8 minute read

PL LINES

ALIMENTARI NON-FOOD

CARREFOUR IL MERCATO (FRESH VEGETABLES)

CARREFOUR CLASSIC (DAILY-CARE PRODUCTS)

CARREFOUR ESSENTIAL (HOMECARE)

CARREFOUR EXPERT (HOME CLEANING)

CARREFOUR EXTRA (QUALITY INGREDIENTS) TEX (SUSTAINABLE FASHION)

CARREFOUR SENSATION (PRODUCTS FROM THE WORLD)

CARREFOUR HOME (HOME PRODUCTS AND ACCESSORIES)

CARREFOUR ORIGINAL (TRADITIONAL PRODUCTS) MY CARREFOUR BABY (CHILDREN HYGIENE AND CARE)

SIMPL (DAILY AND AFFORDABLE PRODUCTS)

CARREFOUR COMPANINO (PETFOOD)

CARREFOUR ECOPLANET (SUSTAINABLE HOMECARE PRODUCTS)

CARREFOUR NECTAR OF BIO (PERSONAL CARE ORGANIC PRODUCTS)

CARREFOUR BIO CARREFOUR SOFT (DAILY PERSONAL CARE)

FILIERA QUALITÀ CARREFOUR (CONTROLLED FRESH)

TERRE D’ITALIA (TRADITIONAL ITALIAN PRODUCTS)

CARREFOUR SELECTION (GOURMET PRODUCTS)

CARREFOUR NO LACTOSE

CARREFOUR NO GLUTEN

Your relationship with suppliers: what’s the average duration?

Carrefour has a long-lasting relationship, also of 20-30 years, with different suppliers, among which, for example, those of Terre d’Italia, Carrefour bio and Filiera Qualità. Precisely this year, it’s our 20th anniversary with Filiera qaulità and with other companies, which have been with us since the very first day.

Are there any tensions due to macro-economical factors?

In difficult moments, like the one we’ve been living in for several months now, characterized by inflation and price increase - it’s essential, for us, to act responsibly. Not just with our consumers, but also with all the Italian producers we collaborate with, to find common solutions to mitigate the consequences of this situation. In the current scenario of an overall price increase we, distributors, don’t have big margins to counteract it. For this reason, the objective is to do our job, by optimizing the system, where possible, to limit the impact on consumers and protect their purchasing power. Moreover, we need to make a distinction between suppliers, as some sectors have faced greater problems due to drought, or sharp increases in raw materials. To mention one, the confectionery industry.

Any solutions?

In 2021 we launched an initiative with more than 80 of Carrefour product suppliers, to reduce end-to-end costs, for example by perfecting logistic flows and limiting the use of plastic. The project represented a great example of collaboration with partners, with whom we collaborated for greater sustainability and efficiency. l

Inflation is rising and ITALIANS have their shopping cart more and more filled with PL PRODUCTS

Consumers prefer private label products, excellent performances also for the Fresch and Pet Care categories. An insight into the data of XIX Marca Report by BolognaFiere presented by Iri.

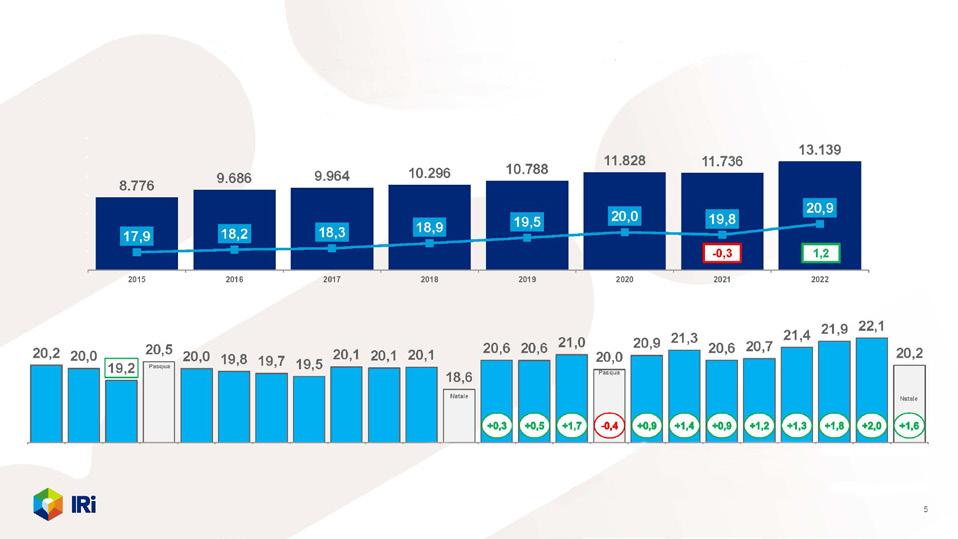

While the shopping cart of Italians in 2022 had to face a very high inflation and the cut on promotions applied by the large-scale distribution chains, PLs continue to grow. In fact, PLs prove to be consumers’ favorite in such a period of crisis where the world has been disrupted first by the pandemic and then by the war and the consequent inflation. The picture of PL’s 2022 essential role can be found in the XIX Marca Report carried out by IRI-Information Resources, and presented on January 18 at BolognaFiere during the 19th edition of the exhibition. Considering all the channels, the most important datum of the Report is that, after 2021, which was characterized by a PL contraction, 2022 ended with a positive trend and a total turnover of 13.1 billion euros (+12%) and a 20.9% share, +1.2% more than the previous year.

The PL Share is growing, supported by the turnover and volume increase

PL LCC - Channel performance - 2022 share

The year 2022 seems to have reversed any paradigm previously observed. Inflation, for example, which in 2021 showed a decrease (- 0.7%), last year accounted for +7.9% with a remarkable upswing in the last months of the year. December 2022 ended with a double digit inflation in packaged FMCG (+14.1%). Speaking of reversed trends, this strong price increase has two other consequences: reversal of promotion and volume trends.

In 2022, PLs goes back to gaining market share, on the upswing in particular in the second half of the year

PL LCC - Turnover in million€ and PL Value Share - Years 2015-2022

After a slight increase in the promotional pressure observed in 2021, 2022 ended with promotions accounting for 22.5% of sales (-2.3 percentage points compared to the previous year and -3.9 points compared to the period before Covid-19 pandemic). Finally, volumes, after a positive sales trend in the last 3 years, saw a negative trend in 2022, recording a contraction of 0.3%. In this difficult context, PLs continue to grow substantially, recording a 2.9% trend in volume, despite the major impact of inflation. This is a cross-channel growth, encompassing hypermarkets, supermarkets, mini-marts and discounters.

The novelty that has conquered Italy, now storable at room temperature!

Fresh, ready in 5 minutes!

Hand made

With mother yeast

Preservative free Cooked on stone

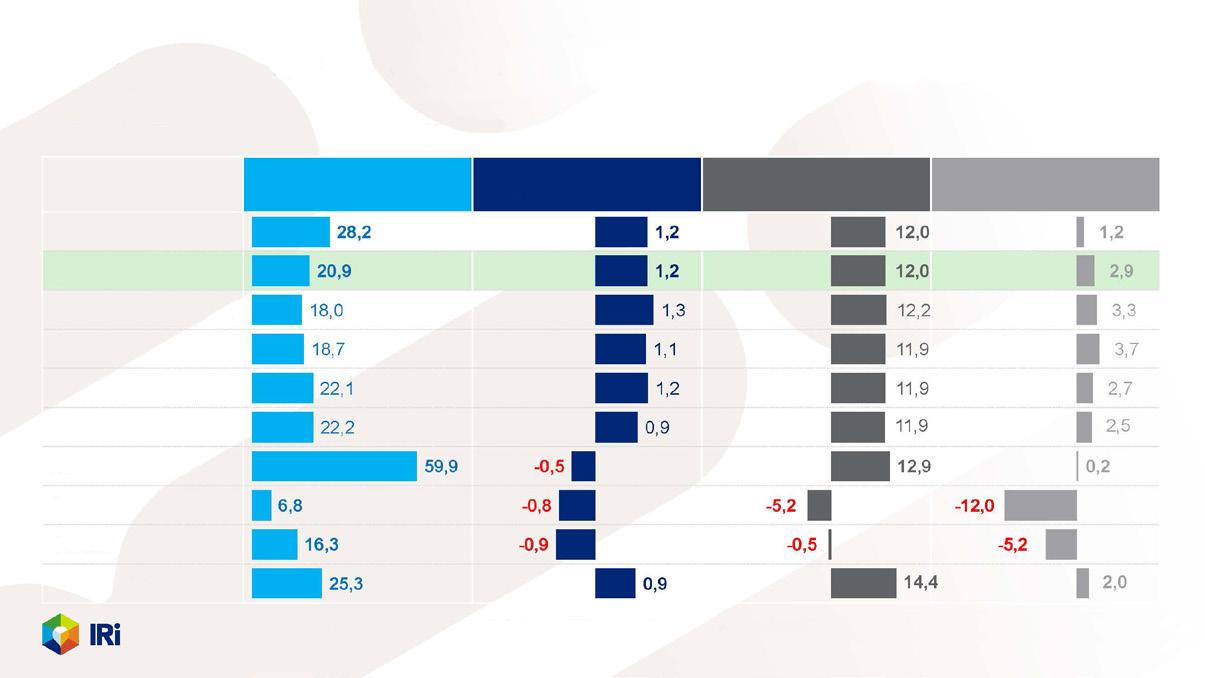

Looking at the PL market product, the competitive positioning of all product sections, especially in the Fresh and Pet care categories, has improved. Not only has a growth in value been recorded, but also a strong increase in volume (Fresh +5.7% and Pet Care +5.9%).

The growth of PLs goes hand in hand with that of the supply, reaching an assortment share of 15.5%, +0.5 point. This supply, despite the inflation, had positive performances/trends in 2022 in its specialized lines and high-added value: the Premium segment recorded +8.9% in value and +2.3% in volume, while the Functional line +14.2% in value and 6.6% in volume. As for the Organic segment, it has slowed down: in fact, despite its increase in volume (+3.9%), it’s the only negative figure recorded in volume (-1.6%).

High-range lines are constantly dynamic, with the exception of Organic/Eco. First-price grows, but the Mainstream continues to be determinant

The mainstream segment, the most important for PL accounting for 76% of the total turnover, drives growth: 9.8 points out of 12 of the PL trend, in fact, come from these products. As in the market, PL prices skyrocketed: on average, in 2022, the inflation on PL products was 9.2% with the Store Brand reaching 9.8%. In other words, being relatively affordable is the main growth factor for PLs. Despite the high rate of inflation, the ‘affordability positioning’ together with the quality of products, let the volume grow. The introduction of new products also continues to generate growth, as do both the segmentation of supply and the constant expansion of PL assortments and, consequently, their share on the shelf. l

IT’S NOW MARTINA BOROMELLO, MARKETING AND COMMUNICATION DIRECTOR AT ORTOROMI WITH PL MAGAZINE .

OrtoRomi, vegetables climbing to the top of PLs

Mixed salads and baby salad, bagged iceberg lettuce, endive or escarole, mushrooms or vegetables ready to be cooked: these are the specialties of a company that get great satisfaction from working for PLs.

by Maria Teresa Giannini

Set up in 1996, in Veneto, from the experience of the two co-founders, the farmers Elio Pelosin and Rino Bovo, OrtoRomi originally sold I range products, and started to invest in the IV range products in 1999. In 2006, the company turned into a Cooperative and it now has 10 shareholders (9 farms and the Co.Ve.Ca.A. cooperative), as well as 40 farms throughout Italy providing it with their own raw materials. Mixed salads and baby salads, bagged iceberg lettuce, endive or escarole, mushrooms or vegetables, ready to be cooked such as spinach, savoy cabbage, chard and kale: these are the specialties of OrtoRomi, which boasts two plants one in Borgoricco (Padua) - fully automatized in 2013 - and the other in Bellizzi (Salerno). The company ended 2022 with a turnover of almost 120 million euros with 37,000 tons of production in volumes, confirming its great national position among other competitors and it had great satisfactions also working for private labels, as Martina Boromello, Marketing and Communication Manager at OrtoRomi.

According to Nielsen, you rank third among the IV range suppliers. However, as suppliers of PLs, what’s your positioning?

That's right, as a branded industry our 4% market share places us in third spot after Bonduelle and private labels, put together, which hold the largest share (over 60%). On the other hand, if you look at the industry itself, our share, as far as the sector we operate in is concerned, is far greater and is about 14%.

Over your total turnover, what’s the percentage of contract manufacturing?

In 2022, 118 million euros, 58%, so most of it, comes from contract manufacturing.

What are the benefits of being PL suppliers? And what are the advantages you provide?

As PL suppliers, we get the chance to strengthen the relationship we’ve built over the years with large-scale distribution and to prove every day the effort and the quality of our job. As partners of distributors for several years now, we have been able to grow together and improve, stimulating each other. Plus, we can offer expertise and innovation, which are reflected in our products and professionalism.

What Italian and foreign brands do you, as PLs, supply?

As far as the Italy is concerned, we are PL suppliers for all the major national brands, such as Conad, Coop, MD, Crai, Gruppo Selex, Prix and IN’s market (Pam Group), but also for those international ones like Carrefour, Despar, Penny, Eurospin. On the other hand, abroad, we supply Lidl and Erisprin Croatia.

Your collaborations with the brands are so successful that on May 31, 2022, one of your PL products was awarded in Amsterdam, during the event of the pre-tradeshow of PLMA...

We were awarded with one of the International Salute to Excellence Awards for the ‘Apulian Soup’, which we produce for Lettere dall’Italia by MD. It is a tasty fresh soup, with no glutamate nor preservatives, that you only need to warm up before tasting. The soup has all the typical Apulian flavors, since it’s made of regional high quality ingredients: - turnip tops, peas, onion, extra-virgin olive oil, pepper. Salute to Excellence Awards prizes innovation and quality in food, non-food and wine industries. During the last edition, they especially rewarded sustainability, from product to packaging. In fact, the great value of our product comes from its affordability, taste and packaging: the latter, in particular, made the product get the highest score in the category, which makes us very proud.

According to your experience, do you think supplier-brand relationship is important only within the company (working rules, quality standards, business rules) or is it something that also customers perceive and which drives their choice?

We’re positive that the relationship between OrtoRomi and large-scale distribution is essential not just for B2B, among industry professionals, but that it is also something the end consumer is able to feel. This is because, when consumers are loyal to the brand, they trust the choices the brand makes.

According to Ipsos data, the majority of Italians that regularly buy PLs are willing to spend more for certified foods: what are the certifications you have obtained so far?

Certifications, for us, are synonymous with freshness and quality in terms of products, but also of safety in terms of industrial process, which undergoes many voluntary audits: in the first case, we can mention the Ifs and Brc certification, for the second one, Global G.a.p. and the adoption of Uni En Iso 11233 and Dtp021 standards.

What’s cooking for 2023, in terms of PL innovation?

For 2023, the goal is to continue to grow as partners and co-packers, together. In this particular historical period, we want to face first those difficulties linked to the price increase and the drop of the purchasing power of families, with constructive dialogue and a bi-directional exchange. The idea is to start from constructive dialogue and bidirectional exchange to move towards a proactive approach and, consequently, the possibility to leverage our know-how of the industry.l