3 minute read

4.4. Case studies

Table 10: Effects of sustainability approaches and control variables

Variable

Advertisement

Best-in-class (n=16) Engagement (n=23) ESG integration (n=19) ESG Impact [A+; D-] resp. [1; 0] Carbon intensity (tCO2eq / mUSD revenue) Critical economic activities (% revenue)

Major environmental controversies (% involvement)

no sig. influence no sig. influence no sig. influence no sig. influence

no sig. influence no sig. influence no sig. influence no sig. influence

no sig. influence no sig. influence no sig. influenceno sig. influence

Exclusion (n=42) no sig. influence no sig. influence no sig. influence no sig. influence Impact investment no sig. influence no sig. influence no sig. influence no sig. influence

(n=5)

Positive selection no sig. influence no sig. influence no sig. influence -0.9% (n=27) p-value=0.020 * Thematic products +0.04 no sig. influence no sig. influence no sig. influence (n=11) p-value=0.002 **

Regional investment focus

Global: -0.02 p-value<0.001 *** USA/N-America: -0.06 p-value<0.001 *** no sig. influence no sig. influence USA/N-America: +1.1% p-value=0.017 *

Benchmark type no sig. influence no sig. influence no sig. influence no sig. influence

Concentration conc. +0.01 → +0.005 p-value=0.025 * conc. +0.01 → -58 p-value=0.027 * conc. +0.01 → -1% p-value=0.003 ** no sig. influence

Tracking error no sig. influence no sig. influence no sig. influence no sig. influence

Coverage cov. +0.01 → +0.001 p-value=0.026 * no sig. influence no sig. influence no sig. influence

This table summarises the results from the four regression models. We report estimates and p-values of significant variables. * significant at 0.05-level, ** significant at 0.01-level, *** significant at 0.001-level

Source: Inrate ESG Impact data and Climate Impact data as of October 2020.

4.4.1. Case study 1: ESG fund

The fund we examine in this case study is an example of a fund that included “ESG” in its name but failed quite clearly to deliver on this premise. The fund was passively managed, i.e. aimed to replicate the performance of its sustainability benchmark, which had a regional focus on the USA.

The sustainability approaches used in the company selection for the benchmark were exclusion criteria and best-in-class. In this case, we knew that the exclusion was focused on

controversial weapons, controversies (not further specified) and compliance (including ethical standards).

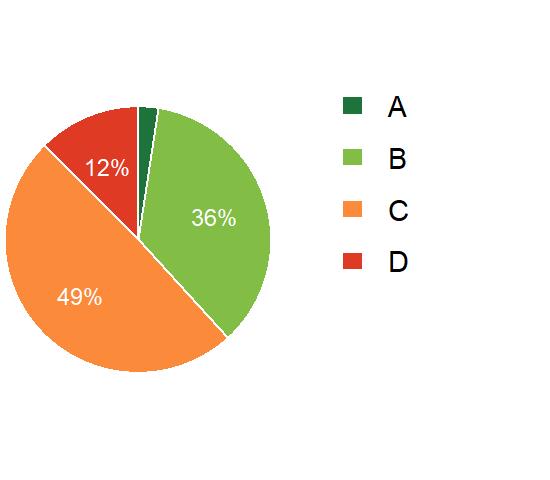

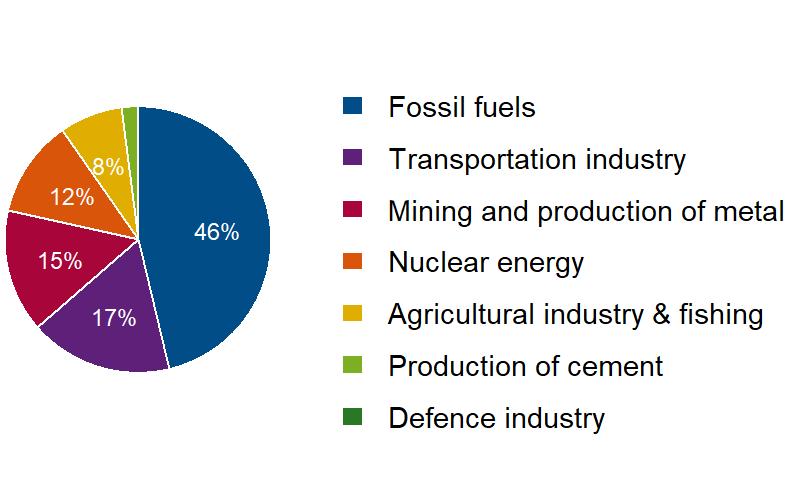

Quite strikingly, 12% of this fund’s volume was invested in companies that had an ESG Impact in the D range (D+, D or D, Figure 15). In total, over 60% had an ESG Impact in the C or D ranges resulting in an overall ESG Impact score of 0.39. Over a third of the fund’s capital (35%) was invested in critical activities (Figure 15), which was more than double the average share amongst the conventional funds. Most of the critical activities that the sustainability fund was invested in were fossil fuels (16%, half of which were derived from coal and oil), climate-intensive transportation (6%) as well as mining and production of metal (5%).

It turns out that the mere application of exclusion and best-in-class approaches does not necessarily lead to a positive portfolio impact. This does not mean that these approaches should not be used. The missing portfolio impact could be due to missing strictness of the approaches or the lack of consistency in their application.

Figure 15: Categorisation of the fund holdings

Left: This pie chart shows the shares of weighted ESG Impact scores of invested companies in the ranges A (A+, A, A-), B (B+, B, B-), C (C+, C, C-) and D (D+, D, D-). Right: The fund had a weighted percentage revenue derived from critical activities of 35%. This pie chart displays how these 35% were split into the seven categories of critical activities.

Source: Inrate ESG Impact data as of October 2020, Bloomberg data as of 31.12.2019.

4.4.2. Case study 2: Thematic fund

In the second case study, we take a look at a thematic sustainability fund. The fund was actively managed and had a global investment focus. ESG integration, positive selection, engagement as well as impact investment were the sustainability approaches applied. There was a clear and explicit intent stated that investing into this fund should help improve the climate impact of the portfolio. However, according to the fund factsheet, these sustainability approaches were not applied to the entire fund.