SUPPORTED BY: SILICON VALLEY BLUES: HOW VCs ARE ADAPTING TO A DOWN MARKET PRIV A TE EQUITY WIRE SEPTEMBER 2022

OVERVIEW PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 2 CONTENTS

VC fundraising is also starting to show signs of weakness, with significantly fewer managers closing funds during H1. Many of the recent entrants that helped to push up the market in 2020 and 2021 are now focused on other parts of their portfolio. When they return, it is set to be a different market indeed.

Welcome to Private Equity Wire’s 2022 Venture Capital Insight Report, where we present the latest trends and market shifts across the world of VC. Much like the dot com bubble in the late 1990s, it’s clear now that last year represented a peak in the venture capital cycle that had to come down to earth sooner or later. Evidence of this hard landing is not difficult to find and a marked change in mood is clear in Private Equity Wire’s exclusive survey of the industry. Valuations have been cut in several high-profile fintech start-ups already this year and, although the full extent of this ‘reset’ is yet to be seen in the 2022 data, the trend is set to continue in the months to come, ultimately impacting fund performance. Seed stage and early-stage start-ups (which typically have a longer runway to exit) so far, appear to be more resilient, but VC fund managers say they are thinking harder about the bets they are making across the board. Their focus on tech hasn’t changed, but the business models they are prioritising are now very different.

PrivateMETHODOLOGYEquityWiresurveyed 65 venture capital fund managers and investors during July and August 2022 on how fundraising, investment and valuations have changed in the past 12 months. Of the group surveyed, 87% were fund managers and the remainder were a mix of allocators and service providers.

KEY FINDINGS 3 SECTION 1 | FUNDRAISING 4 SECTION 2 | INVESTING 11 SECTION 3 | EUROPE 19 SECTION 4 | VALUATIONS 26

EXECUTIVE SUMMARY

COLIN LEOPOLD HEAD OF RESEARCH & INSIGHT

More than half of all the unicorns in Europe – start-ups with a valuation at or above $1bn – have been created in the last year, and VC investment here is slowing at a lower rate than in the US. VC firms are now operating across a handful of hubs on the continent – from London to Berlin, Paris and Scandinavia – but covering so many countries will present a challenge to even the largest investor.

Valuation ‘reset’ is not over VC funds face an uphill struggle to deliver above-average returns in the coming quarters as valuations are slashed at the late-stage. Seed stage valuations are holding up and have not fallen from the previous quarter since the onset of the pandemic, attributed to the high participation of non-traditional investors and micro-funds still active at seed stage.

Fundraising becomes difficult Global VC fundraising is trending downwards, after reaching an historic high in 2021. The number of funds closed in Q2 this year was the lowest seen for the past five years, once Q2 2020 is excluded. Recent entrants to VC – drawn in by the allure of a quick exit at high valuation – are retrenching, and some LP investors are now less able to make or increase commitments due to the denominator effect.

Europe is a bright spot

New tech cycles loom Fintech start-ups – where $1 in every five VC dollars went last year – may look less attractive to some VC firms as valuations continue to reset. But given VC dry powder has increased by $100bn in 2022 already, and now stands at $539bn, a focus on Web3, deep-tech and blockchain, among other areas, is opening up new channels of VC funding in other parts of the tech economy.

KEY FINDINGS KEY FINDINGS 13 24 PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 3

STARTS TO THIN

In July, Bay Area-based Lightspeed Ventures said it raised more than $7 billion across three new US funds, and one focused on India. A few days later, London-based Index Ventures announced close on three funds totaling $3.1 billion. Andreessen Horowitz and New Enterprise Associates have also announced fund closes above $2 billion already this year.

SECTION ONE: FUNDRAISING PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 4

“We’ve seen VC firms, especially in top five or top 10, invest heavily in their IR teams [to hit record fundraising levels]. This is a natural evolution for VC as the menu for investors expands across the private markets,” says Miguel Luina, head of global venture and growth equity at investment manager Hamilton Lane.

VC FUNDRAISING PARTY

Despite the valuation bubble bursting in parts of the venture capital market, the amount of capital raised by funds during the first half of 2022 has continued to boom, driven by record numbers of followon funds in the US and funds closing at more than $1 billion.

At 2022’s current rate of fundraising – $112 billion up to June 30, according to Preqin –this year’s total would eclipse the previous record of $210 billion raised in 2021. This is unlikely to be the case, however.

A survey by Private Equity Wire during July found that 85% of respondents believe the industry is in a “more challenging” fundraising environment than a year earlier.

In Q2, global VC fundraising was down year-on-year and the number of funds closed was the lowest seen in the past five years once the Covid-19 panic months of Q2 2020

Historically high levels of venture capital are still being raised by fund managers, but the number of them doing so is starting to fall

There is also a second reason, which is impacting private markets more generally: LP investors are pulling back on commitments as the value of their VC investments appears overweight, relative to a lower valued stock market, known as the denominator effect.

“The denominator effect is real,” says Ophir Shmuel, managing director at fund placement agent Eaton Partners. “We saw it during the global financial crisis and we’re seeing it now, especially in VC where valuations have been quite lofty. Macroeconomic factors are also playing a part and LPs are being more weary and conservative [about their commitments].”

Figure 1: Industry was asked ‘How would you describe the fundraising environment for VC in 2022, compared to 2021?

With VC valuations still somewhat elevated (see Chapter 4), the denominator effect will force more LPs to continue tweaking their allocations through 2022 and possibly until early 2023, say sources. Further slowdown “The VC fundraising market hasn’t really been tested yet,” says Luina at Hamilton Lane. “I think Q1 2023 is when you will see the ‘new normal’. Performance is still really strong, but a further slowdown is expected.”

In a presentation by VC giant Sequoia

SECTION ONE: FUNDRAISING PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 5 areWithexcluded.only560 fund closes in H1, even if the same number return during the second half of the year, the 2022 total would be a staggering fall from last year’s peak of 1,790 fundsThereclosing.aretwo possible explanations for Firstly,this. the new entrants or ‘crossover funds’ – hedge funds, institutions and corporates – drawn into late-stage venture in hope of cashing out quickly during the boom are retrenching (see box page 6).

The recent public market correction is unlike the financial crisis or the V-shaped Covid recovery, however.

Around $33 billion worth of stakes in private funds were sold during the first six months of the year, up from $19 billion in the same period in 2021, according to investment bank Jefferies, with almost half of these involving a first-time seller. Stakes in venture capital funds were sold at an average 71% of their most recent valuation. A recent survey by Preqin found that a third of institutional investors plan to cut their exposure to VC over the coming 12 months, compared to only 13% last year.

Source: Private Equity Wire survey, August 2022

SoftBank’s Vision fund and Tiger Global, which placed record bets in VC, both disclosed heavy losses this year. In August Softbank’s CEO was reported as saying he will be making significant changes at the company’s tech-focused venture capital funds to be “more selective in making invest ments [as] the market and the world is in Cambridgeconfusion”.Associates’s Aylott notes a retrenchment by crossover funds, or VC tourists as they are known, as their ability to gain alpha through an IPO exit or liquidity event has diminished.

TOURIST SEASON SLOWS IN VC I think Q1 2023 is where you will see the ‘new furtherPerformancenormal’.isstillreallystrong,butaslowdownisexpected

Driven by fear of missing out, hedge funds, private equity firms, sovereign wealth funds, corporate VCs and mutual funds represented two-thirds of all the money that went into venture capital globally last year, according to PitchBook data.

SECTION ONE: FUNDRAISING PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 6

As the market toughens, many are expected to wait out new fundraising plans in 2022, while others lick their wounds from the public market or face internal problems of their own.

“I think some of those investors will have a lot on their hands in terms of dealing with the issues in their portfo lio,” he says, “and that’s where we’ll see the biggest contraction.” At the same time however, the underly ing motivation of many of these cross over players has not disappeared. The current public market uncertainty will “temper their enthusiasm,” says Ed Knight at Antler, “but I don’t think the paucity of public market returns is go ing to diminish anytime soon and most of the growth and value creation in the world at the moment is happening with technologies in private markets.” Some crossover players are also finding more intelligent ways to access VC, through partnerships and acquisition of established VC brands. In May, one of the world’s largest private equity firms Apollo said it was taking a minority stake in long-established life sciences VC firm Sofinnova. The partnership of fers a clear benefit to each party, with Apollo promising a wider fundraising network and €1bn of managed capital and Sofinnova bringing expertise and investment opportunities across healthtech and life sciences, a key pillar of venture capital.

SECTION ONE: FUNDRAISING PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 7

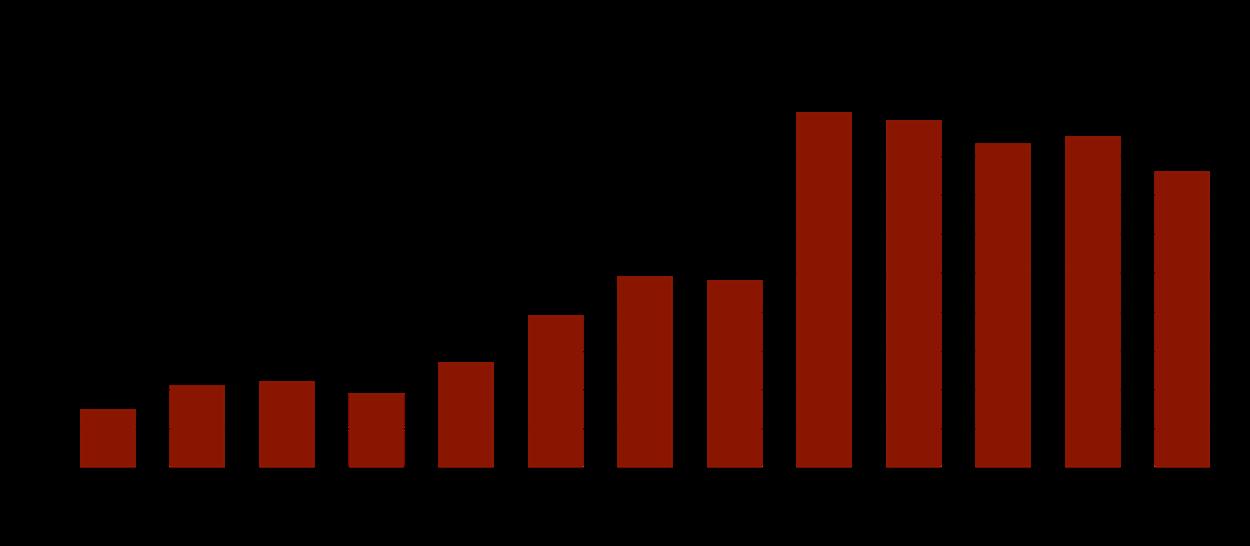

Analyst note: Venture Capital Historical Fundraising (USD bn) as at 11 Aug 2022

Source: Preqin Pro

Capital to founders in May, the company described a “crucible moment” with a long economic recovery and massive implications for fundraising. At the same time, Sequoia is reported to be raising two new US funds totalling more than $2 billion, alongside closing almost $9 billion for Chinese VC. So, what gives? Given VC is typically only a small percentage of an LP’s overall portfolio, wild swings in allocations are not expected. Established fund managers may also seize the opportunity to “steal market share” from LPs still active, says Stephanie Choo, partner at Portage Ventures, who notes a pullback from family offices, many of whom can be more flexible in their allocations. Large allocations of VC capital are still out there. In April, the $190 billion Ontario Teachers’ Pension Plan Board said it plans to more than double the size of its venture portfolio from 3% of net assets to 7-10% over the next five to 10 years. “This will set a precedent,” says Ed Knight, president at VC firm Antler, “bigger pools of capital are coming in and longerterm allocations I think are going to remain very, very positive.” Public pension funds outside the US may be another pool. In US VC, public pension funds contribute 65% of the capital but the figure is only 18% in Europe and 12% in the UK, according to 2020 figures. In Ireland, where the figure is less than 1%, an industry body has called on government to help scale up domestic VC pension contributions.

Figure 1.2: VC fundraising by quarter, since 2017

section one: VC FUNDRAISING IS MORE DIFFICULT THIS YEAR KEY less10%FINDINGSchallengingIndustry was asked ‘How would you describe the fundraising environment for VC in 2022, compared to 2021?’ more85%challenging5%same

Figure 1.3: The rise of venture tourism - crossover funds’ participation by deal

Source: Preqin Pro

VCs in fundraising mode remain optimistic, dependent on their strategy. Washington DC-based venture fund Starbridge recently launched a $125 million fundraising process for its third fund, targeting first close in September and final close in summer 2023. “The markets are down and everyone’s turtling,” says Michael Mealling, a general partner at the fund, “especially people who have not experienced a normal recession. I see many people whose only experience of a down market was the 2008 financial crisis and they’re equating it with now. [The current correction] is not a structural problem with the financial system and some of them are starting to realise that. So in terms of LPs, we really do expect and are already starting to see some green shoots beginning to come through.”Asaspecialist fund targeting spacetechnology, which also tends to be less exposed to economic cycles, Starbridge Fund III should still appeal to LPs in the current climate, he adds. Another LP priority can also be predicted. “There is a focus now [from LPs] on less cyclical funds; also for more niche and differentiated strategies – whether that be AI or cyber or deep tech, where there is less competition with everyone else,” says Shmuel.Withlate-stage VC valuations typically the first to be hit by a public market correction (see Chapter 4), there may also be an opportunity for fund managers to provide strategic solutions here, as others exit or look to early-stage investment.

Where does this leave VC in H2 2022?

SECTION ONE: FUNDRAISING PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 9

Analyst note: Other includes Investment Company, Sovereign Wealth Fund, Superannuation Scheme, and Investment Trust.

Source: Preqin Pro, 2021

With fewer parties from in and outside the VC world in fundraising mode, there is an opportunity for established names to steal market share Portage – a well-known fintech VC fund – recently reached first close on a new opportunistic late-stage fund, making it able to step in where others have pulled back.“We could not have picked better timing,” says Stephanie Choo, at Portage. “LPs see the need for this type of capital solution now and it requires a specific skill set.” For more generalist VC managers in the middle of fundraising, patience is advised. “Unless you are a top-tier fund, be prepared to take a little bit longer and be a little bit more understanding of the position LPs are in – many are now looking to 2023 allocations,” says Dan Aylott, head of European private investments at Cambridge Associates.

KEY TAKEAWAY – GP s

SECTION ONE: FUNDRAISING PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 10

Figure 1.4: No. of corporate investors in VC more than triples since 2017

SECTION TWO: INVESTMENT PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 11

“We’re seeing a pullback in fintech [funding], which has been disproportionately hit from a public markets valuation standpoint,” says Stephanie Choo at Portage, “and we’re seeing a reversion to valuing these companies more like financial services

THE NEXT TECH CYCLE TURNS

Dry powder now exceeds $500 billion but VC funds are more likely to be cautious and counter-cyclical in the current market

Global start-up funding is slowing but still exceeds pre-pandemic levels, both by deal number and total deal value. Q2 saw the largest quarterly drop in investment in nearly a decade (by 23%), according to data from CB Insights. The $108.5 billion total marked a six-quarter low but was still the sixth largest quarter for investment on record. The scale of the venture boom during 2021 has overshadowed the dot com bubble at the end of the 1990s. After almost a decade of easy money, the party appears over and the hangover is currently worst for late-stage start-ups and fintech, which captured one in every five VC dollars last year but as a sector is seeing redundancies build up this year.

section one: Private equity Insight report august 2022 | 12 We’re seeing a reversion to valuing fintech companies more like financial services companies, and less like tech companies Stephanie Choo, partner, Portage Ventures

Waiting for offense For example, grocery delivery app start-ups now look vulnerable, say sources, with retail tech funding down 43% quarter-on-quarter to hit $13.2 billion, marking a 7-quarter low for the sector, according to data from CB Insights.“VCsare being much more thoughtful and robust about which companies in their portfolios they’re going to continue to support and doubling down on what they believe to be long term winners,” says Aylott. “There will be pockets of opportunity and I think the savvy GPs will be waiting to play offensive in some of those areas.” Dry powder in the asset class has increased by $100 billion in 2022 already, and now stands at $539 billion, according to Preqin. But given VC strategies can differ, opinions vary on where this doubling down

Figure 2.1: Industry was asked ‘What one sector offers the most attractive investment opportunities in the current market?

“I think we’re in the early innings of this reset fully playing out,” says Dan Aylott at Cambridge Associates. “We’ll see VCs being much more cautious in terms of their deployment until valuations settle [as] they will have more issues in their portfolios to deal with.” A more rigorous approach to due diligence has returned among VCs with some sectors facing more challenges than others. New and more pertinent questions are being asked by VCs than a year ago: ‘do you have enough cash to last 24 months?’ is more relevant in the current market than jaw-dropping revenue growth, say sources. Generally, attention has moved away from late-stage funding and growth equity, towards seed and early-stage companies with a longer path to IPO and less inflated valuations [see Chapter 4]. In a July op-ed published in Fortune magazine, the co-founder and CEO of Canada-based Portage Ventures wrote: “Some may find that making a quick buck from investing in the cutest CryptoKittie is more fun than pouring over spreadsheets or A/B testing, but that part of the cycle has passed... venture capital isn’t easy for investors or founders, nor is it supposed to be. We must understand and adapt to the shifts of a new cycle”.

SECTION TWO: INVESTMENT PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 13

Source: Private Equity Wire survey, August 2022 companies, and less like tech companies, in terms of recurring revenue.” More broadly, investment rounds are being extended and have shifted in favour of fund managers with capital to deploy, instead of previously bullish start-up founders. But according to sources in the market it is still too early to predict the winners and losers.

SECTION TWO: INVESTMENT PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 14 Figure 2.2: After the boom - VC activity slows

Analyst note: Data as of August 11, 2022

Source: Preqin Pro is taking place. All agree that technology –whether this be Web3, deep-tech or blockchain – will continue to drive growth. A Private Equity Wire survey during July shows the majority of respondents (57%) believe technology still offers the most attractive investment opportunities across VC. This compares to only 7% for consumer/retail investments, and 13% for life sciences.

“AI has been a hot sector for a while and there has been a lot of excitement about the potential of Web 3.0 and cryptocurrency,” says Nic Brisbourne, CEO and managing partner at Forward Partners. “It may seem like there has been a lot of hype, but the reality is many of these technology businesses are building the future of digital applications and tech infrastructure – that underlines basically everything we do. For years, many sectors –law, or medical science, for instance – have

In fintech, debt collection or debt resolution and PropTech companies are considered counter-cyclical, says Choo at Portage, but it

According to McKinsey, the past three years have seen a boom in VC funding for biotech companies, raising more than $34bn globally in 2021 – over twice the total a year previous.

The first VC firms were not typically fans of investing in life sciences: the stakes were often high, and it was usually a win/lose bet on finding successful medical treatments. Now more commonly known as biotech investing, start-ups are turning to AI and machine learn ing to improve the odds of a drug breakthrough and a towering wall of private capital has built up behind them [see chart on p17].

Large pharmaceutical companies face a patent cliff over the next five years as revenues on many of their biggest drugs expire, says Antoine Papiernik, chairman and managing partner of Paris-based Sofinnova Partners, which announced a strategic partnership with private equity giant Apollo in May to “significantly accelerate [its] “Thegrowth”.pharma industry has indicated they will use the cash they have to buy the next set of successful [biotech companies] – this is a security net to the life sciences VC industry,” he says.

Sofinnova has a large scope within the sector, but one area of focus is cell engineering to produce cell ther apies. Other emerging biotech opportunities for VC include RNA and DNA processing, precision medicines to diagnose patients earlier and new delivery methods for Withtreatments.technology helping VCs to make smarter bets on the medical companies of the future, there may be more winners, but there will be some losers too.

VCs GATHER AT THE PATENT CLIFF

Counter-cyclical

In a recent note to investors, JP Morgan pointed out the recent record levels of VC investment into cryptocurrency and blockchainbased start-ups, despite the crypto crash earlier this year. VC firms here are sitting on record levels of dry powder: in Q2, VC giant Andreessen Horowitz said it had raised $4.5 billion for its fourth and largest crypto fund, giving it a total of more than $7.6 billion to invest in the Predictably,space.there is greater focus on startups less exposed to a cyclical downturn and a stronger line is being drawn between B2B and B2C start-ups in the crypto and blockchain world in particular.

“We are deliberately focusing on companies that we believe to be operating in fundamentally defensive or sectors that are more recession-proof and inflation protected,” says Natalie Hwang, founding managing partner of Apeira Capital Advisors, a VC investment and advisory firm.

SECTION TWO: INVESTMENT PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 15

The Covid-19 pandemic has placed a spotlight on new treatments and technologies.

been desperate for a way to reduce costs and increase pace. Now we have the start-ups and tech to deliver this, and we’ve seen that AI, in one shape or another, has been widely adopted by businesses across the world. Of course, market conditions have an impact and investors need to be more discerning than ever, but if a start-up is genuinely providing a solution to a big problem facing businesses, that is where the growth will be, and investors will follow.”

Large tech-based VCs including Andreessen Horow itz and Madrona Venture Group are crossing over and (even larger) private equity firms such as Apollo, EQT and Blackstone have recently taken stakes or acquired well-known life sciences VC funds. If the start-ups they back can disrupt drug discovery and unlock more tailored treatments for aging popu lations, exit opportunities await through big pharma.

section one: TECH STILL LEADS VC FUNDING APPETITE KEY FINDINGS said tech start-ups offered the most attractive funding opportunities of survey respondents said energy was the most attractive sector for VC13%tobelieve22%57%lifesciencesbemostattractive

“People are also spending a lot of time on cyber-insurance and anything at the intersection of climate and fintech,” she adds. Climate-tech and VC start-ups based on the energy transition are indeed showing signs of growth, despite a broader market slowdown. In Q1 this year, five climate-tech investments made it into CB Insight’s top 10 lists covering seed and venture capital rounds, growing to eight by Q2. Since 2017, the sector has tripled in size, according to PitchBook data, but the path to revenue can often be longer than for other tech start-ups. In the Private Equity Wire survey, 22% of respondents believed ‘energy’ to be the most attractive area for VC investment, second afterBut‘technology’.cluestopredict some of more vulnerable VC sectors may be found in the boom. According to analytics firm BryceTech, the amount of money invested in commercial space start-ups – known as space-tech –

SECTION TWO: INVESTMENT PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 17 Figure 2.3: VC funding into biotech peaked in early 2021

Analyst note: Capital raised by privately funded biotech companies at seed to series C

Source: McKinsey; PitchBook can be difficult to find public market valuation comparables here.

The advantage of investing at an earlier stage is that you are playing a longer-term game. On average, you will invest in a start-up for 7-10 years and across that period there will inevitably be a cycle of boom and bust. But you can afford to be patient, build strong businesses, and exit when the time is right. When you invest in later stage companies, your timeframe for an exit will be shorter and so you are less insu lated from broader market move ments.The dynamics of early-stage investment are different too. We invest small amounts of money into a wide portfolio. Start-up businesses grow faster, earlier – and the earlier you invest, the longer you have to compound these growth rates. This, combined with a diversified portfolio can bring better returns at lower risk. Behind the model, the key to success really comes down to the business fundamentals. The firms that are best placed to do well are those that are laser focused on identifying and in vesting in robust businesses that will be best positioned for growth when markets turn. We’re always thinking about what the next round is going to look like and what the next round of investors will want. At a high level, investors signing onto funding rounds at the moment are taking a more conserv ative stance. Investors still want to see growth, but they also want to see strong unit economics and other metrics. For many investors, particu larly at the later stage, growth at any cost used to excite. Now it just won’t stick. We’ve always prioritised busi ness fundamentals over break-neck speed growth. What we are asking founders in the due diligence process has not really changed – what is the market opportunity? Do you know your customers? How will you create value? How do you plan to capture market share? What is your cash flow, burn rate and runway? Those questions were just as important before as they are now.

The ‘hype’ sectors of 2021 will receive less attention this year but the underlying technology infrastructure that helped create them will continue to drive forward VC in the years to come

SECTION TWO: INVESTMENT PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 18 doubled last year to more than $15 billion. Elon Musk’s private space company, SpaceX, was valued at $125 billion in its latest funding round and at the time of writing was the highest valued start-up in the world, outside China.Can VC investment in an area such as space-tech continue to grow in a down market? According to Michael Mealling, at space-tech VC Starbridge, ‘good deals’ in the sector are still over-subscribed but risks exist on the upstream, through unstable supply chains, and on the downstream, by misreading your customer base. On a website which tracks the progress of space-tech start-ups, he notes a high watermark of 176 companies in the rocket launch market alone – “far more than the market can support”. “As you find any technology space, you have a lot of entrepreneurs looking for somebody to give them money so they can go away and play with the technology. And [despite the market slowdown] we still have that.”

KEY TAKEAWAY – GP s

NIC BRISBOURNE, CEO AND MANAGING PARTNER, FORWARD PARTNERS

Globally, Europe saw the smallest regional drop in start-up funding in Q2, down 13%, compared to a 25% fall in the US and Asia. Even if it lags the US decline, the long-term outlook for the region remains positive.

Billion-dollar start-ups are spreading across Europe at a rapid rate. US VC firms have taken notice. But do hubs in London and Paris really have an advantage over Silicon Valley? Once considered a frontier market by VCs in Silicon Valley, Europe has developed a network which currently leads the industry by several measures. Of the total number of unicorns created there – start-ups valued at $1 billion or above – more than half were created last year alone.Though they still only represent a slice of last year’s global total (14%, according to Crunchbase), the high number of births seems unlikely to fade, even as start-up funding is squeezed elsewhere.

SECTION THREE: EUROPE PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 19

EUROPE’S VC ECOSYSTEM BLOOMS

“Historically, there has been a valuation arbitrage opportunity in Europe [for global VC funds] – companies have probably been on average more attractively priced,” says Dan Aylott at Cambridge Associates, “but the outstanding performance here up until

Remaining compliant is a high priority for both the start-up and the VC investor, as failure to meet local compliance requirements could prevent them getting their next round of investment or achieving the correct market valuation. An established and experienced Employer of Record will help ensure they remain compliant in every country in which they operate.

PRIVATE EQUITY & VENTURE CAPITAL AT GLOBALIZATION PARTNERS

VC-backed start-ups expanding beyond their home market typically need to spend both time and money carrying out due diligence on new markets they plan to enter. This is especially true for smaller, less experi enced portfolio companies that lack the processes, procedures and knowhow needed to scale internationally. But due diligence is just the begin ning, as these start-ups move on to building a legal and HR infrastructure. During a process which can take at least six months and cost tens of thousands of pounds, most start-ups will also make their first hire in the new territory. If a hiring decision does not work out, there can be huge costs associated with exiting that country and as a result of local labour laws, a start-up could also be left with human capital in the market. Delivering the agility start-ups need to identify and fast-track the onboarding of strategic hires, a global employ ment platform can often accelerate how they navigate international mar kets to scale up. As they expand, VC-backed start-ups also need to address compliance. Ensuring that they remain compliant with local employment and privacy laws when hiring talent in multiple jurisdictions can be complicated. As an example, the US and France both have complex and challenging labour laws and failure to adhere to these laws could cause serious problems and incur unplanned costs.

SECTION THREE: EUROPE PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 20

SAM PERRY, DIRECTOR OF STRATEGIC ALLIANCES –

I don’t see the European opportunity going away anytime soon. In fact, I see it continuing to evolve and expand

SECTION THREE: EUROPE PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 21

last year has fueled further interest. I don’t see the European opportunity going away anytime soon. In fact, I see it continuing to evolve and expand.” US-based VC firms including Bessemer Venture Partners, Lightspeed Venture Partners and General Catalyst have all recently hired or added to their teams in London and Europe to better access the region. Last year, Sequoia Capital opened its first permanent London office, more than 10 years after first investing in Europe, through Swedish fintech Klarna.

Despite potential language barriers across the continent, start-ups in the region are learning to leapfrog between emerging VC hubs to access talent, investors and broaden their customer base.

Source: Private Equity Wire survey, August 2022

“Originally there was a bit of a scouting mentality with US VC firms seeking investment opportunities here,” says a Parisbased VC source, “but that has gone out of vogue... it’s probably proved less efficient and there were a lot of raw deals.”

In a sign of closer ties between the US and Europe’s VC markets, the EU will open a new outpost in Silicon Valley this month.

To reach its goal of 500 employees, Estonian online-identification start-up Veriff opened an office in Barcelona last year, saying it has “some of the best product and

Figure 3.1: Industry was asked ‘In Europe, which one region do you expect to see the most interesting investment opportunities over the next 12 months?’

In a survey by Private Equity Wire, respondents were asked which region in Europe will see the most interesting investment opportunities over the next 12 months. The UK was the most selected, with 25%, followed by Germany (20%).

A handful of cities in northern Europe dominate investment: London, Berlin, Stockholm, Munich, and Paris are home to start-ups which represented more than half Europe’s total VC funding last year.

Without one major hub, I think one of the biggest challenges is figuring out the coverage model for Europe

SECTION THREE: EUROPE PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 22 engineering talent in the world”. With a presence already in New York and London, such geographic diversification can offer resilience in a down market, say sources.“Ifyou build a company in Milan, in Copenhagen, in Dusseldorf, in Madrid... as long as the technology is world class, as long as you build it in a global way, it should be like any of the companies from Silicon Valley or Boston,” says Antoine Papiernik at Sofinnova Partners. “Europe’s problem in the past has been translating science and innovation into companies and ultimately the winners of tomorrow, so it has been the little brother of Silicon Valley for a long time.” A strong university network is fostering much of this innovation, with Paris-based business school Insead and HEC Paris in France, Cambridge University and London’s LSE in the UK, and Stockholm’s main university and institute of technology in Sweden responsible for a large proportion of Europe’s recent unicorn founders.

A source at an investment bank which serves the VC market claims much of the new activity is coming from “the beer drinking countries, rather than the wine-drinking countries [of Europe]”. Even if there’s some truth to this, it may not be the case for long.

Flywheel spins “The locations where big tech companies are built tend to generate an enormous amount of activity and creativity,” says Ed Knight at Antler, “they become a magnet for talent, and you get a flywheel spinning. Cloud computing now means that businesses can be built from anywhere, meaning that entrepreneurship is no longer limited to just Silicon Valley.”

According to Alex Ferrara, who leads VC giant Bessemer’s European efforts from London, the shift to remote working means European start-up founders no longer need to move to the Bay Area early on, and this is drawing VC investors more into the region. Knight’s Antler started investing in the UK in 2019 and closed a new seed fund last year to help develop 70 UK tech startups in the country. It’s easy to see why: London attracted more than double the amount of VC funding in 2022 than Paris and Berlin and ranks third only behind New York and Silicon Valley. Funding rounds this year

SECTION THREE: EUROPE PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 23 Figure 3.2: Global unicorn births by region, Q2 2022 Source: CB Insights, State of Venture Q2 2022

Europe is generating increasing interest from VC firms but many will need support to co-ordinate their business across the various hubs of London, Berlin and Paris

A lot of the local and regional European consumer internet companies and online retail are facing headwinds as they’ve started to realize that there are minimal advantages of scale and brand across Aregions.brand like Uber is powerful because consumers know that wherever they travel around the world there is a good chance they can use the Uber app to book a car. This creates some nice global network effects. However, that doesn’t really exist for categories like grocery or food delivery. A consumer in the UK is never going to need to use a grocery delivery or food delivery service in France or Germany, and so there really isn’t much benefit to operating in multiple countries. I think a lot of these companies have realized this, have begun to retrench, and are now contending with the reality that the market size for their service is smaller than they originally anticipated.

SECTION THREE: EUROPE PRIVATE EQUITY WIRE INSIGHT REPORT SEPTEMBER 2022 | 24 have included digital payments business GoCardless and software payments provider Paddle. In July, London’s Deputy Mayor for Business crowned the city the “fintech capital of the world” claiming it was home to more fintech companies than any other city globally. But in the same breath he also warned of a problem facing all of Europe’s VC hubs as they expand: the race for talent between them, and with VC hubs in the US, will only intensify. “I think one of the biggest challenges is figuring out the coverage model for Europe,” says Ferrara. “Unlike the Bay Area or Israel, Europe doesn’t have any one major hub. You can find great founders and companies in many different cities across Europe. Figuring out how to best cover so many regions is one of the bigger challenges.”

I think cybersecurity will remain an attractive area given how much of the global economy has shifted from physical manufacturing to digital software and services over the past two decades and the need to protect this relatively new attack surface. If you look at the public market comps, the cyber sector has been more insulated from the meltdown than other areas. We expect spending for cybersecurity software, especially cloud security, will remain Capitalstrong. was basically free for the past few years but that’s no longer the case and so there’s now more of an emphasis on scaling with efficiency. I think that’s one reason why we’re seeing so much talk of product-led growth and bottomup customer acquisition models. I think this is one area where Europe has an advantage. We’ve generally found European SaaS companies to be more efficient than those in the US, which puts them at an advantage when it comes to fundraising.

ALEX FERRARA, PARTNER, BESSEMER VENTURE PARTNERS

KEY TAKEAWAY – SERVICE PROVIDERS

section one: THREE COUNTRIES DOMINATE EUROPEAN VC KEY FINDINGS of survey respondents believe UK will have the most interesting funding opportunities over the next 12 25%months With Berlin a major VC hub, Germany is a close second 20% Despite Paris ’ network, only 5% see France as most5%promising

M&A BECKONS AS FROTHY

SECTION FOUR: VALUATIONS

DataVALUATIONSFINTECHCUTisyettocapturethefullextentofthe‘valuation reset’ across late-stage VC, while lower valued early-stage start-ups could face consolidation Late-stage VC has been hit hardest by the reset in valuations, with the number of high-profile examples snowballing through 2022. At one point last year, payments startup Stripe was the most highly valued VC investment in the US. Last month its valuation was slashed by 64% by one investor. Weeks earlier, valuations were cut at Swedish buy-nopay-later fintech Klarna, following delivery app Instacart before it.

“The startups that enjoyed sky high valuations based on hype and ‘FOMO’ are the ones that will feel the brunt of the downturn,” says Nic Brisbourne, CEO and managing

SECTION FOUR: VALUATIONS PRIVATE EQUITY INSIGHT REPORT SEPTEMBER 2022 | 27 partner at London-based VC firm Forward Partners.“While there has been a recalibration of valuations, this also reflects the fact that many of the impacted companies were overvalued. Now the market has a chance to normalise, and investors can sift out the hype and froth. This has been painful for many companies, but it’s prompted an important exercise; startups and their investors are working out whether they can justify valuations and are evaluating the robustness of business fundamentals.”

With an IPO in their sights during 2021, many late-stage start-ups now face more pressure to justify high valuations as public market equivalents have crashed. UK-based digital bank Zopa had planned to go public this year, but in July, the CEO told one reporter: “The markets have to be there [and they are] not there — not for fin, not for tech”.First-half data from 2022 is yet to show the full extent of the damage to late-stage start-up valuations. During H1, US median late-stage deal value fell only 7.1% compared to 2021, according to PitchBook’s latest valuations report. In Europe, late-stage valuations and round sizes paced above 2021 figures.

More falls are expected in H2, given the widespread uplift in valuations over the past few years. In a Private Equity Wire survey in July, over half of all respondents (53%) expected to see a markdown in the valuation of their VC investments in 2022, compared to 2021. Eighty percent of investors still view venture capital as overvalued, according to a Preqin survey of 300 LPs in June. Disciplined returns According to Natalie Hwang at Apeira, the significant influx of capital into private markets has led to aggressive growth and equity multiples for many start-ups, which can create a wide range of assumptions in pricing and valuation risk. “We’ve been cautious to the risks of investing in companies on prices that we believe are over driven by momentum versus underlying fundamentals,” she says, “because they can price at a number that far exceeds their actual realisable liquidity values, and subsequently fail to yield desired returns and investors can be seeking. But as the pool of potential buyers diminishes, caused in part by the rotation of non-traditional investors outside of the asset class, we are seeing more disciplined valuation practices begin to take place across the sector.”

According to data from CB Insights, the average increase in valuation between all financing rounds has been trending down since the end of last year. But look more closely... The valuation uplift in the growth stage of the market was around nine times over the past five years, says Ed Knight at Antler, compared Figure 4.1: Industry was asked ‘Do you expect to see a markdown in the valuation of your VC investments in 2022, compared to 2021?’

Source: Private Equity Wire survey, August 2022

The startups that enjoyed sky high valuations based on hype and ‘FOMO’ are the ones that will feel the brunt of the downturn

section one: Private equity Insight report august 2022 | 28

Nic Brisbourne, CEO, Forward Partners

Early-stage impact According to Stephanie Choo at Portage, early-stage valuations have shifted from “easily in the $20m-$30 million range, up to $50 million last year”. In the current market, they are dropping to low teens and high single digits, she says.

The opportunity here may be for VC fund managers to bolt-on undervalued start-ups to their existing investments. Some start-up founders have said publicly that a wave of consolidation now seems likely among latestage fintech start-ups, if the IPO window remains closed. “I expect acquisition opportunities to continue to increase through the next two years as companies want to exit and can’t exit through the public markets,” says Choo. Seed stage valuations are holding up and have not fallen from the previous quarter since the onset of the pandemic. This was attributed by PitchBook to the high participation of nonFigure 4.2: Unicorn birth rate is falling

SECTION FOUR: VALUATIONS PRIVATE EQUITY INSIGHT REPORT SEPTEMBER 2022 | 29 to around two times in the early stage. Will the full ‘reset’ be proportional to the uplift, as it trickles down to early-stage VC too. The Q2 median pre-money valuation for early-stage VC in the US fell 16.1% quarter-on-quarter, according to PitchBook data. In Europe, earlystage valuations paced above 2021 figures in H1 2022.

Source: CB Insights, State of Venture Q2 2022

PitchBook’s preliminary benchmark quarterly IRR for VC in Q1 was negative – this is only the second time it has moved into negative territory in seven years, excluding the onset of the pandemic in 2020. But while VC funds above $250 million in size follow the broader market, funds below $250 million have outperformed and remain at historically elevated levels, by rolling one-year horizon IRRs [see chart above].

Source: PitchBook Analyst note: Data as of December 31, 2021 traditional investors and micro-funds still active there.Lower start-up valuations and funding rounds ultimately impact VC fund performance and investments made by VC funds at booming valuations will have to perform even better to deliver target returns to investors. The median VC fund that was raised in 1996, as the internet boom was just gathering steam, returned over 40% a year over its life. After the dot com crash, US VC 1999 vintage year funds still report an overall negative internal rate of return in most data sets.

Over the last five years, VC has shown a 29.5% internal rate of return, nearly double the annualised rate over the trailing 15 years. This seems unlikely to continue.

SECTION FOUR: VALUATIONS PRIVATE EQUITY INSIGHT REPORT SEPTEMBER 2022 | 30 Figure 4.3: Rolling one-year horizon IRR for VC funds by fund size

“We believe we will continue to see a decline

of all respondents expected to see a markdown in the valuation of their VC investments in 2022, compared to 2021

Over (53%)

section one: VALUATIONS ARE SLIDING AT LATE-STAGE START-UPS BUT SEED STAGE IS HOLDING UP KEY FINDINGS

half

SECTION FOUR: VALUATIONS PRIVATE EQUITY INSIGHT REPORT SEPTEMBER 2022 | 32 in VC fund valuations over the coming quarters as the reality of a slower growth environment sets in and public market valuations settle,” says Dan Aylott at Cambridge Associates. “However, venture capital is a long-term asset class and experienced GPs will be focused on helping their companies and entrepreneurs through these challenging times, so that they can take advantage of the upswing when it comes. We have confidence in the long-term outlook for venture capital globally, but there will be some bumps in the road in the near and medium term for sure.”

KEY TAKEAWAY – LP s Falling valuations at VC-backed start-ups may still take months to feed through to reported VC fund NAVs but funds which invested in the run-up to 2021’s peak will be most exposed Figure 4.4: Venture capital financing deal rounds from 2015 to 2022 Analyst note: Data as of June 13, 2022 Source: PitchBook

HeadColinCONTRIBUTORS:LeopoldofResearch & ReporterFionacolin.leopold@globalfundmedia.comInsightMcNally fiona.mcnally@globalfundmedia.com Scott Newman Art jack.hassall@globalfundmedia.comSeniorJackENQUIRIES:FORscott.newman@globalfundmedia.comDirectorSPONSORSHIP&COMMERCIALHassallCommercialDirectorPublishedby:GlobalFundMedia,LionCourt,25 Procter St, London WC1V 6NY ©Copyright 2022 Global Fund Media Ltd. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the Investmentpublisher. Warning: The information provided in this publication should not form the sole basis of any investment decision. No investment decision should be made in relation to any of the information provided other than on the advice of a professional financial advisor. Past performance is no guarantee of future results. The value and income derived from investments can go down as well as up. SUPPORTED BY: PRIV A TE EQUITY WIRE