Operators, suppliers & affiliates discuss what it takes for European firms to succeed stateside From Vegas penny slots to advertising in India, our columnists deliver We run through the victors at the Global Gaming Awards Asia COMING TOassessesAMERICAthepast,futureandpresent of live gaming WINNERS REVEALED

Grover Ho Grover.Ho@gamblinginsider.comTel:+44(0)2034355628

DESIGN ASSISTANTS

COO, EDITOR IN CHIEF

ALEXIA SMILOVIC RØNDE Relax Gaming, Chief Regulatory O cer

COMMERCIAL DIRECTOR

STAFF WRITERS

Peter Lynch Peter.Lynch@gamblinginsider.com Matthew Nicholson Matthew.Nicholson@gamblinginsider.com

JUNIOR STAFF WRITER Louis Thompsett Louis.Thompsett@gamblinginsider.com

ADVERTISING SALES EXECUTIVE - U.S. Ariel Greenberg Ariel.Greenberg@playerspublishing.comTel:+1.7028339581

Clive Waite Clive.Waite@gamblinginsider.comTel:+44(0)2077290643

t is that time of the year again: network time, pitch time, partnership time and maybe even M&A time. I'll stop short of saying party time á la Joey Tribbiani. Although, I'm sure plenty of our readers will grace the industry networking scene at G2E Las Vegas – or any other show you're attending over the next few months.

It's a wide-reaching topic, so we've provided as comprehensive an outlook as we can on the European firms looking to tackle the North American market in the coming months and years: how the market will pan out, the pitfalls to avoid and more.

With so much of our sector heading to Las Vegas for the trade show, there is of course a much larger migration to Las Vegas and the wider North American market in progress, on an industry-wide scale. That's why our main theme for the September/ October edition is Coming to America, addressing this migration from a 360-degree viewpoint: the supply side, the operator view and the a liate take.

On our cover, Interblock Global CEO John Connelly is symbolically welcoming you to G2E and the American market. In our exclusive interview with the industry veteran (page 32), he talks us through how Interblock went from a European table game supplier to a global company with a US hub. Joining him are suppliers Yggdrasil, BetConstruct, Relax Gaming and Kambi (page 36), operators Betfred (page 40) and Kindred Group (page 46), consultancy Fast O shore (page 48) and a liate BestOdds (page 50).

DESIGNERS

Radostina Mihaylova, Svetlana Stoyanova, Gabriela Baleva

CREDIT WITHRachelMANAGERVoitTHANKSTO: John Connelly, Alexia Smilovic Rønde, David Bretnitz, Björn Krantz, BetConstruct US team, Stephen Crystal, Liv Biesemans, Ron Mendelson, Will Armitage, Bill Miller, Korbi Carrison, Jeevan Jeyaratnam, David Bonnefous, Dean Nicolls, Je Millar, Yury Ermantraut, Simeon Hristov, Irina Cornides, Lee Richardson, Clive Cottrell, Anne Hay, Leighton Webb, Ranjana Adhikari, Gustaf Hoffstedt, Rob Ziems, Matthew Kelemen, Hamza A , Martin Cheek, Dr Joerg Hofmann

ACCOUNT MANAGERS William Aderele William.Aderele@gamblinginsider.comTel:+44(0)2077392062

JEFF MILLAR Evolution, Commercial Director North America

MARKETING & EVENTS MANAGER

Earlier in the magazine, we celebrate the winners of our inaugural Global Gaming Awards Asia (page 28), with the Global Gaming Awards Las Vegas also set to take place during G2E week. Asia's growth is not lost on this particular Editor so, while we have a heavy US focus in this issue, expect more on the Asia-Paci c region in the November/ December edition of the magazine.

EDITOR’S LETTER

Elsewhere in the issue, I'd like to single out industry experts Gustaf Ho stedt (page 82) and Alex Czajkowski (page 83) for their best articles yet; the former arguing against state-run gambling companies, the latter arguing in favour of penny slots in Las Vegas.

Mariya Savova

Julian Perry

BUSINESS DEVELOPMENT MANAGER Michelle Pugh Michelle@GlobalGamingAwards.comTel:+44(0)2077395768

Deepak Malkani Deepak.Malkani@gamblinginsider.comTel:+44(0)2077296279

SENIOR BUSINESS DEVELOPMENT MANAGER - U.S. Aaron Harvey Aaron.Harvey@playerspublishing.comTel:+17024257818

Fantini Research, GBGC, Enrico Bradamante,

TP, Editor

EDITOR

Julian Perry, COO, Editor in Chief

Tom Powling

I

Olesya Adamska, Christian Quiling

Tim Poole Tim.Poole@gamblinginsider.com

SENIOR ACCOUNT MANAGER Michael Juqula Michael.Juqula@gamblinginsider.comTel:+44(0)2034870498

Dr Joerg Hofmann rounds o the magazine in our Final Word section (page 98) with a – hopefully promising in the long term – regulatory update in Germany. We also have a Product Review section packed with land-based o erings (page 90), and a UK horseracing section featuring industry veterans Lee Richardson (page 72) and Clive Cottrell (page 74). While we hope you enjoy G2E, we know you'll enjoy reading!

LEAD DESIGNER Brendan Morrell

FINANCE AND ADMINISTRATION ASSISTANT Julia Olivan

Gambling Insider magazine ISSN 2043-9466Produced and published by Players Publishing Ltd All material is strictly copyrighted and all rights reserved. Reproduction without permission is forbidden. Every care is taken in compiling the contents of Gambling Insider but we assume no responsibility for the e ects arising therefrom. The views expressed are not necessarily those of the publisher.

Tim Poole, Editor

IT MANAGER

FEATURED IN THIS ISSUE

32 Coming to America

LIV BIESEMANS IRINA CORNIDES

AWARDSGAMINGGLOBAL

46 Uniting fragmenteda market

08 Facing Facts

12 In numbers

24 Life after M&A

BestOdds Co-Founder Will Armitage discusses the challenges European affiliates face moving into different US markets

Asia: The winners revealed FEATURESCOVER

20 Taking stock

40 Beware the shake out Stephen Crystal, Head of North America Development for Betfred, speaks to Gambling Insider about the operator's US migration from Europe

A gaming snapshot by Fantini Research, this time looking at data from Pennsylvania

50 An affiliate's take

644636

ISSUES

Pariplay CCO Enrico Bradamante speaks to the GI Huddle about the NeoGames merger and its aims for the North American market

28 Global Gaming Awards

Interblock Global CEO John Connelly discusses the supplier's growth in the US market

Global Betting & Gaming Consultants, the global gaming data expert, provides exclusive data to Gambling Insider

HUDDLE

18 The global outlook

Ron Mendelson of iGaming consultancy Fast Offshore outlines the progress of the biggest European operators in the US market

BJÖRN KRANTZ

Gambling Insider takes a close statistical look at financial results for Q2 2022

C ONTENTS

36 The supplier story so far Gambling Insider speaks with Relax Gaming, BetConstruct, Kambi and Yggdrasil about how European suppliers are faring in the US so far

48 The consultant's viewpoint

We track operator and supplier stock prices across a six-month period

Liv Biesemans, Group Deputy General Counsel at Kindred Group, discusses Kindred's US development, via its flagship Unibet brand

ONTENTS

Evolution, Atmosfera, Amusnet and Pragmatic Play evaluate how live gaming has evolved, why the vertical is so popular and what the future holds The bettingsecond-favouritenation'ssport

RMG Director of Marketing Clive Cottrell speaks exclusively to Gambling Insider about bringing horseracing to younger audiences The US payments problem

82

54 G2E Las Vegas preview

83

INSIDERS 85 Rob

89 Martin

56

PayNearMe's Anne Hay and Leighton Webb talk through the issues surrounding deposits and withdrawals in the US

Advertising in India

86 Adrian Bailey Pariplay 88 Hamza

How have risk management strategies developed to reduce live trading debt? Do you know who I am?

FINAL WORD 98 Dr Joerg Hofmann Melchers Law 78 88 98

JOERG HOFMANN

FEATURES

HAMZA AFIFI

Gambling Insider looks at the upcoming G2E trade show in Las Vegas Big Question

SmartSearch REVIEWSPRODUCT 90

Lee Richardson MBA, CEO of Gaming Economics, discusses the overall state of horseracing in the UK

Roundtable: Innovation in live gaming

Ranjana Adhikari and her associate at IndusLaw, Arjun Khanna, discuss the gambling advertising situation in India The case for burning gambling profits

64

72

Aruze

74 The Holy Grail of the sport

Gustaf Hoffstedt contemplates the morally contentious points associated with being a state-owned gambling organisation We love penny slots

60

80

78

Alex Czajkowski assesses how macroeconomic indicators can influence the determination of optimal wager amounts Ziems Gaming Afifi Soft2Bet Cheek What's new in land-based gaming?

Oosto CMO Dean Nicolls discusses facial recognition inside casinos

ANNE HAY

Gambling Insider takes a closer look at some of the new products now available on the casino floor

FEATURES NUMBER CRUNCHING

million)(€Revenue million)($Revenue

Source: Macau Gaming Inspection and Coordination Bureau (DICJ)

Comparing Macau Q2 2021 and Q2 2022 gross gaming revenue (MOP billion)

2021 2022

• Total Q2 2022 revenue amounted to $1.05bn

• Despite respite in May that saw a slight increase, revenue was straight back down again for June

• Q2 2022 revenue totalled €343.9m ($350.1m)

Source: Evolution

• All three months reported year-on-year declines

8 GAMBLINGINSIDER.COM

2021 2022

Las Vegas Sands revenue for Macau Operations, Q2 2022 ($ million)

Source: Las Vegas Sands

billion)(MOPGGR

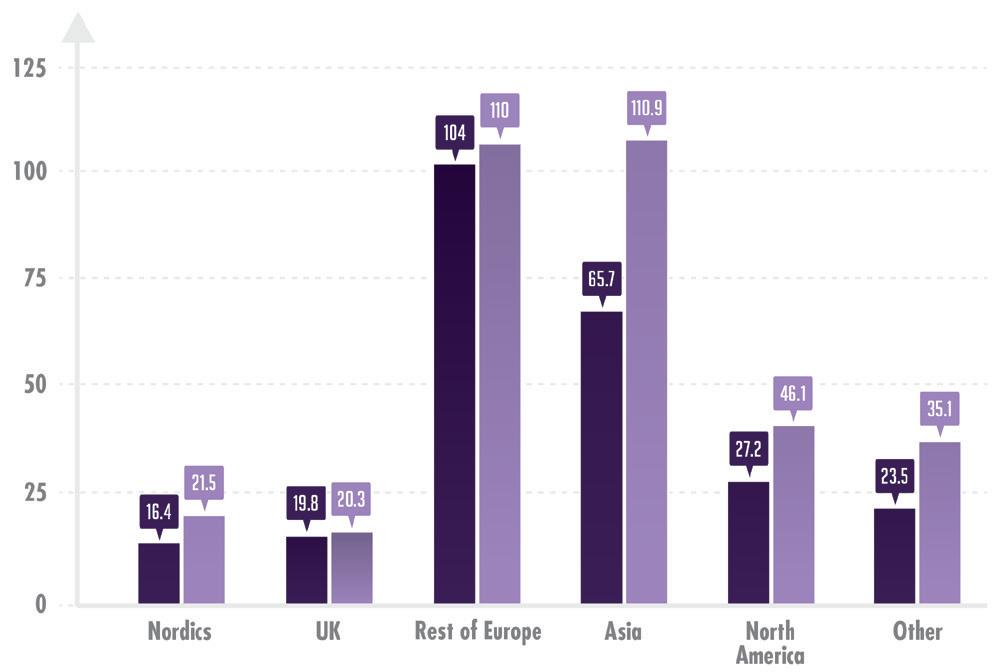

Comparing Evolution Q2 2021 and 2022 revenue per geographical region (€ million)

Gambling Insider presents data from Q2 2022 results across the industry. Which operators and suppliers fared well? And which markets proved most lucrative?

2021 2022

• Macau Operations declined 56% year-on-year from $855m to $374m

• Evolution's main region was Asia, followed by the 'Rest of Europe' market

FACING FACTS

million)($Revenue

•Live and Historical Racing was the only segment to increase year-on-year 2022 2022

million)($Revenue million)($Revenue million)($Revenue

• Q2 2022 total revenue amounted to $894.5m

• Revenue increased 18% year-on-year

Comparing Q2 2021 and 2022 revenue for three major Swedish companies ($ million)

Comparing Monarch Casino & Resort (Reno, Nevada and Black Hawk, Colorado) Q2 revenue, income and adjusted EBITDA ($ million)

•Record net revenue of $582.5m

Source: Boyd Gaming Corporation

Source: Monarch Casino & Resort

• However, Kindred and Kambi (supplier) revenue decreased year-on-year, Svenska Spel (operator) increased

9GAMBLINGINSIDER.COM

Comparing Boyd Gaming Corporation Q2 2021 and 2022 revenue by segment ($ million)

• Income and adjusted EBITDA increased 7% and 12% respectively year-on-year

NUMBER CRUNCHING

Source: Churchill Downs Incorporated

FEATURES

2021 2022 2021

2021 2022 2021

Comparing Churchill Downs Incorporated Q2 2021 and 2022 revenue per segment ($ million)

Source: Company reports

• Kindred Group (operator) reported the highest revenue for both years

• Las Vegas Locals and Downtown Las Vegas revenue was up year-on-year, while Midwest & South was down

Source: International Betting Integrity Association (IBIA)

from Q1

• Football provided by far the most alerts, although esports alerts are on the rise and tennis remains problematic as a sport

Betsson Q2 revenue by region and product (€ million)

• The 88 alerts spanned 36 countries

• Total revenue amounted to PHP 8.96bn ($160.4m)

Q2

*CEECA = Central and Eastern Europe and Central Asia

to

• Total Q2 2022 revenue amounted to $3.26bn

quarterly

10 GAMBLINGINSIDER.COM 203040100 Football Tennis Horseracing Esports Basketball Handball GreyhoundRacingTennisTable IBIA suspicious betting alerts for Q2 2022 32 27 8 3 1 12 4 1 14320 VIPGamesTable Mass Market Table Games MachinesGaming Comparing Tiger Resort Q1 2022 and Q2 2022 revenue by segment (PHP billion) ($million)Revenue 2.54 3.24 1.53 2.19 1.95 2.86 Comparing Tiger Resort (Manila, Philippines) Q1 2022 and Q2 2022 revenue by segment (PHP billion) Q1 2022 Q2 2022

• This was a huge 44% increase year-on-year

Comparing MGM Resorts 2021 2022 revenue by segment ($ million)

International

Source: Tiger Resort

2022

• This represented a 40% increase 2022 Q2

Source: MGM Resorts

Source: Betsson

*ceeca33.0% western13.0%europe latinnordics27.0%25.0%america rest of 2.0%world casino66.0%sportsbook33.0% Other1.0%

and

2021 2022 billion)(PHPRevenue million)($Revenue

• Q2 2022 revenue amounted to €186.3m ($190.4m)

• Organic growth for the period was 13%

IBIA suspicious betting alerts for Q2 2022

2022

South Philly Turf Club (Greenwood) $0.194 -43.42

CASINO PROPERTIES

JUNE REVENUE (M)

Parx at Malvern (Greenwood) $0.044 N/A

Hollywood (PENN) $57.616 +5.18

Live! Pittsburgh (Cordish) $8.168 -2.37

Fantasy Sports $1.506 -20.39

PENNSYLVANIA: Pennsylvania’s June figures capped off a record-breaking 2021/2022 fiscal year for the Keystone State, where annual gaming revenue surpassed $5bn for the first time. June’s figures highlight a continued resurgence from Pennsylvania’s land-based operations.

Harrah's Philadelphia (CZR) $14.057 -9.72

Mount Airy $19.563 -12.03

The Meadows (PENN) $18.067 -13.54

CHANGE (%) YEAR-ON-YEAR

Mohegan Lehigh Valley $0.041 -72.10

Total $399.948 +1.14

Slot Routes $3.507 +6.15

Caesars Interactive $3.266 N/A

Valley Forge (BYD) $39.330 -13.69

In partnership with Gambling Insider, Fantini Research provides data from around the US; in this issue, we analyse June revenue gures from Pennsylvania

Presque Isle (CHDN) $8.983 -13.59

Wind Creek Bethlehem $42.007 +15.25

Mohegan Sun $20.653 +8.68

Lady Luck Nemacolin (CHDN) $1.724 -14.41

Hollywood York (PENN) $7.279 N/A

IN NUMBERS

Parx (Greenwood) $52.392 -9.93

Rivers (Rush St) $29.384 +2.17

12 GAMBLINGINSIDER.COM NUMBER CRUNCHINGISSUES

Hollywood Morgantown (PENN) $7.057 +120.26

Rivers Philadelphia (Rush St) $42.783 -2.25

Live! Philadelphia (Cordish) $22.328 +8.49

NUMBER CRUNCHINGISSUES

ENT/MGM -19.37

Rivers Philadelphia $0.802 RSI -59.36

FLTR (FOX Bet) -57.96

Hollywood $1.793 PENN -48.40

Live! Philadelphia $0.274 SGHC -57.36

www.FantiniResearch.com

Valley Forge $10.190

Parx at Malvern $0.044 Greenwood N/A

FLTR (FanDuel) -49.27

Hollywood York $0.700 PENN N/A Mount Airy $0.400

Mohegan Sun Pocono $0.225

Harrah's $0.043 CZR -61.99

Mohegan - Lehigh Valley $0.041 Kindred -72.10 Wind Creek $0.036 Betfred -56.83

Total Sports Betting $22.890 -46.14 Handle $393.494 -6.35

14 GAMBLINGINSIDER.COM

Parx $1.261 Greenwood -32.64

SPORTS BETTING: Despite Pennsylvania’s land-based casino rebound, sports betting took a marked dip in June. The Keystone State's sports betting numbers traditionally start to pick up again from August due to the sporting calendar; however, the figures below still show year-on-year falls across the board, with Presque Isle even suffering a three-figure percentage drop.

Kindred -56.90 South Philly Turf Club $0.194 Greenwood -43.42

Live! Pittsburgh $0.064 RSI -53.67

Rivers $1.321 RSI -27.52

Presque Isle ($0.082) CHDN -114.04

Hollywood Morgantown $2.583

The Meadows $3.000 DKNG -54.09

MORE IMPORTANT THAN YOUR MORNING COFFEE

SPORTS BETTING JUNE REVENUE (M) OPERATOR CHANGE (%) YEAR-ON-YEAR

Rivers

Parx

Presque

SPORTS BETTING:

Multiple Operators – Of the operators working on multiple sites, Flutter Entertainment's FanDuel brand led the way in the Keystone State once again. FanDuel's lead is no surprise but Penn Entertainment's Barstool Sports generated over $4m in sports betting revenue, with Rush Street Interactive (RSI) following, then Greenwood Gaming and Kindred Group.

$0.284 CHDN

16 GAMBLINGINSIDER.COM

iGaming Total $102.924

IGAMING: Pennsylvania’s sportsbook slump has been made up, in part, by vastly increased revenue from the state’s iGaming sector. Relationships can be drawn between the Keystone State’s improved land-based returns and iGaming revenue, as US operators continue to integrate and homogenise their online and offline offerings.

THAN YOUR MORNING COFFEE

MULTIPLE OPERATORS

JUNE REVENUE (M)

Flutter (FLTR) $10.929

Barstool $4.377 RSI $2.122 Greenwood $1.499 Kindred $0.266

NUMBER CRUNCHINGISSUES

www.FantiniResearch.com MORE

Caesars

Mohegan $2.245 Kindred

Mount

Wind BethlehemCreek $1.233 Wind

Live!

IGAMING

Valley

JUNE REVENUE (M) OPERATOR CHANGE (%) YEAR-ON-YEAR Hollywood $42.030 DKNG, ENT/MGM, PENN +20.53 Philadelphia $25.484 RSI, MGM +9.20 Forge $18.401 FLTR +23.05 Airy $4.183 FLTR -28.54 Interactive $3.266 CZR +90.02 $2.920 Greenwood -18.17 Philadelphia $2.878 +284.28 +5.75 Creek -1.49 Isle -42.12 +15.76 IMPORTANT

Cordish

US commercial casino GGY (US$bn) 2003 – 2020

GLOBAL OUTLOOK: US FOCUS

US gaming machine GGY ranked by state (US$m) for 2020

18 GAMBLINGINSIDER.COM

• In pandemic-hit 2020, US commercial casino GGY dipped more than in the 2007-2008 recession

Global Betting & Gaming Consultants (GBGC), the global gaming data expert, provides exclusive statistical data to Gambling Insider on markets from around the US; visit www.gbgc.com for more

The above graph shows US commercial casino GGY in the period from 2003 to 2020

• Here, New York with its racinos is the leading state, with machine GGY of US$449m in 2020, followed by Illinois' large video gaming sector

The graph shows US states ranked by gambling machine gross gaming yield (GGY) for 2020

FEATURES NUMBER CRUNCHING

• The US gambling machine market consists of slot-only racinos, slot-only casinos and machines found in establishments with a liquor licence

• Due to its relatively small population size, but large Native American gambling industry, Oklahoma is the leading state by Native American gambling GGY per adult

• Lottery sector leads the way, closely followed by commercial casinos and Native American gambling

The graph shows top 20 US states ranked by GGY (US$bn) in 2020. The GGY is derived from all gambling sectors

The graph shows % of gross gambling yield (GGY) from each gambling vertical for the US gambling market in 2020

The graph shows the top 15 US states ranked by Native American gambling GGY per adult (18+)

Leading 20 US gambling states by GGY (US$bn) for 2020

• Due to its large Native American gambling industry, California leads the way, followed by Nevada due to its commercial casinos

Leading 15 US states by Native American gambling GGY per adult (US$)

19GAMBLINGINSIDER.COM NUMBER CRUNCHING FEATURES

US gambling industry make-up (%) in 2020

month FEATURES NUMBER CRUNCHING

• Market capital - £15.31bn (US$18.49bn) LAS VEGAS SANDS 888 HOLDINGS

WYNN RESORTS

The

20 GAMBLINGINSIDER.COM

- 58.18

OPERATORS high - 40.30 (Mar) low - 35.16 (Jun) capital - US$29.32bn

across

• Market

• Six-month

• high 9,456.00 (Mar) (Aug)

FLUTTER ENTERTAINMENT

• Six-month low - 8,278.00

TAKING STOCK

• Market capital - US$7.74bn • Six-month high - 216.80 (Mar) • Six-month low - 144.40 (Aug) • Market capital - £695.39m (US$839.84m)

-

• Six-month

Six-month

LAS low (Jul)

VEGAS SANDS 20305040100 March US$ April May July AugustJune 888 HOLDINGS 100150250200500 March GBP April May July AugustJune 1001257550250 March US$ April May June WYNN RESORTS OPERATORS FLUTTER ENTERTAINMENT 12,500.0010,000.007,500.005,000.002,500.000.00 March GBP April May JulyJune LAS VEGAS SANDS 20305040100 March US$ April May July AugustJune 888 HOLDINGS 100150250200500 March GBP April May July AugustJune 1001257550250 March US$ April OPERATORS FLUTTER ENTERTAINMENT 12,500.0010,000.007,500.005,000.002,500.000.00 March GBP April May LAS VEGAS SANDS March April May July AugustJune 888 HOLDINGS May July AugustJune 1001257550250 March US$ April May July AugustJune WYNN RESORTS FLUTTER ENTERTAINMENT 12,500.0010,000.007,500.005,000.002,500.000.00 March GBP April May July AugustJune VEGAS SANDS May July AugustJune July August 1001257550250 March US$ April May July AugustJune WYNN RESORTS FLUTTER ENTERTAINMENT 12,500.0010,000.007,500.005,000.002,500.000.00 March GBP April May July AugustJune • Six-month high - 81.64 (Mar) • Six-month

Gambling Insider tracks operator and supplier stock prices a six-month period (March to August 2022). stock price is taken from the first day of each

AU$

March April May July AugustJune

Six-month low - 33.16 (May)

• Six-month high - 13.59 (Mar)

1,250.001,000.00750.00500.00250.000.00

July AugustJune

ENTERTAINMENT AugustJune April May July AugustJune

Market capital - AU$23.7bn (US$16.67bn)

GAMING GROUP

• Six-month low - 163.10 (May)

20

101550 March US$

40

KAMBI GROUP

SEK

March SEK April May July AugustJune April May

• Market capital - US$293.39m

March SEK April May July AugustJune April

ARISTOCRAT 2030100 March AU$

EVOLUTION GAMING GROUP

ARISTOCRAT 2030100 March AU$

KAMBI GROUP

INSPIREDEVOLUTIONENTERTAINMENT ARISTOCRATKAMBI

FEATURES NUMBER CRUNCHING

101550 March US$

SUPPLIERS 40

SUPPLIERS

20

GAMING GROUP

250200150100500

INSPIRED ENTERTAINMENT April May July AugustJune April May

July AugustJune

• Six-month high - 1,063.00 (Mar)

• Market capital - SEK 207.18bn (US$20.32bn)

ARISTOCRAT 2030100

March April May July AugustJune

Six-month high - 36.44 (Mar)

EVOLUTION GAMING GROUP

March April May July AugustJune

ENTERTAINMENT

40

SUPPLIERS 40

• Six-month low - 8.58 (Jul)

ARISTOCRAT 2030100 March AU$

22 GAMBLINGINSIDER.COM

SEK

• Market capital - SEK 5.44bn (US$530m)

July

1,250.001,000.00750.00500.00250.000.00

250200150100500

• Six-month low - 920.50 (Jul)

• Six-month high - 220.40 (Apr)

KAMBI 250200150100500 March SEK

KAMBI 250200150100500 March SEK

INSPIRED ENTERTAINMENT April May July AugustJune April

July AugustJune

FANTASTICAJOURNEYFORMEGOINGFROMTHESUPPLYSIDETOTHEAGGREGATIONLAYEROFTHEBUSINESS"

a year since I became CCO (Chief Commercial Officer).

phenomenal in previous years, and I’m glad to now be responsible for taking this forward.

really great team, a fantastic mix of developing

I have now been in the iGaming industry for the past 10 years. I was Managing Director at NetEnt for the first six years, then I started a few studios as an entrepreneur and 7/8 years ago I joined Pariplay. Time has really flown; I can’t believe it’s coming up to

And, yes, as CCO I also

I’m a big believer in this internal

like years, but it’s only months. I think the When

"IT’S BEEN

LIFE M&AAFTER

24 GAMBLINGINSIDER.COM FEATURES THE HUDDLE

We have been fortunate to have had a lot of things to celebrate over these past 7/8 months – it feels like years, but it’s only months. I think the one achievement I’m most proud of is the team. When I joined, one of my key objectives was to consolidate, build and grow the commercial team. This has now happened. We have commercial functions in our main office in Sofia, Bulgaria, here of course in Malta and we have a commercial office in Gibraltar. We have account managers in those locations and we managed to bring together a really great team, a fantastic mix of experienced professionals, new blood coming from outside our industry and also developing colleagues internally.

fantastic journey for me Pariplay is a very successful company, our growth rate has been

have the responsibility here for the Malta side of things, so I’m the Managing Director here of our legal entity and operations. It’s been a going from the supply side to the aggregation layer of the business, in terms of personal and professional development.

Pariplay CCO Enrico Bradamante speaks to the GI Huddle about its recent acquisition by NeoGames, nding the right balance in Europe and its aims for the ever-growing North American market

In terms of your first year in the role – have you got any celebrations planned for the anniversary? And, more importantly, how do you reflect on your first few months as CCO?

Watch the full video online at gamblinginsider.com/gi-huddle

functions in our main office in

for to

Can you tell us a little bit about your background and your career in gaming before you became CCO last November?

I wanted to pick your brain about the breadth of the B2B offering with iLottery being added in.

From a personal perspective and a Pariplay perspective, there has been essentially zero operational impact on the day-to-day. It’s, of course, a fantastic development for the company and the group to now be a part of NeoGames.

26 GAMBLINGINSIDER.COM FEATURES THE HUDDLE

For Pariplay, the North American market is strategically important as one of our growth engines and we are executing state by state; we expect to be live in Michigan and Pennsylvania very soon, with others following afterwards. We launched in Alberta and Ontario when it comes to Canadian provinces, and I think the key for us as an aggregate is to be the number one aggregator in every market we enter. We have a portfolio of over 80 vendors and over 80 content suppliers on our books. But, for the North American market, we need to have content that is focused on North American players.

We’re doing this within the Wizard portfolio – but there are also existing brands, existing companies that we want to add for a localised offering, which has been a success for Pariplay in our market entries; so for the US, Canada and North America in general we are adopting the same strategy.

development of our talent pool, so I’d say that’s the one significant milestone I’d like to call out.

I’d say it’s been a recipe for success for the current NeoGames Group to have had individual companies focused into their markets, and become market leaders and successful in their own specific area. And subsequently, with the acquisitions of Aspire Global first, and NeoGames now, we continue with this same strategy of having the individual companies retain the brand name, retain the structure, retain the organisation, so that focus is maintained. At the same time, looking for synergy on a commercial level, on a customer level and on a technology level.

We have now created one of the only two companies on the B2B side from the technology perspective that cover the entire spectrum.

"WE ARE EXECUTING STATE BY STATE; WE EXPECT TO BE LIVE &MICHIGANINPENNSYLVANIAVERYSOON"

For Pariplay specifically, I expect this will give us some synergy and market access in the iLottery business, where we’ve not really been present before. From a game development perspective, NeoGames have their own development studio – and within Pariplay we have our Wizard Studio, so there will be some interesting synergy and cross-pollination with the two studios.

Wizard is the product spearheading our entry into the North American market and is being followed by the aggregation business. So, in Ontario for example, we’re also offering third-party vendors and we’re starting to aggregate with Ignite, which is the third-party studio that is leveraging our licences to enter the US market.

On the sportsbook, Aspire Global had acquired BtoBet and their focus has been to develop a fantastic platform for sports, which is now also integrated in the Pariplay offering. So, with one API, you have access to not only the casino content, but also the sportsbook content.

NeoGames and Aspire Global are companies that I have known & worked with over the years. They are companies and people that I’m already familiar with and I’m very comfortable with.

At the top level for Pariplay there’s been a few changes recently – obviously Aspire Global acquired Pariplay – but more recently NeoGames acquired Aspire. Does that change much and how has that impacted the day-to-day for your team?

Wizard as a brand was launched at Sigma last year, pretty much when I joined in November. We hired a new management team and started to create new and better content as a result – so, that has been a step up when it comes to the game quality and production. In addition, we have been very busy from a distribution perspective and from a licencing perspective, especially when it comes to North America and the US & Canadian market. The whole industry is focusing on those as being a huge opportunity and Pariplay has identified this as a strategic market, so now we’re executing that strategy.

A quick question on a few of those locations you mentioned: which one’s your favourite!

That’s a perfect segue for our final topic and question. You have already discussed Wizard, North America, Canada and the US. Overall, what are Pariplay’s ambitions and targets on the North American continent, given that there is so much international expansion into these markets right now?

You've mentioned a few products and brands, but Wizard Games in particular has come up a couple of times. Can you talk us through what’s been happening with this part of the business recently and your plans with it moving forward?

I can’t have a favourite, they’re all very different – I haven’t yet been to our Sofia office, which is where I'm going in September, so I look forward very much to visiting. I have been to Gibraltar several times before in different capacities. So, yes, I will not call any single one a favourite, but the one I’m looking forward to going the most is Sofia – because I’ve never been there before.

A hypothetical question I sometimes ask is: is it better to be a market leader in one area, or have a strong offering in every vertical? What is better in your opinion, specialist or generalist?

I think the reality of the component pieces that are within the NeoGames Group is that they have been assembled from having companies that are really focused on those areas. So, from a Pariplay perspective, certainly the focus area is aggregation – number one; and the Wizard brand – our own game content – number two, which is for the casino market.

Aspire Global, a platform with player management and account management, provides the glue for everything from a casino perspective and the managed services to run the B2C brands. NeoGames is iLottery and has been on End 2 End bingo, which is a very exciting technology company coming from Latin America, one of our focus markets. Again, through the Pariplay fusion platform with the same API, you also have access to the bingo product.

So it has been a fantastic journey that I have personally contributed to – and the future is even more exciting, the company is very pleased with the progress made and we’re looking at further investments into the quality of the games, and into the team.

28 GAMBLINGINSIDER.COM FEATURES GLOBAL GAMING AWARDS ASIA 2022 CONGRATULATIONSTOTHEWINNERS

Lead Partner Event Sponsors

Following the inaugural Global Gaming Awards Asia, Gambling Insider breaks down the worthy winners in each category

Although this is the first ceremony recognising the work of Asia-facing companies, the Global Gaming Awards have played host to the industry's most trusted and prestigious Awards for over nine years.

The

BetConstruct was the Lead Partner of Global Gaming Awards event sponsors coming the shape Digitain, Play SimplePlay. section below

in person next year, alongside

“We have been thinking about expanding the Global Gaming Awards and adding an event for Asia-Pacific for a number of years now. To see this event finally happen, albeit virtually, is a huge moment for us,” said Julian Perry, Editor-in-Chief of Gambling Insider.

SA Gaming, Pragmatic

“Congratulations to all winners, and of course well done to all the companies that were nominated. A big thank you to our Judging Panel, the event sponsors and KPMG in the Crown Dependencies for supporting our event,” he added.

and

all winners from the inaugural

and

like

Companies were shortlisted based on merit, with the winners chosen by a panel of multiple senior industry executives from the Asia-Pacific, with KMPG in the Crown Dependencies independently adjudicating the voting process.

Gambling Insider would congratulate Global Gaming Awards Asia looks forward event KPMG.

to hosting the

The winners of the inaugural Global Gaming Awards Asia have been revealed. A virtual event in its first year, the Awards recognise the efforts of operators and suppliers working in the Asia-Pacific region.

the

details this year’s winners across nine categories. Categories are as follows: · Casino Operator of the Year · Casino Supplier of the Year · Integrated Resort of the Year · Casino Product of the Year · Table Game of the Year · Corporate Social Responsibility of the Year · Digital Operator of the Year · Digital Supplier of the Year · Executive of the Year (see above)

of

Asia 2022, with

ENRIQUEEXECUTIVEOFTHEYEARK.RAZON JR. CHAIRMAN & CEO, BLOOMBERRY RESORTS CORPORATION 29GAMBLINGINSIDER.COM GLOBAL GAMING AWARDS ASIA 2022 FEATURES

in

CASINO PRODUCT OF THE YEAR MDXLIGHTSHUFFLER&WONDER INTEGRATED RESORT OF THE YEAR SOLAIRE RESORT & CASINO CASINO OPERATOR OF THE YEAR BLOOMBERRY RESORTS CORPORATION CASINO SUPPLIER OF THE YEAR LIGHT & WONDER 30 GAMBLINGINSIDER.COM FEATURES GLOBAL GAMING AWARDS ASIA 2022

CORPORATE MELCORESPONSIBILITYSOCIALOFTHEYEARRESORTS&ENTERTAINMENTTABLE GAME OF THE YEAR NOVO LINE NOVO UNITY II NOVOMATIC DIGITAL SUPPLIER OF THE EVOLUTIONYEAR DIGITAL OPERATOR OF THE SPORTSBETYEAR 31GAMBLINGINSIDER.COM GLOBAL GAMING AWARDS ASIA 2022 FEATURES

Lookingtoday.atthe sales business vs recurring revenue, we built a recurring revenue stream, which is considerably larger than it was five years ago. Thus giving us the cash flow and ability to operate and innovate; in other words, doing all the things that Interblock is known for doing – just more of it.

about the key factors a gambling company has to consider when moving from Europe to the US. It's a journey many will emulate in the coming months and years

diversification standpoint and, subsequently, discovered Interblock wasn’t very diversified in any sense of the definition. It had limited customers, limited markets and it was a sales business – very cyclical and tied to broader economic factors. From then on, we quickly worked hard to diversify the company, and now we are licensed in over 320 markets around the world; while our product portfolio has extended to over 30 products vs the one the company had in its first quarter century. Taking into consideration features and functionality, there are probably close to 200 different variations of our products out there

Two months ago, the original two Founders sold 100% of their shares, as Interblock was acquired by funds managed by Oaktree Capital Management. I stayed on as the company became a new entity and I’m very excited about having private equity inside the organisation now, which feeds into the transition of Interblock becoming a global company.

Has Interblock ever considered IPO-ing (Initial Public Offering) or using a SPAC (Special Purpose Acquisition Company)? I have a lot of friends in SPACs so I don’t want to talk about that specifically! But Interblock did not consider SPACs; honestly, I was always of the mindset that the next step for us was going to be private equity. Going public these days vs 10 or 15 years ago is far harder – the industry, costs involved and the expectations associated with it are massive. There are a lot of positives, but until your company is of a certain size and

COMING AMERICATO

grow. In fact, Interblock remained a sales business of mechanical roulette wheels for close to two decades.

32 GAMBLINGINSIDER.COM FEATURES INTERBLOCK

One of the first things I did was evaluate the company from a

It's good to speak with you again, John. On our main theme of 'coming to America,' can you talk us through the history of Interblock’s transition from a European company to a more global company with a US hub?

Interblock Global CEO John Connelly speaks to Gambling Insider Editor Tim Poole

In essence, the company is close to 30-years-old. The first ever electronic table game (ETG) was created by the founder of Interblock, Joc Pececnik, in Slovenia. From this, a small company comprised of a group of high school friends that went to university started to

Personally, the first time I had the opportunity to look at Interblock was as an executive at Bally’s, because we considered acquiring it back then. So, I was in discussions with Joc when I got to look under the hood of the organisation and do some due diligence. Lo and behond, the subsequent sale of Bally’s was not something we anticipated, it was quite rapid, when Bally’s was sold to Ron Perelman. In valuating Interblock, I thought it had the potential to go global, so I decided to go to and work with them. I joined Joc in 2015 and we decided to push ahead to see if we could take the concept of ETGs to a new level.

There’s nothing wrong with being public. Being public is an amazing opportunity and, at some point, perhaps we will also consider going public. Again, with the size of Interblock and the trajectory we’re on, having private equity and the ability to do M&A is a big boost. When you have private equity, you can acquire things even larger than yourself. The leverage of your company means you’re able to provide equity in cash vs straight borrowing, and it leaves the entire gamut of choices at our disposal to do what we feel is best for the future of Interblock.

33GAMBLINGINSIDER.COM INTERBLOCK FEATURES

What were some of the biggest challenges for you as a European supplier entering the US market? And hypothetically for the wider supplier market, what are the biggest hurdles they'll face in the US?

“Right now, it looks like the world is headed towards automation, a type of automation consumers are more comfortable with”

Looking at North America, Covid-19 was a complete shock for everybody. For us, the pandemic vastly accelerated a business plan we put in place. Rather than our business model taking five years it took two, maybe even a little less – so that was quite interesting, and a good insight to know what was going on with electronic table games during Covid. As a result of this shortened time frame, it meant we had to put an enormous amount of focus on North America. Luckily, we had laid a lot of groundwork between 2015-2020, meaning we had good infrastructure in the North American market already. So when Covid hit, we weren’t starting from ground zero. Having a pre-existing foundation created an opportunity to capitalise on the momentum we saw from both a player and operator perspective, in terms of increased interest during the pandemic.

scale, it’s definitely better to stay private in myForopinion.now, we are private equity, with the flexibility and ability to remain focused day-to -day on growing the business, and having the tools necessary to react quickly. Sometimes on Wall Street, the rules can be quite prohibitive, which wouldn’t live with our strategy. So I couldn’t be more pleased with having private equity as our owner in the form of Oaktree. Oaktree’s reputation is stellar, and its culture and way of doing business are very much aligned with the way we do things. Let’s see what the future brings.

the product. That's a fascinating prospect many might not have predicted. It's new ground that we’re all treading here. To your point about North America and how quickly Interblock has evolved here, I don’t want to take away from the team, their hard work and dedication, but it’s the primary product that people like. I think the growth we had before Covid was still staggering. But when Covid hit, that trajectory skyrocketed, growth was consolidated from five years into two. This is why people who’re entering America are saying they are seeing Interblock everywhere compared to a couple of years ago. The gaming industry is evolving, and more cost pressures are being placed on casinos to be more labour efficient. Covid created the need for efficiency, and post-Covid I don’t think casinos want to give

games – it’s a growth area of gaming that’s sustainable. The new generation of gamblers are very attuned to table games. So provided we continue to innovate, using technology to keep the segment competitive, I would say we are just getting started.

Again, we were quite fortunate that the portfolio of products we had created from 2015 to 2019 had grown and diversified to such a point that it was really conducive to an environment such as the one Covid presented. The fact that we had stadiums and single-seat products vs everything being very close together, where we could separate our offerings very easily, fit perfectly into what the public and casinos were looking for.

“There are a lot of positives to going public, but until your company is of a certain size and scale, it’s definitely better to stay private in my opinion”

As of today, I believe the vision of the company is to improve our marketing, so when people think of table games of any type, they think of Interblock. No matter which segment of gaming you think about across the world, both horizontally and vertically, we are working very hard to build a foundation and platform that can quickly expand. This is our current path, where we see ourselves, and I personally very much like being associated with table

Thinking out loud, Interblock is possibly the biggest supplier operating privately. At the same time, on the operator side you have bet365 – a huge global firm with no signs of going public, and no signs of this troubling it either – the operator reports great numbers every year.

What’s even more fascinating is that post-Covid, you would think there would be some type of a pullback or a recession of demand to the gaming environment people were looking for, but this hasn’t changed. If anything, it’s continuing to grow. It’s almost as though a whole new segment of players tried ETGs and were encouraged to stay with

“With competition comes more momentum in a particular sector”

Hypothetically, you couldn’t do the job you’re doing now in the US if you were based in say, London, could you? Well, anything is possible nowadays. But without question it would take you longer. Being local and present no matter where you’re doing business is critical, and essential to navigating your business toward growth. Whatever company is looking to come to the US, forming a subsidiary or an office with a management team in place is going to increase your chances of success 10-fold. This doesn’t mean it isn’t possible to manage from abroad, it will just take longer and posesses a higher risk of failure.

and '90s. Back then, the lottery segment was so dominant, and we saw supplier-side consolidation between casino and lottery suppliers. I see that as a very similar case study to casinos in the traditional and online sense. I think we’re going to have a consolidation over the next five years of the online world and traditional casino space.

As a B2B supplier, Interblock is working hard and innovating very diligently to make sure our product offering is conducive to the traditional and online space merging. Sooner or later, players will ask for the seamless ability of two wagering options in one space – online or land-based. If a company can start to integrate online and offline services into one, and it is seamless for a player no matter where they are, this is great for business. It’s also crucial to make your services as user-friendly as possible and provide content in a very seamless fashion that is competitive. I think we’re going to see some very, very large gaming companies fall out of the US market. This market fallout is going to be much, much bigger than anything we’ve seen on the supply side in the past, and the remaining companies will most likely end up being very dominant. So if you’re a supplier and you’re not careful, you can fall behind to a point where you can’t catch up. In my opinion, all suppliers in the US need to move quickly now if they want to be a success.

34 GAMBLINGINSIDER.COM FEATURES INTERBLOCK

Have you seen greater competition as more and more suppliers migrate? Do you think pandemic-led growth has led non-US companies to accelerate their plans to move stateside? We are seeing a tremendous influx of new forms of gaming, both in online, sports and traditional verticals. Loads of suppliers are coming to the states and Canada now; and for all intents and purposes, North America remained open over the past couple of years. In many other markets, if you were trying to build or expand your business, whether that be in Europe, Asia or Latin America – it was incredibly volatile, which made it very difficult to establish a business plan there. Although North America has had volatility and challenges, it was definitely one of the more stable places in the world to evolve over the past 30 months.

that up – if anything, I think casinos want to maintain the efficiencies they were able to implement during that period.

Right now, it looks like the world is headed towards some type of automation, a type of automation that consumers are more comfortable with. In many cases, the consumer demands things more immediately – we're trying to fit in with a wider trajectory towards automation.

Because of this, people that were looking to grow, those that had competitive new products, entered the US because it was a place to drive short-term gains. On the other hand, I think people at these companies underestimated the complexity of entering this particular region, from a regulatory and competitive landscape. Every part of the world is very different, they all have different thresholds – but the Covid situation has definitely brought a slew of companies here. Interblock has definitely seen more competition as a result of this, which I think is very good. My philosophy on competition is that with more competition comes more momentum in a particular sector. With that being said, many companies contact other companies asking about potential partnerships and mergers. The effort it takes to build up a company in North American markets is not something you can do overnight, you need to be really integrated in the US and have the capital to see through what you want to get done;

as well as time to establish all that. A lot of companies run out of capital and, quite frankly, the energy to pursue a return on their efforts. Conversely, Interblock is almost 30 years old, already had an international infrastructure, with cash flow and private equity to sustain us. This allowed us to focus on North America over the past couple of years to get where we are today. So we’re very fortunate to have that backing, unlike other companies.

Looking forward, what trends can you see occurring to determine how markets unfold in the US?

Well, who knows? But one thing I can say for sure is the US market definitely won’t be the same. Where we’re going is something I’ll equate to the 1980s

John Connelly

36 GAMBLINGINSIDER.COM FEATURES SUPPLY SIDE

European migration to the US has been on the rise since the overturning of PASPA in 2018. But, focusing specifically on suppliers, how much progress has been made so far and what does the future hold, with so many new suppliers choosing now to make the move?

Relax Gaming Chief Regulatory Officer Alexia Smilovic Rønde, Kambi Senior Director of Sales, US, David Bretnitz, Yggdrasil CEO Björn Krantz and the BetConstruct US team collectively share their thoughts with Gambling Insider.

There are, of course, plenty of similarities between the European and North American markets, though the broad differences outweigh any comparisons, with the BetConstruct US team quick to point out that the “biggest obvious difference is in the history.” The team told Gambling Insider that sports betting has been around for decades in Europe and in some cases even centuries. This is in stark contrast to the US, where legal sports betting has only been permitted for a few years and not legal in every state.

Bretnitz added: “It is also worth remembering that Europe and North America aren’t really markets per se as they are made up of dozens of markets all with slight differences.”

THE STORYSUPPLIERSOFAR

As noted by Krantz, it means getting the job right from the very beginning is crucial, with companies risking a return on heavy

David Bretnitz

“If you don’t deliver on player needs and motivations, players will walk away after playing just a few game rounds, meaning the lifetime value of the game will be very short.”

high-performance sportsbook remain the same.

EUROPEAN AND NORTH AMERICAN MARKET DIFFERENCES

Kambi’s Bretnitz agreed that the North American sports betting market is very much in its infancy, with several large states and provinces still yet to regulate. It remains a very exciting prospect for this reason alone, according to the company’s US Senior Director of Sales.

However, while noting the evident differences that such a situation brings about – from the importance of tribal gaming in the US to differences in player betting behaviour – Bretnitz adopted the stance that “the fundamentals of a

Yggdrasil CEO Krantz, meanwhile, added one important factor to the mix: European players in general are quite well educated. He explained: “Higher market maturity,

"Whether it’s a stable core platform, strong risk management or competitive pricing, the key is having the flexibility to provide a genuine localised offering that players can enjoy.

The BetConstruct US team touched on some other differences it has witnessed so far, too – such as the “sports covered and types of bets offered,” before advising that “operators will have to listen to consumers and dial in on the needs of the market to be really successful.”

combined with a higher degree of player awareness, puts high pressure on game developers to balance math and mechanics in game design and delivery. It is a win or lose battle as you don’t have the luxury of a second or a third try in a mature gaming environment.

Gambling Insider speaks with leading executives from Relax Gaming, BetConstruct, Kambi and Yggdrasil to hear how European suppliers are progressing so far in North America

“Strive to be unique and don’t try to copy what everyone else is doing”

Relax Gaming’s Chief Regulatory Officer explained: “The route to getting games certified in North America can often be long and arduous, particularly in US states. Even then, it’s vitally important that suppliers realise that content popular in markets such as Europe isn’t necessarily going to work in North America.”

That sentiment is very much shared by the US team at BetConstruct, which told Gambling Insider: “European firms that are willing to listen and adapt to the market are meeting with a great deal of success. Firms that are doctrinaire and say ‘this is how we do it in Europe, we will train them [North America] to do it our way’ aren’t having so much success.”

“In our field of sportsbooks and online gaming, there are too many competitors and tooAlexia Smilovic Rønde

Despite the many differences between the two sports betting markets, European companies can, of course, use all their experience to thrive in these foreign lands. But as former US President Theodore Roosevelt once said, nothing worth having comes easy.

HAS EUROPE MADE AN IMPACT IN NORTH AMERICA?

“In a mature market, trust and confidence in your ability to consistently provide strong roadmaps with high quality and innovation is fundamental. When entering a mature market as a new player, you need to prove that you are unique, can clearly support customers in terms of differentiation and add value to the player ecosystem.”

investments if they fail. Moreover, the market entry barrier for new game developers is not only high, but a costly affair. This is particularly true of mature markets such as Europe.

She added that most providers are beginning to come to terms with this, and are consequently adapting internal roadmaps accordingly in an attempt to meet the needs of such players.

Yggdrasil, meanwhile, has just started its US go-to-market journey, with the company live with one game – Vikings Go Wild – via its collaboration partnership with IGT. As noted by the company’s CEO Krantz, a second game – Cazino Zeppelin – is ready for its 7 September launch in Michigan.

The North American market is, naturally, not only limited to the United States. Canada in recent months has shown that it is a major player when it comes to this new age of sports betting. On 4 April 2022, a total of 13 sportsbook apps were granted approval to launch in the hugely influential province of Ontario, and it is a region that has continued to grow in stature since launch. That has undoubtedly been helped by the fact Ontario is the country’s most populous province, and is home to over 10 million potential players.

“What's also attractive is that Ontario has already been exposed to online slots in the past as a grey market, therefore players are accustomed to European-style games,” she said. “Couple this with the Alcohol and Gaming Commission of Ontario’s (AGCO) regulatory model, that’s significantly friendlier than we’ve seen elsewhere on the continent, and I think it’s fair to say things are poised nicely for suppliers.”

Krantz offered the following advice to any and all interested parties out there: “Strive to be unique and don’t try to copy what everyone else is doing.”

While Relax Gaming’s Rønde acknowledges that European companies are slowly starting to flourish in the North American market, she concedes it has been far from easy for suppliers, “particularly those with little to no experience in the market.”

The team continued by explaining that any business that wants to survive and grow must adapt and speak the local language, as it were, particularly when it comes to the hugely competitive world of sports betting.

On the other side of the spectrum is the burgeoning US market, where Yggdrasil has noticed some “fantastic growth” in key regulated states, while the underlying growth is However,“enormous.”Krantzexplained that with more actors and more games comes “higher pressure to bring consistent high value to stay relevant and not be down-prioritised. This means that you need to go 'all in,' in both mature and immature markets, creating a niche with a key focus on optimising and maximising long-term growth ambitions.”

“A new entrant needs to compete with legacy game developers who have built their top-of-mind brand awareness, cross-player communities, customers and markets over several years,” explained Krantz.

Relax Gaming wasted no time in taking advantage of this opportunity, with the company’s Chief Regulatory Officer Rønde saying “it made complete sense for us to announce our presence in North America via Ontario for that reason alone, as it’s very likely that Ontario will remain the largest market for some“Alltime.signs indicate that neighbouring provinces will be much slower to come online, but perhaps Ontario could act as a goodButexample.”itwasn’t solely the huge numbers of potential bettors that attracted the supplier to the province, as explained by Rønde.

He said: “As we do not run parallel game development processes, we can manage both Europe and US go-to-market roadmaps simultaneously."

“We have been following the market

The group is very much in its early stages in the US, but Krantz explained that any progression will in no way impose on its European operations.

WHY GO TO THE NORTH AMERICAN MARKET?

38 GAMBLINGINSIDER.COM FEATURES SUPPLY SIDE

developments very closely in the US and several of my colleagues have extensive experience and insights from US operations. We know that European content resides well with US player behaviour and are confident that our legacy Yggdrasil portfolio will do well once launched in the US.”

The BetConstruct US team opted for a perhaps more blunt approach when asked the question of what the future holds, stating that “the strong will survive, the weak will perish; it’s the rule of the jungle.” The team added that “new markets will drive innovation and technology, which will flow around the globe.”

He concluded: “Besides that, there is a continued evolution of technology and tools supporting operators to optimise their omnichannel strategy.”

“The strong will survive, the weak will perish; it’s the rule of the jungle”

– BetConstruct US team

“In the same vein, there will be lawmakers in other Canadian provinces that have watched on admirably at what the AGCO (Alcohol and Gaming Commission of Ontario) has achieved so far and how smooth market entry has proven to be for most. In time they will look to emulate this success so that they

particularly if such states adopt a similar

As Krantz previously alluded to, the company is just starting out on its US journey, and so needs to ensure it enters with a “high level of trust and confidence that will support our long-term operational ambitions in the US.

“In the same vein, there will be lawmakers and Gaming Commission of Ontario) has achieved so far and how smooth market entry can get their own slice of the pie.”

US, “it isn’t really a case of Europe versus betting.” But he has no doubt that will “continue to play the development of sports betting in North America in collaboration with

39GAMBLINGINSIDER.COM SUPPLY SIDE FEATURES

many choices for customers,” said BetConstruct. “So providers need to be customer-focused and customer service-driven or they will face certain peril.”

“Ontario took an approach of ‘let’s work with our providers, provide the appropriate protections and oversights and show the world regulation doesn’t need to be adversarial to be effective.’ Whereas the United States’ commercial, tribal and governmental can be a hodgepodge of regulations, Canada has a more uniform approach, within the individual provinces, and the industry will be better for it.”

suppliers, making a difference in the US, are more or less digital natives. I believe this has supported the US online gaming market growth, attracting a new online-focused audience with an appetite for new exciting mechanics and fresh online-focused content.”

One vertical that remains rather behind in the legalisation process in the US, at least when compared to Europe, is online casino. It’s a vertical in which Yggdrasil has a particular interest, but CEO Krantz is not currently preoccupied with how the lack of legalisation will impact the company’s strategy going forward.

As for the “impressive” Canada, a hugely important aspect of the thriving North American sports betting market, BetConstruct explained that Ontario regulators are among the best in the world and are only getting started.

Ontario does, however, differ somewhat according to Bretnitz, primarily because there was already a large grey market in place in the province, one that consisted of operators that had previously focused on Europe, “with a couple of operators commanding a large slice of the market prior to full regulation.”

For Kambi’s Bretnitz, European companies have undoubtedly played a “significant” role in the evolution and growth of the regulated US sports betting market. This is thanks to longstanding sports betting heritage, experience and is something particularly evident on the B2B side of things.

“We have very exciting times ahead of us with highly motivated and talented colleagues that cannot wait to make a difference in the US.”

Whether it's online gaming or sportsbook, European firms entering North America will only increase in volume. But it's how they continue to fare in terms of success that remains most intriguing.

local expertise and organisations.”

of player preferences in the US.

Krantz added that there is also an enhanced omnichannel opportunity, one that will "offer and convert land-based content to online and vice versa." Yggdrasil specifically sees this as an opportunity to “capture a wider ecosystem of players to support sustainable content growth and innovation.”

For Kambi's Senior Director of Sales, US, “it isn’t really a case of Europe versus North America when it comes to sports betting.” But he has no doubt that ‘traditional’ European firms will “continue to play an important role in the development of sports betting in North America in collaboration with

Björn Krantz

Interestingly, however, Bretnitz is of the belief that ‘European firms’ no longer really exist. He used Kambi as an example, saying that the company is now live in over 40 jurisdictions across six continents, with offices in Australia, the Philippines and the US. Moreover, the majority of the group’s revenue now comes from outside of Europe.

The market, she added, is “only going to get bigger and better as new states open up,” particularly if such states adopt a similar regulatory model to the one seen in Ontario.

WHAT DOES THE FUTURE HOLD FOR NORTH AMERICA?

For Relax Gaming’s Chief Regulatory Officer, the future looks “extremely bright” for European companies in the US. She noted that several European studios that have already entered the market have begun to comprehend all the intricacies and quirks

For Yggdrasil, European firms are playing a hugely supportive role in this rapidly growing market. Telling Gambling Insider how European suppliers have done in the North American market to date, Krantz said: “I would say very well, and also considering that today more than 50% of the top 25 slot games are built with a pure online focus in mind.”

He continued by notin: “European

Much of the current focus for European suppliers is on the here and now, with the North American market just getting started. But that is not to say there isn’t one eye on what the future holds for this hugely exciting region.

However, this is only half of the equation. The second half of the equation is to ask: Can you then go on to utilise the same approach used in the UK in the US? This includes leveraging retail into mobile and brand development. These are issues that have proven to be very expensive with the way the US market is rolling out.

you compare Betfred to William Hill, which first appeared on the US scene between five to seven years before Betfred. The question was could Betfred still establish its brand in the US state by state, without a partnership?

And how did Betfred fare when it chose to go down this path?

There were clearly difficulties finding partnerships, so I came up with a strategy to strike agreements with American tribes. Tribal agreements are incredibly hard; it’s a difficult market to penetrate. Deals with tribes were thought out and approached on a state-by-state basis, a process we started in 2020. At present, Betfred has several tribal partnerships and is live in six markets today, with 15 more set to go live. The company is continuing to answer the question of whether it can establish a state-by-state operating roadmap, in 20+ states.

40 GAMBLINGINSIDER.COM FEATURES OPERATOR VIEW

BEWARE THE SHAKE OUT

How did Betfred’s migration from Europe and other world markets to the US come about?

Stephen Crystal, Head of North America Development for Betfred, speaks to Gambling Insider about the operator’s migration from Europe to the US, and how the brand hopes to achieve long-term success there

Stephen Crystal

The feeling in the US is that if a business needs expertise, it will go out and acquire it – it would not feel the need to merge or partner ofsecondItchangedsomebody.withSoafter9monthswithnosuccess,despiteseveralconversations,Betfreditsmind.waspartoftheorthirdwaveactivityintheUSif

So we went through a series of discussions, isolating a dozen potential candidates. We got close but, in the end, it wasn’t a natural enough thing for a brand to partner with a sportsbook – or recognise that a company such as Betfred has expertise a US-founded brand doesn’t have.

was to link up with an existing US partner – a US brand – and bring what they know best, which is bookmaking, to a US-facing brand. The first six to eight months of my partnership with them focused on trying to find a US brand looking for a partnership.

So far, broadly speaking, the US has been less about brand and more about the willingness of an operator to spend thousands and thousands of dollars to acquire a customer worth a fraction of what the operators are spending on that customer. This is where the market, in general, has evolved. It doesn’t play into the strengths of Betfred as a nuts-and-bolts operator, but more so the big hitters: DraftKings, MGM Resorts and Caesars, which can use their balance sheet to spend money without regard to making a profit. This is the short answer of where we started and where we are now with Betfred US.

To be clear, Betfred in the US operates mobile and land-based businesses. It has six mobile operations with an agreement to

It was in 2019 at G2E, which is coming up in October this year, when Betfred approached me asking to bring its brand to the US. The guys at Betfred asked what I thought about the ability of Betfred to achieve market access. The initial thought from Betfred

Betfred is a well-established brand in the UK. This has never been in doubt. Its strategy in the UK has to use five decades of experience to focus on leveraging a retail experience into a mobile business. It was retail-first in the UK when the brand was made. It was built with professional sports team partnerships and sports events across what is now 1,500 betting shops. Then, Betfred migrated online and was able to capture its fair share of the mobile market by leveraging its retail brand.

more on the profitability of operations, the success of investments in customers and retention, and the return that they’re getting in these investments. What people had been rewarded for was their topline handle month-to-month, even though most of that growth was being fuelled by the investment of operators in bonuses and free play.

OPERATOR VIEW

of customers. None of this, though, gets to the heart of the issue – which is first and foremost to be a brand. An operator either needs to have a well-working brand or be willing to invest in it. The second thing is a platform, operators need to have a platform in which it controls their destiny, one which is differentiated from competitors. Staffing is an issue too; there aren’t enough qualified experts locally in gaming and iGaming. Companies are having to take people from other e-commerce businesses and

Pretty soon we’ll see a shake out, a consolidation of the market because there’s only so long you can operate and lose money. What will happen as we advance will more resemble the experience of mature markets. That means innovation and differentiation in products; you’ll see a rise in the ability to differentinvestmentthecustomers,segmentandappropriateinsegments

Comparing European and US customers, how different are the sports betting cultures? Has Betfred had to adapt its offerings to a market where the idea of wagering is “newer?”

I think many from a European perspective don’t fully appreciate just how intense and rapid the rollout has been in the US. We’ve seen multiple markets go live at the same time; new challenges arise with respect to technology. Putting aside the product, just to be up and operational in a retail context, in a mobile context, just to be able to confirm your platform to the state-by-state regulatory approach, taxation approach and compliance approach, is a huge challenge. What we’re seeing now is the race for operators to get up and running with a functional platform and then to go after customers they consider to be low-hanging fruit; those they believe to be accustomed to betting or to come up with strategies to cast a wider net and get more customers in. The reality is that the market today shows its potential of what the market could look like once the platform and products are up to speed. In my view, it’s almost irrelevant to talk about the customer-facing metrics now, because the numbers of people, bets and revenue we see is a result of a number of markets opening simultaneously. In the future, you will see companies judged much

train them in gaming – this has opportunity but also peril. This is why William Hill merged with Caesars, why Entain is partnered with MGM Resorts and why Flutter (then Paddy Power Betfair) acquired FanDuel. A company like Betfred has to be nimbler and more strategic. The US market is not one size fits all, a company like Betfred can find its way into a market as big as America. But it has to leverage its

seen multiple markets go live at the same compliance approach, is a huge challenge. of markets opening simultaneously. In the

"In my experience as a gaming lawyer for 30 years, as long as you’re an above-board business operation, which Betfred is, where there is a will there is a way to navigate the regulatory process"

42 GAMBLINGINSIDER.COM FEATURES

launch 15 more in other states. Obviously, in some states gaming is retail only, but almost every state either has mobile live today or has mobile expected to be live very soon. Furthermore, Betfred has reserved the right to use iGaming in all of these states in the future. So, overall, the footprint will see Betfred go ahead with retail sports, mobile sports and iGaming.

assets, which is a process Betfred has been undergoing for four years.

How much of a challenge is it in general when going live in multiple different states, given the vastly different regulations in all of them?

44 GAMBLINGINSIDER.COM FEATURES OPERATOR VIEW 44GAMBLINGINSIDER.COM

Illinois, Wisconsin, Minnesota, Kansas and Missouri. So there’s more to come in terms of market access for Betfred: the operation has grown from zero a year and a half ago to there being close to 150 personnel in Las Vegas. The operation and the platform partnership with OpenBet is growing state by state. As these relationships get larger, Betfred will get more control over the platform and the types of upgrades to its online site. Furthermore, the company is continuing to pursue media and sports team partnerships for branding – making investments there – all while seeing how the market is Obviously,evolving.Betfred wants to be one of those companies that survive the shake out of the US market, and get its fair share of the market. All Betfred has to do is manage between 3% and 5% profit per market and it will have a hugely successful business in the US. If it does this, it will have revenue and cash flow that will far surpass that of its existing operation everywhere else. The potential is huge. All Betfred has to do is what it has already done in another heavily competitive market, the UK, where it has 20% of the retail market space and 5% of the mobile space. The UK has over 300 operators. However, in the US we’ll have fewer than 25 real operators when all is said and done. This is for a country that’s over four times the size of the UK in terms of the market. That’s how Betfred has got to look at it to make sure it is one of the remaining operators in the US. If Betfred can get to 5% of the mobile space in every market it is present in, that would represent a huge success. The company needs to make wise investments, and rely on 50 years of operating history and industry nous, to succeed in a highly competitive US market.

Coming back to Betfred, what’s the next goal for the operator in the US? What’s the mission going forward?

Betfred is live in states like Arizona, Iowa, Colorado and Louisiana. The next states the operator will go live in are Indiana, Virginia, Ohio, where Betfred announced a partnership with the Cincinnati Bengals, and Nevada. Other states in the pipeline include

Betfred has managed to navigate dozens of jurisdictions. What we’ve found is you end up having more compliance staff than the number of staff in your product team. When your compliance team is larger than your product team, that tells you about the lengths operators need to go to in America.

STEPHEN CRYSTAL FEATURES

Honing in on somewhere like New York, where only the “big hitters” operate, is this a market Betfred would ever look to enter, given its high tax rate?

Only eight operators are live in New York. Betfred had a chance to join them, but the state’s 51% tax rate on all gaming activity made market entry there a non-starter. Even though handle numbers would be significant, the fact the state government would be a 51% partner on day one was a bit of a disincentive.

The UK prides itself on having, quote unquote, “tough regulations." But I think most operators that have migrated to the US have realised some states are even more rigorous than the UK. It’s always surprising to them, even for Betfred. Some of the questions posed by operators are: “Why do regulators need to know about non-gaming business?” “Why do the regulators care about everywhere else we do business?” These are the requirements of some states that create tough issues for operators to Innavigate.my30 years experience as a gaming lawyer, as long as you’re an above-board business operation, which Betfred is, where

Ontario has adopted more of a European regulatory model. Can you see the approach of Ontario impacting US regulations in the future?

I would say Ontario is much more similar to what Europeans are used to. I do not feel by any stretch that Ontario regulations are anywhere near as strict as those in the US. I’m finding that a lot of European operators are using Canada as a jumping-off point to the US. I think operators doing this are mistaken; the US and Canada are completely different ballparks altogether.

"Betfred had a chance to move into New York, but the state’s 51% tax rate on all gaming made market entry a non-starter"

there is a will there is a way to navigate the regulatory process. It just takes time, resources and some adaptation to the mode of doing business. Regulators in the US care about the entirety of the people they’re doing business with and how they approach corporate culture. You have to take a much more holistic view and, in the US, you almost have to be proactive in terms of self-regulation. In the UK, you wait for the Government to tell you: “You can no longer do this or that”. But in the US, regulators expect you to, in essence, self-regulate and go the extra mile to do the things that regulators feel responsible, ethical businesses should do. This is something that’s a little different culturally from what we see in the UK and across Europe.

What are some of the challenges you’ve faced tapping into local US culture?

What are some of the broader regulatory differences Kindred has experienced in the US market compared to Europe? Do you find yourself with more flexibility in terms of the odds you can offer and how you are able to market those odds? Europe and the US are both very fragmented markets. In the US, you’re also dealing with a state-by-state (similar to the EU country -by-country) regime but with a more complex regulatory framework of state, tribal and federal legislation. Our experience in dealing with that regulatory fragmentation and being able to achieve scalability despite this has definitely helped our expansion in the US. What we’ve noticed in the US is that sports and advertising are a much more integral part of life, and the tolerance towards (the volume of) marketing of US customers is perhaps higher than in Europe. The budgets are also exponentially greater. That doesn’t mean we shouldn’t learn from the developments in Europe, where marketing restrictions and bonus bans are now more common than not in the main markets (UK, Sweden, Belgium, Netherlands, etc.) after years of over-advertising. As an industry, we definitely have a responsibility in mitigating this risk proactively in the US.

Each state has different regulations. Is there a fine line between what you can do in one state compared to another? The US is a fragmented market and gambling regulations are managed on a state level. In

Our brand positioning is the same across

When it comes to the variety of odds and markets, there are two interesting distinctions. Firstly, when it comes to the top sports, we see a much wider offering in the US, as a result of years of fantasy games – the customers’ appetite for player props is definitely higher than in Europe and the market has done very well to meet that demand. At the opposite end, we see more restrictions in terms of non-sports markets (like Oscars, politics etc.) which is understandable for a younger market – but this is likely to relax as regulators grow confidence that the industry can manage the risks.

Liv Biesemans

practice, it means that whenever we plan to enter a new state, we have to approach that state as a standalone project that requires a local licence: a dedicated analysis of the regulatory framework in place, a customisation of your platform and website setup, a separate platform certification, additional supplier integrations etc. We also operate both retail and online sports betting operations in Pennsylvania and Arizona, which is a different operational setup entirely. The biggest difference between the states is the product scope: most states cater for sports betting (although there are local restrictions and differences) but only a number of states allow for iGaming. Payment methods are another area where we notice differences between some states. However, we also see a great deal of commonalities between the different states in terms of know your customer (KYC), responsible gaming, advertising, etc, so we can definitely build on a shared baseline across the different states.