THE SHAPE OF FUTURE BANKING

www.globalbankingandfinance.com Issue 46

Joe Myers

Executive Vice President, Global Banking, Diebold Nixdorf

Let’s elevate your great with Absa Business Banking solutions.

Whatever inspired you to start your business, we offer a variety of business banking solutions to help you take it to the next level.

We see your great. Now let’s elevate it. Speak to an Absa Relationship Manager today. That’s Africanacity. That’s Absa.

We are doing big things... Are you subscribed?

Chairman and CEO

Varun Sash

Editor Wanda Rich email: wrich@gbafmag.com

Head of Distribution & Production

Robert Mathew

Project Managers

Megan Sash, Amanda Walker

Video Production and Journalist

Phil Fothergill

Graphic Designer

Jessica Weisman-Pitts

Client & Accounts Manager

Chanel Roberts

Business Consultants

Rick Saikia, Monika Umakanth, Stefy Abraham,

Business Analysts

Samuel Joseph, Dave D’Costa

Advertising Phone: +44 (0) 208 144 3511 marketing@gbafmag.com

GBAF Publications, LTD

Alpha House

100 Borough High Street London, SE1 1LB

United Kingdom

Global Banking & Finance Review is the trading name of GBAF Publications

LTD

Company Registration Number: 7403411

VAT Number: GB 112 5966 21 ISSN 2396-717X.

The information contained in this publication has been obtained from sources the publishers believe to be correct. The publisher wishes to stress that the information contained herein may be subject to varying international, federal, state and/or local laws or regulations.

The purchaser or reader of this publication assumes all responsibility for the use of these materials and information. However, the publisher assumes no responsibility for errors, omissions, or contrary interpretations of the subject matter contained herein no legal liability can be accepted for any errors. No part of this publication may be reproduced without the prior consent of the publisher

I am pleased to present Issue 46 of Global Banking & Finance Review. For those of you that are reading us for the first time, welcome.

As we head into 2023, Joe Myers, executive vice president of global banking at Diebold Nixdorf, explores some of the key themes having impact and driving change for the banking industry. Turn to page 24 to read ‘The shape of future banking.

In this edition we also take a look at the 2023 outlook for US equities and fixed income, along with top predictions for fintech, payments and the financial industry, discover how the cost of living crisis could change how future generations engage with financial services, and much more.

We strive to capture the latest news about the world's economy, financial events, and banking game changers from prominent leaders in the industry and public viewpoints with an intention to serve a holistic outlook. We have gone that extra mile to ensure we give you the best from the world of finance.

Enjoy!

Wanda Rich Editor

BANKING

32

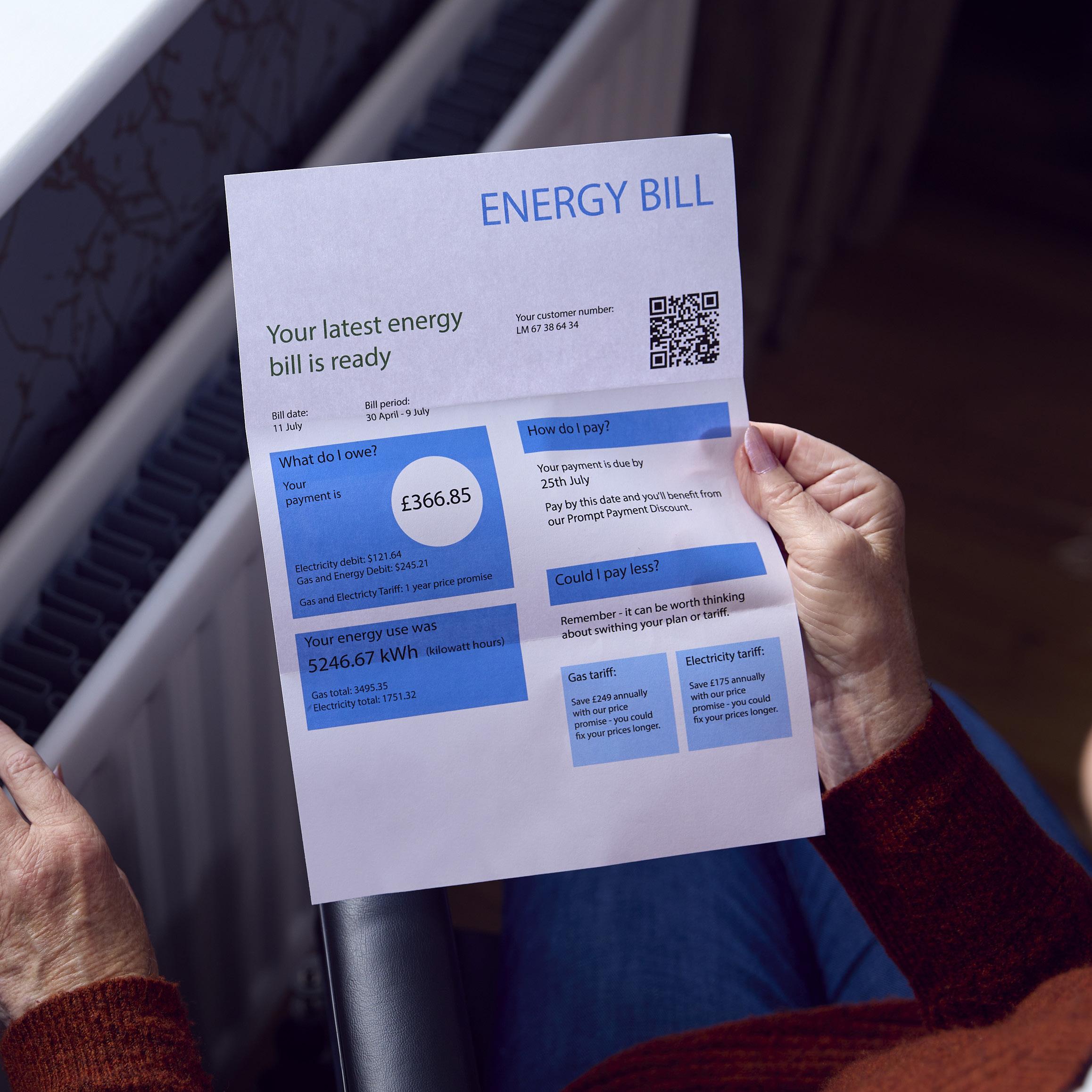

Top tips for Avoiding Bank Account Scams in 2023

Gemma Staite Threat Analytics Lead BioCatch

How banks should approach their modernisation journeys

John da Gama-Rose Head of BFS, Global Growth Markets Cognizant

How Artificial Intelligence is Transforming Banking

Ankur Rawat, Director, Products and Solutions, Banking and Financial Services, Newgen Software

10

30 46 32

Looking into the lens of 2023

Christian Müller, Chief Financial Officer Moss

The opportunity for C2C marketplaces during the cost-of-living crisis

Luke Trayfoot Chief Revenue Officer

MANGOPAY

How your financial team can become a revenue driver

Mark Gilham Director & Evangelist

2023

Hugh Scantlebury CEO and Founder Aqilla

Eyal Sivan Head of Open Banking Axway

Russell Gammon Chief Solutions Officer Tax Systems

Andrew Doukanaris Business Director Fintech Europe

Galen Chui SVP of engineering and products Cubic Transportation Systems

2022 was the year businesses emerged from the shadow of the pandemic and the many disruptions it caused. While life has returned to normal for many companies, and some even discovered new growth opportunities, unfortunately, the light at the end of the tunnel is not in reach just yet.

As we look into the lens of 2023, the same questions around financial uncertainty linger: How long will inflation continue? Will there be a recession? What measures should be put in place to protect the future of a business?

It’s challenging to find clear answers. Still, the past few years were focused on responding and surviving. With that in mind, 2023 looks to be the time for business leaders to leverage technology and build long-term resilience, achieving sustainable growth for their organisations.

Here are my top 5 predictions for the year ahead:

2023 is sure to be the year of frugality, and the pressure will be placed heavily upon the shoulders of CFOs to provide financial stability as the economic downturn hits.

The impending recession highlights the need to prepare for future economic uncertainty and streamline processes wherever possible.

Business approaches have been changed forever in the past couple of years thanks to rapid digitisation, with markets becoming a more level playing field and competition increasing. As a result, companies are encouraged to seek innovative ways to achieve a competitive advantage, despite the new and continually changing circumstances.

To best prepare for future economic battles, businesses should start exploring now how to manage spending in a recession and operate beyond just looking at budget cuts. For example, establishing internal controls that monitor spend approvals, improving visibility across all company outgoings and automating time-consuming tasks that don’t add business value.

Financial tracking and spend management tools will prove their weight in gold for the year ahead. Finance leaders require the best tools to help them confidently make informed decisions, particularly regarding cost control and cash flow visibility.

As we approach 2023, it’s clear that the world’s business leaders will continue to grapple with economic, political, and environmental uncertainty. The good news is that dealing with uncertainty does not mean operating our businesses blindly.

Digital processes have created a new era of visibility, collaboration and strategic decision-making based on real-time and accurate data. With the right technology, finance professionals can access an integrated view of total business spend and deep visibility into their supply chain. This advancement enables improved inventory management, predictable lead times, cost savings and, crucially, more accurate financial reporting. It also helps businesses tackle some of their most complex challenges, such as achieving sustainability compliance and building long-term resilience for their company.

Acceleration of automation is a safe bet in 2023, allowing finance teams to automate their day-to-day tasks and remove the notoriously labourintensive month-end processes and management of accounts payable.

In a nutshell, automation increases productivity, frees employees from manual tasks and allows them to concentrate on strategy and innovation. Automated spend management processes empower teams to add more value to the bottom line instead of wasting days pulling together spending data.

Manual tracking and auditing spend to increase the risk of mistakes, repeated entries or gaps in the data. By reducing these risks, businesses can make significant cost savings.

More visible spend data leads to precise predictions and better decisions. With the right spend management software, you can make light work of previously laborious manual tasks, get complete control and visibility and have more time to focus on growing your business, even in difficult times.

We now see a trend towards integrating software stacks via interoperability of systems with high-quality tech integration or even with multi-purpose software that solves multiple problems at once.

With all the software systems we use today, things can get messy and complicated with so many tools, especially when synchronicity between software is not guaranteed.

An increase in tech stack integration means all tools complement each other, working together to provide seamless access to relevant data. The beauty of accessible data is that everyone in the business can get involved at any stage, which can help streamline production and delivery.

Instead of having to rely on IT to provide information, with tech stack integration, all your tools work together, so it’s easy to jump in at any point and get the information you need to make a decision.

With this kind of functionality, you can avoid all types of bottlenecks, as no one has to wait for data provision before moving forward. It also creates a single source of truth for financial reporting, reducing the likelihood of costly errors.

If everyone on your team is empowered to make decisions based on accessible data, you’ll also see massive productivity improvements.

We believe in providing a customised solution for businesses, not a onesize-fits-all approach. Teams should offer a bespoke service rather than only helping with the initial implementation.

A customisable modular solution based on specific needs allows for more flexible issuing of virtual and physical credit cards, better digital invoice management, easier accounting, and more reliable liquidity management.

Prior preparation prevents poor performance.

The new year is the perfect time to review spending insights and correct workflow challenges. By studying and improving spend management in economic uncertainty, leaders can position their businesses to be ready for any future economic challenge and set themselves up for a prosperous long-term future.

Christian Müller Chief Financial Officer Moss

The modern business landscape, to cybercriminals at least, is a land of opportunity. At every turn, paths lead to low hanging fruit, easy pickings, and most tempting of all, the gold at the end of the rainbow. To cybercriminals, financial services and fintech industries data is that gold. A brand new FS-ISAC new report found a growing list of cyber threats facing financial institutions in 2022, including third party risk and ransomware.

Fintech is a sector which, by its very nature, money flows through. Money attracts attention from cybercriminals, and the fintech industry is then charged with responding in kind. One major way that they can take control of their security is to appropriately guard the gates to the kingdom, with authentication. The current widespread authentication methods which we use – namely, passwords –to not meet the rigorous standards our industry upholds, both from a security and regulation perspective. Therefore, we need to turn to authentication alternatives. In this case, that alternative is a programme of multifactor authentication.

In an industry such as financial services, effective authentication security is necessary for two main reasons: To ensure that their clients, network and operating systems are secure, and to appropriately match any regulatory compliances necessary.

The first part of this is self-explanatory: Financial services products, organisations and services exist to facilitate the transfer or management of capital. A failure to undertake a rigorous, robust security posture for companies like ours could be terminal, as it would reflect a failure to safely complete the very function of our business, and would therefore reflect an immediate loss of reputation with our customers; Particularly if their assets were not simply stolen orput beyond use, but appeared for sale on dark web marketplaces where they can be purchased by further threat actors, to increase even more damage.

The second part is somewhat more complex. Regulations differ from industry to industry, and country to country, and failing to adhere to them will almost certainly result in a significant fine or loss of license from the associated regulatory bodies.

In this instance, we are going to focus on just one example: PSD2. PSD2 is a European regulation for electronic payment services. It seeks to make payments more secure in Europe, boost innovation and help banking services adapt to new technologies. In practice, this means that fintech companies such as ours are tasked with ensuring that our products meet the new standard for access and payment validation: specifically, multifactor authentication, and making sure that the people authorising payments or accessing accounts are who they say they are and leave an indelible

record of their actions. This is where partnering with a trusted MFA/ authentication partner can give fintech providers, and their customers, the assurances that they are compliant with the relevant regulations, and secure. However, this is just one part of the conundrum.

Multi-factor authentication is a great tool for helping financial service organisations to ensure that they remain compliant with relevant legislative directories, and secure from the cyberattacks we know are constantly targeting end users trying to access their corporate networks. But if not done correctly, it can create friction between employees trying to complete their job functions, and IT teams seeking to authenticate. In our industry, it is of crucial importance that things happen smoothly and quicky, as well as with security and compliance accounted for.

The best authentication partners will understand this: They will understand fraud protection steps need to be taken, but also recognise that making this system as simple as possible, from training and onboarding through to deployment and customer integration, is the best way to keep fintech customers happy.

The financial services industry is going to be targeted in 2023 and beyond. Cybercriminals will continue to find new and inventive ways of helping themselves to or blocking access to an organisation’s data. Additionally, regulators will continue to impose new forms of accountability for the industry to adhere to as the financial repercussions of cybercrime continue to spiral. As a result of this precarious landscape, every login counts. Making sure that people can log into their online accounts with as little friction as possible, and with as much success as possible. Losing customers’ confidence at the point of logging in breeds frustration, which could turn into a customer eventually turning away from this solution. Our current partnership works to mitigate this risk, with recent logins hitting a 99.9% successful login rate.

It is the responsibility of the industry to make sure that they seek out the right partners to support them in this turbulent environment; And the responsibility of these partners to facilitate compliance and assure security, without affecting the function of the business. The right partners can help you to do that.

Despite the current economic environment, our desire to travel hasn't dimmed. Amadeus’ June Consumer travel spend priorities report , which surveyed 4,500 consumers in the US, UK, Germany, France and Singapore, revealed that two out of five (42%) rated international travel a high priority for the coming year. When compared with the other responses, travel ranked well. Approximately 32% of respondents said they would prioritise domestic holidays, 28% cited online entertainment, 27% valued eating out and 20% said buying a new car or home was a priority. As a global travel technology provider with close relationships with customers across areas, including hospitality, business travel and aviation, we know that many businesses are hedging their bets on this recovery.

Many travel firms are investing now to offer the best customer experience to returning travellers. One area where there is significant investment is in payments and fintech. A prime example is the introduction of advanced airline retailing capabilities under the International Air Transport Association’s (IATA) New Distribution Capability, which removes payment friction to enhance merchandising. Once again, Amadeus research confirms that most industry players

share our view. According to our Travel fintech trends research of 70 senior industry leaders, more than 50% of respondents plan to surpass 2019 payments and fintech investment, with 30% likely to match it. So, what are these capabilities and why are they looking to offer them?

Many travel businesses are grappling with chargebacks — the formal process initiated when a cardholder disputes a transaction, often leading to them being reimbursed funds directly by their issuing bank. Recent high levels of disruption and strained industry refund processes have led to significantly more chargebacks since 2020. According to the Travel Fintech Trends research, 70% of travel businesses saw an increase in chargebacks, increasing by 50% during the pandemic in 2021 when compared to 2019 averages, and by more than 100% for a significant minority of travel companies (20%). This led to one in three firms increasing headcount to manually process chargebacks during the pandemic, a time when operational roles were often reduced. Almost a quarter of respondents admitted that their companies can’t handle the increased burden and are currently unable to respond to or challenge chargebacks.

According to chargeback management firm, Chargebacks 911, around two-thirds of all chargebacks are categorised as ‘friendly fraud’ for which merchants should not be held liable. This occurs when a customer makes a purchase with a credit or debit card and then disputes the charge with their bank even if they don’t have a legitimate reason to do so. There have also been reports of travellers submitting chargebacks in situations where they haven’t received the signature cocktail during a flight or when a trip was ‘unreasonably turbulent’.

One way the industry is working to rethink chargebacks, is through automation powered by improved information visibility. Often the key to resolving a dispute is transparent access to information. By making certain information more visible via application programming interfaces (APIs), for example, booking and payments information, there is an opportunity to automate and improve this important backoffice function.

Where the opportunities lie

Buy Now Pay Later (BNPL) — where travel is paid for in a series of instalments based on a rapid credit assessment — is becoming increasingly common in travel. Of course, BNPL is already a widely accepted payment solution in other sectors, with data showing that by 2024 around 10% of all e-Commerce sales in the US will be made using BNPL, up 300% since 2018. This payment solution is particularly well suited to travel, which has a high average purchase cost representing a significant up-front investment on the part of the traveller.

However, travel companies aren’t banks, and assessing credit risk is complicated. Specialist providers have gained traction by offering plugand-play BNPL capabilities for the sector. These providers assess the traveller’s credit score and the ability to pay the instalments. They may also offer models where they assume the consumer default risk, including providing the fare to the merchant at the time of booking.

There are several scenarios where travellers choose to use BNPL, including upgrading to business class experiences and spreading the costs across 12 monthly instalments for a oneoff fee at the time of booking. Meanwhile, many travellers who can afford the initial up-front cost still choose to spread the payments to preserve their free cash flow. For travel businesses, BNPL helps improve the customers’ booking and payment experience while increasing conversion and boosting ancillary revenue opportunities.

According to Amadeus' Pay When You Fly research , 49% of 5,000 travellers surveyed said they would be more likely to book an airline ancillary service, while 68% said they would spend more overall on their trip if BNPL was offered.

Meanwhile, almost a third of travel companies this year see the pricing of services in multiple currencies as a priority. If travellers book a flight or holiday using a third-party website non-native website, they are likely presented with the price in a foreign currency which is unfamiliar to them. Often this may lead to basket abandonment and might direct potential buyers to a third-party website where they will manually convert the price.

A growing number of travel companies are interested in simplifying this experience by presenting services in a currency the traveller understands. Enabling them to select their preferred currency to settle the payment on an airline’s website helps the company assume greater control over the foreign exchange transactions to which its customers are exposed. Rather than a financial intermediary completing an FX transaction and adding conversion spread, travel companies can work with an FX provider so travellers can play in their native currency with greater transparency. It also avoids the need for travellers to navigate away from the booking stream to a third-party website to manually convert the price.

Fintech will become more intertwined in travel and tourism as travel companies begin to offer regulated financial products that play to loyalty advantages they have established over the years. For example, the online travel agency Hopper has been performing strongly thanks to its array of fintech products. One such tool enables customers to pay a fee to leave a hotel after check-in for any reason

Additional fintech services include disruption protection in the event of delayed flights and cancellations and another that lets customers pay to freeze the price of a hotel room before it rises.

prevalent too. Imagine a traveller arriving at the airport and identifying themselves by using biometrics at

the kiosk. Then they decide to buy fast-track security and lounge access quickly and simply by presenting their face at a scanner. This method could also be used in place of a boarding pass and passport, or when a traveller picks up a rental car or checks into a hotel. With identity stored on a traveller’s phone, travel companies can reduce compliance risk as they no longer need to store as much sensitive passenger data.

Payments are essential to the overall travel experience. To meet the new expectations of today’s traveller, the industry needs greater innovation and investment. The expansion of fintech in travel presents a wide range of possibilities for travel companies looking to improve their digital experience, boost customer loyalty and, most importantly, ensure a smooth traveller experience across all touchpoints.

Travel will always remain an escape from the stresses of everyday life, we should ensure it is enjoyable and as smooth as possible.

Damian Alonso Head of Platform and Partnerships Amadeus

U.S. markets could change course more quickly, and in different ways, than investors might assume. Even if the economy succumbs to recession in 2023, if history is a guide, the equity market would likely begin a new bull market cycle before the recession ends. In fixed income, we think the window to put money to work is now open, but could close sooner than expected. In our view, it’s time to bring portfolio asset allocations in line with long-term strategic recommendations.

We’re not there yet, but we are getting closer

Kelly Bogdanova, Vice President, Portfolio Analyst Portfolio Advisory Group – U.S. at RBC Wealth Management, says:

“Are we there yet?” This classic question that parents and grandparents are often asked on long road trips was posed by our U.S. Investment Committee in June 2022. At that point, we noted there were orange cones along the roadside and there was a need for more economic data for better visibility. Some months later, our answer now is, “We’re not there yet, but we are getting closer.”

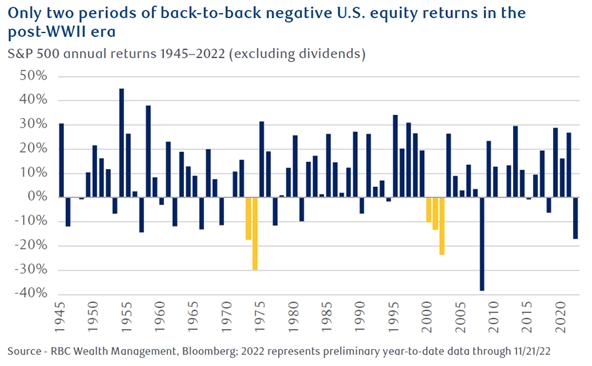

First, it would be rare for the S&P 500 to deliver back-to-back negative return years. They have occurred only twice in the postWWII era. The market has already absorbed significant blows, including one of the Fed’s fastest and biggest tightening cycles in history. On the former, we think the Fed will slow the pace of rate hikes, maybe as soon as the December 2022 meeting; and on the latter, we think the rate hike cycle is poised to end in 2023.

Second, the corporate earnings outlook is “less bad” than in previous periods of economic stress. If 2023 S&P 500 earnings end up flat compared to 2022 at roughly $220 per share—a scenario we think is possible—most institutional investors would likely breathe a sigh of relief. Even if a recession materializes and brings with it deeper cuts to consensus earnings estimates, we think household spending would be relatively more resilient than in recent economic contractions. Household balance sheets appear to be in better shape due to sturdier employment trends and high savings levels when this period began.

Third, equity market sentiment could benefit from declining inflation in 2023. Price trends for commodities and goods are already pointing in this direction.

But don’t misunderstand—we’re not Pollyannaish about the market’s prospects for 2023. There are reasons to remain vigilant. The economy is still at risk of succumbing to a recession. If S&P 500 earnings come in around $220 per share or less, this below-average growth rate would leave little room for price-to-earnings valuation expansion and profit margins could come under pressure. And while we anticipate inflation will decline, there is an open question as to how fast and to what degree. This can impact the market’s valuation. Generally, elevated inflation and interest rates over the medium term result in lower equity market valuations, and vice versa.

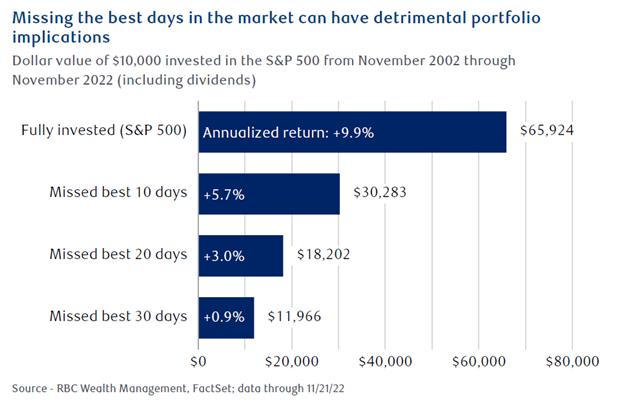

We think the most important objective for investors is to review portfolios and bring them in line with long-term strategic allocation recommendations. Allocations naturally get out of whack during corrections, and there is industry evidence that large cash positions have piled up in portfolios. We think attempting to time the market is a precarious exercise. There is no bell that rings when a new bull market cycle begins. Missing the biggest rally days can have detrimental long-term performance consequences, and such rallies often occur unpredictably before all of the obstacles are out of the road.

Once allocations are brought back into balance, we would keep an eye out for opportunities as the economic, interest rate, and earnings pictures start to become clearer.

Currently, we favor the small-capitalization and midcap segments of the U.S. equity market. Their valuations are relatively inexpensive compared to large caps and their own historical averages. This should provide a cushion as earnings estimates adjust further. When the U.S. economy works through challenging periods, these more economically-sensitive segments often lead the early stages of the next bull market phase.

Within the large-cap S&P 500, we continue to favor the Energy sector. Consensus earnings revisions are holding up better than most sectors. Tight energy commodity supplies are unlikely to be fully resolved in the near or medium term due to many years of capital underinvestment. This should help support commodity prices and Energy company earnings to a greater degree than in typical periods of economic weakness.

2023 to see the Federal Reserve embark on its third act

Thomas Garretson, Senior Portfolio Strategist Fixed Income Strategies Portfolio

Advisory Group – U.S. at RBC Wealth Management, says:

A dual mandate. In 2021, the Fed’s sole focus was returning U.S. labor markets to “full employment,” the first side of its congressionally-given dual mandate, and long-judged by the Fed to be around 4.0%. Unemployment fell to 3.9% in December 2021 and has remained at and even below the target level since. In 2022, the Fed became hyperfocused on returning the economy to “price stability,” the second side of its mandate and defined as prices rising 2% annually on average through any given business cycle. While it will take time for the inflation to get there, the aggressive action from the Fed in 2022 has laid the foundation for it to return to target in due course, in our view.

Financial stability in focus. That now sets the stage for the Fed to turn its focus in 2023 to its unofficial third mandate—financial stability. The historically aggressive tightening campaigns by the Fed and many other global central banks will likely necessitate a far more cautious approach from policymakers, and a heightened focus on—and consideration of—domestic and global financial vulnerabilities that may come as a result of higher interest rates, particularly from the strength of the dollar. This could mean the Fed soon places the blunt tool of rate hikes back in the toolbox and employs more surgical, macroprudential measures that help to ensure the soundness of, and liquidity within, the financial system.

Interest rates to peak in early 2023. We anticipate the Fed’s likely 50 basis point rate hike at the Dec. 13–14 meeting will bring short-term rates to a 4.25%–4.50% range and will mark the last of the jumbo-sized moves.

Any further rate hikes in 2023 should continue at 25 basis point increments, and only if justified by the incoming data, while attaining a level no higher than 5.00% by Q1 2023, in our view. Then, as the generally assumed 12– to 18–month lagged impact of rate hikes that began in March 2022 begin to significantly weigh on economic activity by the middle of 2023, we foresee the Fed delivering a series of modest rate cuts over the course of the back half of the year as it works to engineer some semblance of an economic soft landing.

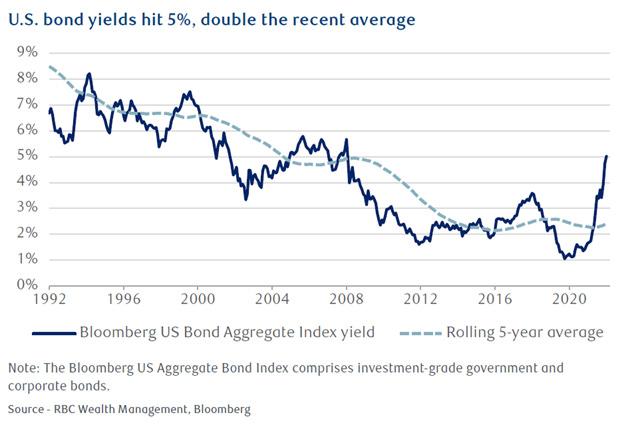

Yields to fall. Markets, forward looking as they are, may already be in the process of pricing in such a scenario as recent soft consumer and producer price data have driven Treasury yields sharply lower from this year’s highs. We believe the sharp rise in yields across the fixed income landscape that played out over the course of 2022 will give way to the opposite in 2023. For example, the benchmark 10-year Treasury yield could fall below 3.5% by the end of the year, from levels close to 4.0% currently, based on RBC Capital Markets’ forecast.

Lock in high yields. The net result for fixed income investors is that the window to put money to work is open, and it could close sooner than expected. Based on Bloomberg bond indexes, Treasuries yielded 4.2%, investment-grade corporate bonds 5.4%, and tax-exempt municipals 3.7% as of November 22. Should yields on offer fade over the course of 2023, as we broadly expect, that could introduce heightened reinvestment risk for short-maturity securities. We continue to favor a strategy of locking in historically-high yields in intermediate and longer-dated bonds to maintain income, and to benefit from capital appreciation should bond prices move higher, and yields lower, due to recession risks in 2023 and the potential for Fed rate cuts as a result.

Kelly Bogdanova Vice President, Portfolio Analyst Portfolio Advisory Group – U.S. RBC Wealth Management

Kelly Bogdanova Vice President, Portfolio Analyst Portfolio Advisory Group – U.S. RBC Wealth Management

2022 was a year of transition for consumers, as BNPL (Buy Now, Pay Later) and mobile payments became mainstream, SoftPOS technologies swept into the retail world, and CBDCs took another major step forward in their development. But what’s coming next?

Tommaso Jacopo Ulissi, Head of Group Business Strategy, Nexi Group exploressome key trends to expect in 2023…

Lessons learned from 2022

BNPL

As many predicted at the end of 2021, 2022 was the year Buy Now Pay Later (BNPL) became a mainstream payment method. For merchants, BNPL has boosted sales and has driven conversion rates, attracting consumers by offering more flexible payment options.

On one hand, BNPL has broadened the opportunities for consumer purchasing and merchant sales, but on the other, its business model may soon face harder times with higher interest rates and increasing costs of capital, shifting the focus from pure growth to sustainability in the long-term. There are also persisting concerns about unsustainable overconsumption by consumers: the world faces a challenging macro-economic environment in 2023 and regulators must focus on further understanding how to balance the need for growth and innovation with sufficient protection for consumers.

Additionally, consumer payment preferences have continuously evolved from paper-based to digital payments, with mobile payments surging as a popular in-store payment method. This has been driven by convenience offered by ubiquitous technology, such as the security offered by biometric authentication in mobile payments.

We at Nexi have seen mobile payment transactions booming in 2022 with a 185% increase compared to 2021. By the end of the year, we predict mobile payment values to reach €445 billion at European market level.

SoftPOS

2022 confirmed that adoption rates of solutions designed to solve customer problems and address merchant needs is continuously growing. The most notable example is SoftPOS technology, tailored to provide additional opportunities for merchants to accept payments with increased flexibility and convenience simply from their smartphone devices.

SoftPOS can provide customers with a streamlined and flexible shopping experience in which they do not need to queue at a specific Point of Sale (POS). This helps the merchant free up staff from cash registers to focus on enhancing the customer experience. Without the reliance on dedicated hardware at the POS, rollout can take place much faster, and at a minimal cost compared to standard payment infrastructure. This brings even more versatility to an already flexible and simple solution, especially as a companion or as a back-up device for merchants.

Consumers are becoming more sophisticated with online payments. They expect not only a frictionless and safe payment experience, but also a more personalized customer journey, starting from their mobile. We anticipate further growth of other smart devices (also powered by the Internet of Things, "IoT") and digital wallets, which will be tied closer to our digital identities as legislation in Europe continues to advance. Moreover, an increasing

uptake of other complementary payment methods such as Account-toAccount will characterize the ongoing digitalization of everyday purchasing.

For merchants, digital is becoming central to their businesses strategy. While we expect SoftPOS to catalyze momentum for increased digitalization, we also expect the merchant's offering to become more sophisticated, delivering increasingly seamless payment experiences to their clients. Merchants will progressively adopt omnichannel solutions, aiming to capture eCommerce growth, and will implement data-driven value-added services (VAS) to increase conversion on online and offline platforms.

This reflects increasing convergence between software and payments into commerce platforms, also via Independent Software Vendor (ISV) and Personal Software Process (PSP) partnerships, to provide business management capabilities to merchants across the entire lifecycle. This is tailored to the specific needs of each differentiated segment, including the restaurant, hospitality, and retail industries. Such platforms will become a one-stop commerce solution for merchants where financial and other additional services will be progressively embedded.

Lastly, the ever-evolving payment ecosystem is facing upcoming changes at a systemic level in 2023. Such change will see accelerated efforts from Central Banks to develop regulated and viable digital currencies. In 2022, the EU, China, India and many other countries all made steps towards developing their own Central Banks Digital Currencies (CBDCs). More countries will do so in 2023.

CBDCs have the potential to offer a safer, faster, cheaper cross-border payment experience for banks, retailers and consumers. This promotes greater financial inclusion in a world where new forms of private-led money, namely cryptocurrencies and stablecoins, have turned out to be risky investment assets rather than a digital storage and transfer of value. As economies around the world are put under increased strain in 2023, CBDCs can provide an opportunity to strengthen central monetary sovereignty. In this regard, the launch and progressive roll-out of the Digital Euro will be one to "watch out" for in the European industry.

Looking ahead, corporates will navigate under uncertain economic environments in 2023. To succeed during this challenging time, they need to be closer to consumers and merchants and put them at the centre of their strategy. Equally, fintechs must develop products and solutions to best answer specific client needs.

Investment in new skills is crucial to the acceleration and transformation of the digital payments market in 2023. Fintechs should focus on how to attract new recruits in a challenging talent market, while they commit to upskilling new hires, to ensure that they have the specific technical skills required to develop the next generation of payment technology. With strong internal expertise, businesses can develop innovative solutions at a reduced time-tomarket and get ahead of competitors.

Financial institutions are under increasing pressure from investors and regulators to prove their commitment to sustainable finance and net-zero. Fintech companies should define firm priority actions regarding climate in 2023, looking to provide services that address the need for a more informed and environmentally friendly approach to daily consumption habits.

As we head into 2023, Joe Myers, executive vice president, global banking at Diebold Nixdorf, explores some of the key themes having impact and driving change for the banking industry.

What are the main drivers in the banking industry right now?

As the industry continues to navigate a path of change, I see three main drivers right now. Firstly, it’s all about the customer. Keeping the customer at the heart of all strategic decisions is not just a ‘nice to do’ but a ‘must do.’ Influenced by experiences within the retail sector, customers are more demanding than ever; therefore, the need to keep pace with these expectations is forcing banks to revaluate when, how and where services are offered.

Secondly, efficiency is top of the internal radar. Increased competition, costly legacy infrastructure and complex regulatory requirements are all driving the need to improve the efficiency ratio. To achieve this, we are seeing the concept of simplicity being introduced with heightened vigour. Striping out complexity and focusing on the areas that drive customer satisfaction or generate revenue are all strategies the industry is adopting to drive a laser focus on efficiency.

Finally, the third driver we are seeing is futureproofing. We’ve seen more change in the banking industry in the last few years than we have in the last twenty years. Therefore, there

has never been a more critical time to take a step back and re-evaluate what future success will look like, as well as how to get there. As a result, banks are streamlining operations, collaborating with joint ventures, outsourcing and introducing valueadded services for customers to drive new revenue streams.

How are banks that are leveraging technology able to engage clients across channels?

Technology provides the backbone for integration, and integration is what enables the delivery of a more connected consumer experience across multiple channels. Whether it’s through mobile banking or at the selfservice channel, the ultimate goal is to make the end-to-end experience as seamless as possible.

The industry has taken huge strides towards more connected experiences, but the gap between physical and digital still exists. This is where technology makes the difference. We’ve been supporting banks across the globe to get the right technology mix and navigate the migration path between physical and digital services. Essentially it is about creating more convenience and more value, enabling services to be presented in a way that the customer wants to consume them.

How does digital transformation improve customer experience, optimise operational efficiency and create new opportunities within the banking industry?

The rise of digital has touched every part of our lives and the banking industry is no different. This increase in digitisation has ultimately provided the opportunity for two key factors for consumers – convenience and choice. From 24/7 mobile banking to prestaging a cash transaction on your mobile phone, which is then fulfilled through the self-service channel, digital is creating the opportunity for consumers to bank on their terms.

As consumer behavior changes and with many routine transactions shifting to digital channels, banks have naturally been able to optiwmise operations, as well as reevaluate branch networks. However, this leads to the vital question of how to maintain the balance between physical and digital channels, as well as how to leverage existing investments. We believe self-service continues to be this bridge and through open APIs, flexible software and advanced functionality, we’re shifting the ATM from a simple “cash & dash” machine to a strategic point of engagement.

What can banks do to ensure their services remain meaningful in an increasingly digital world?

At the end of the day, we all want to feel like our banks know us and can meet our financial needs. Gone are the days when branch staff would know us personally, but maintaining an emotional connection is still possible in the new era of banking. In order to achieve this, personalisation and delivering fit for purpose services are incredibility important.

Banks hold a huge amount of data on individuals, and this must be harnessed in order to maintain meaningful relationships. Using this data to create customer profiles and develop multi-layered segmentation can help support this process, alongside embracing the power of technologies such as artificial intelligence.

Applying this data effectively can also ensure optimised customer journeys are in place, making sure the right services are delivered in the right way. This may require new customer journey mapping, re-evaluation of product offerings and a shift from an internal process driven mindset to a customer centric view, but it’s the essential foundation of any interaction, whether physical or digital.

There seems to be an increasing industry openness to outsourcing. What trends, challenges and barriers are impacting this?

The industry has hit an inflection point where the balance between achieving customer satisfaction and delivering operational effectiveness is becoming challenging for some organisations. Banks need to become more nimble and more adaptive, and that requires both a modernisation of solutions and systems, as well as a strategic plan to remain competitive.

Delivering solutions that allow banks to compete at the same speed as fintechs often means a shift from the status quo. As a result, we’ve seen many banks outsource services and elements of their organisation to industry experts, allowing them to focus on their core business, customer retention and revenue generation.

Inertia, trust and mindsets of ‘this is how we’ve always done it’ can sometimes create barriers for such change. These initial worries are soon dispelled as banks’ operations and service offerings elevate and excel – allowing customers to be served in a quicker, easier and more profitable fashion.

Collaboration is a trend we will see continue to accelerate. With the rising competitive pressures and increasingly complex regulatory environmentalongside of course the more demanding consumer - partnering has given many organisations the ability to remain relevant, as well as new opportunities for growth. Whether it’s teaming up with a fintech, strategic partnering with industry experts or joining forces with other financial institutions for shared banking services, working together is the future of banking.

Joe Myers Executive Vice President, Global Banking, Diebold Nixdorf

David Ritter Director of Financial Services Strategy CI&T

David Ritter Director of Financial Services Strategy CI&T

As we enter a new year, we often look forward to a period of respite, in which we can think positively and prepare for a healthier, happier future. However, today’s imminently tougher economic conditions may not align with such an optimistic outlook.

The Bank of England has already warned that the UK faces its longest recession on record , with a potential two-year slump doubling unemployment rates. Meanwhile, food and energy prices continue to soar, leaving households struggling to pay bills and businesses facing a tough future as consumers rein in their spending.

However, volatility also often brings opportunity—with new ideas and technologies waiting to transform how we interact with customers and capital. Whether we like it or not, we’re set for a period of change. So, buckle up, banking and finance professionals: if 2022 was a bumpy ride, 2023 is set to be a stormy, pothole-filled marathon. Here are my top three predictions for the year ahead.

As the cost-of-living crisis bites, we’ll likely see buy now, pay later options reigned in.

The very nature of this type of payment option can cause people to overextend themselves leading to late payment penalties and growing debt.

To protect against the threat of increased credit risk, we’ll see buy now, pay later providers undertaking greater due diligence and becoming much stricter when it comes to eligibility criteria, credit checks, and the size of loans on offer.

There needs to be much greater communication between this group of lenders. There’s a black hole in consumers’ credit histories as providers have no insights into how many different buy now, pay later debts a consumer is carrying, and this creates enormous risk to both the provider and the consumer.

The integration of open banking may help here but it is reliant on consumers agreeing to share their data. And while responsible borrowers are likely to do so, those who struggle to repay may refuse consent in order to protect their future borrowing prospects.

Recent regulatory advancements, such as the EU’s markets in crypto-assets (MiCA) proposal and the UK’s recently concluded consultation into the regulatory approach to crypto-assets and stablecoins, indicate that there is a desire for more control.

However, there is currently little international cooperation, and this country-by-country approach is all we’re likely to see for now.

Ultimately, we need a worldwide approach, which is coordinated, consistent, and compressive. It’s up to the early pioneers to set the rules and standards – if a predefined, universal policy emerges, we’ll see wider opportunities for global commerce.

I’m already seeing a number of banks using augmented and virtual reality (AR and VR) to train customer-facing employees. But, as the internet evolves, we can’t rule out big banks utilising the metaverse to improve the customer experience. In light of extensive branch closures, it will help to provide a more personalised approach with a human touch.

of the metaverse in the banking sector is consumer access to the technology required. Headset prices make them inaccessible for many and whilst technological advancements may drive down the cost of headsets there is still some way to go. Only once there is a solid user base in place will our banks start to take this brave new metaverse world more seriously.

78% of Gen Z say the cost-of-living crisis has made them more likely to talk about finances with their peers, but what headwinds do they face and what’s causing them to open up?

The cost-of-living crisis is really starting to bite. Prices are going up due to rampant inflation, which in turn is impacting how much disposable income we have to spend each month.

For many of us, when you see the strength of your pay packet diminishing each month, with less and less available for doing the things you love or for putting aside, it can be disheartening. This is especially true when you’re at the beginning of your career, when there is less of a buffer and every penny really does count.

This of course impacts how we interact with money, and shapes our future attitudes as to how we spend or save. According to our research in partnership with Samsung, Gen Z are now the generation most likely to talk about money, with the vast majority (78%) attributing this to the cost-of-living crisis. What’s more, it’s also impacting financial education, with 62% of Gen Zs saying the costof-living crisis has helped them to understand terms like inflation and recession - perhaps due to their prevalence in the media. Most tellingly, nearly four in five, 79%, say it’s made them more aware of their finances.

No matter which area of financial services you work in, these statistics matter. Why? Because it means

younger people are getting financially savvier quicker, as the pressure on their pay packet is more intense than ever. Let’s take a look at some of the key drivers.

For those Gen Zs who have not yet joined the workforce full-time, or have taken their first steps into a career in retail or foodservice, the rise in the National Living Wage will be a welcome boost. The hourly 92p increase, worth nearly £1,800 a year for those working a standard 40-hour week, arrives in April 2023 - and not a moment too soon for the workers battling increasing living costs due to rampant inflation.

While the living wage is going up, overall wage stagnation remains an issue that many younger workers will have to contend with for at least the next few years. According to the Resolution Foundation, the economic outlook means that real wages are not expected to return to 2008 levels until 2027. Plus, with the freezing of tax bands dragging more and more workers into paying tax by 2028, the ‘squeezed middle’ of the UK workforce is set to become more saturated.

The impact of this ‘stealth’ tax increase is significant. We estimate the average UK earner with a salary of £33,000 in 2021/22 would pay a total amount of £28,944 in income tax over the next five years if the tax band thresholds were frozen for the whole period. This compares to £24,145 in

income tax if the thresholds were linked to inflation over the same period. This is a big difference of 20%. For those starting out in their careers and trying to put money aside for their future, this tax raid not only slows earning power, but future wealth too.

While not many Gen Zs will be in a position to buy a house following years of rapid price growth (last year prices increased 9.5% alone), the Stamp Duty cut freeze will provide an incentive to try and put some money aside for a deposit. Nevertheless, with the average house now costing £295k , this will likely still be out of reach for many, and the average age of a first time buyer is now reaching 32

Renting doesn’t provide a positive picture either. Rent in the UK overall has risen 12%, while in the capital it has increased by 18% year-onyear, according to Zoopla . Data from SpareRoom shows that even if you just want to rent a room in London, you’re looking at £857 per month, compared to an average of £554 elsewhere in the UK.

It’s clear that Gen Z is facing a combination of financial challenges as they enter the workforce. Considering the headwinds, it’s no wonder they’re opening up to their peers about their finances. We know from our data that Gen Z are most likely to learn about personal finance topics from friends (63%), parents (62%), traditional media (53%) and financial influencers (52%), as they look to balance rising costs with wages that can’t keep up.

The bad news is, it’s arguably going to get worse in 2023. Energy price support will end in April, and with rising interest rates likely impacting student loan repayments, it’s easy to see how costs can start spiraling. It’s good to see that young people are trying to sort out their financial future, even if it’s looking a little bleak currently. The best thing they can do is to keep learning. Look at ways to improve your financial footing and help your money grow - be that highinterest savings accounts, paying down debt, or investing regularly for the long term, even if it’s small amounts at a time.

Meanwhile, businesses must ensure that this shift in attitudes does not catch them unawares. Brits are traditionally tight lipped about their finances, so this is an excellent new opportunity for education. Provide the information people want in simple yet concise formats. Engaging Gen Zs directly may also help firms get on the front foot, as people try to grapple with their finances themselves, instead of turning to experts to help them make returns.

In 2023, we’ll see prices of goods continue to increase in the UK as rising inflation takes effect. Many consumers are already struggling to afford basic products and becoming increasingly cautious in their spending habits to combat the cost-of-living crisis. In fact, 87% of shoppers globally have admitted they are looking for ways to make purchases more cheaply.

While many retailers are seeing steep declines in sales, The UK Office for National statistics stated that, in October, ‘the sub-sector of other nonfood stores reported a monthly rise in sales volumes of 3.6% because of strong growth in second-hand goods stores.’ In turn, this is generating a rise in the use of resale marketplaces and platforms.

Resale marketplaces - often referred to as customer-to-customer (C2C) marketplaces - are an alternative way to buy and sell goods, often at a lower price than available at traditional retailers. They provide a complete shopping experience, usually including fast and reliable payment options, delivery services and more. Today’s economic climate presents marketplaces with the opportunity to act as crucial lifelines for consumers searching for ways to navigate the ongoing impact of inflation.

Typically, pre-loved goods sold on C2C marketplaces are less expensive than brand-new products from the original retailer. While resale stores aren’t new, online C2C marketplaces have their own unique set of benefits setting them apart from other e-commerce players. Marketplaces allow sellers to offer the same products as others on the same platform and set their

own prices, enabling them to remain competitive. As a result, consumers can shop around and compare prices, all on a single platform.

In addition, shoppers can purchase items from multiple sellers via a single transaction - eliminating the need to visit multiple e-commerce sites and make several purchases to secure items at a lower price. This means consumers have a single, unified payment journey, creating a more seamless experience.

Marketplaces have complex payment requirements as they need to manage buyers, sellers, and transactions on a local, and potentially global, scale. As payment preferences and regulations vary somewhat from country to country, it’s crucial that marketplaces are constantly innovating to guarantee the best payment experience for their users, whether they are for buyers or sellers.

Given today’s economic climate, many marketplaces are now offering alternative payment methods (APMs) such as Buy Now, Pay Later (BNPL), to allow consumers to pay for items over a longer period in manageable instalments. This means that even on a tighter budget, consumers can still access necessary goods, at lower, spread-out costs.

In addition to varied payment offerings, marketplaces need to consider the security of their platform and transactions. Recent research shows that over half ( 59% ) of consumers are more concerned about becoming a victim of fraud now than they were in 2021, following the cost-of-living crisis. What’s more, 62% of people are now so concerned about fraud they feel

it is simply an inevitable risk of online shopping, up 17% compared to those who said the same in 2021. To further secure the digital payments process, marketplaces should work strategically with fintechs that offer sophisticated fraud and detection solutions to further instil trust with consumers.

Sustainability is now a key concern for many consumers. As there is a greater understanding of consumer impact on the world, consumers are looking for ways to consume more responsibly. According to Deloitte, however, price is the top reason many consumers have not adopted a more sustainable lifestyle in the last 12 months, with 52% claiming it’s just too expensive.

Resale marketplaces lower the barriers to entry for eco-conscious consumers, allowing them to continue shopping at a lower price. Furthermore, as well as being consumers, they can also be sellers and pass on pre-loved items. As shopping patterns continue to change, particularly among Gen Z and Millennials, resale marketplaces will be viable for consumers in fighting rising costs.

The same Deloitte report revealed that 40% of consumers have bought second-hand or refurbished goods in 2022 and this trend is likely to continue as economic issues remain prevalent and awareness of sustainable commerce practices grows.

It’s not just existing marketplaces such as Vinted or Wallapop that are recognising the opportunity presented by the rise in demand for pre-loved goods. Many established

fashion brands are now creating their own resale or recommerce marketplaces to create additional revenue streams, enhance customer loyalty during tough economic times, and reach a broader range of customers.

For example, in October 2022 Zara unveiled plans to launch its new, pre-owned platform in the UK (Zara Pre-Owned) where customers can resell their Zara items through a peer-to-peer process - integrated through Zara’s physical stores, its e-commerce site and its mobile app. This launch will help companies continue to take steps towards a circular economy model, while encouraging customers to make more sustainable decisions on fashion consumption.

Looking forward, the resale fashion market alone is predicted to grow by 52% between 2023 and 2026 as shoppers continue to tighten their belts. As a result, there is clear space for C2C marketplaces to seize this as an opportunity to grow in popularity and cement themselves as key players in the e-commerce sector.

Trayfoot Chief Revenue Officer MANGOPAY

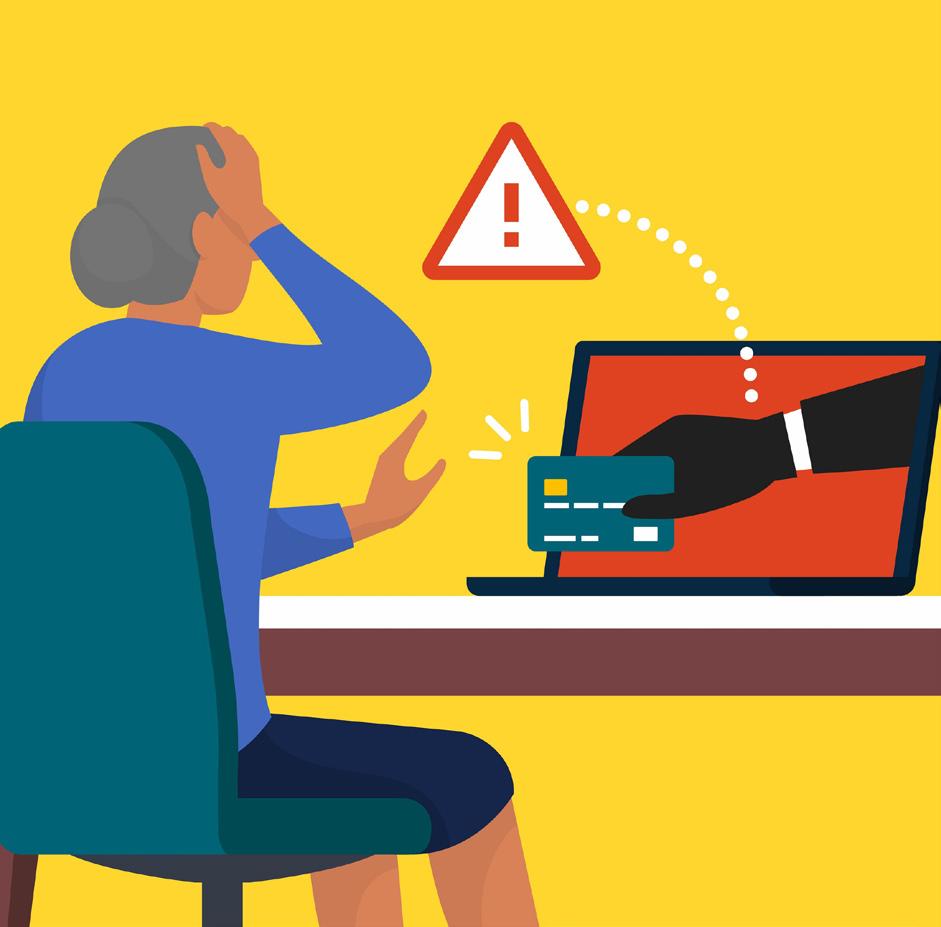

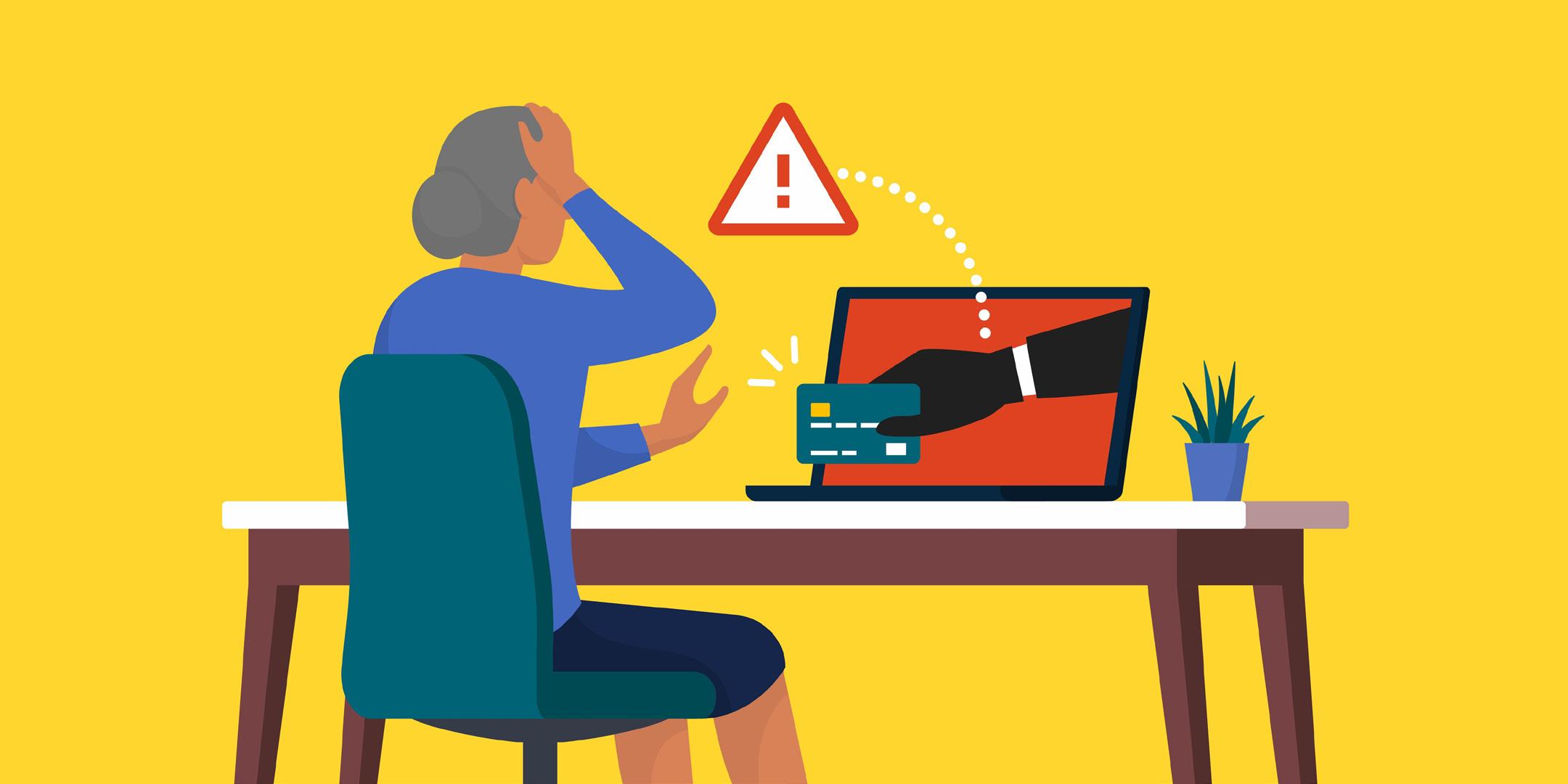

Record levels of fraud are being dealt with in the financial services industry. In comparison to the offences committed in 2018, there has been a 151% increase in fraud in 2022, according to a recent UK Finance report.

The upcoming "scampocalypse" is being caused mostly by two things. Peer-to-peer payment apps' emergence, the sudden shift in labour, and a hastily devised pandemic stimulus plan have all contributed to an increase in scammers. So, why have social engineering bank account scams dramatically increased, and what can financial institutions (FIs) do to stop a scampocalypse?

For banks to address the scam issue, a practical definition of what constitutes a scam is required. Most financial institutions concur that a scam is a social engineering attack intended to deceive the victim into providing crucial information or directly paying the attacker, even though definitions vary depending on who you ask.

It’s helpful to divide the universe of scams into those that exist for the primary purpose of coercing the victim into making a fraudulent payment and those that exist primarily for the purpose of harvesting sensitive information in support of fraud attacks that may take place later. That gives us two categories of scams: Harvesting scams and payment fraud scams.

Harvesting scams - An attacker uses a harvesting scam to trick the victim into disclosing information such as login credentials or financial and personal information. The attacker then holds on to the information to use for future bank account scams — primarily account takeover fraud.

Payment fraud scams - Payment fraud scams, such as authorised push payment (APP) fraud, occur when an attacker coerces a victim into making an authorised bank transfer or sending money in real time over a P2P payment network. Because of the increased acceptance of digital banking and payments, as well as the convenience with which it may be done, this type of scam approach is flourishing.

Who is responsible if you fall victim to fraud?

Banks are typically the first place scam victims turn to obtain compensation. The customer support staff at the victim's bank will take prompt action when the victim phones to stop further financial loss.

APP fraud makes it harder to recover stolen funds if the account owner sent money to someone because of a scam - for example, if they paid a fake invoice or bill. Most banks will agree to repay lost funds voluntarily if a customer falls for a scam. However, the customer may be asked to present additional evidence to prove they are truly a victim. This may include the customer being asked to prove:

• If they obeyed any security warnings sent by the bank

• That they believed the transaction was legitimate

• They were not acting careless when the payment was made

In the UK, where a “scampocalypse” of sorts began in 2013, the APP Contingent Reimbursement Model Voluntary Code , dubbed “The Code,” provides some protection. Recent changes to the reimbursement code , specifically “confirmation of payee” checks which require a user to input

a person’s first and last name and account details before sending them money, may help reduce the impact of scams. In addition, the UK government has stated that legislation will be introduced to help combat this specific type of fraud, but it hasn’t happened yet, and there is still uncertainty of what it will look like.

The PSR wants the payments industry to change the way it manages APP scams. The measures being proposed include:

• Requiring reimbursement in all but exceptional cases – so more victims will get their money back.

• Improve the level of protection for APP scam victims –so there is greater consistency in protections for all victims, irrespective of who they bank with.

• Incentivise banks and building societies to prevent APP scams – because responsibility for allowing fraudulent payments is the responsibility of both the sending and receiving banks or building societies.

The question of accountability does not have a straightforward solution. In the UK this year, victims in 73% of bank and credit account fraud cases, 64% of advance fee fraud cases, and 46% of consumer and retail fraud cases received full compensation.

While there may be no legal consequences for FIs who refuse to refund a victim following a payment fraud scam, it severely damages the faith that customers hold in them. In addition to being robbed, falling prey to a scam causes tremendous emotional damage, which is only made worse when a victim calls their bank and is told they will not be reimbursed. It adds a feeling of betrayal to an already terrible situation. Ignoring this issue only sets FIs up for failure in the long run; the industry is based on trust, and customers will leave their FI for another if they don’t feel their money is being protected.

While the prospect of a "scampocalypse" is terrifying, there are strategies available to avoid even real-time scams, allowing institutions to protect their consumers from becoming victims. Behavioural biometrics is a preventative measure implemented by FIs that can be used to detect social engineering scams.

Since a person under duress behaves differently than one banking under normal conditions, behavioural biometric models catch on and help prevent payment fraud scams as they happen. It’s critical to remember that there is a human element to this problem. Some customers stand to lose their life savings to one of these attacks. In an industry where trust is everything, it makes sense for FIs to get ahead of the problem and do their best to prevent their customers from becoming victims.

Whether or not regulatory actions influencing reimbursement models are undertaken, banks can be proactive in resolving the scam problem before it negatively impacts customers. The only certainty is that FIs and customers will have to work together to avert a total scam catastrophe.

It’s been a roller coaster of a ride for the financial community lately, and odds are the coming year will bring more of the same. Many experts see a bear market on the horizon, which will put investors under even more pressure. One of the thorniest challenges is figuring out the best strategies for ultra-high net worth individuals (UHNWIs), a segment expected to increase by almost 30% over the next few years.

In such a volatile market, technology and data are essential to success. Family offices in particular need to up their game. Many still use a cobbled-together infrastructure relying heavily on spreadsheets, various portfolio software platforms and general systems, with reporting available only on an ad hoc basis. An ideal fintech solution would handle all these functions and enable financial managers to expand portfolio volume and improve performance.

In the following, we’ll look at the technology and trends that will be fueling family offices in 2023.

Data is incredibly valuable — provided it’s complete, up-to-date and accurate. When it’s reliable, data can support strategic insights and smart decision-making. But most organizations, and family offices in particular, don’t have the time or resources to cope with the overwhelming amount of data now available. They need to adopt a sophisticated platform with software that can manage data and optimize its value.

Rather than using separate accounting systems for each type of investment, all with different formats, family offices will increasingly enlist the latest data engines to gain a clearer view into disparate data in the year ahead. Purposebuilt software can address general ledger and hierarchical ownership structures, drilling into specifics of different investments and pulling out the most relevant information. With timely reports and insights, managers can gain a high level of confidence and better understanding of the data to make decisions that’ll enhance returns.

While there’s no question that technology upgrades are essential, it’s challenging to implement them without significant resources. Most family offices run lean operations with minimal headcount. Given the light staffing, they tend to deal with many outside service providers, averaging 40 or more. Some of those vendors have been pitching all-in-one solutions for managing complex asset portfolios. These often sound great in theory, but in practice, they may not deliver all they promise. That’s when users learn a tough lesson - no single platform can do it all. In fact, a single point of failure spells disaster when it’s the only platform deployed.

Partnering with outside experts is a sound strategy for 2023, as long they can provide a solid plan and a reliable solution. The emerging class of purpose-built platforms with data cores engineered for multi-asset class portfolio management and accounting are a smart and safe option for family offices. They handle both processes expertly which is a huge plus if top managers don’t have the skills or in-depth knowledge required to optimize systems when switching from spreadsheets and QuickBooks.

Taking the time to find the right service providers will pay off both in day-to-day operations now and as the business expands. To ensure positive outcomes, consider bringing in consultants, particularly for business process review and strategic goal setting. Look for ones with proven family office expertise, deep technology knowledge, and a hightouch approach so they, and all of your staff members, really understand your business and can best-position it for success.

Given the wild swings in the market, many investors nowadays are seeking alternative vehicles and diversifying across asset classes. Instead of sticking with individual stocks or funds recommended by a wealth advisor, they’re considering other avenues.

Some family offices are putting resources into specific businesses, much like a venture capitalist. Others are embracing impact investing, funneling dollars into environmental, social and corporate governance

(ESG) ventures with the goal of bolstering their philanthropic efforts. The arts, environment and social justice arenas are among those attracting investors more interested in supporting causes than in netting the biggest returns.

Fintech systems need to be able to cope with these complex and evolving portfolios. Whatever the vehicle, it will be vital for family offices to choose software designed for managing these broad range of assets. Modules for functions such as private investment tracking are a plus. Also important will be a high degree of automation coupled with a user-friendly interface that won’t overwhelm financial executives without an IT background.

Like businesses of all types, family offices have been moving to the cloud. However, they’ve been doing so more slowly than other sectors. That’s due in large part to worries about privacy and security. Those are certainly legitimate concerns. More than one in three North American family offices suffered at least one cyber attack during the previous 12 months, according to Campden Wealth’s North America Family Office Report 2022.

No doubt, we’ll be seeing even greater activity by hackers.

Family members tend to be especially aware of the risks of exposure, given their tendency toward anonymity, rather than self-promotion. But that shouldn’t deter them from embracing the cloud, as well as SaaS, in 2023. Further, they should digitize with all speed, while paying special attention to both data protection and privacy.

That calls for instituting standard best practices on the security front, including strong passwords, ensuring credentials aren’t shared or reused, as well as dual-factor authentication. Also recommended in the year ahead: a single sign-on infrastructure and a partnership with a cybersecurity solution provider.

Outside consultants and outsourcers with expertise in fintech for family offices can be valued partners when it’s time for a transition. They can help identify processes that are limiting growth and put in place state-of-the-art systems that will allow for future expansion. Establishing the right architecture now will go a long way to ensure survival and promote success in the years to come — regardless of how volatile the market becomes.

Nicole Eberhardt is CEO of Ledgex, creators of a platform built by investment office pros to solve multi-asset data quality and usability challenges. Called Ledgex Pro, the solution enables investment firms to confidently and successfully manage complex asset portfolios with game-changing improvements in data accuracy, transparency and timeliness. For more information, please visit www.ledgex.com

Businesses across the world are facing a combination of crises, from inflation to growing energy prices to the long-term consequences of the pandemic. As a result, companies are battling challenges around technological change, talent attraction and retention, as well as fulfilling the environment, social and governance (ESG) role expected of them by regulators and society.

The Future Ready Business survey by Economist Impact, commissioned by Cognizant, looked at the status of companies across sectors and explored how they could prepare to thrive in this environment. One of the industries that scored the lowest was banking and capital markets, which scored fifth of eight in futurepreparedness. The survey concluded that banks, asset managers and financial intermediaries need to urgently modernise if they are to become future ready.

The sector is still suffering from the 2008-2009 financial crises, which led to tighter regulation of its activities and reputational damage that many businesses haven’t managed to shake off. In addition, the financial industries have seen a sharp increase in the number of competitors, as the amount of tech-savvy, client-obsessed FinTechs has exponentially grown over the last decade. In fact, the UK’s fintech market is now valued at £11 billion and represents 10% of the global market.

But it’s not all doom and gloom. Leading players in the banking industry have made notable progress in key areas, such as modernisation of their core and personalisation of

services. These are positive steps in the right direction for individual companies, but the banking and capital markets industry as a whole still has a lot to do to build on these initial successes and continue on its modernisation journey.

The pandemic brought to light many banks’ digitalisation deficits, as remote solutions had to be quickly implemented and internal workflows proved to be less smooth than usual. In the UK, some banks have begun to reprioritise their digital transformation journey to switch certain services online, such as PIN resets, filling out forms and changing loan terms.

Digital solutions – particularly around cloud migration and automation – are already playing a key role in banks’ efforts to modernise and will continue to do so over the next decade. Cloud migration is chosen by many banks to streamline their processes more efficiently. Although cloud migration can be complex, as it often requires tailored solutions, banks that have adopted it have reported cost reductions, improved employee experience and built-in automation capabilities leading to a shorter time-to-market.

Digital transitions are highly complex operations that demand strong, long-term support from banking and financial institutions’ leadership teams and deep alignment throughout the company. Unfortunately, this is where a gap in support can harm organisations; our survey found that only 43% of senior banking and capital markets executives strongly support modernisation in their organisations.

The direct climate impact of banks and financial services companies is relatively modest. Banks’ direct carbon emissions usually come from office operations, data centre use or business trips. Their indirect environmental impact, however, is considerably higher, as it includes the carbon emissions produced by their investment and/or loan portfolios.

This is why banks need to take a proactive stance when it comes to assessing their loans and investments’ sustainability impact. And it seems like many are already doing so, as 87% of banking and capital markets institutions see environmental sustainability as somewhat or very important for businesses today. In practice, however, only one-third of banks actually have resources and staff dedicated to reducing their impact on the environment, and less than half claimed to pursue relevant professional development activities.

One thing is clear; companies in the industry can and must do more. Action can be taken in the shape of assessing the sustainability impact of their many investments and loans, or nudging customers to opt for greener products through special promotions or discounts.

Another area banks need to work on is talent attraction and retention, which has proven to be a top challenge across most industries. Banks, asset managers and financial intermediaries are in a good position having not fully lost their appeal to high-flying professionals, but the sector’s reputation remains scarred by the Global Financial Crisis.

But employees are key to making a business future-ready, as there can be no success without skilled and motivated people. Addressing the industry’s shortcomings in their environmental impact, as well as on diversity and inclusion would go some way towards increasing its appeal to purpose-driven younger talent but would not suffice in and of itself.

Leaders must use technology to improve the work environment and optimise the employee experience, if they are to create an engaged, motivated and satisfied workforce. Many banking and capital markets institutions have already understood this and acted accordingly. Fiftyfour percent reported that their company's technology improvement efforts had a significant positive impact on their employees‘ satisfaction over the past year.

Organisations in the banking and financial sector do have remarkable resilience. Ninety percent of the employees surveyed reported that their companies would be able to keep operating in the case of significant IT disruptions. However, these business’ tech infrastructure needs to go beyond simply being able to operate in the case of an emergency.

To ensure that the industry is ready for anything, the sector needs to eradicate outdated operating models and invest in innovation to double down on efforts to modernise the core of their operations.

John da Gama-Rose Head of BFS, Global Growth Markets Cognizant

Change has been the one constant of the last few years, with 2022 proving no different. Organisations across the financial sector have had to weather the storm fuelled by the sustained impact of a global pandemic, geopolitical tensions and the looming recession. However, for many firms across the industry, uncertainty became resilience and agility, as they used this time to advance digital capabilities and ecosystems.

As 2022 comes to an end and we again look ahead to the new year, we spoke to five industry experts to learn their predictions for 2023 and what organisations can do to stay one step ahead of the tide.

A serious problem for next year comes from inflationary pressures, causing rises in food, fuel, energy, and resources. For businesses and individuals, the cost of living and operating will go up. Although salaries will rise accordingly, Hugh Scantlebury, CEO and Founder of Aqilla, urges that “all those things must be accounted for, so we will need to keep a much closer eye on what’s coming in, and what’s going out.