www.financederivative.com Asia | Americas | Africa | Middle East | Europe

CEO and Publisher

Mehtab Chisti

Editor Mara KI

Head of Distribution

Stefan Stavic

Project Manager

Emma Bakker

Business Consultants

Lena Thomas, Aaron Menon, Blair & Allan Mendez

Business Analyst Rachel Thomas, Amalia Rubio

Graphic Designer Sachin MR

Digital Marketing Mithun Gowda

Web Development and Maintenance Sonu Kumar

Advertising Phone: +31208943644 Email: info@financederivative.com

FM. Publishing Tussen Meer 345 1069DR Amsterdam Netherlands Phone: +31208943644 Email: info@financederivative.com

Finance Derivative is the trading name of FM. Publishing Company Registration Number: 71674233 VAT Number: NL002483895B26 ISSN 2666 6715

Image credits: https://www.istockphoto.com/ https://www.rawpixel.com https://pixabay.com

Finance Derivative Awards is established with the aim of honoring excellence in performance and rewarding Companies across different domains of business & financial world.

Our award honors companies and their key players who have performed extraordinarily well and who strive for fineness & provide a platform for recognition.

Check our online publication at www.financederivative.com

FROM THE CEO

Greetings from Finance Derivative and A very warm Welcome to all our readers.

We thank you all the Outstanding and young supporters who keep us inspired to bring this edition to you each time. The engaging content for the year 2022 we bring a lot of exciting topics covering the automated networking, Cyber security and Biometric technology.

Technologies are constantly evolving and will always bring opportunities to always bring opportunities to unlock new areas of business. More than just helping meet regulatory requirements and reducing costs, organisations are increasingly recognising that there are limitless possibilities for innovation if they can stay agile and flexible. Have a deep overview about Digitalisation being the continuous process.

We witnessed the proliferation of mobile banking in the late 00s and, most recently, the cryptocurrency boom of the past decade. But what is the next technological advancement of banking? Let’s find out.

Hope you will enjoy reading this issue of Finance Derivative. Wishing you all great business and success. Enjoy!

Mehtab Chisti CEO

BANKING: 28. How banking could benefit from the metaverse 42. How is Banking-as-a-Service helping retailers lead the market? TECHNOLOGY: 6. The practicalities and best practices for deploying conversational AI 15. Cyber security: Combating automated attacks with automated privileged processes 22. Leveraging innovative technology to improve financial processes 36. Improving Customers’ Experience at Banks using Biometric Technology FINANCE: 9. Return on data and the balance sheet 46. 6 success factors 50. Digital finance: BUSINESS: 12. Automated Networking: 64. Resilience in Volatility 67. The Importance CONTENTS 22 64

assets: A new way for leaders to think about data sheet factors for the digitalisation of the financial sector finance: a guide to virtual inheritance BUSINESS: Networking: Better Connectivity, Better Business The Real-Estate Market Despite Economic Importance of Cyber Security for Small Businesses SPECIAL FEATURES: 18. An Exclusive Interview with AsiaPay CEO -Joseph Chan 26. Finance derivate Q&A with Ibrahim 52. Finance Derivative || Global Award Winners 2022 60. Finance Derivative Talks To Tianjin Port Development Holdings Limited 70. Exclusive Session With Roosevelt Ogbonna WEALTH MANAGEMENT: 32. Why Data Center Location and Speed Matter for Trading Success 40. Selling risk – how innovation can be brought to the front at insurers 50 6 28 40 67 36 12 32 46 42

In its predictions for 2023, Forrester noted that, despite some dampening, data-driven automation would continue apace into the next year. Conversational AI is

one such automation technology growing in profile for the banking and financial services market. Virtual agents are one of the most widely applicable and easily implemented data-driven automation technologies available to financial organisations.

6 Technology

What financial organisations need to know to get the most out of their virtual agents

The practicalities and best practices for deploying conversational AI

Bespoke conversational AI platforms can transform finance businesses when regularly maintained and managed properly. However, this technology isn’t as commonplace across the sector as it should be. Many banks and financial institutions may have basic chatbot functionality to assist customer enquiries. Still, when it comes to fully-fledged automation, many are yet to leap into conversational AI as they are unsure where to start.

In order to progress and adopt a properly automated approach to customer service and the employee experience, businesses need to take four important steps to achieve the best results from a conversational AI solution.

Do your homework

The first step for any business is identifying a use case. No two conversational AI solutions are the same, or at least, they shouldn’t be. Businesses' use cases can be as simple as checking account balances or as high-level as automating multi-layered customer enquiries. Identifying what solution works best for you is key.

Responsible implementation is integral here. Conversational AI shouldn’t be all or nothing; slow and considered implementation works for everyone, customers, stakeholders, and

the AI itself! The most successful conversational AI cases have been allowed to grow and take on greater responsibility at a manageable rate. Make sure you know what you want to achieve and set yourself attainable targets. Treating the AI as a digital colleague will help change perceptions of investing time into training the AI models. We know that to get the best out of humans, it isn’t just the initial training that matters; ongoing learning creates world-class output levels. The benefit of doing this with AI is that it's many times more scalable and consistent in customer outcomes.

Nurture your virtual agent

Once you’ve established a use case, it is time to implement your AI. Conversational AI uses Natural Language Processing (NLP) to interpret and understand voice and text commands by cross-referencing with a catalogue of relevant information. In a matter of weeks, your conversational AI can be up and running. However, just because you have a virtual agent up and running doesn't mean your work is over. The most successful conversational AI-powered virtual agents are kept up to date, honed and tended to over time. Preparing a team to manage your bot is important during the initial scoping phase. Don’t

worry – they don’t have to be quantum computer scientists; quite the opposite is required! The best AI trainers understand customer priorities and can craft the training data for the programmes accordingly. Expect some challenges along the way

Of course, it is unlikely that everything will be smooth sailing, particularly if you plan to be innovative with your solution. For example, voice-adapted virtual agents are still in their relative infancy, but the human voice represents one of the ‘holy grails’ of automation. “Talking to a robot on the phone” is often the target of much customer ire, but poorly maintained voice assistants give the rest of them a bad name. Make sure you keep an eye on your bots and update them in line with innovations, as this will ensure you’re always at the cutting edge.

Moreover, NLP requires vast datasets and needs to straddle many different areas of a business to be effective. This requirement presents unique challenges for larger organisations with labyrinthine and archaic IT setups. Creating a hospitable data infrastructure for conversational AI is a huge task but a necessary one for all businesses. The benefits of a coherent data strategy are apparent. Still, the potential

7 Technology

for smooth implementation of conversational AI only emphasises these benefits and makes it imperative to have a clear data strategy.

Work out how you want to measure success

There are three pillars of success for conversational AI for customers.

1. Automation: Have your customer resolution rates improved? How widely adopted and used is your conversational AI?

2. Commercial value: Have you seen upsales because of your conversational AI? Is it adding value?

3. Customer satisfaction: Are customers receiving an improved service? Are you seeing less customer churn?

Conversational AI may not always run smoothly, but that is no reason to give up on the technology. Re-evaluating an underperforming virtual agent, reassessing the use case and retraining your AI solution can unlock unrealised potential. AI is a constantly evolving technology, and with patience and fine-tuning, it can work for organisations of every shape and size. The important thing is to understand your goals for the business and how your AI platform can help you to achieve

these goals, as this will guide how you develop the solution over time.

Getting started with conversational AI, but should you Build or Buy?

The build or buy debate is one that the financial industry is incredibly familiar with. Suppose you’re in a fortunate enough position to afford to build your own conversational AI platform - you’ll need to wait several years before you can get going with it. You’ll need the knowledge and insight in-house to make it work. Whilst many large institutions will have vast development resources and feel the need to maximise their utilisation, the expertise in this new area will take time to achieve and delay further successful implementations.

Hence, we are seeing a rapidly rising level of interest from many organisations choosing to buy into solutions having taken a first stab at building themselves. Not only is it faster to buy readymade solutions to meet consumer demand for new services immediately. Third parties can take a more objective view of your operations, bring in their experience, and help to hone your solution with their knowledge and expertise in AI technology.

Ultimately, whether you build your virtual agent yourself or bring in a third party, your involvement in every step is the secret to success. For example, establishing things like tone-of-voice phrasing needs to happen in-house, but outside experts can provide invaluable insight.

Time to get started with conversational AI

Conversational AI is here to stay. This is not a flash-in-thepan technology; automation is the future of customer service in the finance industry, as well as having many other use cases to help financial businesses operate more efficiently. Implementing any new technology to your business will be a little scary – there will always be unknowns. However, by following the steps above, and taking a pragmatic approach, banking and finance organisations can lean on conversational AI, virtual agents, and automation to drive transformational results for their business.

Sanjeev Kumar, VP of EMEA, Boost.ai

8 Technology

Return on data assets:

sheet

In today's digital society, one could easily argue that data is the most valuable asset for any organisation. Companies like Uber and Netflix consume billions of data points to constantly improve their understanding of customer trends and behaviour, while simultaneously improving the overall user experience. Without data, there would be no ride-sharing option, and creating content that captivates specific audiences or geographies would be impossible. The irony, however, is that despite its apparent intrinsic value, data assets are still not captured on the balance sheet of any organisation. The reason? It turns out that it's incredibly difficult to quantify the monetary value of data

accurately. In order to do so, business leaders are required to think outside of the box.

While technically, data meets the minimum acceptable criteria for a balance sheet asset, current accounting practices still prohibit organisations from capitalising data as an asset.

There are two main reasons for this: first, current practices introduce certain practical inefficiencies, and second, a lack of ability to establish a direct link between data and measured business outcomes. The latter of the two leads to priceless data assets being either under-utilised or disregarded altogether in the organisation's strategy to build new or alternative revenue streams.

The first step towards avoiding this trap is for organisations to create a culture of visibility and access to data that can supplement and improve the thought processes of everyone. Data must become the secret sauce that inspires and empowers people to drive revenues and enhance profitability. Data cannot be added to the balance sheet unless it underpins the value-creation process across the entire organisation.

The question becomes how to measure this movement. Wall Street analysts use a metric called Return on Assets (or ROA) to help assess how efficiently a company uses its assets to generate profit. A high value for ROA means that a

9 Finance

A new way for leaders to think about data and the balance

company is more efficient at leveraging its assets to produce positive returns. ROA provides a crucial benchmark for CxOs and forces them to consider the strategic implications of operations on profitability. However, since data is not reflected on the balance sheet, current metrics still fail to capture the returns from investing in data practices.

Proposing a new financial metric: Return on Data Assets

Considering the shortcomings of existing metrics like ROA, it is clear that an alternative approach is required for companies to quantify the returns generated from using their data. One possible alternative is to consider the Return on Data Assets (or RODA). The foundation of RODA is to look at the income driven by data assets (both direct and indirect) and compare that with the costs of creating and curating the data assets.

In this scenario, we can classify a "data asset" as any object that provides information (e.g., a dataset containing customer records) or a service that augments information to deliver insights (e.g., a model used for risk assessment). Having complete visibility of how data is used across the organisation becomes essential to construct a clear framework for comparing project outcomes. The

basic formula for RODA is as follows:

RODA =(Yield from Data Assets)/(Cost of Data Assets)

Taking this formula, companies can quantify their ability to monetise data assets cost-effectively and efficiently. The principles of RODA require that CDOs optimise both the yield from data assets and the cost of those assets. On the income side, CDOs must focus on use cases where data can be leveraged to drive the maximum business value (direct or indirect). Looking at the cost, CDOs must work to construct a data strategy for the most cost-effective way to create, maintain and secure data assets. Existing data assets must either be monetised or decommissioned and replaced to create an ecosystem of high-productive data assets.

At the micro level, RODA can help CDOs and business leaders prioritise projects and use cases. At the macro level, it can help CFOs allocate capital more effectively and help CTOs make better decisions on which technologies to implement. Simply put, if RODA is greater than the cost of capital, a project or use case creates positive economic value. Conversely, if the cost of capital is greater, a project or use case erodes the bottom line and is not worth pursuing.

Conclusion: Understanding how data is driving the business

Adding data to the balance sheet as an asset means completely rethinking the organisation's approach to evaluating and quantifying the value derived from its data, whether direct or indirect. Companies like Uber likely didn't have to undergo significant transformation to quantify its data asset value, but that's because data was already embedded as a value driver at the core of the corporate strategy. Most organisations, however, still struggle to understand how data is powering the business, let alone capturing it as a tangible asset on the balance sheet.

It's vital for any organisation serious about building a data asset strategy to prioritise establishing a simple yet clear financial metric to quantify the tangible value of its data assets. Whether it's fundamental or financial, data has always been and always will be the core driver of value to the organisation's bottom line. It's time to move data to its rightful place: as an asset on the balance sheet.

10 Finance

Eon Retief, Technical Director, Financial Services, Databricks

11

Automated Networking: Better Connectivity, Better Business

For the modern organisation, reliable connectivity is essential for any industry to work efficiently and safely. To have the most impactful and consistent networking, many companies are turning to automation to streamline their operations. By using automated networking processes, companies can improve their solutions and allow their IT teams to work to their full potential by using software to perform repetitive, manual tasks.

Fewer Errors, Better Service

By integrating automated software, network providers can guarantee a higher level of service for their customers 24 hours a day, seven days a week. Automation in networking can detect and resolve a flaw in the service even before

a human has been notified. This improved level of service also leads to less calls to support lines and engineer visits. As internet connection is vital to the everyday running of a business, automation, and the use of machine learning to resolve issues guarantees a better service.

Automated software can aid engineers in their work by processing huge amounts of data accurately and in a short space of time. By automating these processes, human error is removed and can allow for better connection to the network. Errors are also further reduced as automated software only follows rules that are set by a human operator, stopping the system from making rogue or interpretive decisions without prior instruction.

This reduces customers’ frustration with the network and makes them less likely to look to another provider. Many businesses now rely on high bandwidth, low latency connectivity in their everyday operations. To deliver this, au tomated processes provide better accuracy, reliability, and productivity. Ultimately, au tomation allows providers to supply an enhanced service package which is unrivalled by companies who don’t utilise automation.

Enhanced Security

Automated networking can provide a higher level of security as human error is reduced in the

12 Business

13 Business

application of policies. As processes are repeated, this guarantees a better level of security as there is greater consistency in the network’s own defences. Moreover, by identifying and resolving threats using automated tools, automation can help to mitigate risk by deflecting before an engineer has even been notified. As threats to networks are constant and evolving, automation provides a solid first defence, reducing potential issues.

Using Automation to Improve Job Satisfaction

By incorporating automation into networking processes, companies can ensure that their IT teams are feeling more fulfilled, focusing them on more interesting, creative jobs, as opposed to mundane tasks. Rather than spending hours repeating processes and trawling through data to look for anomalies, IT teams can better utilise their skills and ultimately complete the tasks that bring them greater job satisfaction. Over-stressed or uninspired staff are more likely to become demotivated and make mistakes as they have less interest in their role. Automated processes can carry out these repetitive tasks more quickly and thoroughly,

giving IT teams time to make higher level decisions. This is important as 87% of companies worldwide are aware that they have a skills gap or will have one in the next few years. If IT teams are more fulfilled, staff retention is likely to be higher, and they will tend to provide a better service for the company. Putting experienced employees in more interesting roles is a more cost-effective method than hiring and training new staff. Over the longer term, IT roles should see an improvement in terms of retention and better recruitment of new talent.

Cost Cutting on Operations

As many companies are looking for ways to improve the cost-effectiveness of operations, many IT teams are looking to automation as a safe investment which will further improve as technology becomes more capable and readily available at a reasonable cost. Because automated networking reduces the number of trouble tickets and callouts, this ultimately leads to better profit margins for enterprises. As many companies rely on connectivity to generate profit, any inefficiencies in the network could ultimately impact the bottom line and drive

clients into the arms of better-prepared competitors.

Rather than allocating resources to resolving issues and callouts, enterprises can be more involved in network design, outage planning and infrastructure improvement. This is a better return on investment for employers as their staff are no longer wasting resources and are instead using their time and skills to enhance the service and business offerings. Ultimately, this will go a long way to improve customer retention as well as attract new prospects.

Through automation, IT teams now have more consistency and insights into the network, monitoring its health and being able to mitigate issues before they happen. With a strong foundation of automation in place across networks, engineers can feel empowered to innovate and determine ways that networks can add further value to end users.

14 Business

Jamie Pitchforth, Head of Education Practice, EMEA, Juniper

Combating automated attacks with automated privileged processes

Cyberattacks present the biggest risk to the UK financial system, according to research released this summer by the Bank of England. Three quarters (74%) of respondents to its H2 systemic risk survey believe a cyberattack poses the highest risk to the sector in both the short and long term. The number of respondents who believe their company is at high risk of attack doubled from 31% in the first half of the

year to 62% in the second.

Cyber-criminals are constantly evolving their attack strategies to take advantage of advancing technologies, including IT automation. Hackers and bad actors are progressively developing and deploying automated tools that enable them to carry out a high volume of attacks, rapidly, and on an ongoing basis, without the need for human involvement.

These attacks might include credential stuffing, where sets of stolen login details are tried across multiple applications until they hit the jackpot, or using pre-programmed tools to steal login credentials from commonly used websites and applications.

To effectively compete against this level of sophistication, organisations need to combat automation with automation.

15 Technology

Securing privileged IT processes

Many common IT and business functions need to be carried out by privileged administrators with secure access to systems and applications. Their accounts have a great deal of power – for example to access sensitive data, change configurations, and unlock, create, delete or update user accounts. A cyber-criminal who gets hold of the credentials for one of these privileged accounts could cause extensive damage, particularly as these processes often involve multiple systems.

Securely automating tasks and processes that require privileged access can protect them from being compromised by cyber attackers, preventing the exposure of valuable admin credentials, while taking the human out of the equation. This ensures that processes are followed to the letter, while reducing the chance of mistakes that might open the door to a hacker. The business will also benefit from having a full end-to-end audit trail around everything that has gone on, a vital part of governance and compliance with financial

Reducing the burden on IT

Account management tasks such as resetting someone’s forgotten password or setting up accounts for new joiners are performed multiple times every day. They may be simple, but due to security risks associated with the changes they’re assigned to senior staff. Most IT teams are overworked, with experts spending precious time on tasks they’d rather not be doing.

When a new team member joins, for example, the traditional process is to send a request to the IT service desk to provision the user’s accounts, which may be in four or five systems. When someone leaves, all those accounts must be removed as quickly as possible to ensure security.

Delays in implementing these seemingly simple requests can impact the business directly, and frustrate users by slowing operations down. Even worse, if errors are made while making the changes this can give rise to security risks such as granting a user access to more systems than they need.

Automating these routine processes also has the potential to transform

Wrap those tasks up in secure automation and they can be safely delegated to a helpdesk engineer or even the user themselves. Alongside saving costs and time, this will free up IT professionals to focus on more value-added activities.

16 Technology

The barriers to adoption

Automation hasn’t been as broadly adopted for IT operations as one might think. According to recent independent research commissioned by Osirium, 92% of IT professionals see the value in delegating IT tasks from admins to the helpdesk or end-users, but less than half (43%) delegate most of their work at present. Risk was listed as the main reason holding respondents back – with concerns over security risks (29%), compliance risks (25%), performance risks (24%) and cost risks (18%) all cited.

The key to mitigating these risks and implementing automation securely is to select a suitable software platform. Currently, just over one third of organisations use robotic process automation (RPA) for IT automation. However, while this approach is good for processing a high volume of similar transactions over and over, IT operations tend to be more complex and require more flexibility. Other automation systems, meanwhile, need to embed usernames and passwords to be able to run commands, which of course introduces the risk of exposure.

Organisations should seek a platform that prevents privileged credentials from being exposed, offers secure connections to IT systems and devices, and makes it quick and easy to

build automation scripts – for example through providing pre-built ‘playbooks’ that IT can use for frequent tasks and processes, or as templates from which to create customised scripts. It’s also a good idea to look for a solution that features human-guided automation, which enables non-specialist end-us ers to ‘self-service’ without calling the helpdesk, but allows IT to review and approve changes before execution.

Automation must now be considered as a critical component of any robust cybersecurity programme. Trying to keep pace with sophisticated cyber-at tackers manually is a losing battle.

Automating privileged processes as sociated with account management tasks will improve an organisation’s defences against ransomware and other cyberattacks. It will also trans form efficiency, simplify compliance audits, and reduce the load on IT, while – just as important in the midst of ‘the great resignation’ – delivering an im proved service for end-users.

17 Technology

Mark Warren, Product Specialist, Osirium

An Exclusive Interview with AsiaPay CEO -Joseph Chan

18 SPECIAL FEATURES

Q. It’s a pleasure to have you. Tell me a bit about your journey and about heading AsiaPay.

A. * As the founder and CEO of AsiaPay Group, Joseph started up the first high-quality third-party digital payment service and technology firm in 2000 in Hong Kong, spearheaded the company’s business strategies and product development together with his management team, and leads AsiaPay becoming one of the most successful world-class digital payment companies in Asia.

* In regard to business growth and market recognition, Joseph presents his long-term vision which is to operate a successful and socially responsible company that continually provides individuals and corporate entities with the newest digital payment values, readily enhances one’s quality of life, and maximizes business opportunities, efficiency and productivity.

Q. On that note of innovation, what are your views, on things like blockchain, Artificial intelligence, and robotics?

A. *AsiaPay works closely with our partners in the AI, metaverse, crypto, and NFT-related businesses. With the capabilities of the web3 payment, we aim to strengthen the sales scene, use virtual social space as attraction, product display, and sales as a reality, and enhance the interest and purchase intention of potential buyers, coupled with cryptocurrency-led payment.

Decentralizing blockchain can guarantee the fidelity and security of transactions and digital payments. While combining digital record authenticity in blockchain technologies and the automation of artificial intelligence can enhance data security to prevent fraud in the fintech and digital commerce industries.

Along digital transformation, there has been successful applications of robotics in F&B n hotel industries in Asia and more digital payment solution adoption follows to provide more seamless and valued payment experience to customers.

* AsiaPay continues to work closely with partners and startups in these technology areas and also web3 area like metaverse, crypto to well capitalise on these technologies to provide more advanced payment solution to address coming business and market needs

Q. How do you manage the making in the area of diversity and inclusion in terms of gender and cultural background?

A AsiaPay always aims to remain a balanced and fair working environment with diversity and inclusion over its 15 country operations in Asia. As we serve merchants covering wide range of industries and operating across borders with close interaction with our teams in Asia, we respect the unique background, needs, perspectives, and potential of all team members. We:

1. Identify diversity and inclusion as key strategic priorities

2. Recruit and hire openly across Asia

19 SPECIAL FEATURES

Q. AsiaPay continues its business expansion in Asia with 16 operation offices as of date. What are the strategies for the Indonesian market?

3. Establish snd enforce cross-country mentorship

4. Promote team work and foster relationship by overseas team training, yearly executive meeting...etc ...

5. Acknowledge holidays of all cultures and celebrate

6. Be aware of any unconscious bias.

7. Ensure benefits and programs are inclusive

And, we set up a variety of staff performance and long-service awards to appreciate our team member’s contributions regardless of their genders, races, religion, nationalities, and sexual orientations. Every team member is equally involved in and supported in all areas of the workplace.

Even under this highly competitive Fintech market, we have enjoyed relatively high retention over the years.

A. Indonesia is one of the key emerging markets in Asia, according to a YStats.com report points that Indonesia mostly used “online wallet” (69%) alternatively to traditional payments in 2020. “Online wallet” was commonly used as an alternative payment method after the onset of COVID-19;

BimoPay is a payment gateway platform service offered by AsiaPayto address the Indonesian digital payment needs, as Indonesia is one of the fastest-growing economies in the world. Our key strategies shall emcompass,

* Sales strategies and programs targeting key merchant segments;

* Bank and payment and channel partnership;

* Digital marketing campaigns enhancing brand and service awareness;

* Localised product and service innovation and development;

Q. Do you see AsiaPay expanding its offering in the future? How do you see 2023 coming?

A.* With digitalization and technological innovations taking over the economic sector of the world, AsiaPay will continually bring advanced, secured, integrated, and cost-effective digital payment processing solutions and services to banks and eBusiness globally.

* We will continually embrace change and innovate capitalizing on the technological trends and strength especially addressing the coming evolution of digital commerce, smart retail, web 3.0 payment, payment data analytics, crypto/CBDC and blockchain technologies.

* Apart from our existing 16-country operations in Asia, we will continue to expand our footprint in the world to expand our payment solution and service coverage, and further scale-out.

21 SPECIAL FEATURES

The pandemic brought attention to the “digital divide” between businesses that had previously made investments in digital systems had not. Agile technology, automation, and machine learning have allowed organisations to remove tedious manual chores from essential the freedom to develop strategies to accelerate corporate growth. Implementing adequate steps towards financial ‘independence’ is journey of implementing automated financial systems?a

22 Technology

systems for their financial operations and others that essential processes. This has given finance experts is a challenge in itself. How then, can we start the

Incorporating digital finance expertise

Moving forward, many traditional finance roles will be automated or superseded by digital and data-driven skillsets needed to get the best returns from technology and automation. With technology automation taking over transactional processes, finance departments must evolve from “number crunching” teams to strategic advisors. Finance teams need to build digital competencies in their teams now to better deliver results in the future.

Technology literacy, digital translation, digital learning, digital bias management, and digital ambition are all financial skills worth learning. Once systems are automated, the human side of the business can better dedicate its time to planning for the future and adding real value, instead of counting data in the present.

Streamlining with innovative technology

Finance transformation requires the right technology. The right finance platform solution can help streamline processes, increase accuracy, and reduce costs. It can automate and manage financial processes and help to provide actionable insights that drive business strategy and growth. This would allow finance teams to gain visibility across the entire business, helping to manage risk locally and abroad.

Technology vendors can provide innovative platform cloud solutions so that it is easier to maintain and adapt to ever-changing business demands. Being equipped with the latest financial platform technology while reaping the benefits of optimised costs of maintenance means that businesses can remain agile with minimal investment.

23 Technology

Devising smart and optimal strategies

The right financial management platform serves as a one-stop shop for the entire financial process, including budgeting, planning, and forecasting. This effectively transforms finance from static and disparate into an agile, flexible, and fast-moving strategic business function. This transformation is providing the organisation with an intelligent platform that integrates systems of records and systems of reports across the entire firm, removing the need for various tools and reducing the need for spreadsheets.

Companies can move to dynamic forecasting and budgeting models instead of scheduled reporting, which provides deeper insights and the means to understand the impact of business events whether planned or incidental.

Utilising the right insights

Financial data analytics gives an in-depth study and real-time view of a company’s financial position. Predictive and advanced analytics improve decision-making by delivering significant information in bulk, creating a more thorough financial story – often accomplished using dashboards.

These dashboards might be difficult to construct as selecting

and arranging meaningful data, and then converting them into actionable insights require specific knowledge and expertise. This is where an external partner can assist, as those abilities are difficult to find and retain inhouse in a competitive market. Many finance teams, not making this investment, continue to rely on out-of-date dashboards and apps, and as a result spend more time gathering data and building ad hoc reports than analysing data.

Enacting smart and efficient finance automation

In recent years, the use of robotic process automation (RPA) and artificial intelligence (AI) technologies have grown across many corporate areas. However, adoption has been slower in finance as the true benefits of quick end-to-end business process automation and expedited digital transformation have yet to be realised. Many key finance processes remain manual, with dull and repetitive tasks, susceptible to human mistake and perceived as inefficient.

Bookkeeping, procurement, and accounts payable, invoicing and accounts receivable, tax compliance, payroll, and cost management are all good candidates for automation. Not only can this save time and money, but it can also lower the

danger of fraud, credit risk, and data theft, as well as increase the accuracy and consistency of financial data. It can transform the tasks performed by finance professionals, changing the required skills and abilities of finance teams.

To financially transform a company, constant changes must happen. Ahead of selecting the skills needed to accomplish the intended results, it is critical to have well-defined strategies towards commercial goals. These skills have got to provide proven strategies that steer the business in the right direction.

Innovative technology is the first step towards financial transformation. Once a stable financial platform is in place, business leaders can turn their attention to retraining and upskilling their finance staff. Standardised procedures should be adopted, complemented with round-theclock refinement. If done right, organisations will be equipped to adapt to a fast-changing world whilst embracing their corporate goals.

Marie-Laure Burg Autier, EMEA Workday Finance Solution Architect

at Alight Solutions

25

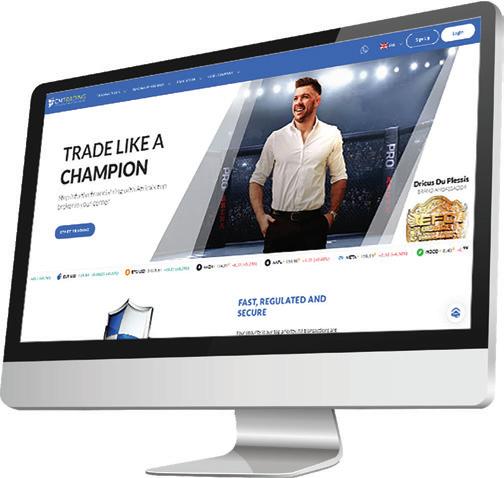

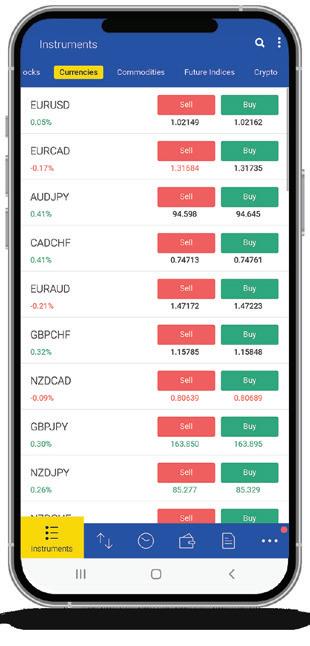

A: “We’re incredibly grateful and proud of all our awards. Each one validates our efforts to deliver a world-class trading platform and pushes us to ever-greater service delivery.

“For me, the best measure of our success is hearing direct customer feedback and that we continue to lead through great reviews.”

A: “We are a licensed, regulated, award-winning broker trusted by 1,000,000 subscribers. We believe in transparency, fair treatment and education, and this is where we’ve carved our niche.

“Trust is our primary currency, and we can only gain our customers’ trust through consistent service and transparency.

“Whether you’re new to trading or a high-tier fund manager, CMTrading is your one-stop shop for all your trading needs. We achieve this by delivering effortless financial solutions through

various trading instruments such as stocks, indices, commodities, forex, and cryptocurrencies.”

A: “We believe in emerging countries and have made great strides in Africa. We understand the difficulties that people from this continent experience.

“Emerging countries strive for better service, education, and new opportunities, including investment, and this is where we have built a compelling reputation.

26 SPECIAL FEATURES

Q: What does it mean for CMTrading to be awarded “Best Performing Broker South Africa 2022”?

Q: What sets CMTrading apart from rivals?

Q: Tell us about CMTrading’s African expansion

“We have offices in Nigeria, Kenya, and South Africa where we host seminars. They’ve been hugely successful in these regions, allowing us to engage with our clients physically.”

Q: Your business focuses on trading education; why is that?

A: “Part of our business philosophy is to make trading accessible to everyone and help people from all walks of life understand that they can become traders when they have the right broker on the journey. We pride ourselves on being an inclusive broker.

“One of our most important attributes is providing our clients with education delivered by experienced brokers. As they become better traders, their journey will be more profitable. This is a win-win scenario.

“Every customer matters equally, no matter their investment size. Service and transparency are our most important attributes for us. Any customer can openly contact us, consult with one of our experts, join one of our webinar sessions, view training videos on demand, and more.”

Q: What trading trends can you share for 2022 and beyond?

A: “So, 2022 will be remembered as the year that was almost a blood bath in terms of a vast historic selloff in the markets. We saw this in the tech sector, with major companies reporting record profits in 2021 and

experiencing a colossal share selloff. The cryptocurrency market also experienced a massive crash early in 2022, which persisted throughout the year. The oil and energy sector has been highly volatile in 2022, with record-high prices.

“So, it’s been quite a ride when we look back at the markets. Some signs point towards slowing interest rate hikes, but recessionary and inflationary pressures are still there. We’re not out of the woods yet.

“It doesn’t mean that the markets will come back roaring to all-time highs, but we could be looking to a return to normalcy in 2023. It does mean that there will be a bumpy ride again as countries are doing their best to avoid a deep recession. This is something to consider going into 2023.”

Q: Are there any developments we can look forward to?

A: “We’re increasing the number of events and seminars we host globally. These events are important to us, presenting an incredible opportunity to physically engage with customers, listen to them, and understand their desires. In 2022, we hosted successful events in Nigeria and South Africa.

“We hope to host even more events in major cities focusing on education. I’m sure clients will find them highly informative and helpful in their decision-making.”

27 SPECIAL FEATURES

How banking could benefit from the metaverse

In the past century, the banking sector has seen remarkable developments that have dramatically updated everyday banking as we know it today. Since the introduction of the credit card in the 1950s, each decade has brought significant technological advancement to the industry.

In the 60s, the new tech was ATMs; in the 70s, the first e-payment was made; and in the 90s, infamous tech investor Peter Thiel and his co-founders revolutionised banking again with

one of the few companies to survive the .com boom and bust, PayPal.

More recently, we witnessed the proliferation of mobile banking in the late 00s and, most recently, the

cryptocurrency boom of the past decade. But what is the next technological advancement of banking? As we enter the era of Web3, could it be the metaverse’s time to disrupt the industry and level up banking as we know it?

Metaverse for banking

Although the metaverse is not a new concept, with the term first coined in the sci-fi novel Snow Crash in 1992, the past few years have seen a significant advancement in consumer awareness and access to the metaverse, thanks to

28 Banking

cheaper devices and Meta’s huge push to own the space.

The metaverse is not just about gaming and entertainment. Businesses can use the technology to deliver more extraordinary B2B and B2C experiences for clients and customers alike. For example, at RendezVerse, we allow event managers to explore potential venues on the other side of the globe from the comfort of their office via the metaverse, saving time, money and significantly reducing carbon emissions.

There are clear, real-world benefits to the metaverse in business which would be equally valuable in the banking space. In short, the metaverse could revolutionise banking, and it will be the early adopters who benefit the most from this early advantage.

Customer service

In the first instance, by providing a personal banking experience in the metaverse, banks can help customers access the support and information they need without having to leave their homes.

While they could use web chats or call a helpline, the ‘face-to-face’ interaction of a metaverse meeting is far more valuable and engaging. When it comes to asking for financial advice, a personal connection and a sense of trust are vital in putting a customer at ease and finding the best solution for them.

Oftentimes physical banks are only open during office hours, so visiting the bank in person means taking time out of work. With metaverse banking, your visit ‘in branch’ can be easily scheduled into a lunch break, with no need to leave your desk.

Furthermore, with so few high street branches open nowadays and many customers

using digital banks with no physical presence, the metaverse allows customers to experience the ‘physical’ interaction of in-person meetings without needing to open new branches.

First mover advantage

Given that this moment marks the early days of the metaverse, especially for banking in the metaverse, those who choose to get involved now will have an undisputable head start. Early adopters will cement their presence within the metaverse and benefit from developing the best technology and customer service before the market is fully mature.

Banks that take the leap will make a powerful statement that they are innovators within the industry and willing to try new things to bring the best experiences to their customers.

Marketing and awareness

Consider this, having a bank headquarters in the City of London, or in Bank itself, can provide a great deal of grandeur and publicity, but imagine being the first bank with a presence in the likes of Decentraland?

Unfortunately, HSBC has already claimed that title, but there are many metaverses out there, and even in these digital

29 Banking

worlds, it can be all about location, location, location. So, securing prime real estate for your bank in the metaverse will be a powerful marketing tool.

NFTs, crypto, and the blockchain

As a Web3 technology, the metaverse lends itself to offering other Web3 services, such as NFTs and cryptocurrencies. Not only because the tech can be easily set up for such transactions – with metaverses built on the blockchain – but because the audience of people who engage with a bank in this digital world is highly likely to be interested in these products.

Consider the possibility of banks offering secure digital deposit boxes for people to hold their digital goods, such as NFTs, or acting as secure crypto wallets. If banks are the best place to store gold in the real world, perhaps they can become the golden place to secure digital currency and assets in the metaverse.

Future of banking

The gaming and entertainment industries have significantly benefited from entering the metaverse, and the world of business is beginning to follow suit. At RendezVerse, we are already seeing tremendous interest and value in using the

metaverse for travel, hospitality, and events. Banking can benefit just as much.

With customer service in banking having taken a nosedive due to the closure of branches, the banks which choose to enter the metaverse will reap great rewards from their first-mover advantage, increased awareness, and ability to offer new technologies and digital products.

Peter Gould, CEO and Founder, RendezVerse

30 Banking

Why Data Center Location and Speed Matter for TRADING SUCCESS

The best trading strategies require a highly resilient and scalable infrastructure. Many factors affect latency, especially hardware location and the resiliency of an infrastructure’s architecture, including both the scale and power of network connectivity. The key is to provision powerful servers housed in close proximity to the exchange matching engines, lowest available latency connectivity and immediate access to global market data sources.

What is Colocation?

Data center exchange colocation is when a firm locates its computer equipment in a data center managed by a third party. Financial markets, exchanges and trading venues make space available within their data centers for financial institutions and managed services providers to colocate. Originally firms colocated their trading platform as close as possible to the exchange matching engine to benefit

from ultra-low latency trading. Drivers have since expanded to include achieving deterministic latency, access to accurately time-stamped market data and connectivity to other venues, counterparties and cloud services, which appeals to a wide group of capital markets participants. The main advantage in colocating at a trading venue’s data center is gaining direct access and proximity to the venue’s matching engine, trading network and data to reduce latency.

32 Wealth Management

Latency Matters

Low latency is vital for algorithmic trading. It is the time taken for a piece of data on a network to travel from one endpoint to another and is measured in fractions of a second. Reducing latency is crucial for traders, as it means they can be more responsive to rapidly changing market conditions.

Many factors affect latency, especially hardware location and network connections. Trade execution speed is critical in maximizing profit, and a competitive advantage comes from having the best communication links to hardware in the best location.

TNS’ ultra-low latency Layer 1 technology for exchange direct access inside the data center was the first architecture of its kind to be offered and deployed globally. It eradicates the need for multiple switches by using a simple, single-hop architecture to deliver direct exchange connectivity in as little as 5 to 85 nanoseconds.

Factors to consider when moving a data centre from one jurisdiction to another

With Euronext migrating from Basildon to the Aruba Global data center IT3 in Bergamo and London Stock Exchange Group (LSEG) moving trading access to a new venue, participants need to consider data center location and speed for trading success.

33 Wealth Management

Finance Derivative Awards

Submit Your nomination now to awards @financederivative.com

Working with an expert provider that knows the local rules and regulations is paramount when a data center moves jurisdiction. Outsourced providers give access to a suite of services in a new location including order routing, market data and the procurement, installation and management of trading infrastructure. They can make the process of moving location less stressful and more efficient, with a single point of contact and 24-hour access to both technical and exchange specialist expertise.

occupancy down to a single rack unit, which means businesses can lease exactly the right amount of space for their trading infrastructure requirements and scale up and down as required.

sometimes running into tens of gigabits.

The benefits are many for a trading firm that choses to work with a provider that can easily accommodate these requirements and handle data bursts, including those seen on many recent occasions due to market volatility caused by medical, political and economic events.

A

“DIY”

approach versus a managed service mode

A do-it-yourself (DIY) approach is when a company arranges the installation, configuration, connectivity and monitoring of its data center equipment within the space leased from the exchange in-house. There are several things to consider when using a DIY approach, including how much space and power is required now and for the future, as well as network connections, bandwidth, latency, market data feeds and the need to connect to additional third-party data or services.

Managed service providers offer space within the data center to their clients. This can be divided into cabinets and racks, as well as the opportunity to benefit from fractional

Connectivity, market data, power and space costs can quickly add up to tens of thousands of dollars per month. On top of these fees are additional capital costs for equipment and staffing for support and maintenance. Trading organizations looking to colocate need to seriously consider if they have the skills, understanding, resources and bandwidth in-house. For most, the answer will be ‘no’, and they will need to use a managed service provider to architect, install, configure, manage and support their collocated trading infrastructure for the best outcome.

Future-Proof

There is a significant advantage to be able to future-proof a trading infrastructure by working with a provider that has experience in managing vast amounts of raw market data, can support multicast requirements and is able to offer scalable solutions. As traders diversify, their market data needs can place excessive network capacity pressures on their infrastructure,

Jeff Mezger is Vice President of Product Management at TNS with responsibility for its managed services for the financial industry. TNS’ infrastructure brings together over 2,800 financial community endpoints to address the needs of financial market participants worldwide. Traders using the company’s Managed Hosting solution benefit from global point-of-presence footprint and extensive existing onnet connections, including uninterrupted access to more than 60 exchanges with local, physical support around the globe. For more information visit tnsi.com

Jeff Mezger, VP of Product Management TNS

35 Wealth Management

Improving Customers’ Experience at Banks using BIOMETRIC TECHNOLOGY

You wouldn’t have to cast your memory so far back to a time when the bank manager would sit across from a new customer. The manager would then ask the customer to hand over a form of a physical photo ID and a paycheck to prove they are whom they say they are.

While a small number of banks still prefer physical banking for both identification and financial transactions, the majority of today’s onboarding process can take place without either the customer or the banker having to physically interact. Through modern technologies such as biometrics, artificial intelligence and connected databases, customers' banking experience have become faster and more convenient.

With 61% of customers claiming that they are more likely to use contactless transactions and expect contactless experiences. The demands that

customers are making are clear. They expect exemplary customer experience. Where possible they want to minimise physical interactions and quick results.

The question is, is this possible to be done safely?

Safety comes first

Unlike other sectors, the data and information passed between the customer and the bank are very sensitive. With the Know-Your-Customer (KYC) regulations that banks have to follow and the sensitive customer information customers give to banks, both

36 Technology

financial and personal data must be safe. Especially during the onboarding process.

Between the years 2018 and 2022, financial data breaches accounted for 153.3 million leaked records. Increasingly, bad actors are hacking and accessing customers' data. Banks can prevent customers' data from being hacked via the use of biometric authentication. Because each specific customer's biometric makeup is unique to them as a person, it will be very hard for hackers to be able to access customers' data. So, if a bank requires a thumbprint scanner,

to access data, due to each individual's biometric makeup, their encrypted data will be hard for hackers to access.

We all know that one aspect of providing a good customer experience for banking customers is making sure that the customers' data is kept safe. However, with society becoming used to frictionally experiences can banks afford not to have contactless experiences?

Contactless experiences for the win

The COVID-19 pandemic changed the mindset of people across the world. Where

previously people wouldn’t mind physical interactions, people have become accustomed to contactless experiences due to imposed lockdowns and the advancements made in technology. The financial sector especially has seen an increase in customers reverting and wanting contactless experiences. A study by NCR found that 70% of their participants increased their use of digital banking. They also stated it as their preferred way of banking.

Now more than ever customers preferred way of banking is contactless. This contactless

37 Technology

Move forward with us and invest in the future

Looking to invest in a fund that really matters? Give your assets every chance to grow, while helping the world move forward. Thanks to thematic investing, you can do just that by investing in companies of the future.

Want to learn more about thematic investing?

38

experience can be achieved by having an onboarding process that is digital which then enables online banking to take place. Having an onboarding system in the same app as the banking platforms offers the customer ease and simplicity. As a result, the enrolling process is as easy as installing an app and completing an online form, the customer will not only feel more in control of their banking experience but will potentially feel less pressure than physical banking. There is less of a need to cultivate interpersonal relationships. The customer’s experience is less based on the training or disposition of a banking relationship manager.

As with most things in life, it comes at a cost and contactless technology is no different. Yet still, the question has to be asked, are their banking institutions investing in this?

We can all reap the benefits

Much has been made about the cost of investing in technology. In an economic climate where

the cost of living is rising for all and inflation is predicted to steadily increase no bank can afford to be wasting money. Still, in the long run, investing in contactless technology has its financial benefits.

Traditional banking, whether it’s onboarding or physical transaction of money is driven by manpower and this requires specialists to be paid. Even in a system with an online banking portal, human specialists are needed to process and verify the information gathered.

This can be costly not only in wages but also in training and upskilling when legal or regulatory changes happen in the industry.

Process such as digital onboarding which is automated so that much of the ongoing human cost is mitigated, to the degree that the need for human interaction is eliminated.

Even though technology is becoming more advanced, a small fraction of banks are still refusing to embrace contactless technology. Could the

decision of banks to not implement contactless technology, affect their future?

Banking in the future

Banking today is different from what it was in previous decades. Where previously you may have been able to have multiple opportunities to make a good impression on the customer, you only have one now. As like in other sectors, contactless technology that helps enhance security and create better seamless experiences are paramount.

Biometric authentication technology such as faceless identification, voice recognition and fingerprint ID can do this. Allowing customers to bank, without physically being in the bank is the future of banking as we know it.

Stewart, VP of EMEA Incode

39 Technology

Andre

SELLING RISKhow innovation can be brought to the front at insurers

Jay Chitnis,

Senior

Business Consultant at Endava, looks at how a traditionally riskaverse industry can start to embrace innovation and keep evolving.

Innovation has been one of the key topics of the last decade. It seems like every company, whether they’re working in technology or not, has to brand itself as innovative, making this the very cornerstone of their marketing and sales outreach. But, with this drive for innovation, are we at risk of it becoming an empty buzzword, with no true

meaning, or even worse, could innovation simply become a justification for spending money on endless projects with no true goal or definition? How can we get back to the real meaning of the word, making sure that companies are truly remaining at the cutting edge and continuing to push boundaries?

Today’s consumers and businesses expect more. They’re not content with inefficient processes that simply ‘get the job done’. Instead, they’re looking for their service providers to bring renewed experiences that are simple and intuitive. If

a company cannot provide a dynamic and evolving sense of innovation then they run a very real risk of both losing existing customers and failing to win more and grow their customer base. This can be fatal for companies but, if an entire industry is perceived to be stagnating, then this can mean that people are hesitant to engage with it unless they have to, losing sight of the actual benefits and importance of the sector and damaging its reputation as a whole.

In fact, the insurance sector makes for a very interesting

40 Wealth Management

case study. The sector has a reputation for being ‘old’, ‘traditional’ and even, sometimes, ‘stuck in its ways’. What’s more, insurance can be seen by its users as a ‘necessary evil’, rather than a positive force. While there have undoubtedly been innovations, such as telematics in the car insurance industry and the first moves to embed insurance within other services, the industry has been slower than others to embrace innovation.

So what are the barriers? At the heart of the matter is a very simple irony. For a sector that deals so heavily in risk, it’s actually very risk averse. Nowhere is this clearer than in the struggle over innovation. If innovation is incorrectly positioned as an impetus or method for change without actually being tied to real objectives that show value then it can become linked to a strategic ambition rather than connected closely to real, tactical milestones, increasing a feeling of risk. Without tangible outcomes that prove the concept as the work progresses, the actual benefits can feel cloudy and unclear. This is often the case when a new strategy is put solely in the hands of innovators and success is expected but failure will damage the whole strategy. The insurers that are able to be successful innovators are those that see it as a way of

defining strategy—taking risk first and renewing processes or embracing new tech to test a strategy and then setting key, tactical milestones to keep proving the concept.

Ultimately, innovation Directors must be able to articulate the objectives and set a proper timeline for delivery, as well as demonstrate the benefits and value. In industries like insurance, where risk is not always well-received, if a new project isn’t clear in its deliverables and showing real value—and these aren’t communicated—then it can be very difficult to get projects off the ground. If timelines are long and objectives aren’t clearly defined, it’s not hard to see how board members might want to stick to business as usual, particularly when insurance customers are already essentially a captive audience—insurance is needed throughout much of our daily personal and corporate lives.

At the same time though, innovation is critical to keep industries current and deliver real value to their customers. A lot relies on the people that are delivering projects. Innovation Directors and leaders must be prepared to talk to the concerns that others may have. They must also be doers and able to scrub in and lead the way, particularly when working closely with sales teams that

will have technical questions and need proper guidance on how innovations should be sold and implemented. They must also carefully consider their projects and methodology and set clear strategies, goals and achievable milestones to prove the project on an ongoing basis.

For anyone seeking to innovate, approaching such projects as ‘digital acceleration’ may be the key. Digital acceleration seeks to keep companies at the cutting edge in the long term, while also being agile in the short and delivering value as fast as possible. These projects may be multi-year but at their heart, they set achievable, bitesize milestones, able to pivot to meet evolving needs and the demands of a rapidly-changing operating environment.

While it may not be possible to de-risk innovation entirely, properly defining and designing projects to more properly fit into an already-understood framework may help explain them and reassure risk-averse board members and investors.

Jay Chitnis, Senior Business Consultant Endava

Jay Chitnis, Senior Business Consultant Endava

41 Wealth Management

How is Banking-as-a-Service helping retailers lead the market?

Retailers once navigated a much smaller world before the COVID-19 pandemic kickstarted mass migration to online channels. Even those ahead of the curve could only serve customers locally via an online shop. Now, digital platforms allow retailers to cast their nets much wider and enable them to do business with the whole world.

Less than a year ago, a KPMG study found that a strong majority of retail CEOs (74%) aim to proactively disrupt the market before it is disrupted by competitors. So, to sustain growth internationally, retailers’ next challenge is to meet local needs with disruptive experiences, but on a global scale.

- James Butland

Where digital platforms like Amazon and Flipkart have already brought opportunity to retail, how will they now help the industry satisfy a growing appetite (and need) for frictionless and seamless financial services worldwide?

42 Banking

Take advantage of banking technology innovation

Open banking, embedded finance and Banking-as-a-Service (BaaS) are enabling consumers to interact with financial services beyond traditional functions like withdrawing or depositing cash in-branch. For example, purchasing items on your phone now takes one or two clicks and cashing a cheque can be done on-the-go simply using a smartphone camera.

By adopting an embedded finance model, businesses can create a holistic experience for their customers, wherein they can easily send and receive money in near real-time, without any sacrifice to the overall user experience.

With BaaS, retailers and online merchants can now easily take advantage of embedded financial services without having to source the skills to manage back-end technology in-house. They can do this via digital platforms which integrate tailored modules and offer financial capabilities that streamline the entire financial process for consumers.

From a business point of view, banking technology has introduced even greater advantages. Aside from creating operational efficiencies, digital platforms that integrate embedded finance, BaaS and open banking capabilities have allowed businesses to become location agnostic. That means they can do business with anyone, anywhere in the world, no matter the size or location of their business. Adding other internationalisation features via the digital platform, such as localised payment methods, offer yet more ways to engage with customers and aid expansion in new markets.

Understand the post-COVID impact on retail

Despite global supply chain crises, inflation and ongoing uncertainty, there are now more tools available than ever before to help businesses grow, and it is no coincidence. To understand how they can use these tools to benefit their business, retailers must first understand what these tools have to offer and what pain points they address.

From the consumer’s perspective, one key shift from the pandemic has been trust. Customers’ perspectives on trust have changed throughout COVID because it has altered purchasing habits by forcing people to shop online or use a digital service which they might not have done before the pandemic.

The biggest barrier to innovation is trust, but once customers see the benefit, more opportunities inevitably arise. Specifically, older generations who do not take as many technological risks as their younger counterparts will gradually adopt services that are simple, convenient and familiar.

Furthermore, digital platform financial services are not just for the consumer. The issue of trust often trickles up the ladder to the vendor-user too. Digital platform providers need to also consider the person selling the product to solve retailers’ pain points and deliver ease of use to scale. In doing so and implementing BaaS, improvements to the user experience filter through to the end customer who will return as a result.

43 Banking

Stay ahead by leveraging technology and partnerships with innovative fintechs

As a traditional retailer, merchants need to accommodate key consumer drivers such as price, speed, quality. In today’s digital age, retailers need to also be seen as the frontrunner in terms of customer service, preferred payment methods and disruptive user interface (UI).

If customers can find a slicker, more convenient shopping experience elsewhere, retailers will lose out on their business.

On the international retail stage, consumers want a local shopping experience online. To achieve it, retailers need

to incorporate local payment methods plus preferences, local currencies, and any financing options that are frequently used in that market.

By accessing various functionalities and partnering with a wide network of global financial services providers via a digital platform, retailers can open up a wider customer base for the long-haul. If retailers can provide familiarity, a trusted payment method and a transparent price, they will ultimately convert more people at checkout, anywhere in the world.

Continue to lead the market

From financial uncertainty to

upticks in digital fraud, more challenges lie ahead for retailers in the current economic climate. However, those that were able to use innovations to their advantage are entering a new stage of global retail that comes with boundless opportunity. To fully immerse your business, staff and customers in the possibilities of global trade, embedded finance that takes the friction out of payments is the way to go. With financial disruption at their fingertips, any retailer can meet, or indeed lead the market.

James Butland, VP of Financial Partnerships, EMEA at Airwallex

44 Banking

Trade Your Way With

At home or on the go – with AvaTrade trade comfortably from anywhere! And you can also get trade protection with the unique AvaProtect™!

success factors for the digitalisation of the financial sector

Many services from banks and insurance companies are already available online and are popular with individuals and businesses. However, the fact that accounts can be managed online and claims can be settled digitally is just one facet of digitalisation in the financial sector. Customer

expectations and regulatory requirements continue to evolve and new competition such as fintechs, comparison portals and large internet companies continue to disrupt the sector, driving the need for accelerated digitalisation efforts.

Maintaining focus on developing better end-to-end digital

processes will help financial institutions and insurance companies keep pace. Digital interfaces for customers, partners and services are needed to ensure companies can continue to deliver innovation. We have identified six strategic considerations that can help guide your digitalisation journey.

46 Finance

6

1. Digitalisation is not just a “technology issue”

Choosing the right technologies is central to successful modernisation, but it is only one component among many. Corporate processes and culture also need adapting in parallel.

Digital solutions make new and more open collaboration possible and present opportunities for process improvements via automation across departmental and company boundaries.

Employees need the freedom and support to try out new solutions - and sometimes to fail. Making sure to share knowledge about mistakes and successes lets other teams build on the experiences and innovate more effectively.

2. Lead from the ground up as well as top down

Management certainly needs to be a driving force behind digital transformation, not least by providing budget and giving employees the freedom they need to get the job done. However, digitalisation is not just a matter for leadership.

Comprehensive transformation requires everyone to pull together and participate. Front line workers are often the best source of fresh ideas because they regularly encounter internal processes and applications as well as the company’s products and services, and therefore know best where the problems are and where improvements can be made. Continuous communication from management about the opportunities of modernisation including how it will make everyday work easier will help motivate people to get involved. Open communication also helps alleviate the fears that come with change, for example around job security and workload.

3. We can't do it alone

External partners can contribute empirical value to strategically important digitalisation projects. As well as bringing practical experience and technology implementation knowledge to the table, partners can also provide support as coaches around internal change processes. They can help identify and remove structural barriers and promote agile collaboration between departments.

Working closer with third parties opens up a new world of innovation, particularly around customer experience. Using open APIs, an ecosystem of diverse companies can work together to create new digital offerings. To take one example, the financial services and aviation industries can join forces to enable automated proactive claims settlements in the event of flight delays or flight cancellations. The scope is endless, and if you stay focused on your core business – what is it that you do that no one else can –you can make informed decisions on what to build yourself, where to use external people to solve a problem, and what areas need third party software to do the job. Entrusting partners with those tasks outside of your core business will enable you to focus on the exciting innovation opportunities rather than keeping the lights on.

47 Finance 47

4. There is more to cloud than migration

Financial services organisations often focus on migrating legacy workloads to the cloud to help reduce IT costs. Looking beyond this use case, cloud-native application development tools and cloud platforms provide huge potential for simplifying infrastructure management and making it easier to develop and scale applications both old and new.

With flexibility being a major consideration, hybrid cloud is becoming a widely used cloud strategy – meaning an integration and orchestration layer that provides consistency and security across different clouds. Data from Red Hat's 2022 Global Tech Outlook Report shows 30 percent of the 1,300 IT executives surveyed rely on a hybrid cloud strategy and 13 percent on a multi-cloud approach, meaning the use of multiple public cloud providers. The dynamic use of private and public clouds is also necessary for incoming regulatory requirements such as the Digital Operations Resilience Act (DORA), incorporating the need for a future-ready Cloud Exit Strategy.

5. Digitalisation needs customer focus and crossdepartmental cooperation

Banks and insurance companies often start by digitalising existing products and processes. This is understandable because they tend to work in silos – products, risk management, claims processing, technology, customer service and so on. However, it is just the tip of the iceberg.

Innovative solutions emerge when cross-departmental teams gather together and put the customer at the centre. For example, in the world of corporate banking, a bank might be applying data analytics from customer onboarding verification checks to help boost customer satisfaction. The next step is looking at how these insights can be used by other teams such as sales, which might be to make timely offers around financing for company mergers or D&O (Directors and Officers) insurance policies for new management.

6. Digitalisation is a continuous process

It would be naive to assume that digitalisation has an end point. Technologies are constantly evolving and will always bring opportunities to unlock new areas of business. More than just helping meet regulatory requirements and reducing costs, organisations are increasingly recognising that there are limitless possibilities for innovation if they can stay agile and flexible. This entails an ongoing mission of adapting and automating processes and nurturing a culture of open communication and collaboration, inside the organisation and beyond.

48 Finance

Nikolai Stankau, Director, Business Development, EMEA Financial Services, Red Hat

China Asset Management Company

With $252 billion in total assets under management*, China Asset Management Company (ChinaAMC) is one of the largest and most established asset managers in China. Founded in 1998, it serves 198 million retail investors and 105,000 institutional investors*, including global institutions such as sovereign wealth funds, central banks, banks, family offices, and asset management and securities companies across Europe, America, and Asia.

*Source: ChinaAMC, data as of September 30, 2022. Website: https://en.chinaamc.com CONTACT US