Email-based, real estate fraud schemes are on the rise. One common scenario is altering wiring instructions with the intention of rerouting funds.

Keeping this in mind, First American Title is changing the way we receive payment information. It is imperative that we are familiar with the people in our transactions.

RELYING ON EMAIL ALONE IS NO LONGER AN OPTION.

Fraudsters often use email to send falsified wire instructions to unsuspecting victims. Please warn your buyers and sellers to only follow wire instructions they receive personally from First American Title.

Additionally, we will not accept disbursement instructions for seller or buyer funds via email OR from any third party (attorney, real estate agent, etc).

If your buyer or seller receives alternative wiring instructions that appear to be from First American Title, make sure they contact their escrow officer at a trusted phone number for confirmation.

Know that our wiring instructions do not change so any communication is suspect. Our banking institution is First American Trust.

IN SHORT – wire instructions will not be accepted by email. New wire instructions must be hand-carried or uploaded to the First American Secure Portal.

Thank you for joining First American Title in fostering a secure real estate transaction process. Have questions or concerns? Please contact our office or your escrow officer.

Welcome to the home-buying process. Throughout this process, you can count on First American Title to guide you smoothly through your transaction and provide expert answers to your questions. We are happy to serve you.

First American Title’s professionals are proud to provide the title insurance that assures people’s home ownership. Backed by First American Title Insurance Company, your transaction will be expertly completed in accordance with state-specific underwriting standards and state and federal regulatory requirements.

First American Title is the principal subsidiary of First American Financial Corporation, and one of the largest suppliers of title insurance services in the nation. With roots dating back to 1889, we’ve served families for generations.

First American Title has a direct office or agent near you, offering convenient locations throughout Arizona. We also have an extensive network of offices and agents throughout the United States, and internationally.

First American Financial Corporation offers more than title insurance and escrow services through its subsidiaries. Our subsidiaries also provide property data, title plant records and images, home warranties, property and casualty insurance, and banking, trust and advisory services.

Not sure if you should buy a home? The rent you pay could build equity in your own real estate. Do you realize how much you pay in rent over a period of years? The chart below gives you a total picture of what is happening to your money. The rent you pay adds up to a sizeable sum.

- No interest payment deductions

- Rental amount may increase at any time

- Landlord approval needed for any changes

- No capitalization; your money disappears forever

- Rental is temporary and is often subject to 30 day’s notice

- Deductions for your mortgage interest paid

- Mortgage payments could be fixed

- Decorate and make changes without prior approval

- The value of your property may increase in time

- Your house will become a home, not a temporary living situation; you are not at the mercy of a landlord

This formula is only a guide and not to be construed as actual lending calculations.

Contact your loan officer to determine more accurately what price range you should consider. Lenders abide by certain ratios when calculating the loan amount their customers can qualify for and the ratios vary by lender and loan program. Many use 28% of your gross monthly income as the maximum allowed for your mortgage payment (principal/interest/taxes/insurance or PITI); for your total monthly debt, the ratio is 36%. Total monthly expenses means PITI plus long-term debt (such as auto loans) and revolving/credit-card debt. Do not include other expenses such as groceries, utilities, clothing, tuition, etc., to calculate this ratio.

An estimate of value of property resulting from analysis of facts about the property; an opinion of value.

The borrower’s costs of the loan term expressed as a rate. This is not their interest rate.

The recipient of benefits, often from a deed of trust; usually the lender.

Closing Disclosure form designed to provide disclosures that will be helpful to borrowers in understanding all of the costs of the transaction. This form will be given to the consumer three (3) business days before closing.

Generally the date the buyer becomes the legal owner and title insurance becomes effective.

Sales that have similar characteristics as the subject real property, used for analysis in the appraisal. Commonly called “comps.”

Occurs when the borrower becomes contractually obligated to the creditor on the loan, not, for example, when the borrower becomes contractually obligated to a seller on a real estate transaction. The point in time when a borrower becomes contractually obligated to the creditor on the loan depends on applicable State law. Consummation is not the same as close of escrow or settlement.

An instrument used in many states in place of a mortgage.

Limitations in the deed to a parcel of real property that dictate certain uses that may or may not be made of the real property.

The date the amounts are to be disbursed to a buyer and seller in a purchase transaction or the date funds are to be paid to the borrower or a third party in a transaction that is not a purchase transaction.

Down payment made by a purchaser of real property as evidence of good faith; a deposit or partial payment.

A right, privilege or interest limited to a specific purpose that one party has in the land of another.

As to a title insurance policy, a rider or attachment forming a part of the insurance policy expanding or limiting coverage.

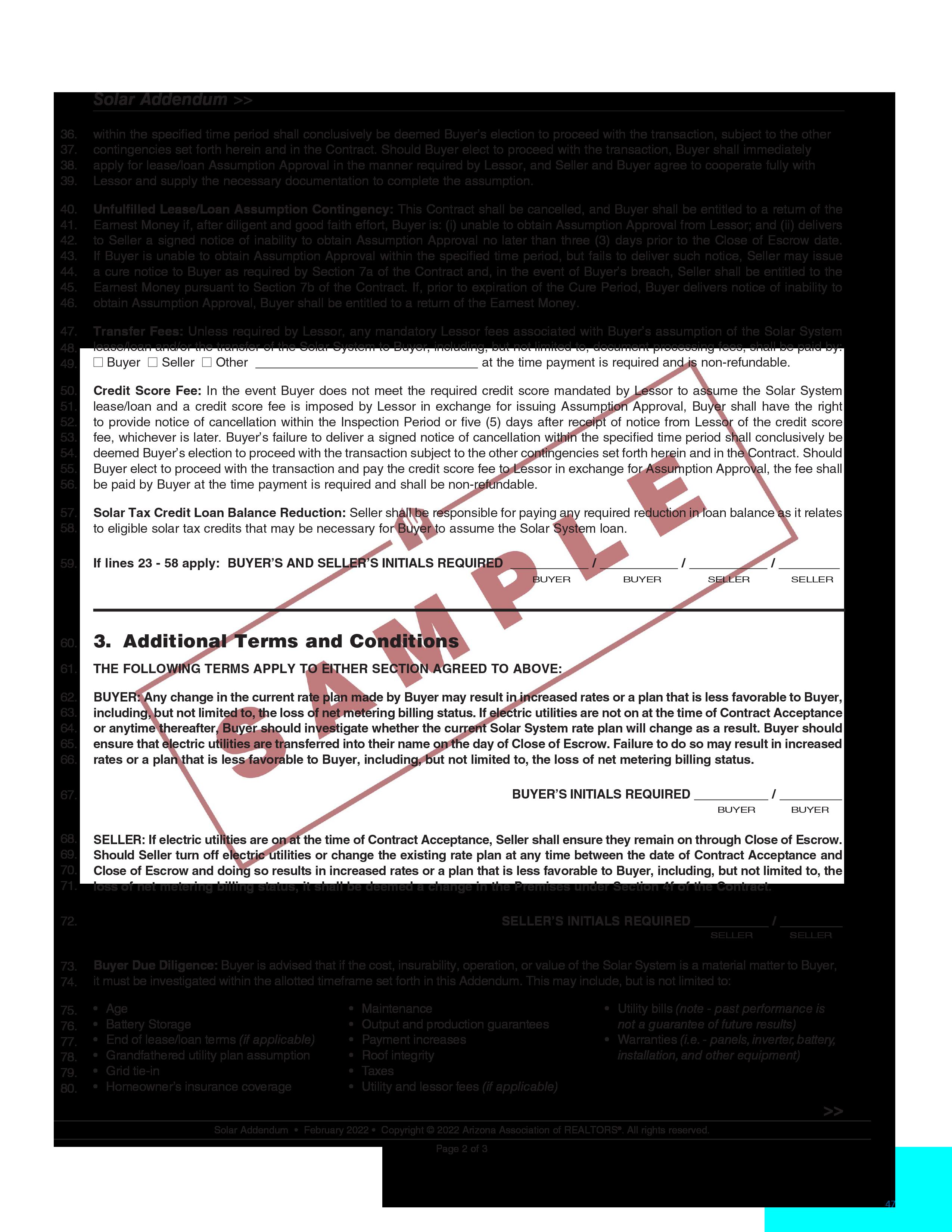

Real estate insurance protecting against fire, some natural causes, vandalism, etc., depending upon the policy. Buyer often adds liability insurance and extended coverage for personal property.

A trust type of account established by lenders for the accumulation of borrower’s funds to meet periodic payments of taxes, mortgage insurance premiums and/or future insurance policy premiums, required to protect their security.

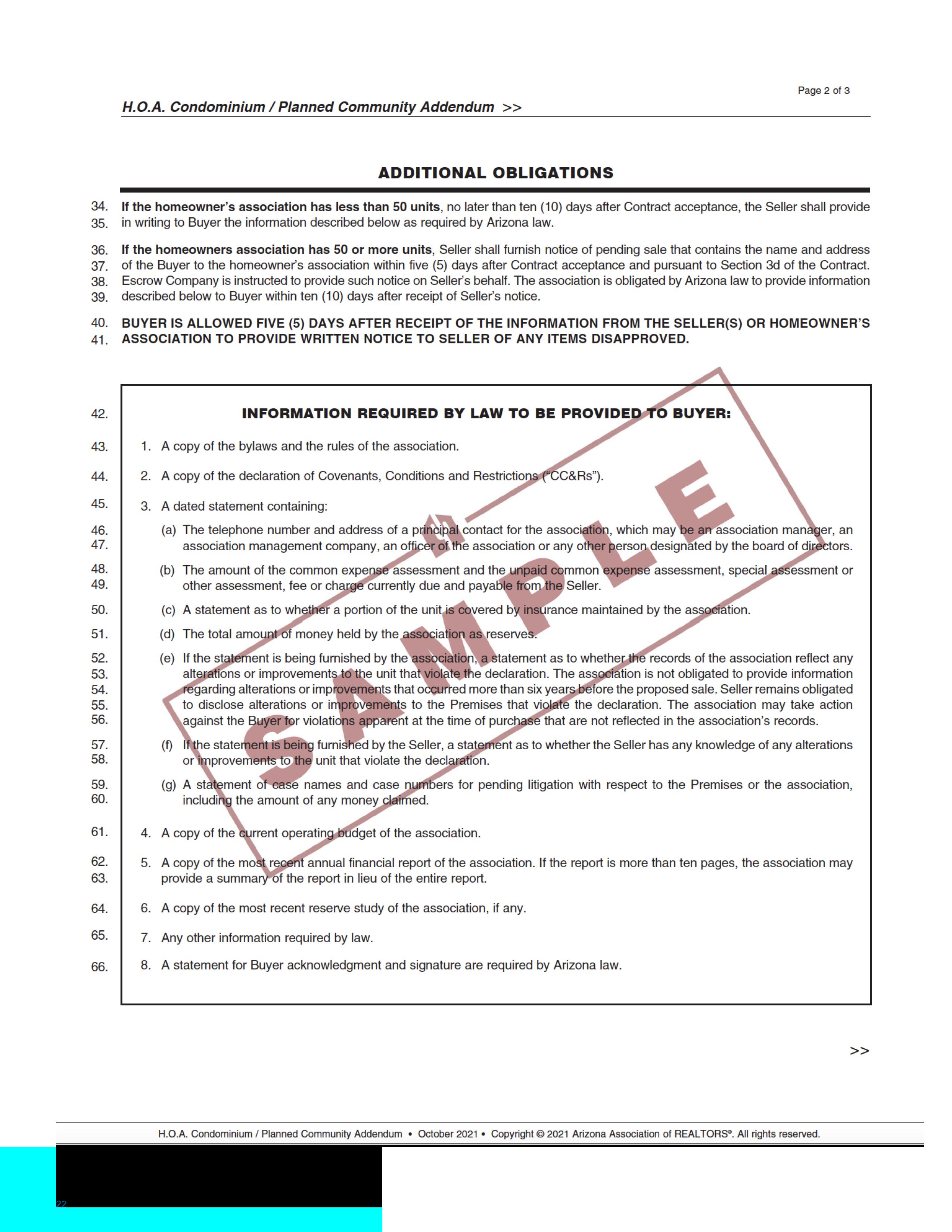

A description of land recognized by law, based on government surveys, spelling out the exact boundaries of the entire parcel of land. It should so thoroughly identify a parcel of land that it cannot be confused with any other.

A form of encumbrance that usually makes a specific parcel of real property the security for the payment of a debt or discharge of an obligation. For example, judgments, taxes, mortgages, deeds of trust.

Form designed to provide disclosures that will be helpful to borrowers in understanding the key features, costs and risks of the mortgage loan for which they are applying. Initial disclosure to be given to the borrower three (3) business days after application.

The instrument by which real property is pledged as security for repayment of a loan.

A payment that includes Principal, Interest, Taxes, and Insurance.

A written instrument whereby a principal gives authority to an agent. The agent acting under such a grant is sometimes called an “Attorney-in-Fact.”

Filing documents affecting real property with the appropriate government agency as a matter of public record.

Provides a complete breakdown of costs involved in a real estate transaction.

TILA-RESPA Integrated Disclosures

A REALTOR ® is a licensed real estate agent and a member of the National Association of REALTORS,® a real estate trade association. REALTORS ® also belong to their state and local Association of REALTORS.®

A real estate agent is licensed by the state to represent parties in the transfer of property. Every REALTOR ® is a real estate agent, but not every real estate agent has the professional designation of a REALTORS.®

A key role of the listing agent or broker is to form a legal relationship with the homeowner to sell the property and place the property in the Multiple Listing Service.

A key role of the buyer’s agent or broker is to work with the buyer to locate a suitable property and negotiate a successful home purchase.

The MLS is a database of properties listed for sale by REALTORS ® who are members of the local Association of REALTORS.® Information on an MLS property is available to thousands of REALTORS ®

These are the people who carry out the title search and examination, work with you to eliminate the title exceptions you are not willing to take subject to, and provide the policy of title insurance regarding title to the real property.

An escrow officer leads the facilitation of your escrow, including escrow instructions preparation, document preparation, funds disbursement, and more.

Congratulations on your decision to buy a home! It’s a challenging project, and there are many ways a professional can help. Here are some of the many ways you may benefit from working with a REALTOR ®:

Your REALTOR ® has thousands of homes to choose from through the Multiple Listing Service (MLS), so you’re more likely to find the home that’s just right for you and find it quicker. In fact, a majority of the homes for sale are listed by REALTORS® and aren’t available to you unless you are working with a REALTOR.®

Unfortunately, it’s true. Some transactions fall apart before closing. An experienced REALTOR ® may be able to resolve problems and see your transaction through to a successful closing.

New home subdivisions will welcome you and your REALTOR.® If you’re interested in buying a new home, take your agent with you on your first visit to each subdivision. Your professional REALTOR ® is an important source of information who can supply background on the builder, nearby subdivisions, and the local community.

You use a professional for your legal, financial and health needs. Why gamble on what may be your biggest investment without a professional at your side?

If you consider a “For Sale By Owner,” take your REALTOR ® along to help negotiate the contract.

You may have more protection from legal and financial liability, especially as real estate transactions become more complicated.

Your experienced REALTOR ® will negotiate and prepare the purchase contract for you and assist you throughout the escrow process.

The following home comparison chart is designed to help you remember the homes you visit and what you liked best and least about each one. Rate features or make notes that will help you determine what pleased or displeased you.

Remembering each home would appear easy, but it can quickly become confusing. Which home was near the school? Which one had the great pool? Did it have a family room? And how many bathrooms?

In the “Something Memorable” category, note something you think is unusual and memorable about each home, such as a stained glass window, fruit trees, a child’s playhouse. This will make it easier for you to recall the property later and refer to a specific address. And, last but not least, maybe the most important question, does this house feel like home?

Chooses a Real Estate Agent

Gets pre-approval letter from Lender and provides to Real Estate Agent.

Makes offer to purchase. Upon acceptance, opens escrow and deposits earnest money.

Finalizes loan application with Lender. Receives a Loan Estimate from Lender.

Completes and returns opening package from First American Title.

Schedules inspections and evaluates findings. Reviews title commitment/ preliminary report.

Provides all requested paperwork to Lender (bank statements, tax returns, etc.) All invoices and final approvals should be to the lender no later than 10 days prior to loan consummation.

Lender (or Escrow Officer) prepares CD and delivers to Buyer at least 3 days prior to loan consummation.

Escrow officer or real estate agent contacts the buyer to schedule signing appointment.

Buyer consummates loan, executes settlement documents, & deposits funds via wire transfer.

Documents are recorded and the keys are delivered!

Chooses a Real Estate Agent

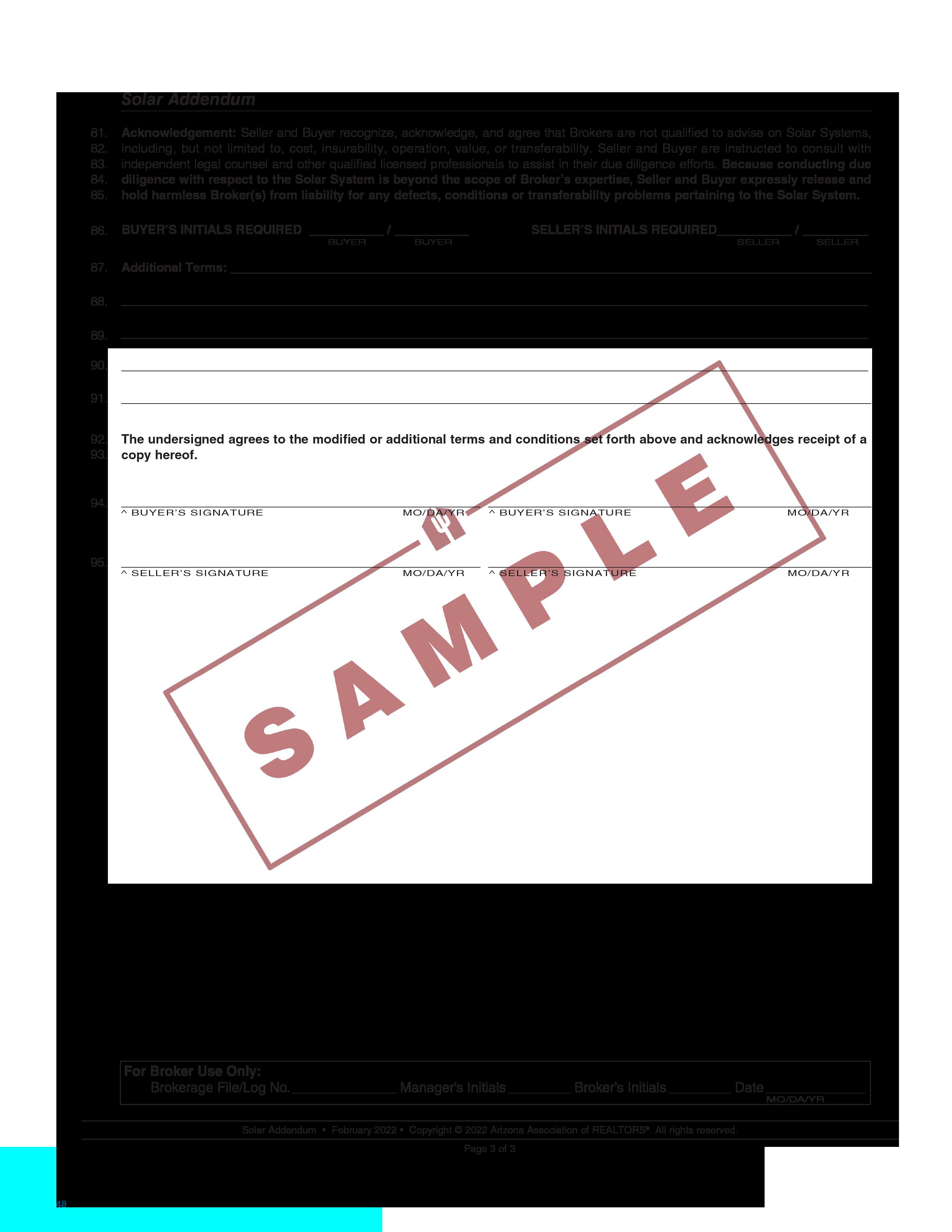

Accepts Buyer’s offer to purchase.

Completes and returns opening package from First American Title, including information such as forwarding address, payoff lender contact information and loan numbers.

Orders any work for inspections and/or repairs to be done as required by the purchase agreement.

Escrow officer or real estate agent contacts the seller to schedule signing appointment.

Documents are recorded and all proceeds from sale are received.

Upon receipt of order and earnest money deposit, orders title examination.

Requests necessary information from buyers and sellers via opening packages.

Reviews title commitment / preliminary report.

Upon receipt of opening packages, orders demands for payoffs. Contacts buyer or seller when additional information is required for the title commitment/ preliminary report.

All demands, invoices, and fees must be collected and sent to lender at least 10 days prior to loan consummation.

Coordinates with lender on the preparation of the CD.

Reviews all documents, demands, and instructions and prepares settlement statements and any other required documents.

Schedules signing appointment and informs buyer of funds due at settlement.

Once loan is consummated, sends funding package to lender for review.

Prepares recording instructions and submits docs for recording.

Documents are recorded and funds are disbursed. Issues final settlement statement.

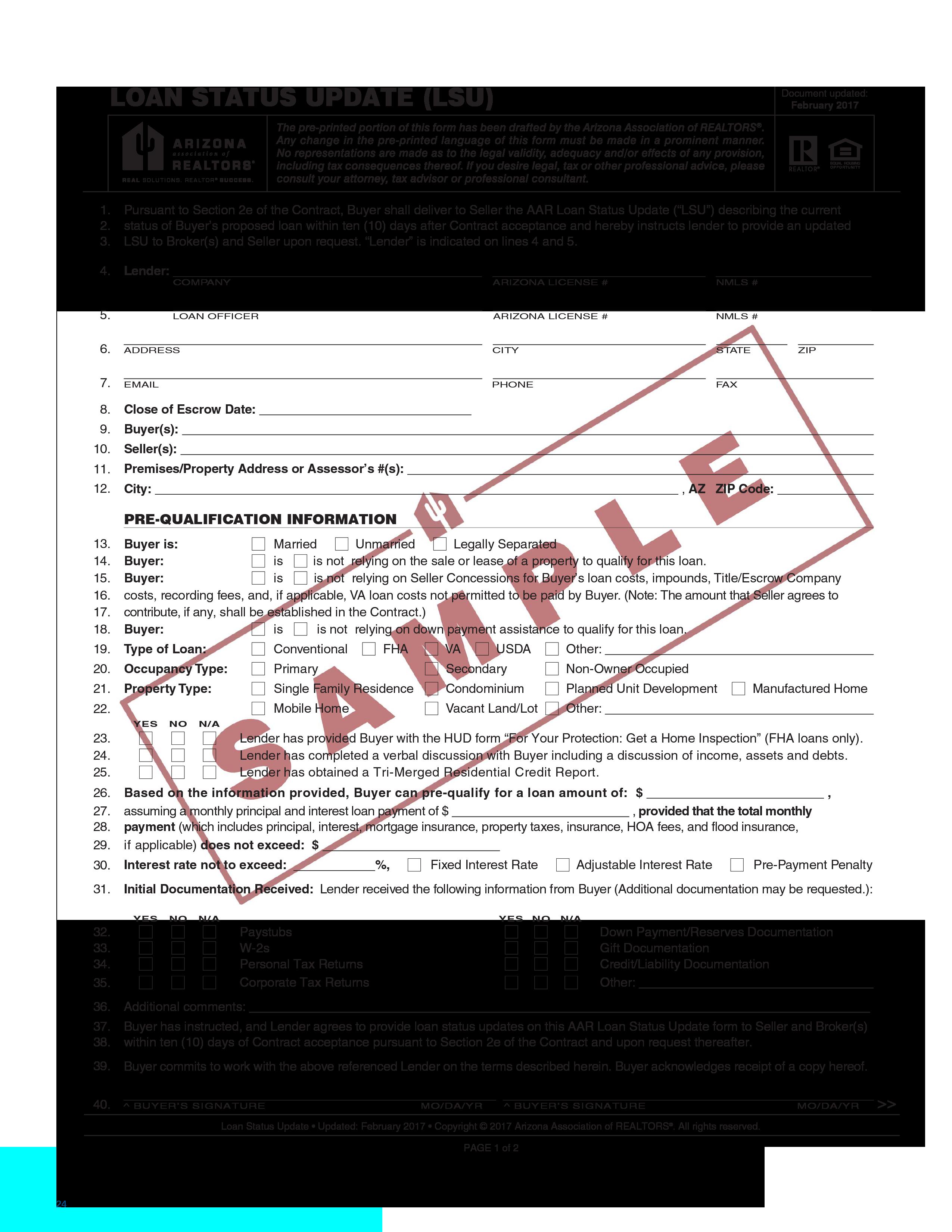

Accepts Buyer’s application and begins the qualification process. Provides Buyer with Loan Estimate.

Orders and reviews title commitment / preliminary report, property appraisal, credit report, employment and funds verification.

Collects information such as title commitment / preliminary report, appraisal, credit report, employment and funds verification. Reviews and requests additional information for final loan approval.

Underwriting reviews loan package for approval.

Coordinates with Escrow Officer on the preparation of the Closing Disclosure, which is delivered to Buyer at least 3 days prior to loan consummation.

Delivers loan documents to escrow.

Upon review of signed loan documents, authorizes loan funding.

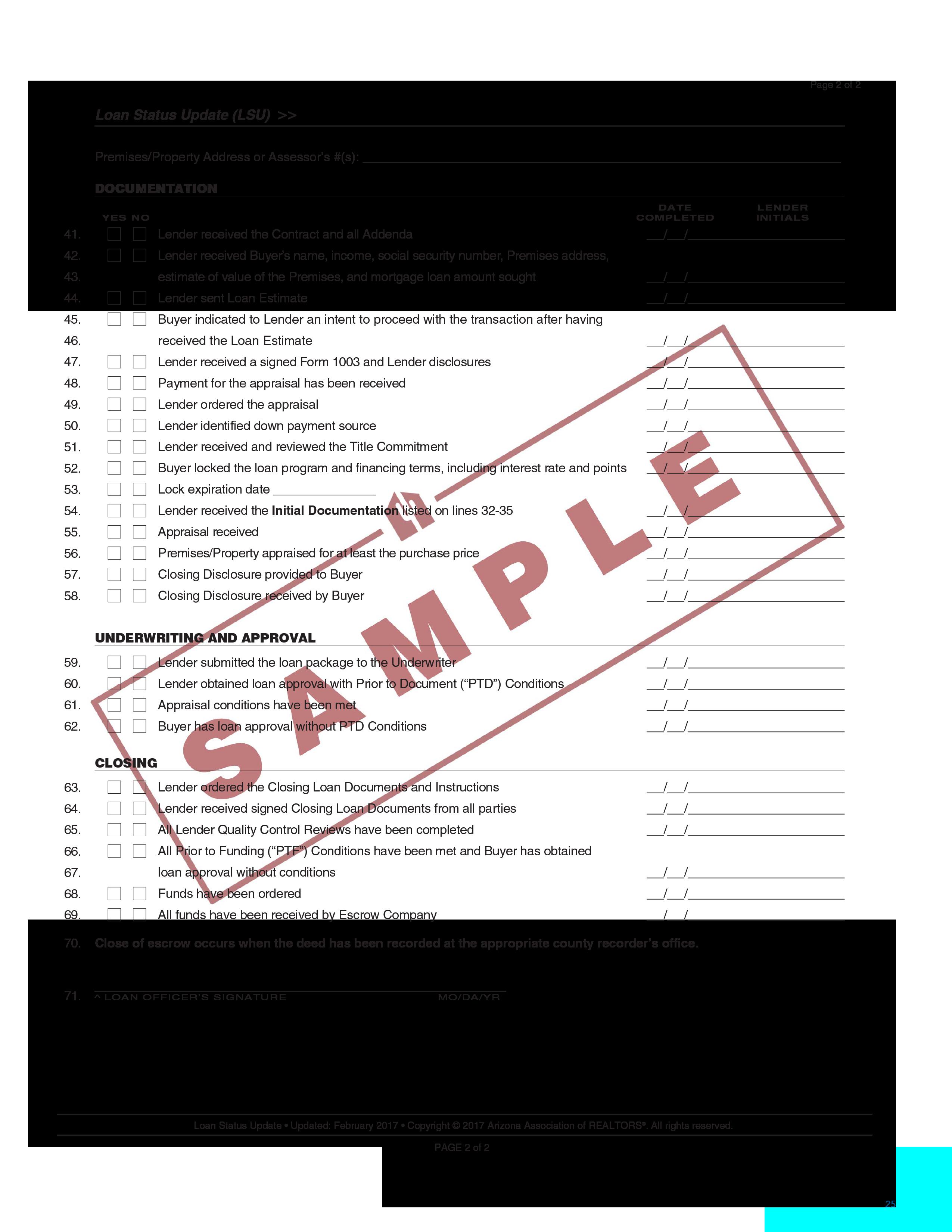

There are many sources for home loans including banks, credit unions, mortgage companies, and mortgage brokers. Your REALTOR ® may give you several names of lenders who have proven reliable in their previous transactions. Apply for your loan as soon as possible. In fact, it’s probably a good idea to know what you can afford before you begin looking for your new home. It can give you more bargaining power when negotiating with a Seller, especially in today’s market. A lender can prequalify you for a certain price range and help you avoid disappointment later.

and order an appraisal on the property you are buying. If your lender asks for additional items, please comply promptly with those requests to avoid delaying loan approval.

Hazard insurance covers the dwelling itself and is required by the lender to protect their “risk” in your home. Your lender or REALTOR ® will explain the necessary hazard insurance coverage to you. If you are buying a condominium, a master policy already exists which includes your unit—but it does not cover your personal belongings.

in the process, because this coverage must be provided so the lender can release loan funds to First American Title. Hazard insurance is one of the items frequently postponed until the last minute, and this can result in delaying the closing for a day or more. Order your insurance as soon as your loan is approved; then furnish your escrow officer with the agent’s name and phone number. When you talk with your insurance agent, be sure to ask about additional coverage in a homeowner’s policy to insure your personal belongings and to protect against liability for such events as injuries to visitors.

After loan approval and just prior to your planned closing date, the lender will send loan documents to First American Title, and your escrow officer will prepare an estimated settlement statement. This statement indicates what funds go where, and at this time your escrow officer can tell you how much money you need to bring to the closing appointment. Be aware that this amount may be higher or lower than previously estimated due to changes in such items as prepaid interest, prorated fees, courier fees, and impound accounts.

BE PREPARED TO PROVIDE SOME OF ALL OF THESE ITEMS TO YOUR LOAN OFFICER:

- Addresses of residences for last two years

- Social Security Number

- Driver’s License or other valid ID

- Names and addresses of employers for last two years

- Two recent pay stubs showing year-to-date earnings

- Federal tax returns for last two years

- W-2’s for last two years

- Last two months statements for all checking and savings account

- Loans: Names, addresses, account numbers, and payment amounts on all loans

- Real estate loans: Names, addresses, account numbers, and payment amounts on all loans for other real estate you own

- Credit cards: Names, addresses, account numbers, and payment amounts on all credit cards

- Addresses and values of other real estate owned

- Value of personal property. Your best estimate of the value of all your personal property (autos, boats, furniture, jewelry, television, stereo, computer, other electronics, etc.)

- For a VA loan, Certificate of Eligibility or DD214s

- Divorce decree if applicable

- Funds to pay upfront for the credit report and appraisal

- Letters of Explanation regarding credit inquires or special circumstances

Adjustable or variable rate refers to the fluctuating interest rate you’ll pay over the life of the loan. The rate is adjusted periodically to coincide with changes in the index on which the rate is based. The minimum and maximum amounts of adjustment, as well as the frequency of adjustment are specified in the loan terms. An adjustable rate mortgage may allow you to qualify for a higher loan amount but maximums, caps and time frames should be considered before deciding on this type of loan.

A true assumable loan is rare today. This loan used to enable a buyer to pay the seller for the equity in the home and take over the payments without meeting any requirements. Assumables these days generally require standard income, credit and funds verification by the lender before the loan can be transferred to the buyer.

This program is designed to assist first-time buyers by offering a fixed rate and a low downpayment, such as 3 to 5% down. The program doesn’t require cash reserves, and qualifying ratios are more lenient; however, the buyer’s income must fall within a certain range and a training course may be necessary if required by the program. Ask your loan officer if this program is available in your community and whether or not you might qualify.

This simply describes a loan that is not obtained under any governmentinsured program, secured by investors. It could be a fixed rate or adjustable.

This program is beneficial for buyers who don’t have large downpayments. The loan is insured by the Federal Housing Administration under Housing and Urban Development (HUD) and offers easier qualifying with less cash needed upfront but the condition of the property is strictly regulated. The seller will pay a portion of the closing costs that would typically be paid by the buyer in a conventional loan program.

This loan has one interest rate that is constant throughout the loan.

People who have served in the U.S. armed forces can apply for a VA loan which covers up to 100% of the purchase price and requires little or no downpayment.

The escrow is the process of having a neutral party manage the exchange of money for real property. The escrow holder is known as an escrow or settlement officer or agent. The buyer deposits funds and the seller deposits a deed with the escrow holder along with all of the other documents required to remove all "contingencies" (conditions and approvals) in the purchase agreement prior to closing.

Once a purchase agreement is signed by all necessary parties, the agent representing the party who will pay the fee selects an escrow holder and the buyer's earnest money deposit and contract are submitted to the escrow holder. From this point, the escrow holder will follow the mutual written instructions of the buyer and seller, maintaining a neutral stance to ensure that neither party has an unfair advantage over the other. The escrow holder also follows the instructions of the Buyer's new lender, the seller's existing lender, and both parties' agents. The escrow holder ensures the transparency of the transaction, while carefully maintaining the privacy of the consumers.

Open escrow and, if instructed to do so, deposit your good faith funds in a separate escrow account

Order a title search to determine ownership and status of the subject real property

Issue a preliminary report and begin the process of eliminating the title exceptions you and your lender are not willing to take title subject to

Request payoff information for the seller's loans, other liens, homeowner's association fees, etc.

Coordinate with the buyer’s lender on the preparation of the Closing Disclosure (CD)

Prorate fees, such as real property taxes, per the contract, and prepare the settlement statement

Set separate appointments allowing the seller and you to sign documents and deposit funds

Review documents ensuring all conditions and legal requirements are fulfilled; request funds from lender

When all funds are deposited, record documents with the County Recorder's Office to transfer the subject real property to you

After the recordation is confirmed, close escrow and disburse funds, including Seller's proceeds, loan payoffs, etc.

Prepare and send final documents to all parties involved

The Title Industry & Title Insurance in Brief

Prior to the development of the title industry in the late 1800s, a home-buyer received a grantor’s warranty, attorney’s title opinion, or abstractor’s certificate as assurance of home ownership. The buyer relied on the financial integrity of the grantor, attorney, or abstractor for protection. Today, home-buyers look primarily to title insurance to provide this protection. Title insurance companies are regulated by state statute. They are required to post financial guarantees to ensure that any claims will be paid in a timely fashion. They also must maintain their own “title plants” which house duplicates of recorded deeds, mortgages, plats, and other pertinent county property records.

Title insurance provides coverage for certain losses due to defects in the title that, for the most part, occurred prior to your ownership. Title insurance protects against defects such as prior fraud or forgery that might go undetected until after closing and possibly jeopardize your ownership and investment.

Title insurance insures buyers against the risk that they did not acquire marketable title from the seller. It is primarily designed to reduce risk or loss caused by defects in title from the past. A loan policy of title insurance protects the interest of the mortgage lender, while an owner’s policy protects the equity of you, the buyer, for as long as you or your heirs (in certain policies) own the real property.

You pay for your owner’s title insurance policy only once, at the close of escrow. Who pays for the owner’s policy and loan policy varies depending on local customs.

Unlike other forms of insurance, title insurance emphasizes loss prevention for the insured. Title professionals perform labor-intensive work to find and address title issues that could threaten your homeownership. This upfront analysis gives you, as a policy holder, the peace of mind that your title risk has been effectively reduced. In contrast, insurance based on loss assumption (such as auto or property and casualty insurance) requires little upfront work because claims cannot be predicted or prevented, and premium funds are needed only in the event of an accident or other covered issue. These types of insurance also require annual coverage payments, unlike title insurance which is paid for only once upon the purchase of your home or establishment of a new mortgage.

There are many title issues that could cause you to lose your real property or your mortgage investment. Even the most careful search of public records may not disclose the most dangerous threat: hidden risks. These issues may not be uncovered until years later. Without title insurance from a reputable and financially solvent company, the ownership of your home could be jeopardized.

Here are some examples of title issues that may occur:

Deeds by persons supposedly single, but secretly married

Deeds in lieu of foreclosure given under duress

Marital rights of spouse purportedly, but not legally, divorced

Impersonation of the true owner of the land

Deeds by minors

Deeds by persons of unsound mind

Deeds to or from defunct corporations

Defective acknowledgments by notaries

Duress in execution of instruments

Erroneous reports furnished by tax officials

Forged deeds, releases, etc.

Mistakes in recording legal documents

Surviving children omitted from will

Administration of estate of persons absent but not deceased

Birth or adoption of children after date of will

Claims of creditors against real property sold by heirs or devisees

Deed of community property recited to be separate property

Deeds by foreign parties

First American Title’s Eagle Policy® for Owners provides expanded title coverage for natural persons who purchase one‐to‐four family residences, including condominiums. Coverages included in the Eagle Policy® for Owners offer the highest levels of protection available to homeowners.

Eagle Policy® for Owners benefits you won’t get with a Standard ALTA Owner’s Policy:

Post-policy Forgery

Post-policy Encroachments

Post-policy Adverse Possession

- Coverage extended to homeowner when someone claims to have the insureds title arising out of someone else’s continued use and occupancy

Post-Policy Easement by Prescription

- Coverage if another claims right to use a part of the insureds land as an easement because of continuous use over time

Building Permit and Zoning Violation

- Coverage for losses up to $25,000, after a small deductible, for building permit violations and forced remediation of zoning violations, and up to the full policy amount for forced removal of structures due to zoning violations

Expanded Access

- Expanded to include both vehicular and pedestrian access to and from land, based upon legal right

Encroachment of Improvements onto Easements and Set-backs

Subdivision Violation

- Homeowners are covered up to $10,000, after a small deductible, for protection against subdivision violations prior to purchase

Restrictive Covenant Violations

- Coverage provided for violations of restrictive covenants, occurring before homeowner acquired land if the homeowner is forced to correct or remove the violation or if the homeowner’s title is lost or taken because of the violation

Structural Damage for Mineral Abstraction or Easement Use

Encroachment of Boundary Walls and Fences

- Protection of up to $5,000, after a small deductible, for encroachments onto a neighbor’s land, onto an easement, or over a building set-back line

a)

b)

Requires a valid marriage between two persons.

Parties need not be married; may be more than two joint tenants.

Requires a valid marriage between two persons.

Each spouse holds an undivided one-half interest in the estate.

One spouse cannot partition the property by selling his or her interest.

Requires signatures of both spouses to convey or encumber.

Each joint tenant holds an equal and undivided interest in the estate, unity of interest.

One joint tenant can partition the property by selling his or her joint interest.

Requires signatures of all joint tenants to convey or encumber the whole.

Each spouse can devise (will) one-half of the community property.

Upon death the estate of the decedent must be “cleared” through probate, affidavit or adjudication.

Estate passes to surviving joint tenants outside of probate.

No court action required to “clear” title upon the death of joint tenant(s).

Each spouse holds an undivided one-half interest in the estate.

One spouse cannot partition the property by selling his or her interest.

Requires signatures of both spouses to convey or encumber.

Estate passes to the surviving spouse outside of probate.

No court action required to “clear” title upon the first death.

Parties need not be married; may be more than two tenants in common.

Each tenant in common holds an undivided fractional interest in the estate. Can be disproportionate.

Each tenant’s share can be conveyed, mortgaged or devised to a third party.

Requires signatures of all tenants to convey or encumber the whole.

Upon death the tenant’s proportionate share passes to his or her heirs by will or intestacy.

Upon death the estate of the decedent must be“cleared” through probate, affidavit or adjudication.

IDENTITY STATEMENT

You will be asked to fill out an Identity Statement that enables our title department to distinguish you from others with identical names during our search of County records. It also provides basic information that will be useful to your escrow officer.

Unless you are paying cash, assuming a loan, or the seller is financing, you will need to apply for a home loan if you have not already done so. Apply as soon as possible to comply with the purchase contract and prior to insuring to avoid delaying the closing.

RESPONSE TO SELLER’S NOTICES

If directed by the contract, you may receive the following items which require a response from you:

- Seller’s property disclosure statement listing any existing problems known to the seller

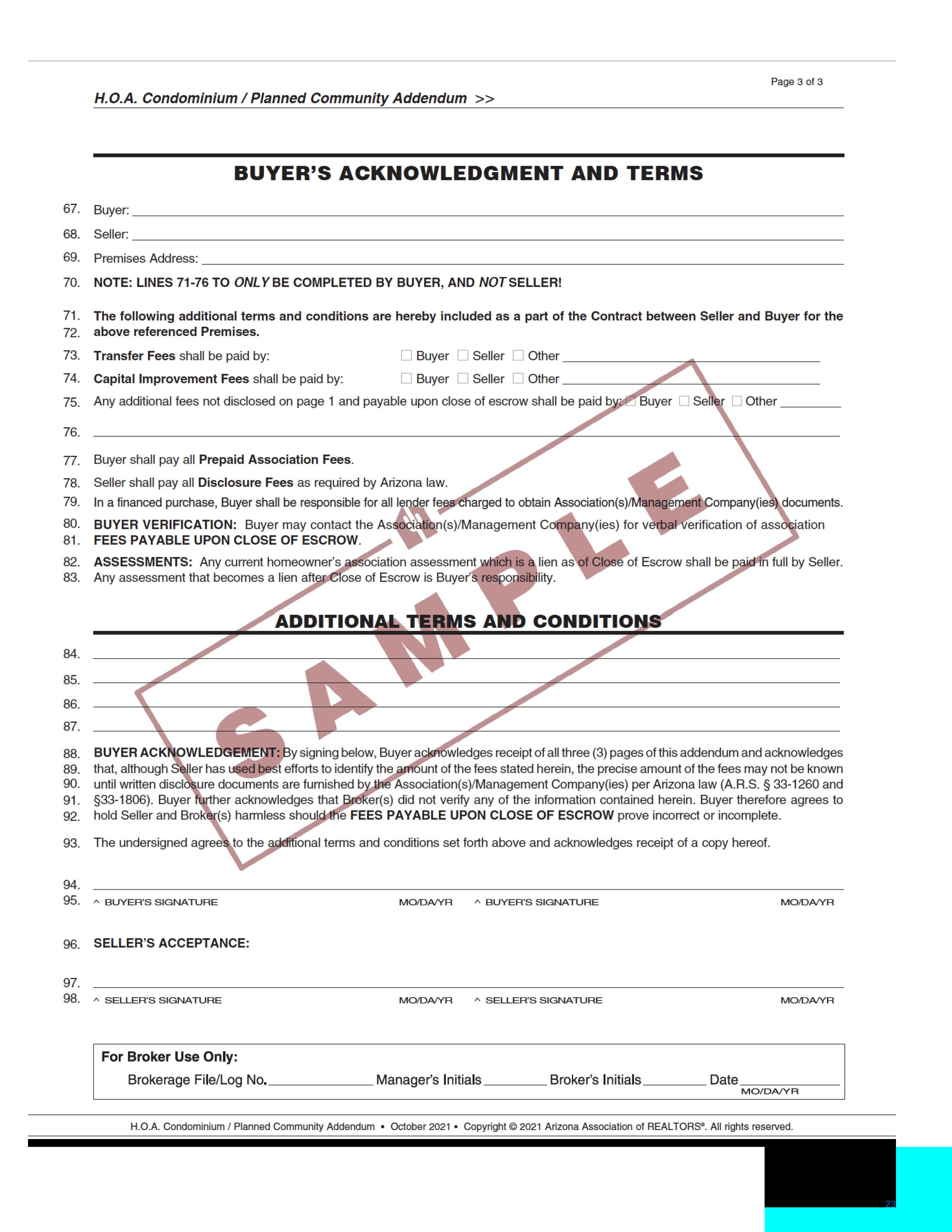

- Information pertaining to the Homeowners Association (HOA) or Planned Unit Development (PUD), such as Covenants, Conditions and Restrictions (CC&Rs), if applicable

- Flood hazard disclosure if the real property is in a flood area

- Independent inspections, such as termite and septic, and any repairs as required

You will receive a copy of the title commitment when we complete the title search. If you have questions about the title commitment, contact your real estate agent or your escrow officer.

One escrow transaction could involve over 20 individuals, including real estate professionals, buyer, seller, attorney, escrow officer, escrow technician, title officer, loan officer, loan processor, loan underwriter, home inspector, termite inspector, insurance agent, home warranty representative, contractor, roofer, plumber, pool service, and so on. And often one transaction depends on another.

When you consider the number of people involved, you can imagine the opportunities for delays and mishaps. While your experienced real estate professional, escrow, and title team can’t prevent unforeseen problems from arising, they can help to ensure as smooth a closing as possible.

The information below is to help you understand the contents of the title commitment you will receive from First American Title.

This is the information submitted to our title department by the escrow officer. It contains the basic information given to us by the buyer or real estate professional, such as the legal description of the real property, sale price, loan amount, lender, name, and marital status of buyer and seller.

The Schedule B “exceptions” are items which are tied to the subject property, and the buyer's rights in the title will be subject to these exceptions. These may include easements, Homeowners Association by-laws, leases, Covenants, Conditions, and Restrictions (CC&Rs) and other items which will remain of record and transfer with the property. The buyer is asked to sign a receipt for the Schedule B documents which states the buyer has read and accepts the contents.

These are items that First American Title needs to delete and/or record prior to insuring title to the real property. Items that need to be addressed include:

- Current property-tax status

- Any assessments that are owed, such as those for a Homeowners Association

- Any encumbrances (or liens) on the real property

Sometimes items show up against a parcel of real property because another person has a name similar to an involved party. This is one reason we ask for an Identity Statement, to determine if items are inaccurate and can be deleted.

A job change may result in your loan being denied, particularly if you are taking a lower-paying position or moving into a different field. Don’t think you’re safe because you’ve received approval earlier in the process, as the lender may call your employer to re-verify your employment just prior to funding the loan.

AVOID SWITCHING BANKS OR MOVING YOUR MONEY TO ANOTHER INSTITUTION

After the lender has verified your funds at one or more institutions, the money should remain there until needed for the purchase.

AVOID PAYING OFF EXISTING ACCOUNTS UNLESS YOUR LENDER REQUESTS IT

If your loan officer advises you to pay off certain bills in order to qualify for the loan, follow that advice. Otherwise, leave your accounts as they are until your escrow closes.

A major purchase that requires a withdrawal from your verified funds or increases your debt can result in your not qualifying for the loan. A lender may check your credit or re-verify funds at the last minute, so avoid purchases that could impact your loan approval.

Once the loan is approved and all invoices and paperwork have been provided, the lender and escrow officer will collaborate on the preparation of the Closing Disclosure (CD). In order to close on time, all paperwork and invoices should be submitted at least 10 days prior to the expected close of escrow date. The borrower must receive the CD at least three days* prior to consummation of the loan (typically the signing date). The escrow officer will also prepare an estimated settlement statement and inform the buyer of the balance of the down payment and closing costs needed to close escrow.

*For purposes of the Closing Disclosure“business day” is defined as every day except Sundays and Federal legal holidays.

The escrow holder will contact you or your agent to schedule a closing or signing appointment. In some states, this is the "close of escrow." In some others, the close of escrow is either the day the documents record or that funds are disbursed. Ask your escrow holder if you would like clarification about your state's laws.

You will have a chance to review the settlement statement and supporting documentation. This is your opportunity to ask questions and clarify terms. You should review the settlement statement carefully and report discrepancies

We recommend you keep all records pertaining to your home together in a safe place, including all purchase documents, insurance, maintenance, and improvements.

If you have a home warranty plan with First American Home Buyers Protection, please call them directly and have your home warranty number available.

to the escrow officer. This includes any payments that may have been missed. You are responsible for all charges incurred even if overlooked by the escrow holder, so it's better to bring these to their attention before closing.

The escrow holder is obligated by law to have the designated amount of money before releasing any funds. If you have questions or foresee a problem, let your escrow holder know immediately.

You will need valid identification with your photo I.D. on it when you sign documents that need to be notarized (such as a deed). A driver's license is preferred. You will also be asked to provide your social security number for tax reporting purposes, and a forwarding address.

If you are obtaining a new loan, your signed loan documents will be returned to the lender for review. The escrow holder will ensure that all contract conditions have been met and will ask the lender to "fund the loan." If your loan documents are satisfactory, the lender will send funds directly to the escrow holder. When the loan funds are received, the escrow holder will verify that all necessary funds are in. Escrow funds will be disbursed to the seller and other appropriate payees. Then, you’ll receive the keys to your home!

The original deed to your home will be mailed directly to you by the County Recorder, generally within four to six weeks.

First American Title will mail your policy to you in about two to three weeks.

You may not receive a tax statement for the current year on the home you buy; however, it is your obligation to make sure the taxes are paid when due.

Check with your mortgage company to find out if taxes are included with your payment. For more information on your property taxes, visit your County Auditor/Controller's web site.

Create an inventory sheet of items to move

Research moving options You’ll need to decide if yours is a do-it-yourself move or if you’ll be using a moving company.

Request moving quotes. Solicit moving quotes from as many moving companies and movers as possible. There can be a large difference between rates and services within moving companies.

Discard unnecessary items. Moving is a great time for ridding yourself of unnecessary items. Have a yard sale or donate unnecessary items to charity.

Packing materials. Gather moving boxes and packing materials for your move.

Contact insurance companies. (Life, Health, Fire, Auto) You’ll need to contact your insurance agent to cancel/transfer your insurance policy. Do not cancel your insurance policy until you have and closed escrow on the sale.

Seek employer benefits. If your move is work-related, your employer may provide funding for moving expenses. Your human resources rep should have information on this policy.

Changing Schools. If changing schools, contact new school for registration process.

Contact utility companies. Set utility turnoff date, seek refunds and deposits and notify them of your new address.

Obtain your medical records. Contact your doctors, physicians, dentists and other medical specialists who may currently be retaining any of your family’s medical records. obtain these records or make plans for them to be delivered to your new medical facilities.

Note food inventory levels. Check your cupboards, refrigerator and freezer to use up as much of your perishable food as possible.

Service small engines for your move by extracting gas and oil from the machines. This will reduce the chance to catch fire during your move.

Protect jewelry and valuables. Transfer jewelry and valuables to safety deposit box so they can not be lost or stolen during your move.

Borrowed and rented items. Return items which you may have borrowed or rented. Collect items borrowed to others.

Plan your itinerary Make plans to spend the entire day at the house or at least until the movers are on their way. Someone will need to be around to make decisions. Make plans for kids and pets to be at the sitters for the day.

Change of address Visit USPS for change of address form.

Bank accounts Notify bank of address change. Make sure to have a money order for paying the moving company if you are transferring or closing accounts.

Service automobiles. If automobiles will be driven long distances, you’ll want to have them serviced for a trouble-free drive.

Cancel services. Notify any remaining service providers (newspapers, lawn services, etc) of your move.

Start packing. Begin packing for your new location.

Travel items Set aside items you’ll need while traveling and those needed until your new home is established. Make sure these are not packed in the moving truck!

Scan your furniture Check furniture for scratches and dents before so you can compare notes with your mover on moving day.

Prepare Floor Plan Prepare floor plan for your new home. This will help avoid confusion for you and your movers.

Review the house. Once the house is empty, check the entire house (closets, the attic, basement, etc) to ensure no items are left or no home issues exist.

Sign the bill of lading. Once your satisfied with the mover’s packing your items into the truck, sign the bill of lading. If possible, accompany your mover while the moving truck is being weighed.

Double check with your mover. Make sure your mover has the new address and your contact information should they have any questions during your move.

Vacate your home. Make sure utilities are off, doors and windows are locked and notify your real estate agent you’ve left the property.

Your Notes:

1 SUN CITY WES T

623.299.3644

13940 W. Meeker Blvd, #119 Sun City West, AZ 85375 N of Meeker Blvd W of R.H. Johnson

2 THE LEGENDS

623.537.1608

20241 N. 67th Ave, #A-2 Glendale, AZ 85308 E side 67th Ave/N of 101

3 ARROWHEAD

623.487 0404

16165 N. 83rd Ave, #100 Peoria, AZ 85382

SE corner of N 83rd Ave and W Paradise Ln

4 ANTHEM

623.551.3265

39508 N. Daisy Mountain Dr, #128 Anthem, AZ 85086 NE corner Daisy Mtn Dr/Gavilan Peak Pkwy

5 TATUM RIDGE

480.515.4369

11211 N Tatum Blvd, #A150 Phoenix, AZ 85028 N of Shea, E side of Tatum

6 CAREFREE

480.575.6609

7202 E. Carefree Dr, Bldg 1, #1 Carefree, AZ 85377 NE corner of Tom Darlington/Carefree Dr.

7 SCOTTSDALE FORUM

480.551.0480

6263 N. Scottsdale Rd, #110 Scottsdale, AZ 85250 E Side Scottsdale/S of Lincoln

8 RAINTREE

480.563.9034

8605 E. Raintree Dr, # 130 Scottsdale, AZ 85260

SW corner of E Raintree Dr and N 87th St

9 CHANDLER PORTICO

480.777.0051

2121 W. Chandler Blvd., #100 Chandler, AZ 85224 SW Corner Chandler Blvd./Dobson Rd.

10 GILBERT SAN TAN

480.777.0614

1528 E. Williams Field Rd. #101 Gilbert, AZ 85295 NW corner of Williams Field Rd./Val Vista Rd.

11 MESA

480.401.3738

1630 S. Stapley Dr, #123 Mesa, AZ 85204 N of Baseline / W of Stapley

12 GOLD CANYON

480.288.0883

6877 South Kings Ranch Rd, #5 Gold Canyon, AZ 85118 E of 60/South Side Kings Ranch Rd.

1 MAIN OFFICE

520.885.1600 | Fax 520.885.2309

6390 E. Tanque Verde Road Tucson, AZ 85715

2 BROADWAY

520.747.1644 | Fax 520.747.1403

3777 E. Broadway Blvd., Suite 130 Tucson, AZ 85716

3 CAMBRIC

520.577.8707 | Fax 520.529.5034

1840 E. River Road, Suite 200 Tucson, AZ 85718

4 CASA GRANDE

520.426.4600 | Fax 520.426.4699

442 W. Kortsen Rd. Suite 101 Casa Grande, AZ 85122

5 CASAS ADOBES

520.575.1900 | Fax 520.432.0168

6760 N. Oracle Road, Suite 100B Tucson, AZ 85704

6 FOOTHILLS

520.299.4606 | Fax 520.577.6993

6262 N Swan Road, Suite 205 Tucson, AZ 85718

7 GREEN VALLEY

520.625.1095 | Fax 520.958.9663

210 W. Continental Rd., Suite 248 Green Valley, AZ 85622

8 ORO VALLEY/LA CANADA

520.877.9200 | Fax 520.202.6348

11165 N. La Canada Dr., Suite 143 Oro Valley, AZ 85737

520.297.2576 / 520.219.6451 Fax 520.229.9210 | 520.742.5866

8500 N. Oracle Rd., Suite 100 Oro Valley, AZ 85704 10 HOUGHTON ROAD

520.618.7790 | Fax 520.901.1720

8280 S. Houghton #130 Tucson, AZ 85747

11 SKYLINE

520.529.0506 | Fax 520.529.8998

2890 E. Skyline Drive, Suite 200 Tucson, AZ 85718

Good

with

The following home comparison chart is designed to help you remember the homes you visit and what you liked best and least about each one. Rate features or make notes that will help you determine what pleased or displeased you.

Remembering each home would appear easy, but it can quickly become confusing. Which home was near the school? Which one had the great pool? Did it have a family room? And how many bathrooms? In the “What’s Memorable” category, note something you think is unusual and memorable about each home, such as a stained glass window, fruit trees, a child’s playhouse. This will make it easier for you to recall the property later and refer to a specific address. And, last but not least, maybe the most important question, does this house feel like home?

Even during this pandemic, Arizona’s 50,000+ REALTORS® are well-positioned to continue meeting the needs of their clients and the communities they serve. REALTORS®, escrow companies, mortgage lenders, home inspectors, appraisers and other service providers remain hard at work, making sure buyers and sellers have all the services they need to complete their real estate transactions safely and efficiently.

To practice “social distancing” while conducting real estate transactions, Arizona REALTORS® can:

• Create virtual property tours and conduct video chats that allow buyers to see properties in a realistic way online. REALTORS® can also conduct virtual listing presentations with sellers.

• Use electronic documents and encourage buyers and sellers to sign paperwork through platforms like Authentisign and eSign to minimize in-person contact. In fact, much of the transaction was already conducted online, even before COVID-19.

• Assist in securing a mobile notary, thereby helping their clients finalize the transaction without ever leaving their home.

• With the increased use of technology, however, we encourage buyers and sellers to be aware of scams. Before sending money, buyers and sellers should always call their title company using an independently verified number to confirm wiring instructions.

During property showings and inspections, REALTORS® are encouraging the following to prevent the spread of disease:

• Having all parties wash hands and/or use hand sanitizer before and after entering a home.

• Asking buyers to avoid touching anything in the home.

• Canceling showings if buyers, sellers or others are sick.

• Opening all interior doors prior to showings to minimize the need for buyers to touch door handles.

• Turning on all lights before showings to prevent touching light switches.

• Disinfecting all door handles and high-touch areas prior to and after showings.

• Limiting the number of individuals in the home at any one time and having all parties stand six feet away from each other during showings.

In the event that a seller chooses not to hold an open house, REALTORS® remain ready and able to market the property in a number of alternative ways.

REALTORS® currently report that real estate transactions are moving smoothly. Nevertheless, should any issues arise, the Arizona Association of REALTORS® continues to provide its members with the most up to date information and tools they need to help their clients through any delays resulting from the outbreak.

Real estate closings continue to take place each day, and the demand for real estate in Arizona remains high. Arizona REALTORS® stand ready to help their community and serve their clients.

DOCUMENT UPDATED: November 2023

Provided by the Arizona Association of REALTORS® and the Arizona Department of Real Estate

A real estate agent is vital to the purchase of real property and can provide a variety of services in locating a property, negotiating the sale, and advising the buyer.

A real estate agent is generally not qualified to discover defects or evaluate the physical condition of property; however, a real estate agent can assist a buyer in finding qualified inspectors and provide the buyer with documents and other resources containing vital information about a prospective property.

This Advisory is designed to make the purchase of real property as smooth as possible. Some of the more common issues that a buyer may decide to

investigate or verify concerning a property purchase are summarized in this Advisory. Included in this Advisory are:

1. Common documents a buyer should review;

2. Physical conditions in the property the buyer should investigate; and

3. Conditions affecting the surrounding area that the buyer should investigate.

In addition, a buyer must communicate to the real estate agents in the transaction any special concerns the buyer may have about the property or surrounding area, whether or not those issues are addressed in this Advisory.

This Advisory is supplemental to obtaining professional property inspections. Professional property inspections are absolutely essential: there is no practical substitute for a professional inspection as a measure to discover and investigate defects or shortcoming in a property.

Please Note:

The property may be subject to video and/or audio surveillance. Buyer should therefore exercise caution and not discuss features or pricing while in the home.

The documents listed below may not be relevant in every transaction, nor is the list exhaustive. Unless otherwise stated, the real estate broker has not independently verified the information contained in these documents.

Buyers should protect themselves by taking the time to read the Arizona REALTORS® Residential Resale Real Estate Purchase Contract and understand their legal rights and obligations before they submit an offer to buy a property.

Residential Resale Real Estate Purchase Contract (Arizona REALTORS® Residential Resale Purchase Contract)

The Purchase Contract contains numerous contingencies, including, but not limited to, the loan contingency, the inspection contingency, and the appraisal contingency. Should a buyer elect to waive any such contingencies in conjunction with their purchase offer, adverse consequences may result that place buyer at risk of losing their Earnest Money or incurring monetary damages if buyer decides not to purchase the property after their offer is accepted. Before offering to waive any contractual contingencies, buyers should weigh the risks and consult with independent legal counsel.

A listing is a contractual agreement between the seller and the listing broker and may authorize the broker to submit information to the Multiple Listing Service (MLS). The MLS printout is similar to an advertisement. Neither the listing agreement nor the printout is a part of the purchase contract between the buyer and seller. The information in the MLS printout was probably secured from the seller, the builder, or a governmental agency, and could be inaccurate, incomplete or an approximation. Therefore, the buyer should verify any important information contained in the MLS.

A Subdivision Disclosure Report (Public Report) is intended to point out material information about a subdivision. Subdividers (any person who offers for sale or lease six or more lots in a subdivision or who causes land to be divided into a subdivision) are required to give buyers a Public Report. Read the Public Report before signing any contract to purchase a property in a

subdivision. Although some of the information may become outdated, subsequent buyers can also benefit from reviewing the Public Report. Public Reports dating from January 1, 1997, are availableon the Arizona Department of Real Estate (ADRE) website. https://services.azre.gov/publicdatabase/SearchDevelopments.aspx (ADRE Search Developments)

https://azre.gov/consumers/property-buyers-checklist-home-or-land (ADRE Property Buyer’s Checklist)

ADRE does not verify the information in the Public Report. Therefore, the Report could be inaccurate, so it should be verified by the buyer.

Most sellers provide a SPDS. This document poses a variety of questions for the seller to answer about the property and its condition. The real estate broker is not responsible for verifying the accuracy of the items on the SPDS; therefore, a buyer should carefully review the SPDS and verify those statements of concern.

Aseller’s disclosureobligation remains even ifthebuyer and seller agree that no Seller’s Property Disclosure Statement will be provided.

https://bit.ly/3HDnA0u (AAR Sample SPDS)

http://www.azre.gov/PublicInfo/PropertyBuyerChecklist.aspx (ADRE Property Buyer’s Checklist)

The CC&Rs are recorded against the property and generally empower a homeowner’s association to control certain aspects of property use within the development. By purchasing a property in such a development, the buyer agrees to be bound by the CC&Rs. The association, the property owners as a whole, and individual property ownercan enforce the CC&Rs. It is essential that thebuyer review and agree to these restrictions prior to purchasing a property.

http://www.azre.gov/PublicInfo/PropertyBuyerChecklist.aspx (ADREProperty Buyer’sChecklist)

It is the law of this state that any covenants or restrictions that are based on race, religion, color, handicap status or national origin are invalid and unenforceable A.R.S. 32-2107.01

https://www.aaronline.com/arizona-deed-restrictions/ (Arizona Deed Restrictions webpage)

ADRE ADVISES: “Read the deed restrictions, also called CC&Rs (covenants, conditions and restrictions). You might find some of the CC&Rs are very strict.” Buyers should consult legal counsel if uncertain of the application of particular provisions in the CC&Rs.

In addition to CC&Rs, HOAs may be governed by Articles of Incorporation, Bylaws, Rules and Regulations, and often architectural control standards. Read and understand these documents. Also, be aware that some HOAs impose fees that must be paid when the property is sold, so ask if the purchase of the property will result in any fees. Condominium and planned community HOAs are regulated by Arizona statutes. They are not under the jurisdiction of the Department of Real Estate (ADRE). Nonetheless, the Arizona’s Homeowner's Association Dispute Process is administered by the ADRE.

http://bit.ly/2ebBSLH (A.R.S. 33-1260);

http://bit.ly/2e8jdM3 (A.R.S. 33-1806)

http://bit.ly/1rCq9kd (ADRE HOA Information)

If purchasing a resale home in a condominium or planned community, the seller (if fewer than 50 units in the community) or the HOA (if there are 50 or more units) must provide the buyer with a disclosure containing a variety of information.

http://bit.ly/2ebBSLH (A.R.S.33-1260); and http://bit.ly/2e8jdM3 (A.R.S. 33-1806)

Community Facilities Districts (CFDs) are special taxing districts that use bonds for the purpose of financing construction, acquisition, operation and maintenance of public infrastructure that benefits the real property owners comprising the CFD members. Roadways, public sewer, utility infrastructure and public parks are examples of the types of public infrastructure paid for by CFDs. CFDs have a Governing Board that may be the City Council acting as the board or a stand-alone board. Any member of a CFD may request disclosures from this board. Questions to ask include: the amount still owed and how many more payments are left in order to pay off the CFD for the property. It is important that you review the Detailed Property Tax Statement which will show the current amount due to the CFD.

CFDs are most commonly found on the property’s detailed property tax statement from the County Tax Assessor. The local municipality or county can also be a source of CFD information.

The title report or commitment contains important information and is provided to the buyer by the title/ escrow company or agent. This report or commitment lists documents that are exceptions to the title insurance (Schedule B Exceptions). Schedule B Exceptions may include encumbrances, easements, and liens against the property, some of which may affect the use of the property, such as a future addition or swimming pool. Make sure you receive and review all of the listed documents. Questions about the title commitment and Schedule B documents may be answered by the title or escrow officer, legal counsel, or a surveyor.

https://www.homeclosing101.org/ (American Land Title Association)

https://bit.ly/34KkCaQ (CFPB - What is title insurance?)

Unless a buyer is paying cash, the buyer must qualify for a loan in order to complete the purchase. A buyer should complete a loan application with a lender before making an offer on a property if at all possible and, if not, immediately after making an offer. It will be the buyer’s responsibility to deposit any down payment and ensure that the buyer’s lender deposits the remainder of the purchase price into escrow prior to the close of escrow date. Therefore, make sure you get all requested documentation to your lender as soon as possible.

https://www.consumerfinance.gov/owning-a-home/ (Buying a house: Tools & Resources for Homebuyers) https://www.hud.gov/topics/buying_a_home (HUD.gov)

A home warranty [policy]is a service contract that typically covers the repair and/or replacement costs of home appliances and major systems such as heating, cooling, plumbing, and possibly other components of a home that fail due to normal usage and age. Coverage varies depending on the policy. Be aware that pre-existing property conditions are generally not covered. A home warranty may be part of the sale of the home. If so, buyers should thoroughly read the home warranty contract to understand coverage, limitations, exclusions, and costs associated with the policy.

If the buyer is purchasing five or fewer parcels of land (whether improved or vacant), other than subdivided land, in an unincorporated area of a county, the seller must furnish the buyer with an Affidavit of Disclosure.

https://bit.ly/2ZLwvdX (AAR Sample Affidavit of Disclosure)

If the home was built prior to 1978, the seller must provide the buyer with a lead-based paint disclosure form. Buyer is further advised to use certified contractors to perform renovation, repair or painting projects that disturb lead-based paint in residential properties built before 1978 and to follow specific work practices to prevent lead contamination.

http://bit.ly/2O4pL4A (AAR Sample Form)

https://bit.ly/3uzq5Kb (ADRE Lead Based Paint Information)

The importance of having a property inspected by a professional inspector cannot be over-emphasized. An inspection is visual physical examination, performed for a fee, designed to identify material defects in the property.

The inspectorwillgenerally providethebuyer with a report detailing information about the property’s condition. The buyer should carefully review this report with the inspector and ask the inspector about any item of concern. Pay attention to the scope of the inspection and any portions of the property excluded from the inspection. https://www.homeinspector.org/ConsumerInformation (ASHI Home Buyer’s Guide)

The county assessor’s records contain a variety of valuable information, including the assessed value of the property for tax purposes and some of the physical aspects of the property, such as the reported square footage. The date-built information in the assessor’s records can be either the actual or effective/weighted age if the residence has been remodeled. All information on the site should be verified for accuracy.

Apache: https://bit.ly/3CVkXTu Cochise: http://bit.ly/1oUS7ok

Coconino: http://bit.ly/2F9PstM Gila: http://bit.ly/Yq3bV9

Graham: http://bit.ly/2JGz2ZO

La Paz: http://bit.ly/2HzhhdR

Mohave: https://bit.ly/2Y8QH9g

Pima: https://www.asr.pima.gov/

Santa Cruz: http://bit.ly/1yRYwXl

Yuma: https://bit.ly/3uO8BbW

Greenlee: http://bit.ly/2SCTZu6

Maricopa: https://mcassessor.maricopa.gov/

Navajo: http://bit.ly/1pWxgVA

Pinal: http://www.pinalcountyaz.gov/ Assessor/Pages/home.aspx

Yavapai: Assessor's Office Home (yavapaiaz.gov)

Termites and other wood destroying insects are commonly found in some parts of Arizona. General guidance, inspection report information and the ability to search a property for past termite treatments may be found on the Arizona Department of Agriculture website.

https://agriculture.az.gov/pestspest-control/termites (AZDA-Termite Information)

http://bit.ly/2GiGlIR%20 (AZDA-Wood Destroying Insect Inspection Reports)

https://tarf.azda.gov/ (AZDA-Search for Termite Reports)

Foreign Investment in Real Property Tax Act(FIRPTA) may impact the purchase of property if the legal owner(s)of the property are foreign persons or nonresident aliens pursuant to FIRPTA. If so, consult a tax advisor as mandatory withholding may apply.

https://bit.ly/3w10GsF (I.R.S. FIRPTA Definitions)

https://www.irs.gov/Individuals/International-taxpayers/firptawithholding (I.R.S. FIRPTA Information)

https://www.irsvideos.gov/Individual/education/FIRPTA I.R.S. FIRPTA Video)

Because every buyer and every property are different, the physical property conditions requiring investigation will vary.

The seller may have made repairs or added a room to the property. The buyer should feel comfortable that the work was properly done or have an expert evaluate the work. Request copies of permits, invoices or other documentation regarding the work performed.

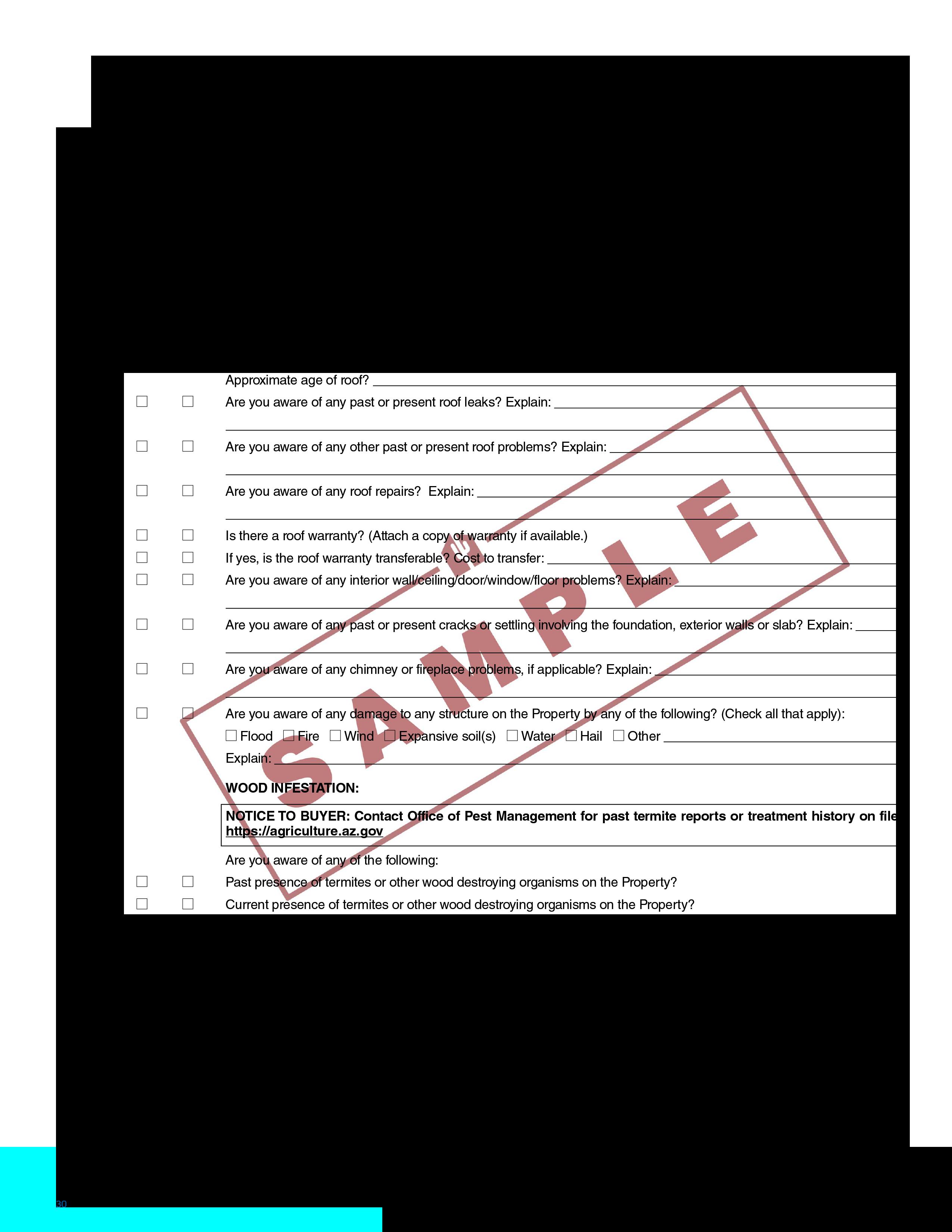

A contractor’s license is required for work performed on a property unless the aggregate contract price, including labor and material, is less than $1,000, the work performed is of a “casual or minor nature,” and no building permit is required. An unlicensed property owner may also perform work themselves if the property is intended for occupancy solely by the owner. If, however, the property is listed or offered for sale or rent within one year of the completed work, it is considered prima facie evidence that the owner performed the work for purposes of sale or rent.

Owners of property who are acting as developers, who improve structures or appurtenances to structures on their property for the purpose of sale or rent, and who contract with a licensed general contractor must identify the licensed contractors’ names and license numbers in all sales documents.

https://roc.az.gov/before-hire (Before you Hire a Contractor–Tips)

https://remodelingdoneright.nari.org/ (National Association of the Remodeling Industry)

https://apps-secure.phoenix.gov/PDD/Search/Permits(Phoenix Building Permit Search)

https://www.tucsonaz.gov/Departments/Planning-DevelopmentServices/Permits (TucsonBuilding permitrecords)

Othercities- search Planning&Development

Square footage on the MLS printout or as listed by the county assessor’s records is often only an estimate and generally should not be relied upon for the exact square footage. An appraiser or architect can measure the property’s size to verify the square footage.

If the square footage is important, you should have it confirmed by one of these experts during the inspection period in a resale transaction and prior to executing a contract on a new home transaction.

https://difi.az.gov/industry/RealEstateAppraisers (Licensed Real Estate Appraisers)

If the roof is 10 years old or older, a roof inspection by a licensed roofing contractors highly recommended.

www.azroofing.org (Arizona Roofing Contractors Association) https://roc.az.gov/before-hire (Before you Hire a Contractor)

If the property has a pool or a spa, the home inspector may Exclude the pool or spa form the general inspection so an inspection by a pool or spa company may be necessary.

https://www.aaronline.com/2010/10/27/pool-barrier-law-contactinformation/ (AAR-Pool Barrier Laws & Information) 36-1681 - Pool enclosures; requirements; exceptions; enforcement (azleg.gov) (A.R.S. 36-1681 Swimming Pool Enclosures)

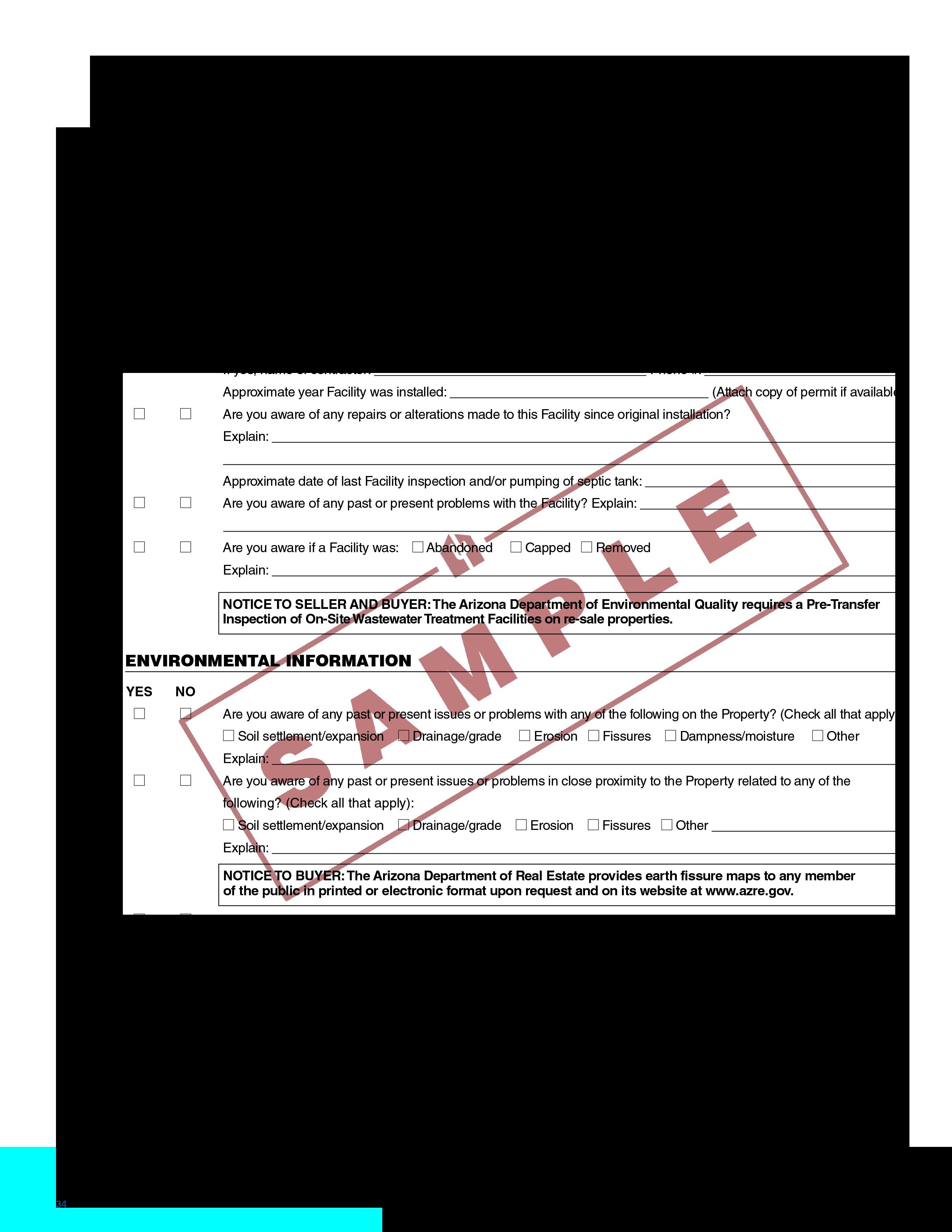

If the home is not connected to a public sewer, it is probably served by an on-site wastewater treatment facility (conventional septic or alternative system). A qualified inspectormustinspectany suchfacility within six months prior to transfer of ownership. For information on current inspection and transfer of ownership requirements, contact the specific county environmental/health agency where the property is located or the Arizona Department Environmental Quality (ADEQ).

https://azdeq.gov/notice-transfer-and-inspection-onsitewastewater (ADEQ – AZ Statewide Inspection Program File a Notice of Transfer Online)

Even if the listing or SPDS indicates that the property is connected to the city sewer, a plumber, home inspector, or other professional should verify it. Some counties and cities can perform this test as well.

The property may receive water from a municipal system, a private water company, or a well. You should investigate the availability and quality of the water to theproperty, as well as the water provider. A list of Arizona’s water companies is available at the Arizona Corporation Commission.

https://www.azcc.gov/utilities/water (Arizona Corporation Commission- Utilities Water) https://new.azwater.gov/aaws/statutes-rules (Assured and Adequate Water Supply)

Adjudications: Arizona is undertaking several Stream Adjudications, which are court proceedings to determine the extent and priority of water rights in an entire river system.

For information regarding water uses and watersheds affected by these adjudications, and the forms upon sale of the property, visit the Department of Water Resources online.

https://new.azwater.gov/adjudications Department of Water Resources – Adjudications)

CAGRDs: The Central Arizona Groundwater Replenishment District (CAGRD) functions to replenish groundwater used by its members, individual subdivisions and service areas of member water providers. Homeowners in a CAGRD pay an annual assessment fee which is collected through the county property tax process based the amount of ground water served to member homes.

www.cagrd.com (Central Arizona Ground Water Replenishment District)

The soil in some areas of Arizona has “clay-like” tendencies, sometimes referred to as “expansive soil.”

Other areas are subject to fissure, subsidence and other soil conditions. Properties built on such soils may experience significant movement causing a major problem.

If it has been disclosed that the property is subject to any such soil conditions or if the buyer has any concerns about the soil condition or observes evidence of cracking, the buyer should secure an independent assessment of the property and its structural integrity by a licensed, bonded, and insured professional engineer.

https://azgs.arizona.edu/center-natural-hazards/problem-soils (Problem Soils -UA Science AZ Geological Survey)

http://bit.ly/2yfzVHR

(Information on Land Subsidence & Earth Fissures)

www.btr.state.az.us

(State Certified Engineers & Firms)

If it is disclosed there has been a fire or flood on the property, a qualified inspector should be hired to advise you regarding any possible future problems as a result of the fire or flood damage and/or any subsequent repairs. For example, if the property was not properly cleaned after a flood, mold issues may result. Your insurance agent may be able to assist you in obtaining information regarding fire, flood, or other past damage to the property.

Cockroaches, rattlesnakes, black widow spiders, scorpions, termites and other pests are common in parts of Arizona. Fortunately, most pests can be controlled with pesticides. Scorpions: Scorpions, on the other hand, may be difficult to eliminate. If buyer has any concerns or if the SPDS indicates the seller has seen scorpions or other pests on the property, seek the advice of a pest control company.

Bed Bugs: Infestations are on the rise in Arizona and nationally.

Roof Rats: Roof Rats have been reported in some areas by Maricopa County Environmental Services.

Termites: Consumer Information is available from the Arizona Department of Agriculture.

Bark Beetles: Bark beetles have been reported in some forested areas.

https://agriculture.az.gov/pests-pest-control/household-pests/scorpions (Scorpions – Information)

https://agriculture.az.gov/pests-pest-control/household-pests/bed-bugs (Bed Bugs – Information)

https://agriculture.az.gov/pestspest-control/household-pests/roof-rats (Roof Rats)

https://agriculture.az.gov/pestspest-control/termites (Termite Information)

https://agriculture.az.gov/pestspest-control/agriculture-pests/bark-beetles (Bark Beetles – Information)

Certain areas in the state may have issues related to federally listed endangered or threatened species that may affect land uses. Further information may be obtained on the U.S. Fish and Wildlife website or by contacting the appropriate planning/development service department.

Arizona Ecological Services Field Office | U.S. Fish & Wildlife Service (fws.gov) (Arizona Ecological Services) (Arizona Endangered Species)

Arizona law states that sellers and real estate licensees have no liability for failure to disclose to a buyer that the property was ever the site of a natural death, suicide, murder or felony. This information is often difficult to uncover; however, the local law enforcement agency may be able to identify incidents related to a property address.

http://bit.ly/2lo53MZ (A.R.S. § 32-2156)

Attention has been given to the possible health effects of mold in homes, apartments and commercial buildings. Certain types of molds may cause health problems in some people while triggering only common allergic responses in others. Mold is often not detectable by a visual inspection. To determine if the premises you are purchasing, or leasing contains mold or airborne health hazards, you may retain an environmental expert to perform an indoor air quality test. This is particularly important if any of the inspection reports or disclosure documents indicate the existence of past or present moisture, standing water, visible water stains, or water intrusion in the Premises.

The Arizona Department of Health Services, Office of Environmental Health, states:

“If you can see mold, or if there is an earthy or musty odor, you can assume you have a mold problem.”

Epa.gov/indoor-air-quality-iaq (EPA-Indoor Air Quality)

https://www.epa.gov/mold (EPA-Mold)

https://www.cdc.gov/mold/default.htm (CDC-Mold Information)

Imported Drywall: There have been reports of problematic drywall, produced in China, used in Arizona homes. Residents in homes with problem drywall report health issues such as respiratory irritation, and other problems such as copper corrosion and sulfur odors. Visit the Consumer Product Safety Commission website for more information.

Radon Gas and Carbon Monoxide: Radon gas and carbon monoxide poisoning are two of the more common and potentially serious indoor air quality (IAQ) concerns. Both of these concerns can be addressed by the home inspector, usually for an additional fee. For information on radon levels in the state, visit Arizona Radiation Regulatory Agency online.

Drug labs: Residual contamination arising from the illicit manufacture of methamphetamine and other drugs carried out in clandestine drug laboratories presents a serious risk of harm to human and environmental health.

Other: For information on other indoor environmental concerns, the EPA has a host of resource materials and pamphlets online.

bit.ly2kRk7jm (Drywall Information Center)

http://bit.ly/2GclWpM (About Radon)

http://bit.ly/2t1CAPq (Carbon Monoxide Infographic)

https://www.epa.gov/asbestos (Asbestos Information)

http://bit.ly/2qUZcSt (Voluntary GuidelinesMethamphetamine & Fentanyl Laboratory Cleanup) Formaldehyde | US EPA (EPA Formaldehyde)

If the property boundaries are of concern, a survey may be warranted. For example, a survey may be advisable if there is an obvious use of property by others, i.e., a well-worn path across a property and/or parked cars on the property or fences or structures of adjacent property owners that appear to be built on theproperty. For more information, visit the Arizona Professional Land Surveyors online. A search for surveyors may be found online at the Board of Technical Registration.

https://www.azpls.org/secure/find_surveyor.asp (AZ BTR Land Surveyors)

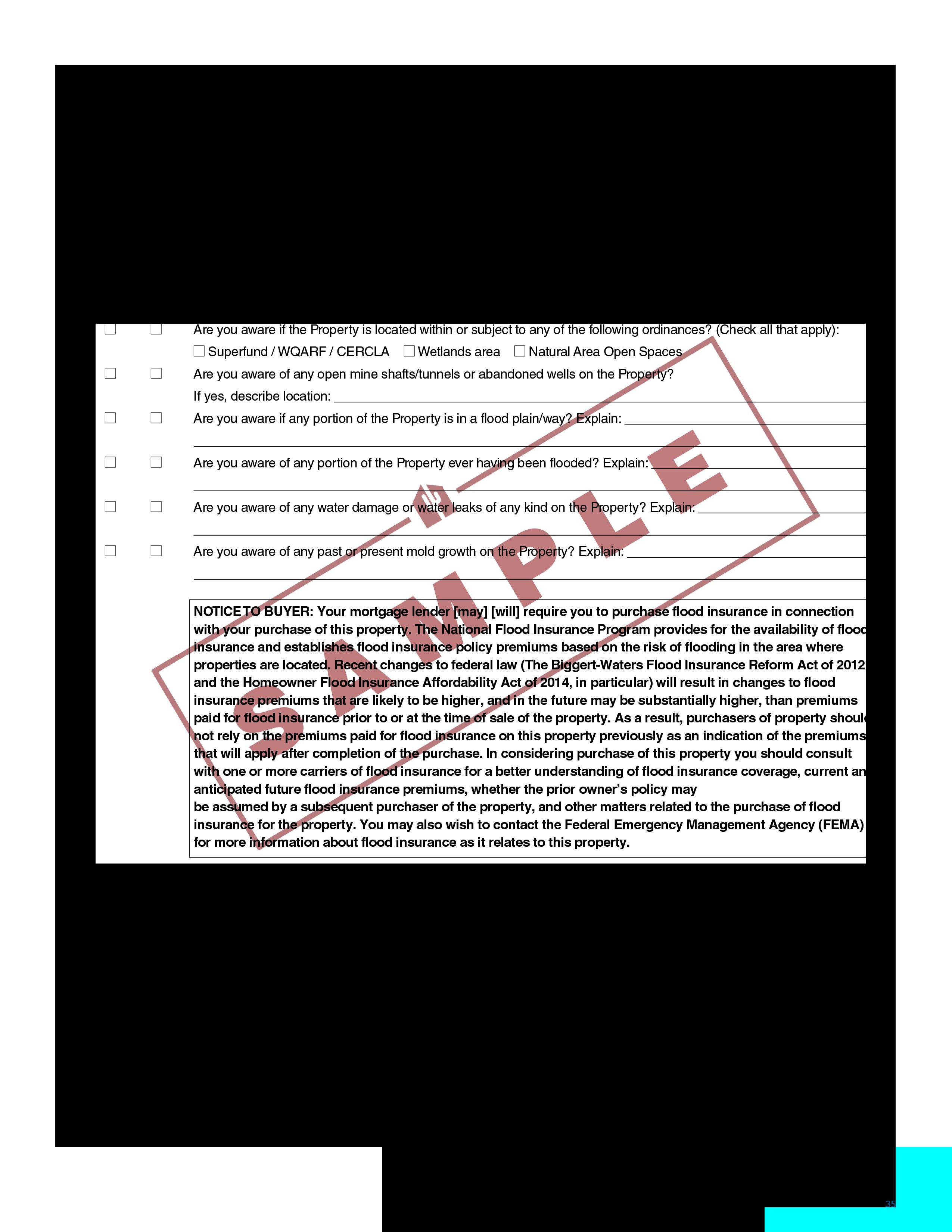

Your mortgage lender may require you to purchase flood insurance in connection with your purchase of the property. The National Flood Insurance Program provides for the availability of flood insurance and established flood insurance policy premiums based on the risk of flooding in the area where properties are located. Changes to the federal law (The BiggertWaters Flood Insurance Reform Act of 2012 and the Homeowner Flood Insurance Affordability Act of 2014, in particular) will result in changes to flood insurance premiums that are likely to be higher, and in the future, may be substantially higher, than premiums paid for flood insurance prior to or at the time of sale of the property. As a result, purchasers of property should not rely on the premiums paid for flood insurance on the property previously as an indication of the premiums that will apply after completion of the purchase. In considering purchase of the property, you should consult with one or more carriers of flood insurance for a better understanding of flood insurance coverage, current and anticipated future flood insurance premiums, whether the prior owner’s policy may be assumed by a subsequent purchase of the property, and other matters related to the purchase of flood insurance for the property. If community floodplain information is not available for a specific property, and in order to obtain flood insurance, it may be necessary to have an elevation survey and obtain an elevation certificate. This is necessary to determine a properties insurability and premium rate. You may also wish to contact the Federal Emergency Management Agency (FEMA) for

Section 3

more information about flood insurance as it relates to the property.

National Flood Insurance Program (FEMA)

https://www.realtor.com/flood-risk/ (Flood Risk Information)

https://www.floodsmart.gov/flood-map-zone/elevationcertificate (Elevation Certificates: Who Needs Them and Why - fact sheet)

http://azgs.arizona.edu/center-natural-hazards/floods(Floodingin Arizona)

https://www.fcd.maricopa.gov/5308/Flood-Control-District (Maricopa County Flood Control District-Services)

Other Arizona Counties: Consult County Websites.

Many factors affect the availability and cost of homeowner’s insurance. Property owners may request a five-year claims history from their insurance company, an insurance support organization or consumer reporting agency.

Consumer Resources (naic.org) (Helping You Navigate Insurance and Make Better Informed Decisions)

Plumbing: Check functionality.

Cooling/Heating: Make sure the cooling and heating systems are adequate. If it is important to you, hire a qualified heating/cooling inspector.

https://www.epa.gov/ods-phaseout (Phaseout of Ozone-Depleting Substances -ODS)

Electrical Systems: Check for functionality and safety.

Every property is unique; therefore, important conditions vary

It is often very difficult to identify environmental hazards. The Arizona Department of Environmental Quality (ADEQ) website contains environmental information regarding the locations of open and closed landfills (Solid Waste Facilities), wildfire information, as well as air and water quality

information, as well as air and water quality information (and more).

https://azdeq.gov/landfills (ADEQ-Landfills)

https://www.azdeq.gov/solidwaste(ADEQ-Solid WasteFacilities)

https://www.azdeq.gov/wildfire-support (Wildfire Support)

Approximately two-thirds of the City of Scottsdale is affected by the Environmentally Sensitive LandOrdinance (ESLO), which requires someareas onprivate property be retained in their natural state and designated as National Area OpenSpace(NAOS).

https://www.scottsdaleaz.gov/codes/eslo (ELS and NAOS)

For information on electric and magnetic fields, and whether they pose a health risk to you or your family, visit the National Institute of Environmental Health Sciences website.

https://www.niehs.nih.gov/health/topics/agents/emf/index.cfm (National Institute of Environmental Health Sciences)

There are numerous sites in Arizona where the soil and groundwater have been contaminated by improper disposal of contaminants. Maps may be viewed on ADEQ’s website to see if a property is in an area designated by the ADEQ as requiring cleanup.

https://azdeq.gov/superfund-sites (AZ ADEQ-Superfund Sites) https://www.epa.gov/superfund (EPA Supefund)

Although the existence of a freeway near the property may provide highly desirable access, sometimes it contributes to undesirable noise. To search for roadway construction and planning, visit the Arizona Department of Transportation (ADOT) website.

https://azdot.gov/projects (ADOT Statewide Projects) https://az511.com (ADOT Road Conditions)

5

Crime statistics, an imperfect measurement at best, provide some indication of the level of criminal activity in an area.

https://communitycrimemap.com/ (Crime Statistics - All Arizona Cities)

Since June 1996, Arizona has maintained a registry and community notification program for convicted sex offenders. Prior to June 1996, registration was not required, and only the higher-risk sex offenders are on the website. The presence of a sex offender in the vicinity of the property is not a fact that the seller or real estate broker is required to disclose.

https://www.azdps.gov/services/public/offender (Registered Sex Offender and Community Notification) https://www.nsopw.gov/ (National Sex Offender Public Site)