The information contained in this publication has been obtained from sources the publishers believe to be correct. The publisher wishes to stress that the information contained herein may be subject to varying international, federal, state and/or local laws or regulations.

The purchaser or reader of this publication assumes all responsibility for the use of these materials and information. However, the publisher assumes no responsibility for errors, omissions, or contrary interpretations of the subject matter contained herein no legal liability can be accepted for any errors. No part of this publication may be reproduced without the prior consent of the publisher

editor

Dear Readers’

Welcome to Issue 71 of Global Banking & Finance Review. This issue covers some of the most pressing topics in finance today—payments innovation, retail banking growth, and financial fraud.

In "Five Untapped Opportunities for Payments Change", Chris Beard of Diebold Nixdorf explores key areas shaping the future of payments, including expanding consumer choices, strengthening financial inclusion, and adapting to regulatory demands.(Page 28)

Retail banking plays a critical role in bringing financial services to more people. In "Building Mongolia’s Financial Future", State Bank CEO Gantur Ulzii discusses how the bank is expanding its nationwide branch network, introducing digital banking tools, and ensuring financial access for underserved communities across Mongolia.(Page 24)

At the same time, financial scams are becoming more sophisticated. In "Romance Scams: A Growing Threat and How to Fight Them", Anurag Mohapatra of NICE Actimize reveals how criminal groups are using AI, deepfakes, and social media to defraud victims—and what banks can do to protect consumers. (Page 18)

At Global Banking & Finance Review, we remain committed to providing expert insights on the forces shaping global finance. Whether you're focused on payments, banking accessibility, or fraud prevention, we hope this issue offers valuable perspectives.

Enjoy the journey through our latest issue!

Wanda Rich Editor

Stay caught up on the latest news and trends taking place by signing up for our free email newsletter, reading us online at http://www.globalbankingandfinance.com/ and download our App for the latest digital magazine for free on Google Play and the Apple App Store

Mr. Gantur Ulzii, CEO, State Bank

The Subscription Economy Surge: How Recurring Revenue Models Are Reshaping Global Commerce

The global economy has undergone a structural shift, with the rise of the subscription-based business model fundamentally transforming how companies generate revenue and how consumers access goods and services. Over the past decade, the subscription economy has expanded by 435%, reshaping industries and customer expectations. This growth trajectory is set to continue, with market projections estimating that the subscription economy will reach a valuation of $3 trillion this year.

The Evolution of Subscription Models

Once limited to newspapers and magazines, subscription-based revenue models now permeate nearly every sector, spanning entertainment, technology, e-commerce, and financial services. At the heart of this transformation is a shift in consumer preferences from ownership to access. Companies leveraging subscription models provide ongoing value while securing predictable revenue streams, a particularly attractive proposition in an increasingly volatile economic landscape.

According to recent industry data, 89% of businesses report optimism about the long-term growth of their recurring revenue strategies despite inflationary pressures and macroeconomic uncertainty. This confidence stems from the model's inherent stability, which fosters stronger customer relationships and enables data-driven personalization, ultimately enhancing customer retention and lifetime value.

Changing Consumer Behavior

The proliferation of subscription-based services has driven notable changes in consumer behavior, particularly in how individuals allocate discretionary spending and interact with brands. Research from the Journal of Service Theory and Practice indicates that this shift has not only raised consumer trust but also their expectations, leading to a more optimistic outlook for the future.

1. From Ownership to Access

The preference for access over ownership is particularly pronounced among younger demographics, who prioritize flexibility and convenience over longterm commitments. Streaming services, software subscriptions, and even product-based subscriptions— ranging from fashion rental to automotive leasing—have gained traction as consumers seek more adaptable consumption models.

2. Growing Demand for Personalization

The rise of data-driven decision-making has significantly raised the bar for consumer expectations. Subscription businesses now leverage consumer insights to not just refine offerings, but to optimize pricing strategies and deliver highly personalized recommendations. This level of personalization is not just a feature, but a necessity for enhancing engagement and brand loyalty in the subscription economy.

3. Subscription Fatigue and Budget Constraints

While consumers have embraced recurring payment models, an increasing number report experiencing “subscription fatigue”—a growing reluctance to manage multiple ongoing payments. Research indicates that younger consumers, in particular, are reassessing their subscriptions, weighing necessity against discretionary spending amid rising costs. This trend forces businesses to refine their value propositions and offer greater flexibility, such as tiered pricing and bundled services, to retain subscribers.

Industry Disruption and Growth

The subscription model has redefined business strategies across multiple industries, driving revenue diversification and customer retention in traditionally transactional markets.

Technology & SaaS

The Software-as-a-Service (SaaS) sector has become dominant, replacing conventional licensing models with cloudbased subscriptions. This transition has democratized access to enterprise-grade tools, enabling businesses of all sizes to leverage cutting-edge technology without the burden of significant upfront investment.

Entertainment & Media

Streaming platforms like Netflix and Spotify have revolutionized content consumption, steering the entertainment industry away from ownership-based models. The subscription market’s momentum is expected to continue, with revenue forecast to exceed $996 billion in transaction value by 2028, mainly driven by digital content consumption.

Consumer Goods & E-commerce

Product subscriptions, from curated fashion boxes to grocery delivery services, have gained significant traction. Retailers and brands leverage the model to establish recurring revenue streams while fostering direct-to-consumer relationships. Companies increasingly focus on enhancing subscription flexibility and sustainability as customer expectations evolve to remain competitive.

Challenges and Considerations

Despite the subscription economy’s rapid expansion, companies face several key challenges that could influence long-term viability.

Market Saturation

The surge in subscription-based offerings has resulted in intense competition, making differentiation a growing challenge. Businesses must demonstrate clear value and continually innovate to maintain customer engagement.

Subscription Fatigue & Retention Risks

Research indicates that consumers are experiencing subscription fatigue, particularly in markets with competing services. This fatigue manifests as dissatisfaction, tension, and a desire to simplify subscription commitments. As consumers become more selective about their recurring expenses, businesses must focus on retention strategies. Offering greater flexibility—such as pause options, loyalty perks, and hybrid models combining one-time purchases with subscription benefits—can help mitigate churn.

Data Privacy & Regulation

The increased reliance on customer data to drive personalization raises concerns about privacy and security. Stricter data protection regulations, such as the GDPR and evolving U.S. consumer privacy laws, require businesses to strike a balance between leveraging data-driven insights and maintaining consumer trust.

The Future of the Subscription Economy

As the subscription economy continues to evolve, several key trends are likely to shape its trajectory:

Retention-Focused Strategies: Businesses will shift their focus from aggressive acquisition to long-term retention, prioritizing customer experience and engagement.

AI-Driven Personalization: Advanced analytics and AI will be pivotal in refining customer segmentation and enhancing personalized recommendations, opening up exciting possibilities for the future.

Hybrid Revenue Models: Companies will explore blended approaches, integrating subscriptions with one-time purchases or pay-as-you-go options to appeal to a broader customer base.

Sustainability & Ethical Consumption: As consumers demand greater transparency and accountability, businesses will incorporate sustainability initiatives, such as eco-friendly packaging and ethical sourcing, into their subscription models, fostering a sense of responsibility and commitment to these values.

The Future of Subscription-Based Business Models

The subscription economy is more than a passing trend—it represents a structural shift in how businesses generate revenue and engage with consumers. While the model has driven significant growth across industries, companies must now focus on sustainability, differentiation, and long-term customer value to remain competitive.

In its early stages, subscription-based businesses prioritized rapid customer acquisition, often at the expense of profitability. However, as the market matures, investors and industry leaders are placing greater emphasis on operational efficiency, retention strategies, and lifetime customer value. The next growth phase will require companies to refine their cost structures, optimize pricing models, and minimize churn to build sustainable businesses.

Adapting to changing consumer preferences is a challenge and a critical necessity. As economic conditions shift and discretionary spending becomes more selective, businesses must provide greater flexibility in their offerings. Hybrid models that blend subscriptions with one-time purchases, usage-based billing, or freemium structures are already gaining traction, allowing companies to cater to a broader customer base while maintaining revenue stability. Striking the right balance—offering convenience without overwhelming consumers with excessive subscription commitments-will be the key to success in the subscription economy.

As the subscription economy evolves, technology and AI will play an ever more critical role in its transformation. From hyper-personalized experiences and predictive analytics to AIdriven customer support and churn prevention, businesses that harness data effectively will strengthen their competitive edge. At the same time, as subscription models become more data-

reliant, regulatory compliance and ethical considerations around consumer privacy will become more pressing. Transparency in data collection, clear billing practices, and adherence to evolving privacy laws will be essential in maintaining consumer trust.

Market dynamics are also shifting as competition intensifies. With saturation in key industries—particularly media, entertainment, and software—the subscription economy is entering a consolidation phase. Larger firms are acquiring smaller players to expand their ecosystems, while niche providers differentiate themselves through highly specialized offerings. Strategic partnerships and mergers are likely to shape the next wave of innovation, with companies leveraging economies of scale to enhance value propositions and profitability.

The subscription economy is no longer just about recurring revenue but about creating lasting relationships with consumers through continuous value delivery. Businesses that can navigate market saturation, address consumer fatigue, and integrate technology-driven enhancements will be best positioned for long-term success. As companies refine their strategies, those that remain agile, customer-focused, and financially resilient will set the standard for the next evolution of subscription-based commerce.

The outlook remains promising for investors, but success will require discerning between sustainable models and those reliant on unsustainable growth. The businesses that thrive will combine scalability with financial discipline, demonstrating a clear ability to balance growth with profitability. As the landscape evolves, innovation, adaptability, and consumer-centricity will define the future of the subscription economy.

AI, Big Data, and the Future of Business Insurance

AI and Big Data are having a significant impact on the insurance industry. As insurers seek to improve efficiency, enhance risk assessment, and personalize policies, these technologies are redefining how products are designed, priced, and delivered. This shift goes beyond automation—it's a reinvention of the entire insurance value chain.

Historically, insurers assessed risk and set prices based on actuarial models and past data. Today, real-time inputs from IoT sensors, financial transactions, and behavioral analytics enable them to make faster, more precise decisions. AI-driven underwriting, dynamic pricing models, and automated claims processing are reshaping the industry, offering insurers a competitive edge while improving customer experience.

As insurers navigate emerging risks—from climate change and cyber threats to economic volatility—AIpowered analytics are helping them shift from reactive protection to proactive risk mitigation.

Transforming Risk Assessment and Underwriting

Risk assessment and underwriting have long been fundamental to the insurance industry, providing the foundation for evaluating exposure and determining policy pricing. Traditionally, insurers relied on actuarial models and historical claims data to assess risk, a method

that, while effective in past decades, is increasingly inadequate in today's rapidly evolving business landscape. The rise of artificial intelligence and big data has transformed this process, allowing insurers to shift from a reactive approach to a more dynamic, predictive model that enhances accuracy and efficiency.

AI-powered risk assessment enables insurers to analyze vast amounts of structured and unstructured data, revealing insights that traditional methods often miss. Real-time inputs from IoT devices, cybersecurity monitoring systems, financial transactions, and satellite imagery feed into sophisticated algorithms that identify nuanced risk patterns. These AI-driven processes operate within strict privacy and security frameworks, ensuring that personal and sensitive data remains protected.

This shift allows insurers to refine risk pricing more precisely, ensuring policies are tailored to real-world conditions rather than broad statistical assumptions. Integrating AI into underwriting is particularly impactful in cyber insurance, where policies can adjust dynamically based on a company's security posture, or in commercial property insurance, where predictive climate models and sensor data offer a more comprehensive view of potential hazards.

Rather than replacing human expertise, AI is augmenting the role

of underwriters by automating routine assessments and providing data-driven recommendations that enhance decision-making. Underwriters can now focus on complex, high-value cases, leveraging AI-driven insights to refine risk evaluations while applying human judgment to ethical considerations and client relationships. This collaborative model strengthens underwriting accuracy while increasing operational efficiency, allowing insurers to process policies faster without compromising diligence.

The ability to assess risk dynamically rather than relying on static historical data is reshaping underwriting across industries. In manufacturing and logistics, AIdriven analysis of supply chain disruptions and geopolitical risks is allowing for more responsive insurance products. In financial services, AI is helping insurers evaluate corporate credit risk with real-time economic indicators, providing more adaptive policy terms. Across sectors, the fusion of machine learning and traditional underwriting expertise is creating a new standard for risk assessment— one that is faster, more precise, and better aligned with the complexities of modern business environments.

AI-Driven Personalization and the Rise of Dynamic Pricing

Traditional business insurance, once defined by standardized policies and broad risk classifications, is rapidly becoming obsolete. With advancements in artificial intelligence and big data analytics, insurers can now take a more customized and adaptive approach, tailoring policies to each business's unique risks and operational needs. This shift is transforming how insurers assess risk, determine pricing, and structure coverage, making business insurance more precise and adaptable.

AI-driven personalization allows insurers to evaluate a company's realtime risk profile rather than relying on static actuarial tables. By analyzing data from IoT sensors, cybersecurity monitoring tools, financial transactions, and even employee training programs, insurers can develop policies that reflect the actual risk exposure of a business at any given moment. For instance, commercial property insurers can adjust premiums dynamically based on weather forecasts, building sensor data, and maintenance records, ensuring that businesses pay rates aligned with their risk levels. Similarly, cyber insurance providers can modify policy terms based on a company's cybersecurity posture, factoring in breach attempts, security updates, and overall risk management strategies.

The integration of dynamic pricing models further enhances this transformation. Unlike traditional pricing methods that remain static over the policy term, AI-powered algorithms allow for real-time adjustments, ensuring that businesses are neither overpaying for coverage nor exposed to unforeseen risks. Supply chain insurance, for example, can be adjusted dynamically based on geopolitical events, port congestion, and shipping route disruptions, allowing businesses to maintain adequate protection without unnecessary cost burdens. This capability is particularly valuable in industries where risk factors such as manufacturing, logistics, and financial services fluctuate frequently.

Beyond improving accuracy, AI-powered personalization is also reshaping the

customer experience. Businesses now have access to flexible, usage-based policies that can scale with their evolving needs. This model optimizes risk management and enhances cost efficiency, enabling companies to allocate resources more effectively. By leveraging AI-driven insights, insurers are creating a new era of hyper-personalized business insurance, where coverage is dynamic, data-driven, and closely aligned with real-world risks.

Streamlining Claims Processing and Fraud Detection

Claims processing has historically been one of the most complex and timeconsuming aspects of business insurance. Insurers have long struggled with delays, administrative inefficiencies, and the challenge of distinguishing legitimate claims from fraudulent ones. Integrating artificial intelligence and big data transforms this process, significantly improving speed, accuracy, and fraud detection capabilities.

AI-powered automation is streamlining claims handling by reducing manual intervention and expediting approvals. Machine learning algorithms can analyze claims documentation, damage reports, and third-party verification data in real-time, allowing insurers to process straightforward cases almost instantly. For more complex claims, AI can route cases to the most relevant adjusters, ensuring a faster and more efficient resolution. These advancements enhance operational efficiency and improve customer experience by reducing processing times and minimizing disputes.

Fraud detection is another area where AI is having a profound impact. Advanced predictive analytics software enables insurers to isolate fraudulent claims while simultaneously accelerating the approval process for legitimate ones. By analyzing vast datasets, including past claim histories, financial transactions, and behavioral indicators, AI can detect suspicious patterns with a high degree of accuracy. This approach has already proven successful in the industry, with some insurers identifying and preventing a significant percentage of fraudulent claims, ultimately reducing financial losses and operational delays. These capabilities are particularly valuable in corporate liability claims, workers' compensation cases, and cybersecurity breach claims, where fraudulent activity can result in substantial financial exposure.

Beyond fraud detection, AI also improves risk mitigation by enabling insurers to anticipate claims before they happen. Predictive analytics allow insurers to identify businesses with heightened risk exposure based on real-time data, offering proactive risk management solutions that help prevent losses before they occur. This shift from reactive claims processing to proactive risk prevention redefines the insurance landscape, allowing insurers to operate more precisely while providing businesses with more effective coverage solutions.

The Future of Business Insurance: Emerging Trends in AI and Big Data

Integrating AI and big data into business insurance is still evolving, with several emerging trends shaping the industry's future. As insurers embrace these technologies, new advancements are redefining underwriting, claims management, and risk mitigation. Among the most significant trends are AI transparency and regulation, insurtech disruption, predictive analytics, and the shift toward proactive risk prevention.

One of the most pressing developments in AI-driven insurance is the need for transparency and regulatory compliance. As AI models become

more complex, regulators are increasingly focused on ensuring that algorithmic decision-making remains explainable, unbiased, and compliant with industry standards. Insurers operating in highly regulated sectors such as finance and healthcare must demonstrate that their AI models adhere to ethical and legal guidelines, particularly regarding data privacy and risk assessment. The push for greater AI transparency drives insurers to adopt more interpretable machine learning models and invest in governance frameworks that mitigate algorithmic bias.

At the same time, insurtech firms are reshaping the competitive landscape, leveraging AI to drive efficiency and improve customer engagement. NEXT Insurance and Coalition are among the insurtech firms leveraging artificial intelligence to enhance underwriting and claims processing. NEXT Insurance employs AI-driven automation to streamline underwriting and provide instant quotes for small business owners, incorporating machine learning models such as Z-PROPERTY and Z-FIRE to refine risk assessments. Similarly, Coalition specializes in cyber insurance, using AI-powered security tools and its Active Data Graph to assess cyber risk and offer dynamic policy adjustments.

Another key trend is the reliance on predictive analytics to enhance underwriting and claims management decision-making. AI-powered models

are increasingly used to provide next-bestaction recommendations, guiding underwriters and claims adjusters toward more informed decisions. By 2025, many insurers are expected to integrate AI-driven decision support tools that help optimize coverage terms, pricing structures, and fraud detection efforts.

Perhaps the most transformative shift is the movement from reactive claims management to proactive risk prevention. Instead of simply insuring businesses against losses, AI-driven analytics enable insurers to help companies anticipate and mitigate risks before they escalate. Real-time monitoring of cybersecurity vulnerabilities, supply chain disruptions, and environmental hazards is allowing insurers to offer predictive risk alerts and tailored risk reduction strategies. This approach reduces claim frequency and strengthens partnerships between insurers and policyholders, creating a more resilient and forward-looking insurance model.

As AI and big data continue to reshape business insurance, insurers that successfully integrate these technologies will gain a competitive edge, offering smarter, faster, and more personalized solutions. The shift toward AI-powered decision-making is not just enhancing operational efficiency but fundamentally redefining the role of insurance in business risk management.

Navigating AI’s Challenges: Regulation, Ethics, and Integration

While AI and big data are revolutionizing business insurance, their adoption comes with significant challenges. As they implement AI-driven solutions, insurers must navigate data privacy concerns, regulatory compliance, integration with legacy systems, and ethical considerations. Successfully addressing these challenges will determine how effectively the industry can leverage technological advancements while maintaining transparency and trust.

One of the most pressing issues is data privacy and security. AI-driven insurance models rely on vast amounts of sensitive business and financial data to assess risk, detect fraud, and personalize policies. However, the increased use of realtime data streams from IoT devices, financial transactions, and cybersecurity monitoring raises concerns about how insurers collect, store, and process this information. Regulatory frameworks such as the General Data Protection Regulation (GDPR) in Europe and industry-specific compliance standards require insurers to implement robust data governance strategies to prevent breaches and ensure responsible AI deployment.

Regulatory compliance is another critical challenge. As AI becomes more embedded in underwriting, pricing, and claims management, regulators are demanding greater transparency and accountability in AI-driven decisionmaking. In some jurisdictions, insurers must demonstrate that their AI models are explainable, unbiased, and free from discriminatory outcomes. The industry is increasingly moving toward interpretable AI models that allow regulators and stakeholders to understand how AI systems make decisions, reducing concerns about algorithmic bias and unfair risk assessments.

Beyond regulatory concerns, insurers also face technical and operational hurdles when integrating AI into their existing infrastructures. Many traditional insurance firms still operate on legacy IT systems not designed to support AI-driven automation and analytics. Upgrading these systems requires significant investment in digital transformation and retraining employees to work with AIpowered tools. While AI promises greater efficiency and accuracy, insurers must carefully balance these benefits

against data security risks, compliance challenges, and operational disruption during the transition.

Ethical considerations are at the heart of AI-driven insurance, shaping its development and regulatory oversight. As machine learning algorithms advance, insurers must ensure that their AI models uphold fairness and equity in decision-making. Concerns over algorithmic bias, opaque decision-making, and data-driven discrimination have prompted calls for stronger ethical guidelines in AI adoption. The challenge for insurers is to strike a balance between leveraging AI for efficiency and maintaining fairness in risk assessment and pricing.

Successfully navigating these challenges is essential for insurers aiming to remain competitive in an AI-driven landscape. Those that effectively manage data privacy, regulatory compliance, infrastructure modernization, and ethical concerns will be best positioned to build trust, enhance risk management, and drive sustainable growth in the evolving insurance sector.

The Future of AI and Big Data in Business Insurance

AI and big data are enhancing business insurance and redefining its foundation. From more precise risk assessments and dynamic pricing models to streamlined claims processing and fraud detection, these technologies are reshaping how insurers operate, making policies more adaptive, responsive, and data-driven.

As insurers navigate this transformation, the balance between innovation and responsibility will be critical. AIdriven underwriting and predictive analytics promise greater accuracy and efficiency, but they also introduce challenges related to data privacy, regulatory compliance, and ethical decision-making. The insurers that successfully integrate AI into their operations—while ensuring transparency and fairness—will be the ones that remain competitive in an increasingly digital-first market.

The future of business insurance is shifting from passive protection to proactive prevention. By leveraging realtime data, insurers can anticipate risks before they occur, offering businesses more tailored, efficient, and forwardthinking coverage solutions. As adoption accelerates, AI will enhance insurers' efficiency and reshape their role in risk management, providing deeper insights and stronger partnerships with policyholders.

For insurers that embrace AI and big data responsibly, the opportunities are game-changing. The industry is at a turning point—innovation is no longer optional; it is imperative. The leaders of tomorrow will not only adopt these technologies but master them, setting new benchmarks in risk management, efficiency, and customer-focused solutions.

How Fintech is Reshaping Enterprise Transactions

Financial technology is no longer just an enabler—it is redefining how businesses transact, manage liquidity, and mitigate risk. From AI-driven automation to blockchain-powered payments, fintech is revolutionizing enterprise finance at an unprecedented pace. Cross-border transactions are accelerating, blockchain is unlocking new capital flows, and artificial intelligence is transforming financial operations. Meanwhile, regulatory shifts are compelling enterprises to integrate compliance technology, ensuring resilience in an era of heightened oversight.

B2B finance stands at a pivotal moment. The convergence of these innovations is not just reshaping financial infrastructure, it is fundamentally altering the way enterprises manage risk, optimize operations, and drive growth. Companies that effectively harness fintech solutions will gain a competitive edge, while those slow to adapt risk losing relevance in an increasingly digitalized financial ecosystem.

The Acceleration of Enterprise Payments

Global payment infrastructure is transforming as enterprises demand faster, more cost-effective solutions. Cross-border blockchain transactions have surged by 48 percent year-over-year, with total transaction volumes projected to reach $5 trillion by the end of the year. For multinational corporations managing complex supply chains and vendor networks, this shift is particularly significant because it enhances efficiency, transparency, and cost reduction. The global payment processing market, valued at $79.6 billion in 2024, is forecasted to more than double, reaching $161.9 billion by 2030, driven by the need for seamless, real-time settlement solutions.

Beyond improving transaction speed, this evolution is prompting businesses to rethink financial structures, accelerating the adoption of blockchainbased financial instruments to optimize cash flow and enhance liquidity management. This increasing reliance on digital assets marks a shift toward a more automated and decentralized corporate finance ecosystem.

The Rise of Digital Assets in Corporate Finance

The adoption of digital assets in corporate finance has moved beyond speculation to become a strategic necessity. Financial institutions and multinational corporations leverage blockchain technology to enhance transaction efficiency, liquidity management, and security. While early blockchain initiatives were confined mainly to experimental pilots, enterprise adoption has now shifted to full-scale implementation, driven by regulatory developments, institutional demand, and costefficiency benefits.

The financial blockchain market is forecast to expand to $49.2 billion by 2030, underpinned by increasing corporate adoption. Tokenization is fueling this shift, with demand for tokenized assets expected to surpass $600 billion as businesses digitize real estate, commodities, and financial instruments to enhance liquidity and tradability. Companies are already integrating tokenized assets into supply chain financing, trade settlement, and cross-border transactions, reducing counterparty risks and accelerating settlement cycles from days to seconds.

Institutional players are at the forefront of this shift. Global banks and asset managers are launching tokenization platforms to support blockchain-based financial instruments while leading exchanges are adapting their models to incorporate institutionalgrade digital assets. The line between traditional finance and decentralized finance (DeFi) is beginning to blur, creating new opportunities for capital markets and investment vehicles.

However, widespread adoption still faces hurdles. Regulatory uncertainty remains a significant challenge as jurisdictions vary in their approaches to digital asset oversight and compliance frameworks. While some regions, such as the European Union and Singapore, have taken proactive steps to establish clear regulatory guidelines, others remain in the process of defining their stance. These evolving policies will shape how enterprises navigate compliance, security protocols, and risk mitigation strategies.

As digital assets gain further traction, corporate finance leaders must take a proactive approach to blockchain integration. Success will depend on identifying clear use cases, ensuring regulatory alignment, and leveraging blockchain for real-world operational efficiencies. While adoption will progress at different rates across industries, enterprises that effectively incorporate tokenization into their financial strategies will be positioned for long-term success in an increasingly digital and decentralized global economy.

CBDCs and the Institutional Shift

Central Bank Digital Currencies (CBDCs) continue to evolve but at a more measured pace than initially anticipated. Nearly a third of central banks have pushed back their plans to launch digital versions of their currencies, citing the need for regulatory clarity, interoperability testing, and risk assessment. However, a majority remain committed to eventual implementation and motivated to maintain control over monetary policy and currency issuance. At the same time, crossborder wholesale CBDC projects have more than doubled in recent years, reflecting a growing institutional focus on enhancing interbank settlements and streamlining global financial flows.

Several central banks, including the People’s Bank of China (PBOC), the European Central Bank (ECB), and the Federal Reserve, have launched pilot programs aimed at testing digital currency infrastructure for wholesale transactions. Among them is Project mBridge, which connects banks in China, Thailand, the UAE, Hong Kong, and Saudi Arabia. The initiative is expected to expand to additional countries this year, further advancing the institutional use of digital currencies. As central banks focus on enhancing interbank settlements and streamlining global financial flows, wholesale CBDCs are becoming an increasingly viable solution for cross-border trade finance, liquidity management, and large-scale corporate transactions.

The implications of CBDC adoption for enterprises are significant and promising. Businesses engaged in international trade could benefit from lower transaction costs, faster settlement times, and reduced reliance on intermediaries. Wholesale CBDCs have the potential to reduce foreign exchange risks by enabling faster settlement speeds and reducing dependence on intermediary currencies, particularly in emerging markets where currency volatility poses operational challenges. By enhancing transparency in cross-currency transactions and allowing for direct currency exchanges, CBDCs could mitigate the risks associated with FX fluctuations in cross-border payments.

Despite these advantages, concerns around cybersecurity, monetary policy impact, and privacy regulations remain key obstacles to widespread adoption. While some jurisdictions, such as China and the UAE, are rapidly advancing their digital currency frameworks, others remain cautious, awaiting clearer guidance on CBDC governance and integration with existing financial systems.

As CBDCs continue to develop, enterprises must stay ahead of evolving regulatory and technological frameworks. Understanding how digital currencies integrate into corporate finance, liquidity management, and global payment infrastructure will be critical in navigating the next phase of financial digitalization. This emphasis on continuous learning and adaptation underscores the importance of staying informed and proactive in the rapidly evolving fintech landscape.

Artificial Intelligence and the Future of Enterprise Finance

Artificial intelligence is no longer just an efficiency tool—it is becoming a core pillar of enterprise finance, reshaping everything from real-time risk management to advanced financial modeling. Investment in AI-driven compliance, fraud detection, and predictive analytics are accelerating as companies race to integrate automation and machine learning into financial operations.

In the B2B finance sector, AI is proving particularly valuable for automated risk assessment. It allows enterprises to analyze large-scale financial data sets to detect anomalies and predict credit risks with unprecedented accuracy. AI-driven fraud detection systems, now embedded in global payment networks, analyze transactional behavior in real-time to flag suspicious activity, reducing financial crime losses by up to 50%.

The rise of generative AI is also driving transformation in corporate finance. AI-powered automation is now used to process complex legal documents, streamline contract analysis, and enhance regulatory compliance reporting, reducing processing times by up to 90%.

As AI continues to evolve, enterprises face new challenges in security and compliance. While AI enhances financial decision-making, regulators increasingly scrutinize AI-driven financial services, requiring businesses to adopt explainable AI models that maintain transparency and compliance.

AI is no longer an optional investment for financial institutions—it is a strategic imperative. Companies that fail to integrate AI-powered financial tools risk being left behind in an increasingly automated and data-driven economy.

Regulatory Technology: The Compliance Backbone of Fintech Adoption

As financial technology reshapes enterprise transactions, regulatory compliance remains a central challenge. The increasing complexity of global financial regulations—combined with the rise of digital assets, AI-driven financial services, and CBDCs—is forcing businesses to rethink their approach to compliance. Regulatory technology (RegTech) is emerging as a critical component of enterprise fintech strategies, providing automated solutions for real-time monitoring, risk assessment, and fraud prevention.

Several key factors are driving the demand for RegTech. Cross-border operations require companies to comply with multiple regulatory frameworks, increasing the burden of reporting and compliance costs. AI-powered RegTech solutions enable businesses to automate compliance processes, ensuring adherence to evolving jurisdictional requirements while reducing operational risks. According to Allied Market Research, the RegTech market was valued at $11.7 billion in 2023 and is projected to reach $83.8 billion by 2033, growing at a CAGR of 21.6% as enterprises increase automation to manage regulatory complexity.

AI is already being leveraged to streamline regulatory processes in finance, healthcare, and manufacturing. AI-driven RegTech platforms have been shown to significantly reduce compliance costs by automating risk assessments, fraud detection, and legal reporting. In legal departments, AIbased tools have led to a 90% reduction in document filing time, enhancing operational efficiency and lowering the costs of regulatory compliance.

Governments and financial authorities are also accelerating digital compliance initiatives, particularly with the rise of digital currencies and decentralized finance (DeFi). As CBDCs and blockchain-based transactions gain traction, regulatory frameworks must evolve to monitor these financial innovations effectively. Enterprises that fail to integrate automated compliance solutions risk exposure to regulatory penalties, legal scrutiny, and operational inefficiencies.

By leveraging RegTech, enterprises can reduce compliance costs, enhance fraud detection capabilities, and improve regulatory reporting efficiency. Integrating AI-powered compliance tools is proving indispensable in managing evolving regulations and mitigating financial crime risks. As financial technology continues to grow at a rapid pace, businesses that proactively implement RegTech solutions will be better positioned to navigate the increasingly complex global regulatory environment.

The Strategic Imperative for Enterprises

For businesses, accelerating financial technology adoption presents both opportunities and challenges. The integration of blockchain-based payments, AI-driven automation, and advanced regulatory technology is driving down transaction costs, improving efficiency, and expanding access to global markets. However, success in this evolving environment necessitates a strategic approach. Enterprises must ensure that their infrastructure is adequately prepared for digital asset integration, invest in workforce development to optimize AI applications and implement rigorous compliance protocols to navigate an increasingly stringent regulatory landscape. Cybersecurity remains a paramount concern, requiring businesses to adopt sophisticated risk mitigation strategies to safeguard digital transactions.

The adoption of financial technology within the B2B sector has historically lagged behind consumer finance, but 2025 represents a pivotal inflection point. Companies that fail to integrate financial technology risk operational inefficiencies and diminished competitiveness, particularly as the industry moves toward full-scale digitalization. The imperative now is to transition from experimental adoption to strategic deployment, ensuring that technological investments address specific operational challenges and deliver measurable business value.

The accelerating pace of financial technology adoption is creating opportunities, but enterprises that fail to plan strategically may struggle to maintain resilience in a rapidly evolving environment. Successful adoption requires more than just technology upgrades—it demands a holistic approach that integrates infrastructure readiness, workforce development, regulatory alignment, and cybersecurity preparedness. Businesses that embrace digital finance innovations today will define the future of enterprise transactions—while those that hesitate risk falling irreversibly behind in a rapidly evolving financial ecosystem.

Smart Advertising Strategies That Work for Small Businesses

If you’re running a small business, throwing money at ads isn’t enough—you need a smart, strategic approach that delivers results. The rise of digital marketing, the evolution of traditional advertising channels, and the growing influence of AI-driven solutions have fundamentally reshaped how small businesses connect with their audiences. Gone are the days when a simple newspaper ad or a few local radio spots would suffice. Today’s small business owners must navigate an increasingly complex, data-driven landscape where customer behavior is constantly shifting.

With digital platforms proliferating and competition intensifying, success requires more than just visibility—it demands a clear, results-driven strategy that maximizes every advertising dollar. Whether through social media, search advertising, or AI-powered tools, the most successful businesses take a strategic, multi-channel approach to engage their audiences effectively. Here’s what actually works.

The Digital Revolution in Small Business Advertising

The numbers tell an interesting story about where small businesses are placing their bets. According to recent data, social media now accounts for 27.2% of total ad spend among small businesses, with online search ads following at 16.3%. This shift toward digital isn't just a trend—it's a fundamental change in how small businesses reach their customers.

Rather than relying solely on traditional advertising methods, businesses are embracing digital platforms that offer precise targeting, real-time analytics, and scalable results. Social media, in particular, allows brands to engage directly with their audience, build communities, and drive conversions through interactive content. Search advertising, on the other hand, capitalizes on consumer intent, ensuring businesses appear at the right moment when potential customers are actively looking for their products or services.

Beyond paid advertising, a strong digital presence has become a cornerstone of small business success.A78% of small businesses report their websites successfully generate new leads and customersbut also enhance brand awareness and drive sales. This underscores an important reality: having a well-optimized online presence is no longer optional—it’s essential for long-term growth and competitiveness.

The Most Effective Channels for Small Business Advertising

1. Social Media Marketing

Small businesses are finding success with platforms like Instagram, Facebook, and TikTok. The data shows that 52% of small businesses now use social media marketing, making it the most widely adopted advertising channel. The key is choosing the right platform for your specific business type and audience. For instance, visually-driven businesses such as fashion boutiques and restaurants thrive on Instagram, while service-based businesses often find better engagement on Facebook. TikTok, with its viral potential, offers opportunities for brands that can create authentic, engaging content tailored to younger audiences. The real advantage of social media advertising is its ability to foster direct connections with customers, allowing businesses to build relationships, drive brand loyalty, and create highly targeted ad campaigns with measurable results.

2. Short-Form Video

Perhaps the most significant trend in digital marketing is the rise of short-form video content. 56% of marketers plan to invest more in short-form video this year, recognizing its power to engage audiences quickly and effectively. This format works particularly well on platforms like TikTok, Instagram Reels, and YouTube Shorts, where attention spans are short but engagement rates are high. Video content not only captures interest but also helps businesses showcase their products or services in an authentic and

relatable way. Whether it’s a behind-the-scenes look at a small business, a customer testimonial, or a product demo, short-form videos can drive stronger connections and higher conversions. Importantly, these videos don’t require large production budgets— simple, well-crafted clips filmed on a smartphone can often outperform highly polished commercials.

3. Search Advertising

Pay-per-click (PPC) advertising continues to deliver strong returns for small businesses. 40% of small businesses are now using search ads, finding them effective for reaching customers actively looking for their products or services. Unlike social media ads that rely on interest-based targeting, search ads place businesses in front of users with immediate purchase intent. Google Ads remains the dominant platform, but Microsoft Advertising (Bing Ads) can also be a valuable tool, particularly for businesses targeting professional or older demographics. The key to success with search advertising is optimizing ad copy, using relevant keywords, and continuously refining campaigns based on performance data. When done correctly, PPC ads can drive highly qualified leads and offer a strong return on investment.

Maximizing ROI in Small Business Advertising

The goal isn't just to advertise—it's to advertise effectively. A typical successful digital marketing campaign achieves a 5:1 return on investment, meaning for every dollar spent, five dollars are generated in return. However, this requires strategic planning and careful execution.

Cost-Effective Strategies:

• Start with Clear Targeting: Define your audience precisely before spending a dollar on advertising.

• Test and Measure: Begin with small budgets and scale what works.

• Focus on Local: For brick-and-mortar businesses, local SEO and targeted local advertising often provide the best returns.

• Leverage Multiple Channels: The top businesses are investing in both digital (18%) and traditional marketing (10%), suggesting a balanced approach works best.

The AI Revolution in Small Business Advertising

One of the most significant shifts in small business advertising is the growing integration of AI. With artificial intelligence becoming more accessible and sophisticated, small businesses are leveraging it to enhance efficiency, reduce costs, and improve targeting precision. Business owners are increasingly turning to AI and machine learning to optimize their advertising efforts, enabling them to compete more effectively with larger companies.

AI-driven tools now power everything from automated ad creation to predictive analytics, helping businesses make data-backed decisions. Advanced AI algorithms analyze customer behavior, identify high-performing ad creatives, and personalize messaging at scale—boosting engagement and conversion rates. Platforms like Meta, Google, and TikTok use AI to refine ad placements, ensuring businesses reach the right audience at the right time.

Beyond ad targeting, AI is transforming content creation and customer interaction. AI-powered copywriting tools generate compelling ad headlines and product descriptions, while chatbots and virtual assistants provide real-time customer support, improving response times and engagement. Small businesses are also utilizing AI-powered video editing software to create high-quality, engaging short-form videos—one of the fastest-growing ad formats today.

As AI continues to evolve, the key for small businesses is to embrace these tools strategically. Those who integrate AI into their advertising workflows—whether through automation, personalization, or predictive insights—stand to gain a competitive edge in an increasingly crowded digital landscape.

Looking Forward

The most successful small businesses aren’t just selecting advertising channels at random—they're crafting integrated, data-driven strategies that align with their growth goals. This means using social media to build brand awareness, leveraging search ads to capture high-intent customers, and deploying email marketing for lead nurturing. It’s not just about spending on ads; it’s about investing in the right platforms, continuously optimizing campaigns, and staying ahead of industry trends.

The key to long-term success in advertising is adaptability. Consumer behaviors shift, platforms evolve, and new technologies emerge—all requiring businesses to remain flexible and willing to experiment with new approaches. What worked last year might not work today, and what drives success for one business might not be effective for another. The small businesses that thrive in are those that stay informed, embrace innovation, and maintain a relentless focus on maximizing ROI while delivering meaningful customer engagement.

Romance Scams: A Growing Threat and How to Fight Them

In an age where digital connections flourish, love has become a double-edged sword. With romance scams soaring to alarming heights, the UK Finance 2024 Report reveals a staggering 17% increase in financial losses from these scams, coupled with a 14% rise in reported cases, while the FBI's IC3 2023 report highlights over 17,823 victims in the US, collectively drained of a jaw-dropping $652 million.

Yet, these figures only scratch the surface, as an estimated 70% of victims remain silent, their stories buried beneath shame and heartbreak. Behind every statistic lies a real person—someone who believed in love, only to find themselves ensnared in a web of deceit that resulted in major financial loss. As banking institutions and regulators scramble to implement reimbursement laws, the battle against these emotional and financial predators demands a united front. With social media as the breeding ground for such fraud, tech companies and lawmakers must join forces to close the gaping loopholes that allow these scams to thrive, transforming the digital landscape into a safer haven for genuine connections.

Romance scams are no longer the work of individuals alone like the infamous "Tinder Swindler." Today these scams are perpetrated by organized criminal groups. The United Nations Office on Drugs and Crime (UNODC) reports that these groups treat scams like a business—complete with departments for generating fake identities, groomingscamming victims and laundering money. These networks stretch across Southeast Asia, West Africa, and Eastern Europe. In Nigeria and Ghana, "Yahoo Boys" have shifted from the old "419" email schemes to romance fraud, chasing higher payouts.

Technology: A New Weapon for Scammers

Technology is giving scammers a dangerous edge. Deepfakes and AI tools make their lies more convincing than ever. AI-generated images can't be traced through simple reverse-image searches, and scammers can now appear as entirely different people on live video calls. Voice cloning tools make phone calls seem more legitimate, blurring the line between reality and deception.

Frank McKenna, reporting for Frank on Fraud, unveiled the sophisticated AI tactics employed by "Yahoo Boys." Scammers leverage the latest advancements in AI, including deepfakes to both generate fake identity documents but also create fake images and videos to scam victims on social media. The rapid advancement and accessibility of AI has led to widescale use of these by criminal groups. New research from Stanford University and Google DeepMind, shows that AI can now clone entire personalities in as little as two hours.

AI systems analyze a person's speech patterns, word choices, and emotional expressions to replicate their voice, unique mannerisms, and communication style. Criminal groups can use such technology to create digital personas that would be indistinguishable from real people. These developments underscoring the urgent need for regulation around AI's ethical use and updated fraud detection systems.

Social Media's Role in Facilitating Scams

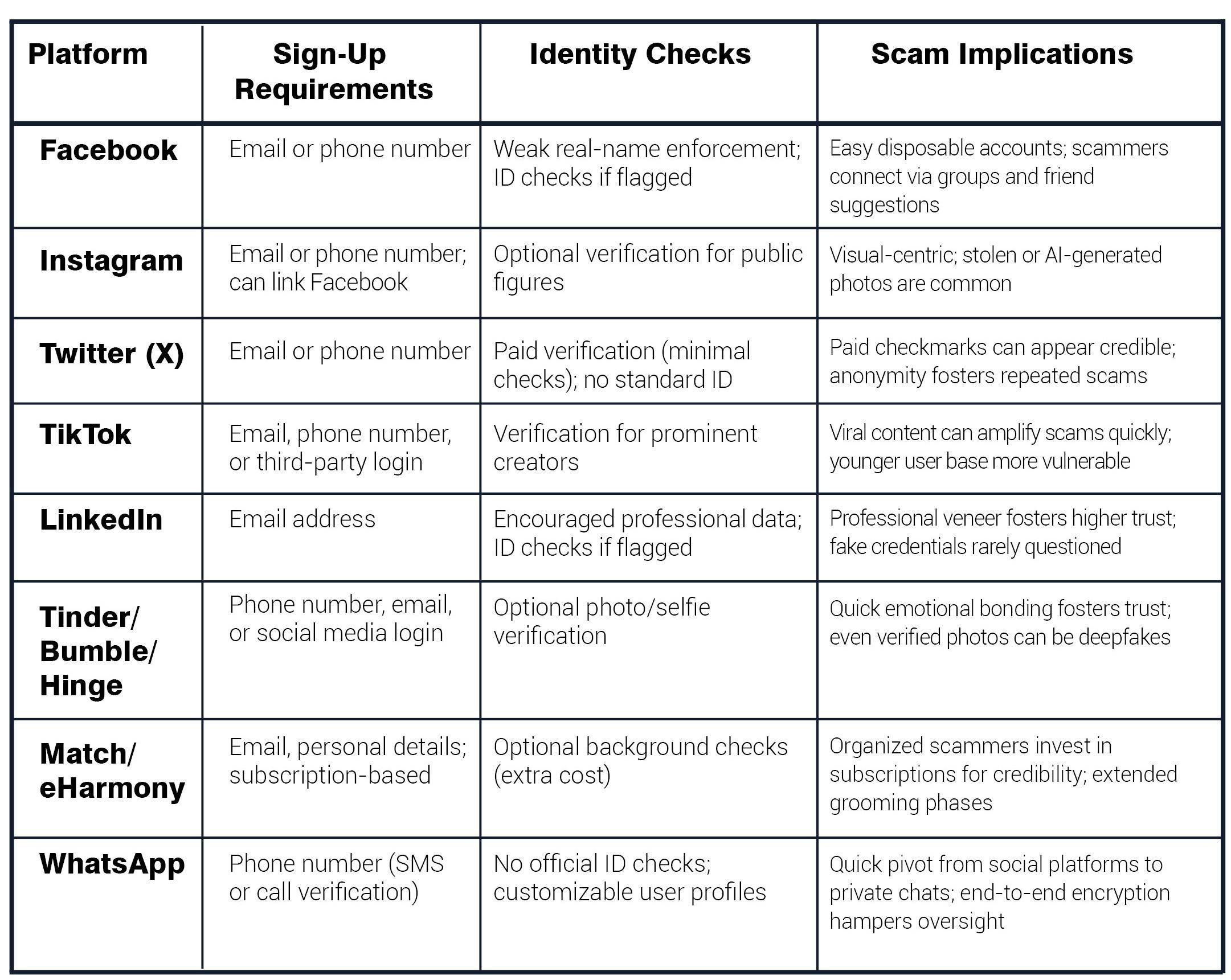

Social media and dating apps are fertile hunting grounds for scammers because creating fake profiles is ridiculously easy. Tightening user verification might slow down scam activity, but it could also reduce user numbers—a tough trade-off for platforms focused on growth.

A research study conducted by TSB Bank revealed that a staggering 80% of all social media fraud cases were linked to Meta-owned companies like Facebook, Instagram, and WhatsApp. Victims often encounter scammers through fake profiles, with poor moderation allowing fraudulent accounts to thrive. The data underscores how inadequate oversight and reactive moderation contribute to the proliferation of romance scams. The table below illustrates the different sign-up requirements and identity checks employed by some of the most popular social media and dating platforms. A phone number or email is often all it takes to create multiple accounts. Platforms like Facebook and Instagram don't strictly enforce their real-name policies, allowing scammers to blend in. Most platforms act only after a scam has been reported—and by then, the damage is done.

Even when fake profiles are reported, social media platforms take minimal to no action to remove them. Social media platforms like Meta have taken action to combat organized crime groups. As reported by Axios, Meta blocked over 2 million accounts linked to scam compounds in Myanmar, Laos, Cambodia, the UAE, and the Philippines. However, experts argue that these measures are insufficient given the scale of the problem.

The Legal Shield: Section 230: why it needs revised

Section 47 U.S.C. § 230 is a law enacted in 1996 to foster innovation by protecting internet companies from liability for user-generated content. The law encouraged "Good Samaritan" moderation without incurring publisher-level liability. Although written with the spirit of innovation, at heart the law hasn't kept up with technology and how the internet has evolved.

Platforms now host billions of users and manage sophisticated content algorithms, but thanks to Section 230, they still aren't legally responsible when scammers use their services. This legal shield means platforms have little incentive to invest heavily in fraud detection.

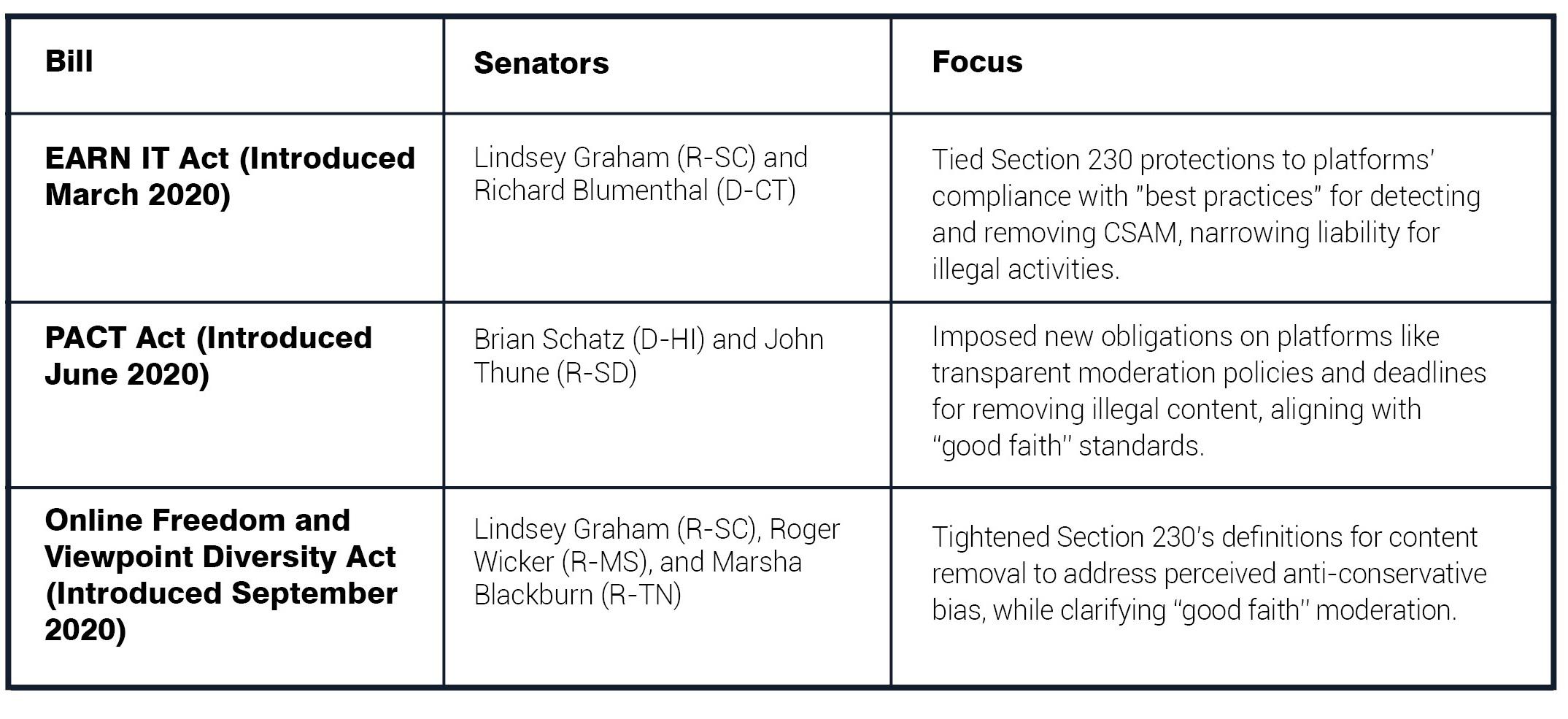

In 2020, the US Department of Justice reviewed Section 230, proposing reforms to hold platforms accountable when they knowingly allow scams, establish clear standards for good-faith moderation, and introduce a duty of care requiring platforms to implement basic fraud detection tools.

Several legislations have been introduced by a number of senators, as summarized in the table below, all seeking to narrow the broad immunity currently protecting platforms from liability

If passed, such legislation will hold platforms accountable and require them to shut down accounts that are engaged in scam activity.

The Financial Sector's Role in Combatting Romance Scams

In the U.S., transparency around scam reimbursements is limited because actual reimbursement data isn't publicly available. In contrast, the U.K. provides better reporting on reimbursement practices, with 66% of all losses related to authorized push payment (APP) fraud reimbursed in 2023. This transparency stems from the Contingent Reimbursement Model, a voluntary code signed by banks before the U.K. Payment Systems Regulator (PSR) reimbursement requirements took effect in October 2024. While reimbursements are crucial, banks must prioritize proactive measures to prevent scam transactions. Leveraging advanced technologies like machine learning, behavioral analytics, and real-time transaction monitoring can help identify and block scams as they occur.

Given the irrevocable nature of many faster payment systems and high transaction limits, real-time monitoring is critical. Fraud detection systems that utilize machine learning models can flag risky transactions, but building mechanisms and processes to intercept these transactions is equally essential. Scammers often create a false sense of urgency, leading victims to initiate and authorize transactions that result in financial loss.

Automated methods, such as push notifications through banking apps or text messages, can alert customers to potential risks. For example, a pop-up message could inform users that the intended beneficiary has been linked to three recent scam claims under investigation. Such transparency, when combined with empathetic human agents, can significantly reduce the number of romance scam transactions.

Data sharing is vital for building a collective defense against fraud. Sharing scam patterns and risk lists enables financial institutions to identify high-risk beneficiaries suspected of fraud. The Federal Reserve's Scam Information Sharing Industry Work Group has recommended enhancing this collaborative approach, emphasizing real-time information sharing and standardized data formats.

What Can Be Done to Stop Romance Scams?

Addressing romance scams requires coordinated efforts across various sectors, including social media platforms, regulatory frameworks, and financial institutions. Social media platforms need to strengthen their user verification processes and enforce stricter moderation policies. Additionally, these platforms should publish regular transparency reports that detail scam-related activities.

There is also a need to amend Section 230 to narrow the broad immunity that currently protects platforms from liability when scammers exploit their services. Recommendations from the Department of Justice for clearer "good faith" moderation standards and a defined duty of care are essential in this regard.

Banks play a crucial role by enhancing real-time fraud detection through machine learning and behavioral analytics. They should also implement robust interdiction mechanisms to prevent fraudulent transactions from being completed.

Furthermore, promoting cross-industry data sharing is vital for identifying high-risk accounts and beneficiaries. Collaboration between banks, social media platforms, and law enforcement is key to effectively curbing these scams. By taking these steps, we can strengthen defenses against romance scams, reduce financial losses, and better protect vulnerable individuals.

Anurag Mohapatra SME and Sr. Product Manager, NICE Actimize

Accelerating into the era of AI-driven finance

The McKinsey Global Institute (MGI) estimates that generative AI (gen AI) could inject between $200 billion and $340 billion into the global banking industry yearly, representing 9% to 15% of operating profits. What we are seeing in this domain is AI’s growing ability to boost productivity, streamline operations, and drive innovation, creating significant economic benefits. AI is no longer a distant concept; it’s now actively reshaping the financial sector, influencing everything from traditional institutions to the latest Fintechs. There’s now increasing recognition of AI’s transformative potential, with particular focus on gen AI.

Financial services institutions (FSIs) are automating complex tasks like detecting fraud and enhancing risk management processes, while improving productivity by reducing time spent on repetitive tasks like loan eligibility analysis or market trend forecasting. Beyond efficiency, gen AI is catalysing innovation by unlocking entirely new possibilities. Firms can now develop highly personalised financial products tailored to individual customer needs and simulate complex market scenarios to refine investment strategies. Additionally, its ability to generate creative solutions, such as optimised portfolio structures or new credit scoring methodologies, is paving the way for breakthroughs in how financial products are designed and delivered.

Strategic implementation is essential to harness the opportunity here. FSIs must move beyond superficial applications if they want to fully capitalise on AI’s potential. Integrating AI requires a broader, more holistic approach, ensuring the technology is seamlessly woven into the fabric of existing operations. The real challenge lies in navigating risks while embedding these advanced capabilities into business systems without causing too much disruption.

The engine behind financial transformation

The significant potential of AI to revolutionise financial services is powered by foundational and large language models. These highly sophisticated neural networks, trained on vast datasets, have revolutionised how we approach machine learning. Models like FinGPT and BloombergGPT are already making impressive strides in the finance sector, offering solutions that are finely tuned to the needs of the industry. As mentioned, the success of these models ultimately depends on how seamlessly they are built into existing processes.

To implement AI smoothly, FSIs can use techniques such as Retrieval Augmented Generation (RAG) and Reinforcement Learning from Human Feedback (RLHF). RAG enhances the accuracy and relevance of AI models by incorporating data from internal or external sources, while RLHF makes AI more intuitive by refining models based on human feedback. These techniques are essential for continuously improving AIdriven financial solutions, helping them to evolve and remain relevant in a rapidly changing environment.

Taming AI with intelligent agents and guardrails

If large language models are the engines in our AI equation, then intelligent agents are the drivers. These systems interact with their environment, make informed decisions and execute tasks to achieve specific goals. In other words, intelligent agents keep AI systems on track and focused on their objectives. By breaking down complex processes into smaller, more manageable tasks, intelligent agents help ensure that each part of the system functions properly.

Despite the immense potential of generative AI, its inherent risks must be managed carefully. Issues like inadequate training data, incorrect assumptions and biases in AI models can lead to unethical outcomes and inaccurate results, such as data hallucinations. Additionally, gen AI models often operate as “black-box” opaque systems, making it challenging to explain their outputs or decisions – this lack of transparency can undermine trust and complicate regulatory compliance. FSIs must apply robust monitoring systems and explainability tooling and establish ethical guardrails to mitigate these risks. These measures are essential for maintaining the integrity of AI systems and ensuring they operate within ethical and regulatory boundaries.

Handling the speed of AI development

FSIs must adopt a modular and adaptable approach to integrate AI into their digital infrastructures to cope with the breakneck speed of the technology’s evolution. Modularity allows for the seamless adoption of new technologies without requiring a complete system overhaul. Instead of starting from scratch, institutions can build on their existing systems, gradually adding microservices as needed. This approach preserves the value of prior investments and ensures a smoother transition to AI-enhanced operations.

By scaling AI implementation, financial institutions can test and refine individual AI components at each implementation stage. This method minimises downtime and improves system resilience, allowing institutions to quickly adapt to new technological advancements and maintain a competitive edge in the marketplace.

Redefining the future of finance with AI

It is now business-critical for financial services firms to achieve greater efficiency, reliability, and flexibility to meet the evolving needs of their customers and stay competitive. However, the true competitive edge will belong to those firms that move beyond merely transforming existing workflows and fully embrace AI-driven innovation to reimagine their offerings and business models.As AI continues to develop, its impact on the financial sector will only deepen. According to the World Economic Forum, AI may have the power to identify the patterns that predict financial crises before they happen and take pre-emptive action to mitigate or even avert them. Automated crisis prevention represents a revolutionary shift in how the industry manages risk. Gen AI, still in its infancy, is already a powerful tool for the present – but as it matures, it is poised to reshape and define the future of financial services.

Abi Wareing, Senior Manager, Airwalk Reply

Building Mongolia’s Financial Future: An Exclusive Interview with State Bank CEO Gantur Ulzii

State Bank is a leading financial institution in Mongolia, playing a crucial role in delivering banking services, supporting government initiatives, and driving sustainable economic growth. With a strong focus on financial inclusion, green banking, and digital transformation, the bank continues to expand its reach and impact across the country.

Wanda Rich, Editor of Global Banking & Finance Review, interviewed Mr. Gantur Ulzii, CEO of the State Bank of Mongolia, to discuss the bank’s strategic evolution, its role in strengthening Mongolia’s financial sector, and its initiatives to enhance financial accessibility, sustainability, and digital banking solutions.

How has the bank evolved from its early beginnings to become a significant player in Mongolia’s financial sector today?

The State Bank is recognized as one of the five systemically influential banks in the Mongolian financial system. Since its establishment, we have consistently met, and often surpassed, the criteria set by the Bank of Mongolia, maintaining a prudential ratio well above the required standards. We have also successfully fulfilled our annual business plan objectives, with completion rates ranging from 100% to 130%. As of the end of 2024, the bank has reported a profit of 108 billion tugriks. In summary, we have consistently honored our obligations to our customers and depositors, entering the next 15 years with their trust fully intact.

As a state-owned bank, we have a responsibility to deliver government programs, projects, and policies to citizens through our banking services. Additionally, we provide essential welfare and pension services that other banks are often reluctant to offer, thereby contributing significantly to both economic and social development.

In 2021, the Government of Mongolia designated the State Bank as a key institution supporting the middle class. In support of this mandate, we have developed and implemented a comprehensive strategic plan.

Furthermore, as part of broader reforms in the banking sector, the Banking Law was amended, enabling the transformation of systemically important banks into joint-stock companies. The State Bank led this initiative, becoming the first systemically important bank to transition to a publicly traded joint-stock company, offering new investment opportunities to the public.

The banking sector plays a crucial role in national development, driving progress, fostering sustainable growth, and setting an example in social responsibility. The State Bank is particularly focused on strengthening its partnerships with both public and private sector organizations to advance key goals, such as mitigating climate change, financing environmentally sustainable projects, and supporting green development. Through our commitment to green financing, we aim to raise public awareness, promote its benefits, and improve accessibility, thereby contributing to the achievement of the United Nations Sustainable Development Goals.

Expanding financial inclusion is a key priority for many banks. How is State Bank reaching underserved populations and making retail banking more accessible to Mongolians, especially in rural areas?

The State Bank was established in 2009 with the primary objective of safeguarding the interests of customers and depositors while ensuring the bank's financial stability. In 2013, the bank expanded its operations to serve small and medium-sized businesses and individual citizens, with the vision of becoming a nationwide institution that reaches every corner of the country. Today, the State Bank serves over 2.3 million customers through a network of 500 branches located in Ulaanbaatar, 21 provinces, and all soums.

This extensive network ensures that even customers in remote areas, including farmers and nomadic communities, have access to world-class banking and financial services. Our customers are fully equipped with the ability to easily access savings, loans, and card products through self-service kiosks, ATMs, and the Gyalsbank / the mobile bank/ app. In addition, they can

conveniently make payments for various services, including consumption, taxes, and insurance, as well as receive 66 types of reference information from 12 government organizations, all free of charge.

Customer trust and satisfaction are at the heart of retail banking success. What are some of the key measures State Bank has implemented to enhance customer experience and build lasting relationships?

As part of its commitment to fostering financial literacy within the framework of supporting the middle class, the State Bank has provided free financial education to students in secondary schools, universities, and colleges. Additionally, the bank has adapted its products and services to better meet the evolving needs of citizens, making them more flexible and accessible. Special products tailored to the daily lives of citizens—such as those focused on health, education, housing, and SME employment—have been introduced to the market.

Furthermore, enhancing customer satisfaction involves not only ensuring smooth daily operations but also steadily improving financial performance. Over the past six years, the bank's profit has demonstrated consistent growth, particularly over the last three years. This increase in profitability has led to higher dividends for small shareholders of the State Bank JSC, as well as a rise in taxes paid to both the state and local budgets.

What challenges has the State bank faced over the past 15 years, and how have these shaped the bank’s growth and strategy?

Over the past 15 years, the State Bank has navigated and overcome numerous challenges to reach its current level of success. The most significant of these challenges was the global COVID-19 pandemic, which occurred between 2020 and 2022. In hindsight, we can reflect on the many obstacles we faced during that period and how we were able to overcome them with minimal health and economic impact. During the emergency situation brought on by the pandemic, the State Great Khural, the Parliament and the Government of Mongolia launched the "10-Billion-Dollar Comprehensive Plan to Protect Health and Restore the Economy." In support of this initiative, the State Bank provided loans totaling 442 billion tugriks to approximately 9,000 citizens and businesses, helping to preserve 20,000 jobs. Furthermore, our team played a leadership role, collaborating with other organizations and banks to deliver essential banking services while strictly adhering to infection prevention protocols.

The State Bank has consistently enhanced its credit risk management systems, ensuring the effective implementation of operational policies and procedures. Notably, for the first time in Mongolia, the Government of Mongolia and the Bank of Mongolia successfully passed the Asset Quality Assessment (AQA) review conducted by the International Monetary Fund (IMF) under the "Extended Financing Facility" program. This review evaluated the quality of banks' loan portfolios. As a result, in 2022, the Bank of Mongolia, alongside PWC Kazakhstan, an international audit firm, successfully assessed five systemically important banks based on the AQA review results, further validating the State Bank’s ability to offer risk-free financial services.

ESG is becoming an essential part of banking globally. What specific ESG goals does the State Bank aim to achieve, and how are these integrated into the bank’s long-term strategy?

In recent years, governments and financial institutions around the world have placed increasing emphasis on environmental, social, and governance (ESG) issues, studying and adopting best practices to achieve sustainable development goals. As a result, strategies and goals that promote environmental sustainability, social well-being, and transparent governance have been proposed, accompanied by long-term action plans and phased measures for their implementation.

As a state-owned institution, the State Bank is dedicated to supporting environmentally and socially responsible activities that minimize negative impacts and foster good governance, all in alignment with Mongolia’s sustainable development goals. For example, we are promoting renewable energy and energy-efficient technologies through tailored financial products, as well as working to enhance livestock productivity within the agricultural sector. The bank’s long-term strategy centers on advancing green banking initiatives that contribute to sustainable development as a key focus area.

How does the bank plan to contribute to Mongolia’s broader sustainability goals, particularly in supporting businesses and individuals adopting more sustainable practices?

In 2022, the State Bank renewed its vision and mission, aligning with the goal of "Supporting the Middle Class." As part of this initiative, the bank introduced household and start-up business loan products to the public, while also offering financial education and consulting services for aspiring entrepreneurs. As a result of these efforts, in 2023, the bank issued shares to the public, successfully raising 25.4 billion tugriks. This made the State Bank the first jointstock company among the leading banks in Mongolia’s financial system.

Fifty percent of the funds raised from the primary market were allocated to support the middle class, while the remaining 50% was directed towards loans aimed at sustainable development, marking a significant milestone in the bank’s sustainability initiatives. In 2024, the Government of Mongolia tasked the State Bank with becoming a green bank dedicated to sustainable development. In response, we are planning a series of key initiatives to further enhance the bank’s business model by integrating sustainability into our policies. These initiatives include attracting green financing, issuing green bonds, introducing new green products and services focused on sustainable development, and transitioning to renewable energy technologies to reduce energy consumption across our offices and branches.

What role do you think the State Bank of Mongolia will play in leading the financial sector toward a more sustainable and inclusive future?

The State Bank extends its services to every citizen through a network of 500 branches across Mongolia, actively supporting and implementing government programs designed to maximize their impact. As of this year, we have clearly defined our goal of becoming a leading green bank. Our ongoing efforts are focused on achieving sustainable development goals through banking and financial services that prioritize environmentally responsible practices, respect human rights, and ensure accessibility to meet the diverse needs of our customers.