4 minute read

Beverage TECH

TRENDS IN FORMULATING, PROCESSING, PACKAGING & CONSUMPTION OF BEVERAGE PRODUCTS

Premiumization's Pause: Beverage Alcohol's Stalled Ascension in the Shadow of Inflation

By Paul Ongeto

Over recent years, the beverage alcohol industry has seen a consumer demand trend in the direction of more “premium” products, i.e products characterized by an increased focus on flavor, highquality ingredients and more appealing packaging.

Increasing societal wealth, broader options for high- quality products and categories, and consumer appreciation for production and origin have been the main drivers behind this trend.

However, recent economic pressures and geopolitical uncertainties have cast a shadow on this trajectory, prompting a critical question: is premiumization taking a pause?

The Rise And Promise Of Premiumization

“Premiumization across beverage alcohol has been an ongoing trend for over 20 years, particularly among wine and spirits,” says Brandy Rand, the COO of the Americas at IWSR Drinks Market Analysis during an interview with Beverage Alcohol Insights.

The desire for higher quality drinks, at premium prices, particularly thrived during the pandemic as consumers restricted from going out to their favorite restaurants and bars, resorted to spending their discretionary budgets on luxury experiences they could bring into the home, such as make-at-home cocktails, and sophisticated wines and spirits. According to IWSR, premiumization in spirits and wines was broad-based across many geographies during the height of the Covid pandemic. Globally, according to the drinks market analysis firm, premium-and-above brands (excluding baijiu) grew 6% compared to 2019.

The trend gathered pace post-pandemic. Overall, a survey by IWSR revealed that 33% of Americans said they had spent US$50 or more on a bottle of alcohol in 2022, against just 24% in 2021. In addition, most drinkers enjoyed their alcohol at home and 46% of those surveyed said they are likely to treat themselves to premium options there – a factor which is particularly beneficial for wine and beer.

People spending more money on better quality beverages also tended to drink less often, something that impacted volumes. Data from IWSR show that while total volumes of wine (-2%), beer (-2%) and cider (-4%) all declined in 2022, the premium-and-above segments of each grew: wine (+6%), beer (+4%) and cider (+11%). Total spirits volumes were up +2%, with premium+ up +13%, while RTDs showed moderate gains at less than +1% with premium+ up +38%.

British alcohol drinks company Diageo saw an opportunity in premiumization early on and developed a multi-faceted approach to drive growth by catering to a shifting consumer landscape. The company acquired premium brands like Don Papa Rum and intensified its focus on super-premium segments like Tanqueray gin, Johnnie Walker, and The Singleton. This strategy paid off handsomely for the London-based company. According to its recent financial results, premium plus brands contributed 57% to net sales growth and 65% to organic sales growth in the first half of fiscal 2023. Its super-premium-plus brands aided organic net sales by 12%.

Challenges In The Era Of Inflation

The long-running premiumisation trend in beverage alcohol however weakened significantly in the first half of 2023, as consumers felt the full impact of economic pressures and geopolitical uncertainty. For example, in H1 2023, consumption of premium-and-above spirits went into reverse vs H1 2022 in markets including Brazil, Colombia and the UK. Meanwhile, volume declines in premium-plus Cognac and Armagnac were driven by a double-digit drop in the US – due to the cost-of-living challenges.

Emily Neill, COO Research at IWSR, confirms this, stating, “The growth rate of premium-and-above products weakened significantly across beer and spirits during the first half of 2023, although their share of overall category volumes broadly continued to increase,” notes Emily.

“Economic pressures did not relent, as inflation remained high –a backdrop that was more globally widespread than during the same period last year. Geopolitical uncertainty from the war in Ukraine heightened the pressures mounting on brand owners, which passed on increased costs to consumers.”

The effect of inflation is particularly pronounced in emerging markets where even slight price increases disproportionately impact households. In Kenya, for instance, a recent report by the National Campaign Against Alcohol and Drug Abuse (Nacada) cited by the Daily Nation revealed that consumers are increasingly trading down premium alcohol brands for cheaper ones and in the extreme cases traditional brews due to a high cost of living that is greatly constraining their budgets.

Diageo is already feeling the heat of depremiumisation of beverage alcohol. The Guinness to Johnnie Walker drinks maker recently issued a profit warning as a result of cashstrapped customers in Latin America and the Caribbean consuming less alcohol and seeking cheaper brands.

A Glimmer Of Hope

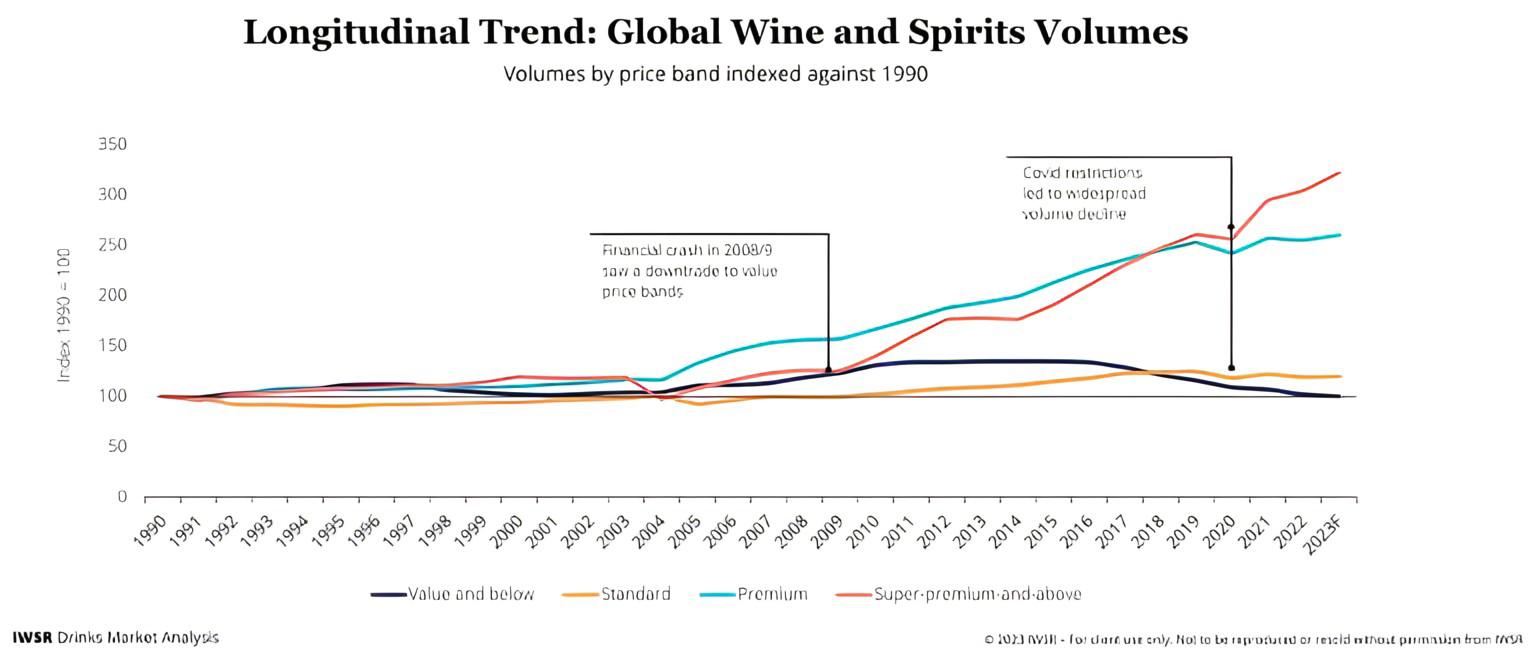

Despite the overall downturn, there are glimmers of hope for premiumization's future. A historical analysis reveals that premium-plus products have shown resilience during past economic crises, such as the 2008-09 financial crash. During this period, consumers traded down to value-priced products, but premium-plus options proved surprisingly resilient.

IWSR predicts a similar scenario playing out in the current economic climate. Emily Neill even points out evidence of premiumization in H1 2023, particularly in spirits and beer. She suggests that beer might be one of the few gainers during this period, as consumers trade down from other categories. “Beer is generally more affordable, including premium variants,” she says.

As premiumization decelerates, beverage alcohol makers need to analyze its evolution across different categories and regions. "Despite overall category declines, pockets of premiumisation still exist in many markets," says Neill.

One of these markets is China where premium-and-above spirits volumes rose by +2% in H1 2023 versus H1 2022, or by +7% if national spirits are excluded – a return to prepandemic levels. Other hotspots in the region, according to IWSR, include India, the Philippines and Thailand.

How will the global alcohol industry fare amid these latest threats to its prosperity? IWSR says that as a discretionary purchase, it is likely to lose some volume as less well-off consumers rein in spending. The drink market analysis is however optimistic of a rebound. “While volatility may persist in the short term, the longerterm picture is one of stability,” it says.