The information contained in this publication has been obtained from sources the publishers believe to be correct. The publisher wishes to stress that the information contained herein may be subject to varying international, federal, state and/or local laws or regulations.

The purchaser or reader of this publication assumes all responsibility for the use of these materials and information. However, the publisher assumes no responsibility for errors, omissions, or contrary interpretations of the subject matter contained herein no legal liability can be accepted for any errors. No part of this publication may be reproduced without the prior consent of the publisher

editor

Dear Readers’

Welcome to Issue 66 of Global Banking & Finance Review. Whether you are a longtime reader or joining us for the first time, we are delighted to bring you the latest insights and trends shaping the financial sector.

Our cover story delves into "How the Proposed U.S. ‘Protecting Consumers from Payment Scams Act’ Could Impact Financial Institutions’ Fraud Prevention Efforts," by Anurag Mohapatra, Senior Product Manager at NICE Actimize. As fraudsters continue to evolve alongside digital payment platforms, this piece explores how the proposed legislation aims to address growing fraud concerns. Mohapatra outlines how financial institutions can prepare for shared liability and the new regulatory landscape to better protect consumers and prevent fraud. (Page 24)

We also explore the future of cloud-based solutions in financial services in Chris Beard’s "The Top Three Barriers to Cloud-Based Software." As financial institutions seek agility and scalability, this article highlights the key obstacles preventing widespread cloud adoption and offers strategic insights for overcoming them to build more resilient and transparent operations. (Page 18)

Next, we turn our focus to the global stage with "Fosun International: The Hidden Gem Ready to Shine." In an exclusive interview with Co-CEO Chen Qiyu, we uncover Fosun’s impressive global expansion and how the company is unlocking new value for investors. From healthcare innovations to new developments in the Middle East, Fosun's commitment to globalisation and innovation is transforming industries and communities alike. (Page 30)

Pat Bermingham, CEO of Adflex, offers a grounded look at the true potential of AI in financial services with "The AI Act: What Impact Will Artificial Intelligence Really Have on B2B Payments?" With the EU’s AI Act now in force, Bermingham discusses how businesses can navigate the complexities of AI deployment, distinguishing between hype and reality. This article highlights the opportunities for AI to optimise B2B payments, driving efficiency and enhancing cash flow, while keeping human oversight at the core. (Page 20

At Global Banking & Finance Review, we are committed to being your trusted source of insights in the financial sector. As the industry continues to evolve, we strive to bring you the most relevant stories and expert perspectives to help you stay informed and ahead of the curve. We welcome your feedback and invite you to share your thoughts on how we can better serve your needs in future editions.

Enjoy the journey through our latest issue!

Wanda Rich Editor

Stay caught up on the latest news and trends taking place by signing up for our free email newsletter, reading us online at http://www.globalbankingandfinance.com/ and download our App for the latest digital magazine for free on Google Play and the Apple App Store

Building Compliance into Business Culture is Essential in Fintech

Tetyana Golovata, Head of Regulatory Compliance, IFX Payments

FINANCE

Monetizing legal: How CFOs are extracting value from legal assets

Jordan Licht CFO

Burford Capital

Navigating the complexities of internal client money reconciliations

Murray Campbell, Product Manager at AutoRek

Al Hamidi, Business Intelligence Manager, EBC

M&A

5 Tips for Mid-Market Financial Firms to Adopt Automation Fabrics

Charles Crouchman, Chief Product Officer, Redwood Software

Innovative Payment Solutions Boost Spend for Holiday Parks

Fivos Polymniou, Director, Ask Global Solutions..

From Compliance to Resilience: Adapting to DORA in Financial Services

Shilpa Doreswamy, Sector Director of Retail Banking, GFT

Phil

Ronen Assia, Managing Partner, Team8

Digital experience strategy: Capitalizing on the $84 trillion wealth transfer

Joe Scheffler, Director of Client Engagement, Think Company

The top three barriers to cloud-based software

Chris Beard

Solution Sales Director – Europe, Diebold Nixdorf

The AI Act: what impact will Artificial Intelligence really have on B2B payments?

Pat Bermingham, CEO of B2B digital payment specialist, Adflex

Empowering financial service providers: Vulnerability toolkits to support those in need

Craig Wilson, Head of Private Sector, Sopra Steria UK

Mastering complexity: the premium payment processing revolution in insurance Piers Williams, Global Insurance Manager, AutoRek

Chen Qiyu, Executive Director & Co-CEO, Fosun International

Cover Story

How the Proposed U.S. “Protecting Consumers from Payment Scams Act” Could Impact Financial Institutions’ Fraud Prevention Efforts

Anurag Mohapatra, NICE Actimize, SME and Sr. Product Manager

Building Compliance into Business Culture is Essential in Fintech

Regulation plays a critical role in shaping the fintech landscape. From Consumer Duty and FCA annual risk reporting to APP fraud, the tectonic plates of the sector are shifting and whether you consider these regulations as benefiting or hindering the industry, businesses are struggling to keep up.

According to research by fraud prevention fintech Alloy, 93% of respondents said they found it challenging to meet compliance requirements, while in a new study by Davies a third of financial leaders (36%) said their firms had been penalised for compliance breaches in the year to June. With the FCA bringing in its operational resilience rules next March, it is more important than ever to ensure your company makes the grade on compliance.

Lessons from history

Traditionally, FX has struggled with the challenge of reporting in an ever-developing sector. As regulatory bodies catch up and raise the bar on compliance, responsible providers must help the industry navigate the changes and upcoming deadlines.

Fintechs and payments companies are entering uncharted waters – facing pressure to beat rivals by offering more innovative products. When regulators have struggled to keep up in the past, gaps in legislation haveallowed some opportunists to slip between the net, as seen in the collapse of FTX. Because of this, implementation and standardisation of the rules is necessary to ensure that innovation remains seen as a force for good, and to help identify and stamp out illegal activity.

Culture vs business

Culture has become a prominent factor in regulatory news, with cases of large fines and public censure relating to cultural issues. As the FCA’s COO Emily Shepperd, shrewdly observed in a speech to the finance industry, “Culture is what you do when no one is looking”.

Top-level commitment is crucial when it comes to organisational culture. Conduct and culture are closely intertwined, and culture is not merely a tickbox exercise. It is not defined by perks like snack

bars or Friday pizzas; rather, it should be demonstrated in every aspect of the organisation, including processes, people, counterparties, and third parties.

In recent years, regulatory focus has shifted from ethics to culture, recognising its crucial role in building market reputation, ensuring compliance with rules and regulations, boosting client confidence, and retaining employees. The evolving regulatory landscape has significantly impacted e-money and payments firms, with regulations strengthening each year. Each regulation carries elements of culture, as seen in:

• Consumer duty: How do we treat our customers?

• Operational resilience: How can we recover and prevent disruptions to our customers?

• APP fraud: How do we protect our customers?

Key drivers of culture include implementing policies on remuneration, conflicts of interest, and whistleblowing, but for it to become embedded it must touch employees at every level.

This is showcased by senior stakeholders and heads of departments facilitating close relationships with colleagues across a company’s Sales, Operations, Tech and Product teams to build a collaborative environment.

Finance firms must recognise the trust bestowed on them by their customers and ensure the protection of their investments and data is paramount. Consumer Duty may have been a wakeup call for some companies, but progressive regulation must always be embraced and their requirements seen as a baseline rather than a hurdle.

Similarly, the strengthening of operational resilience rules and the upcoming APP fraud regulation in October are to be welcomed, increasing transparency for customers.

Compliance vs business

Following regulatory laws is often viewed as a financial and resource drain, but without proper compliance, companies are vulnerable to situations where vast amounts of money can be lost quickly.

A case in point is the proposed reimbursal requirement for APP fraud, which will mean payment firms could face having to pay compensation of up to £415,000 per case.

Complying not only safeguards the client and their money, but also the business itself. About nine in ten (88%) financial services firms have reported an increased compliance cost over the past five years, according to research from SteelEye. Embedding compliance earlier in business cultures can be beneficial in the long run, cutting the time and money needed to adapt to new regulations and preventing the stress of having to make wholesale changes rapidly.

Building a cross-business compliance culture

Compliance is a key principle at IFX, and we strive to be a champion in this area. In response to these challenges, the business restructured, establishing dedicated risk and regulatory departments, along with an internal audit function.

Regulatory compliance aims to support innovation by developing and using new tools, standards, and approaches to foster innovation and ensure product safety, efficacy, and quality. It has helped the firm to navigate the regulatory landscape while driving growth and maintaining high standards.

This organisational shift allowed each business line to own its own risk, with department partaking in tailored workshops designed to identify existing, new, and potential risk exposure. Shared responsibility for compliance is the only way to create a culture which values it. We see this as a great way for organisations to drive innovation while sticking to the rules.

Tetyana Golovata Head of Regulatory Compliance IFX Payments

Monetizing legal:

How CFOs are extracting value from legal assets

Business disputes have historically been met with scepticism by finance leaders like me: Litigation is seen as a drain on resources and a distraction from core business activities, presenting hefty price tags, unpredictable outcomes and prolonged timelines. That makes litigation a landmine for those of us focused on maintaining financial stability and growth.

However, CFOs are increasingly able to recognize that high-value claims are assets, albeit highly contingent ones. When a business suffers significant financial harm to the tune of scores of millions of dollars, any CFO is going to work with the company’s legal team to ensure the business recovers what it is owed in the most financially advantageous way available. It’s about seeing beyond the nuances of the legal documentation to very real impact of meritorious claims on the bottom line.

The challenge CFOs need to solve along with their GCs is this: As in so many other areas of business, it costs money to make, or in this case recover, money. Litigation is expensive and expected to increase even more in cost in the years to come. According to Burford’s 2024 Litigation Economics survey, 41% of CFOs think litigation spend will increase between 10% and 24% in the next five years, while 32% expect an increase of 25% or more. Another important factor for CFOs to consider when evaluating the significant cost of commercial litigation is duration risk: it can take years for litigants to go through the courts, deal with appeals and eventually get paid. Litigation is a marathon not a sprint, and as CFOs well know, money spent now in anticipation of a recovery at some point in time that may not happen is very expensive money.

Fortunately, businesses now have alternative financing options to recover the value of large and meritorious claims. CFOs are increasingly exploring these options as part of their legal department strategies. By conserving cash that would have been spent on lawyers, businesses can generate value and reallocate funds to other areas of the business. In fact, 37% of finance leaders believe their organization could redirect at least $5 million to other business initiatives through dispute financing.

While the stress of potential liabilities and the fear of damaging financial statements can cast a long shadow over the finance department, CFOs increasingly appreciate that the legal department can be a source of hidden value— generating cash that can be reinvested in the business. Below, I explore what recent research reveals about where CFOs see opportunity in the legal department.

CFOs recognize the potential to create value through the legal department

The majority of CFOs believe cost containment should be a top priority for legal departments. However, a staggering 70% of CFOs also express the need for legal departments to focus on finding new ways to recover value. This indicates a significant desire among CFOs to reframe the legal department from a cost center to a capital source.

This sentiment aligns with the growing trend of formal affirmative recovery programs in many companies. An affirmative recovery program is simply an organized effort by the legal department to recover money from meritorious claims and judgments that would otherwise be lost if the business’s meritorious claims and judgments were left unpursued, and to do so in a systematic, numbers-driven way. These programs aim to identify and pursue litigation and arbitration claims that can generate real monetary recoveries for the company.

Recent research shows that over half of businesses either have an affirmative recovery program in place or are developing one. However, only 21% of in-house lawyers and 16% of finance professionals perceive their organization’s recovery programs as robust. If only one in six CFOs thinks the business’s recovery program is operating at the level needed, that highlights the need for increased attention—and increased involvement by finance leaders.

CFOs acknowledge the value of minimizing cost and risk—and a viable solution

CFOs are increasingly considering alternative funding options for litigation instead of using their own working capital. This is because dedicating resources to litigation and arbitration claims comes with significant risks. Disputes are unpredictable, and CFOs have limited information about their potential outcomes. As a result, CFOs have valid concerns about spending working capital on disputes. These concerns include the high cost of litigation, the risk of prolonged case durations and the opportunity cost of allocating funds away from other business areas like R&D or marketing. To address these challenges, CFOs can reframe litigation as an asset and find ways to mitigate these risks.

Legal finance through the lens of a CFO

According to research, CFOs in particular advocate for innovative solutions like legal finance—which is clearly embraced beyond the legal department as a tool with broad corporate benefits.

Legal finance is the practice of valuing and monetizing legal assets, most often in the form of providing capital to finance meritorious claims to accelerate the expected value of claims, judgments and awards. Some of the most common legal finance solutions are:

• Fees and expenses financing: Legal finance arrangement in which a company shifts to a third party the cost of paying fees and expenses to pursue high value litigation and arbitration claims.

• Monetization: Legal finance arrangement in which a third party accelerates a portion of the expected entitlement of a pending claim, judgment or award, providing the claimant with immediate liquidity, often with a continuing back-end participation for the claimant company.

• Portfolio finance: Legal finance capital facility backed by multiple litigation and/or arbitration matters, which may include claims and defense matters and a mix of dispute types and sizes. Portfolios may be created to provide a pool of capital backed by existing and/or future matters and may offer lower financing costs because risk is diversified.

• Asset recovery: The practice of enforcing and collecting outstanding judgments and awards when the losing side fails to pay, which may be financed on a non-recourse basis (i.e., repayment contingent upon successful resolution or recovery).

Finance professionals are champions of the use of legal finance within their organizations, with nearly half of CFOs (45%) saying they expect legal finance to become commonplace for businesses like theirs in the next 15 years. What’s more, CFOs are consistently slightly more likely to predict increased use legal finance tools than their legal counterparts, suggesting that finance has a big role to play in the conversation about funding.

Research shows that CFOs are interested in exploring the potential value of their legal assets, especially as litigation costs are expected to increase. And since CFOs may have concerns about dedicating financial resources to litigation, legal finance offers innovative solutions to transform litigation into an asset by removing financial risk.

Jordan Licht CFO

Burford Capital

Ronen Assia Managing Partner, Team8

Fraud Prevention: Rethinking the Evolving Landscape

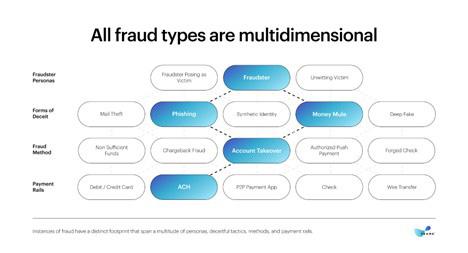

As fraud continues to transform and expand, it’s important to understand the various typologies and methods used by fraudsters. Without this knowledge, identifying your vulnerabilities or maximizing ROI on fraud prevention efforts becomes nearly impossible. Fraud is no longer just a nuisance; it has become a significant economic threat with losses estimated to exceed $250 billion by 2031. The need for a revolutionary approach in fraud prevention is clear. Rapid development of Generative AI technologies promises immense potential but also poses new risks, necessitating a shift in the strategies we must deploy.

Fraud can no longer be viewed as a simple, isolated event that fits neatly into categories like ACH fraud or synthetic identity fraud. Instead, it should be understood as a series of actions fraudsters meticulously plan, investing time (and often money) to ultimately steal funds. To accurately define any instance of fraud, you must first identify the payment rail (e.g., ACH, card), the tactics employed by the fraudster (e.g., phishing, stolen identity), and the method by which money was stolen (e.g, chargebacks, authorized push payment).

All Fraud Types are Multidimensional Final (1)

With these typologies in place, each fraud incident can be analyzed as a sequence of actions that collectively enabled the fraudulent transaction, helping professionals to better communicate about various types. For example, you can talk about what portion of fraud was executed on ACH versus credit card versus check, or which forms of deceit –such as synthetic IDs, phishing, or deep fakes – were employed.

Our current understanding of fraud is often too narrow to effectively capture the multifaceted tactics employed by modern fraudsters. A more granular approach can provide clearer insights:

• Integrated Fraud Typologies: Breaking down fraud into specific actions, payment methods, and execution strategies helps in understanding the entire lifecycle of fraudulent activities.

• Examples and Case Studies: Detailed case studies can illustrate how different types of fraud, such as synthetic identity fraud or firstparty fraud, are interconnected across various payment rails and actions.

Fraud needs to be tackled in a holistic manner. When someone uses phishing to steal an identity, opens a checking account, and then executes a series of transactions with insufficient funds, is that ACH fraud, phishing, or stolen identity? It’s all three. Fraud can involve synthetic identities to exploit ACH or credit card networks. In reality, an incident can simultaneously be first party fraud and card fraud; or both synthetic identity fraud and ACH fraud. Money mules, meanwhile, aren’t a distinct type of fraud but a tactic fraudsters use, often in combination with other methods, to move illicit funds out of the system.

Financial platforms need to consider the impact that technological advancements have on fraudulent activity and consider using vendors that are focused on specific fraud scenarios, rather than continue to rely on generic “payment fraud” solutions and hope for the best. Some of these technological advancement include:

• Hyper-Personalized Phishing: AI technologies are now able to craft phishing emails that are incredibly personalized, making them difficult to distinguish from legitimate communications.

• Advanced Document Forgery: The use of deep learning to create forged documents and IDs is alarming, as these often bypass conventional detection systems.

• Synthetic Media Threats: AI-generated audio and video clips can impersonate public figures or loved ones to manipulate victims, presenting a formidable challenge to existing security measures.

Building a Resilient Framework for Fraud Detection

While cyber and fraud may differ in business considerations, they are similar in how cyber criminals and financial criminals search for vulnerabilities in defense layers. It’s not just about leveraging the same technology but also adopting the same mindset.

On a practical level, a deep understanding of fraudsters’ technology stack – from devices and emulators to accounts and identities – positions you to identify the right fraud signals and reduce fraud more efficiently.

Adopting a multi-layered security approach that continuously learns and adapts to new fraud patterns is essential to defend against the dynamic nature of fraud. For maximum impact, fraud prevention systems need to be fully integrated and holistically applied across various scenarios including::

• Comprehensive Onboarding Checks: Enhanced due diligence during the customer onboarding process to prevent synthetic identity fraud.

• Advanced Authentication Measures: Implementing multi-factor authentication and biometric verification to fortify access controls.

• Enhanced Transaction Monitoring: Monitoring systems must be fully integrated with onboarding and authentication systems to properly identify fraud patterns that start well before the transaction itself.

A Need for Collective Action

Advancements in technology will likely make fraudsters more brazen, persistent, and unfortunately, more successful – unless technology rises to the challenge. The fintech industry has the power to deliver a new generation of fraud tools that can evolve just as rapidly. Developing a more robust language around fraud typology will empower fintechs and their future customers to cut through the noise and effectively combat fraud.

Digital experience strategy: Capitalizing on the $84 trillion wealth transfer

It’s being called the greatest transfer of generational wealth in the history of the world. According to the NY Times, over the next decade, Baby Boomers will pass along $16 trillion to their Gen X, Millennials, and Gen Z heirs, a jaw-dropping $84 trillion total by 2045. When it comes to family wealth, there’s never been an inheritance like it, and while a boon for the wealth management industry, it’s an opportunity that comes with significant challenges.

First, the industry will have to shift its focus and adapt to the needs of younger generations. With different investment priorities, they’ll be seeking products that differ from those of their predecessors. Equally important are the digital experiences they’ll be expecting if you want to win their business.

Future experiences

To capitalize on this once-in-a-generation opportunity, wealth management firms must adopt a modern digital strategy that is simple and intuitive for advisors to use. Younger investors value efficiency and ease of use, so they’ll seek those capable of providing multiple services fast and accurately. Further, they’ll expect every interaction to be informative and provide a better understanding of what’s happening with their investments.

Finally, any digital strategy needs to scale, because not only is the amount of wealth being transferred enormous, Boomers usually have multiple heirs, which increases the potential number of new clients.

Thankfully, well-implemented digital tools can increase productivity while also improving the employee experience (EX) for advisors. Additionally, user-friendly, self-service wealth management apps should be available to customers. Younger investors prefer to use apps to explore opportunities and understand investment performance.

Building a digital experience strategy with apps

Now is the time for wealth management firms to create a digital experience strategy that will enable them to compete for new business and capitalize on this massive generational wealth transfer. Here are the main points to consider when embarking on a digital strategy to accomplish this:

• Conduct customer research: Understand what heirs expect from their wealth management experiences. For example, maybe you have a lucrative subset of Generation X who requires more personal relationships with advisors based on formal and informal meetings. Conduct “voice of the customer” research on a regular basis to keep pace with trends and changing customer desires.

• Determine strategy and plan: Map out your goals and tie them to your strategy. For instance, is your emphasis going to be on winning new clients or serving the ones you have at a deeper level? Plan this out based on your customer research data. Expect the solutions you need, for both customers and personnel, to be overwhelmingly, if not entirely, digital from the outset.

The future is all about the overall digital experience, and apps are how the industry and customers will get there.

• Constantly improve: Create a list of improvements to be made based on feedback that grows and evolves with time. Build in listening posts to regularly check in on what customers are experiencing. This can support a trial-and-error approach that’ll identify gaps and enable resolution of issues.

• Design and develop: You’ll need to employ a DesignOps framework with processes and measures that support the development of scalable solutions. You’ll also need a process to optimize development—most likely DevOps or a similar agile framework—and one to manage how these teams will collaborate. While you may be a wealth management firm, you’ll need to think like a product team.

• Determine resources: Get a handle on what design and development resources are going to be required. Do you have internal developers and designers to achieve your goals? Do you need to look outside the firm? Determine the resources you’ll need and how you’ll get them.

• Be consistent and easy: Employees are critical to customer satisfaction, so listen to their voices as well, particularly front-line advisors. Can you streamline their workflows? Determine what processes cause the biggest pain. Advisors are often working with different tools to manage each financial product, and these are typically not well integrated, nor are their user interfaces consistent with one another. Enabling advisors with consistent, integrated tools can go a long way toward helping them provide clients with the best possible product mix to meet their financial goals.

Joe Scheffler Director of Client Engagement, Think Company

Joe Scheffler is Director of Client Engagement at Think Company, a consultancy that designs and builds worldclass digital experiences for enterprise organizations.

• Consider ethical and compliant AI: Artificial intelligence can drive greater efficiency and deliver a scalable online experience similar to working with a human. Harness the technology, but be sure there are “guardrails” in place to prevent generative AI from including incorrect or noncompliant information.

Ready for the transfer?

This transfer of wealth is a huge opportunity for wealth management firms. Delivering the digital experiences younger generations expect presents considerable challenges, but the potential rewards are staggering. What’s more, this will change how the industry operates, so those who don’t adapt will be left behind.

Navigating the complexities of internal client money reconciliations

The strength of any financial organisation hinges on its ability to manage data effectively. In the financial services sector, where data permeates every facet of business operations, efficient data management is crucial for maximising value and minimising operational costs.

Reconciliations are a fundamental control mechanism for finance and accounting. Organisations that fail to modernise their reconciliation process risk overwhelming their finance and operations teams with cumbersome manual tasks and data overload. As UK regulators adopt a more data-centric approach, effective data management has become essential for compliance. For many firms, the internal client money reconciliation (ICMR) is one of the most complex elements of CASS 7 and is often the source of breach and audit issues.

Navigating CASS 7 and the ICMR

The Financial Conduct Authority’s (FCA) CASS 7 rules apply to investment businesses, involving asset managers, wealth managers, stockbrokers, and investment platforms. These rules govern the handling of client money – funds held by investment firms in connection with regulated investment activities. CASS 7 imposes strict requirements that firms must follow, ensuring that client money is managed safely and compliantly.

However, compliance with CASS 7 is widely recognised as a costly aspect of doing business and one with material regulatory scrutiny; for example, firms must complete a Client Money and Assets Return (CMAR) to the FCA on a monthly basis and undergo an annual external audit. One often overlooked aspect of CASS 7 compliance is reconciliations. Firms must perform ICMR daily, following FCA-defined methods and using only the correct data sources. Businesses should be able to distinguish between money held for each client and be able to distinguish client money from its own money. But, due to the manual nature of many reconciliations, firms often do not have the time or resources to investigate the root cause of reoccurring discrepancies.

Key challenges in data management

The calculations required for ICMR involve vast amounts of internal data. Managing financial data is complex due to a variety of data sources and formats, including transactions, market updates, regulatory reports, and client information. Integrating these disparate data streams into a cohesive system is a significant challenge, and without a unified approach, organisations risk dealing with information that is fragmented and inconsistent.

Beyond achieving correct ICMR results, auditors are interested in how firms arrive at these figures. This requires not only precise calculations but also a transparent process. Data transparency is critical, especially when demonstrating the robustness of the reconciliation process during audits. However, maintaining such transparency is challenging when dealing with siloed data across different systems, which can cause discrepancies and undermine both decision-making and operational effectiveness.

Access to detailed, reliable data and the ability to repeat processes accurately are crucial for maintaining consistency. Flexible systems that seamlessly integrate new data sources and standards are necessary to adapt to regulatory changes.

However, more than nine in 10 asset managers acknowledged a significant reliance on manual processes for reconciliation procedures, despite the increasing complexity of regulatory requirements. Historically, tools such as Excel were sufficient for reconciliations, but the evolving regulatory landscape now demands more advanced solutions.

Murray Campbell Product Manager AutoRek

It’s also important to remember that spreadsheets, while familiar, are often inefficient, prone to human error, and lack the robust audit trails necessary for compliance. The reliance on such outdated methods complicates compliance efforts, as the data management requirements of CASS 7 far exceed the capabilities of manual processes.

However, addressing these challenges is not without a cost. Firms need to invest heavily in people, controls, systems, and processes to meet the stringent demands of regulatory rules such as CASS 7. This investment is a required cost of doing business, necessitated by the complex and multifaceted demands placed on financial institutions.

Enhancing transparency through unified systems

A unified approach to data is crucial for managing ICMR effectively. Defining sources is essential to ensure compliance. A unified data system captures full end-to-end transactional data throughout the client life cycle, including client-level records and client money adjustment values. This approach ensures that the data used in the ICMR is accurate, comprehensive and consistent.

Data silos often obstruct this clarity, making it challenging to achieve a transparent view of financial information. A unified system enhances transparency by providing a holistic perspective on financial information, thereby supporting strategic decisions and improving overall performance by mitigating the inefficiencies associated with siloed data management.

The need for technological investment

High-quality data is fundamental to effective financial management. Investing in technologies that facilitate data validation helps guarantee the accuracy and integrity of the information, leading to more reliable reconciliations and better compliance with regulatory requirements.

Automating the ICMR process is critical for organisations aiming to enhance accuracy, efficiency and compliance. By automating repetitive tasks like data entry, reconciliation, and reporting, organisations can significantly reduce the risk of human error, leading to more accurate and reliable financial records. Moreover, automation leads to improved operational efficiency, allowing for issues to be identified and resolved quickly, freeing up resources for more strategic tasks. Automated review and approval processes further enhance efficiency, while generating management information (MI) and reports with greater speed and accuracy.

In today’s fast-paced, data-driven environment, embracing technology—such as automation, data integration, and improved data quality—is essential for overcoming the challenges of managing ICMR and adhering to CASS 7 requirements. By investing in advanced technology, organisations can achieve cost savings and enhance their ability to adapt to a rapidly evolving financial landscape.

The top three barriers to cloud-based software

Many organisations are assessing cloud-based software options, as the financial services industry strives for stable, inclusive services and growth. Remote applications and infrastructures are, of course, not new, but as the economy becomes increasingly turbulent and unpredictable, new operating methods are being considered across all parts of the organisation.

Chris Beard

Solution Sales Director – Europe, Diebold Nixdorf

Simply keeping pace with today’s market demands is a huge challenge, and many are looking towards technology as an enabler to shift towards a more agile model. Creating scalable processes that will facilitate a more flexible and transparent way of working now and laying the foundation for the future, are rising on the list of strategic priorities.

Many financial institutions are embracing cloud-based software as part of this revaluation of operating models and technology stacks. Research shows that the percentage of workloads that have moved to the cloud has doubled recently, highlighting that the movement is gaining momentum. On the flip side, some organisations are struggling to leap ahead, hesitating to follow the market. Let us consider the three main barriers to pushing the green light to go.

Tackling organisation change

Any type of organisational change can be daunting. Often built on complex staffing infrastructures that have evolved and morphed over time, implementing significant operational transformation can pose challenges for financial institutions. On the flip side, newcomers to the market and those early adopter organisations are setting new heights for competition in the industry. Those already embracing cloud-based operations and next-generation software are elevating consumer expectations and setting standards that need to be followed to remain competitive and profitable.

As with all change, engaging the workplace and involving all teams is the secret to success. Agile software can promote the upskilling of staff, allowing teams to be empowered by new technology and enabling them to better meet customer needs. Embracing and applying the data streams from more intelligent software can also provide staff with greater insights and the most relevant information to complete their daily tasks more effectively.

Ultimately, it is about creating a culture open to embracing innovation. Meaningful, strategically aligned and wellcommunicated changes can be the make or break to success and profitability in such a rapidly evolving market.

The weight of legacy infrastructures

It is well known within the financial services industry that legacy infrastructures can pose significant barriers to implementing technological change quickly and effectively. However, with the pace of change showing no signs of slowing down, prioritising agility is key to moving an organisation forward.

With shifts in innovation and focus over recent years, we have seen layer upon layer of software stacks that now need simplifying. Most systems are old and take time, effort and resources to keep them active. This may require some heavy lifting in the first instance, but once a flexible and adaptable platform has been achieved, both the short and long-term benefits can be powerful. The ability to implement new distribution models and meet customers where they are provides significant competitive advantage.

Cloud-based software also creates an opportunity to increase transparency across the business and value chain. The pure action of simplifying processes and systems delivers advantages on many levels. In addition to decreasing cost barriers for future innovation, the ability to create scalability and be responsive in an unpredictable economy is materially valuable for any organisation. Agile remote applications can create newer, simpler ways to process and share information through a service-based architecture, alongside low code technology, which allows functionality to be added quickly in response to customer needs.

The path of least resistance

Risk aversion can often be part of the mix when organisations hesitate to move towards cloud-based software. Maintaining the status quo can often seem like the safest option when this is coupled with a complex legacy infrastructure. To manage this, many organisations have taken a phased, building block approach to reduce risk. With this course of action, innovations can be added step by step, updating processes channel by channel.

Moreover, moving forward with cloud-native software can actually help manage risk across the organisation. Firstly, creating simple and sustainable platforms which are future proofed can serve as a strong foundation for a resilient and flexible organisation. Additionally, adhering to regulation and industry compliance is often streamlined, with a simplified software approach that can roll up changes quickly and effectively when needed.

In summary, taking a tech-powered industry approach to cloud-based software is a clear driver for future success. Enabling real-time digital customer experiences, increasing transparency across the organisation, and building reliability and resiliency into infrastructures are truly allowing organisations to build value from software.

Allowing core software to keep pace with the demands of today’s market also drives revenue growth and profitability, alongside the reduction of costs. In an industry and economy that is constantly increasing in complexity, striving for simplicity and agility within our operational models will be a key differentiator for the future.

The AI Act: what impact will Artificial Intelligence really have on B2B payments?

Visit any social media newsfeed and countless posts will tell you that AI means “nothing will ever be the same again” or even that “you’re doing AI wrong”. The sheer volume of hyperbolic opinions being pushed out makes it almost impossible for businesses to decipher between the hype and reality.

This is an issue the European Union’s ‘AI Act’ (the Act), which came into force on 1 August 2024, aims to address. The Act is the world’s first regulation on artificial intelligence, setting out how to govern the deployment and use of AI systems. The Act recognises the transformative potential AI can have for financial services, while also acknowledging its limitations and risks.

Within the ongoing debate about AI in financial services, B2B payment processes have been identified as an area where AI has huge potential to accelerate digital innovation. Today, I will do my best to go beyond the hype to provide a true perspective on what AI really means for B2B payments specifically.

Understanding what artificial intelligence is, and what it isn’t

In a nutshell, AI is a system or systems that can perform tasks that normally require human intelligence. It incorporates machine learning (ML), which has been used by developers for years to give computers the ability to learn without being explicitly programmed. In other words, the system can look at data and analyse it to refine functions and outcomes.

A newer part of this is ‘deep learning’, which leverages multilayered neural networks to simulate the complex decision-making power of our brains. The deep learning benefits outlined later in this article are based on Large Language Models (LLM), that are pre-trained on representative data (such as payment/transaction/tender data). Deep learning AI does not just look at and learn patterns of behaviour from the data, it is becoming capable of making informed decisions based on this data.

Before I explore what this could mean for B2B payments, I want to make one caveat clear: human supervision is still needed to ensure the smooth running of operations. AI is a supporting tool, not a single answer to every question. The technology is still maturing, so you cannot hand over the keys to your B2B payments process quite yet. Manual processes will retain their place in B2B payments today, but AI tools will help you learn, adapt and improve more quickly and at scale.

The AI Act – what you need to know

The Act attempts to categorise different AI systems based on potential impact and risk. The two key risk categories include:

1. Unacceptable risk – AI systems deemed a threat to people, which will be banned. This includes systems involved in cognitive behavioural manipulation, social scoring, and real-time biometric identification.

2. High risk – AI systems that negatively affect safety or fundamental rights. High-risk AI systems will undergo rigorous assessment and must adhere to stringent regulatory standards before being put on the market. These high risk systems will be divided into two further categories:

• AI systems that are used in products falling under the EU’s product safety legislation, including toys, aviation, cars, medical devices and lifts.

• AI systems falling into specific areas that will have to be registered in an EU database.

The most widely used form of AI currently, ‘generative AI’ (think ChatGPT, Copilot and Gemini), won’t be classified as high-risk, but will have to comply with transparency requirements and EU copyright law.

High-impact general-purpose AI models that might pose systemic risk, such as GPT-4o, will have to undergo thorough evaluations and any serious incidents would have to be reported to the European Commission.

The Act aims to become fully applicable by May 2026, following consultations, amendments and the creation of ‘oversight agencies’ in each EU member state. Though, as early as November, the EU will start banning ‘unacceptable risk’ AI systems and by February 2025 the ‘codes of practise’ will be applied.

So, with the Act in mind, how can AI be used in a risk-free manner to optimise B2B payments?

AI will transform payment data analysis

Today’s B2B payment platforms are not one-size-fits-all solutions; instead, they provide a toolkit for businesses to customise their payment interactions.

AI-based language models and machine learning can be used by payment providers to rapidly understand and interpret the extensive data they have access to (such as invoices or receipts). By doing this, we gain insights into trends, buyer behaviour, risk analysis and anomaly detection. Without AI, this is a manual, time consuming task.

One tangible benefit of this data analysis for businesses comes from combining the extensive payment data available, with knowledge of a wide range of vendors’ skills, products and/or services. AI could then, for example, identify when an existing supplier is able to supply something that is currently being sourced elsewhere. By using one supplier for both products/services, the business saves through economies of scale.

Another benefit of data analysis comes from payment technology experts. Ours have been training one service to extract data from a purchase order or invoice, to flow level 3 data, which is tax evident in some territories. This automatically provides the buyer with more details of the transaction, including relevant tax information, invoice number, cost centre, and a breakdown of the products or service supplied. This makes it easy and straightforward to manage tax reporting and remittance, purchase control and reconciliation.

AI-driven data analysis isn’t just a time and moneysaver, however. It also adds new value by enabling providers to use the data to create hyper-personalised payment experiences for each buyer or supplier. For example, AI and ML tools could look out for buying and selling opportunities, and perform a ‘matchmaking supplier enablement service’ that recommends the best payment methods – and the best rates – for different accounts or transactions. The more personalised a payment experience is, the happier the buyer and more likely they are to (re)purchase.

Efficient data flows mean stronger cash flows

Another practical application of AI is to help optimise cash management for buyers. This is done by using the data to determine who is strategically important and when to pay them. It could even recommend grouping certain invoices together for the same supplier, consolidating them into one payment per supplier, reducing interchange fees and driving down the cost of card acceptance.

AI can also perform predictive analysis for cash flow management, rapidly analysing historical payment data to predict cash flow trends, allowing businesses to anticipate and address potential challenges proactively. This is particularly valuable in the current economic climate where cashflow is utterly vital.

By extracting value-added, tax evident data from a purchase order or invoice, AI can rapidly analyse invoices and receipts to enable efficient, accurate automation of the VAT reclaims process. Imagine: the time comes for your finance team to reclaim VAT on recent invoices and receipts, but they don’t have to manually go through every receipt or invoices and categorise them into a reclaim pile or not reclaimable. It sounds like a dream but it will be the reality for business everywhere: AI does the heavy lifting and humans verify it, saving significant time and resources.

Quicker, more accurate invoice reconciliation

The third significant benefit of AI is automated invoice reconciliation. By identifying key information from an invoice and recognising regular payees, AI can streamline and automate the review process. This has the potential to significantly speed up transactions and enable more efficient payment orchestration.

Binding together all supporting paperwork, such as shipping, customs, routes, and JIT (just-in-time) requirements can also be done by AI, and it’s likely to be less prone to human error.

This provides an amazing opportunity to make B2B payments faster, reduce costs and increase efficiency. Businesses know this: 44% of mid-sized firms anticipate cost savings and enhanced cash flow as a direct result of implementing further automation within the next three years. According to American Express, 48% of mid-sized firms expect to see payment processes accelerate, with more reliable payments and a broader range of payment options emerging.

When. Not if.

There are significant opportunities to leverage AI in B2B payment processes, making it do the heavy lifting. It is, however, essential to view these opportunities with a balanced understanding of the limitations of AI.

While all the opportunities for AI in B2B payments outlined today are based on relatively low-risk AI systems, human oversight of these systems is still essential. Having said this, with all the freed-up time and resource achieved through the implementation of AI, this issue can be avoided.

AI in B2B payments is not an if, but a when. The question is, when will you make the jump, hand in hand with technology, rather than either fearing it or passing full control over to it.

In order to grow, it is essential for users to see the tangible benefits. For example, by enhancing efficiencies in account payable (AP), businesses can reallocate time and resource previously spent in AP to other areas of the business. Early adopters are starting to test the water but only time will tell how much of an impact AI will make.

Most businesses will likely wait for the early adopters to fail, learn and progress. As we know, if something goes wrong in B2B payments, it can have a huge impact on individuals, businesses and economises. Only when the risk is clearly defined and manageable will AI truly become the gamechanger in B2B payments that all the adverts claim.

Pat Bermingham CEO of B2B digital payment specialist, Adflex

How the Proposed U.S. “Protecting Consumers from Payment Scams Act” Could Impact Financial Institutions’

Fraud Prevention Efforts

As digital payment platforms continue to evolve, so do the fraudsters. The traditional protections under the U.S. 1978 Electronic Fund Transfer Act (EFTA), designed primarily for unauthorized transfers, are proving insufficient in the face of deception and social engineering.

Addressing this insufficiency, the proposed Protecting Consumers from Payment Scams Act, introduced jointly on August 2, 2024, by the House of Representatives and the Senate presents its own roadmap which addresses the EFTA’s critical oversight by ensuring that fraudulently induced transfers receive the same level of protection as unauthorized transactions. This act highlights the urgent need to strengthen consumer protections in the face of rising digital payment fraud, building on existing laws to adapt to the complexities of modern financial scams.

Fraudsters are increasingly resorting to authorized fraud, with growing focus on investment and romance scams. NICE Actimize’s 2024 Fraud Insights report found that while the overall fraud value decreased by 26%, authorized fraud increased by 11%. Furthermore, NICE Actimize industry data shows a significant shift in domestic wire payments related to scams: a 44% increase in investment scams by value and 17% by volume and increases of 133% in romance scams by value and 50% by volume, away from purchase and impersonation fraud. These fraud typologies are often of higher value which results in increasing losses.

Key Amendments to the Electronic Fund Transfer Act

The U.S. Protecting Consumers from Payment Scams Act introduces several significant amendments to the EFTA aimed at enhancing consumer protections and ensuring greater accountability among financial institutions. These include:

• Expanded Definitions - The act broadens the definition of "unauthorized electronic fund transfers" to include transactions where a consumer’s authorization was obtained through fraud. This expansion is crucial as it extends protections to consumers misled into authorizing a payment, ensuring they are not left to bear the financial burden.

• Shared Liability - One of the most significant changes introduced by the act is the concept of shared liability. Under this provision, the financial institution holding the consumer’s account and the institution receiving the fraudulent transfer share responsibility for reimbursing the consumer. This encourages all parties involved to adopt more robust fraud prevention measures.

• Enhanced Error Resolution - The act expands the EFTA definition of an "error" to now include mistakes made by consumers due to fraudulent inducement. This ensures consumers who mistakenly authorize a fraudulent transaction due to deception can seek resolution and recover their funds through established channels.

• Regulatory Oversight - The act grants the U.S. Consumer Financial Protection Bureau (CFPB) the authority to issue new rules necessary to enforce these provisions. This includes setting guidelines for shared liability and ensuring that the protections adapt as fraud tactics continue to evolve.

By Anurag Mohapatra, NICE Actimize, SME and Sr. Product Manager

Implications for Financial Institutions

The Protecting Consumers from Payment Scams Act introduces several new responsibilities for financial institutions, which will have significant operational and legal implications.

Operational Adjustments and Compliance

Requirements: Financial institutions will need to make significant adjustments to comply with the new shared liability provisions introduced by the act. This includes enhancing fraud detection and prevention mechanisms, improving customer verification processes, and ensuring robust dispute resolution systems are in place.

One critical area of focus will be the detection and monitoring of money mules—individuals who transfer illegally acquired funds on behalf of criminals. Financial institutions that fail to stop mules moving funds through their institutions could be found liable for those transactions. This risk drives the need for incoming transaction monitoring, in addition to outgoing transaction monitoring commonly done today.

Institutions may also need to invest in staff training and system upgrades to meet the act’s requirements, ensuring that all aspects of transaction monitoring and fraud prevention are effectively addressed.

Legal and Financial Risks: The introduction of shared liability increases financial institutions' legal and financial risks. Banks and payment service providers must now take even greater care in processing transactions, knowing they may bear financial responsibility for fraudulently induced transfers. Failure to comply with the act could result in regulatory penalties and reputational damage.

Strategic Partnerships and Collaboration: To mitigate these risks effectively, financial institutions may need to collaborate more closely with other stakeholders, including telecommunications companies, counterparty banks, and digital platforms. This is particularly relevant as many scams originate on social media platforms and over the phone, making it crucial for all sectors involved in digital communication and transactions to collaborate in preventing and mitigating scam activities. Cross-sector partnerships can enhance information sharing and enable more coordinated responses to emerging fraud threats and improve claims management.

U.S. Consumer Protection Legislation vs. Global Counterparts

When evaluating the effectiveness of different regulatory frameworks for combating payment scams, four key aspects stand out: Sector-specific obligations, liability for banks, enforcement and penalties, and information sharing. These aspects are critical because they collectively represent the essential components of a robust regulatory framework that ensures comprehensive consumer protection against scams.

• Sector-specific obligations - This aspect evaluates whether the regulatory framework imposes tailored obligations on different sectors (e.g., banks, telecoms, digital platforms) involved in payment processing.

• Liability for banks - This aspect looks at how the framework assigns liability to banks for fraudulent transactions and the extent of their responsibility to reimburse consumers.

• Enforcement and penalties - This aspect assesses the enforcement mechanisms in place and the penalties for non-compliance with the regulatory requirements.

• Information sharing - This aspect reviews the framework’s requirements for sharing information about scams between institutions and across sectors.

Aspect

Regulatory Overview

U.S. Protecting Consumers from Payment Scams Act

Amends EFTA to address fraudulently induced transfers with shared liability.

Sector-Specific Obligations

Liability for Banks

Information Sharing Enforcement and Penalties

No sector-specific obligations

Shared liability between financial institutions for losses due to scams.

CFPB oversees enforcement, but there is room to enhance multisector oversight

Encourages cooperation but lacks mandatory information-sharing protocols.

Australia’s Proposed Scams – Mandatory Industry Codes

A comprehensive, whole-ofecosystem approach with mandatory scam codes across multiple sectors.

Distinct codes for banks, telecoms, and digital platforms with adaptable implementation strategies.

Does not explicitly modify liability for banks

Strong enforcement with oversight by multiple regulators and significant penalties for noncompliance.

Mandatory information sharing across sectors, coordinated by the National Anti-Scam Centre (NASC).

UK Payment Systems Regulator (PSR)

Comprehensive protections with mandatory reimbursement for APP fraud.

Sector-specific charters for banks and telecoms with voluntary commitments.

Sending and receiving banks share responsibility for reimbursing consumers.

PSR enforces mandatory reimbursement, with penalties for non-compliance.

Information sharing is part of voluntary charters, focusing on fraud detection.

Singapore’s Shared Responsibility Model

Emphasizes shared responsibility across financial and telecommunications sectors.

Obligations for both banks and telecoms, with a tiered approach to liability.

Banks are the first line of liability, followed by telecoms if banks meet their obligations.

MAS enforces compliance, with penalties tied to meeting obligations under the framework.

Mandatory sharing of scam-related data between financial institutions and telecoms.

The comparative analysis reveals that the U.S. Protecting Consumers from Payment Scams Act aligns closely with the UK's Payment Systems Regulator (PSR) by emphasizing shared liability and consumer reimbursement for fraudulently induced transfers.

However, the U.S. Act does not include the cross-sector provisions seen in other jurisdictions. Australia’s proposed Scams – Mandatory Industry Codes provide an example of how robust scam controls can be implemented without altering existing liability rules for banks. Instead, it mandates improvements in systems, such as payee verification and enhanced transaction controls, to prevent scams. This approach focuses on proactive prevention and disruption across sectors, ensuring that each industry plays a role in combating fraud.

Meanwhile, Singapore’s Shared Responsibility Model also highlights the importance of cross-sector controls involving financial institutions and telecommunications providers. This is particularly relevant as many scams originate on social media platforms, making collaboration crucial in preventing and mitigating scam activities.

Strengthening Against Scams

Financial institutions can take steps to protect their customers from scams that impact the bottom line, regardless of whether the proposed legislation is signed into law by U.S. Congress. These include using additional external intelligence resources to ascertain beneficiary risk, target first-party fraud, and aid in authorized fraud detection. Other options include creating multiple risk profiles to aid models and rules, including beneficiary and institution risk and the payer and payers' institution risk. as well as putting in place separate machine learning (ML) models and scoring for ATO and authorized fraud.

There are also a number of strategic and industry-facing steps that an organization can utilize. First, an FI can participate in an industry information sharing or collective intelligence initiatives that provides holistic insights beyond what the individual FI could see independently. An organization should also create strategies or policies that address each specific fraud type, such as setting up distinct step-up authentication for ATO and scams. Another approach is to use distinct processes for fraud investigations that detect first-party authorized claims and manage cases and refunds within regulatory timescales where regulated. Last, it's crucial to improve reporting capabilities to better measure scams separately from unauthorized fraud and claims fraud rates, empowering you with better control and insights.

Should the legislation pass, financial institutions should also consider the implications of liability shifts on their fraud detection program. Money mules, which previously had little financial impact on your institution, could significantly contribute to your overall fraud losses with mandatory reimbursements to counterparty institutions. When strengthening money mule detection, one key place to start is setting up fraud monitoring on incoming transactions.

Don’t Wait to Start

The proposed legislation is expected to take some time to pass through the U.S. House and Senate. During that timeframe, the contents of the act could be modified. Financial institutions shouldn’t wait for a passed act to start preparing their program for the potential implications. There are steps they can take today to protect their customers that will reduce scam-related fraud losses, bill or not. To learn about how you can use the latest technology to stop scams and mules, check out NICE Actimize’s Scams and Mule Defense solution.

Anurag

SME and Sr. Product Manager NICE Actimize

Mohapatra

5 Tips for Mid-Market Financial Firms to Adopt Automation Fabrics

The technological demands of financial clients continue to expand. What might have only been possible with the help of a trained advisor can now be accomplished with a few clicks on your phone. This increased efficiency is great for customers but poses difficulties for financial organizations, particularly small to mid-market firms.

Automation fabrics are critical to managing this influx of data and continued need for digital transformation. These tools enable efficient growth by automating manual processes and expanding the productivity of each team member.

However, only 26% of small and medium enterprise (SME) finance companies have fully automated processes in at least one function, compared to 41% of larger organizations, according to McKinsey & Company.

Putting the challenges that face SME finance companies into context will help them understand and navigate the road to implementing helpful automation. From there, utilizing strategic tips will put them on the fast-track to increased productivity and higher frequency releases.

Why Small to Mid-Sized Financial Firms Are Struggling to Adopt Automation Fabrics

Larger financial firms tend to be on the leading edge of adopting new technology and solutions. They can customize them to fit their exact needs, which affords them cutting-edge capabilities and reduces complexities.

One major challenge for smaller companies is that they’re not able to follow a blueprint when integrating new capabilities because they are playing the role of trailblazer. Any new technology is going to have bugs that are worked out as it’s used. And quite often, financial companies are the first ones figuring out how to solve these problems. This period of alignment can be difficult for smaller companies to absorb.

The needs of SME finance companies are at odds with each other: they need to be able to adopt these new technologies but don’t have the resources for large-scale implementations. This means they often need to utilize products that are ready to use right out of the box.

SME finance companies also don’t have the internal resources to customize new applications. Larger companies will have a staff of developers that can create bespoke solutions. These expansive technology departments enable enterprise companies to be more sophisticated in their approach, which is something SME companies can’t match even though they have the same needs. This contributes to their need to rely on off-the-shelf SaaS solutions.

The overarching theme for these difficulties is that SME companies lack the various resources needed to source automated solutions like their enterprise counterparts. There needs to be an initial investment to see the desired results, and SME finance companies often don’t have the capacity to make that investment.

5 Tips to Fully Embrace Automation Fabrics

Small and medium enterprise finance companies can use automation fabrics to expedite services and propel their organizations forward with the following five tips.

1. Solve for Future Problems as Well as Current Problems

SME finance companies must take a macro view of their automation needs. It can be tempting to solve for immediate pain points, but this will only create more work in the future.

Choose an automation provider that aligns itself with your goals down the road as well as the problems you are currently facing. Failing to account for future needs will lead to buying a new product every time a new challenge arises, which increases adoption time and reduces return on investment (ROI).

2. Understand ROI Comes from Multiple Sources

Assessing the amount of money a new tool will save the company is a major consideration for new, automation fabric tools. The immediate factor that decision-makers will focus on is cost reduction. And while this is a great way to make a business case for a new tool, it is not the only factor in the ROI of automation fabric tools.

Automation fabric tools don’t make mistakes. This is a huge differentiator when compared to addressing a problem manually, which saves a company a significant amount of money. Also, organizations gain a competitive advantage when automation fabric tools expedite their product delivery timelines.

These ROI factors must be communicated to justify the initial investment in automation fabric tools.

3. Be Flexible to Maximize Returns

Processes evolve over time, especially when automation fabric tools are introduced. And while it’s tempting to view this as an opportunity to reduce labor costs, SME finance companies often don’t have expendable team members.

Automation fabric tools enable organizations to repurpose their workers and avoid hiring new individuals to meet goals. Avoiding future increases in headcount enables flexible teams to move people around to more complex tasks within a company.

4. Recognize a Difference in Needs

Time to value differs for large and small companies. Larger companies can absorb lengthy, complex implementations of expansive products, while SME companies require faster returns.

Assess your needs and resources to determine how complex your expected returns from automation actually are. The software you choose should match this level of complexity, which will determine the depth of the onboarding process.

5. Find a Platform to Evolve Along with You

At the end of the day, you can either source automation to address a specific task or you can find a solution that will encompass all of your current and future needs. And while the initial investment can be prohibitive, organizations that are able to handle a longer implementation to source an automation platform will see the greatest benefits down the road.

Charles Crouchman Chief Product Officer

Redwood Software

Charles is the Chief Product Officer at Redwood Software, with 25 years of experience as a technology executive. He has held CTO or CPO roles at five software companies, guiding them from startup to global expansion. Specializing in enterprise software sales, infrastructure management, automation, and machine learning, Charles brings a unique perspective to his role. At Redwood, he focuses on creating winning strategies for delivering innovative products and scaling high-performance product management and engineering teams.

Choose a platform that evolves with your needs instead of singular products. Your financial organization aims to grow, and it’s important that your tools grow along with you. This will save money over time by avoiding multiple implementation and learning periods while also providing continuous benefits that your team can rely on.

Automation Fabrics are Available for Finance Companies of All Sizes

The first step might be intimidating but the rewards of automation fabric tools greatly outweigh the initial investment. Reduced errors, expedited release schedules, and increased productivity are benefits that provide exponential returns that continue to expand over time.

Fosun International:

The Hidden Gem Ready to Shine – Co-CEO Chen Qiyu

on Unlocking True Value for Investors

Chinese multinational conglomerate Fosun International Limited is a global innovation-driven consumer group whose mission is “creating happier lives for families worldwide.” Since its inception in 1992, Fosun has accumulated profound technology and innovation capabilities and a significant industrial presence in more than 35 countries and regions worldwide.

Fosun International’s overseas development has been steadily rising in recent years, with its number of overseas employees reaching 48,500 in the first half of 2024, its overseas business accounting for 47% (RMB45.87 billion) of its total revenue, and the 10-year CAGR of overseas revenue reaching 55%.

When Chen Qiyu, Fosun International’s Executive Director and Co-CEO, spoke to Wanda Rich, editor of Global Banking & Finance Review, he provided some insight into how Fosun has achieved this balance between domestic and overseas operations by sharing some successful examples of the company’s globalisation efforts.

“One example is Fosun Pharma, which began its internationalisation journey ten years ago,” he began. “It has now become a leading global integrator of pharmaceutical and healthcare innovation. In the first half of 2024, Fosun Pharma achieved overseas revenue of RMB5.51 billion, representing a year-on-year increase of 15.13%, and accounting for 27.03% of total revenue.”

Regarding global R&D and business development, HANQUYOU, a biologic medical product used in the treatment of breast cancer and self-developed and manufactured by Shanghai Henlius Biotech, Inc., a subsidiary of Fosun Pharma, received marketing approval from the US Food and Drug Administration in 2024. “HANQUYOU has now been approved for marketing in 48 countries and regions, and benefits more than 200,000 patients in China,” Qiyu reported. “In addition, HANLIKANG (approved by the National Medical Products Administration for the treatment of nonHodgkin’s lymphoma, chronic lymphocytic leukaemia, and rheumatoid arthritis) received its first overseas marketing approval in Peru.”

Developments also transpired in terms of Fosun’s cultural outreach, with the Yuyuan Garden Lantern Festival making its overseas debut in Paris, France, and attracting nearly 200,000 local visitors. Regarding global operations, Qiyu revealed a number of key areas that have enjoyed recent growth. “Fosun Insurance Portugal achieved business growth both domestically and internationally in the first half of 2024, with the net profit of international business accounting for over 40%,” he said. “Club Med, a subsidiary of FTG (Fosun Tourism Group), achieved a record-high business volume of RMB8.89 billion in the first half of the year. Its business in the EMEA region and the Americas continued to grow, while its business in the Asia-Pacific region recovered significantly. Furthermore, Easun Technology achieved new overseas orders of RMB3.99 billion in the first half of the year, with orders from the US market more than doubling year-on-year.”

A Long Recognised Champion of Globalisation equipped with Global Operation and Investment Capabilities.

Fosun, a company that has been long recognised as a champion of globalisation, has developed into one of the few in China to be equipped with global operation and investment capabilities. Recent reports from Fosun’s subsidiaries have highlighted that development is currently being pursued in the key focus areas of the Middle East and Southeast Asia. “The globalisation gene has been deeply rooted in all of Fosun’s business segments,” Qiyu confirmed. “We continue to strengthen our marketing capabilities and advance local manufacturing capabilities in Africa and the Middle East. In June 2023, Fosun Pharma established a partnership with the International Finance Corporation to build the integrated Cote d’Ivoire park that encompasses drug R&D, manufacturing, and logistics and distribution, promoting the local production and supply of antimalarial and antibiotic products in Africa.

“In the Middle East, Hainan Mining reached a memorandum of understanding with Ajlan & Bros Mining Company in July 2024 to explore the feasibility of jointly building a lithium salt plant in Saudi Arabia. In May 2024, Club Med, Fosun’s high-end lifestyle brand that offers all-inclusive luxury holidays, announced its entry into the Middle East. Its first resort in the region is scheduled to open in Oman in 2028.”

He added that, looking ahead, Fosun plans to continue strengthening its multidimensional cooperation with partners in the Middle East in industry, projects, and funding. “We believe that, in leveraging Fosun’s extensive experience in globalisation and operational capabilities, along with our deep understanding of the Chinese market, we can connect our Middle East partners with leading global enterprises and products, thereby achieving win-win cooperation across various fields.”

Fosun has adhered to a ‘focused’ strategy in recent years, aiming to develop industry-leading companies in advantageous industries to achieve stable profit growth, while also prioritising its asset-light operation capabilities. Qiyu outlined the business areas the company plans to target for further development in this vein. “We will continue to focus on the four core business segments: Health, Happiness, Wealth, and Intelligent Manufacturing,” he emphasised. “Core companies in these businesses include Fosun Pharma, Yuyuan, Fosun Insurance Portugal and FTG. We hope to quickly establish competitive advantages and build profitability in these segments and companies while increasing our investment in sustainable development. On the one hand, we will continue to pursue globalisation. On the other hand, we will make use of resources for necessary mergers and acquisitions and integrations. We aim to divest from heavy assets and control expansionary investments related to production and operations.

“Fosun’s asset-light operation model has proven to be an effective one. Currently, 85% of Club Med resorts have adopted a leasing and management model, with the proportion of self-owned resorts declining to 15%.”

A continuing element of Fosun’s future strategy will involve reinforcing in-depth cooperation to achieve win-win results by implementing joint ventures that complement all parties’ strengths. “In June 2024, FTG joined hands with the Taicang Municipal Government to build Phase II of the Taicang Alps Resort,” Qiyu revealed. “The project, with a total investment of over RMB5.0 billion, is funded by the Taicang Municipal Government and operated and managed by FTG.

“In addition, in March 2024, Fosun Pharma, Shenzhen Guidance Fund and seven other investors jointly established a RMB5.0 billion biomedical industry fund, exclusively managed by Fosun Pharma’s subsidiary, Shanghai Fujian Equity Investment Fund Management. In April 2024, Fosun Capital, together with Wuhan Innovation Investment and Wuhan Fund, established a RMB3.0 billion industry fund focusing on the four major sectors of next generation information technology, dual carbon, intelligent manufacturing, and consumption.”

Given that Fosun has consistently promoted innovation within the Group and its subsidiaries, Wanda asked Qiyu to share some recent achievements in R&D, product, marketing and digital innovation. “Innovation is a crucial driving force in Fosun’s strategy,” he acknowledged. “In the first half of 2024, Fosun invested approximately RMB3.5 billion in R&D and innovation.

Chen Qiyu, Executive Director & Co-CEO of Fosun International