1 minute read

MELBOURNE CBD OFFICE - MARKET REPORT, Q1

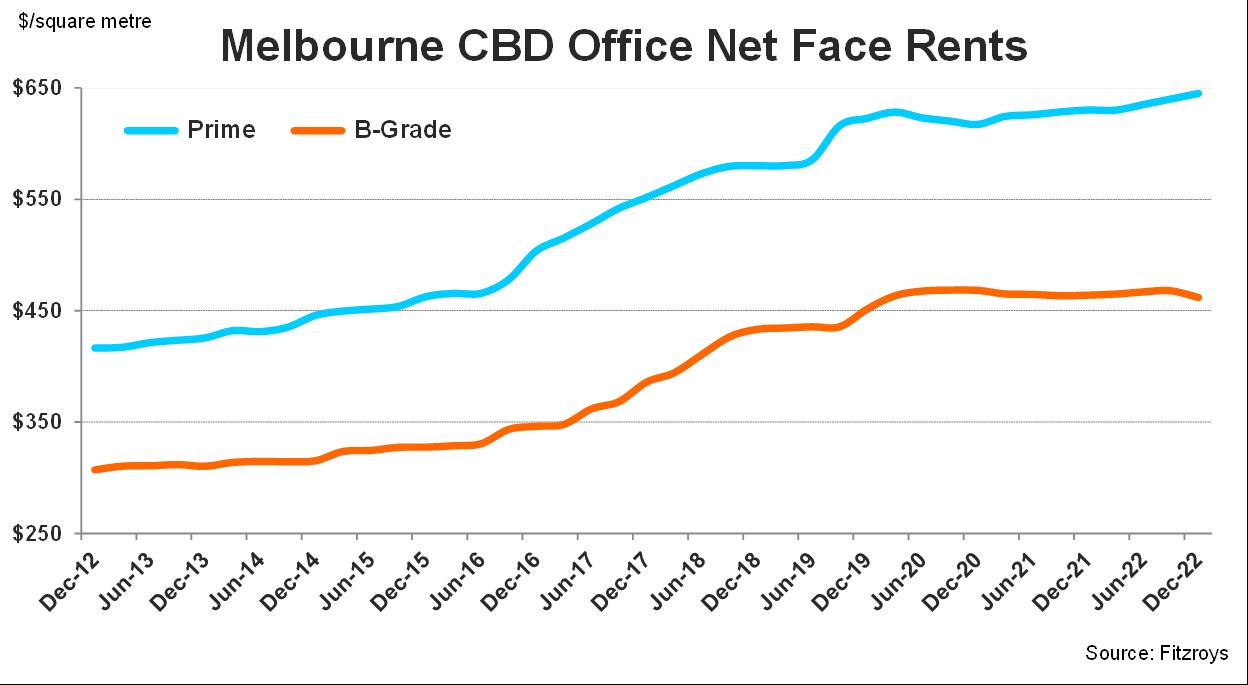

Rents & Incentives

Prime face rents continued to show resilience; with the level of incentives now showing signs of peaking having stabilised over the second half of 2022. Reflecting the preferences of tenants, face rents in the secondary market have remained stable as tenants focus their interest in prime quality office space leading to a divergence in rental levels between prime and secondary office space.

While incentive levels for both prime and secondary offices in the Melbourne CBD market remain elevated, incentives for prime space have recorded a marginal decline, reflecting the increased tenant enquiry levels.

Looking ahead, prime office face rents are expected to continue increase, with incentives beginning to moderate, leading to effective rental growth for prime office stock in the Melbourne CBD market. In contrast, rental growth for secondary offices is likely to remain modest for the medium term until the vacancy rate has peaked.

Sales Activity

Despite the subdued leasing environment, sales activity in Melbourne’s CBD office market has surpassed $3.6 billion in 2022, its highest third annual level over the past decade, a 46% increase on levels the preceding year. Transactional activity was relatively subdued in the second half of 2022 with purchasers cautious given the increasing cost of capital.

Transactional activity across the CBD office market this year has been dominated by domestic institutions boosted with a number of major transactions such as Charter Hall’s 50% share of Southern Cross Towers. With sales activity above average for the past four consecutive years, investment activity is expected to fall below average levels in coming years with the cost of capital likely to remain elevated through 2023.

Foreign investors continued to be attracted to the Melbourne CBD office market, accounting for 44% of total office sales volume over 2022, albeit with some domestic purchasers