Management Report

August 2020 - December 2022

GENERAL DIRECTORATE OF INTERNAL TAXES (DGII)

Content Introduction.............................................................................................................................1 1. General Advances.................................................................................................................2 1.1. Improvements implemented in terms of Registration, Income, Legal, Collection, Inspection and Special Regimes........................................................................................2 1.2. Efficient Government Program – Zero Bureaucracy.............................................................3 1.3. Digital Transformation.......................................................................................................4 1.3.1. Virtual Office (OFV).........................................................................................................4 1.3.2. Tax Migration.................................................................................................................5 1.3.3. Mobile app......................................................................................................................5 1.3.4. Digital interoperability....................................................................................................5 1.3.5. Business intelligence.......................................................................................................5 1.3.6. Electronic billing.............................................................................................................6 1.3.7. Motor vehicles................................................................................................................6 1.3.8. Certifications obtained....................................................................................................7 1.4. DGII 360 Program..............................................................................................................8 2. Collection...........................................................................................................................10 3. Facilitation and Services Advances......................................................................................12 3.1 New control modality: Electronic Invoicing........................................................................12 3.1.1 Importance of Electronic Invoicing.................................................................................12 3.1.2 Count on legal bases of Electronic Invoicing and Bill......................................................12 3.1.3 Approach of the General Bill of Electronic Billing in the Dominican Republic...................13 3.1.4 Free Billing Technological Tool......................................................................................13 3.1.5 Statistics / Advances in Electronic Billing.......................................................................14 3.2 Tax Education Program....................................................................................................14 3.2.1 University Program: Tax Education Subject....................................................................15 3.2.2 Other programs created and implemented....................................................................16

3.2.3 Tax Education Program for Universities..........................................................................16 3.2.4 Accounting and Fiscal Support Nucleus Program (NAF)..................................................16 3.2.5 Program to Create a Tax Culture in the University..........................................................16 3.2.6 Program One Step from Your Formalization...................................................................16 3.2.7 Implementation of the Tax Culture Week with University Students.................................17 4. Advances in legal matters...................................................................................................18 4.1 Technical Consultations....................................................................................................18 4.2 General Standard..............................................................................................................19 4.3 Resolutions......................................................................................................................21 4.4 Reconsideration Appeals..................................................................................................24 4.5 Department of External Representation............................................................................25 4.6 Tax Fraud and Crime Investigation...................................................................................28 4.7 Prevention of Money Laundering and Terrorist Financing..................................................29 4.8 Modification project of Title I of the Tax Code..................................................................30 5. Advances in auditing..........................................................................................................31 5.1 Risk-Based Tax Compliance Management Model ...............................................................31 5.2 Development projects......................................................................................................38 6. Management and Compliance Advances.............................................................................42 6.1 Post COVID Facilities........................................................................................................42 6.2 Application Law 46-20......................................................................................................43 6.3 Agreements to avoid double taxation...............................................................................44 6.4 Digital Economy...............................................................................................................45 6.5 Implementation of the Inclusive Framework......................................................................46 6.5.1 Action 5: Minimum Standard to Counter Harmful Tax Practices More Effectively:.....................................................................................................................46 6.5.2 Action 6: Minimum Standard to Prevent Treaty Abuse....................................................46 6.5.3 Action 13: Minimum Country-by-Country (CbC) Reporting Standard...............................46 6.5.4 Action 14: Standard to Make Dispute Resolution Mechanisms More Effective.................46 6.6 Coordination and Management of International Projects...................................................47 6.6.1 Project for the Institutional Strengthening and Modernization of the DGII-JICA...............47

6.6.2 Data Collection Study on Big Data and Artificial Intelligence (AI) in Tax Administration-2020-2021 with McKinsey & Company and JICA.....................................47 6.6.3 Project for the Institutional and Operational Strengthening of the DGII - UNDP...............47 6.6.4 Support in the adoption of new technologies in the tax administration with the Korea Public Development Fund for Economic Development (KPC) and IDB..............................47 6.7 Coordination and Management of International Technical Assistance...............................48 6.7.1 Public Finance Department (FAD) of the International Monetary Fund (IMF)....................48 6.7.2 IMF Regional Technical Assistance Center for Central America, Panama, and the Dominican Republic (CAPTAC-DR)..................................................................................48 6.7.3 United States Treasury Office of Technical Assistance (OTA)..........................................48 6.7.4 Inter-American Development Bank (IDB).........................................................................49 6.7.5 Organization for Economic Cooperation and Development (OECD).................................49 6.8 Offer of International Cooperation....................................................................................50 6.9 Management of International Tax Consultations...............................................................50 6.9.1 Made by the DGII...........................................................................................................50 6.9.2 Received from other tax administrations........................................................................51 6.10 Management of International Activities...........................................................................51 Annexes....................................................................................................................................................................53 1. Statistics on the management of international cooperation in the DGII..............................53 2. International Activities according to organizations 2020-2022...........................................53

The General Directorate of Internal Taxes (DGII) oversees the administration and collection of local taxes and fees in the Dominican Republic. In this sense, it continuously implements improvements and international good practices that allow the simplification and streamlining of its processes for the benefit of taxpayers.

For the correct administration, application of taxes, as well as to administratively interpret the provisions of the Tax Code and its regulations, from August 2020 to December 2022, a total of 24 General Standards have been published. Likewise, to facilitate and make tax actions operational, establishing the required procedures, 27 Resolutions have been published and put into effect.

On the other hand, a digital transformation process began to improve information technologies and systems available in the tax administration, and which have included the redesign and development of all the functionalities of the Virtual Office, the institution's mobile application, digital interoperability between this General

Directorate and other institutions of the state apparatus, as well as business intelligence and Electronic Billing.

To achieve the reduction of tax avoidance and evasion, it has had the support of different international organizations through assistance and technical consultations made to other tax administrations. From August 2020 to date , 23 technical assistances have been received and 6 consultations have been made to other tax administrations regarding treatments or interpretations on the matter.

In the same way, contact with the taxpayer has been promoted through the DGII 360 program and the tax education programs, and work has been done to update and introduce improvements in Title I of the Tax Code, which dates from 1992, to streamline processes and guarantee the rights of taxpayers.

Below is a brief management report on the most relevant progress for the period August 2020- December 2022.

1 Introduction December, 2022 1

Management Report August 2020 - December 2022

1. General Advances

1.1. Improvements implemented in terms of Registration, Income, Legal, Collection, Inspection and Special Regimes

• Simplification and efficiency of the registration processes for taxpayers and operational areas, which allows for greater control, alerts, and a level of security;

• New RNC statuses for taxpayers with compliance with Rule 04-21, through which the name of inactive status was changed to suspended. Additionally, the temporary cessation state was created and the criteria for entering or leaving each state were updated;

• Mark of obligated subjects, to identify natural and legal persons that carry out non-financial, commercial or business professional activities that by their nature are susceptible to being used in activities for money laundering and financing of terrorism supervised by the DGII;

• Generation and updating of the records to indicate various taxpayer statuses (active, suspended, temporary cessation, discharged);

• Corrections to the proforma processes and resolutions: automation and improvement of the determination resolution flow in TAX;

• Creation of the automation of the asset laundering prevention processes in the TRE system;

• Creation of an internal debt table, which shows the operational areas a standardized and automatic summary table that reflects the situation of a taxpayer, reducing processing times and possible human errors;

• Modifications to the payment agreement in persuasive and coercive collection through the correction of several problems that impacted the current tax account at the time of generating payment agreements, renegotiations of payment agreements and cancellation of renegotiations;

• Automation of collection, with which it is possible to reduce times, reduce manual activities, human errors and have a greater systematized control of management, with the aim of increasing collection;

• Creation and parameterization of loading of new delinquency inconsistencies, allowing Local Administrations to have delinquent cases available immediately upon expiration of the tax;

• Phase 2 risk profile, which includes the inclusion of new indicators to support the verification of the taxpayer's profile and determine the treatment according to their level of risk;

• Adjustments to the formats for sending transactions in the stock market, adding controls to the declaration formats 654 and 655;

• Update to the form of modifications for companies;

• Updating the affidavit form and/or payment of the selective consumption tax;

• Updating the sworn declaration form and payment of the tax on lottery and sports benches;

2 Management Report August 2020 - December 2022

• Update to the sworn declaration form and/or payment of the tax on gaming casinos;

• Update to the sworn declaration form and/or payment of the tax on slot machines;

• Creation of a new ex officio declaration for the payment of the Solid Waste Tax, which is automatically generated for the taxpayer in his OFV at the time of declaring IR2 or ISFL;

• Automation of the sending of daily collections to the Financial Management Information System (SIGEF);

• Modifications for the authorizations of tax receipt number sequences and electronic tax receipts;

• Modifications to the exemption process of the Tax on the Transfer of Industrialized Goods and Services (ITBIS);

• Updating of the declaration forms of the Simplified Tax Regime (RST), with the aim of simplifying the sworn declaration process for taxpayers and allowing them to benefit from this tax regime more easily. Likewise, new boxes and validations were enabled;

• Creation of the declaration for the payment of contribution for the management and co-processing of solid waste for RST taxpayers, according to Law 225-20; and

• Update to the affidavit form and/or payment of the Income Tax (ISR) for individuals of the RST based on income.

1.2 Efficient Government Program – Zero Bureaucracy

The Zero Bureaucracy Efficient Government Program is the first reform corresponding to the National Competitiveness Strategy and its objective is to promote efficiency in the Public Administration, through clear, timely and transparent regulatory frameworks that allow the simplification of procedures and public services, as well as the improvement in the quality of regulations, reducing times and costs for citizens and companies.

DGII is among the twenty-one (21) institutions that were prioritized for the year 2021, committing 14 procedures belonging to the Institution. Of these procedures, 10 were completed, representing 66% of the goal for that year. These procedures are:

1. Credit for Renewable Energy ISR Investment – Legal Entity

2. Credit for Renewable Energy ISR Investment - Physical Person

3. Transferable Film Credit

4. Incorporation into the National Taxpayer Registry (RNC) of Physical Persons– In person

5. Incorporation to the RNC of Physical Persons - Virtual

6. Incorporation into the RNC of Foreign Legal Entities

7. Request for Assignment of Sequence of Tax Receipts Legal Entities - Virtual

8. Request for the Assignment of the Sequence of Tax Receipts for Physical Persons - Virtual

3

Management Report August 2020 - December 2022

9. Request for Assignment of Sequence of Tax Receipts Physical Persons - In person

10. Approval of tax receipts with fiscal value

11. Incorporation to the RNC of Legal EntitiesVirtual

12. Transfer of Motor Vehicles – Physical Person, Trailer or Tow

13. Automation of Property Appraisal for payment of real estate transfer tax, and tax certification

14. Automation of Court Fees

As of December 2022, 7 of these completed procedures, related to the RNC and NCF (Tax Receipts) have been executed in 80% of the identified stages, while the procedures for Motor Vehicles and Renewable Energy ISR Investment Credit are in process; For the Transferable Film Credit, an internal efficiency module is being implemented and the payment of real estate transfers through Commercial Banks and NetBanking is in the process of starting.

1.3 Digital Transformation

DGII began a digital transformation process to promote the efficient use of information technologies and systems available to the tax administration, as detailed below:

1.3.1 Virtual Office (OFV)

• Redesign and development of all its functionalities.

• Incorporation of soft token as a security mechanism for transactions carried out.

• Inclusion of information regarding the assigned official of a taxpayer.

• Improvements in the user experience, enabling a personalized calendar that indicates which are the obligations that are about to expire, frequently asked questions and an expanded portfolio of services, with a friendlier and more intuitive graphical interface.

• Case management module in the Taxpayer Case Monitoring System (SECCON), which allows knowing the situation of the cases notified by internal control and carrying out the necessary actions without having to attend the Local Administrations in person.

4 Management Report August 2020 - December 2022

• Modification of the Message Box, Standard 05-21, which allows the acceptance or rejection of the virtual fiscal domicile.

• Adjustments to Standard 04-21 and the Web Portal on status queries of the National Taxpayer Registry (RNC), allowing or restricting access according to status. In the case of the suspended state, it allows you to make tax payments, declarations, change your password and request a password.

• Implementation of the unification of reimbursements of hydrocarbons and correction of the method to allocate the requests: Creation of the activities of analysis and verification of the request of the Ministry of Finance, as well as the other activities of the process of introducing a request for hydrocarbons.

1.3.2 Tax Migration

• Migration of the internal CORE to a more modern and efficient platform that will facilitate internal processes, guaranteeing a better service to users.

• Integration of the application module for registration and updating by OFV.

• Registration of pre-registered.

• Visualization of the history of RNC Minutes of a taxpayer.

1.3.3 Mobile app

• Redesign and development of the institutional mobile application, with the incorporation of multiple services.

1.3.4 Digital interoperability

• Web service for interconnection with the General Directorate of Customs (DGA), from where information is obtained on customs declarations for the use of inputs in motor vehicle processes.

• Strengthening technological solutions that facilitate interactivity with our processes for users: satisfaction surveys, digital evaluation of services, others.

• Happy Family Plan interconnection service, which allows the interconnection between the DGII and the Presidency of the Republic through web services to obtain relevant data on real estate.

1.3.5 Business intelligence

• Development and implementation of new business intelligence analysis entities that allow the elimination of manual processes in the generation of statistics on taxpayer service efforts and inconsistencies in tax information.

5 Management Report August 2020 - December 2022

1.3.6 Electronic billing

• Development and implementation of the Fiscal System of Electronic Billing.

• Provision of the free biller, which is a portal designed to facilitate the electronic billing process for compliance with current regulations, especially for Physical Persons and Micro, Small and Medium enterprises (MSMEs)

• Access to the Electronic Billing (EB) portal.

• Simplification of the validation process in accordance with the tax obligations of taxpayers from the OFV. Taxpayers who have users in Electronic Billing may directly access the FE portal without the need to authenticate via OFV.

1.3.7 Motor vehicles

• Electronic Provisional Plates: the application and payment process were enabled via the OFV, as well as the consignment of motor vehicles and trailers to duly authorized dealers, distributors, or sellers.

• Web consultation for the values of the motorcycles, which reduces the personalized services to a user who requests to know the value of the motorcycles to estimate the cost to pay for the transfer, which makes the attention time efficient for those who are going to carry out other transactions.

• Reversal of consignment and cancellation of license plates through electronic provisional license plate module.

• Cancellation of sales for the return of the vehicle.

6 Management Report August 2020 - December 2022

1.3.8 Certifications obtained

During this period, the DGII has obtained four (04) National Certifications granted by the Presidential Office of Information and Communication Technologies (OPTIC). They are detailed below:

• E1: Standard for the Management of Social Networks in Government Organizations.

• A3: Standard on Publication of Open Data of the Dominican Government.

• A4: Standard on Interoperability between the Organizations of the Dominican Government.

• A5: Standard on the provision and automation of public services of the Dominican State.

Likewise, a project is carried out to design and establish technology management processes in accordance with international reference frameworks such as COBIT 2019 and ITIL 4, which in turn are aligned with the requirements of the international standard ISO/IEC 20000-1:2018, which ensures the quality of the processes, strengthens the structure of governance and management of information technologies (IT) aligned with the institutional objectives.

7 Management Report August 2020 - December 2022

1.4 DGII 360 Program

It is a television program inaugurated in June 2022, dedicated exclusively to tax education, guiding taxpayers and the public on tax administration issues. It is broadcast weekly on the following channels and times: DGII

CERTV, Channel 4

South TV, Channel 57

As of December 2022, the topics discussed have been the following:

• Billing components, sequence of Tax receipt numbers, allocation algorithm, progress in Latin America with interviews from Chile, Brazil, and Mexico.

• Functions and processes of the Department of Motor Vehicles.

• Experience of the taxpayer and the citizen facing the tax administration.

• Virtual office.

• Know your Local Administration.

• Real estate value, property registry, what to do when a property is acquired? what is the IPI? etc.

• Functions of the Examination Branch, tax risks, control functions of examination management.

• Simplified Tax Regime, types of taxpayers eligible and advantages.

• Free biller as a facility for RST taxpayers.

• Projects of the Legal Sub direction.

• Default Reduction Plan.

• Functions and achievements of lawyers before the courts.

• What are obligated subjects?

• Administrative executor and conservatory measures.

• Technical inquiries and formal duties.

• Functions of the Fraud and Tax Crimes Investigation Management.

• Role of the DGII in the prevention of money laundering, the law that regulates this matter, as well as the standard that regulates cash payments and reliable proof of payment.

• Educational Expense Report

• Goods and Services (ITBIS), its behavior and impact on collections and details to consider in commercial operations related to IT-1

8

Television channels Color Vision, Channel 9 Saturday 8:00 to 8:55 a.m. 9:00 to 9:55 a.m. 9:00 to 9:55 a.m. 6:00 to 7:00 a.m. 8:00 to 9:00 a.m. Sunday Saturday Wednesday Sunday

360 Streaming Media

CTT (Santiago) Days Hours

Management Report August 2020 - December 2022

• Information related to tags.

• Information related to Income Tax (ISR) and some of the important processes that revolve around this tax.

• Special transmission in celebration of the School Day of Tax Culture with coverage of the activities carried out in 25 educational centers throughout the country, the General Director shared the vision of management regarding tax education.

• Tax on inheritance and donations and the process for the transfer of vehicles by inheritance.

• Selective Consumption Tax and the fiscal control and traceability system (TRAFICO), its objectives and contributions of this system to the collection process.

• Basic Internal Control Standards (NOBACI), its implementation and the launch of the internal Self-control contest "INNOBACIÓN".

• Simplified Tax Regime System, the important aspects to be considered by taxpayers when applying for this modality of taxation and the issue of the DGII's inspection and control power is discussed.

• Advances in the fight against corruption and policies implemented to improve transparency in the procurement and contracting processes.

• Elements to consider on invoices when making purchases during the Christmas season.

• Processes related to vehicle registrations and the main procedures that are carried out in the DGII offices and important aspects that revolve around the acquisition of the first license plate.

• Special transmission on the eve of the Christmas holidays, where a compilation of the DGII 360 program is detailed throughout its first months on the air.

9 Management Report August 2020 - December 2022

2. Collection

Since August 2020, the General Directorate of Internal Taxes has been focused on strengthening trust and transparency for Dominican citizens through the efficient administration of their resources and promoting tax compliance, through closeness and openness towards taxpayers and control measures through risk perception. These strategies have been the impetus to guarantee compliance with the budget goal during the period August 2020 until December 2022.

Although the Tax Administration began in a stage of great challenges and challenges, after a period of economic slowdown and health crisis in 2020, this was not an obstacle to the implementation of economic and health strategies such as the flexibility of mobility measures, the execution of the National

Vaccination Plan, the monetary stimuli implemented and the tax facilities granted, among others, which allowed a recovery in collection, returning to levels similar to those observed prior to the start of the pandemic.

When evaluating the behavior of collections in the period August 2020 to December 2022, it is observed that the effective collection exceeded more than one hundred percent of what was budgeted by the Ministry of Finance in the reformulated estimate. This performance is also perceived when evaluating collections with the original estimate for the years 2021 and 2022, with a compliance of 125.1% and 110.9% respectively. Similarly, this positive behavior is evident when comparing the interannual growth of collections.

Reformulated estimate and effective collection of the General Directorate of Internal Taxes August 2020 – December 2022; in millions of RD$

10 Management Report August 2020 - December 2022

Restated estimate Cash Compliance 177,116.4 601,554.5 643,801.6 200,163.8 607,446.4 656,812.1 113.0% 101.0% 102.0%-2020 2021 2022

In the period from August to December 2020, the observed collection was RD$200,163.8 million, presenting a compliance of 113.0%, for a positive difference in relation to the reformulated estimate of RD$23,047.4 million.

By the year 2021, the Dominican economy begins to perceive both an economic and health recovery when compared to the year 2020, thus allowing the relaxation of curfew measures and increased mobility. The above allowed the collection of the year 2021 to be RD$607,446.4 million, for a compliance of 101.0%, equivalent to RD$5,891.8 million above the reformulated estimate. This year's collection was boosted by Barrick's payments for RD$28,721.5 million, advances from Financial Entities RD$20,000.0 million, income received by Law no. 46-20 on Transparency and Patrimonial Revaluation, of RD$29,594.5 million and the liquidation of Income Tax in April 2021.

In 2022, different actions and measures were carried out to further promote tax compliance, such as the large-scale implementation of the

Electronic Billing model, the transformation of the Virtual Office, the reduction of service response times, new strategies control using the risk classification method, among others, thus allowing an accumulated collection of RD$656,812.1 million, for a compliance with collections of 102.0%, equivalent to RD$13,010.5 million more than the estimate in the reformulated General State Budget for the 2022.

In short, the period from August 2020 to December 2022 has benefited from fiscal and health strategies implemented by the authorities to mitigate the effects of the Pandemic, serving as a boost for budget compliance for this period. On average, the DGII contributed 72% of the total income obtained by the State through the collection entities and which is used transparently by the Government to cover the actions of providing public goods and services for the population and carrying out infrastructure works and investments, as well as for the payment of the public debt.

11 Management Report August 2020 - December 2022

Effective 2021 Effective 2022 607,446.4 656,812.1

Growth of the effective collection of the General Directorate of Internal Taxes 2022 vs. 2021; in millions of RD$

3. Facilitation and Services Advances

3.1 New control modality: Electronic Invoicing

Electronic Billing is an innovative billing modality, which allows the exchange of Electronic Tax Receipts (e-CF) between an issuer and a receiver in a standard invoice format; guarantees the authenticity of the tax documents issued, as well as the integrity of their content.

3.1.1 Importance of Electronic Invoicing

Esta modalidad de facturación incentiva y facilita el cumplimiento tributario de los contribuyentes a través del uso de las nuevas herramientas tecnológicas, a la vez garantiza y posibilita a la Administración Tributaria obtener informaciones de calidad y fiables para la correcta aplicación de los impuestos utilizando nuevos mecanismos para recolección y procesamiento de la información.

3.1.2 Count on legal bases of Electronic Invoicing and Bill

In August 2020, Electronic Invoicing was at the conclusion of the pilot phase where 11 large companies participated, in this year the General Standard 01-2020 was issued that regulates the issuance and use of Electronic Tax Receipts (e-CF), where the mechanisms that guarantee the integrity of documents using digital certificates are incorporated.

In 2021, General Standard 10-2021 was published, which establishes the procedure for the certification of Providers for Electronic Invoicing Services, with this the bases are laid for the certification of taxpayers as providers of Electronic Invoicing services and thus encourage the massive incorporation of

Management Report August 2020 - December 2022

The Executive Power deposited on September 13, 2022, before the Senate of the Republic, the General Electronic Invoicing Bill, which seeks innovation in legal systems to establish the mass use of Electronic Invoicing as a mandatory commercial modality. The initiative sent by the Executive Power has the purpose of regulating and establishing the electronic invoice to optimize the tax system. In it, entry deadlines are established gradually, as well as incentives for those who adopt it in the voluntary period.

On December 13, 2022, the Plenary of the Senate began the second (2nd) reading of the bill, leaving the continuity of its review on the table.

3.1.3 Approach of the General Bill of Electronic Billing in the Dominican Republic

• Innovation in legal systems to establish the mass use of electronic invoicing as a mandatory commercial modality.

• Establishment of electronic invoicing tax systems, which brings advantages for taxpayers by reducing the cost of compliance with tax obligations.

• Make available to small and medium taxpayers electronic invoicing applications in free lines or downloadable electronic invoicing systems.

• Improve efficiency, productivity, and tax transparency, as well as the fight against evasion and facilitate the exchange of tax information.3.1.4

Herramienta Tecnológica Facturador Gratuito

3.1.4 Free Billing Technological Tool

During 2022, the Free Invoice was implemented, which consists of a free technological facility provided by DGII that allows issuing and receiving e-CF, in accordance with the Electronic Invoicing tax system established in the Dominican Republic, for those taxpayers who wish to invoice electronically. operating from your computer with internet services, especially Liberal Professionals, Individuals and Mipymes, who do not have any system for these purposes.

In September of this year, a survey was carried out on users who have issued e-CF through the Free Biller, with the aim of evaluating the level of satisfaction with the tool and knowing their suggestions and comments, with a view to optimizing the operation of it.

In this sense, the users agreed that the Free Biller is a friendly and intuitive tool, since it facilitates the process, both in the issuance and reception of e-CFs, as well as in the assignment of sequence, likewise, a positive impact in administrative processes. In conclusion, the vast majority are very satisfied when using this new tool.

13 Management Report August 2020 - December 2022

3.1.5 Statistics / Advances in Electronic Billing

To date, more than 126 MM of Electronic Tax Receipts (e-CF) have been successfully issued, and a total of 270 taxpayers have been certified as Electronic Issuers, of which 146 issue their invoices through the Free Invoice tool.

We currently have 278 taxpayers who are in the certification process. About certified

Electronic Billing Service Providers, we have a total of ten (10).

3.2 Tax Education Program

DGII is committed to actions that promote a new tax culture in the Dominican Republic. For this reason, during the period August 2020 - December 2022, a total of 2,887 meetings were held in which 139,783 people have been trained, as detailed below

2022 reflects an increase in participants of 67% compared to 2021.

14 Physical Persons, Legal Entities, and the General Public Segments targeted by the Tax Education Program August 2020 – December 2022 Primary and Secondary Level Students (Tax Culture) 661 45,598 Meeting Trained MINERD Teaching Staff 262 8,196 Teachers and University Students 638 23,497 Micro, Small and Medium enterprises (MiPymes) 220 6,259 986 53,011 State Employees 120 3,222 Total 2,887 139,783 46,287 77,327 2021 2022

Management Report August 2020 - December 2022

3.2.1 University Program: Tax Education Subject

Tax issues in the universities of the Dominican Republic over time have been applied in careers directly related to the field of taxes, such as Accounting, Law, Auditing and Administration. It is important to highlight that the curricula of these careers develop technical skills exclusively for the future professional practice of the university; Leaving aside, what corresponds to Education and Tax Culture, the importance of correlating taxes on their Social Role and what it represents at the State and Citizen level.

For this reason, the General Directorate of Internal Taxes (DGII) and the Ministry of Higher Education, Science and Technology (MESCYT) presented a program proposal for the Tax Education subject to be incorporated into the curricular offer in universities and higher institutions of the country.

3.2.1.1 Foundation of the subject

The Tax Education subject is based on the need to train future professionals with the skills of knowledge, procedures, values and attitudes, which allow them to enter the tax environment of the Dominican Republic, fully aware of their duties and rights as citizens and professionals, with a high social sense, tax morale, fiscal conscience, and civic values.

3.2.1.2 Description of the subject

La Asignatura Educación Tributaria es de formación especializada. Consta de seis (06) unidades las cuales desde una visión holística buscan desarrollar competencias profesionales en el área tributaria, la conciencia fiscal, y los valores ciudadanos.

3.2.1.3 Course objectives

Recognize the importance and value of the constitutional duty to pay taxes, compliance with the duties and rights of citizens as a guarantee of citizen coexistence and contribution to the sustainable development of the nation and build a healthy tax culture and social responsibility in educational institutions superior.

3.2.1.4 Learning Competencies within the subject

• Values the social meaning of the taxes.

• Shows fiscal awareness in accordance with citizen values.

• Explains the structure and characteristics of the Tax Administration and its role with respect to taxes.

• Conceptualizes taxes to contribute to the quality of goods and services offered by the State to citizens.

• Analyzes the tax cycle, as well as the duties and rights of taxpayers.

• Analyzes the duties and powers of the Tax Administration.

• Exhibits professional ethical conduct and social civic commitment.

• Recognizes the importance of knowledge in Tax Education.

15 Management Report August 2020 - December 2022

3.2.2 Other programs created and implemented:

3.2.3 Tax Education Program for Universities

It consists of accompanying university professors in the content of their subjects, developing activities that reinforce the content that they share in that current semester or four-month period. Coordinate directly with the teacher.

3.2.4 Accounting and Fiscal Support Nucleus Program (NAF)

The objective of this program is to train a group of university students so that they can serve the public in basic orientation on tax processes; This program is developed with the signing of an agreement between the Tax Administration and the University, promotes the Tax Culture and Social Responsibility in the student body. We currently have two (2) universities participating in the program.

3.2.5 Program to Create a Tax Culture in the University:

It is a program that we have just started, it has been designed with the purpose of deploying a series of educational strategies with the purpose of Promoting and Creating Tax Culture in university environments. This program aims to achieve its objective through the following strategies: Cultural Days on Social Role of Taxes for all university actors, especially students and teachers.

3.2.6 Program One Step from Your Formalization

Develop an exclusive training program for university students, from various areas who wish to start a business and who need the essential tools to carry it out, linking Entrepreneurship centers of the country's Universities as promotion and dissemination allies.

16 Management Report August 2020 - December 2022

3.2.7 Implementation of the Tax Culture Week with University Students:

EIt is a project designed to promote fiscal awareness, develop in students a critical attitude, voluntary and reflective compliance with social responsibility.

Another of the strategies developed was because of the Covi-19 pandemic, which prompted us to innovate, creating new ways of approaching the university public; creating virtual training of open call at the national level, on different tax topics. This modality provides the facility for the university student to participate in the subject of his interest according to his availability of time, and for personal interest in terms of expanding his knowledge. The calendar is shared through mass mailings to the universities, as well as using social networks. This program facilitates activities from the basics, which is to understand the Dominican Tax System, the process for formalization, and the main taxes and tax procedures.

Also included was the presence of tax educational materials in university libraries nationwide, a club or specialized study groups to strengthen the filling of forms, learn in depth about specialized topics, as well as provide practical activities that the university requires strengthening, on tax processes. This program is made known through mass mailings to universities, as well as through social networks.

17 Management Report August 2020 - December 2022

4. Advances in legal matters

4.1 Technical Consultations

With the aim of promoting transparency and complying with the duty of publicity provided for in the Tax Code, the DGII, as of June 2021, has taken the initiative to publish the technical queries issued on its website.

Through this publication, citizens can have access to the criteria and interpretation of the Tax Administration on a certain legal text and its correct application and, in turn, comply

with the principle of equal treatment established in our Constitution and in the Law 107-13 2.

The following table shows the detail of technical consultations received and processed in the periods between August 2020 and December 2022, divided by calendar year:

Technical Consultations

18 Detail of Technical Consultations Aug – Dec 2020 2021 2022 Total Observations Inquiries received 2,535 Queries answered on time 2,372 6,507 5,945 8,779 7,711 17,821 16,028

0 2,000 4,000 6,000 8,000 10,000 2,535 2,372 6,507 5,945 8,779 7,711 16,028 17,821 12,000 14,000 16,000 18,000 20,000 Aug – Dec. 2020 2021 2022 Total Inquiries received Queries answered on �me Management Report August 2020 - December 2022

From May 2021 to October 2022, more than 609 responses to technical queries have been posted. This initiative has improved the unification of criteria within the Administration itself on issues of the same nature.

The following table shows the detail of the technical queries published by year:

4.2 General Standard

For the correct administration and application of taxes, as well as to administratively interpret the provisions of the Tax Code and its regulations, from August 2020 to December 2022, a total of 24 General Standards have been published, the details of which are found below:

19 Published Technical Consultations Years Quantity 2021 290 Published Technical Consultations 2022 319 319 Published Technical Consultations 290 319 Published Technical Consultations 2021 2022

Management Report August 2020 - December 2022

Promotion and Tax Optimization of the Stock Market. 2021

Reincorporation of the provisions of General Standard no. 05-2020 for application of the provisions of Law no. 46-20 of Transparency and Equity Revaluation.

Application of exemptions for the agricultural sector.

About the National Taxpayer Registry (RNC).

Modifies General Standard no. 05-2014 on the use of Telematic Media of the DGII.

General Standard no. 06-18 on Tax Receipts.

Application of the provisions of Law no. 46-20 of Transparency and Equity Revaluation and its modifications, dated October 7, 2020. 2021 07-2021

Fiscal Security and Control Mechanisms for Manufacturers, Producers and Importers of Finished Alcohol and Tobacco Products. 2021

Establishes the procedure for the certification of providers for Electronic Invoicing services.

Establishes the characteristics, issuance procedure and use of provisional plates and transfer plates for motor vehicles and trailers.

Procedures related to the payment of the tourist card in air and sea tickets.

Regulates external audits on the prevention of money laundering, financing of terrorism and financing of the proliferation of weapons of mass destruction.

Concept Published General Standard Year 2020 No. 05-2020 2021 01-2021 Validity Repealed Repealed Repealed In Force In Force

In Force

11-2021 In Force

2021

02-2021

2022 03-2022 03-2021 In Force

05-2021 In Force

06-2021 In Force

2021

Modifies

2021

10-2021 In Force In Force

2021

2022 02-2022

04-2021 In Force Country-by-Country

2021 08-2021 In Force Inventory withdrawals not invoiced 2021 09-2021 In Force Reorganization of Companies. 2022 01-2022 20 Management Report August 2020 - December 2022

2021

Report

Incorporation, permanence, exclusion, and affidavit in the Simplified Tax Regime (RST).

Regulates the application of the enforceability of the reliable proof of payment by the DGII in the procedures of motor vehicles and trailers.

Regulates the application of the enforceability of the reliable proof of payment by Public Notaries.

Modifies article 3 of General Standard no. 08-2021 on the Country-by-Country Report.

Establishes the procedure for the application to the DGII of sanctions, conservatory, and precautionary measures that, under the protection of the Law, are required by the bodies and entities of the public administration.

Establishes the refund or compensation of the Tax on the Transfer of Industrialized Goods and Services (ITBIS) for exporters.

4.3 Resolutions

To facilitate and make tax actions operational, establishing the required procedures, during the period August 2020 - December 2022, 27 Resolutions have been published and put into effect, which are detailed in the following table:

Concept Normas Generales publicadas Year No. 2022 04-2022 Validity In Force 2022 06-2022 In Force In Force

2022

2022 09-2022 07-2022 In Force

2022 11-2022 In Force

Establishes the granting of benefits contained in international conventions to avoid double taxation.

2022 12-2022 In Force

2022 08-2022 In Force Agreement procedures for dispute resolution 2022 10-2022 In Force In Force

of

for the agricultural sector. 2022 05-2022 21 Management Report August 2020 - December 2022

Application

exemptions

DDG-AR1-2020-00001

2021 128-20

2021 DDG-AR1-2021-00001

2021 DDG-AR1-2021-00002

Exemption from advance payment of Income Tax for periods August-December 2020 and Exemption of the first installment of Asset Tax (ISA) for micro and small businesses for the year 2020.

Appointment of the DGII Administrative Executor.

Granting of facilities due to COVID-19, January-April.

Information on multipliers, adjustments and various regulations for the December 2020 fiscal year, and others for the 2021 fiscal year.

2021 DDG-AR1-2021-00003

2021 DDG-AR1-2021-00004

Information on multipliers, adjustments and tax exemptions for the agricultural sector, fiscal year 2021.

Informative of the specific amounts of the Selective Consumption Tax on cigarettes and alcohol.

2021 DDG-AR1-2021-00005

2021 100-2021

2021 DDG-AR1-2021-00006

2021 DDG-AR1-2021-00007

2021 DDG-AR1-2021-00008

Income Tax taxpayers with fiscal closing March 2021 and RST taxpayers for fiscal year 2021.

DGII Code of Ethics

Facilities for the second quarter 2021, due to Covid-19

Indexation of specific ISC amounts and temporary exemption from ITBIS in respiratory devices.

Multipliers, adjustments, and various regulations for the fiscal closing of June 2021.

2021 DDG-AR1-2021-00009

2021 DDG-AR1-2021-00010

2021 162-2021

Informative indexation of specific amounts ISC and temporary exemption from ITBIS in respiratory devices.

Information on multipliers, adjustments, and various regulations for the fiscal closing of September 2021.

Designation of the DGII administrative executor.

Concept Published Resolutions Year 2020 Numeration

22 Management Report August 2020 - December 2022

Year Numeration

2021 163-2021

2021 DDG-AR1-2021-00011

2021 DDG-AR1-2021-00012

2022 DDG-AR1-2022-00001

2022 DDG-AR1-2022-00002

2022 DDG-AR1-2022-00003

2022 DDG-AR1-2022-00004

2022 DDG-AR1-2022-00005

2022 DDG-AR1-2022-00006

2022 DDG-AR1-2022-00007

Published Resolutions

Concept

Appointment of the DGII Procurement and Contracting Committee.

Abbreviated procedure for unvoiced inventory issues.

Informative of indexing specific amounts ISC.

Multipliers and adjustments for the fiscal year of December 2021, and others for fiscal year 2022.

Tax exemption for individuals and adjustments to the RST, fiscal year 2022.

Indexation of specific ISC amounts.

Multipliers and adjustments for fiscal closing March 2022.

Informative of indexing specific amounts ISC.

Multipliers and adjustments for fiscal closing June 2022.

Indexing specific amounts ISC for the period October –December 2022.

2022 DDG-AR1-2022-00008

2022 56-2022

Multipliers and adjustments for fiscal closing December 2022.

Repeals Resolution No. 162-2021 and appoints the Administrative Executor of the DGII.

2022 DDG-AR1-2022-00009

Indexing specific amounts ISC for the period January –March 2023.

23 Management Report August 2020 - December 2022

4.4 Reconsideration Appeals

During this period, 13,120 reconsideration cases have been worked on, which are classified as detailed in the following table:

General summary of outgoing cases for reconsideration (Aug 2020 – Dec. 2022)

General summary of outgoing cases for reconsideration (Aug 2020 – Dec. 2022) Quantity Reconsideration resources worked 11,229 Resources failed and worked 365 Not Appealable 367 Extemporaneous 2,238 Withdrawals 14,199 Total

24

Resources failed and worked Not Appealable Extemporaneous Withdrawals 11,229 365 367 2,238 0 2,000 4,000 6,000 8,000 10,000 12,000 Management Report August 2020 - December 2022

Management Report August 2020 - December 2022

4.5 Department of External Representation

From the area of external representation, the representation of the Institution before the courts is coordinated, in all appeals filed by taxpayers against administrative decisions and tax determination. In that sense, as of August 2020, the following actions have been carried out:

Tax Actions (August 2020 – December 2022)

Other actions (Cassation, precautionary measures, amparo, review, delay)

Tax Actions (August 2020 – December. 2022) Quantity 2,067 Contentious Tax Resources worked 967 Contentious Tax Resources (retardation) 1,906 Other actions (Cassation, precautionary measures, amparo, review, delay) 2,634 Judgment in favor 349 Judgment against 7,923 Total

25 2,067 967 1,906 2,634 349 7,923 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 Contentious Tax Resources worked Contentious Tax Resources (retardation)

Judgment in favor Judgment against Total

Likewise, during the period mentioned above, the external representation area participated in the following hearings on tax matters:

Tax Hearings (2020 - 2022)

Tax Hearings 2020 19 2021 72 2022 145 Action for amparo 33 94 256 Precautionary Measure 0 9 98 Contentious Tax Resources 6 100 153 Applications for judicial review 2 6 15 Proceedings for delay 2 63 181 Appeals for review 2 12 75 Others 64 356 923 Total

26 19 33 0 6 2 2 2 64 72 94 9 100 6 63 12 356 145 256 98 153 15 181 75 923 0 100 200 300 400 500 600 700 800 900 1000 Action for Amparo Precautionary Measure Contentius Tax Resources Applicactions for judicial review Proceedings for delay Appeals for review Others Total

Tax Hearings 2020 Tax Hearings 2021 Tax Hearings 2022 Management Report August 2020 - December 2022

In the civil part, we have:

Tax Hearings 2020 1 2021 4 2022 7 Action for amparo 2 23 16 Application for intervention 5 32 50 Referral 4 18 21 On claims registered 4 Applications for judicial review 3 15 Claim for damages 1 1 5 9 4 1 1 8 2 Suit for dissolution Demand for accountability Specification requirements i Demand for return of consigned values 18 108 251 Total Demand for annulment of amicable partition/donation between living persons 27 0 50 100 150 200 250 300 Action for amparo Application for intervention Referral On claims registered Applications for judicial review Claim for damages Suit for dissolution Demand for accountability Specification requirements i Demand for return of consigned values Demand for annulment of amicable partition… Total Tax Hearings (2020 - 2022) Tax Hearings 2022 Tax Hearings 2022 Tax Hearings 2022 Management Report August 2020 - December 2022

4.6 Tax Fraud and Crime Investigation

Among the processes carried out by the Legal Subdirectorate, is the planning of the processes of investigation and study of those cases, sectors and figures involved in tax evasion schemes, to contribute to the fight against tax fraud. Thus, taxpayers involved in (i) complaints, (ii) cases or sectors investigated are followed up, through which the modus operandi and the impact on the tax administration are identified.

Tax Fraud and Crime Investigation

Tax Fraud and Crime Investigation

Quantity Actions (aug. 2020 – dec. 2022) 571 Tax investigations carried out 422 Complaints answered 4,367 Request for information answered 20 Tax intelligence projects executed 26 Judicial litigation 38 Requests for investigation (complaints and judicial litigation) 5,444 Total

28

(Aug. 2020 - dec. 2022) Tax investigations carried out Request for information answered Tax intelligence projects executed Judicial litigation Requests for investigation (complaints and judicial litigation) Complaints answered Total 571 422 4,367 5,444 20 38 26 Management Report August 2020 - December 2022

4.7 Prevention of Money Laundering and Terrorist Financing

In the last three years, the General Directorate of Internal Revenue, in its capacity as supervisory entity in matters of prevention of asset laundering, financing of terrorism and proliferation of weapons of mass destruction (PLAFT), in accordance with Law no. 155-17, has carried out supervisions, all with a risk-based approach, aimed at different sectors of non-financial reporting entities, which has gradually led to compliance with the obligations by reporting entities.

As a result of the supervisions, administrative sanctioning procedures have been initiated against those regulated entities that are not complying with the provisions related to the prevention of money laundering. In the period, format 647 was published for the submission of statistical information for risk analysis that obligated subjects must send quarterly, as well as Annex E for RNC registration forms (RC-01 and RC-02), to be able to identify taxpayers who carry out activities that make them non-financial reporting entities under the supervision of the DGII.

n addition, the DGII has been immersed in the implementation of a Software for the

measurement of risks, which will allow a more Iaccurate measurement of the risks of the obligated subjects under its orbit, interrelating quantitative and qualitative elements of the entities, with variables and essential factors of the PLAFT system, thus ensuring that the supervisions have a specific scope, mainly covering the entities with the highest risks.

In compliance with the commitment that supervisors have in this matter to develop regulations that contain the details of the obligations that obligated subjects must comply with, the DGII has issued general regulations 03-2022, 06-2022 and 07-2022; the first one is focused on the obligation of the obligated subjects to carry out external audits of their PLAFT program and the last two focused on the enforceability of the reliable proof of payment.

For the obligated subjects, the employees of this DGII and the public to become aware of the regulations issued, as well as the entire legal framework established in terms of asset laundering prevention, an intense day of training nationwide.

29

Management Report August 2020 - December 2022

Prevention of Money Laundering and Terrorist Financing Cantidad

4.8 Modification project of Title I of the Tax Code

The current Title I of the Tax Code of the Dominican Republic dates to 1992 and the legal progress and experiences acquired since then make it necessary to implement a new Title I, establishing better provisions that ensure and preserve the rights and obligations of taxpayers and taxpayers. tax, as well as those of the Tax Administration.

In this sense, in March 2022 the Draft Modification of the reform law of Title I of the Tax Code was presented with the objective of updating and introducing improvements to streamline processes and guarantee the rights of taxpayers.

30 Prevention of Money Laundering and Terrorist Financing Quantity (August 2020 – December 2022) 66 Supervisions 8 Fines 3 Published Rules 7,801 Trainings (People)

7,801 Supervisions Fines Published Rules Trainings (People) 8 66 3 Management Report August 2020 - December 2022

Some of the most relevant points that are included in the Modification Project of Title I, are:

• Implementation of the catalog of taxpayer rights in the framework of compliance with their tax and formal obligations.

• The surcharges, which are currently 10% for the first month and an infinite 4%, are proposed to be set at a fixed 3% and cannot exceed the amount of 100% of the tax.

• Establishment of interest in favor of the taxpayer in reimbursement procedures where the delay is due to the administration.

5. Advances in auditing

• Establishment of electronic administration, to streamline the reception and delivery services by the OFV.

• Creation of facilitation instruments and others are improved in the payment as a form of extinction of the tax obligation.

• Improvement of the compensation procedure so that excesses or balances in favor can be compensated with any type of tax.

5.1 Risk-Based Tax Compliance Management Model

One of the great challenges that all Tax Administration faces is the materialization of non-compliance with tax obligations by taxpayers, this accompanied by the erosion of tax revenues because of tax evasion and avoidance whose consequence is the reduction of State income to finance public spending and the implementation of social and economic policies for the development of a country.

Recent figures from the tax system of the Dominican Republic place the level of tax non-compliance at around 40% in the Tax on the Transfer of Industrialized Goods and Services (ITBIS), in the case of Income Tax (ISR) a non-compliance is estimated 60% and 40% for the Selective Taxes on Alcohol and Tobacco. (See Default Estimate in Dom. Rep.).

Due to the foregoing, the tax administration has chosen to implement novel solutions provided with the successful experiences of modern tax administrations such as: Australia, Canada, USA, Chile, Argentina and Brazil, which carry out the task of taxes under a "Risk-Based Tax Compliance Management Model" which is a process that allows obtaining a comprehensive view of the tax system with the objective of increasing compliance with tax obligations, through strengthening the knowledge of the taxpayer and the analysis of the causes that explain their tax behavior in order to design targeted control and treatment actions that allow the elimination or mitigation of non-compliance.

This methodology proposes to align the control and treatment actions to the level of tax risk that the taxpayer represents.

31

August

December

Management Report

2020 -

2022

Nivel de Riesgo Tributario

Mecanismos de trazabilidad

Revisiones riesgos oficina

Revisiones riesgos distancia

Atenciones telefónicas

Correos personalizados

Reporte de brechas personales

Apps: Calculadoras y asistentes

Guías meotodológicas

Auditorías

Clausuras

Infracciones graves

Fiscalización Externa

Fiscalización tecnológica

Revisiones Masivas oficina

Revisiones diferencias certeras a distancia

Control en Terreno

Acuerdos de Cooperación Tributaria

Propuestas pre-llenadas

Mensajes emergentes push-up

Mecanismos automatizados de habilitación de contribuyentes

Campañas de comunucicación segmentada

Acciones de Tratamiento

Fuente: Own elaboration based on the Inter-American Center of Tax Administrations (CIAT) (2019).

The Risk-based Tax Compliance Management Model (MGCT in Spanish) is designed to optimize the allocation of resources to manage tax compliance. Its execution requires decision-making at different levels of management, the strategic and tactical levels. For its part, the operational level, which corresponds to the execution of the treatments, allows feedback on the decisions adopted by the different instances.

The implementation of the MGCT consists of different phases, applied through the Tax Risk Management Process. These phases are: Identification, Analysis, Prioritization and Consolidation, Treatment and Evaluation. On the other hand, as a transversal tool for all stages of the model, the Global Risk Classification (CRG) is constructed, one of the main inputs for the analysis and assignment of risk-based treatments.

32

Figura 1: del Contribuyente

Management

Report August 2020 - December 2022

Those that have been developed during the 2020-2022 period are described below.

• Identification of Specific Risks and Gaps: in this process we proceeded to recognize and describe the tax risks and the associated gaps that may impact the achievement of the objectives of the General Directorate of Internal Taxes (DGII), for which multiple tools and instruments have been worked on that allow the identification and classification of the different risks and breaches, resulting in the development of:

• Compilation of Tax Risks (Global and Specific).

• Compilation of Tax Treatment actions.

• Survey of Tax Gaps that detect non-compliance by Taxpayers.

• Analysis and assessment of Risks and Tax Gaps: includes a characterization of the taxpayers that present the tax obligation under study, the levels of compliance and other characteristics of the objective universe. It also includes the study of the causes of non-compliance and the detection of risky behaviors and/or characteristics of each taxpayer, in addition, the probabilities that a tax non-compliance could materialize, and the consequence or potential monetary loss in collection, the progress achieved in said development are:

• The characterization and valuation of Tax Risks.

• Construction of the Institutional File of Specific Risks.

• Construction of the Institutional Catalog of Tax Treatments.

• Preparation of the Tax Treatment Assignment Policy.

• Global Tax Risk Classification (CRG in Spanish): taxpayers were categorized based on the probability of tax non-compliance and the monetary consequence that said non-compliance represents for the administration.

• High risk: high probability of default and high monetary consequence

• Medium risk: moderate probability of default and moderate or low monetary consequence

• Key risk: moderate or low probability of default and high monetary consequence

• Low risk: low probability of default and low monetary consequence.

• An average of 1,321,979 taxpayers per fiscal period have been classified, covering large, medium and small taxpayers, the result of the classification has allowed us to observe that an average of 74.4% of those classifieds are low risk, 21.7% medium risk, 2.5 % key risk and 1.4% high risk.

Management Report August 2020 - December 2022

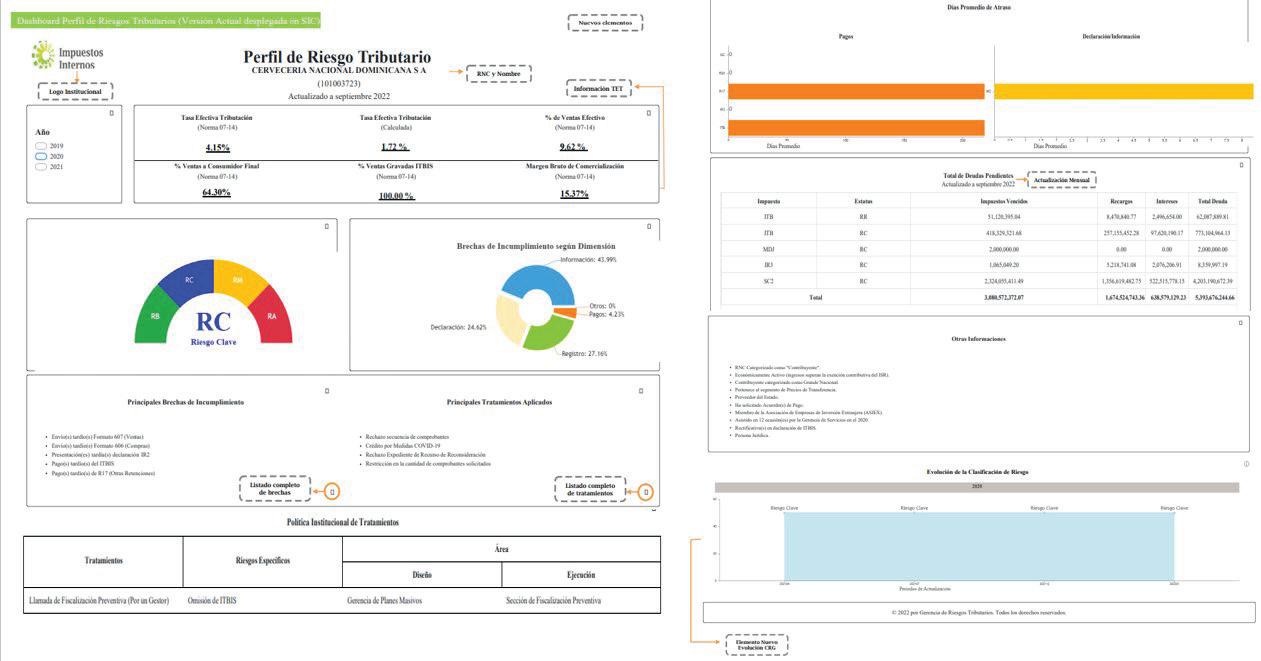

• Tax Risk Profile Dashboard of the (SIC): A tool for internal use was developed where tax officials can consult the risk classification of taxpayers, as well as the main factors of tax non-compliance that explain their risk profile; as well as the treatments applied to them.

34 19,750 18,418 24,401 2020 2021 2022 Riesgo Alto 297,966 333,999 348,670 2020 2021 2022 Riesgo Medio 31,499 42,246 27,228 2020 2021 2022 Riesgo Clave 955,649 972,640 1,007,846 2020 2021 2022 Riesgo Bajo Probabilidad Incumplimiento Consecuencia Monetaria

Figure 2: Number of Taxpayers Classified by Year by Type of Risk (2020-2022)

Management Report August 2020 - December 2022

Figure 3: SIC Tax Risk Profile Screen

• Catalog of Tax Obligations: an instrument was prepared that compiles all the tax obligations that a taxpayer must comply with in relation to the formal duties (registration, information, declaration and payment) defined in the legal and regulatory framework of the tax administration.

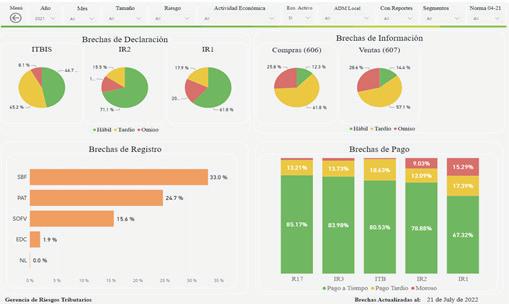

• Map of Gaps in Tax Obligations: an interactive monitor (instrument) was designed and developed that shows indicators of tax non-compliance according to the formal duty of the taxpayer (registration, information, declaration and payment) in said instrument it can determine the percentage of taxpayers that comply their obligations on date, out of date and even those who have not complied with them.

• Identification of Economically Active Taxpayers: Taxpayers who represent a tax interest for the tax administration were identified, thus developing the economically active brand whose scope is all natural or legal persons that carry out an economic activity that incurs in the generation of a tax obligation. and their amounts or annual income exceed the tax exemption (RD$416,220.00) stipulated in the regulatory framework.

• Systematization and automation of the Process of Prioritization and Consolidation of Risks and Tax Gaps: It is a tool that allows receiving, processing and analyzing the information sent by the analysis areas on the risks and non-compliances identified for each taxpayer, for the execution of the Prioritization Process and Consolidation. This continuous process is being developed through database management and exploitation systems, such as SQL Server, RStudio, among others.

35

Figure 4: Dashboard Tax Gap Map

Management Report August 2020 - December 2022

• Consulting on the prioritization process (P and C): The objective of this consultancy is to strengthen the new risk-based tax compliance management model, in relation to the process of prioritization and consolidation of tax risks. Among the main purposes of this consultancy is to understand how to effectively and efficiently allocate resources for compliance management, it being necessary for the process to take measurements of the effectiveness of their execution cost treatments and execution capacities, as well as having risk and gap assessments that are comparable to each other, to have good approximations to the potential benefits that would be derived from the management.

• Policy Proposal for Risk-Based Tax Compliance Management: The purpose of creating this document is to establish the guidelines that will govern the Tax Compliance Management Model (MGCT)

within the institution's internal policies and procedures. This model seeks to achieve greater compliance with tax obligations through a comprehensive and efficient system, as well as establishing the general guidelines as stipulated in the 2020-2024 Institutional Strategic Plan.

• Pilot for the implementation of the Tax Compliance Model based on Risks: Dispatch to the Local Administration of Higüey of a list of taxpayers with their respective tax non-compliances, extracted through the process of Prioritization and Consolidation of to be treated.

• Treatment Action Consolidation Report: This report contains a statistical analysis of a structured process in which the different treatment actions are consolidated: corrective, preventive and facilitation carried out by the tax administration. This report contains the following topics:

36

Acciones de tratamientos y cantidad de RNC’s 01 Acciones de tratamiento según clasificación de riesgo global 02

de tratamientos según estatus de económicamente activo 03

de tratamientos

Management Report August 2020 - December 2022

Figure 5: Dashboard Treatment Actions

Acciones

Acciones

según Administración Local 04

Management Report August 2020 - December 2022

The latest statistics on tax treatment actions generated from September to November 2022 are shown below.

Figura 6: Dashboard Treatment Actions

124,731 Registros únicos tratados.

79,124 Acciones de tratamientos aplicadas e identificadas.

98.97% Acciones correctivas; 1.03% Acciones de facilidades.

de acciones y contribuyentes septiembre-noviembre 2022

Source: prepared by the Tax Risk Management with information from the transactional areas.

• Authorization of the Transferable Tax Credit (refund) of the Cinematographic Activities Companies: Within the framework of the improvement of the internal processes of the business areas of the institution, the Tax Risk Management together with the Special Regimes Management developed an Application of Simplified Review, to respond in less time to the requests for approval of the "Transferable Tax Credit Certificate" and with it, the return of the balances generated.

Broadly speaking, the application allows (1) to unify the information from different sources, (2) to build a history of the film productions evaluated, (3) to identify the means of

payment and invoices that have a higher level of risk. The main achievements have been:

• The automation of the information sent by the companies belonging to this Special Regime.

• The Implementation of a methodology that allows to classify based on risk the means of payment and invoices sent by the companies covered by the regime.

• The simplification of the review and audit processes of the films sent by the companies. The time was reduced from 60 days (audit and response) to 25 days, on average.

2 This request must be previously evaluated by the Directorate General of Cinema (DGCINE).

“Article 39. Transferable Tax Credit. Individuals or legal entities that produce Dominican or foreign cinematographic and audiovisual works in Dominican territory may choose to benefit from a tax credit equivalent to twenty-five (25%) of all expenses incurred in the Dominican Republic. Said credit may be used to offset any Income Tax obligation or may be transferred in favor of any natural or legal person for the same purposes.

2

37

Distribución Contribuyentes según Perfial de Riesgo Global septiembre-noviembre 2022 sep. 2022 24.19% 36.34% 21.71% 17.77% 23.82% 38.46% 18.36% 18.36% 16.12% 57.58% 11.73% 14.56% oct. 2022 nov. 2022 sep. 2022 oct. 2022 nov. 2022

89,651 52,382 72,434 44,922 109,869 85,682 Cantidad de Acciones Cantidad de Contribuyentes

Cantidad

Pefil de Riesgo Riesgo bajo Riesgo Clave Riesgo Medio Riesgo Alto

In continuity with the improvement of the processes of the Special Regimes Management, a dynamic board or dashboard was built in Power BI that gathers the most important information of the Fiduciaries and Trusts, to monitor compliance and behavior of this Economic group. This tool connects the main data sources of the institution, allowing its continuous updating and verification, given that these groups have become highly relevant for the country in recent years.

5.2 Development projects

• Construction of the Tax Scoring for Taxpayers through the Virtual Office (OFV): it is a tool that shows taxpayers the assessment of the tax administration regarding tax compliance with tax obligations of formal duties (registration, information, declaration and payment ) said tool will be available to taxpayers through the virtual office.

associated with the commercial relations of taxpayers with suppliers, clients and shareholders categorized as risky (medium risk and high risk), it allows taxpayers to be imputed a probability of additional non-compliance resulting from these relationships.

• Identification of Hidden Taxpayers: it is the group of natural and legal persons that have commercial transactions in the national economic environment and do not have tax obligations before the General Directorate of Internal Taxes (DGII).

• Dissemination for the generation of "Risk-Based Tax Compliance Management Policy": this process consists of disseminating the proposal for the formulation of the policy with the different instances, within which the guidelines that will govern the Compliance Management Model will be established. (MGCT) in the DGII, to achieve greater compliance with tax obligations through a comprehensive and efficient system.

38 Management Report August 2020 - December 2022

2019

The organizational structure of the DGII is adapted

2019

Preparation of the Tax Obligations Gap Map

2020

Survey of resources available in DGII to apply treatments

2020

Incorporation of the CRG in the internal processes of the DGII

2020

Creation of the Tax Risk Management

2019

Construction of the Global Risk Classification (CRG)

2020

Beginning of the Tax Risk identification phase

2020

Construction Catalog of Tax Treatments

2020

Construction and publication of the SIC Risk Profile Dashboard

Tax Compliance Management Model 3 39

3

Figure 7: Progress and Implementation of the Risk-Based Compliance Management Model (MGCT ). Period (2019-2022)

Management Report August 2020 - December 2022

Figure 7: Progress and Implementation of the Risk-Based Compliance Management Model (MGCT ). Period (2019-2022)

2020

Taxpayer debt management pilot based on the CRG

2020

Incorporation of the MGCT in the 2021-2024 Strategic Plan

2021

Inspection considering risk profile (Key and High)

2021

Compilation report of tax treatment actions

2021

Projects with the Management of Special Regimes (Cinema and Trust)

Analysis of segments of interest for the Tax Administration

2020

Methodological creation for the valuation of specific risks

2021

MGCT 2021 socialization workshops

2021

Incorporation of compliance goals for Economically Active

2021

The consultancies for the implementation of the MGCT begin

2021

Tax Compliance Management Model 4 4 40

Management Report August 2020 - December 2022

Figure 7: Progress and Implementation of the Risk-Based Compliance Management Model (MGCT ).

Calculation of tax scoring by taxpayer

IT requirement update for Scoring development

Incorporation of new elements to the risk profile dashboard published in the SIC

Closing of the consultancy of the Prioritization and Consolidation Process

2022

Development of processes and tools for the Prioritization and Consolidation Process

Implementation of the MGCT pilot in the local administration of Higüey

2022

Preparation of tax risk certifications for the legal department

2022 2022 2022

Preparation of the institutional policy Tax Risk Management

Global Risk Rating (CRG) Update 2022

2022 2022 2022 2022

Tax Compliance Management Model 5

5 41 Management Report August 2020 - December 2022

Period (2019-2022)

6. Management and Compliance Advances

6.1 Post COVID Facilities

To mitigate the effects caused by the pandemic, the DGII implemented tax measures aimed at broad-based tax relief to protect the most fragile and emerging sectors.

Among the specific fiscal measures taken were:

Post COVID Facilities

Facility Tax

Simplified Tax Regime

ITBIS

Income tax

Income Tax (advances)

Income Tax (advances)

Extensions for the declaration

Payment agreements and extensions for declaration presentation

DIOR presentation extension

Period

May-AprilJune 2020

2020

Exemption from payment of the first advance 2019

Exemption from payment of advances

Other withholdings and Income Tax Contributions Payment agreements and extensions for declaration presentation

Asset Tax

Income tax

Income tax

Income Tax (advances)

Likewise, in general terms, the following measures were approved:

Exemption of the first installment for micro and small taxpayers

Extension in presentation and payment

Extension of the deadline for filing and payment

Exemption from the payment of ISR advances to legal persons and sole proprietor businesses

March 2020

April 2020

March 2020

June 2020

June 2020

• ITBIS rectifications through virtual office, periods 2019-2020.

• Digitization of the process of requests for exemption from ITBIS and Selective Consumption Tax (ISC) of taxpayers under special regimes.

• Exemption from the validity of the ITBIS exemption card for companies in free zones.

• ISR deductions for complementary contributions from employers to the Employee Solidarity Assistance Fund (FASE).

42 Management Report August 2020 - December 2022

• Deferral of 30 days for the submission of submission formats and presentations of the monthly sworn statements.

• Remission and presentation of contributions made to suspended employees.

• Extension of the temporary suspension of ITBIS in the transfer of medical materials and equipment from the local market.

• Automation of services through the Virtual Office (OFV), to remotely manage services and procedures.

6.2 Application Law 46-20