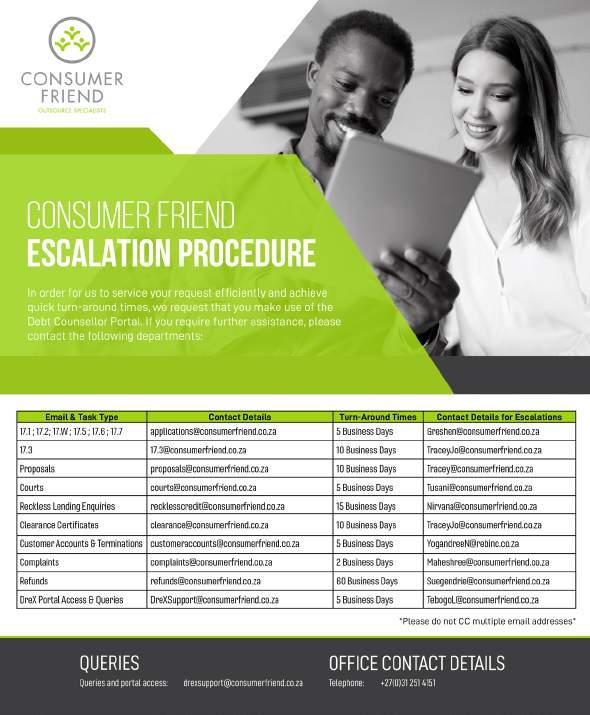

CONTACT DETAILS DEBT REVIEW NIMBLE GROUP

Dear Debt Counsellors,

R E : T H E N I M B L E G R O U P D E B T R E V I E W C O N T A C T D E T A I L S A N D E S C A L A T I O N P R O C E S S .

This letter serves to communicate to the Credit industry to use the following contact details for the Nimble Group when processing Debt Review related applications, enquiries, queries and, complaints escalation process.

Kindly take note Nimble Group hereby consents to service all legal documents applicable to Debt review herein by way of email.

Email & Task Type

Forms 17 1 and 17 7

Forms 17 2, Proposal Summaries, Cascade plans & Court orders

Forms 17.2 Rejection, 17.W & Form 19

Forms 17 3, General queries, settlements, balance, refunds, statements, Paid up letter request & reckless lending allegations, payment allocation queries & Complaints

Contact Details

drcob@nimblegroup co za

drproposal@nimblegroup co za drtermintation@nimblegroup.co.za drqueries@nimblegroup co za

DEBT REVIEW INBOUND CONTACT NUMBERS:

+27 87 250 5533 +27 21 8300 711

DEBT REVIEW ENQUIRIES ESCALATION MANAGEMENT ORDER CONTACT DETAILS

Kindly note that escalations must only be done once you have sent your request to the above mentioned contact email addresses and if your requests are out of SLA in lieu Debt Review forms response business days stipulated in the NCR Act

Kind Regards,

Denvor Rank

Operations Manager: Process Recoveries

1st line escalation

Aletta Tokollo Molelekeng Debt Review: Team Manager

D: +27 11 285 7247

E: AlettaM@normanbissett co za

2nd line escalation

Denvor Rank Operations Manager: Process Recoveries

O: +27 21 830 0750 (Ext 6062)

E: denvorr@nimblegroup co za

3rd Line escalation

Zivia Koff Specialised Process Manager

D: +27 21 492 4554

E: ziviak@nimblegroup co za

We trust this communication finds you well and that it will improve our service to you

CAPITEC BANK CONTACT DETAILS 2021.

Cindy

will be heading up the debt review department and will be supported

and Mrs. Fika Snyders in their capacity as Team Leaders. We have updated our communication and escalation channels in this regard. Please refer to the communication channels listed in tables 1 and 2 below. It is important that documentation be send to the correct communication channels to ensure timeous feedback. Table 1: Debt Review communication channels Channel Description E-mail address 1 Form 17’s All Forms 17’s / Clearance Certificates ccsforms17@capitecbank.co.za 2 Proposals All Proposals ccsproposals@capitecbank.co.za 3 Court documents All Court documents (Notice of Motion’s / NCT applications / Orders) ccsdebtrevieworders@capitecbank.co.za 4 Terminations Termination queries debtreviewterminations@capitecbank.co.za 5 General enquiries General Debt Review Enquiries ccsdebtreviewqueries@capitecbank.co.za 6 Refund / Cancellation requests Debt Review Refund Requests and Cancellation of Debit Orders ccsrefundrequests@capitecbank.co.za 7 Insurance Certificates Replacement Insurance Policies insurancepolicies@capitecbank.co.za 8 Reckless Lending Queries Allegation of reckless lending and document requests Rmcontrol@capitecbank.co.za 9 Credit Insurance Claims All credit insurance claims CreditInsuranceClaims@capitecbank.co.za 10 Payment allocations Payment Allocations queries ccsdebtreviewpaymentqueries@capitecbank.co.za 11 Share Call Contact number 086 066 7783 Option 2 086 066 7783

Mrs.

Mauritz

by Miss Meghan Bruiners

For more information about the escalation process please contact the call centre 0861 111 525

17.1, 17.2, Proposals, General correspondence: debtcounselling@africanbank.co.za To register for Legal Web Access: lwac@africanbank.co.za Reckless Lending investigations: RLA@africanbank.co.za ESCALATION PROCESS DETAILS COMING SOON For more information about the escalation process please contact the call centre debtcounselling@africanbank.co.za

For more information about the escalation process please contact the call centre 0860 111 2265

Authorised Financial Services Provider and a registered credit provider (NCRCP7) Absa idirect ’s FSP 34766 Absa Insurance Company ’s FSP 8030 0861 005 901 ABSADebtReviewDocuments@absa.africa

eviewDocuments@absa.africa debtreviewqueries@absa.co.za

www.nedbank.co.za DC QUERY PROCESS Fax or Email submissions (Level1) Email: DebtCounsellingQueries@nedbank.co.za Fax: 010 251 0055 To be used as a first point of contact for all written communication Call centre (Level 1: Alternative) Tel: 0860 109 279 To be used as a first point of contact for all telephonic communication Attended to by Queries Team Leader (Level 2: First Escalation) Dcescalation1@nedbank.co.za To be used only where no resolution is found from first point of contact after 5 business days Attended to by Senior Manager (Level 3: Final escalation) Dcescalation2@nedbank.co.za To be used only where no resolution is found from the first escalation after 2 Business days NEDBANK DRRS Debt Counselling Query Resolution Contact Points and Escalation Options

For more information about the escalation process please contact the call centre 012 674 7000 For updated consent to service documentation please contact the call centre.