New Gaia Funds Accelerate Ethical Opportunities Exclusive Interview with Dr Hendrik Snyman, CIO of Gaia Fund Managers Hollard Mozambique | Rand Mutual Assurance | Standard Lesotho Bank | Marsh Africa ALSO IN THIS ISSUE:

Unica Iron and Steel is a �rst of it ’s k ind, fully integrated mini steel plant, manufacturing light and medium structural steel from iron scrap. Established in Babelegi 2006, the company has garnered a reputation for manufacturing quality light structural sections (window sections, square bar and angle iron) commercially.

The company boasts a new state of the ar t straight line rolling mill which allows it to produce bigger sections. Unica also has achieved I S O 17025 accreditation for its world class in-house laborator y featuring sophisticated equipment for accurate testing ,which enables Unica to issue the 3.1 cer ti�cate to its customers.

Having established itself as a leader in the local South African market for its sections, Unica is ready to open doors for rest of Africa.

ISO 9001:2015, ISO 14001:2015, ISO 45001: 2018 accredited

012 719 9736| info@unica.co.za

9th Street Erf 87, Babelegi, Pretoria, South Africa

EDITOR Joe Forshaw joe@finance-focus.net

SENIOR PROJECT MANAGER Sam Hendricks sam@finance-focus.net

SENIOR PROJECT MANAGER James Davey jamesd@finance-focus.net

PROJECT MANAGER Ekwa Bikaka ekwa@finance-focus.net

PROJECT MANAGER Eleanor Sarbutt-King eleanor@finance-focus.net

PROJECT MANAGER Jamie Waters jamie@finance-focus.net

LEAD DESIGNER Aaron Protheroe aaron@finance-focus.net

FINANCE MANAGER Isabel Murphy isabel@finance-focus.net

CONTRIBUTOR Manelesi Dumasi

CONTRIBUTOR Timothy Reeder

CONTRIBUTOR Benjamin Southwold

CONTRIBUTOR William Denstone

Finance Focus is written and produced by a team of journalists with a collective experience of over 35 years in business to business journalism. Every month we bring stories, from across the industry, of companies striving to make a positive difference to the sectors they serve, be it through innovative cutting edge technology, entrepreneurial individuals influencing the industrial landscape, ground breaking projects and developments as well as many other inspirational pieces.

The media world is evolving rapidly, technology is helping to connect people and business in an instant. We embrace this and invest heavily in our distribution channels to ensure that the publication is easy to read through a digital circulation which is accessible at your desk or on your travels through smartphone and tablet compatibility. Whilst being at the forefront of the digital push, we also retain a superb quality print run to deliver a traditional hard copy magazine every month.

Our award winning editorial and design teams work tirelessly to produce the best content in the most well designed publication of its type, helping businesses of any size and stature to deliver news, and grow brands.

Our readership is made up of business professionals across every finance industry sector in Europe, the Middle East and Africa. Typically decision makers such as CEO’s, directors, and senior managers read the publication regularly and with a subscriber base of over 110,000 individuals the coverage that Finance Focus offers is perfect for any business with a story to tell or a product to promote.

Get in touch and tell us more about your company’s circular endeavours. We’re online at LinkedIn.

Published by Chris Bolderstone – General Manager E. chris@cmb-multimedia.co.ukFuel Studios, Kiln House, Pottergate, Norwich NR2 1DX +44 (0) 1603 855 161 www.cmb-media.co.uk

CMB Media Group does not accept responsibility for omissions or errors. The points of view expressed in articles by attributing writers and/or in advertisements included in this magazine do not necessarily represent those of the publisher. Whilst every effort is made to ensure the accuracy of the information contained within this magazine, no legal responsibility will be accepted by the publishers for loss arising from use of information published. All rights reserved. No part of this publication may be reproduced or stored in a retrievable system or transmitted in any form or by any means without the prior written consent of the publisher.

© CMB Media Group Ltd 2022

Dr Hendrik Snyman, Chief Investment Officer of Gaia Fund Managers

Dr Hendrik Snyman, Chief Investment Officer of Gaia Fund Managers

PRODUCTION: James Davey

Diversified infrastructure investment company, Gaia, is busy raising funds for important African opportunities. CIO Dr Hendrik Snyman is confident about the company’s outlook following a period of positivity, listing a new fund that is set to democratise internet access in South Africa.

GAIA

GAIA

Changing public attitude, increased demand from investors, and a firm realisation of growth opportunities have seen Environmental, Social, and Governance (ESG) issues climb the priority list for asset managers.

There is an expectation from PwC that ESG and non-ESG products will quickly converge and more than three quarters of institutional investors in Europe will veer away from non-ESG products completely by 2025.

The mantra behind this shift is that people now want to know that their money is being used to do good, with purpose and profit aligned, rather than mutually exclusive.

The practice of ESG investing goes back to the 1960s where some investors excluded stocks from their

portfolio based on negative views around business activity, including tobacco production or any involvement in the apartheid regime. Socially responsible investment, as it was then, was re-labelled as ESG in 2005 and accelerated in 2012/13 when studies were published linking ESG strategy to strong financial performance.

Gaia Group - specialist South African asset manager with a strict focus on infrastructure and agriculture investments – has been concentrated on creating value through positive investment since its formation 10 years ago.

Last year, Chief Investment Officer, Dr Hendrik Snyman told Finance Focus that the company was growing

by targeting climate infrastructure with renewable energy projects. A thorough understanding of engineering processes, industrial development, and project financing allows Gaia to maximise investment options through the project lifecycle.

Now, the company is busy raising funds to put to work in renewable, communication infrastructure, and climate action projects. It’s an exciting time, and Snyman is buoyant about opportunities in South Africa.

“Company-wise, we’re doing well,” he smiles. “The war in Ukraine and the prevalent power outages we face in South Africa are real concerns, but we are certainly still realising significant opportunities.”

After starting out in renewable energy, the company achieved

success, becoming known for its Gaia Renewables 1 fund, listed on the Cape Town Stock Exchange, which holds an economic interest in the Tsitsikamma Community Wind Farm near Humansdorp in the Eastern Cape. More recently, Gaia broadened its scope to include telecoms infrastructure through its Fibonacci Fibre fund, again listed in Cape Town. Here, a new structure was formulated to provide investors with tax efficiency.

“Unlike developed markets, South Africa did not have a broad ADSL rollout and it’s only the very highincome areas that have access. Mobile data is extremely expensive because of the monopoly that the large telcos have. When fibre was launched, it was so much faster than ADSL and it is now cheaper than broadband mobile data,” details Snyman.

Last year, Gaia made its first

investment into fibre to the home networks, buying up 54 fibre network sites diversified across Gauteng, KwaZulu-Natal and the Western Cape as a result of the first round of funding.

“The ISP has to pay a strong

percentage to the fibre network owner,” he explains, adding that a different, economical arrangement was more suitable than a traditional listing as asset managers are not interested in buying entire fibre networks, especially

look at what was the most efficient and effective way to allow asset managers exposure to this asset class.

“We provide the most effective and appropriate ways for our clients to invest into these networks. After reviewing the UK and USA, we decided that Real Estate Investment Trust (REIT) as a vehicle is the most appropriate way to do so. It is tax efficient and allows for gearing.

structure and legislation. It took us a while to understand the tax implications as it hasn’t been done in Africa. We have had tremendous interest in the sector. It is a great thing to do for the country in terms of impact, democratising access to internet rather than it being very expensive through mobile data.”

those needing to build a new site or those with no potential buyer.

“We invested into that through a private mandate and we started to

“We listed Africa’s first REIT in December last year. Our first tranche of investments was R120 million which we deployed by March 22. We deployed the second tranche of R150 million by the end of October. We are looking forward to deploying a third tranche of R500 million. It’s gaining speed quickly and has been really interesting. We have been figuring out how to make this asset class compliant with the REIT

Fibre rollout is expected to continue at pace in South Africa after the government missed a 2014 target of having a fibre connection at every house in the country by 2020. President Ramaphosa has assured that investment will continue in order to drive economic growth and build Fourth Industrial Revolution capacity.

The strength of the ESG principles is clear to see across Gaia’s major funds,

“IT IS A GREAT THING TO DO FOR THE COUNTRY IN TERMS OF IMPACT, DEMOCRATISING ACCESS TO INTERNET RATHER THAN IT BEING VERY EXPENSIVE THROUGH MOBILE DATA”

and the focus is unending, with the company providing funding that makes a real difference to the lives of people and communities in South Africa. Part of the Gaia investment proposition is

delivery of a solution that encompasses ‘positive, sustainable impact on Africa and its people’.

Currently, coal is by far the largest contributor to South Africa’s energy mix. Oil, natural gas, and nuclear are smaller provisions, and renewables make up a trivial percentage. The opportunity is enormous, and transparent funds are vital in ongoing development.

“It doesn’t matter what the UK and US are doing to stave off climate disaster – if Africa, 17% of the world’s population – decides to energise using fossil fuels, then you have trouble,” insists Snyman. “We are saying that the focus should be on Africa, with an effective eco-system working together where a developer knows that they can sell.”

His proposal is that those planning, developing, and operating renewable energy assets must be able to sell at the

right stage, and price, to ensure capital is reused and new projects can thrive.

“That secondary market in Africa is in its infancy and our fund concept is $200 million where we can buy interests in projects that have been developed so those developers can recycle their capital into new greenfield projects. That will start a snowball effect, with a vibrant ecosystem of people developing and funding projects, transferring skills, and selling projects.”

Efficiency and localisation in capital and project development cycle is essential he says.

“If you’re putting money into a greenfield project, you have to know who you are going to sell it to when it is operational, otherwise you have uncertainty and that is a real hurdle. There is a lot of focus on greenfield projects and everyone says we need to

We have partnered with leading manufacturers from across the globe to oer

We can help. Energy DC Power Systems Telecommunications Network Optimization Specialized Services

Key competencies in Design Development Local Manufacturing

Innovative Fibre & Energy Management Solutions

world class solutions

“WE ARE SAYING THAT THE FOCUS SHOULD BE ON AFRICA, WITH AN EFFECTIVE ECOSYSTEM WORKING TOGETHER WHERE A DEVELOPER KNOWS THAT THEY CAN SELL”

build more renewable energy plants in Africa, and that is obvious with 17% of the world’s population here but only 2% of the world’s infrastructure and renewable energy spending.

“Ghanaians should be running Ghanaian projects. They have a better understanding of risk in the country, and they need to know how to develop projects when the need arises in the future. A vibrant secondary market signals demand for projects and that draws people in to develop greenfield projects.”

At the end of 2021, Gaia entered the International Climate Finance Accelerator (ICFA) programme in Luxembourg. A unique two-year programme that accelerates emerging fund managers focusing on key areas within climate action, Gaia was

selected alongside four others – the only African organisation - to support brownfield clean energy projects to catalyse the development cycle and crowd in more actors at all stages of the development ecosystem, thereby providing widespread access to clean energy to fuel a vibrant and sustainable growing African economy.

In sub-Saharan Africa, access to electricity is required to rise above poverty, but around 600 million lack basic access. Just seven countries have populations where more than half are electrified. The result is that many businesses rely on expensive, dirty, unreliable generators to power operations.

“We are taking what we’ve learnt in Luxembourg and we will be expanding that into the commercial and industrial renewable energy space here,” says Snyman. “Where a renewable

energy programme is dependent on government issuing RFPs and a tender process, we ask what is the most effective way for our investors to gain access to renewal energy on rooftops and commercial buildings, or people

“WE THINK THAT ANY INVESTOR, IN ADDITION TO PROFIT, SHOULD CONSIDER THE IMPACT THAT THEIR MONEY IS MAKING. WE DON’T BELIEVE THAT YOU HAVE TO SACRIFICE ONE FOR THE OTHER”

who want to buy directly from big producers. We are busy formalising the structure and will probably list towards the end of 22/early 23.”

Going forward through 2023 and beyond, Snyman and team are keen to further embed ESG principles deep into the company’s culture, prioritising all three elements. Governance specifically is at the heart of discussions right now, following selection at the ICFA where Gaia was able to learn more about European regulations.

“In Europe, there are legislated requirements around reporting on your impact as much as you would on your financial status,” he says. “We have adopted that in its entirety as a good thing. Even though we don’t have to do it, we have decided that Gaia – subject

to SA legislation with the funds we manage – is going to report on impact in line with European legislation. As part of that, we have hired a new Chief Risk and Impact Officer to look at our risk from an environmental, social, governmental, and impact perspective.”

Gaia sees this as a point of difference and something that asset managers will compete on in the future. “It’s positive,” says Snyman “and rather than seeing it as a business hurdle we see it as competitive advantage. We think that any investor, in addition to profit, should consider the impact that their money is making. We don’t believe that you have to sacrifice one for the other. We know you can profit with a purpose.”

Today, ESG investing can accelerate market transformation, and these market-led changes can act as a force

for good, on a large scale. ESG is not just about regulatory compliance – it now incorporates transformation in business strategy, and is often a key enabler in profit maximisation. Gaia will carry on raising funds for the Fibonacci Fibre REIT, and Snyman is confident about the pathway forward.

“We have one large African government employee pension fund that has committed to investing. It’s positive for the country that we have these initiatives during dark times including the war in Ukraine, rising interest rates, stock portfolios being hammered, rolling blackouts – GAIA has a very positive outlook,” he concludes.

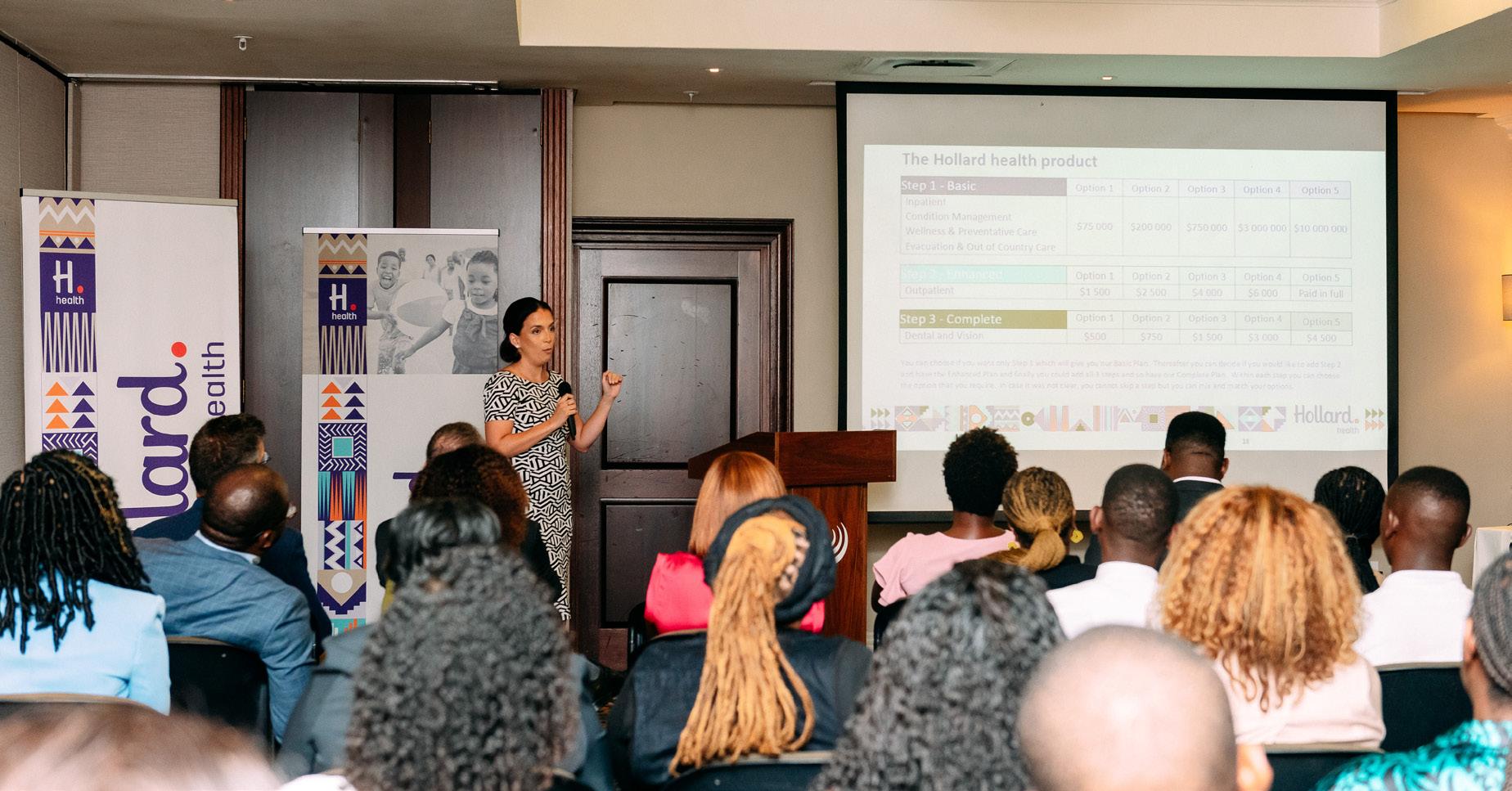

Hollard Mozambique has launched a new health product aimed at providing complete and comprehensive cover for organisations and employees in the country. In a burgeoning market, something special is required to stand out as more look to seize opportunity. Bruna Quintas, Employee Benefits: General Manager and Lee-Ann Dobrescu, Manager: Hollard Health International, tell Finance Focus more about the company’s healthy ambitions.

with Cigna – a multinational managed healthcare and insurance company – providing extensive coverage to employees of some of the country’s biggest corporates. Now, Cigna and Hollard have decided to forge their futures separately in the African Health Insurance market. Hollard has revamped its offering to give clients both protection and freedom of choice. In its never-ending quest to be Mozambique’s favourite insurer, the company is proud of what has been achieved.

“We have grown steadily over the past years and we are now covering 9000 lives. We are number three in Mozambique by Gross Written Premium (GWP),” states Bruna Quintas, Employee Benefits: General Manager.

Perhaps one of the most appealing and potential-packed sectors in Africa today, the health insurance market is rife with opportunity. In 2020, 70% of all premiums were paid in South Africa, leaving the balance of an almost $70 billion spread across 53 other nations. According to McKinsey & Company, ‘steady economic growth in most countries combined with a largely underdeveloped insurance sector have positioned the continent as the second-fastest-growing region for insurance globally after Latin America’.

Even through the Covid pandemic, industry commentators expected the sector to continue on a strong growth trajectory, perhaps slightly delayed rather than totally upended. CAGR of 7% was expected between 2020 and 2025 with Europe, Asia, and North America all facing slower growth.

Some of the big international players are already making moves; acquiring local companies, forming partnerships, and working with local brokers to enter underserved markets. But for Hollard – the largest privatelyowned insurance group in South Africa

– growing on the continent, in complex markets, while solving problems and achieving a purpose, is a long-term plan that requires local knowledge.

In Mozambique, health insurance is nascent with the majority of the population not covered or underinsured. The country itself has weak health infrastructure with many forced to walk for more than an hour to reach the nearest facility. A skills shortage is also prevalent with highly qualified doctors and nurses (mostly expats themselves dealing with expats) centred mainly around Maputo. However, the past two decades have seen vast improvements with treatment for HIV/AIDS much more widely available, and protective measures against malaria – a serious threat in Mozambique – on the rise.

For companies active in Mozambique looking to stand out from the crowd and attract the very best people, against the backdrop of a challenging health environment, Hollard is bringing a new solution. For the past six years, Hollard Mozambique has offered a health product in partnership

“It’s a comprehensive product covering almost every eventuality,” she adds. “We have now structured the product differently and we believe we are bringing something that will meet the needs of clients and members. We have a three-step product structure. Step One is basic, that includes inpatient coverage, condition management, wellness and preventative care, as well as evacuation and out of country assistance. A significant change that we have made here is removing the sublimit for wellness and preventative care, which used to range from $200-$1000. This is in support of our commitment to the well-being of our members and to ensure that they live fully in good health. Here, we have five options starting from $75,000 all the way up to $10 million per member, per year.”

Condition management includes treatment for chronic conditions (as well as cancer, HIV, kidney dialysis, and more). “Unlike many competitors, chronic condition prescriptions do not come out of your outpatient limit,” says Manager: Hollard Health International, Lee-Ann Dobrescu. “Whether you are treated in a hospital or specialist clinic or have monthly medication, that all comes under this first basic step and

the higher option limits offered. We are trying to ensure that we have taken care of the most challenging health events in Step One. Even if you’re just trying to live a healthy lifestyle, if you take Step One, you already have a comprehensive approach to your health and wellbeing.”

Step Two includes outpatient care, and Step Three includes dental and vision. “It is marketed to corporate and commercial clients, and it is only available to employers for the benefit of their employees and their dependents,” says Quintas.

The modular nature of the product allows clients to pick and choose the level of cover they want across the three steps. This allows them to tailor their

benefits to their budget and the specific needs of their employees. By being able to offer international standard cover, employers in the country can attract and retain talent, ensuring their health and wellbeing is completely catered for. With the limited number of healthcare professionals in Mozambique, Hollard will leverage their panel of medical expertise to support the doctors in providing members information on what to expect and how best to manage their condition. Treating people with empathy, care and dignity is what separates a good doctor from others, and what differentiates a favourite insurance company from the pack.

“As Hollard Health, we are committed to this market,” says Dobrescu. “We have made changes to our product based on the feedback we have from our customers. We have made sure we deliver a combination of fabulous digital tools, empowering people to take charge of their health and wellbeing, as well as the important human touch. When big things happen,

real people, with real expertise will guide our members every step of the way. We take care of the details so they can focus on recovery. Our time in health has shown us that it is about way more than paying the bill.”

With clients, mostly recognisable industry leaders, a comprehensive product is required. These multinational corporations must be able to serve staff with an offering they know will protect and provide for in tough circumstances. In Mozambique, where health and education are among the basic services unevenly delivered across the country, a partner that is proven is welcomed. Hollard Mozambique has 20 years of experience, understanding local conditions and building relationships across the fertile country.

“We are looking at employed individuals and we are looking at employers who want to ensure they can attract and retain the most talented individuals,” confirms Dobrescu. “We do particularly well in industries where

“OUR TIME IN HEALTH HAS SHOWN US THAT IT IS ABOUT WAY MORE THAN PAYING THE BILL”

expertise and knowledge are required. Where you have to attract the best skills, you must ensure you are offering a good mix of benefits. This speaks to providing those rich benefits as well as making sure you get access to care outside of Mozambique where required. Because it’s international, if the care is not available locally, we cover the costs of access caring outside of Mozambique. You can also choose to have an area of cover that is wider than just Africa. You might be an expat employee and you want to know that if you are ill, you can return home to be treated by a facility you know and trust. If you regularly commute between another country and Mozambique, you can choose

to be covered in both locations.”

Currently, most European nations including the UK, France, Germany, and Portugal advise on insuring heavily when travelling to Mozambique. But costly travel policies are not suitable for those living and working in the country, looking to safeguard livelihoods and families. Protection must be developed by those who understand the local market, and that is why Hollard Mozambique’s offerings are tried and tested in Mozambique, by Mozambicans.

“Our vision is to be Mozambique’s favourite insurer,” states Quintas. “To grow, we are going to listen to our clients. That is what we have been doing and that is why we have been successful

over the past six years. We have a strong international backing and we have the knowhow to provide quality services, but providing an excellent member experience comes from listening. Where we need to update our benefits, we do so. Where we need to update our services, we do so. Feedback from our clients, broker partners, and our providers – the hospitals, is key to continuously improving our offering,” she says, adding that the company is focussed on a win-win-win mentality.

Already strong in the digital space, doing amazing things across its specialist lines – including agriculture and energy – Hollard Mozambique will not ignore the health space when it comes to digitisation. A new app, designed to encourage members to be healthier, is being launched which could help the company to offer further rewards and lower premiums. Hollard Healthier sees that members are able to obtain multiple health markers through a simple selfie.

“We are giving people information to ensure they can be a little healthier every day and every week,” smiles Dobrescu. “It’s advanced technology where you take a scan of your face using your phone and you can find out your blood pressure, heart rate, risk of stroke, and more, before giving you a personal plan to ensure you become healthier while being rewarded along the way. We want to make sure people feel engaged with their health. Health is the new wealth, and we are committed to helping people live their healthiest lives. Our focus is on ensuring the people of Africa become as healthy as they can be.”

The policy also includes 24/7 access to a doctor through the members Hollard Health App, where they can quickly organise telephone or video consultations delivered by Teladoc. An international partnership,

Continues on page 20

“WE ARE GOING TO LISTEN TO OUR CLIENTS. THAT IS WHAT WE HAVE BEEN DOING AND THAT IS WHY WE HAVE BEEN SUCCESSFUL OVER THE PAST SIX YEARS”Lee-Ann Dobrescu, Manager - Hollard Health International

Continued from page 18

this arrangement is an indicator of the company’s desire to bring global solutions and tailor to local problems, while simultaneously growing.

“We are managing to scale across all of Africa and that makes everything sustainable and our pricing for administration more realistic. Sadly, in Africa, many markets are too small to make sense on their own when it comes to delivering complex administration so we have consolidated and we handle the delivery on the back end from a single platform and that is what makes us more sustainable, across the 12 countries where we offer admitted solutions,” says Dobrescu on plans to roll out their health product to more and more countries across Africa.

“We have learnings which we are taking forward to ensure we have a

sustainable offering. Ensuring that we are profitable in the long term and leveraging our scale across Africa means we will be able to consistently, over many years to come, continuously evolve and find a better way to deliver the best member experience possible.”

Locally, the hope is that more Mozambicans can take up the health product from Hollard. Right now, a premium product in the market, this group health offering should be made available to a wider audience agree Quintas and Dobrescu.

“Currently our clients are multinationals and large corporates. We have a medium-term view to introduce a product that we can offer to SMEs to increase access to health insurance in Mozambique,” says Quintas.

“Over time, in order to secure

our place as Mozambique’s favourite insurer, we need to be a favourite to the full ambit of people who want health insurance,” says Dobrescu.

“We want to service a broader range of consumers in Mozambique using a nice mix of smart technology as well as treating people with care and dignity which aligns with the Hollard purpose. If you can get the balance right between great technology alongside the human touch when people need it, our research shows that is what people really want.”

Competitors in the market are strong with big budgets, but often lacking the local knowledge of Hollard. ‘By Africa, in Africa, for Africa’ is one of the company’s core principles, and this is why it is aware of the need to include maternity care within Step One, and how it knows that psychiatric and psychological care

are more desired than ever before as part of an overall health offering.

“We always use local knowledge to refine and enhance products so that we meet the needs in given markets. We have a great mix of internationalised best practice combined with local knowhow, insight, and relationships,” confirms Dobrescu, a Hollard veteran of more than two decades.

“Hollard is an African company and we are not going anywhere. We are in this market to stay,” she adds. “We are building our business all the time, and we are only going to increase what we do across a range of products and propositions. We are going to build our health proposition to serve a broader range of the community to meet the needs on the ground, learning and growing as we go.”

In 2021, The Financial Sector

Deepening Moçambique (FSDMo) found that 11% of the population was formally insured and 6% was informally insured but coverage was often limited to funeral, personal accident, crop and credit life, with just two providers offering a hospital cash plan. Clearly, like the rest of the continent, there is a wide-open space in the health insurance sector, both for individuals and employee benefits. “Health is the fastest growing insurance product and the largest by premium volume in Mozambique and is therefore high on the priority list for the company,” says Quintas.

Healthcare in Mozambique is at a crossroads. Building on the past 20 years of progress, embracing technology, and adopting new funding models will help the country to grow. But lacking support, infrastructure, and information will result in stagnation. For Hollard Mozambique, where collaboration is key, the wider development of the economy as well as servicing of clients to world-class standards will continue through a mix of innovation and technology, all aimed at providing the best care in Africa.

“We want to be sure we leverage

technology in a way that ensures you get the right access to care. It’s a product you buy and consume from day one and the opportunity with technology is more around the delivery of the care. That is where we see the opportunity going forward,” insists Dobrescu.

“We are in health for the long haul – this is just the beginning of what we are doing in health,” smiles Quintas.

The Deloitte African Insurance Outlook for 22 stated that for the wider continental insurance industry, ‘even though the waters are by no means calm it is clear to see that the industry has reset its course to profitability and growth’. With so much more data available in the health space, a symbiotic relationship is growing between client and insurer. For the likes of Hollard Mozambique, where quality care is the top of their agenda, the fabled win-win-win is now more achievable than ever before.

“HOLLARD IS AN AFRICAN COMPANY AND WE ARE NOT GOING ANYWHERE. WE ARE IN THIS MARKET TO STAY”

Sam Hendricks

Founded in 1894, and with nearly 130 years of know-how, experience, and calibre to draw on, Rand Mutual Assurance (RMA) is a non-profit mutual assurance organisation, owned by its policy holders and overseeing the receipt, adjudication, and administration of workers’ compensation claims. For the organisation, caring for its clients and families is couched in an exhaustive Social Impact Strategy, which continues to benefit those most in need of support and guidance.

PRODUCTION:

PRODUCTION:

“RMA is the warm African sunrise that welcomes warmth, comfort and care to the lives we touch,” sets out the non-profit, mutual assurance organisation owned by its policy holders. “As an organisation that is compassionate and caring, RMA goes the extra mile to ensure that beneficiaries and their families receive the care and compensation they are entitled to when they have sustained either a work-related injury or occupational disease.”

Herein lies the core of RMA’s administration business, in the receipt, adjudication and administration of workers’ compensation claims,

including the payment of medical costs, one-off disability payments and the ongoing payment of pensions in the case of severe disability and death - all according to the Compensation for Occupational Injuries and Diseases Act (COIDA), with principal focuses on the mining and metals sector.

“RMA’s high level of service and quick claims turnaround is underpinned by a market-leading integrated claims management IT

system that allows for paperless adjudication of claims,” it says of a further layer of superior service levels. A wide footprint makes RMA easily accessible to its clients, claimants and other stakeholders, through a head office in Johannesburg and regional walk-in branches in Carletonville, Cape Town, Durban, eMalahleni, Johannesburg, Klerksdorp, Pretoria, Rustenburg and Welkom, as well as satellite offices in Lesotho,

“RMA IS OUR CLIENT’S CONSTANT SOURCE OF WARMTH, COMPASSION AND CARE”© Graeme Williams

Mthatha and Mozambique.

“No matter what a day may bring,” the organisation assures, “RMA is our client’s constant source of warmth, compassion and care when life hands them challenges that seem too hard to face alone.”

Identifying a need to help care for miners who were injured while on duty, RMA was founded in 1894 by three mining companies on the Witwatersrand as a non-profit mutual assurance company, and to this day remains a mutual association whereby policy holders are also shareholders. RMA Life Assurance

Company Limited (RMA Life) was also established in 1990 as a whollyowned subsidiary of RMA, to manage the pension benefits payable to claimants and their beneficiaries.

“Whether clients are injured on duty, ill or pass away and leave family behind, we are here to make life stress-free with a range of policies,” RMA promises. “You are in safe hands with RMA; we are passionate about caring for the lives of our claimants and their families, and embody our brand promise of caring, compassionate, compensation at every level of the organisation.”

An exhaustive array of products come together to represent an

unparalleled helping hand in seeing employees through times of difficulty, whether injured or ill on duty. “With the complete range of occupational insurance products, we can offer you a bespoke group cover policy to meet your company’s needs,” RMA explains. Crime and injury are covered against when commuting, as are group personal accident and injury at work or work-related events.

International COID ensures employees who work outside South Africa can still enjoy workers cover for occupational disability or diseases, and in the worst imaginable circumstances affordable group funeral plans are offered to companies for

the benefit of their employees and provide a lump-sum payment to cover costs related to a funeral.

Value-added products, available to RMA as it operates under both

short- and long-term insurance licences issued by the Financial Services Board (FSB), were pinpointed by Group CFO Kyansambo Vundla last year as housing some of the most lucrative opportunities for growth. “We’ve identified the strategy to ‘build a business of significance’,” she revealed in October. “With a legacy of 127 years behind us, I think we have a trusted brand in the industry, and with a new executive committee to take us forward, it’s an exciting time.”

“RMA lives by its caring and compassionate way,” it sums up. “We see it as a privilege to help communities further their skills;

we enjoy seeing people being educated, reaching for their dreams and achieving their goals. We live to see the joy on people’s faces when they’re empowered and improve their standard of living.

“Lending a helping hand is what warms our hearts.” RMA has invested generously in Enterprise Development (ED), what it sees as a powerful tool in assisting in job creation and addressing poverty.

“The entrepreneurship pillar of RMA’s Social Impact Strategy reflects our sustainable approach to development and collaboration with key stakeholders. Helping entrepreneurs across South Africa will help lead to significant socio-economic growth.”

“RMA IS ON A MISSION TO IMPROVE THE SUCCESS RATES OF ENTERPRISES BY ENCOURAGING STRATEGIC ENTREPRENEURSHIP AND INNOVATION”© Graeme Williams

Most notably, RMA has contributed to South African entrepreneurship development via more than R58 million in funding, made up of an R19.6 million total spend on ED, and R39.3 million investment in Supplier Development (SD), both in 2020. “The intent is to support businesses during their formative years, enabling them to scale, create more jobs and subsequently boost the local economy,” RMA explains.

“Our entrepreneurship projects are divided into Supplier Development Initiatives and Enterprise Development Initiatives, which address the unique needs of each business. In the last few years, over 20 businesses and partners have formed part of these ongoing initiatives and benefited from fruitful entrepreneurship opportunities.”

The funding is made through an enterprise development programme which, over a three-year period, sees RMA cover a large portion of the beneficiaries’ operating and capital expenses. Beneficiaries participate in entrepreneurship programmes and training to eventually become fully independent in terms of operations and finances.

“South Africa has one of the highest failure rates for SMMEs, with five out of seven failing in the first year,” is the stark fact. “RMA is on a mission to improve the success rates of enterprises by encouraging strategic

entrepreneurship and innovation that uplifts their surrounding communities.”

“The support we provide to SMEs in our supply chain enables them to create more jobs, achieve higher revenues and reach sustainable operating levels that are independent of our support. RMA provides support in the form of salaries, office rental, IT equipment, furniture, travel, and other office operating costs.”

Responsible investing represents another key arm of a wide-reaching CSR programme which allows encompasses financial education and inclusion, innovative skills development and diversity and inclusion. “Responsible investing is a broad-based approach that factors in people, society and the environment, and allows RMA to collaborate with a range of medium-sized

businesses in various industries that exhibit major growth,” it delineates, having committed to contributing R125 million over a 10-year period to South African businesses.

“RMA’s Social Impact Strategy is designed to promote economic growth, empower marginalised communities, and alleviate poverty in South Africa. It serves as a definitive plan with measurable outcomes, ensuring that we can make an immediate social impact.”

We provide high quality guarding solutions such as Retail, Residential, Hotel Corporate, Receptions and Close Protection.

“RMA’S SOCIAL IMPACT STRATEGY IS DESIGNED TO PROMOTE ECONOMIC GROWTH, EMPOWER MARGINALISED COMMUNITIES, AND ALLEVIATE POVERTY IN SOUTH AFRICA”

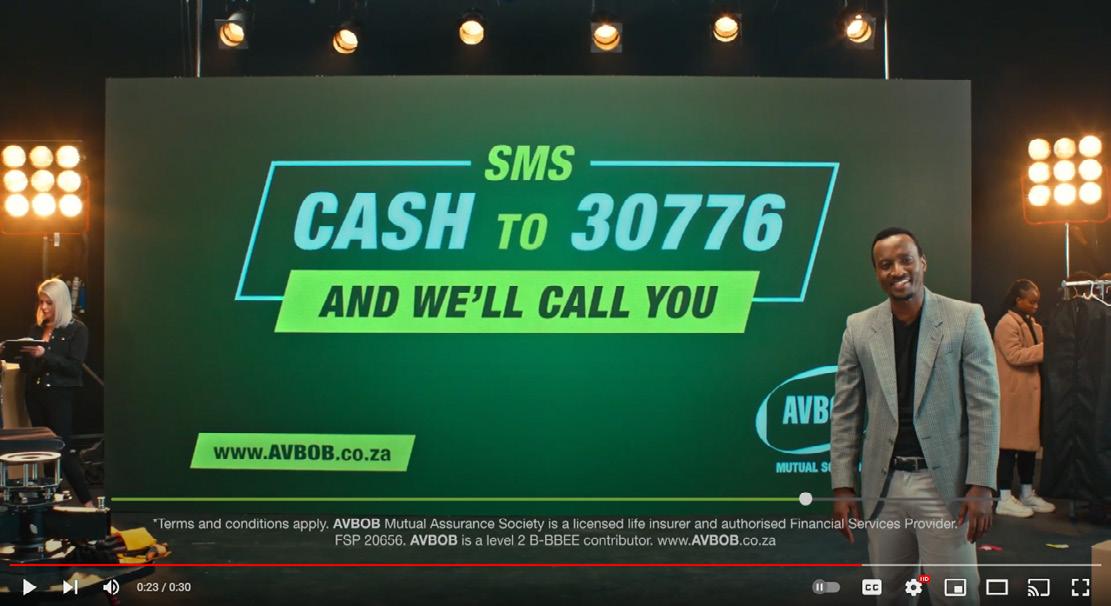

One of South Africa’s best-known and most trusted funeral service providers, AVBOB is the largest Mutual Assurance Society in Africa, and provides specialist funeral insurance and burial services under one roof. “Our business is about people, and whether in life or death, we care for them,” AVBOB declares, as this unique South African proposition looks back with pride on a year of swift adaptation, growth, and success.

PRODUCTION: Eleanor Sarbutt-King

PRODUCTION: Eleanor Sarbutt-King

Established in Bloemfontein in 1918, AVBOB has spent more than a century flourishing into Africa’s largest Mutual Assurance Society, with more than 7,000 staff providing a one-stop funeral insurance and burial service. “We set out to provide our customers with dignity and financial security through our shared value financial model,” AVBOB explains.

“We want to empower our members by providing them with affordable integrated funeral and financial services products and by sharing with them and their communities the value we create,” distilling in just a few words the comprehensive, unique overarching aims of the society.

Partly due to its relative

affordability, funeral cover has a notoriously exceptionally high penetration rate in South Africa, and from the approximately 17

million households in the country currently more than eight million lives are insured by AVBOB.

“AVBOB as a mutual insurance

society is the pacesetter in the funeral industry,” the group states. “Because AVBOB is a mutual, a

family, and family comes first, we place our customers’ interests at the heart of how we do business.”

FAMILY AFFAIR

Being a mutual society means that AVBOB has no external shareholders, instead members receive a share of AVBOB’s surplus profits. “Our members are our policyholdersthe AVBOB family,” it once again stresses. “It is the foundation of our mutuality: to create and share mutual value with our family and be here for all South Africans. Always.

“The defining feature of a mutual society is that it is there for its members

during times of need and everything is done for the benefit of its members.” This was one key element highlighted by CEO Carl van der Reit last year as making AVBOB truly unique. “In South Africa, contrary to the UK or Europe, being a mutual is really rather rare; there are only something like three of us with this status,” he explained.

“There is a significant need for mutual societies such as AVBOB, and our mutual ethos pervades everything that we do. We make regular declarations of profit back to our members, and the model has, in addition, allowed us to offer every person holding a policy with AVBOB a free funeral

“A MUTUAL SOCIETY IS THERE FOR ITS MEMBERS DURING TIMES OF NEED AND EVERYTHING IS DONE FOR THE BENEFIT OF ITS MEMBERS”

through our dedicated division, on top of all the other value for benefits. It is another way for us to be able to return gains to our customers.

“We have created a unique culture of customer centricity that is difficult to replicate elsewhere. Companies that truly stand out from their competitors are those that go the extra mile to offer an exceptional customer experience.”

Across three operating divisions lies a comprehensive range of funeral policies to meet the many and varied needs of the market, backed by a full funeral and cremation service via a network of highly-trained staff and a factory in excess of 14,000m² where an extensive range of coffins, wreaths and fittings is manufactured.

It is tragically inescapable that death, and the associated burial, is a process through which each of us will at some stage have to go through, and in South Africa a high mortality rate together with funerals being so important to the majority of the population mean that a large funeral services industry has been established.

Elaborate burials are still a significant status symbol to many in South Africa, spawning a funeral insurance industry valued at somewhere

between R7.5bn and R10bn. A funeral can be a hugely expensive exercisecan cost anything from R600,000 to R3 million - and as such it is today the most popular insurance cover in South Africa.

GROWTH

AVBOB now has 379 branches nationwide, of which more than 200 are funeral arrangement offices and funeral agencies. Last year alone, this footprint grew by 11 insurance offices, the base from which agents

“OUR IMPACT ON LIVES AND LIVELIHOODS PROVES THE RELEVANCE OF WHAT WE DO AND OUR PURPOSE AND PLACE IN SOCIETY”

provide comprehensive client services to policyholders, and four funeral agencies, which provide the accessible, one-stop funeral care to all of South Africa’s communities.

“Ours is the largest funeral service operation in the country,” van der Reit relayed, adding a further factor to cement AVBOB as a true one-of-akind. “More than simply the biggest, our being an integrated insurance and funeral service operator makes us truly unique in the country. Where other insurers stop at the point of a claim, that’s where our full service kicks in and we take it from there.

“As far as possible, we aim to provide a full-service offering at every AVBOB site.”

The last year was another decked with accolades, as AVBOB was recipient of no fewer than eight of the industry’s most prestigious awards. Thrilled by its selection in October as Best Funeral Provider by Best of Bloemfontein, the Group was then certified as a Top Employer for the fifth consecutive year, perfectly recognising some of the defining AVBOB values.

“We strive for excellence, always looking for ways to improve our systems, processes and products,” the Group stresses, “and our people should be challenged, learn new things, grow and take ownership of the things they do.

“As a key player in the funeral insurance and funeral service industry, we continue to build business strategies that cater for the current

and future needs of customers.”

Not just physical growth, 2021 also saw total assets increase a whopping 23.8% to R35.1 billion. Premium income also rose by more than 10% to R5.7 billion, as total policyholders hit 2.5 million. AVBOB Funeral Service and AVBOB Industries achieved pretaxation profits of R66.4 million and R23.3 million respectively, despite zero price increases for the latter.

“AVBOB entered its 104th year on a strong note on the back of the record performances of the previous year,” van der Reit began his assessment. “In line with industry trends and reflecting the difficult economic times in which our members find themselves, we have endured headwinds in the form of pressure on the persistency levels of our insurance policy book and volatility in investment markets.

In response to these challenges, a number of changes to the business have already been implemented, and it remains exceptionally financially strong and well able to endure the current market turbulence.

“Our mutual status remains the cornerstone of our ethos, our purpose and our competitive differentiation,” he opined, “and being able to offer an integrated funeral insurance product and funeral service also continues to set us apart. Our impact on lives and livelihoods proves the relevance of what we do and our purpose and place in society.”

A consistent partnership builds long-term success.

We’re extremely proud of our partnership with AVBOB and wish them, and their clients, every success in the future.

“OUR MUTUAL STATUS REMAINS THE CORNERSTONE OF OUR ETHOS, OUR PURPOSE AND OUR COMPETITIVE DIFFERENTIATION”

Fo r over 150 years Marsh has grown by helping clients anticipate and meet the needs and challenges of changing times and technologies. In Africa, this has primarily been borne out in specialising in providing clients with the intellectual capital and industry experience to unlock the opportunity in risk. Throughout this long lifetime clients have trusted Marsh to advise them during the most trying and celebratory times, helping them achieve success by becoming more resilient and attaining the possible.

“Our purpose is possibility,” Marsh Africa declares. “At Marsh, the idea of possibility isn’t just something we talk about - it’s something we’ve lived

for over 150 years. With new risks and opportunities constantly emerging, we help clients navigate the changing risk landscape, realise ambitious goals and make their future more secure.”

“We go beyond risk to rewards for our clients, our company, our colleagues, and the communities in which we serve, protecting and promoting possibility and allowing our clients to dream bigger, reach further and plan for the opportunities ahead.”

“Together,” Marsh Africa continues, “we are creating a benchmark of excellence in the risk and insurance industry by harnessing our global and domestic expertise drawing from over 40 years of experience and insight from our continuously expanding operations in the Middle East and Africa.”

Marsh’s staggering number of colleagues worldwide, quickly approaching the 50,000 mark, means

“AT MARSH, THE IDEA OF POSSIBILITY ISN’T JUST SOMETHING WE TALK ABOUT - IT’S SOMETHING WE’VE LIVED FOR OVER 150 YEARS”

that local expertise is always on hand, providing commercial and individual clients with tailored insights, advice and support in the specific markets in which they operate or where their

business may face risks. “We help you understand coverage nuances, regulatory developments and risk trends, and we work together with you on placement, mitigating risk

and optimising your risk spend.”

At the turn of the year, climate risks dominated the list of long-term global concerns as the world entered the third year of the pandemic, while the top shorter-term global concerns included societal divides, livelihood crises and mental health deterioration. Now in its 17th iteration, the World Economic Forum’s

“WE HELP YOU UNDERSTAND COVERAGE NUANCES, REGULATORY DEVELOPMENTS AND RISK TRENDS”

Global Risks Report encourages leaders to think outside the quarterly reporting cycle and create policies that manage risks and shape the agenda for the coming years.

“Health and economic disruptions are compounding social cleavages,” said Saadia Zahidi, Managing Director, World

Economic Forum. “This is creating tensions at a time when collaboration within societies and among the international community will be fundamental to ensure a more even and rapid global recovery.”

Carolina Klint, Risk Management Leader, Continental Europe, Marsh, added the need of prudence

around cyber and space concerns. “As companies recover from the pandemic, they are rightly sharpening their focus on organisational resilience and ESG credentials,” she observed.

“With cyber threats now growing faster than our ability to eradicate them permanently, it is clear that neither resilience nor governance are possible without credible and sophisticated cyber risk management plans. Similarly, organisations need to start understanding their space risks, particularly the risk to satellites on which we have become increasingly reliant, given the rise in geopolitical ambitions and tensions.”

“MARSH AND INOXICO’S COLLABORATION WILL ENABLE OUR SOUTH AFRICAN CLIENTS TO GAIN MORE INSIGHT INTO THEIR COMMERCIAL CREDIT MANAGEMENT FUNCTION”

In March, Marsh announced an exclusive collaboration with technology company Inoxico, specialist in predictive trade credit analytics solutions, to support South African clients in managing their trade credit risks and increasing their profitability generated from trade credit sales.

Trade credit is the most important form of growth capital in developing countries and is estimated to be a significant - and growing - $100bn industry in Africa. Using Inoxico’s Trade Shield solution, Marsh’s South Africa’s clients can use predictive analytics on their accounts receivables to gain debtor credit scores and debtor risk segmentation, as well as access to customer credit reports, credit limits insights and changes to risk profiles.

“Marsh and Inoxico’s collaboration will enable our South African clients, through the use of powerful analytics, to gain more insight into their commercial credit management function, assessed Pieter Dingemans, Credit Specialties Leader, Middle East and Africa, Marsh Specialty. “As a result, our clients will be able to confidently extend the amount of trade credit offered to their customers, while also increasing their operational resilience, boosting their growth strategy and reducing the impact of future shocks.”

“I am proud to formally announce this industry-shaping collaboration,” added Kiashan Moodley, Head of Partnerships at Inoxico. “This is what the market has been waiting for – a partnership that puts the customer back in the driving seat and provides them with powerful tools to confidently navigate the complex business landscape we currently, and will continue to, find ourselves in.”

In November, Marsh revealed that it intends to exercise its option to acquire the majority of shares in Beassur Marsh, a leading insurance broker in Morocco in which it had acquired a stake in June 2019. Beassur Marsh will henceforth operate as Marsh Morocco and current CEO Mehdi Tazi will become CEO of Marsh Morocco. Beassur Marsh team will become part of

Marsh’s expanding network of dedicated regional expertise across the Africa region, benefitting not only from local knowledge and experience but access to Marsh’s global resources and capabilities.

“Through Marsh’s network, leading Moroccan businesses will, for the first time, have local access to unrivalled risk and insurance services and solutions than can support them in realising their growth ambitions and enhance their contribution to the region’s wider economic success,” said Tazi.

“THROUGH MARSH’S NETWORK, LEADING MOROCCAN BUSINESSES WILL HAVE LOCAL ACCESS TO UNRIVALLED RISK AND INSURANCE SERVICES AND SOLUTIONS”

South Africa’s banking sector is once again led by Standard Bank in 2022, retaining its position as the biggest bank in the country based on capital ahead of the likes of FirstRand and Absa. At Standard Lesotho Bank (SLB), a comprehensive digital strategy to improve customers’ accessibility had been instigated long before the global outbreak of coronavirus, with cloud adoption and platform banking marking two of its major current journeys. “Lesotho is our Home, and we drive her growth,” SLB proudly proclaims.

PRODUCTION: James Daveythe full spectrum of financial services offered through two major divisions: Corporate and Investment Banking (CIB) and Personal and Business Banking (PBB), with the CIB division additionally fulfilling a wide range of requirements for banking, finance, trading, investment, risk management and advisory services. The PBB unit offers banking and other financial services to individuals, small-to-medium enterprises, and commercial businesses.

Having been rocked by the passing in October 2020 of CEO Kenrick Cockerill, who leaves the legacy of a dedicated, decorated 32-year career with the Standard Bank group in which he had held several key leadership and specialist roles, Anton Nicolaisen stepped up to assume the position in March 2021. Appointing a successor to a role of this import represents a colossal challenge in the best of circumstances; amid this tragedy and tribulation it becomes near-insurmountable.

Operating since 1995, Standard Lesotho Bank (SLB) currently employs close to 1,000 members of staff and has a national footprint in all the districts of Lesotho via a network of 18 branches, as well as specialised units that house

the Head Office, Data Recovery and Operations Centre. The bank has a system of over 707 Point-of-Sale Machines and 93 ATMs strategically placed throughout the country, and in 2018, also rolled a fleet of seven Bulk Cash Deposit Machines enabling businesses to deposit cash at any time.

“Our vision is to be the preferred and leading financial services provider in Lesotho,” SLB opens.

“But we’re more than just a bank: we look beyond the financial outcome to create more value socially, economically, and environmentally. As a leading Africa-focused financial services organisation, Africa is our home, and we drive her growth.”

Part of the Standard Bank Group, Africa’s largest by assets, SLB provides

As he detailed last year, however, Nicolaisen is a self-confessed ‘career banker’, himself accruing a rich, deep vein of experience over a more than 30year history with Standard Bank Group, always having dreamed of exposure in other geographical areas than South Africa alone. “One thing I always tell people both within and outside of the Standard Bank Group,” he disclosed, “is how many awesome opportunities are there waiting to be seized, to allow you to live out these dreams.”

Most recently deployed in Gauteng, following his move to Lesotho Nicolaisen was immediately able to assess and compare the two modes of operation last year, drawing some surprising conclusions along the way. “As might be the expectation, in the South African context there are certainly some things which are further ahead,” Nicolaisen says, “but actually, I came into Lesotho and found that

Continues on page 42

“AS A LEADING AFRICA-FOCUSED FINANCIAL SERVICES ORGANISATION, AFRICA IS OUR HOME, AND WE DRIVE HER GROWTH”Anton Nicolaisen, CEO

Continued from page 42

other aspects of the business are moving forward much more quickly.

“I have learnt never to assume that one will automatically be better than the other, because there were some very distinct advancements that the Lesotho team had made that were brilliant.”

The economic environment of the last 12 months has been extraordinarily difficult, with consumers under inflation pressures, Nicolaisen explains. “In Lesotho transport contributes a significant percentage to the overall financial basket, and a big part of our population is very dependent on public transport; those prices rising only amplified this pressure. Fortunately, our asset book and our bad debt remain very healthy at this stage.

“From a Lesotho perspective, financial inclusion is something that we are driving very hard, and which is backed by both the government and the central bank. A pricing directive was implemented and had a marked impact on our revenue, and we

were forced to counter that by being more innovative in our approach to serving our customers differently.”

“Customer service is hugely important, and understanding our customers and their changing demands better is critical. Ultimately, we would like to become much more flexible in terms of our offerings and make changes a lot more quickly.” Given the benefits

of agility, flexibility and scalability at low infrastructure and computing costs, it is little wonder that Nicolaisen is able to detail to us SLB’s fervent adoption of cloud technologies.

“Embarking on our cloud migration journey has represented one of our major investments from a technology and investment point of view,” he relays. “Cloud will assist us massively in terms of the value that we will create from having up to date systems and

the software we have available.”

Another of SLB’s key journeys that Nicolaisen wishes to zero in on concerns personalisation, and a landmark partnership with Salesforce, the world’s premier customer relationship management (CRM) platform. It marks a key step in its bid to become a true platform business and deliver positive digital experiences to its clients, he affirms.

“It is a major step towards transforming the Standard Bank Group into a client-centred platform business that delivers a range of individualised, instantly available solutions, services and opportunities,

enabled by modern digital technologies and delivered in whatever way a client prefers,” Nicolaisen explains.

“Our goal is to use our data capabilities to build deeper, better, and more enduring relationships with our clients. Our aim is to be able to digitise and create much more current solutions in order to migrate our customers out of our branches, and onto self-serving platforms. We want to really maximise our use of the digital approach, and we see our platforms as a key way to reach customers especially in the rural areas.”

Nicolaisen stresses the importance of platform banking, and the desire to move toward this model. As the banking sector digitises, platform banking is a technologically- enabled integration of traditional and digital banking, fintech and third parties that transforms the traditional paradigm into a customercentric one. “We want to be a digital, platform-based bank, and we want to achieve this by 2025” he stresses.

“We want inclusivity and we want our customers to use our platform. In

Lesotho, our aim is to reach each and every citizen in the country in some way.” In this bid to increase financial inclusion among citizens of Lesotho and stimulate economic growth for informal markets, SLB has introduced the UNAYO platform, a low-cost, one-stop platform that can be used as a vehicle for growing businesses, providing economic growth for the community and ultimately making individual and collective dreams real.

“As a financial services provider, we are constantly trying to find new ways to deliver our brand promise by enabling business growth and empowering our communities,” rounds off Nicolaisen. “The arrival of UNAYO addresses the need for financial inclusion in our country and has given us the opportunity to increase customercentricity, by continuing to engage and give impeccable service to all.”

“WE WANT TO BE A DIGITAL, PLATFORMBASED BANK, AND WE WANT TO ACHIEVE THIS BY 2025”

Important events and exhibitions taking place across sub-Saharan Africa, giving brands a platform to tell their story.

JAN 23

JAN 23 - 25 | ADDIS ABABA

EITE is a multi-sector trade show that showcases the latest products and services in the consumer market ranging from home decor and electronics to textiles and FMCG products and everything in between. The event is set to be a one stop shop to source and display commodities, meet with industry partners and customers and examine recent market trends and opportunities.

Ethiopia was Africa’s fastest growing economy in 2015 and having the continent’s second largest population, there is a huge demand from the rising middle class for consumer goods. Being a strictly B2B trade show, EITE is guaranteed to offer return on investments for exporters and manufacturers looking for new business contacts in the last big untapped market on the continent, Ethiopia.

FEB 15

FEB 15 - 17 | KIGALI

The African Fine Coffees Conference & Exhibition is Africa’s largest coffee trade platform that – over the three days of the event –brings over 2000 regional and international coffee roasters, traders, producers, professionals and connoisseurs under one roof!

The wonderful exhibition area has increasingly been regarded as pivotal in providing a unique opportunity to exhibitors showcasing the best coffees and affiliated services and providing ample opportunity to network with coffee luminaries from all over the world. This will be the perfect platform for gathering valuable coffee information, building trade relations and buyer/seller interaction.

FEB 27

FEB 27 - MAR 01 | JOHANNESBURG

Meetings Africa 2023 will see the 17th advent of this Business Events Trade Show, owned by South African Tourism, with the specific objective of creating a market access platform, for African Business Events Products. It serves as the primary platform to enable the growth of the business events industry on the continent and ultimately contributes towards its economic growth.

Meetings Africa is a 2-day trade show with a dedicated Educational Day which is executed in conjunction with the key global, continental and national industry associations.

Meetings Africa exists to provide a platform for exhibitors to showcase their offerings to International and local buyers, African associations and corporate planners. It is the most formidable platform on the continent for you to meet face-to-face with the most influential buyers in the world, and to be part of Africa’s growth.

COMPACK NIGERIA LAGOS

ETHIOPIA INTERNATIONAL TRADE EXPO | ADDIS ABABA

SOLAR POWER AFRICA CAPE TOWN

AFRICAN FINE COFFEE CONFERENCE | KIGALI

INVESTEC CAPE TOWN ART FAIR | CAPE TOWN

SENCON DAKAR

MEETINGS AFRICA JOHANNESBURG