4 minute read

Investing in Fallen Angels during COVID-19

By Philip Messow

The pandemic has caused market turbulence on an unprecedented scale. Yet there are strategies which have been able to generate added value for investors, such as investing in Fallen Angels.

Advertisement

The term Fallen Angels refers to bonds of issuers whose creditworthiness has deteriorated and whose credit rating has thus been downgraded from investment grade to high yield. Downgrades can trigger massive overreactions by investors, especially in times of significant market tension and stress. As a consequence, such bonds may temporarily trade below their fundamental value. This overreaction can be systematically exploited within the framework of high yield products.

SALES PRESSURE DUE TO DOWNGRADES

The downgrade of a bond to the high yield universe often leads to forced selling: institutional investors that are obliged to comply with regulatory requirements with regard to credit ratings, as well as ETFs tracking an investment grade index, are forced to sell such bonds. However, the high yield market, with a market capitalisation of €1.7 trillion as of 31 March 2020, is significantly smaller than the investment grade universe, with a market capitalisation of €10.2 trillion. Hence, sales pressure may drive the market price of a bond below its fundamental value.

Downgrades to high yield ratings occur more frequently during an economic downturn. For instance, our analysis shows that there were on average only nine Fallen Angels per month during the period from January 2010 to February 2020, compared to 106 downgrades in March 2020 alone. This demonstrates that Fallen Angels are predominantly influenced by systematic risk factors. Idiosyncratic risks play a lesser role here. Yet during times of crisis, it’s especially difficult to find new buyers in the stressed high yield market. This is due to the fact that many investors’ capacity to assume risk is reduced significantly when they are faced with strong market turbulence. It’s fair to expect the extent of temporary undervaluation of Fallen Angels to be much larger during a crisis.

FOCUS ON ENERGY AND MANUFACTURING SECTOR

The present analysis looks at the performance of USD-denominated Fallen Angels for a period preceding the COVID19 crisis (January 2020 to February 2020) and during the first

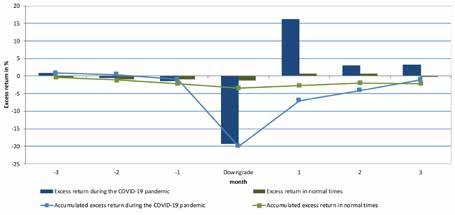

Figure 1: Relative and accumulated performance of fallen angels

Comparison to a reference sample based on similar credit rating, duration and sector for the period from December 2019 to June 2020 (COVID-19) and for the period from January 2010 to February 2020 (normal market). Sources: Intercontinental Exchange, Bloomberg and Quoniam.

month of that crisis (March 2020). For this purpose, we have focused on corporate bonds which were downgraded from the ICE BofA Global Corporate Index to the ICE BofA Global High Yield Index. We analysed a total of 1,133 Fallen Angels, with 106 downgrades which occurred in March 2020.

As a consequence of the COVID-19 pandemic, the energy sector and manufacturers of cyclical consumer goods have been particularly hard hit by downgrades. Together, these two sectors account for almost 90% of all Fallen Angels during the period under analysis.

We have calculated the average excess return1 of Fallen Angels for a sevenmonth period, covering the three months prior to the downgrade, the month during which the downgrade occurred, and the subsequent three months. In addition, we have analysed performance differences between Fallen Angels which were downgraded during March 2020 – at the initial peak of the COVID-19 pandemic – with those downgraded during the period prior to the pandemic (Jan 2010-Feb 2020). We have looked at the relative return of Fallen Angels versus comparable bonds. The reference group consists of bonds with a similar credit rating, duration and sector.

TEMPORARY UNDERVALUATION CAN BE SIGNIFICANT

Figure 1 illustrates the results of this analysis: it shows that holding Fallen Angels during the month of the downgrade resulted in an average negative relative return of 1.3% in normal times and 19% during the COVID-19 pandemic. In both observation periods, Fallen Angels experienced a significant counter-movement after the downgrade and were able to largely recoup the initial loss over the observation period. This is an indication for an overreaction that occurs in the event of a downgrade, leading to a temporary undervaluation when a bond is downgraded from the investment grade universe to the high yield universe. During the COVID-19 pandemic, both the average negative return of comparable corporate bonds and the counter-movement were much larger in size. This indicates that in the course of the March market collapse, there were hardly any investors prepared to work against the tide.

Fallen Angels have experienced particularly strong divergence from their fundamental value due to the COVID-19 pandemic. The temporary undervaluation has turned Fallen Angels into an important segment of the high yield universe for systematic strategies. One way to make these bonds accessible for investors is to integrate Fallen Angels into high yield products. « • Investing in Fallen Angels can be a beneficial strategy in times of market disruption. • The downgrade of a bond from investment grade to high yield often leads to forced selling. • Downgrades occur more frequently during an economic downturn: 106 downgrades in March 2020 alone. • Energy sector and manufacturers have been hard hit by downgrades during the COVID-19 pandemic so far. • Many Fallen Angels experienced a significant counter-movement after the downgrade and were able to largely recoup the initial loss. • Data indicate an overreaction that occurs in the event of a downgrade, leading to a temporary undervaluation when a bond is downgraded. • Fallen Angels have experienced particularly strong divergence from their fundamental value, due to the

COVID-19 pandemic.

1 We have calculated excess return over government bonds with the same duration.