After strong sales activity in September and October, November sales decreased to more modest levels but were notably higher than monthly figures one year ago. November sales included 25 transactions, including the second, top-dollar transaction of the year. This brought a nice bump to annual dollar volume figures which are vying to match what the market saw in 2022, but with significantly fewer transactions. As to be expected, new purchase activity saw a seasonal dwindle while inventory levels remained consistent among most price points. Here are Fisher’s November Market Insights…

KEY MARKET METRICS

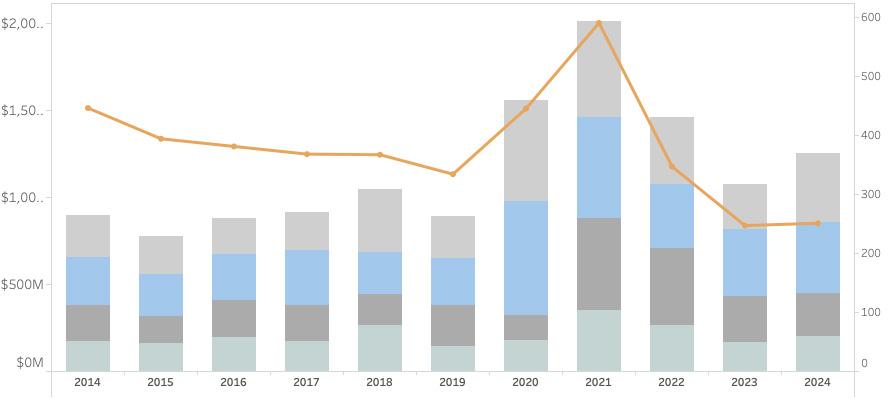

NANTUCKET REAL ESTATE ACTIVITY THROUGH NOVEMBER 2014 - 2024

MONTHLY SALES HIGHLIGHTS

Market Insights BY

JEN ALLEN

RESIDENTIAL SALES ANALYSIS

INCREASE IN TRANSACTIONS AND DOLLAR VOLUME

• Single-family home sales (excluding condos, co-ops & covenant properties) during the month of November measured 25 transactions totaling $132 million. This represented a 56 percent and 71 percent respective increase from November 2023 figures -- a significant rise in the historically low monthly activity from one year ago. This brought the year-to-date total to 225 single-family home sales totaling $1.1 billion through November 30, 2024, a cumulative 2024 increase of 12 percent and 21 percent.

• The highest sale of the month was the waterfront sale of 41 Jefferson Avenue which was purchased by the Nantucket Land Bank. The property had been cumulatively marketed for many years and was initially listed for $38 million in May of 2018. It is by far the highest acquisition price paid by the conservation-entity and certainly on a price per square foot basis.

• There were a handful of resales during the month of November, or transactions where a property trades more than once over a given period, without any major improvements. These sales pointed to annualized returns ranging from four percent to as high as eleven percent.

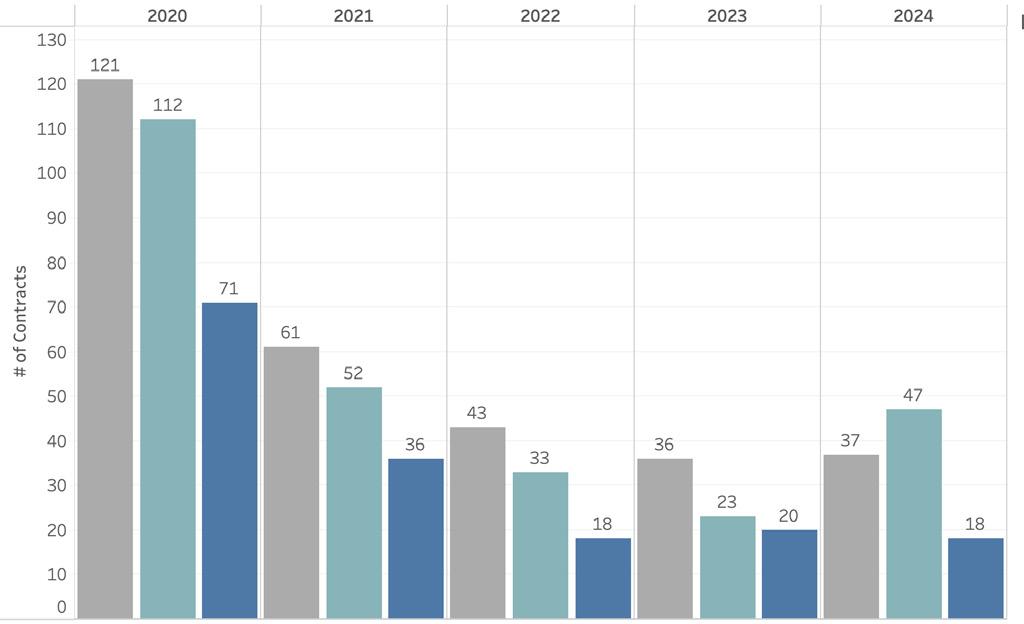

• After a solid amount of new contract activity in September and October, new purchase activity settled into historic norms and dipped considerably in November. New recorded contracts (Offers to Purchase and Purchase & Sale Contracts excluding duplicates) measured 18 properties, slightly below last year and the same as in 2022. The peak in November activity occurred in 2020 when there were 71 contracts reported during the month.

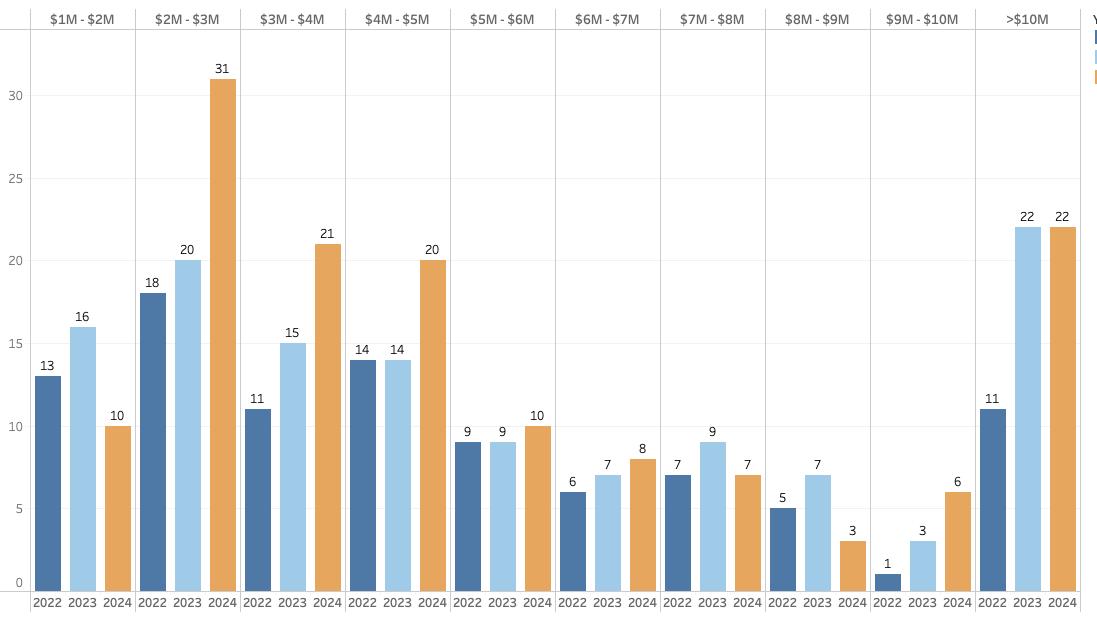

• Of these recorded contracts, two were for properties last listed above $10 million, suggesting there may still be a year-end bump. Most of the contracts were for properties last listed for less than $5 million, five of which were for properties last listed between $1 million and $2 million.

SINGLE-FAMILY INVENTORY MODEST GROWTH ACROSS

• As of November 30, 2024, there were just 173 properties listed for sale including residential, commercial, and vacant land listings. This is 11 percent higher than one year ago and seven percent higher than the five-year average.

• By isolating single-family homes for sale by price point, the chart shows most price points saw an incremental increase in listed properties from 2023. There were also more notable increases from the last two years, namely sales properties last listed between $2 million and $3 million.

• The total months’ supply, or how long it would take to sell all listings based on trailing 12-month sales, measured seven months, an increase of one month from this time last year.