9 minute read

The Challenge for Large-Scale CleanTech Innovation – From Start-Up to Scale-Up

AUTHOR: Taus Nöhrlind

In just a few decades, companies engaged in some kind of technology, concept or solution dealing with the environmental impact of how we produce, live and consume have sored. That’s obvious to anyone. According to Statista.com, the global market for clean energy technology was USD 326 billion in 2023 and the global waste recycling market was an estimated USD 58 billion in 2022. These markets are expected to grow considerably over the coming years.

With the constantly growing focus on reducing carbon emissions, developing sources of clean energy and reducing, reusing and recycling waste, it only makes good sense for our world to support the innovation and expansion of any such technologies serving these purposes.

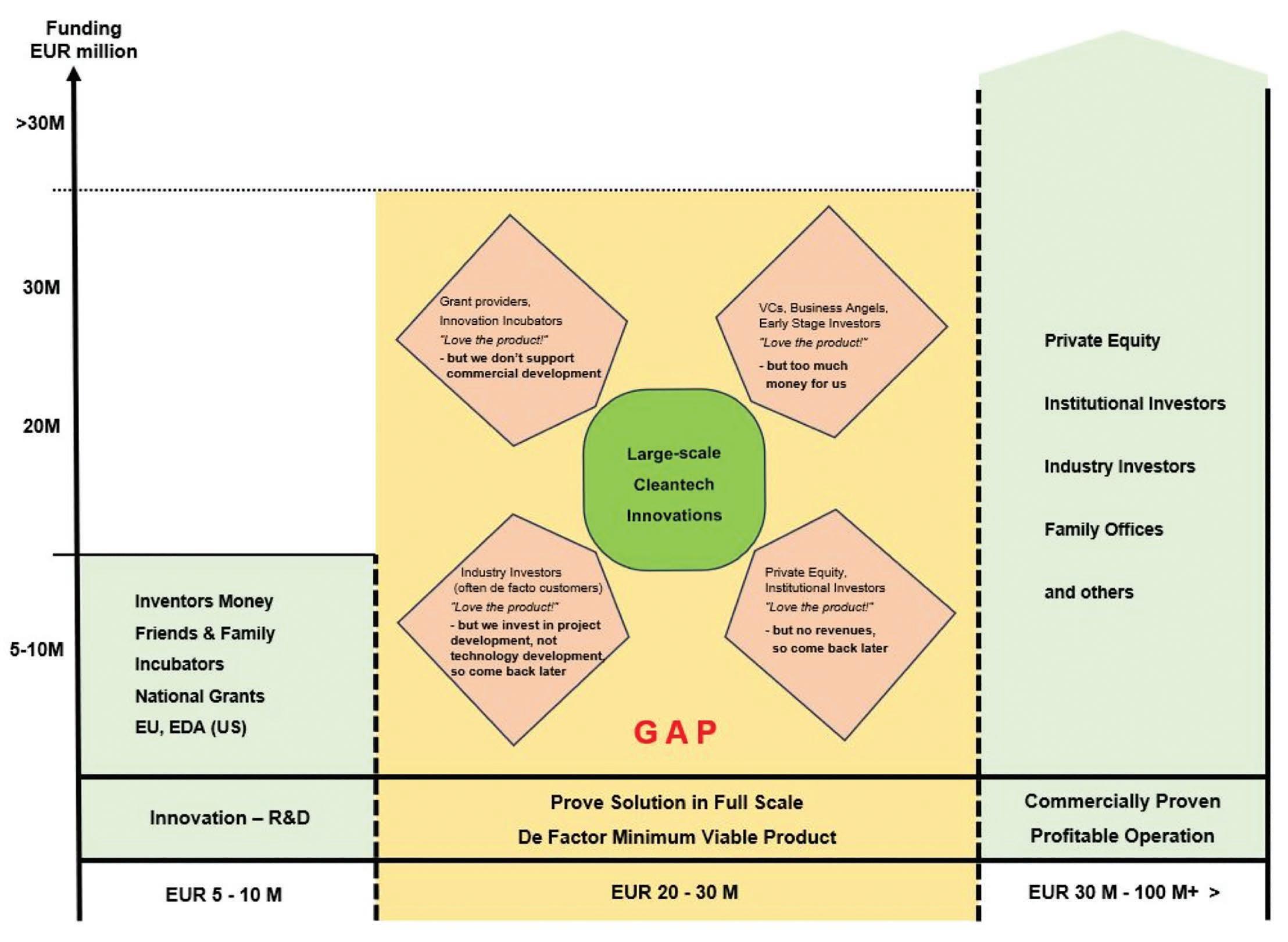

Supporting innovation is happening on many levels. For early stage R&D initiatives, grants from national governments, the EU, the EDA (US) and the like are available, combined with the inventors’ own funds and efforts, and supplemented by the occasional private funding on business angel level.

The challenge for large-scale cleantech innovation is the gap they fall into when having completed the innovative developments and having tested the solution on pilot plant or demonstrator level. They are ready for the next step, setting up or building a full-scale version of their technology – often what they would call their MPV (Minimum Viable Product). They are now often outside the scope of support from the various grant sources, but still not at a level where the first version full-scale technology is proven to be commercially viable – making the professional investors reluctant to get on board.

Three cases of large-scale cleantech projects with this challenge: FIRST CASE:

Wave Dragon

The problem for the world is building renewable energy capacity as fast as possible and at the same time ensuring cost-efficient production, to reduce the carbon footprint from the traditional sources of energy generation. One of the key constraints for building capacity is location, having enough surface space available. The obvious place to look is offshore – ample ocean space is available. So it is with good reason, that floating wind is experiencing a surge in interest and test deployments. Add ocean energy to this, and we certainly have deployment space worth exploring. The key focus for successful exploitation is on optimising the efficiency of the energy technologies, securing access to grid connection etc. targeting how to reach an acceptable cost per kWh for society.

IRENA (International Renewable Energy Agency) estimates that the wave energy potential is some 29.500 TWh per year, more than the total global electricity consumption (estimated to be around 22.500 TWh in 2022; Statista.com). Combining wave energy with wind energy could double the energy potential within the same exploitable surface area. Now we’re exceeding an energy potential of more than twice the global electricity consumption.

Wave Dragon is an offshore floating platform converting waves and wind energy into electricity. It offers some of the largest unit sizes in the offshore arena, featuring capacities from 3 MW to 38 MW per unit, which equates to one unit being able to generate enough electricity to power from worldwide every year. More than half of the raw material for this is coming from recycled sources.

Through this development process, the technology has been pivoted several times, and with a recent pilot plant operation, EnviraBoard is now ready with the 3rd generation technology.

During the production process, using the recycled waste as raw material, around 30% of the mass entering production ends up as waste, so now a secondary waste. EnviraBoard has developed a proprietary and patentable technology to use this secondary waste as raw material to produce high-quality and versatile building boards for the construction industry. Using this secondary waste as raw material, instead of disposing of the waste via incineration, which seems to be a commonly used disposal method of several possibilities, the process offers a significant reduction in the carbon footprint. The EnviraBoard boards themselves offer properties and qualities which exceed many of the commonly used building boards.

Industry sources suggest we may have up towards 10.000 paper mills in the world of which a few thousand operate with a recycling facility – hence they have this costly waste disposal problem with their secondary waste.

2.000 homes up to 30.000 homes. Wave Dragon is highly scalable and connecting several units creates utility-size power plant capacity.

Some EUR 15 million has been invested in the development, and the next step is the construction of a 3 MW commercial power plant unit. This being Wave Dragon’s MVP, the showcase of what customers would buy – is this considered completion of innovation and technology development? Or is it the first step into the commercial arena? Many private investors say this is technology development, and many grant providers say this is commercial development!

SECOND CASE: EnviraBoard

The problem for the world is dealing with huge volumes of waste resulting from newspapers, magazines, cardboard and similar paper and packaging products. According to BIR (Bureau of International Recycling), more than 400 million tonnes of paper and cardboard are produced

During the years of developing the EnviraBoard technology some EUR 20 million has been consumed in the process. Through this development process, the technology has been pivoted several times, and with a recent pilot plant operation, EnviraBoard is now ready with the 3rd generation technology. The next step is building a full-scale factory to produce the building boards. The factory will be EnviraBoard’s MPV and the showcase to the world, and what customers would buy – is this considered completion of innovation and technology development? Or is it the first step into the commercial arena? Many private investors say this is technology development, and many grant providers ay this is commercial development!

THIRD CASE: Papiro

The problem for the world is dealing with huge volumes of plastic and glass waste. More than 500 billion PET plastic bottles are produced every year. Papiro’s mission is to reduce the impact of plastic and glass food and beverage packaging by introducing a recyclable and compostable natural fibre bottle. Mismanaged plastic waste threatens the biosphere and contaminates food chains. In addition, the production of plastic and →

→ glass relies heavily on fossil fuels. Papiro uses renewable, plant-based materials to produce beverage containers and closures compatible with paper and compostable recycling streams. The Papiro solution is patented, and the process can be adapted to different plant-based fibre types, taking advantage of local sourcing of raw materials, and implementing local bottle production, minimising transportation costs.

The Papiro development activities are ongoing at DTU (Technical University of Denmark), and funding so far has been grants and university support, besides the significant efforts and contributions from the team engaged in the development activities.

When R&D has been completed at university level, the natural next step is building a full-scale factory to produce the sustainable bottles. The investment to build such a factory is so far estimated in the range of EUR 20-30 million. The factory will be Papiro’s MPV and a showcase to the world, and what customers would buy – is this considered completion of innovation and technology development?

Or is it the first step into the commercial arena? Many private investors say this is technology development, and many grant providers say this is commercial development!

The shared challenges

Common for the 3 outlined projects, as for many other large-scale cleantech innovations, is that they share the gap they are faced with. The gap between growing out of the innovation and development phase and reaching the commercial stage –but without having proven to be commercially viable with the full-scale technology – a gap which requires funding at the level of EUR 20-30 million for many of such large-scale cleantech initiatives.

The challenge is, that funding for the first full-size entity is beyond what venture capital providers typically invest. Private equity finds the capital need and the investment level interesting, but mainly wants to invest in revenue generating businesses. Industry players tend to focus on project and production development and categorise such investments more as a technology development. So that’s the gap to be closed!

Nothing is black or white – Some funders in the market will take a punt and support the large-scale cleantech developments. But it comes with significant efforts and resource allocation for the cleantech innovators, to overcome this challenge, identify the funder and close the gap.

The need for a twodimensional business model

Another commonly shared challenge for his kind of large-scale cleantech development is the need to focus the commercial development on a two-dimensional business model.

They need one business model and strategy for selling the output from their production, whether that is kWh, cubic meters, square meters, kilograms, tonnes, litres, pieces, or other units.

Then they need a second business model and strategy for succeding with selling their production plant/set-up – and here they are faced with the many delights of very diverse international environments when it comes to the regulatory conditions.

Expanding large-scale cleantech companies internationally Cleantech companies have to operate in the zone between taking a professional commercial approach to developing their business with a focus on the bottom line –and at the same time being hugely impacted at national policy levels; the national and local regulations, required approvals, environmental impact assessments, needed consents etc. All this comes at a huge expense in time and money, not only from what is required of knowledge and manpower internally but often the need to hire local expertise in the form of consultants and advisors, to navigate the local complexities. Different countries have different regulations, standards, and procedures that must be followed, making it challenging to replicate a success achieved in one market to another market. Many local factors such as energy infrastructure, waste recycling culture, consumer behaviour, support mechanisms and economic conditions all play a role in how cleantech companies succeed in particular markets.

To address this hurdle, cleantech companies must as traditionally done when internationalising, conduct thorough market research, including understanding the local demand for their products, consumption behaviour, and identifying potential competitors. All this leads back to the funding gap as outlined – The diverse regulatory environments, and the long time it often takes to make headways within the complexities of regulations, means that more money is needed earlier on to account for these long sales cycles and market penetration times. Hence the gap is getting deeper with more money needed up front.

What Policy Makers can do!

Cleantech companies are paving the way for a cleaner, sustainable future. As consumer awareness continues to increase and demand for clean products, solutions and technologies rises, even greater growth in the cleantech sector will be the result. Across the world, it is often experienced that the mindset and approach of professional investors are fairly similar and a company seeking to raise funding is faced with good consistency in the due diligence questions they are met with. Once you got the documentation and foundation in place as a company on a fundraising mission, you are reasonably well-dressed to engage with investors regardless of their geographical location.

On the policy side, on national and regional levels, incentive programs, tax breaks, capital grants, and revenue subsidies are made available to support the development and deployment of clean technologies. However, there are significant complexities around what is offered and how to qualify for the support, and the minute we look across different jurisdictions, the regulatory environments and the consent and compliance processes differ immensely. What is urgently needed is a much stronger focus on aligning these policy mechanisms cross-boarders, to facilitate a faster and more efficient development and buildout of large-scale clean technologies. As much as regional and national interests often tend to support “companies in our own backyard”, we are all on the same side of the table when it comes to mitigating any negative impact of production and consumption on all levels in our societies.

Simplification of the policy foundation would ideally comprise three areas:

1. Capital grant support with high levels of funding for the innovation activities. (Grant support is often seen from as low as 30% up to 50%-70% and only in a few selected cases 100%. More substantial support will facilitate reduced innovation times).

2. Long-term stable revenue support for innovations ready to step into the gap-phase. (Revenue support will offer financial predictability. From investor perspective, when they engage in due diligence, only technologies which appear to be commercially sound and viable would get funding – hence saving tax-payers money by not offering capital grants in the gap-phase of the technology development, reducing the risk of supporting questionable technologies).

3. Aligning the regulatory environments between countries, will significantly facilitate a less complicated geographical expansion of good sound large-scale cleantech technologies. No doubt, this is the major hurdle to tackle.

Is all this utopia? For many cleantech companies, it is! But to the benefit of us all, this is the direction we need to move in. The world is changing – fast! So hopefully experiences of the past will not be the way of the future! ■