Quantitative Easing and Central Bank Capital Policies

DECEMBER 4, 2024

Keynote Speech at GIC-Bloomberg conference

Tobias Adrian

IMF Financial Counsellor and Director of MCM

Department

This presentation reflects my own views, and not necessarily those of IMF staff, IMF Management, or the Executive Board

Major benefits of strong monetary frameworks

• Rise in inflation to multi-decade highs was major stress test for monetary policy

• Strong policy frameworks – often involving some form of flexible inflation targeting – have performed well

Core Inflation (Percent, year-on-year)

• Kept long-run inflation expectations wellanchored (sharp contrast to 1970s)

• Central bank independence crucial in supporting disinflation efforts

• Resilient financial systems also helped

The Necessity of Independence

“Independence is critical to winning the fight against inflation and achieving stable long-term economic growth”

(IMF Blog, Kristalina Georgieva, March 21, 2024)

Central bank responses during and after COVID have “helped to keep inflation expectations anchored in most countries even as price increases reached multidecade highs (…). [This] success thus far has largely been because of the independence and credibility that many central banks have built up in recent decades.”

Independence pays off: higher central bank independence is associated with lower inflation

But still, some need for rethinking in light of inflation surge…

• Inflation surge – especially its persistence – was a major surprise

• CB models and forecasts significantly underpredicted inflation

• Challenged pre-crisis view that there was little upside inflation risk and its near exclusive focus on the ELB and downside inflation risks

New trade resctrictions (Number)

• Some refinements seem needed, including in models, strategies, and use of tools including quantitative easing (QE)

• Will better prepare for more shock-prone environment (trade, climate, geopolitical)

Source: Global Trade Alert

Note: Data includes adjustment for reporting lags.

My focus here on rethinking QE

• Quantitative easing has been a crucial part of the CB toolkit to provide stimulus in the event of limited policy space

• But its use during COVID has been criticized on the grounds that it may have contributed to overheating (Orphanides, 2023) and led to large CB balance sheet losses

• In this presentation, I will reconsider the conditions when QE likely to be warranted as well as how it should be implemented

• When should QE be used?

• How should the FG accompanying QE be modified (e.g., more escape clauses)?

• Given that a weak balance sheet may pose risks to CB independence, I’ll also consider how CB profit distribution policies might be modified

When is QE likely to be warranted?

Framework for assessing QE

• Appropriate focus from social welfare perspective is to assess the macro benefits of QE against the consolidated fiscal costs

• “Consolidated” includes CB losses but also incorporates how QE benefits government fiscal position by raising tax revenue and lowering interest payments

• But we also look at CB losses, as these can have implications for CB independence

• Use quantitative model with the following key features:

• Bond market segmentation => QE affects term premiums and real activity

• Behavioral discounting => FG cannot provide sufficient stimulus, so QE can help

• Proportional taxes => Fiscal revenue endogenously responds to stimulus

• Nonlinearity in Phillips Curve => Inflation can rise steeply if output near potential

Framework for assessing QE (con’t)

• Explore QE under different conditions: “deep” versus “shallow” liquidity trap

• Deep trap: severe recession with high unemployment and inflation well below target, so CB would like to set policy rate deeply negative if the ELB didn’t bind

• Shallow trap: unemployment only modestly above U* and CB mainly faces a problem of low inflation (so shadow rate not deeply negative)

• Note our focus is on QE for macro stimulus when ELB binds (as in QE2/QE3, not QE1)

• There is broad-based support for using asset purchases and broad-based liquidity during periods of extreme stress (with a quick wind down after conditions ease).

• QE for macro stimulus differs insofar as it may be initiated even when financial conditions are calm; and it may imply a large balance sheet for many years.

Modeling framework

Builds on the two-country NK model of Kolasa and Wesolowski (2020).

Incorporates bond market segmentation to allow QE to affect term premiums on long-term bonds (Andres et al., 2004; Chen et al., 2012):

“Financially Restricted” households: trade only in long-term bonds

“Financially Unrestricted” households : trade in long-term bonds subject to portfolio adjustment costs, and also trade in short-term bonds

Arbitrage on the bond market by “Unrestricted” agents: � �������� �������� ,���� +1 = �������� + ���� (�������� ,���� ���� , … )

Transmission of QE:

• QE reduces supply of long-term bonds => Expected rate of return on long-term bonds ↓

• Lower long-term interest rates (from lower term premium) boost aggregate demand

Model: International Linkages

Bond market segmentation also generates a wedge in the UIP condition with QE causing the exchange rate to depreciate

The upshot is that QE stimulates aggregate demand by lowering interest rates and by causing the exchange rate to depreciate (hence QE also boosts inflation)

Note that movements in the UIP wedge can also be driven by non-fundamental forces, e.g., reflecting swings in risk appetite of international investors

Means there is potential role for FX intervention as in the QIPF model of Adrian, Erceg, Kolasa, Linde, and Zabczyk (2021)

Calibration of Model

Fiscal block:

Fiscal rule assumes that labor income tax rate adjusts gradually to stabilize debt/GDP

Central bank profits/losses are assumed to be immediately transferred to the Treasury

Monetary policy: Policy rate follow Taylor-style rule subject to the effective lower bound constraint

Price and wage stickiness calibrated so that the effects of a monetary policy shock are broadly consistent with VAR evidence for EA and US.

Bond market segmentation calibrated so that effects of QE on term premiums are slightly below median estimates in Fabo et al. 2021 (to provide conservative estimates of the benefits of QE)

More details on model in forthcoming WP (Adrian, Erceg, Kolasa, Linde, and Zabczyk, 2024).

QE highly effective in deep liquidity trap

Baseline: Deep recession and liquidity trap (due to discount factor shock)

With QE: QE (here 10 percent of GDP) has clear macro benefits boosting output and inflation

QE also has favorable fiscal effects: reduces govt debt (partly from higher CB profits)

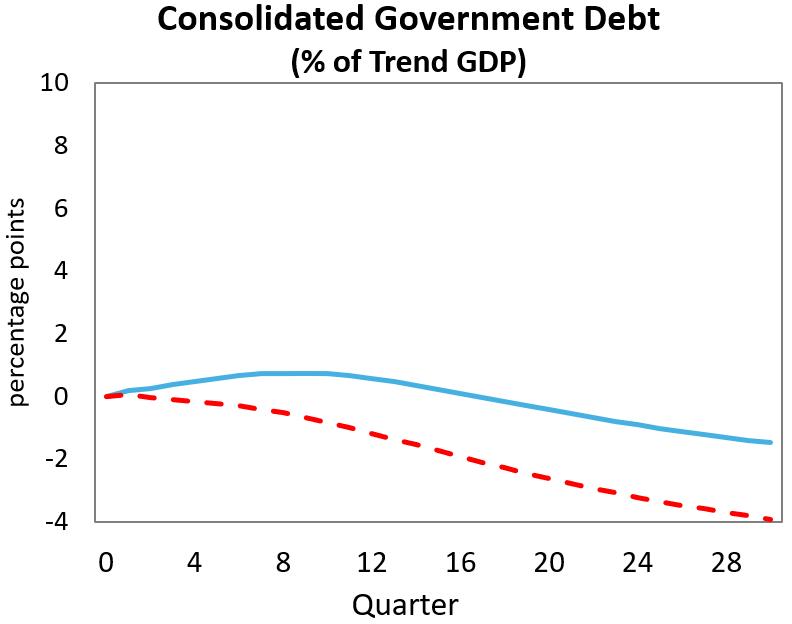

QE versus govt spending in liquidity trap

Here we compare the effects of QE versus expanding govt spending in a liquidity trap on govt debt (both scaled to have the same effects on output)

QE reduces government debt while the spending expansion raises it (dotted aqua lines)

Underscores that QE is an attractive tool to provide stimulus in an environment of high debt

QE can still be beneficial in shallow trap

Baseline: Here output (and inflation) are only modestly below baseline w/o QE (“shallow” liquidity trap)

With QE: QE still beneficial in boosting output (and inflation) and reducing public debt, including through CB profits

But smaller quantitative effects than in deep trap as QE causes future path of policy rate to shift up more

But need to be wary of commitment-based FG

Forward guidance (FG) can make QE more effective in persistently reducing long-term interest rates:

If policy rates are expected to remain low even in face of QE, then more of the decline in the term premium passes through to long-term bond yields

Hence central banks have often complemented QE with forward guidance about policy rates that has some degree of commitment (“Odyssean” forward guidance in the language of Evans et al, 2012)

But such commitment-based guidance can be a bit of a straitjacket and may delay a timely liftoff of policy rates, potentially causing overheating (Orphanides, 2023)

As illustrated next, this risk of overheating is more likely in a shallow liquidity trap, perhaps because recovery turns out to be faster than expected when QE was initiated

Considering high inflation and risk of NL Phillips Curve, CBs should be more careful about such commitments and temper FG with escape clauses

More risk QE can be counterproductive in shallow trap

Here QE is launched in shallow recession, but upside risks to output/inflation materialize in period 5.

QE causes some overheating, in part because the CB makes good on its commitment to keep policy rates low for some time after asset purchases end

QE still improves the consolidated fiscal position, but the CB experiences sizeable losses

Factors affecting CB profits

Average effect (per 10% QE)

QE more likely to lead to CB losses (and less improvement in fiscal position) if the term premium is already low before QE is initiated.

Here we compare the baseline in which the “steady state” term premium is 100 basis points with an alternative in which it is 25 basis points. CB profits are negative in the latter case and the consolidated fiscal improvement smaller.

There are also diminishing returns to QE, so that bigger purchases run more risk of causing profits to fall (the brown dash-dotted line).

Summary on QE

• Strong rationale for using QE in deep trap where risk of rapid liftoff is typically quite small.

• Boosts output and inflation when “needed most”

• Improves the consolidated fiscal position significantly

• But more reason for caution in using QE in a shallow trap, though still may be worth considering

• Smaller macro benefits for given-sized QE program

• More risk that it can lead to overheating if upside surprises materialize after QE is deployed

• Important to be wary of commitment-based guidance and use “escape clauses”

• Simulations illustrate that the consolidated fiscal position (which should matter from a societal welfare perspective) often improves even though the CB may make significant losses. But the losses may still matter for CB independence, as we will next consider…

Should CB profit distribution policies be modified?

Re-design

CB capital policies?

• Should CBs change how they allocate profits to account for their bigger and riskier balance sheets?

• Current policies designed long before GFC when CB balance sheets small and cash-in-circulation the main CB liability (will discuss more below)

• “Lean” CBs were almost always profitable and distributed most profits to the govt

• But QE has exposed CBs to large duration risk and big losses

Cash in circulation as percentage of total monetary liabilities

Why should CB capital or profit distributions matter?

• If a CB has full operational independence, it’s monetary policy strategy and implementation should not depend on its capital or profit distributions to the government

• Some CBs have operated effectively with negative capital (e.g., Chile)

• But in practice, a weak CB financial position and/or its distributions to the government may undermine its operational independence (Stella, 2008)

• May expose central bank to more political pressure (even in budgetary/resource management decisions)

• CBs may feel they have less scope to deploy QE even if well-justified on economic grounds

Importance of CB financial independence

• Hence CB officials typically put a high weight on maintaining CB “financial autonomy”

• Survey of 87 senior CB officials by Adrian et al (2024) ranked CB financial independence as the most important attribute for ensuring operational independence

• So given the balance sheet risks of QE, important to reconsider CB capital policies

First step back to consider existing capital policies…

• Wide range of approaches in distributing CB profits to government

• Distributions may depend on profits relative to statutory minimum: if below, build CB capital; if above, goes to govt.

• Sometimes fixed percentage to govt

• Or outcome of negotiation with govt

• Broad aim – if shortfalls -- is to rebuild capital either organically through profit retention or possibly govt recaps

• Appeal of simplicity, but not risk-based or forward-looking

Distribution of CB profits to government (average over 2019-2022)

An alternative “risk-based” approach

• QE tends to generate large initial CB profits followed by sharp decline, and possibly big cumulative losses

• Intuitively, it seems natural to try to “smooth through” some of this volatility and not simply distribute large upfront profits to the government

• More formally, central banks could modify strategies to take a more riskbased approach (as some are now doing):

• A dynamic capital policy would involve quantifying key sources of risk and making profit allocation decisions to build capital to provision against shocks

• Need model(s): IMF staff have developed “stress-testing” framework that builds on Hall and Reis (2015)

• Can help assess balance sheet risks due to policy actions (QE) as well as from running a floor system

Central Bank Balance Sheets Stress Testing Model

Balance Sheet Stress Testing – Benefits for Central Banks

Forward-looking analysis for extreme but plausible losses. Calculation of adequate capital and riskbased mechanism for its maintenance. Assessment of profit distribution plans. Assessment of likelihood of meeting adequate capital target over the medium term. Determination of recapitalization needs (if minimum capital threshold is breached).

A risk-based central bank capital approach ensures sufficient capital, protecting central bank financial independence, policy solvency, and policy credibility.

CBs may take different approaches

• Considerable appeal of risk-based approach in helping CB maintain a strong financial position and smooth profit volatility, but are challenges:

• Complex process: should CBs look at modal outlook or tail risks in deciding how to allocate profits?

• Government may be averse to CBs building up a large “war-chest”

• Approach CBs take should depend on the risks they perceive of a weak capital position

• Some CBs may view themselves as likely to have high operational independence irrespective of their capital position and want to retain current strategy; but enhanced communication still useful

• Other CBs may regard financial weakness as posing more risk to their ability to conduct policy and use tools such as QE, and may see more appeal in risk-based approach

• Some CBs have already moved toward a more risk-based approach .

• Given that CB balance sheets are very large and highly leveraged, urgent to move forward to better quantify risks and explore merits of more risk-based approaches.

Conclusions

Conclusions

• Strong monetary policy frameworks have helped CBs perform well when faced with a massive inflation shock

• But some refinements helpful in light of what we’ve learned, including to models, strategies, and the use of CB tools

• I’ve focused on QE for macro stimulus, and argued that it can still be a very useful tool given the ELB may well again become binding

• But a higher bar to using QE seems appropriate (with most obvious case in deep liquidity trap). Also need to include escape clauses

• Given CBs are likely to continue using QE, there may be a good case for considering changes to profit distribution policies to protect the capital position of the CB and ultimately better ensure CB independence

Appendix

QE

in shallow liquidity trap: stochastic sims

Stochastic simulations: Here we consider the effects of QE In a shallow liquidity trap, but where shocks occur after QE is initiated

Shocks are calibrated to match macroeconomic volatility over the period 1960-2024

Upside inflation risk makes earlier and sharp liftoff likely

Can see large downside risk for CB profits, though QE still tends to improve overall fiscal position

IMF Tools for Central Banks

• Central Bank Transparency (CBT) Review

• Central Bank Balance Sheet Stress Testing

• Financial Sector Assessment Programs (FSAP)

• Safeguards Assessment (SA)

• Capacity Development (CD)

• Central Bank Board Workshops

• Analytical Work & Research